Europe HCM Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

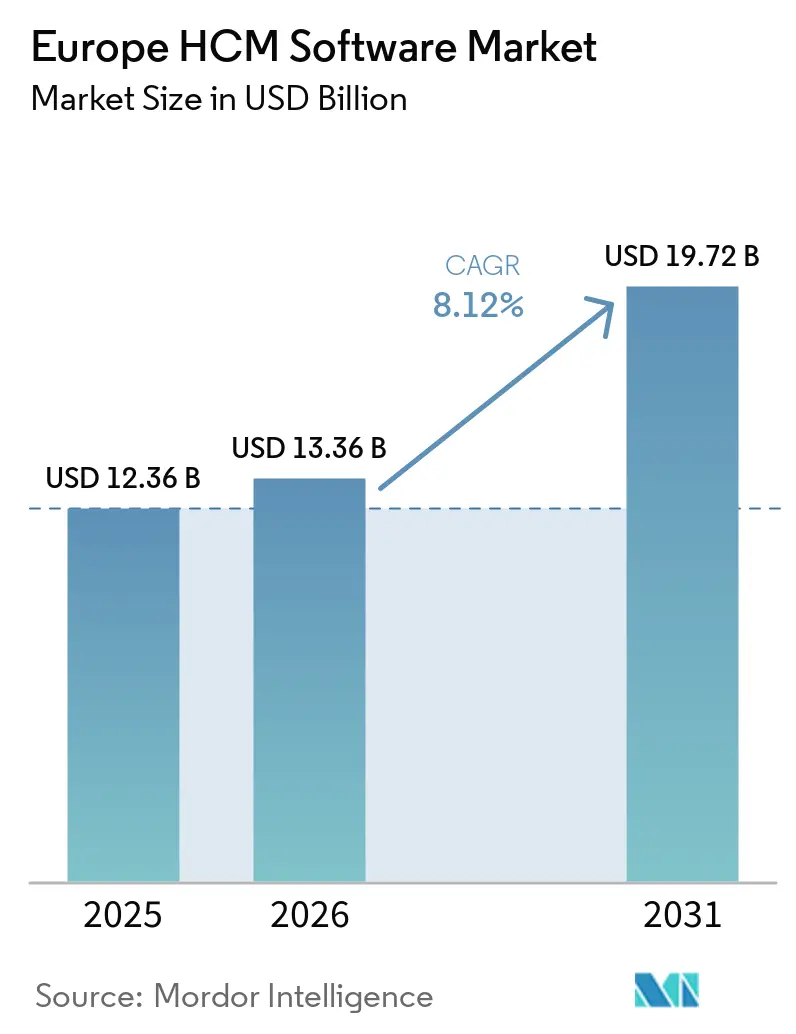

| Base Year Market Size (2025) | USD 12.36 Billion |

| Market Size (2026) | USD 13.36 Billion |

| Market Size (2031) | USD 19.72 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

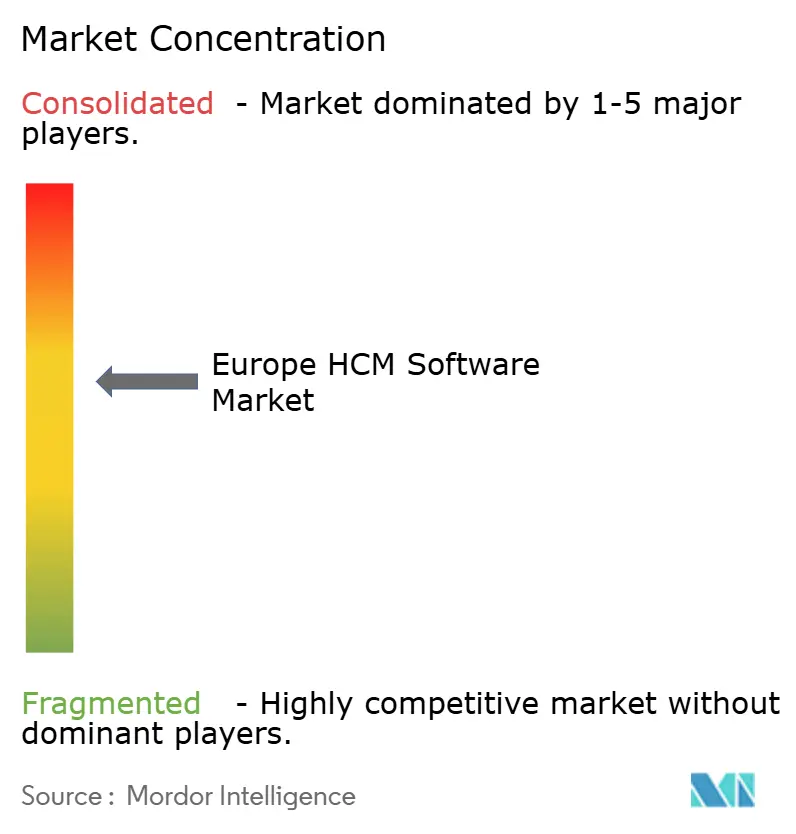

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe HCM Software Market Analysis by Mordor Intelligence

The Europe HCM Software Market size reached USD 12.36 billion in 2025 and is expected to reach USD 13.36 billion in 2026 and USD 19.72 billion by 2031, growing at a CAGR of 8.12% from 2026 to 2031. Adoption is shifting from headcount growth to a focus on unified compliance, analytics, and employee experience capabilities. Mandatory CSRD and Pay Transparency rules are pushing firms to retire spreadsheets in favor of auditable, cloud-ready platforms. Demand for hybrid deployment is rising as regulated industries juggle GDPR data-residency rules with scalable analytics, while services revenue is growing faster than licenses because organizations require deep change-management support. Competitive intensity remains moderate, with global vendors dominating large enterprises and regional specialists gaining ground in the mid-market.

Key Report Takeaways

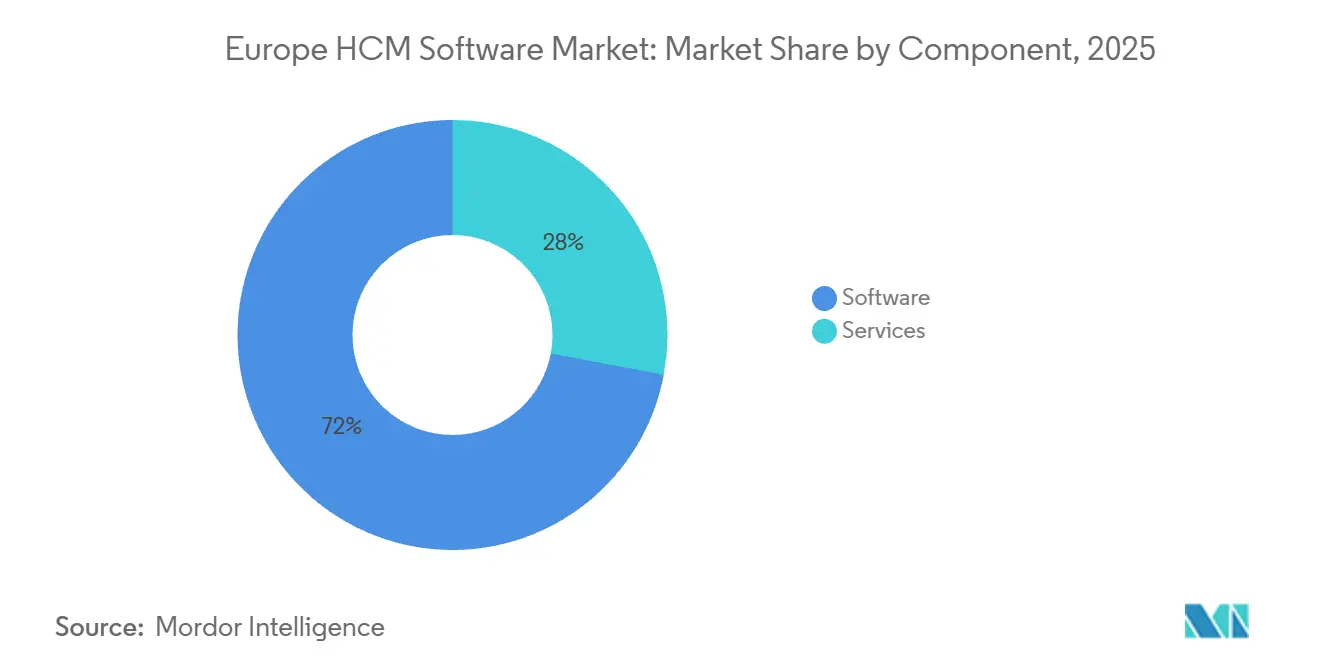

- By component, software led with 72.04% of the Europe HCM Software market share in 2025, whereas services are advancing at a 9.21% CAGR through 2031.

- By deployment mode, cloud held 67.21% share of the Europe HCM Software market size in 2025, while hybrid architectures record the fastest projected CAGR at 9.74% for 2026-2031.

- By organization size, large enterprises captured 61.12% spending in 2025, yet SMEs are forecast to expand at a 9.32% CAGR over 2026-2031.

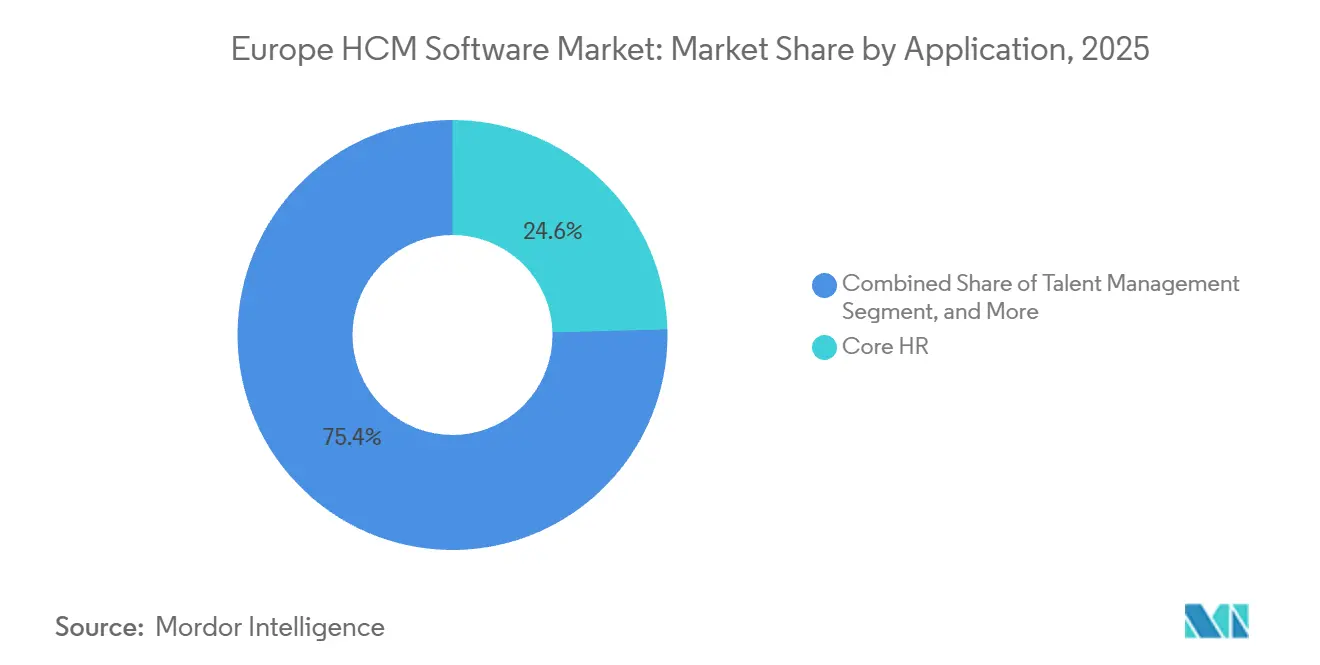

- By application, core HR accounted for 24.58% share in 2025, while talent management is projected to post the highest CAGR of 9.88% through 2031.

- By end-user industry, BFSI represented 21.63% revenue in 2025, whereas healthcare and lifesciences are growing at a 9.51% CAGR to 2031.

- By geography, the United Kingdom commanded 24.11% revenue share in 2025, but Germany is on track for the fastest CAGR of 8.94% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe HCM Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Migration to Cloud-based HCM Platforms | +2.1% | UK, Nordics, Germany | Short term (≤ 2 years) |

| Growing Need for Workforce Analytics and AI-driven Insights | +1.8% | UK, Germany, France, Nordics, Southern Europe emerging | Medium term (2-4 years) |

| Stringent and Evolving EU Labor Compliance Requirements | +1.5% | EU-27, UK, Switzerland; BFSI, Healthcare, Manufacturing | Short term (≤ 2 years) |

| Rise of Digital Employee Experience Platforms Integrating Well-being and DEI Metrics | +1.2% | UK, Germany, Nordics, France | Medium term (2-4 years) |

| Expansion of ESG-linked Human Capital Reporting Mandates | +1.0% | EU-27, UK; listed and PE-backed firms | Long term (≥ 4 years) |

| Adoption of Privacy-Preserving HR Tech to Navigate GDPR Constraints | +0.6% | EU-27, UK, Switzerland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Migration to Cloud-Based HCM Platforms

Cloud held 67.21% share of the Europe HCM Software market in 2025, but the driver extends beyond cost efficiency to regulatory agility that batch-oriented on-premises systems cannot match. Workday responded by launching an EU Sovereign Cloud in Frankfurt and Amsterdam in 2025, staffed exclusively by European-resident administrators, letting customers leverage machine-learning models while satisfying GDPR data-residency rules.[1]Workday, “Workday Launches EU Sovereign Cloud,” blog.workday.com SAP reported that 72% of its European base is already on hybrid deployments in which payroll remains on ERP but talent modules run on SuccessFactors, demonstrating a phased modernization path. As more directives require near-real-time disclosures, cloud penetration is set to accelerate further.

Growing Need for Workforce Analytics and AI-Driven Insights

Eurostat showed in 2025 that only 56% of the EU population held basic digital skills, forcing companies to switch from reactive hiring to predictive workforce planning.[2]Eurostat, “Digital Economy and Society Statistics,” ec.europa.eu Workday’s AI Center in Dublin uses anonymized data from 10 000 customers to reach 82% accuracy in predicting 90-day attrition risk. Oracle embedded skills-ontology graphs that helped Danske Bank cut time-to-fill for data-engineering roles by 40%. Yet SD Worx found that only 22% of firms under 250 employees use predictive analytics, indicating white space for SME-focused vendors. Vendors are adding model-confidence scores to comply with EDPS guidance on human oversight.

Stringent and Evolving EU Labor Compliance Requirements

The EU Pay Transparency Directive obliges firms with 100 or more workers to publish gender-pay-gap data by April 2026, with fines up to 6% of turnover for non-compliance. ADP reported in 2025 that 64% of European HR leaders doubted they could meet the deadline because of fragmented payroll systems. Simultaneously, the CSRD forces about 50 000 companies to disclose workforce metrics, elevating HCM software from administrative to compliance infrastructure. Vendors have embedded automated pay-equity analysis, audit trails, and disclosure templates that legacy systems lack. Ongoing regulatory expansion keeps this driver in the spotlight for at least the next two years.

Rise of Digital Employee Experience Platforms Integrating Well-Being and DEI Metrics

Post-pandemic burnout has made sentiment and wellness tracking central to retention strategies. Evermood’s mental-health platform tripled its client base in 2025 as firms adopted pulse surveys and mood-tracking tools to flag high-stress teams. LumApps paid more than USD 1 billion for Beekeeper in July 2025, creating an employee-experience suite that merges communications with wellness modules. Diversity dashboards that expose gender, ethnicity, and disability ratios satisfy both CSRD disclosures and investor ESG questionnaires. Younger staff favor consumer-grade interfaces; Spotify’s Disco exemplifies systems that prioritize transparency over administrative control. As hybrid work persists, integrated well-being and DEI metrics will remain a medium-term growth catalyst.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Security and Privacy Concerns under GDPR | -1.4% | EU-27, UK, Switzerland; cross-border deployments heightened | Short term (≤ 2 years) |

| Integration Complexity with Legacy ERP and Payroll Systems | -1.1% | Germany, France, Italy; manufacturing and public sector | Medium term (2-4 years) |

| Shortage of HR Tech Implementation Talent | -0.8% | UK, Germany, France, Nordics; acute in SME segment | Medium term (2-4 years) |

| Inflation-Driven IT Budget Compression in Public Sector | -0.5% | UK, Southern Europe; local government and healthcare | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Security and Privacy Concerns Under GDPR

The Schrems II ruling continues to complicate transatlantic data flows, forcing vendors to adopt standard contractual clauses plus encryption and pseudonymization. Workday’s EU Sovereign Cloud keeps processing inside EU borders, but DavidsonMorris reported in 2025 that 58% of UK employers had already faced GDPR audits, with 12% receiving formal warnings for poor data-retention practices. Privacy-preserving analytics like differential privacy and federated learning are emerging, yet they require specialized skills that many mid-market integrators lack, introducing cost and complexity.

Integration Complexity With Legacy ERP and Payroll Systems

Decades-old, heavily customized SAP and Oracle ERP installations anchor payroll and core HR across Europe. ADP estimated in 2025 that integration consumes 40-60% of HCM project budgets. Middleware such as Boomi and MuleSoft alleviates some pain but introduces latency and single points of failure. SD Worx’s new Germany payroll module underscores how localization remains the thorniest issue, especially where church taxes, social-insurance tiers, and collective-bargaining rules vary by region. When the UK raised employer National Insurance to 15% in April 2025, on-premises users needed manual patches, while cloud vendors pushed automatic updates.[3]The Access Group, “Impact of National Insurance Increase on UK Employers,” theaccessgroup.com The resulting budget overruns and timeline slips dampen near-term adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Surge as Implementation Complexity Deepens

Services revenue is forecast to expand at a 9.21% CAGR between 2026 and 2031, even though software captured 72.04% of the Europe HCM Software market share in 2025. Implementation projects increasingly span data migration, change management, and ERP integration, so enterprises are shifting budget from licenses to consulting. This shortage is spawning regional specialists and managed-services arrangements in which outsourcers administer day-to-day configuration.

Software growth remains steady, but margins are tightening as subscription models replace perpetual sales and as composable architectures fragment demand. Vendors that package low-code tools and pretrained compliance templates lower the cost of ownership and protect share. The European HCM Software market rewards players that couple software with advisory know-how, so service lines are expected to keep outpacing pure license revenue through 2031.

By Deployment Mode: Hybrid Gains as Compliance and Analytics Collide

Hybrid deployment is forecast to grow at 9.74% CAGR from 2026 to 2031, the fastest rate among deployment modes, as organizations balance GDPR data-residency mandates with the scalability and innovation velocity of public-cloud analytics. Cloud held 67.21% market share in 2025, driven by SaaS vendors' ability to deliver continuous feature updates and pre-built compliance templates, yet pure on-premises deployments are declining as vendors such as SAP and Oracle phase out support for legacy versions. Regulated industries keep payroll on-premises for data-residency reasons while moving talent, learning, and analytics to SaaS.

Workday’s EU Sovereign Cloud and SAP’s hybrid SuccessFactors deployments demonstrate a middle path that lets firms preserve custom payroll logic but tap elastic analytics. On-premises deployments persist in public agencies that still favor capital expenditure, although the total cost of ownership remains 30% to 50% higher over five years. The hybrid wave will accelerate vendor consolidation because legacy on-premises specialists lack the capital to re-platform.

By Organization Size: SMEs Embrace Vertical SaaS as Compliance Costs Mount

Large enterprises accounted for 61.12% of spending in 2025, but small and medium enterprises are forecast to grow at a 9.32% CAGR through 2031, the fastest growth in the Europe HCM Software market. The EU Pay Transparency Directive's 100-employee threshold, enforceable from April 2026, is driving SME adoption as firms recognize that manual spreadsheet-based pay-gap analysis is neither scalable nor auditable

Vendors such as Personio, HiBob, and Factorial price below USD 10 per employee per month and ship ready-made labor-law templates, compressing implementation from months to weeks. OECD data show only 22% of EU SMEs using AI-powered HR tools in 2025, compared with 55% of large companies, so the runway for penetration remains long.[4]OECD, “SME AI Adoption in Europe,” oecd.org As compliance overhead rises, vertical SaaS packages that hide complexity will continue to siphon share from enterprise suites.

By Application: Talent Management Accelerates as Skills Shortages Intensify

Talent management is forecast to expand at 9.88% CAGR from 2026 to 2031, the fastest growth among applications, as enterprises shift from reactive recruiting to proactive skills development and internal mobility. Core HR, which encompasses employee records, organizational charts, and basic workflows, held 24.58% market share in 2025, yet is being commoditized as vendors bundle these features into entry-level tiers. Eurostat notes only 56% of Europeans possess basic digital skills, so firms rely on AI-driven ontologies to map gaps and promote internal mobility.

SAP’s 2025 purchase of SmartRecruiters and Workday’s USD 1.1 billion Sana deal signal a race to embed learning and recruiting in one flow. Hospitals and manufacturers integrate fatigue algorithms and certification trackers that sit between workforce management and learning, blurring boundaries but boosting attach rates. As CSRD forces disclosure of average training hours, learning modules are shifting from discretionary spend to board-level KPI.

By End-User Industry: Healthcare Leads Growth as Scheduling Complexity Escalates

Healthcare and lifesciences spending is forecast to climb at a 9.51% CAGR, outpacing all other verticals, as nurse-scheduling and continuing-education tracking become mission-critical. Florence, a UK-based healthcare workforce platform, reported in 2025 that its customer base included 40% of NHS trusts, with clients using the platform to match agency nurses to open shifts and track compliance with professional-development requirements

BFSI, with a 21.63% 2025 share, has matured, and growth is slowing as banks rationalize post-pandemic headcounts. Manufacturing seeks skills-certification engines, retail demands demand-based rostering, and the public sector remains cost-constrained. Vendors that localize healthcare rosters, fatigue rules, and mandatory upskilling frameworks are set to capture the most incremental revenue within the Europe HCM Software industry.

Geography Analysis

The United Kingdom contributed the largest slice of the Europe HCM Software market size at 24.11% in 2025, supported by London-based multinationals and broad SaaS maturity. Local surveys show 55% of UK employers already use AI-powered HR tools, well above the 38% EU average, turning the nation into a living laboratory for predictive attrition and skills-inference pilots. Budget pressure inside the NHS and local councils tempers spending but simultaneously raises the value proposition of workforce analytics modules that tie labor expense to clinical and citizen outcomes.

Germany is on track for an 8.94% CAGR, the fastest among major economies, because Mittelstand firms must modernize payroll to handle church taxes, social-insurance tiers, and industry bargaining agreements. SD Worx’s localized payroll engine embodies the demand for pre-built compliance objects that smaller integrators cannot replicate. Cross-border M&A, exemplified by Timegrip’s buyout of Software4You, is creating German-speaking platforms with pan-European reach.

France, Italy, Spain, and the Nordics round out the high-growth cluster. French vendors leverage 35-hour workweek calculations and profit-sharing rules to win local deals, while Nordic firms export pay-equity analytics to the rest of the continent. In Eastern Europe, language and regulatory complexity keep domestic providers relevant, but private-equity owners are knitting them into regional groups that share R&D and hosting infrastructure.

Competitive Landscape

The Europe HCM Software market is moderately concentrated. SAP SuccessFactors, Workday, and Oracle Cloud collectively control about 60% of enterprise accounts with 5 000+ employees, but mid-market share is spreading to Personio, HiBob, SD Worx, and Factorial. A 2025 survey of 1,000 HR executives ranked Workday highest in usability, Oracle in ERP integration, and SAP in breadth of global payroll coverage.

Strategic activity centers on AI and sovereign hosting. Workday opened a EUR 175 million (USD 202.5 million) AI hub in Dublin to build language models spanning 24 European languages, and its predictive attrition engine now runs on a fully EU-resident cloud stack. SAP bought SmartRecruiters to plug a recruiting gap, while Oracle promotes confidential-computing modules that encrypt data in use, aligning with GDPR Article 25. Regional players answer by integrating vertical features such as nurse rostering, retail forecasting, and manufacturing skills passports.

Limited integration capacity is a gating factor, with 68% of enterprises lacking skilled implementation partners in 2025, raising project backlogs and giving vendors with turnkey accelerators an advantage. Private-equity fueled roll-ups, including Hg’s larger stake in P&I and Thoma Bravo’s USD 12.3 billion buyout of Dayforce, signal that financial sponsors expect continued double-digit growth once platform modernization bottlenecks ease.

Europe HCM Software Industry Leaders

SAP SE

Workday, Inc.

Oracle Corporation

Automatic Data Processing, Inc.

UKG Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Thoma Bravo completed its acquisition of Dayforce for USD 12.3 billion, aiming to speed European expansion with localized payroll modules.

- November 2025: Integral bought Cleverlohn and raised EUR 6.3 million (USD 6.8 million) to target SME payroll automation.

- October 2025: SD Worx launched a Germany-specific payroll engine with templates for social insurance and church taxes.

- September 2025: Visma acquired Lönelys to embed pay-equity analytics across its Nordic suite.

Europe HCM Software Market Report Scope

The Europe HCM Software Market refers to the market for software solutions and associated services that enable organizations across European countries to manage and optimize human resources functions throughout the employee lifecycle. It includes platforms covering core HR, payroll, talent management, workforce management, and learning and development, along with related services such as implementation, integration, consulting, and support, delivered through cloud, on-premises, and hybrid deployment models.

The Europe HCM Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, Payroll Management, and Learning and Development), End-User Industry (IT and Telecommunications, BFSI, Industrial Manufacturing, Healthcare and Lifesciences, Retail and E-commerce, Government and Public Sector, and Other End-User Industries), and Geography (United Kingdom, Germany, France, Italy, Spain, Nordics, Russia, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Core HR |

| Talent Management |

| Workforce Management |

| Payroll Management |

| Learning and Development |

| IT and Telecommunications |

| BFSI |

| Industrial Manufacturing |

| Healthcare and Lifesciences |

| Retail and E-commerce |

| Government and Public Sector |

| Other End-User Industries |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Nordics |

| Russia |

| Rest of Europe |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Core HR |

| Talent Management | |

| Workforce Management | |

| Payroll Management | |

| Learning and Development | |

| By End-User Industry | IT and Telecommunications |

| BFSI | |

| Industrial Manufacturing | |

| Healthcare and Lifesciences | |

| Retail and E-commerce | |

| Government and Public Sector | |

| Other End-User Industries | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe HCM Software market in 2031?

The market is forecast to reach USD 19.72 billion by 2031, advancing at an 8.12% CAGR from 2026, according to Mordor Intelligence.

Which deployment model will grow fastest through 2031?

Hybrid deployment is expected to post the quickest 9.74% CAGR as firms blend on-premises payroll with cloud analytics, based on Mordor Intelligence data.

Which industry will add the most new spending?

Healthcare and lifesciences are set to deliver the highest 9.51% CAGR, driven by complex nurse scheduling and mandatory training needs, per Mordor Intelligence findings.

Why are services outpacing software revenue growth?

Implementation complexity, change management, and managed-services outsourcing push services to a 9.21% CAGR, while software shifts toward subscription pricing.

What is the main compliance driver for software upgrades in 2026?

The EU Pay Transparency Directive requires organizations with 100 or more employees to publish gender-pay-gap data by April 2026, prompting adoption of compliant HCM modules.

Page last updated on: