HCM Software In IT And Telecom Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

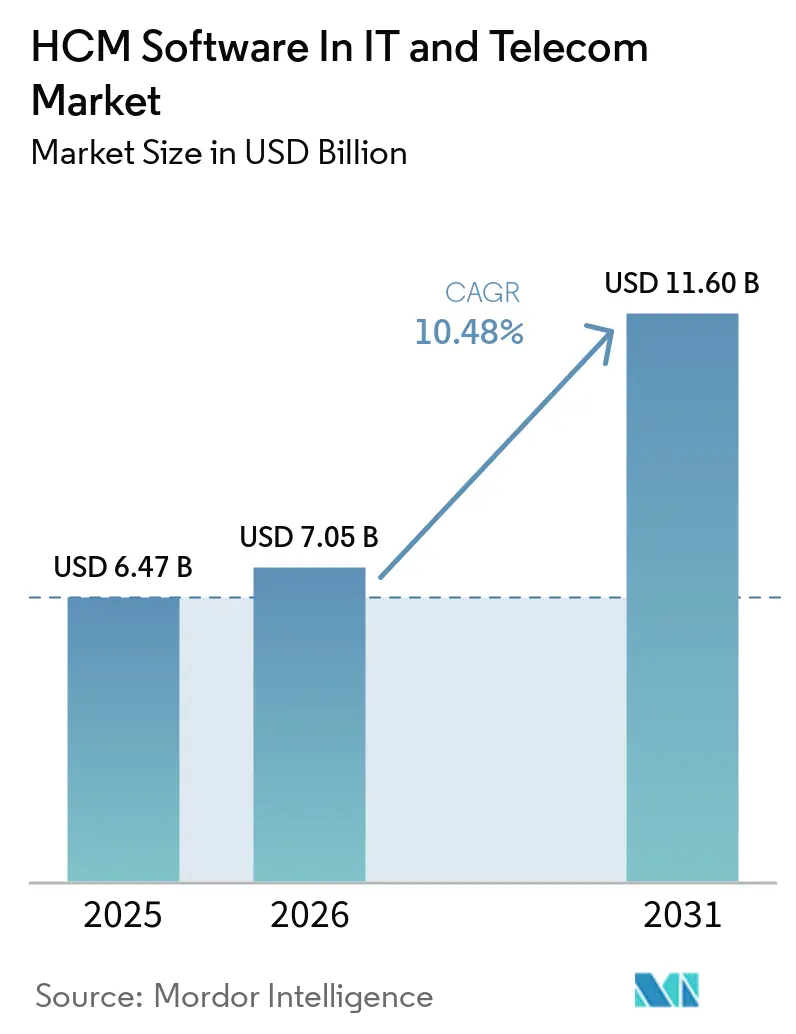

| Market Size (2026) | USD 7.05 Billion |

| Market Size (2031) | USD 11.60 Billion |

| Growth Rate (2026 - 2031) | 10.48% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HCM Software In IT And Telecom Market Analysis by Mordor Intelligence

The HCM software in IT and telecom market size is expected to increase from USD 6.47 billion in 2025 to USD 7.05 billion in 2026 and reach USD 11.60 billion by 2031, growing at a CAGR of 10.48% over 2026-2031. Growth reflects a shift from payroll automation toward AI-guided workforce orchestration that lets telecom operators upskill field engineers for Open RAN rollouts while IT service firms embed real-time skill graphs into staffing engines. Cloud deployment held a 56.88% revenue share in 2025, yet hybrid architectures are growing faster as enterprises reconcile sovereign‐data mandates with SaaS agility. Services revenue is gaining momentum on the back of large-scale migration projects that stitch together fragmented HR databases and configure AI agents to auto-schedule 5G installation crews. Competitive pressure is intensifying as private-equity sponsors buy pure-play vendors and ERP incumbents embed generative-AI copilots to defend installed bases.

Key Report Takeaways

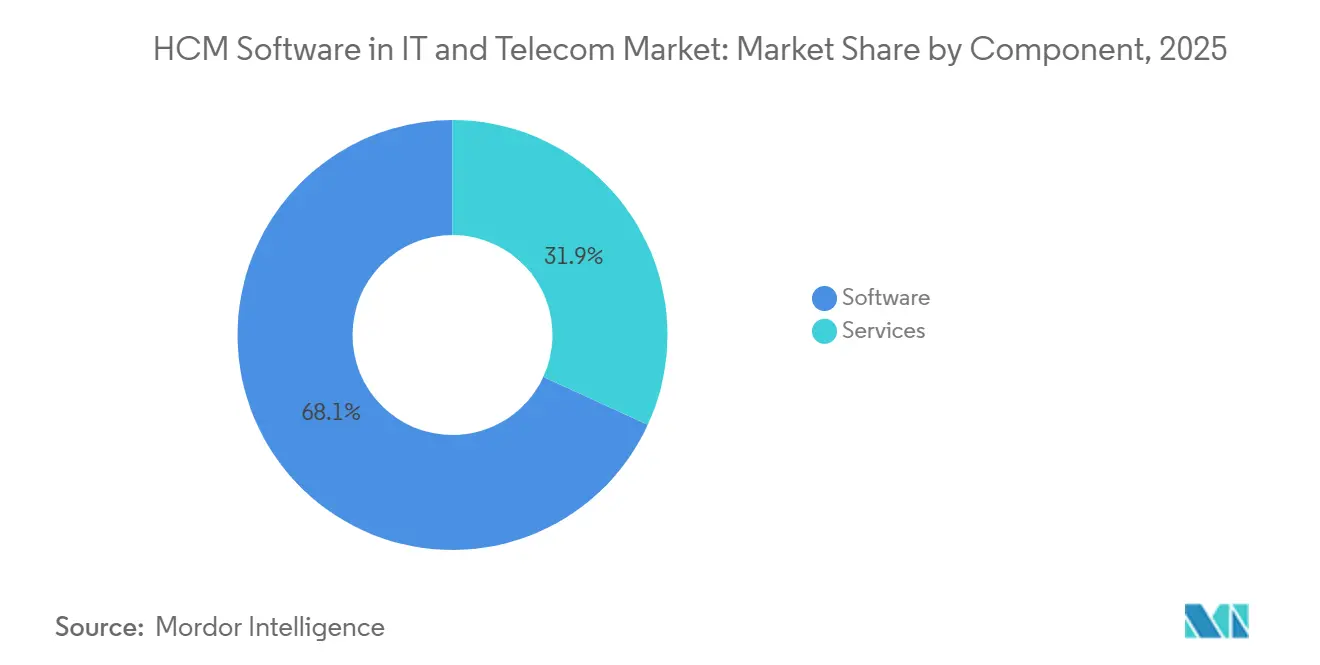

- By component, software captured 68.14% of 2025 spending while services are projected to expand at a 13.76% CAGR through 2031.

- By deployment mode, cloud architectures dominated with 56.88% share in 2025, but hybrid configurations are forecast to post a 12.91% CAGR through 2031.

- By application, payroll commanded 45.31% of 2025 revenue whereas talent management is projected to rise at a 12.52% CAGR to 2031.

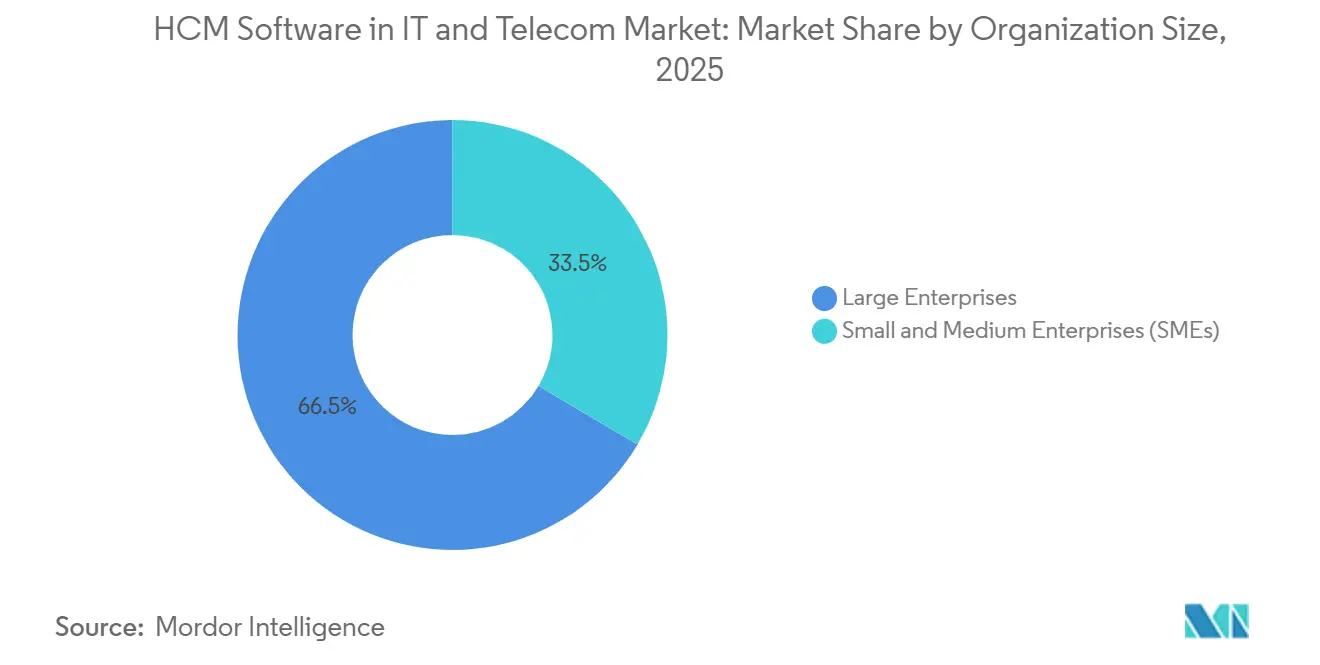

- By organization size, large enterprises represented 66.49% of 2025 outlays, yet small and medium enterprises are expected to advance at a 13.38% CAGR through 2031.

- By end-user industry, IT services led with 47.02% of 2025 expenditure while managed service providers are on track for a 12.14% CAGR to 2031.

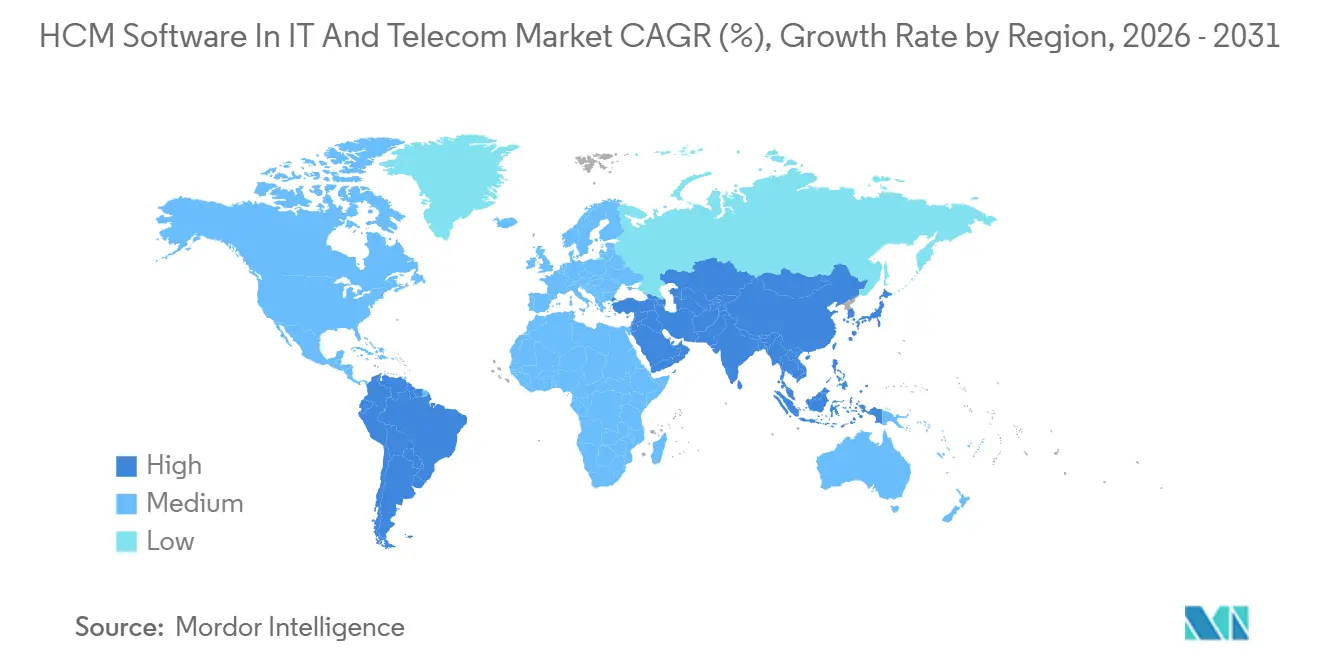

- By geography, North America held 37.12% share in 2025 and Asia-Pacific is anticipated to climb at an 11.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HCM Software In IT And Telecom Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Cloud-Native Adoption in IT Stacks | +3.2% | Global, early focus in North America and Europe | Medium term (2-4 years) |

| AI-Enabled Skill Mapping for Telecom Network Evolution | +2.8% | Asia-Pacific core, spillover to Middle East and Africa | Long term (≥ 4 years) |

| Integrated Analytics Driving ROI Visibility | +2.1% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Compliance Mandates for Distributed Workforces | +1.9% | Europe, Asia-Pacific, South America | Medium term (2-4 years) |

| Rising M&A Activity Among Pure-Play HCM ISVs | +1.5% | North America and Europe | Short term (≤ 2 years) |

| Shift Toward Unified Employee Experience Platforms | +1.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Cloud-Native Adoption in IT Stacks

IT service providers and telecom operators are re-platforming HR workloads onto containerized microservices to gain sub-second API response times for real-time labor allocation. Workday’s EU Sovereign Cloud release in November 2025 lets European carriers keep data in-region without losing functionality, aligning with GDPR demands. SAP SuccessFactors added more than 400 cloud-native enhancements in 2026, including payroll bots that reconcile taxes across 47 countries.[1]SAP SuccessFactors 1H 2026 Release Notes, SAP, sap.com The architecture shift cuts infrastructure overhead by up to 35% compared with on-premises estates and accelerates MSP onboarding cycles from weeks to days.

AI-Enabled Skill Mapping for Telecom Network Evolution

Asia-Pacific telecom operators deploy AI engines that parse certifications and training records to forecast which technicians can shift from copper maintenance to 5G small-cell builds. Eightfold AI identifies flight-risk engineers and triggers retention offers, lowering attrition by 22%. Platforms such as SkillPanel now propose personalized upskilling paths that close gaps within 90 days, helping carriers repurpose legacy staff for Open RAN projects.

Integrated Analytics Driving ROI Visibility

Finance leaders expect hard numbers from HR investments, so vendors embed predictive dashboards that translate engagement metrics into revenue impact. Ceridian documented a 176% three-year ROI for an IT services customer after automating 14,000 manual payroll hours. isolved registered a 330% return for a mid-market telecom operator by consolidating six point tools. Such analytics elevate HR from compliance cost to revenue lever.

Compliance Mandates for Distributed Workforces

Divergent data-localization statutes drive hybrid deployments where core payroll sits in sovereign clouds while talent modules run in global regions. InCountry found 68% of multinational IT services firms chose this split architecture in 2025, boosting license costs by 23%. Brazil’s eSocial and India’s data-protection act require live payroll reporting and local storage of biometric logs, adding integration complexity and raising total ownership costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Residency and Sovereignty Concerns | -1.8% | Europe, Asia-Pacific, Middle East | Medium term (2-4 years) |

| Prolonged Legacy ERP Replacement Cycles | -1.6% | Global, acute in large enterprises | Long term (≥ 4 years) |

| Shortage of Domain-Specific HCM Integrators | -1.1% | Asia-Pacific, Middle East, Africa, South America | Medium term (2-4 years) |

| Capital-Expenditure Freeze in Telcos Under Margin Pressure | -0.9% | Europe, South America, select Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Residency and Sovereignty Concerns

Enterprises juggling GDPR in Europe, China’s CSL, and India’s DPDP Act must maintain multiple HCM instances. Vendors now charge 15%-20% premiums for sovereign-cloud SKUs, squeezing IT budgets at carriers already funding 5G rollouts. The fragmented landscape prolongs implementation timelines by up to six months and forces additional audit layers that strain HR teams.

Prolonged Legacy ERP Replacement Cycles

Roughly half of large telecom operators still run SAP ECC or Oracle E-Business Suite, with hundreds of custom tax scripts that resist lift-and-shift migrations. Re-implementing these rules in SaaS demands middleware and change-management budgets that boards defer when cash is tight. Contractual penalties for workload movement further dampen migration appetite, extending legacy life cycles well into the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Revenue Accelerates on Integration Demand

Services accounted for 31.86% of 2025 revenue, but their 13.76% CAGR means this slice of the HCM software in IT and telecom market size will widen by 2031. Systems integrators configure AI shift-scheduling engines and extract decades of payroll history from on-premises ERPs, workloads that customers are reluctant to tackle alone. The HCM software in IT and telecom market share held by software will remain substantial because vendors embed generative copilots that auto-draft job descriptions and compensation offers, yet subscription growth is leveling as license renewal cycles mature.

Large MSPs standardize Dayforce, Oracle HCM Cloud, or UKG across client portfolios to streamline contractor onboarding, driving recurring advisory fees. Vendors respond with fixed-price migration bundles that include data extraction and 90-day hypercare, turning what was a one-time license transaction into a multiyear services annuity.

By Deployment Mode: Hybrid Bridges Sovereign and Public Clouds

Cloud remained dominant at 56.88% in 2025, but hybrid’s 12.91% CAGR positions it as the fastest-rising slice of the HCM software in IT and telecom market size over the forecast horizon. Enterprises store core payroll in sovereign environments to respect GDPR or India’s DPDP rules while running talent analytics in global regions where GPU capacity sits, a configuration that still meets latency targets for AI workloads.

Hybrid growth underscores the tension between cloud economics and data sovereignty. Vendors such as Oracle now allow administrators to geofence individual tables so salary data never leaves the country, while engagement-survey responses sync to regional clusters for sentiment analysis. On-premises footprints will keep shrinking, though certain carriers bound by union accords continue to host systems locally to satisfy collective agreements.

By Application: Talent Management Gains on Skill-Graph Adoption

Payroll led with 45.31% of 2025 revenue, yet talent management’s 12.52% CAGR signals where vendors are innovating. Workday released Illuminate Agents to auto-draft job descriptions and compensation guidance.[2]Workday, “Illuminate Agents: AI-Powered Insights,” workday.com Modern suites stitch internal competency graphs to external labor data, matching developers to billable projects within hours and improving bench utilization. These dynamics push the HCM software in IT and telecom market share toward applications that influence revenue rather than merely record it.

Telecom operators deploy succession engines that flag copper-line technicians ready to learn fiber splicing, saving recruiting expense and meeting service-level goals. Meanwhile, workforce management modules evolve to predict overtime risk and automate hazard-pay calculations at tower sites, narrowing the performance gap with niche scheduling vendors.

By Organization Size: SMEs Benefit From Embedded Finance

Large enterprises controlled two-thirds of 2025 spending, but SMEs are growing faster as bundled payroll, benefits, and working-capital advances remove banking friction. Consumption-based pricing aligns monthly cost with headcount swings, an attractive proposition for fast-scaling IT consultancies. As a result, the HCM software in IT and telecom market size captured by SMEs will expand meaningfully through 2031.

Platforms such as Rippling expose open APIs so tech startups can bolt custom time-tracking or stock-option modules onto a core system, limiting vendor lock-in. Legacy providers answer with freemium tiers that convert to paid plans once headcount tops preset thresholds, defending share in the mid-market band.

By End-User Industry: MSPs Standardize Contractor Workflows

IT services firms held 47.02% of 2025 revenue, but managed service providers, advancing at 12.14% CAGR, represent the most vibrant demand pool. MSPs need multi-tenant HCM stacks that segregate client data yet surface cross-portfolio analytics, a capability native in modern SaaS suites. This requirement will raise the MSP slice of the HCM software in IT and telecom market size during the forecast period.

Telecom operators invest in AI schedulers to juggle call-center rosters against NPS targets, while data-center builders track electricians and HVAC crews across hyperscale sites to meet safety mandates. Each use case feeds vendor roadmaps that prioritize vertical depth over generic functionality.

Geography Analysis

North America remained the revenue anchor with 37.12% share in 2025, supported by high cloud penetration, abundant venture funding, and deep payroll domain expertise. Most early Workday, ADP, and UKG deployments originated here, and renewal rates stay near 90%. Yet regulatory stability means future growth moderates, even as upsell potential persists for AI modules.

Asia-Pacific delivers the fastest growth at an 11.78% CAGR through 2031 as carriers in India, Indonesia, and the Philippines digitize blue-collar labor to optimize tower energy spend. Carriers in India and Indonesia digitize labor management programs, du Telecom cited 50% efficiency gains after a 2025 deployment of TCS’s HCM platform.[3]TCS, “du Telecom Achieves 50% Efficiency Gains,” tcs.com Domestic data-protection laws push vendors to open in-country zones, creating a springboard for local integrators and boosting the region’s slice of the HCM software in IT and telecom market size. Telecom-specific functionality, such as hazard-pay automation and biometric attendance, drives take-up among operators managing dispersed field crews.

Europe holds significant installed bases thanks to stringent works-council engagement rules and wage-equalization directives. GDPR-driven data-sovereignty spending lifts hybrid adoption, though macro headwinds and protracted ERP replacement slow total license growth. Still, sovereign-cloud releases from SAP and Workday preserve momentum, preventing share erosion.

The Middle East and Africa market expands because nationalization programs require real-time dashboards to prove citizen workforce ratios. Sovereign-cloud demand here mirrors Europe, yet limited legacy burden enables greenfield SaaS rollouts that skip on-premises entirely. South America faces currency volatility, but compliance platforms that automate Brazil’s eSocial reporting keep cloud conversions moving, sustaining a mid-single-digit share.

Competitive Landscape

The top five vendors, Workday, SAP, Oracle, UKG, and ADP, collectively hold roughly 60%-65% revenue, indicating a moderately concentrated arena. Recent leveraged buyouts, such as Thoma Bravo’s USD 12.3 billion Ceridian deal, signal that private equity views recurring HCM cash flows as predictable, funding R&D that bolsters analytics capabilities. ERP incumbents insert generative-AI copilots to defend legacy edges, while disruptors like Rippling and Gusto unbundle suites through API-first architectures that appeal to developer-centric buyers.

Vertical specialization shapes strategy. Vendors are releasing telecom-grade scheduling modules that spike-shifts when traffic surges and data-center payroll engines that manage employer-of-record compliance across 12 jurisdictions. Those niche add-ons command 20%-30% price premiums and create cross-sell hooks into adjacent modules.

Partnership ecosystems also evolve. UKG aligned with Google Cloud in 2026 to fuse Vertex AI into labor-forecasting engines, cutting overstaffing costs for pilot telcos. Workday bolstered learning content through its Sana acquisition to shorten skill-gap closure times. MSPs leverage white-label versions of these suites, extending vendor reach into hundreds of downstream clients without direct sales touch.

HCM Software In IT And Telecom Industry Leaders

Workday Inc.

SAP SE

Oracle Corporation

ADP LLC

UKG Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Kwant launched a real-time location system for hyperscale data-center construction sites, linking hazard-zone dwell time to payroll calculations.

- March 2026: Workday acquired Sana to embed AI-driven learning paths within its talent stack.

- January 2026: ADP rolled out ADP Assist, generative-AI agents that draft job posts and schedule interviews.

- January 2026: UKG partnered with Google Cloud to infuse Vertex AI into shift-scheduling algorithms for telecom operators.

Global HCM Software In IT And Telecom Market Report Scope

HCM Software in IT and Telecom Market features platforms that facilitate talent acquisition, skills mapping, project allocation, and performance management for dynamic, skilled workforces. These solutions empower organizations to navigate global teams, intricate billing/resource dependencies, and the imperative of continuous upskilling. Cloud-based HCM platforms enhance productivity, offer greater workforce visibility, and harness AI for skills intelligence. The market's expansion is driven by digital transformation, the rise of hybrid work, and a surging demand for talent in cloud computing, cybersecurity, and network engineering.

The HCM Software in IT and Telecom Market Report is Segmented by Component (Software, and Services), Deployment Mode (On-Premises, Cloud, and Hybrid), Application (Core HR, Talent Management, Workforce Management, Payroll, and Other Applications), Organization Size (Small and Medium Enterprises, and Large Enterprises), End User Industry (IT Services, Telecom Operators, Data Centers, Managed Service Providers, and Other End User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| On-Premises |

| Cloud |

| Hybrid |

| Core HR |

| Talent Management |

| Workforce Management |

| Payroll |

| Other Applications |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| IT Services |

| Telecom Operators |

| Data Centers |

| Managed Service Providers |

| Other End User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Application | Core HR | |

| Talent Management | ||

| Workforce Management | ||

| Payroll | ||

| Other Applications | ||

| By Organization Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By End User Industry | IT Services | |

| Telecom Operators | ||

| Data Centers | ||

| Managed Service Providers | ||

| Other End User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current HCM software in IT and telecom market size and how fast is it growing?

The market stands at USD 7.05 billion in 2026 and is projected to reach USD 11.60 billion by 2031, reflecting a 10.48% CAGR over 2026-2031.

Which deployment model is expanding the quickest?

Hybrid configurations are advancing at a 12.91% CAGR as firms balance sovereign-cloud mandates with public-cloud analytics.

Which application area is forecast to outpace others?

Talent management modules lead growth with a 12.52% CAGR thanks to AI-driven skill-graph adoption among IT service providers and telecom operators.

Why are services revenues rising faster than software?

Organizations rely on integrators to migrate legacy payroll data and configure AI agents, pushing services to a 13.76% CAGR despite software’s larger base.

Which region will deliver the highest growth through 2031?

Asia-Pacific is projected to post an 11.78% CAGR as carriers in India, Indonesia, and the Philippines digitize workforce management at scale.

Page last updated on: