Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

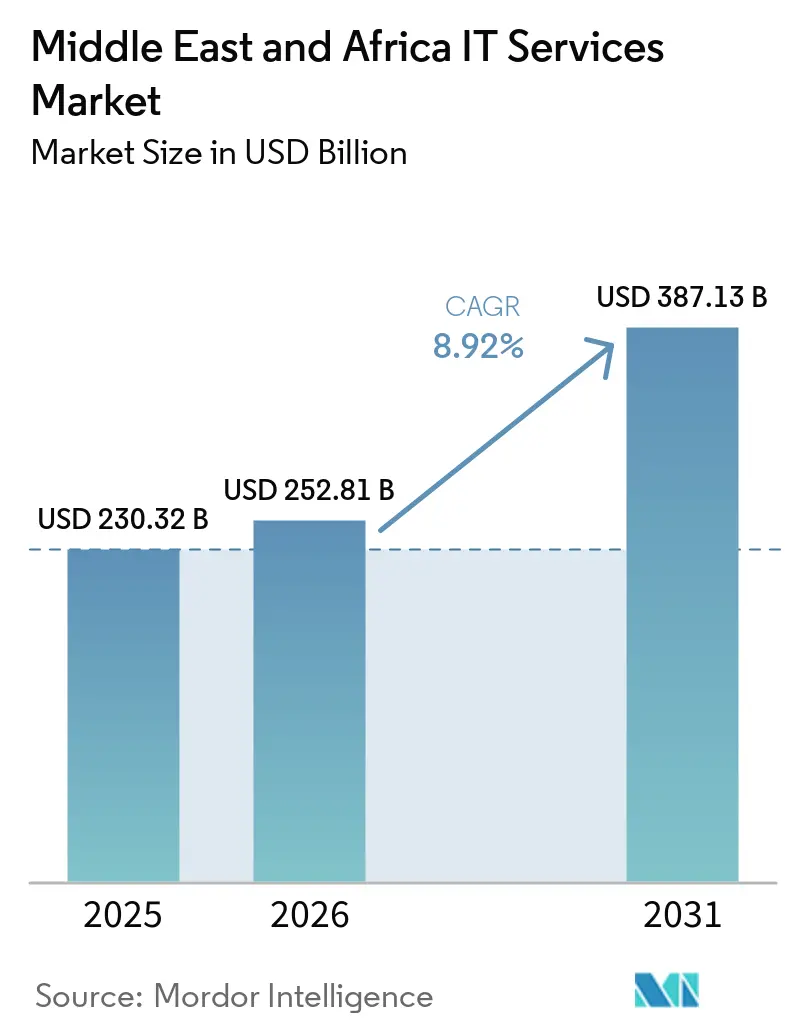

| Base Year Market Size (2025) | USD 230.32 Billion |

| Market Size (2026) | USD 252.81 Billion |

| Market Size (2031) | USD 387.13 Billion |

| Growth Rate (2026 - 2031) | 8.92% CAGR |

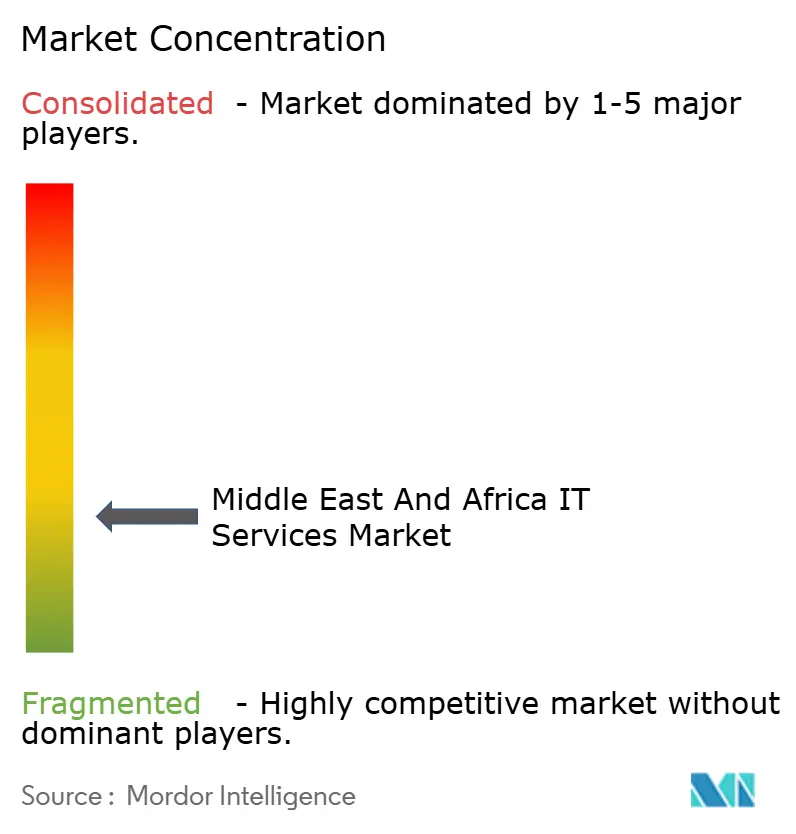

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa IT Services Market Analysis by Mordor Intelligence

The Middle East and Africa IT services market size is projected to expand from USD 230.3 billion in 2025 and USD 252.8 billion in 2026 to USD 387.1 billion by 2031, registering a CAGR of 8.9% between 2026 to 2031. Sovereign digital-transformation programs, all-time-high hyperscale data-center spending, and a structural pivot toward cloud-native architectures keep large deals flowing despite macro uncertainty. The Middle East and Africa IT services market benefits from Vision-2030 mandates that accelerate public-sector cloud migration while African governments leapfrog legacy systems through mobile-first platforms. Hyperscalers rush to add local regions, compressing compute pricing and enabling regional software vendors to launch SaaS offerings quicker than in the past. Skills shortages, fragmented data-flow laws, and energy-cost volatility temper the outlook but do not derail multi-year investment plans.

Key Report Takeaways

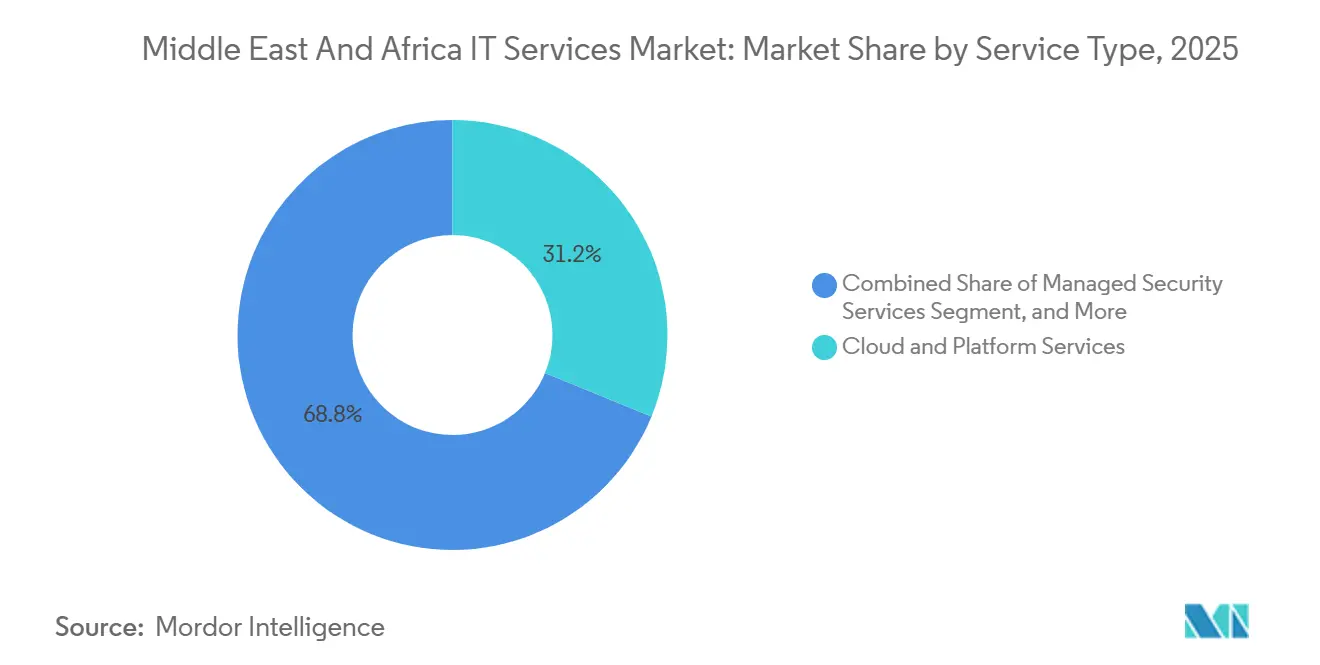

- By service type, Cloud and Platform Services led with 31.2% revenue share in 2025, while Managed Security Services is forecast to expand at a 9.5% CAGR through 2031.

- By enterprise size, Large Enterprises accounted for 66.4% of spending in 2025; Small and Medium Enterprises are the fastest-growing bracket at a 9.8% CAGR to 2031.

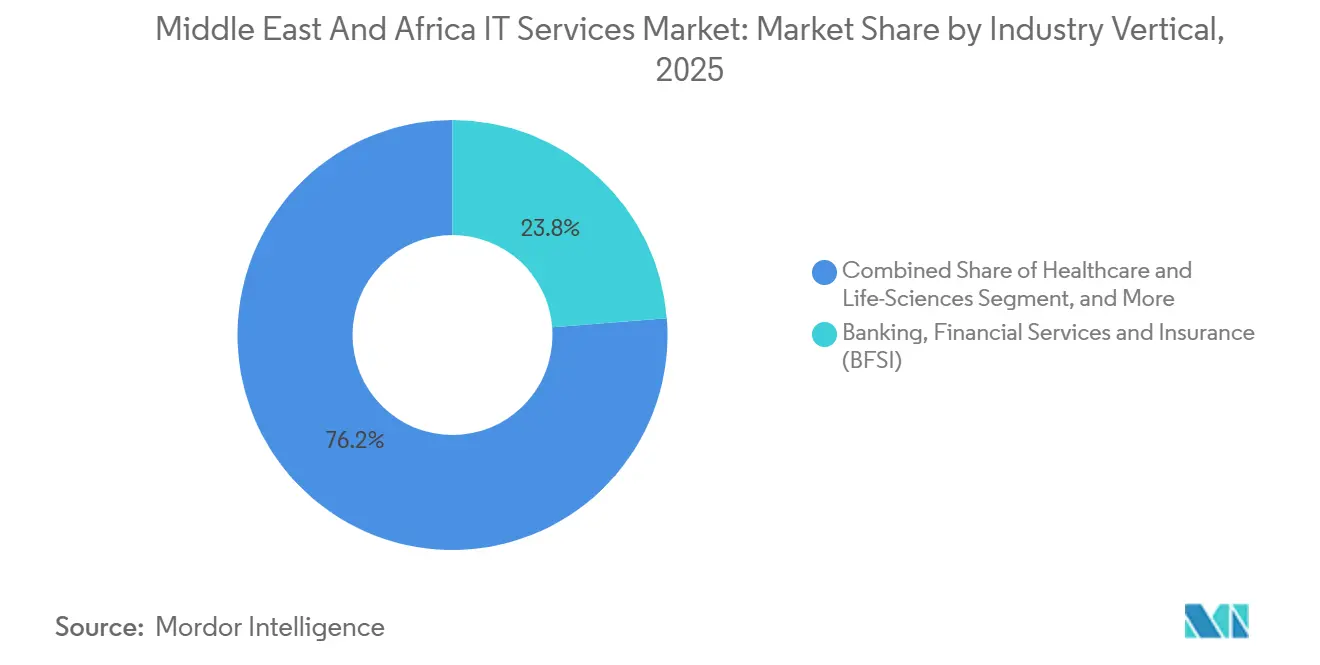

- By industry vertical, Banking and Financial Services held 23.8% share in 2025; Healthcare and Life-Sciences is advancing at a 9.3% CAGR over 2026-2031.

- By deployment model, Onshore Delivery accounted for 45.3% of outlays in 2025; Offshore Delivery shows the strongest trajectory, with a 10.0% CAGR to 2031.

- By geography, the Middle East captured 62.8% of 2025 revenue; Africa is the fastest-expanding sub-region at a 9.8% CAGR for the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East and Africa IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-First Initiatives Under Vision 2030 Programs | +2.10% | Saudi Arabia, UAE, Qatar, Bahrain | Medium term (2-4 years) |

| Surge in Hyperscale Data-Center Investments Across GCC | +1.80% | GCC core, spill-over to Egypt and South Africa | Medium term (2-4 years) |

| Digital Public-Services and E-Government Spending | +1.30% | Global, with concentration in Saudi Arabia, UAE, Egypt, Kenya | Short term (≤ 2 years) |

| Regional Fintech Boom Driving Managed-Services Demand | +1.50% | GCC and North Africa, early gains in Nigeria and Kenya | Medium term (2-4 years) |

| AI and Generative-AI Mandates by Sovereign Wealth Funds | +1.70% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| 5G and Edge-Computing Roll-Out Fuelling Integration Projects | +1.20% | GCC nations, phased expansion to urban Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Initiatives Under Vision 2030 Programs

Government policies push 70% of Saudi public workloads to cloud platforms by 2026, forcing agencies to refactor legacy applications and adopt multi-cloud orchestration.[1]Saudi Data and Artificial Intelligence Authority, “Personal Data Protection Law,” sdaia.gov.sa Similar mandates in the UAE and Bahrain convert capital budgets into operating outlays, generating recurring demand for migration factories and platform integration. As most local engineers still specialize in monolithic stacks, providers field offshore Kubernetes and DevOps squads to fill gaps.[2]PwC, “Middle East Workforce Survey 2025,” pwc.com Certification bootcamps ease pressure, but full labour equilibrium is unlikely before 2028. Vendors able to blend onshore Arabic engagement with offshore agile pods secure a first-mover advantage in the Middle East and Africa IT services market.

Surge in Hyperscale Data-Center Investments Across GCC

Oracle, Microsoft, Google Cloud, and AWS collectively announced more than USD 6 billion of new regions during 2025, expanding total GCC data-center capacity toward 1,200 MW by 2027. Local zones slash latency and satisfy data-sovereignty clauses, letting enterprises lift-and-shift workloads that were previously stranded on-premises. Hyperscalers bundle credits, training, and marketplace incentives, accelerating the Middle East and Africa IT services market pivot toward cloud managed services. Competition intensifies as clients demand vendor-neutral multi-cloud blueprints rather than single-provider lock-in. Integrators able to secure premier partnership tiers and demonstrate cloud-agnostic tooling gain share.

AI and Generative-AI Mandates by Sovereign Wealth Funds

Saudi Arabia’s Public Investment Fund earmarked USD 40 billion for an Arabic large-language-model ecosystem, this sovereign AI investment is a pivotal growth lever for the Saudi Arabia IT services, while the UAE’s Mubadala placed USD 1.2 billion into localized Azure OpenAI services. These moves trigger parallel demand for model-risk governance, prompt-engineering, and enterprise integration in the Middle East and Africa IT services market. Indian majors and global consultancies launch AI centers in Riyadh and Dubai, collapsing proof-of-concept cycles from six months to six weeks. Scarcity of Arabic-fluent data scientists inflates contractor rates by 30-40%, encouraging hybrid delivery models that mix onshore subject-matter experts and offshore engineering benches. Providers that stock reusable Arabic embeddings and compliance playbooks achieve faster deal velocity.

Regional Fintech Boom Driving Managed-Services Demand

Digital payment volumes in the UAE grew 52% year-on-year in Q1 2025, while Saudi fintech licenses nearly doubled, deepening workloads that require 24/7 monitoring and stringent AML compliance.[3]Central Bank of the UAE, “UAE Digital Payments Q1 2025,” centralbank.ae Banks and neobanks alike outsource transaction-monitoring, API-gateway management, and cloud core-banking stacks to avoid heavy capex. As fintech ecosystems spread across Egypt, Nigeria, and Kenya, demand diffuses beyond GCC hubs, creating regional scale economies for security-operations-center providers. The Middle East and Africa IT services market thus finds a durable growth flywheel in payments modernization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Shortage of Bilingual Cloud-Native Talent | -0.90% | GCC nations, North Africa | Medium term (2-4 years) |

| Fragmented Cross-Border Data-Flow Regulations | -0.70% | Regional, with acute friction between GCC and Africa | Long term (≥ 4 years) |

| High Energy Cost and Unreliable Grids in Parts of Africa | -0.50% | Sub-Saharan Africa, excluding South Africa | Medium term (2-4 years) |

| Geopolitical Volatility Affecting Outsourcing Contracts | -0.40% | Middle East, spillover to North Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Shortage of Bilingual Cloud-Native Talent

Nearly 68% of Middle East CIOs struggle to hire Arabic-English DevOps engineers. Universities graduate fewer than 200,000 computer-science majors annually across MENA, a fraction of projected demand. Golden Visas and bootcamps raise supply, yet the gap persists, lifting day-rates for senior cloud architects in Riyadh to USD 200,000, on par with Silicon Valley. Vendors offset shortages with offshore pods, but time zones and data-localization rules add coordination cost, eroding some savings.

Fragmented Cross-Border Data Laws

Saudi PDPL, UAE DPDL, and Egypt’s Data Protection Law each impose unique storage and consent rules, forcing enterprises to duplicate infrastructure in multiple countries. Multinationals maintain parallel cloud landing zones, inflating the total cost of ownership and complicating disaster-recovery topologies. Smaller Gulf markets cannot justify dedicated hyperscale regions, leaving firms to accept higher latency or regulatory risk. Harmonization talks under the African Union and GCC have slipped to 2027, extending compliance drag on the Middle East and Africa IT services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Managed Security Services Outpace Cloud Growth

In 2025, Cloud and Platform Services captured 31.2% of revenue, reflecting accelerated lift-and-shift projects, yet Managed Security Services is projected to show the fastest expansion at 9.5% CAGR, driven by a 74% jump in regional ransomware incidents. The Middle East and Africa IT services market size for Managed Security is forecast to climb steadily as regulators tighten breach-notification rules. Vendors embed identity, data-loss prevention, and zero-trust modules into bundled offers, anchoring long-term contracts.

Demand also rises for IT Consulting and Implementation engagements that manage legacy refactoring, while IT Outsourcing keeps back-office systems running as firms redirect talent toward digital products. Convergence of cloud and security encourages platform providers to sell integrated observability dashboards, simplifying governance for overstretched technology teams. The Middle East and Africa IT services market share for cloud-native security platforms is expected to increase as clients replace siloed point tools with consolidated subscriptions.

By Enterprise Size: SMEs Embrace SaaS to Bypass Legacy Constraints

Large Enterprises drove 66.4% of 2025 spending due to multi-country ERP modernizations, but Small and Medium Enterprises grow quicker, supported by voucher programs such as Saudi Monsha’at grants worth up to SAR 100,000. Falling per-seat SaaS pricing and Arabic-localized interfaces encourage cloud uptake, turning capex into variable opex.

SMEs avoid technical debt by adopting cloud bookkeeping, ecommerce, and CRM suites from day one. Meanwhile, corporate incumbents confront middleware sprawl, data silos, and mainframe reliance that slow full-stack modernization. As vertical SaaS for halal food, Islamic finance, and Arabic retail matures, the Middle East and Africa IT services industry tailors playbooks for faster time-to-value, deepening wallet share among the region’s 23 million SMEs.

By Industry Vertical: Healthcare Digitization Accelerates Post-Pandemic

Banking and Financial Services remained the largest vertical at 23.8% of 2025 revenue, yet Healthcare and Life-Sciences shows the fastest trajectory with a 9.3% CAGR to 2031. Mandatory electronic health record interoperability and rising telehealth sessions in Dubai to 3.2 million spark integration projects and managed-service deals. The Middle East and Africa IT services market size for healthcare solutions is lifted as insurers demand secure video consultations and AI triage chatbots.

Manufacturing outfits deploy predictive-maintenance analytics, while energy and utilities digitize grid control centers. Government portals migrate to low-code stacks that shorten release cycles. Vertical expertise, compliance fluency, and data-privacy controls become must-have credentials for bidders, creating a premium tier of specialist integrators within the broader Middle East and Africa IT services market.

By Deployment Model: Offshore Hubs in Africa Gain Traction

Onshore Delivery still commands 45.3% of 2025 outlays because public tenders prefer local teams, but Offshore Delivery is growing at 10.0% CAGR as enterprises chase 30-50% labour savings. Egypt, Nigeria, and Kenya shape multilingual talent pools that serve European and Gulf clients in overlapping time zones. The Middle East and Africa IT services market share for hybrid models, where a small onshore squad handles governance and Arabic communication while offshore pods build and test code, is rising.

Tax credits, export incentives, and special economic zones boost the attractiveness of African hubs. Coordination overhead persists, yet better fiber connectivity and standardized DevOps toolchains mitigate friction. Nearshore centers in Jordan and Lebanon offer a cultural bridge, giving clients additional choice along the proximity-cost spectrum.

Geography Analysis

Saudi Arabia and the UAE together generated more than half of 2025 regional revenue as oil-funded sovereign programs financed cloud and AI megaprojects. Saudi’s USD 64 billion tech portfolio bankrolls NEOM’s smart-city backbone and nationwide data-management mandates, feeding a robust pipeline for systems integrators. The UAE attracted USD 9.2 billion of FDI into technology during 2024, with free-zone incubators hosting over 2,400 start-ups that outsource app builds and security audits. Qatar, Kuwait, Oman, and Bahrain follow with digital-government platforms, though smaller populations moderate absolute spending.

Africa registers the fastest growth, with a 9.8% CAGR projected to 2031, helped by donor-funded connectivity rollouts and a booming fintech scene. South Africa targets 500,000 new ICT jobs by 2030 under its skills blueprint, expanding domestic demand and offshore export services. Egypt and Nigeria cultivate export-oriented delivery hubs, while Kenya’s Digital Economy Blueprint mandates all public services online by 2026, driving fresh integration contracts.

Lower base effects, mobile-first adoption, and continental trade liberalization act as tailwinds. Yet energy insecurity, fragmented privacy laws, and scarce senior architects dampen momentum in some markets. The balance of these forces still propels the Middle East and Africa IT services market toward double-digit expansion in several African economies, encouraging providers to hedge GCC exposure with pan-African footprints.

Competitive Landscape

The top ten vendors held roughly 42% of 2025 revenue, signalling moderate concentration in the Middle East and Africa IT services market. Accenture, IBM, and Microsoft capture mega-deals by pairing global delivery reach with hyperscale partnerships. Indian majors such as Tata Consultancy Services, Infosys, Wipro, HCL Technologies, and Tech Mahindra compete aggressively on cost efficiency and reusable accelerators.

Regional champions STC Solutions, and (formerly Etisalat), Ooredoo, Gulf Business Machines, and Raqmiyat leverage Arabic fluency and public-sector access to win sovereign contracts. New entrants like Andela and Globant promote agile pods and cloud-native culture, narrowing the differentiation previously enjoyed by incumbents. Strategic moves center on co-investing with hyperscalers, acquiring niche boutiques for local credibility, and opening AI labs that align with sovereign generative-AI directives.

Compliance credentials such as ISO/IEC 27001 and Saudi Essential Cybersecurity Controls now decide shortlists, pushing laggards to fast-track audits. Pricing discipline remains intact despite talent inflation because managed-service contracts include outcome-based clauses that share savings. Overall, rivalry intensifies yet ample greenfield demand lets most providers grow without deep discount wars.

Middle East and Africa IT Services Industry Leaders

Accenture plc

International Business Machines Corporation (IBM)

Oracle Corporation

Microsoft Corporation

Amazon Web Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Microsoft pledged USD 2.1 billion to broaden Azure zones in Saudi Arabia and Egypt, targeting sovereign-cloud projects.

- January 2026: Accenture opened a generative-AI Center of Excellence in Dubai, hiring 200 specialists.

- December 2026: Tata Consultancy Services won a USD 450 million deal to modernize Saudi tax systems.

- November 2025: AWS added a second Bahrain availability zone after investing USD 800 million.

Middle East and Africa IT Services Market Report Scope

The Middle East and Africa IT Services Market Report is Segmented by Service Type (IT Consulting and Implementation, IT Outsourcing, Business Process Outsourcing, Managed Security Services, Cloud and Platform Services), Enterprise Size (Small and Medium Enterprises, Large Enterprises), Industry Vertical (BFSI, Manufacturing, Government and Public Sector, Healthcare and Life-Sciences, Retail and Consumer Goods, Telecom and Media, Logistics and Transport, Energy and Utilities, Rest of Industry Verticals), Deployment Model (Onshore Delivery, Nearshore Delivery, Offshore Delivery), and Geography (Middle East: Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain, Rest of Middle East; Africa: South Africa, Egypt, Nigeria, Kenya, Morocco, Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

By Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

By Industry Vertical

| Banking, Financial Services and Insurance (BFSI) |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Rest of Industry Verticals |

By Deployment Model

| Onshore Delivery |

| Nearshore Delivery |

| Offshore Delivery |

By Geography

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Morocco | |

| Rest of Africa |

| By Service Type | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| By Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Industry Vertical | Banking, Financial Services and Insurance (BFSI) | |

| Manufacturing | ||

| Government and Public Sector | ||

| Healthcare and Life-Sciences | ||

| Retail and Consumer Goods | ||

| Telecom and Media | ||

| Logistics and Transport | ||

| Energy and Utilities | ||

| Rest of Industry Verticals | ||

| By Deployment Model | Onshore Delivery | |

| Nearshore Delivery | ||

| Offshore Delivery | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Bahrain | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Morocco | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Middle East and Africa IT services market in 2026?

The market is valued at USD 252.8 billion in 2026 with an 8.9% CAGR forecast to 2031.

Which service type grows fastest to 2031?

Managed Security Services leads with a 9.5% CAGR as ransomware threats and compliance rules intensify.

Why are SMEs accelerating technology spending?

Voucher programs and falling SaaS prices let SMEs adopt cloud platforms without upfront capex, fueling a 9.8% CAGR.

Which geography shows the highest growth rate?

Africa records a 9.8% CAGR to 2031 thanks to fintech expansion and donor-funded digital infrastructure.

What restrains market momentum most?

Shortage of bilingual cloud-native talent adds cost and delays, subtracting 0.9% from the CAGR outlook.

How competitive is the vendor landscape?

The top ten players hold roughly 42% share, indicating moderate concentration and room for new entrants.

Page last updated on: