South America HCM Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

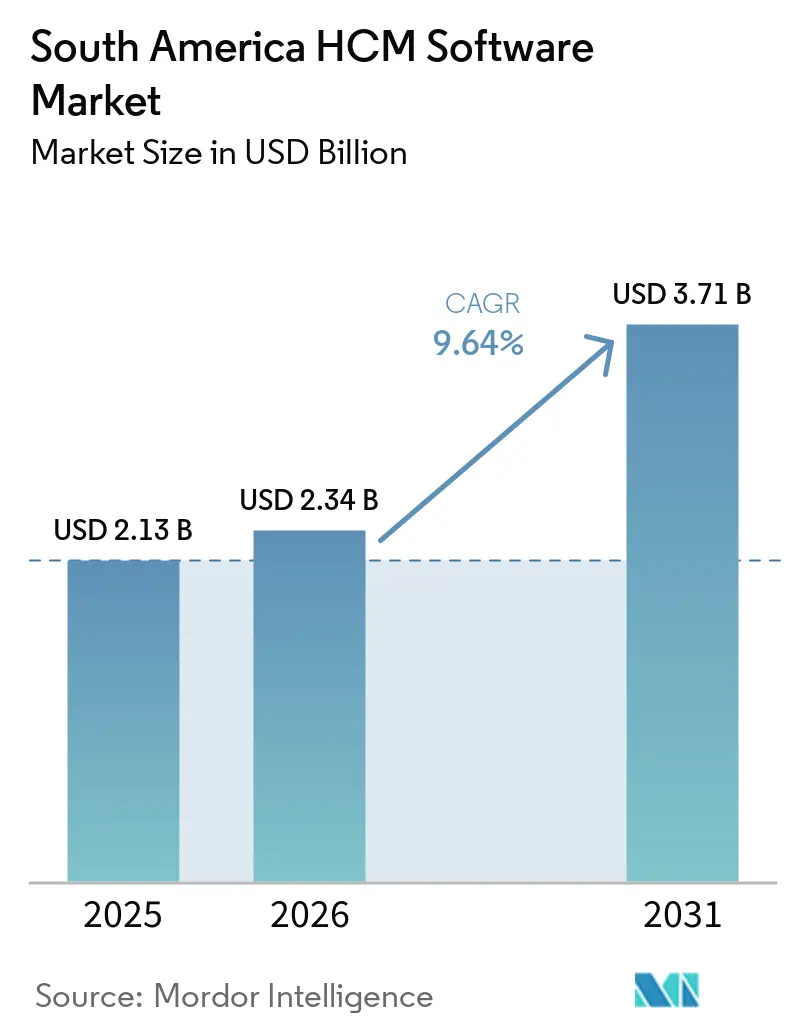

| Base Year Market Size (2025) | USD 2.13 Billion |

| Market Size (2026) | USD 2.34 Billion |

| Market Size (2031) | USD 3.71 Billion |

| Growth Rate (2026 - 2031) | 9.64% CAGR |

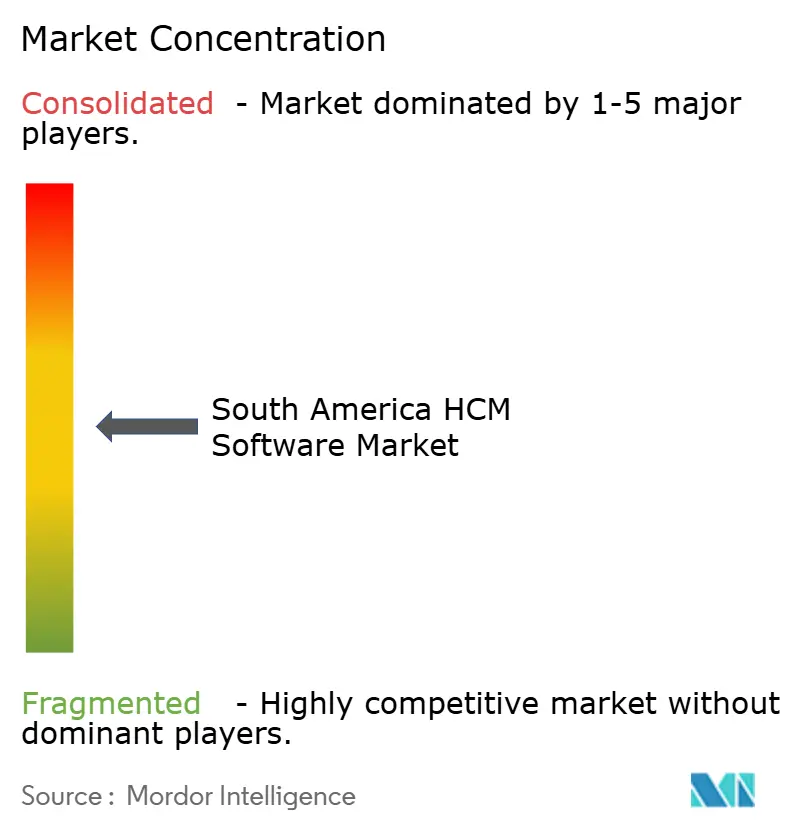

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America HCM Software Market Analysis by Mordor Intelligence

The South America HCM software market size was valued at USD 2.13 billion in 2025 and estimated to grow from USD 2.34 billion in 2026 to reach USD 3.71 billion by 2031, at a CAGR of 9.64% during the forecast period (2026-2031). The expansion reflects mandatory digitization of labor laws, a permanently hybrid workforce, and the gig economy’s entry into sectors that once relied solely on full-time employment. National compliance deadlines, such as Brazil’s Digital Labor Domicile requirement and Chile’s Electronic Labor Registry filing window, have elevated payroll accuracy and submission speed from back-office tasks to board-level priorities. Vendors are monetizing implementation complexity as enterprises discover that integration and change-management costs eclipse pure licensing fees. Cloud deployment is advancing faster than the South America HCM software market overall because real-time regulatory updates cannot be sustained on legacy on-premise architectures. Competitive intensity is sharpening as regional specialists differentiate through deep payroll localization while global vendors lean on multi-country scale.

Key Report Takeaways

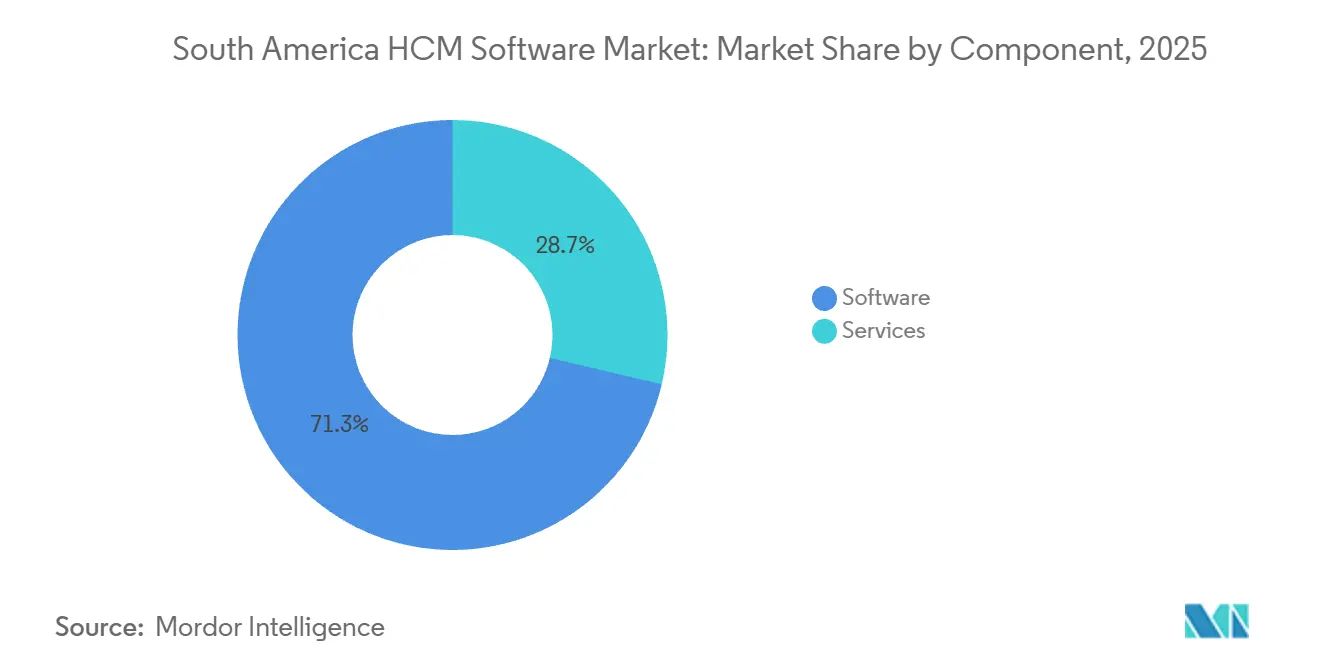

- By component, software led with 71.32% revenue share in 2025, whereas services are projected to register a 10.82% CAGR through 2031.

- By deployment mode, cloud captured 64.18% of the South America HCM software market share in 2025 and is forecast to expand at an 11.24% CAGR to 2031.

- By organization size, large enterprises generated 65.74% of 2025 revenue, while small and medium enterprises are expected to grow at an 11.08% CAGR between 2026 and 2031.

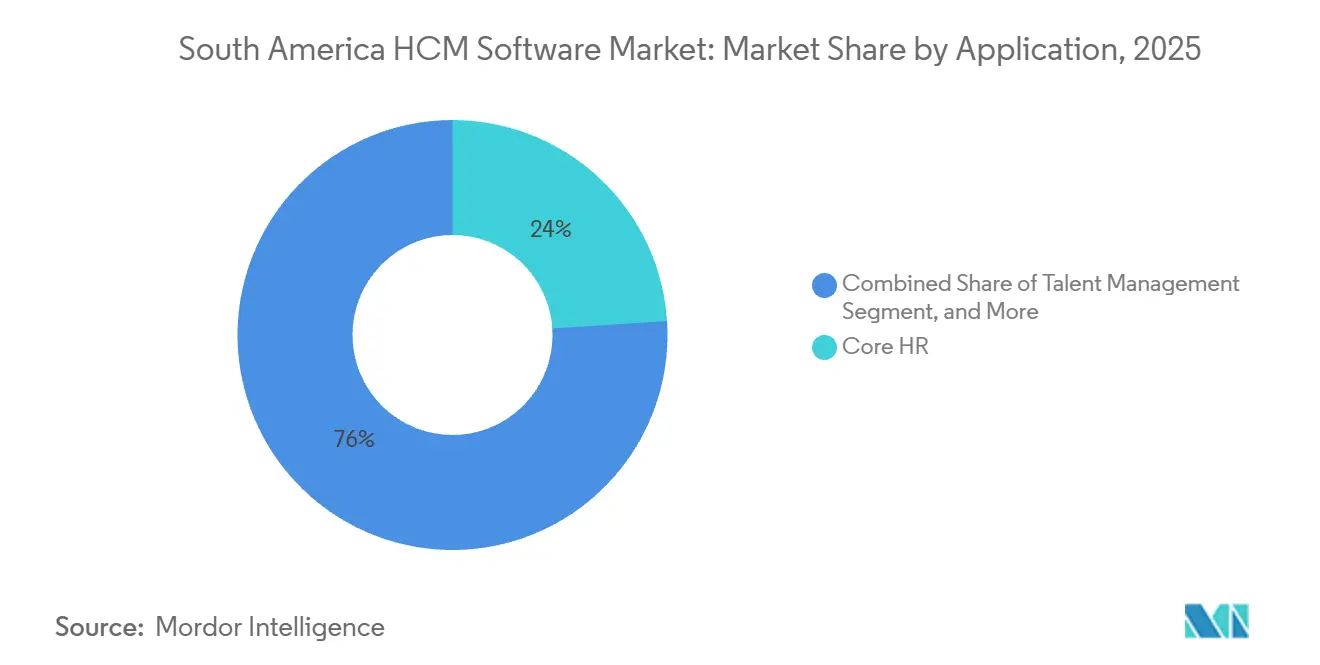

- By application, core HR accounted for 23.96% of 2025 spending, and talent management is poised to rise at an 11.63% CAGR through 2031.

- By end-user industry, BFSI held 24.11% of 2025 revenue, whereas retail and e-commerce are anticipated to advance at an 11.19% CAGR over the forecast horizon.

- By geography, Brazil contributed 41.63% of 2025 revenue, while Chile is projected to record the fastest growth at a 10.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America HCM Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Cloud-Based HCM Suites Among Mid-Sized Firms | +2.8% | Brazil, Chile, Colombia, with spillover to Argentina and Peru | Medium term (2-4 years) |

| Increasing Regulatory Compliance Demands for Labor Laws Digitization | +3.2% | Brazil (DET, equal pay), Argentina (ARCA, Law 27.802), Chile (REL), Colombia (SIGEP) | Short term (≤ 2 years) |

| Growing Remote and Hybrid Workforces Necessitating Digital HR Tools | +2.1% | Urban centers in Brazil (São Paulo, Rio), Argentina (Buenos Aires), Chile (Santiago), with adoption spreading to secondary cities | Medium term (2-4 years) |

| Expansion of Gig Economy Accelerating Demand for Flexible Workforce Management Platforms | +1.9% | Brazil, Argentina, Chile, concentrated in retail, e-commerce, logistics, and platform services | Long term (≥ 4 years) |

| AI-Driven Analytics Enhancing Talent Acquisition Efficiency | +1.4% | Brazil, Chile, Argentina, primarily in BFSI, IT, and telecommunications sectors | Long term (≥ 4 years) |

| Localization of Payroll and Tax Modules for South American Jurisdictions Attracting SMEs | +2.3% | Brazil, Argentina, Chile, Colombia, Peru, with early gains in capital cities and industrial hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Cloud-Based HCM Suites Among Mid-Sized Firms

Mid-sized companies are shifting to the cloud because quarterly compliance patches overwhelm on-premise teams, not because of headline cost savings. Oracle’s HCM Now rollout in March 2024 cut implementation to six months for firms with 500-2,000 workers. Chile’s 15-day REL filing cycle eliminated batch payroll, converting real-time synchronization from a convenience to a requirement.[1]Chile Directorate of Labor, “Electronic Labor Registry (REL) Implementation Requirements,” dt.gob.cl As a result, cloud growth outpaces the South America HCM software market by 166 basis points. Vendors now secure recurring revenue that once drifted to local system integrators. The trend consolidates pricing power and is expected to reshape mid-market negotiations by 2028.

Increasing Regulatory Compliance Demands for Labor Laws Digitization

Brazil’s DET mandate obliges electronic contract submission within 24 hours of hiring, locking enterprises into platforms with automated workflows.[2]Brazil Ministry of Labor and Employment, “Digital Labor Domicile (DET) Implementation Guidelines,” gov.br Argentina’s Law 27.802 centralizes payroll under ARCA starting March 2026, forcing engine overhauls that decentralized systems cannot meet. Chile’s REL fines for late filings make cloud-native architecture the only viable option. Parallel equal-pay analytics under Brazil’s Law 14.611/2023 require dashboards that legacy databases do not support. Together, these statutes convert compliance from periodic audits to always-on monitoring and accelerate retirement of on-premise deployments.

Growing Remote and Hybrid Workforces Necessitating Digital HR Tools

Hybrid work is now permanent, exposing traditional systems that rely on physical presence checks. Enterprises need asynchronous onboarding, multi-timezone scheduling, and contractor oversight inside one interface. São Paulo and Rio de Janeiro firms hire remote staff in secondary cities, but only if platforms manage distributed teams without local HR duplication. The gig economy’s expansion in retail, logistics, and e-commerce forces systems to administer full-time, part-time, and platform workers side by side. The South America HCM software market therefore favors providers with out-of-the-box multi-employment-type support.

AI-Driven Analytics Enhancing Talent Acquisition Efficiency

AI integration in HCM platforms is evolving beyond basic resume screening toward predictive attrition analysis and skills-gap forecasting, enabling HR teams to transition from reactive workforce administration to strategic workforce planning. In sectors such as BFSI and IT across Brazil and Chile, organizations are increasingly adopting AI-enabled talent acquisition tools not primarily to reduce recruitment costs, but to shorten hiring cycles in highly competitive skilled labor markets where talent shortages significantly increase salary pressures. A key market shift is that AI-driven capabilities are rapidly becoming a standard expectation in enterprise HCM deployments rather than premium differentiators. As a result, vendors are increasingly embedding AI capabilities into core platform offerings rather than positioning them as optional add-on modules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Integration Costs for Legacy ERP Environments | -1.8% | Brazil, Argentina, Chile, concentrated in industrial manufacturing and large enterprises with multi-decade ERP investments | Short term (≤ 2 years) |

| Data Privacy Concerns Amidst Cross-Border Cloud Hosting Regulations | -1.3% | Brazil (LGPD Resolution 19/2024), Argentina, Chile, affecting multinational enterprises and cloud vendors without local data centers | Medium term (2-4 years) |

| Shortage of HR Tech Implementation Expertise in Secondary Cities | -0.9% | Secondary cities across Brazil, Argentina, Chile, Peru, Colombia, outside capital and major industrial centers | Medium term (2-4 years) |

| Economic Volatility Reducing IT Budgets for Non-Core Projects | -1.1% | Argentina, Brazil, with spillover effects to Chile, Colombia, and Peru during periods of currency instability | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Integration Costs for Legacy ERP Environments

Manufacturers running SAP or Oracle ERP from the 1990s face 18-24-month integrations with budgets that exceed license spend by up to 300%. Middleware solves technical mapping issues, yet re-engineering decades-old workflows strains the project's scope. CFOs view cloud HCM ROI skeptically, opening doors for incumbent ERP vendors to cross-sell native HCM at a discount. Unless standalone vendors invest in ready connectors, their addressable share of the South America HCM software market may plateau among large enterprises.

Data Privacy Concerns Amidst Cross-Border Cloud Hosting Regulations

Brazil’s LGPD Resolution 19/2024 mandates the adoption of standard clauses for data leaving national borders by August 2025.[3]Brazil National Data Protection Authority, “LGPD Resolution 19/2024 on Cross-Border Data Transfers,” gov.br Vendors hosting employee records in North American or European zones without Brazilian redundancy must re-architect or risk penalties. Multinationals juggling Brazilian, Argentine, and Chilean localization face fragmented residency rules, prompting some to adopt hybrid architectures that erode single-source-of-truth goals. Regional providers with in-country data centers turn compliance into a competitive edge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Signals Implementation Complexity

Services revenue is projected to rise at a 10.82% CAGR to 2031, as enterprises pay for integration, customization, and change management. In 2025, software contributed 71.32% of the South America HCM software market, yet mounting deployment friction suggests total cost of ownership is shifting toward services contracts. Vendors with in-house professional services thus gain margin resilience, whereas pure-play software firms reliant on partners may concede deal control.

The South America HCM software market for services is expanding as mid-sized buyers require guided configuration to meet rapidly changing payroll regulations. Meanwhile, larger enterprises allocate incremental budgets to post-go-live optimization as analytics modules mature. This spending evolution in the South America HCM software market underpins the sustained gap between services growth and overall market averages.

By Deployment Mode: Cloud Dominance Driven By Compliance Velocity

Cloud held 64.18% of the South America HCM software market in 2025 and is forecast to grow at a 11.24% CAGR, outstripping on-premises and hybrid solutions by more than 200 basis points. Brazil’s DET and Argentina’s ARCA compel real-time submission, invalidating batch uploads typical of on-premise tools. Hybrid remains a transitional choice for payroll data sovereignty, but its expansion lags because firms eventually migrate entire stacks once controls mature.

Cloud’s share of the South America HCM software market is expected to grow substantially well before 2031, supported by vendor-managed updates that help organizations quickly adapt to frequent payroll, tax, and labor compliance changes across regional jurisdictions. The model is also gaining traction due to lower upfront infrastructure requirements, faster deployment cycles, and easier scalability for expanding enterprises.

By Organization Size: SME Growth Unlocked By Localized Payroll Modules

Large enterprises accounted for 65.74% of 2025 revenue, yet SMEs are projected to deliver faster incremental growth at a 11.08% CAGR. Localization of tax, social security, and severance rules converted a once manual segment into a digital cohort. Tiered subscription pricing further lowers entry barriers, allowing firms with fewer than 500 employees or small and medium-sized enterprises to attain compliance without custom coding.

Within the South America HCM software market, SME adoption fuels volume, while large enterprises still anchor absolute dollars. Vendors crafting simplified onboarding flows and remote implementation kits capture disproportionate SME logos, creating expansion pathways into adjacent financial and expense modules. The localization of payroll modules for Brazilian, Argentine, and Chilean tax jurisdictions has been the unlock for SME adoption, as these firms lack the IT resources to customize generic platforms and require out-of-the-box compliance that global vendors historically under-invested in building.

By Application: Talent Management Surge Reflects Skills-Orchestration Shift

Core HR accounted for 23.96% of the 2025 application spend because every buyer starts with an employee master file. Yet talent management is projected to climb at an 11.63% CAGR, the fastest among modules, as employers chase predictive hiring and upskilling. The South America HCM software market share for core HR will decline gently as budgets tilt toward performance analytics, learning, and succession mapping.

AI-driven recommendations shorten time-to-skill in BFSI, IT, and telecom, where specialized roles are costly to backfill. Learning and development modules are gaining traction as enterprises recognize that skills gaps cannot be closed through external hiring alone, creating demand for HCM platforms that integrate training content with career pathing and succession planning. Vendors embedding career-path visualizations and micro-learning libraries strengthen renewal prospects.

By End-User Industry: Retail And E-Commerce Growth Driven By Platform-Worker Management

BFSI delivered 24.11% of 2025 revenue owing to regulatory scrutiny and large white-collar headcounts. Retail and e-commerce, however, are expected to register the highest CAGR of 11.19%, driven by the need to manage a blend of full-time associates, part-time staff, and gig couriers in a single system. This complexity steers budgets toward human capital management platforms with schedule automation and contractor tax logic.

Industrial manufacturing prioritizes shift scheduling and safety compliance, whereas healthcare demands credential-tracking modules. Healthcare and lifesciences face unique challenges around credential verification and shift scheduling, creating demand for specialized HCM features that generic platforms handle through customization rather than native functionality. Government adoption increases as public entities digitize HR, echoing Colombia’s SIGEP blueprint. Overall, vertical variability pushes vendors to keep configurable frameworks while prioritizing deep out-of-the-box rules for the fastest-growing industries.

Geography Analysis

Brazil accounted for 41.63% of 2025 revenue due to its large population and the stringent Digital Labor Domicile requirement. Equal-pay disclosures further intensified analytics needs, making Brazil the anchor of the South America HCM software market. Cloud leaders invested early in Brazilian payroll engines to capture this compliance-heavy spend. Chile is forecast to expand at a 10.74% CAGR to 2031, the region’s quickest pace, because the REL system imposes 15-day document filing that manual workflows rarely meet. Mid-sized Chilean companies are now migrating directly to the cloud, bypassing the on-premises stage that characterized earlier adopters elsewhere.

Argentina’s Labor Modernization Law 27.802, effective March 2026, centralizes with ARCA and introduces the FAL litigation fund. Enterprises must rescope payroll structures, driving a replacement cycle that supports sustained double-digit growth through 2029. Data-sovereignty clauses are less restrictive than Brazil’s, but centralized tax reconciliation widens functional gaps in older suites. Colombia, Peru, and the rest of South America trail the large markets by 3-5 years in digital HR maturity. Yet planned registry mandates modeled on those of Brazil and Chile suggest a second adoption wave beginning in 2027.

Urban concentration matters as cities like São Paulo, Buenos Aires, Santiago, and Bogotá house most enterprise IT budgets, while secondary cities rely on vendors that provide remote implementation and pre-configured templates. Strategically, providers must balance deep localization against multi-country breadth. Oracle’s bet on Brazilian-first six-month rollouts contrasts with European entrants Factorial and Visma, which leverage GDPR-aligned infrastructure to win multinational accounts seeking region-wide uniformity.

Competitive Landscape

Competition is moderately fragmented. Oracle, SAP, Workday, and ADP secure large-enterprise deals by bundling with ERP or multi-country payroll. Their slate of features aligns with complex governance needs, yet pricing and implementation cycles deter mid-market buyers. Regional contenders like Meta4, Cegid, and Odoo win SMEs through native Brazilian and Argentine payroll tables that global suites treat as configurable extras.

European newcomers Factorial, Visma, and HiBob combine GDPR strengths with agile rollout, carving share among data-sovereignty-minded customers. Niche disruptors such as Deel and Rippling focus on contractor management, leveraging API-first foundations that reduce middleware costs. White-space opportunities exist in vertical micro-solutions: retail shift planning, healthcare credential management, and public-sector grant-funded workforce programs.

Strategic moves underscore differentiation. Oracle condensed the HCM Now implementation to six months for Brazilian mid-sized firms.[4]Oracle Corporation, “Oracle Announces HCM Now Expansion to Brazil,” oracle.com Meta4 packaged compliance updates into subscription tiers that guarantee deadline alignment. Factorial partnered with local tax advisory firms to embed quarterly threshold alerts inside dashboards. These initiatives shift client selection criteria from raw feature lists to speed of compliance and clarity of total cost.

South America HCM Software Industry Leaders

Workday, Inc.

Dayforce, Inc.

Automatic Data Processing, Inc.

Oracle Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Brazil’s Digital GRU payment system became mandatory for all labor-related fees, obliging payroll engines to sync real-time transactions.

- March 2026: Argentina enacted the Labor Modernization Law 27.802, centralizing payroll under ARCA and creating the FAL litigation fund.

- August 2025: Brazil’s ANPD enforced LGPD Resolution 19/2024, requiring standard clauses for cross-border HR data transfers.

- April 2025: Visma announced the acquisition of Lara AI, a leading AI-driven platform that enhances traditional HR management with AI.

South America HCM Software Market Report Scope

The South America Human Capital Management (HCM) Software Market refers to the market for software platforms and related services that help organizations across South America manage and optimize their human resources functions, workforce operations, employee lifecycle processes, and talent strategies through digital solutions. The market includes integrated HCM software suites and standalone applications delivered through cloud, on-premises, and hybrid deployment models. These solutions support a wide range of HR functions, including core HR administration, talent management, workforce management, payroll management, and learning and development. The market also includes associated implementation, integration, consulting, support, and managed services.

The South America HCM Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, Payroll Management, and Learning and Development), End-User Industry (IT and Telecommunications, BFSI, Industrial Manufacturing, Healthcare and Lifesciences, Retail and E-commerce, Government and Public Sector, and Other End-User Industries), and Country (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Core HR |

| Talent Management |

| Workforce Management |

| Payroll Management |

| Learning and Development |

| IT and Telecommunications |

| BFSI |

| Industrial Manufacturing |

| Healthcare and Lifesciences |

| Retail and E-commerce |

| Government and Public Sector |

| Other End-User Industries |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Core HR |

| Talent Management | |

| Workforce Management | |

| Payroll Management | |

| Learning and Development | |

| By End-User Industry | IT and Telecommunications |

| BFSI | |

| Industrial Manufacturing | |

| Healthcare and Lifesciences | |

| Retail and E-commerce | |

| Government and Public Sector | |

| Other End-User Industries | |

| By Geogrpahy | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the forecast CAGR for the South America HCM software market to 2031?

The market is projected to register a 9.64% CAGR from 2026 to 2031, reporting market size of USD 3.71 billion by 2031 according to Mordor Intelligence.

Which deployment mode is growing fastest across South America?

Cloud deployment is expected to expand at an 11.24% CAGR because real-time compliance updates outpace on-premise capabilities.

Which country contributes the highest revenue today?

Brazil generated 41.63% of 2025 regional revenue, driven by complex payroll laws and mandatory digital submissions.

Which application segment is forecast to grow most rapidly?

Talent management is set to rise at an 11.63% CAGR as firms prioritize predictive hiring and upskilling.

Why are services revenue rising faster than software licenses?

Enterprises incur sizable integration and change-management costs, driving services growth at a 10.82% CAGR, a higher rate than software.

Page last updated on: