Microinsurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

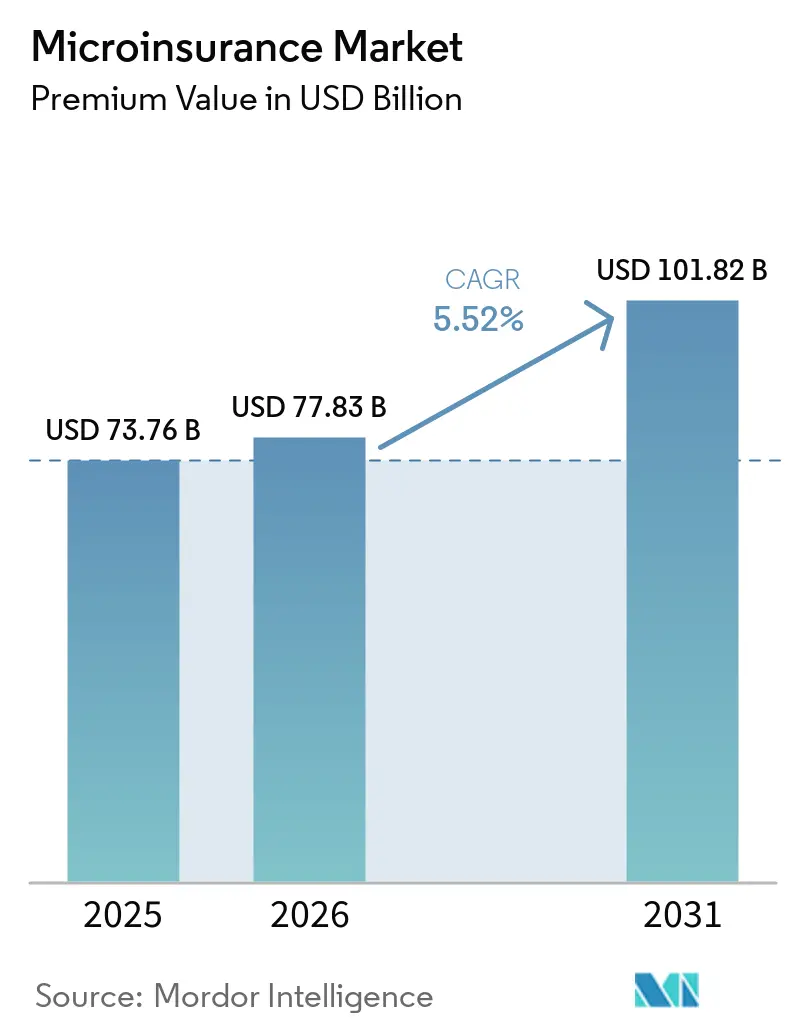

| Market Size (2026) | USD 77.83 Billion |

| Market Size (2031) | USD 101.82 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

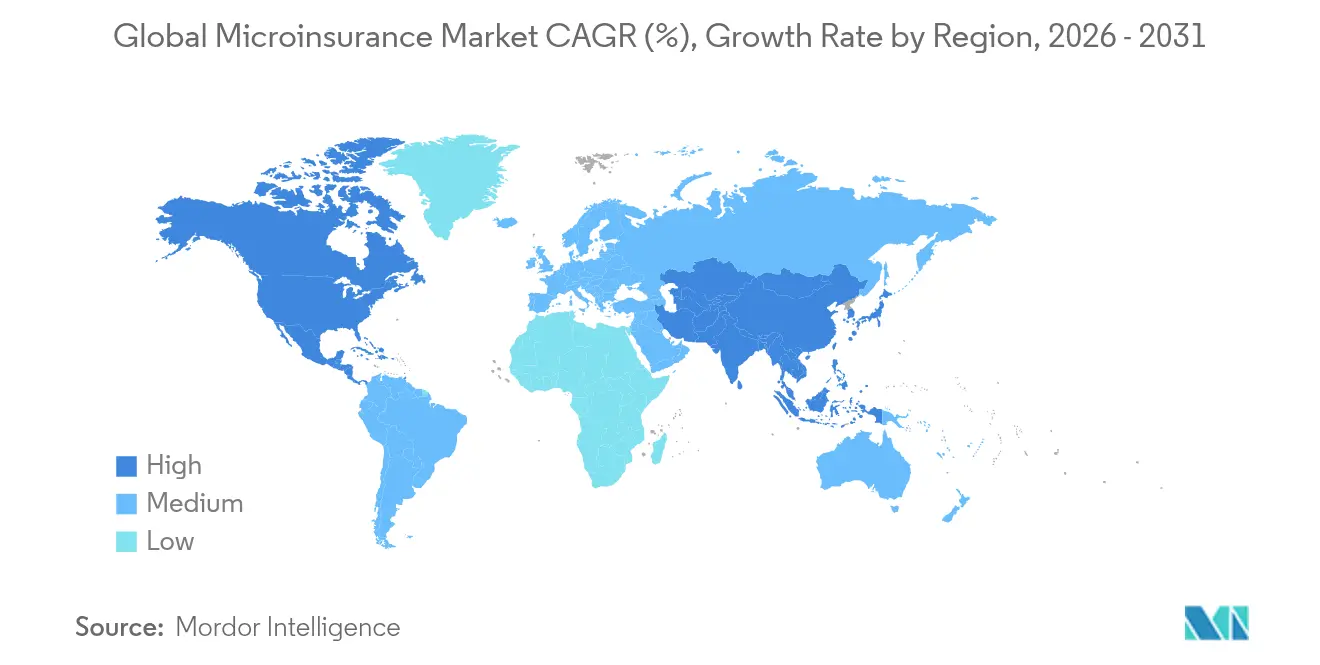

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

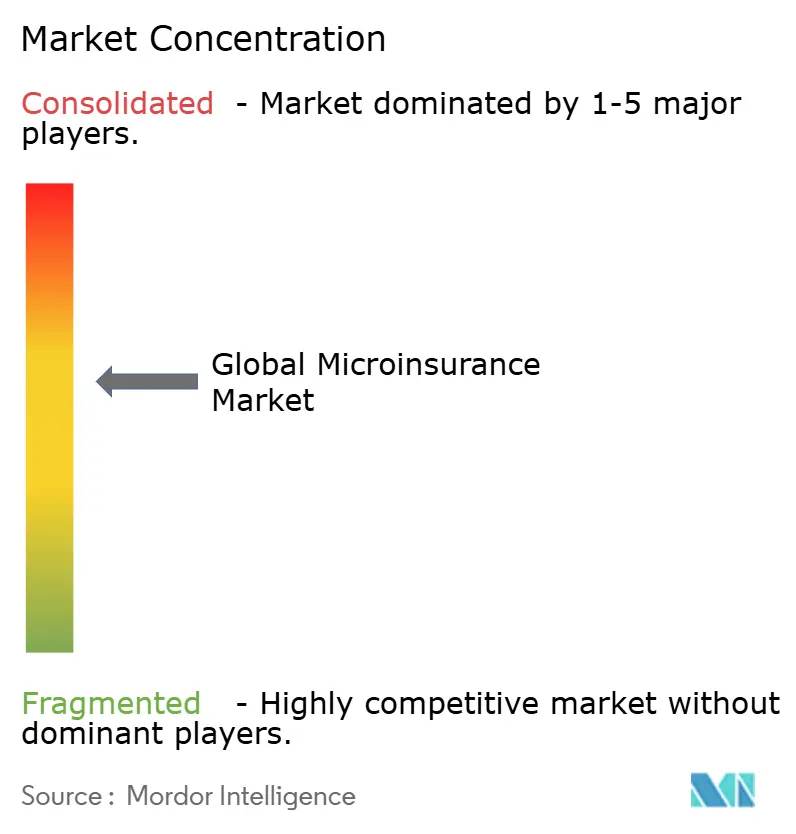

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microinsurance Market Analysis by Mordor Intelligence

The Microinsurance Market size in terms of premium value is projected to expand from USD 73.76 billion in 2025 and USD 77.83 billion in 2026 to USD 101.82 billion by 2031, registering a CAGR of 5.52% between 2026 to 2031.

Expansion is powered by the convergence of mobile money penetration, regulatory mandates for inclusive finance, and rapid insurtech adoption that lowers distribution costs. Digital platforms already control 35.4% of premium flows and are growing faster than agency models, reflecting the appeal of seamless, low-touch onboarding for first-time policyholders. Commercial carriers keep leveraging capital strength and compliance expertise to expand affordable cover, while partner-agent alliances deliver local reach in hard-to-access communities. Asia-Pacific now contributes the highest incremental premium growth in the microinsurance market, yet protection gaps remain wide in every region, sustaining long-run demand for parametric, embedded, and AI-underwritten solutions.

Key Report Takeaways

- By product type, life insurance held 36.22% revenue share in 2025; health & hospital cash is forecast to rise at a 5.49% CAGR to 2031 in the microinsurance market.

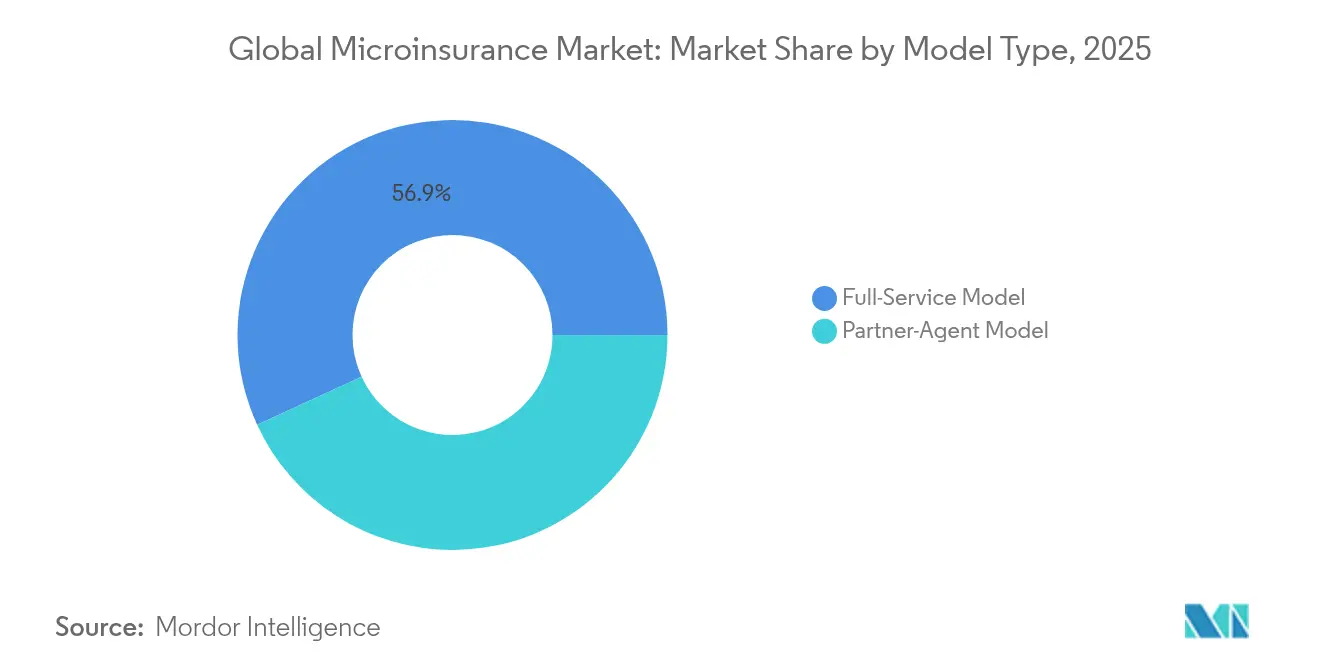

- By model type, the partner-agent model led with 43.15% of the global microinsurance market share in 2025 while posting the fastest 7.92% CAGR through 2031.

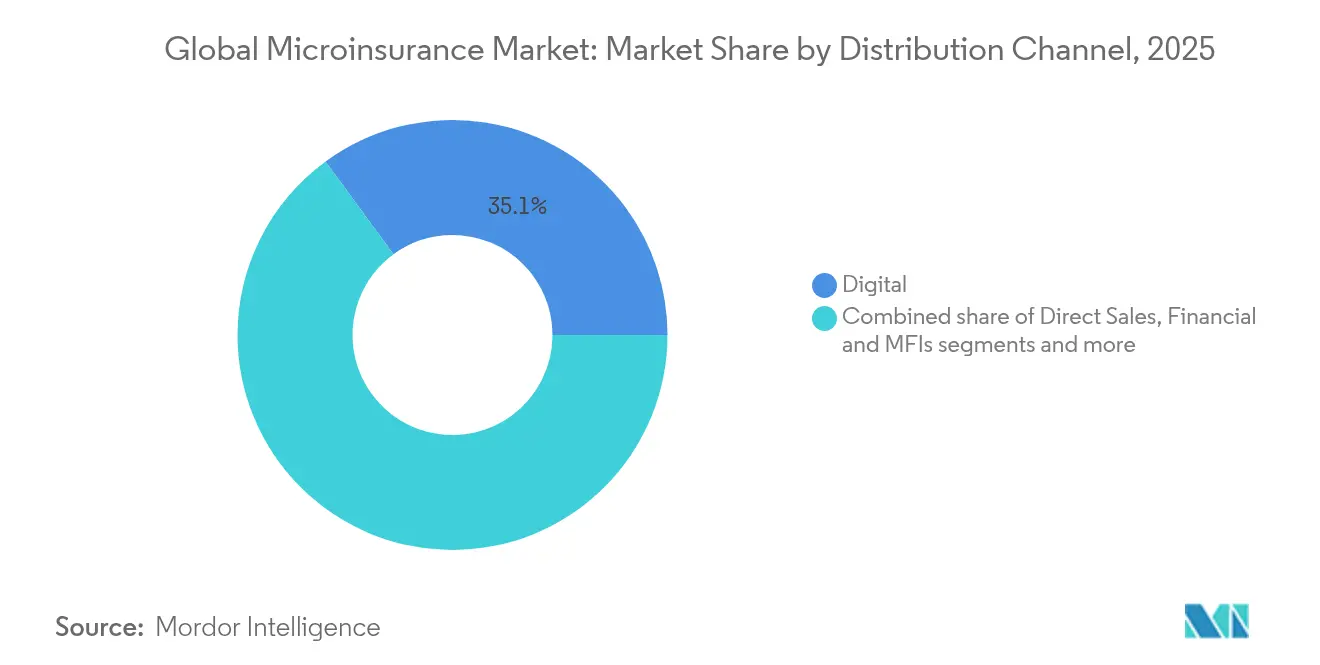

- By distribution channel, digital platforms captured a 35.05% share of the global microinsurance market size in 2025 and are set to expand at a 6.23% CAGR between 2026 and 2031.

- By provider, commercial insurers commanded a 61.72% share of the global microinsurance market size in 2025 and are advancing at a 6.88% CAGR through 2031.

- By geography, North America led with 26.12% global microinsurance market share in 2025, while Asia-Pacific is the fastest-growing region at a 5.97% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microinsurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Access to financial services via mobile money expansion | +1.8% | Sub-Saharan Africa, Southeast Asia | Medium term (2–4 years) |

| Government mandates for inclusive insurance | +1.2% | Asia-Pacific, Latin America | Long term (≥ 4 years) |

| Rise of digital platforms & insurtech partnerships | +1.5% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Parametric micro-insurance for climate risk | +0.9% | Climate-vulnerable regions worldwide | Medium term (2–4 years) |

| Embedded insurance in e-commerce & ride-hailing apps | +1.1% | Urban markets globally | Short term (≤ 2 years) |

| Satellite & remote-sensing data enabling micro crop insurance | +0.7% | Agricultural zones in developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Access to Financial Services via Mobile Money Expansion

Mobile money ecosystems are unlocking first-time cover for low-income users by collapsing payment, identity, and policy servicing into a single handset journey. Ethiopia processed USD 82 billion of mobile transactions in 2024, a 50% jump that widened the addressable base for global microinsurance market growth. Zambia shows similar traction, with 58.4% of adults active on mobile wallets, giving insurers a direct, low-cost channel. Chubb’s Grab Ride Cover sells trip delay protection at check-out, illustrating how contextual offerings convert digital traffic into premium income[1]Chubb, “Grab Ride Cover Product Sheet,” chubb.com. In markets where traditional penetration sits below 5%, handset-first delivery is cutting acquisition expenses by more than 60%, strengthening unit economics for mass-market products.

Government Mandates for Inclusive Insurance

Multiple regulators now frame insurance as an essential service. India’s Insurance Regulatory and Development Authority (IRDAI) launched the “insurance for all by 2047” roadmap, and its Bima Sugam digital marketplace went live in 2024 to offer fee-free policy purchase and servicing[2]IRDAI, “Draft Regulations on Bima Sugam,” irdai.gov.in. Brazil's SUSEP introduced Open Insurance data-sharing rules, enabling customers to transfer their records seamlessly. This initiative is expected to foster significant product innovation by encouraging insurers to develop tailored offerings based on shared data. Meanwhile, Indonesia's OJK Regulation No. 8 of 2024 expedites product approvals to just five days, significantly reducing the time to market for new insurance products. By merging enforcement with robust infrastructure, these regulations aim to ensure consistent premium inflows, enhance operational efficiency, and reduce compliance challenges for the development of innovative designs.

Rise of Digital Platforms & Insurtech Partnerships

Global embedded premium volume is also expanding rapidly with a double-digit growth rate. Point-of-sale insurance is scaling within everyday apps.[3]Smartpay, “Embedded Insurance Announcement,” smartpay.co.jp. Smartpay partners with Chubb to integrate purchase protection into Japan's BNPL checkout, offering consumers added security during their transactions. Meanwhile, Allianz Partners collaborates with Cosmo Connected to embed personal accident coverage within IoT helmets, enhancing safety for users in real time. In Latin America, Prudential teams up with 123Seguro, targeting the under-insured population by leveraging ride-hailing and e-commerce data to provide swift and accurate insurance quotations. These strategic alliances cut distribution costs, boost conversion rates, and provide insurers with a steady influx of behavioral data, enabling them to refine and optimize their underwriting processes for better risk assessment and customer satisfaction.

Parametric Micro-insurance for Climate Risk

Parametric triggers are moving loss adjustments from traditional surveys to satellite readings, which speeds up payouts and boosts customer trust by ensuring transparency and efficiency. As the global pool of parametric premiums expands, it is creating significant opportunities for the growth of the global microinsurance market, particularly in regions vulnerable to climate risks. In the Philippines, CLIMBS Cooperative has significantly expanded its reach from 14 to 126 credit unions, now protecting 85,000 farmers through automatic weather-indexed settlements, which provide timely and reliable financial support during adverse weather conditions. Demonstrating the model's adaptability, Swiss Re has begun covering the non-delivery of carbon credits, showcasing the potential of parametric insurance in addressing emerging risks and sustainability challenges. Furthermore, AI-driven hazard analytics are reducing basis risk, enabling innovators in the global microinsurance market to accurately price agricultural risks that were previously deemed uninsurable, thereby enhancing the accessibility and affordability of insurance solutions for underserved communities.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy & security concerns | -0.8% | EU, North America | Short term (≤ 2 years) |

| Limited actuarial data for pricing | -1.1% | Sub-Saharan Africa, Southeast Asia | Medium term (2–4 years) |

| Low claims-settlement trust due to fraudulent agents | -0.9% | Markets with weak oversight | Medium term (2–4 years) |

| Regulatory arbitrage limiting cross-border product scaling | -0.6% | Multinational offerings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy & Security Concerns

New York's Department of Financial Services mandates board-approved AI governance programs to ensure accountability and transparency in the use of artificial intelligence. Meanwhile, Colorado enforces algorithmic bias testing, which aims to identify and mitigate discriminatory outcomes, thereby increasing compliance costs for insurers leveraging alternative data. The EU AI Act introduces a tiered risk framework, categorizing AI systems based on their potential risks, with penalties for non-compliance reaching up to 6% of global turnover. Insurers relying on handset metadata are compelled to invest in encryption, consent management, and audit tools to safeguard data integrity and privacy, further challenging the already tight economics of micro-insurance. Providers unable to demonstrate algorithmic fairness or compliance with these regulations risk facing significant market-access restrictions, potentially impacting their operational viability.

Limited Actuarial Data for Pricing

Insurers in numerous emerging economies grapple with a dearth of multi-year datasets on morbidity, mortality, and hazards, which are critical for accurate risk assessment and product pricing. In Africa, a staggering 97% of the population remains uninsured, creating an information void that significantly skews loss ratios and hinders the development of tailored insurance products. Rural health pilots in India demonstrated a drop in uptake from 79% at no premium to 60% when a price was introduced, highlighting potential adverse selection in the absence of detailed and granular data. To bridge these gaps, carriers are increasingly leveraging alternative data sources such as satellite imagery, call-detail records, and mobile wallet histories to enhance their understanding of risk profiles. However, the frameworks for validating these data sources and integrating them into actuarial models remain in their infancy, posing challenges to their widespread adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Model Type: Partner-Agent Model Drives Market Expansion

The partner-agent architecture accounted for 43.15% of the 2025 premium, the largest slice of the global microinsurance market, and it is forecast to expand at an 7.92% CAGR through 2031. This dominance reflects how local credit unions, cooperatives, and postal networks act as last-mile enablers in communities where core banking penetration is still below 30% and where consumer trust rests with familiar institutions. Insurers provide the balance-sheet capacity and product design, while agents supply on-the-ground enrollment and servicing capability, producing a blended cost of acquisition that sits 20%-40% below pure agency models. Digital tablets and USSD flows now allow agents to issue policies in under five minutes, slashing paperwork and keeping compliance records audit-ready. These efficiencies are critical because the typical micro-ticket policy generates less than USD 5 of annual premium.

The partner-agent model also supports flexible cash-collection cycles that match informal income patterns. AXA’s essential, for example, bundles accident, life, and hospital cash into a single cover and lets policyholders pay weekly through mobile wallets, a feature that lifted renewal rates by 14 percentage points in 2024. VSure Tech’s SME platform in Malaysia pushes the approach further by embedding liability insurance inside point-of-sale software used by micro-retailers, reaching 60,000 firms without a dedicated sales force. Regulators endorse the arrangement because partner entities typically maintain robust KYC files, reducing money-laundering risk. Due to these advantages, the model is projected to keep widening its global microinsurance market share even as fully digital challengers scale.

By Product Type: Health Insurance Emerges as Growth Leader

Life products, including credit-life, term, and funeral cover, still hold 36.22% of 2025 premium, yet health and hospital cash plans are the global microinsurance market’s fastest-growing line at a 5.49% CAGR to 2031. Post-pandemic awareness, rising out-of-pocket medical costs, and government subsidy programs steer households toward even minimal inpatient cash benefits. India’s INR 48,000 crore (USD 5.7 billion) allocation to low-ticket health schemes created a pipeline of bundled policies that reimburse hospital stays at USD 10–15 per day, bridging liquidity gaps for informal workers. Africa shows similar momentum as mPharma’s pharmacy-led subscription covers 14 chronic diseases and lets members pay monthly fees equivalent to two cups of coffee.

Growth also owes much to product modularity. Carriers can append dental, maternity, or telemedicine riders without redesigning the core policy wording, a strategy that helps keep regulatory filing times short. Index-based crop and livestock lines use satellite weather data to trigger payouts, enabling global microinsurance market size expansion in agricultural regions where traditional loss adjustment is infeasible. Accident and disability riders are gaining traction among ride-hailing and delivery workers who seek income-replacement benefits priced at less than 1% of their monthly earnings. As more governments mandate digital health records, underwriters will gain granular claims data that can further refine pricing and reduce loss ratios.

By Distribution Channel: Digital Platforms Reshape Access

Digital channels generated 35.05% global premium of 2025 in the microinsurance market and are advancing at a 6.23% CAGR, outpacing branches, MFIs, and agency lines. Smartphone penetration above 70% in urban Asia allows insurers to deliver quote-to-bind journeys in under three clicks, pushing conversion rates beyond 30% for embedded checkout offers. Bima Sugam in India demonstrates the regulator-backed platform approach; it serves as a neutral marketplace that houses every policy bought by a user, cutting policy-servicing times from days to minutes and eliminating duplicate KYC. In Latin America, 123Seguro’s white-label API is now connected to more than 40 e-commerce sites, letting merchants upsell freight insurance without leaving the cart page.

Yet physical touchpoints still matter in rural and peri-urban settings. Hybrid models permit policies to be sold face-to-face and then serviced through WhatsApp bots or IVR menus, balancing education needs with cost control. MFIs typically batch-collect premiums alongside loan installments, reducing lapse risk. Branchless banking agents in Kenya now collect micro-premium top-ups as low as USD 0.20, proving that small tickets can be profitable with the right technology stack. As regulatory sandboxes promote remote onboarding, the global microinsurance market size originating from pure-digital journeys is projected to exceed that of agent-first pathways before 2028.

By Provider: Commercial Insurers Leverage Scale Advantages

Commercial carriers controlled 61.72% of the 2025 premium and are projected to post a 6.88% CAGR through 2031, consolidating their lead in the global microinsurance market size. Their solvency capital, reinsurance treaties, and actuarial depth allow them to amortize product development costs across multiple geographies. Allianz’s EUR 4.0 billion operating profit in Q1 2024 funded cloud-native policy-admin platforms that cut issue costs by 45% and allow real-time claims triage. Zurich’s USD 7.4 billion operating profit gives it the bandwidth to pilot parametric drought covers in sub-Saharan Africa without needing external donor backing.

Cooperative and mutual insurers maintain relevance where social cohesion peaks, often bundling savings or dividend components that resonate with community norms in the microinsurance market. Aid-linked schemes step in for ultra-low-income cohorts, but funding volatility limits scalability. Strategic alliances between the three provider categories are rising; commercial insurers front the risk, mutuals handle distribution, and aid agencies supply premium subsidies during launch years. Such tri-partite structures help ensure solvency compliance while safeguarding affordability, anchoring a balanced competitive landscape that supports both profit goals and inclusion mandates.

Geography Analysis

In 2025, North America accounted for 26.12% of global insurance premiums within the microinsurance market, driven by the National Association of Insurance Commissioners' efforts to promote financial inclusion. This initiative has encouraged broader access to insurance products across diverse demographics. In California, major insurers are now mandated to provide basic coverage equivalent to 85% of their market share, a move that directs resources towards areas vulnerable to wildfires, addressing a critical need for risk mitigation in high-risk zones. The U.S. grapples with a concentrated health insurance market, with 95% of states classified as highly concentrated, creating an opportunity for niche micro-products that sidestep traditional employer plans. These micro-products cater to specific consumer needs, offering flexibility and affordability. Meanwhile, Canada fosters growth via federal fintech sandboxes, which provide a controlled environment for innovation in financial services, and Mexico's FinTech Law is hastening the adoption of open data, enabling greater transparency and efficiency in the insurance sector.

Asia-Pacific is on track to be the fastest-growing region in the microinsurance market, boasting a 5.97% CAGR through 2031 as 4 billion consumers transition to digital wallets. This shift is transforming payment ecosystems and driving demand for digital insurance solutions. ZhongAn Online reported a 24.7% surge in gross written premiums in 2024, alongside a 40% boost in tech-export revenue, underscoring the region's "insurance + tech" momentum. The integration of technology into insurance operations is enhancing customer experience and operational efficiency. India's IRDAI is steering reforms towards universal coverage by 2047, aiming to make insurance accessible to every citizen. The Bima Sugam platform offers citizens a portable policy locker across insurers, simplifying policy management and improving transparency. The gig economy in Southeast Asia is driving demand for embedded personal accident coverage, addressing the unique risks faced by gig workers. Additionally, Indonesia is streamlining product launches with five-day approval cycles, enabling insurers to respond quickly to market demands and innovate at a faster pace.

Europe is witnessing steady growth in the microinsurance market, bolstered by the EU AI Act, which standardizes algorithm governance and expedites cross-border operations. This regulatory framework fosters innovation while ensuring compliance and consumer protection. Allianz's acquisition of Viridium for EUR 3.5 billion underscores a trend of life-portfolio consolidation on the continent, reflecting a strategic focus on optimizing portfolio performance and achieving scale. Pilot programs in the Nordics are showcasing the feasibility of real-time policy portability, which enhances customer convenience and promotes market competitiveness. South America is making strides with Brazil's Open Insurance initiative and Mexico's Fintech Law, which are driving innovation and improving market accessibility. However, inflation and currency fluctuations are putting a damper on profit margins, posing challenges for insurers in maintaining profitability. The Middle East & Africa present untapped potential, with Kenya's parametric drought covers and South Africa's flood insurance highlighting the opportunities in the microinsurance market for addressing climate-related risks. However, infrastructural challenges, such as limited technological adoption and underdeveloped distribution networks, pose scalability issues that need to be addressed for sustainable growth.

Competitive Landscape

In the global microinsurance market, the top five players indicate a moderate concentration. Commercial groups, capitalizing on their financial strength, are broadening their reach by offering tailored products and leveraging economies of scale. In contrast, regional cooperatives, bolstered by their local presence and the trust of the community, continue to dominate in village clusters by providing personalized services and fostering long-term relationships. The competitive landscape becomes even more pronounced as mobile network operators venture into underwriting. Their joint ventures introduce technological expertise and vast customer bases, and novel distribution channels, enabling them to cater to underserved segments and enhance accessibility to microinsurance products.

Partnerships have become a strategic focal point for growth and innovation. AXA’s EssentiALL, for instance, targets 20 million customers by 2026, leveraging postal collaborations to enhance accessibility in underserved areas and expand its footprint. ZhongAn, on the other hand, is monetizing its technology by licensing its cloud core to overseas carriers, enabling these carriers to modernize operations without heavy infrastructure investments, thereby creating a new revenue stream. Meanwhile, VSure Tech’s innovative pay-as-you-use model provides SMEs with hour-level liability coverage, addressing the specific needs of small businesses and reflecting a broader trend towards product micro-segmenting to cater to niche demands.

Investments in technology are heavily skewed towards AI-driven underwriting, parametric triggers, and blockchain-based policy administration. Insurers are harnessing data from driving habits, crop yields, and delivery platforms to fine-tune their pricing strategies, improve risk assessment, and enhance operational efficiency. There is untapped potential in areas like climate-related solutions, health plans for informal workers, and cyber coverage for SMEs, which remain largely unexplored but present significant growth opportunities. With low exit barriers, new entrants can swiftly gauge their market fit, leading to a dynamic churn that keeps incumbent players on their toes and fosters continuous innovation in the market. This dynamic environment encourages both established players and new entrants to explore innovative approaches to meet evolving customer needs and address emerging risks.

Microinsurance Industry Leaders

Allianz SE

AXA SA

Zurich Insurance Group

American International Group (AIG)

Hollard Insurance Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Allianz, in collaboration with BlackRock and T&D Holdings, made a significant move by acquiring Viridium Group for a hefty EUR 3.5 billion. This acquisition aims to strengthen Allianz's position in the life-portfolio consolidation market, reflecting a strategic effort to enhance its operational scale and market presence.

- March 2025: Swiss Re, in partnership with Good Carbon, introduced a novel carbon-credit non-delivery insurance. This innovative product is designed to address the risks associated with carbon credit projects by incorporating a buffer pool for replacement credits, ensuring greater reliability and trust in carbon offset mechanisms.

- January 2025: Allianz Partners unveiled its allyz Cyber Care in four EU markets. This offering combines advanced preventive technologies with comprehensive insurance benefits, aiming to address the growing concerns around cyber threats and provide enhanced protection for consumers.

- October 2024: Amwins collaborated with Floodbase, introduced a parametric flood coverage tailored for municipalities in California. This innovative solution is designed to offer faster payouts and improved financial resilience for communities facing the increasing risks of flooding due to climate change.

Global Microinsurance Market Report Scope

Microinsurance aims to offer affordable protection to individuals with limited income, aiding them in coping with and recuperating from setbacks. The microinsurance market is segmented by model type, product type, distribution channel, provider, and geography. By model type, the market is segmented into partner agent model and full-service model. By product type, the market is segmented into life insurance, health insurance, property insurance, and other product types (index insurance, accidental death and disability insurance, etc.). By distribution channel, the market is segmented into direct sales, financial institutions, digital channels, and other distribution channels (clinics, hospitals, etc.). By provider, the market is segmented into commercially viable and through aid/government support. The report offers market size and forecasts for all the above segments in value (USD) and volume (ton).

| Partner-Agent Model |

| Full-Service Model |

| Life (Credit-Life, Term, Funeral) |

| Health & Hospital Cash |

| Property & Crop |

| Accident & Disability |

| Livestock & Index-based Agriculture |

| Direct Sales (Agent / Branch) |

| Financial Institutions & MFIs |

| Digital |

| Commercial Insurers |

| Cooperative & Mutual Insurers |

| Aid-/Government-supported Schemes |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland) | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South East Asia | |

| Indonesia | |

| Rest of Asia | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East |

| By Model Type | Partner-Agent Model | |

| Full-Service Model | ||

| By Product Type | Life (Credit-Life, Term, Funeral) | |

| Health & Hospital Cash | ||

| Property & Crop | ||

| Accident & Disability | ||

| Livestock & Index-based Agriculture | ||

| By Distribution Channel | Direct Sales (Agent / Branch) | |

| Financial Institutions & MFIs | ||

| Digital | ||

| By Provider | Commercial Insurers | |

| Cooperative & Mutual Insurers | ||

| Aid-/Government-supported Schemes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| Nordics (Sweden, Norway, Denmark, Finland) | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South East Asia | ||

| Indonesia | ||

| Rest of Asia | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East | ||

Key Questions Answered in the Report

What is the current size of the global microinsurance market?

The global microinsurance market is worth USD 77.83 billion in 2026 and is projected to reach USD 101.82 billion by 2031.

Which distribution channel is growing fastest?

Digital platforms lead growth with a 6.23% CAGR through 2031, supported by mobile wallets, embedded checkout journeys, and regulator-backed marketplaces.

Why is Asia-Pacific the key growth engine?

Asia-Pacific benefits from rapid mobile money adoption, supportive regulations such as India’s Bima Sugam, and insurtech partnerships that streamline low-ticket policy delivery, resulting in a 5.97% regional CAGR.

How do parametric products fit into global microinsurance?

Parametric designs use pre-agreed triggers like rainfall or wind speed to pay claims quickly, reducing assessment costs and expanding affordable climate risk cover for smallholders and vulnerable communities.

What role do partner-agent models play?

The partner-agent structure combines insurer capacity with local institutions such as MFIs and cooperatives, giving it 43.15% of the 2025 premium and the highest 7.92% CAGR among model types.

What are the main barriers to global microinsurance adoption?

Key obstacles include data privacy compliance costs, limited actuarial data in emerging markets, trust deficits in claims handling, and varying capital rules that complicate cross-border scaling.

Page last updated on: