Market Overview

| Study Period | 2020 - 2031 |

|---|---|

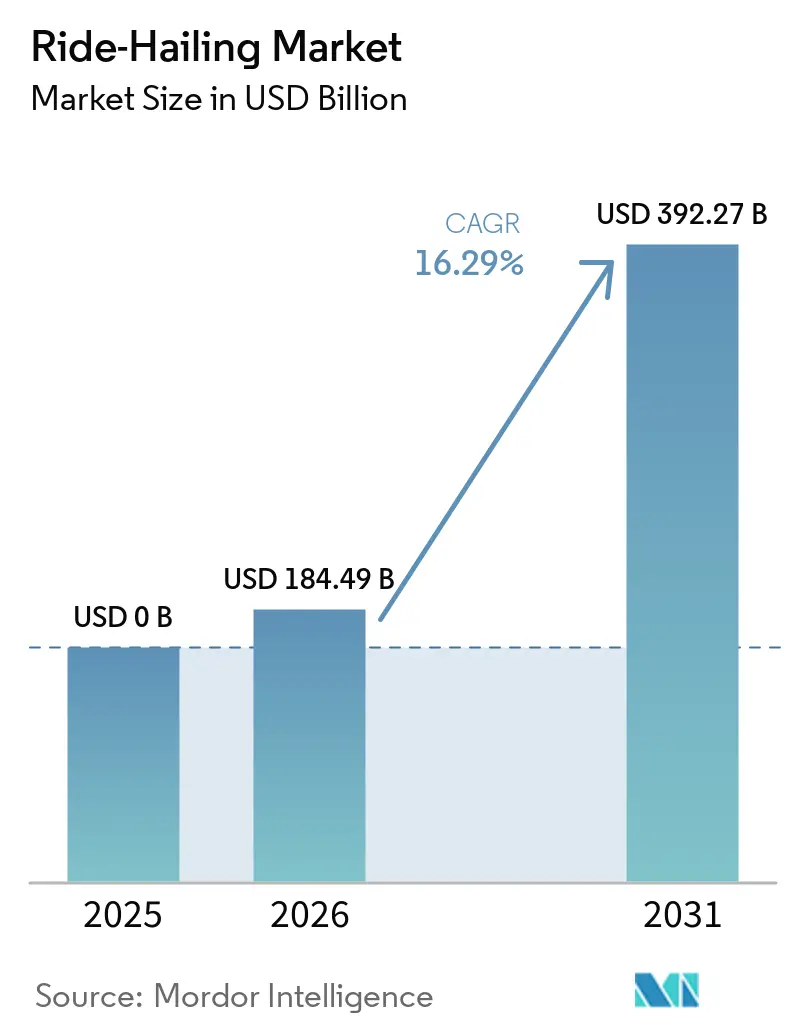

| Market Size (2026) | USD 184.49 Billion |

| Market Size (2031) | USD 392.27 Billion |

| Growth Rate (2026 - 2031) | 16.29% CAGR |

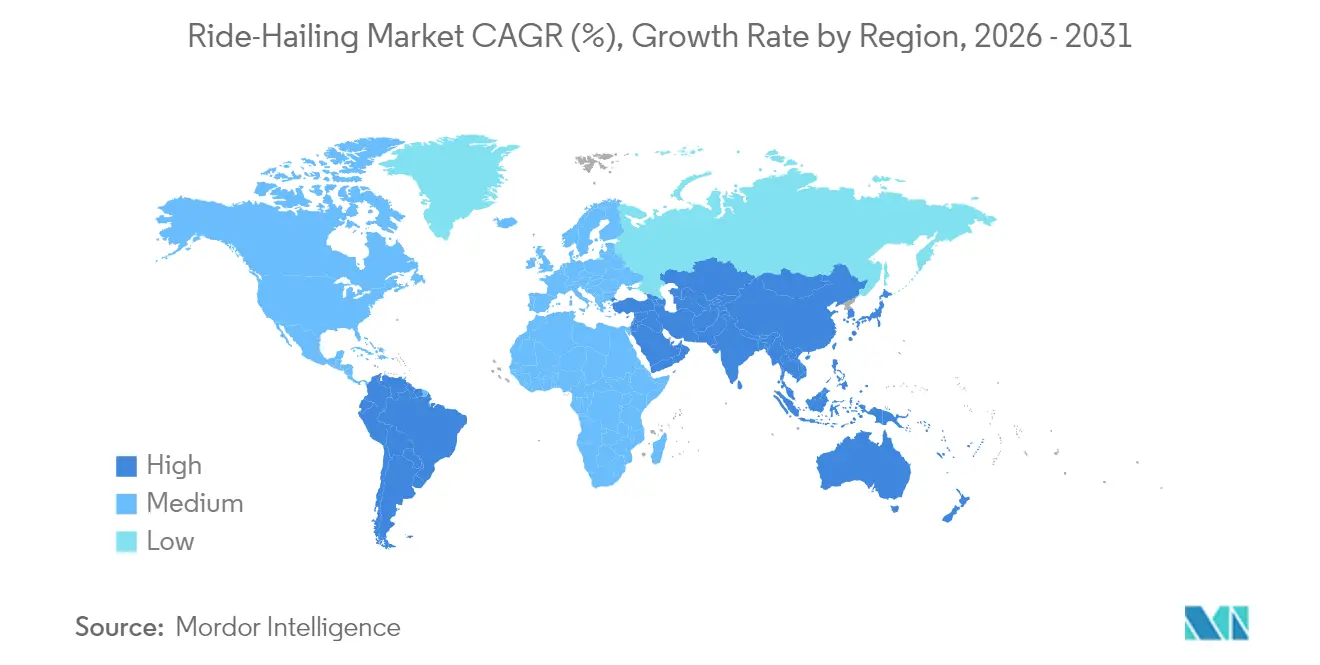

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

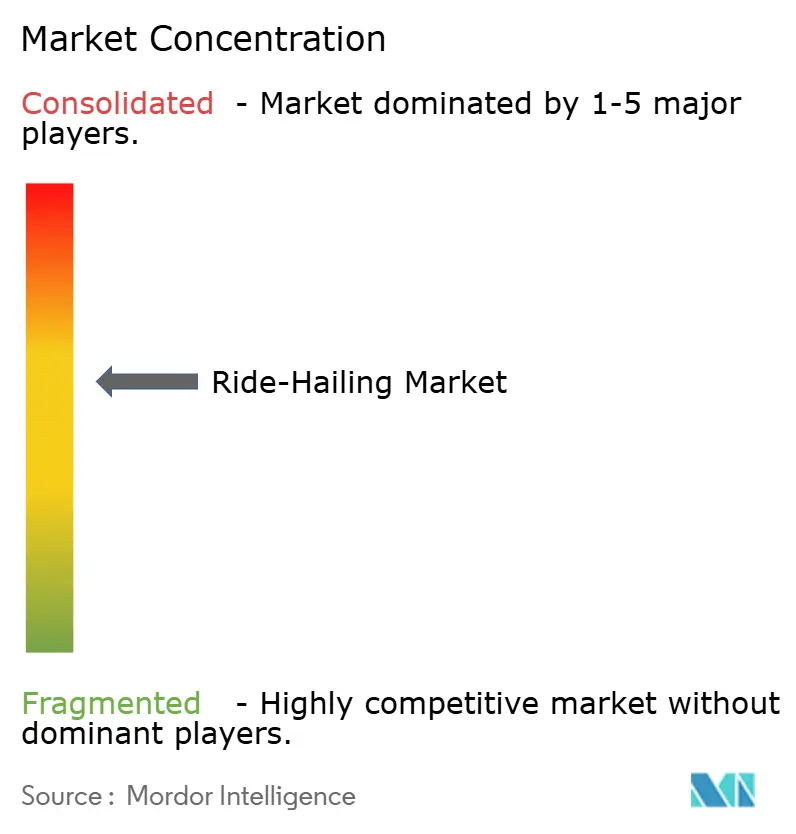

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ride-Hailing Market Analysis by Mordor Intelligence

The Ride-Hailing Market size is projected to be USD 0 billion in 2025, USD 184.49 billion in 2026, and reach USD 392.27 billion by 2031, growing at a CAGR of 16.29% from 2026 to 2031.

Rising urban density, advances in autonomous driving, and supportive policy frameworks jointly accelerate platform adoption across developed and emerging economies. Technology maturity allows operators to pool data, optimize routes, and cut empty-mile costs, while regulators across major cities increasingly nudge commuters away from private vehicle ownership toward shared mobility. Corporate tra vel budgets that now favor ride vouchers over company cars further widen the user base.

Key Report Takeaways

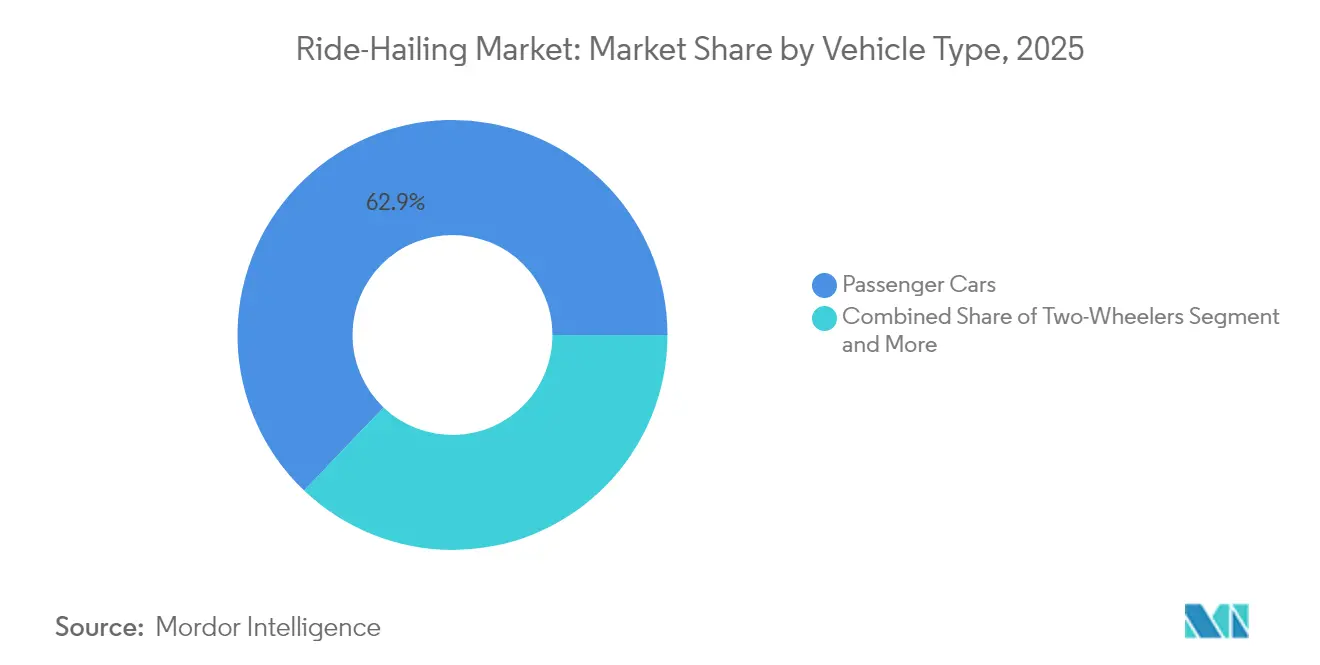

- By vehicle type, passenger cars captured 62.88% of ride-hailing market share in 2025, whereas two-wheelers led segment growth at a 16.54% CAGR through 2031.

- By propulsion type, internal-combustion engines retained 72.74% of the ride-hailing market size in 2025, but battery-electric vehicles are tracking a 16.55% CAGR to 2031.

- By service type, e-hailing commanded 73.62% of the ride-hailing market size in 2025; robo-taxis are expanding fastest at a 16.60% CAGR.

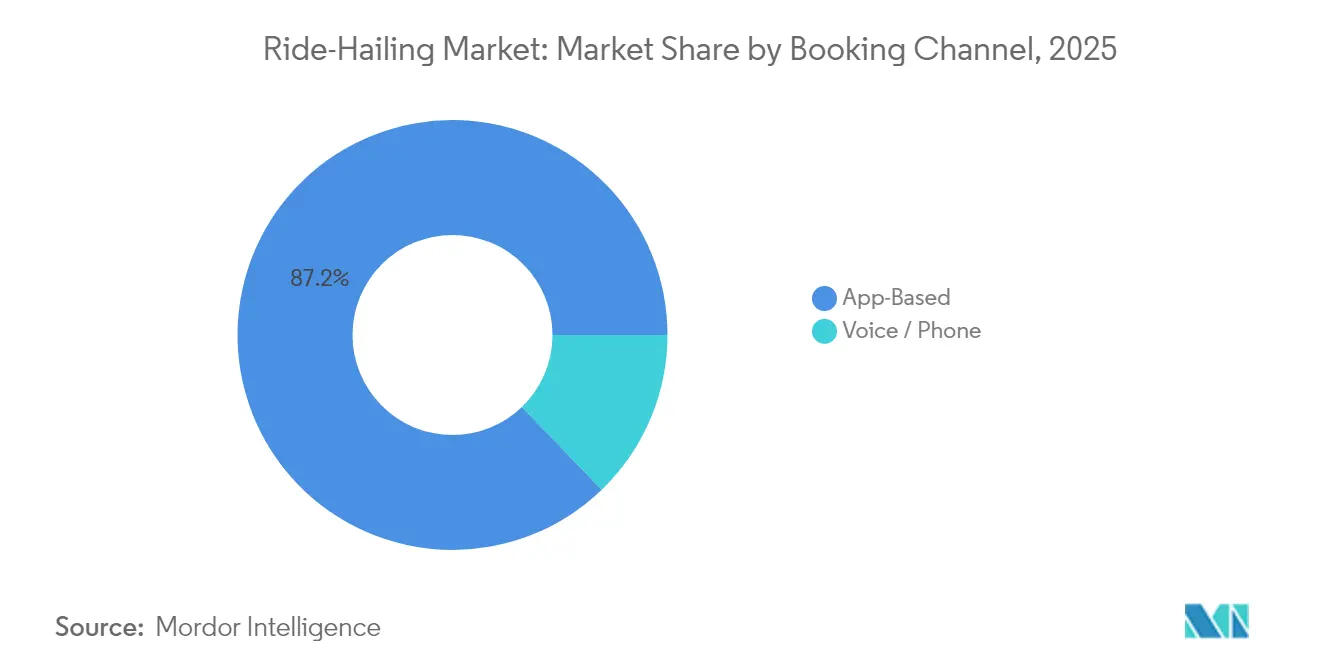

- By booking channel, app-based transactions covered 87.21% of the ride-hailing market in 2025 with a 16.47% CAGR outlook, while voice and phone reservations hold niche relevance.

- By end-user, personal riders contributed 61.12% of 2025 revenue, yet corporate accounts post the highest 16.36% CAGR through 2031 as mobility budgets replace fleet allowances.

- By geography, Asia-Pacific held a dominant 38.44% revenue share in 2025; South America is the fastest-growing region with a 16.43% CAGR led by Brazil’s strong driver base.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ride-Hailing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Traffic Congestion | +3.2% | Global, with highest impact in Asia-Pacific megacities | Long term (≥ 4 years) |

| Growing Smartphone Penetration | +2.8% | Emerging markets in South America, Africa, Southeast Asia | Medium term (2-4 years) |

| Fleet-Wide Electrification Mandates | +2.1% | North America, Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Subscription-Based Multimodal Super-Apps | +1.9% | Asia-Pacific core, expanding to global markets | Long term (≥ 4 years) |

| Employer-Funded Mobility Budgets | +1.6% | North America and EU, with early adoption in urban centers | Short term (≤ 2 years) |

| Early Integration With Urban-Air-Mobility Pilots | +1.1% | Select metropolitan areas globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Traffic Congestion & Urban Population Growth

In megacities such as Jakarta and Manila, heavy peak-hour traffic makes private car use impractical, leading many commuters to choose ride-hailing services[1]“Urban Mobility in Developing Cities,” World Bank, worldbank.org . Platforms offset congestion’s drag on driver utilization by applying AI-based dispatch that predicts demand clusters and trims empty miles; Lyft now achieves sub-one-minute ETA accuracy in San Francisco using historical and live traffic feeds. Public agencies view integrated Mobility-as-a-Service ecosystems as congestion relief. A World Bank study shows fragmentation cuts of up to two-fifths when Ride-hailing, transit, and micromobility are stitched together. The interplay of urban sprawl, limited parking, and growing environmental mandates creates a durable expansion runway through 2030.

Growing Smartphone & Broadband Penetration

Handset adoption is skyrocketing across Brazil, India, and Indonesia, unlocking new demographics for app-based booking and swelling the ride-hailing market user base. Brazil’s market grew exponentially by 2027 alongside Uber’s massive driver fleet. Voice-enabled interfaces reinforce inclusivity: Grab's AI assistant, adept at comprehending local accents, empowers visually impaired and elderly users to easily book on-demand rides independently. Broader 4G coverage in peri-urban zones further improves pickup reliability, tightening the service gap between core and fringe districts.

Fleet-Wide Electrification Mandates By TNCS

Inspired by California's Clean Miles Standard, which mandates ride-hailing firms boost electric vehicle usage by the decade's end, regions such as British Columbia, Paris, and Seoul are pursuing similar initiatives[2] “Clean Miles Standard,” California Air Resources Board, california.gov . Uber’s supply-side push with BYD could introduce 100,000 EVs in Europe and Latin America, buttressed by an OpenAI-powered driver assistant that steers partners toward optimal charging hubs. New York City, ahead of schedule, marked a significant milestone in its sustainability journey by achieving a notable number of zero-emission rides, underscoring its commitment to clean transportation, after Gravity Mobility installed chargers delivering 2,400 mi/h. These milestones illustrate how regulation, OEM alliances, and infrastructure scale align to shrink tailpipe emissions without curbing trip volume.

Subscription-Based Multimodal Super-Apps Boost Stickiness

Grab’s super-app model converts single-service users into multi-product customers who spend triple the average basket, lifting ride-hailing market lifetime value. The company cultivates robust customer loyalty across diverse sectors by weaving together meal delivery, digital payments, and insurance services. It is commanding in Southeast Asia's mobility and food delivery arenas. Public-private MaaS pilots in Vienna and the Netherlands echo this architecture by knitting Ride-hailing with transit and shared bikes under unified billing. Elevated switching costs and embedded fintech services fortify retention across varying income cohorts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict and Fragmented Regulatory Frameworks | -2.4% | Global, with highest impact in Europe and emerging markets | Medium term (2-4 years) |

| Data-Privacy Concerns | -1.8% | Europe, North America, with spillover globally | Short term (≤ 2 years) |

| Rising Gig-Driver Insurance Premiums | -1.5% | North America core, expanding to regulated markets | Short term (≤ 2 years) |

| Persistent Profitability Gaps | -1.2% | Global, with focus on emerging market operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict & Fragmented Regulatory Frameworks

The European Commission’s review of ride-sharing rules spotlights divergent city-level mandates on vehicle licensing, idle-time limits, and driver benefits. Spain capped new licenses based on pollution quotas, and Malaysia revoked inDrive’s permit for compliance lapses, underscoring policy heterogeneity. Localized taxes, such as North Carolina’s levy on exclusive rides, effective July 2025, further inflate operating complexity.

Data-Privacy / Cyber-Security Concerns

GDPR’s stringent consent and data-localization clauses oblige operators to store and process rider telemetry within the bloc, heightening compliance overhead. Cyber-events like the 2024 credential-stuffing attack on a leading platform triggered brief service outages in multiple U.S. metros, highlighting security as an operational risk. Enhanced encryption protocols and third-party penetration testing inflate costs but remain unavoidable prerequisites for retaining consumer trust in a data-rich ride-hailing market ecosystem.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Dominate Amid Diversification

Passenger cars contributed 62.88% of ride-hailing market share in 2025, anchoring revenue while driving a 16.38% segment CAGR through 2031 as automakers release ride-ready trims at fleet pricing. Two-wheelers and three-wheelers gain traction in congestion-prone cities; India’s Rapido now serves 25 million customers and 1.5 million riders, illustrating how motorcycles fill micro-trip demand. Vans and MPVs bolster corporate shuttle contracts, particularly where employer mobility budgets preload recurring pick-ups. The Indian bike-taxi opportunity, forecast to experience exponential growth by 2030, showcases diversification, although regulatory bans in Delhi and Maharashtra underscore compliance risk. Urban logistics add-ons, such as small parcel delivery during rider off-hours, further monetize vehicle time, making passenger cars a resilient core while niche modalities de-risk market saturation.

The segment’s expansion also aids fleet electrification because OEMs prioritize battery platforms for high-volume passenger models. As EV prices fall, operators lock bulk leases with range-optimized sedans, cutting maintenance outlays and boosting driver earnings. The ride-hailing market leverages telematics to ring-fence high-utilization sub-fleets, encouraging asset-light operators to control service quality without owning vehicles. Dual leadership in share and growth affirms passenger cars’ long-term primacy even as two-wheelers and robo-van concepts carve specialized lanes.

By Propulsion Type: Electric Transition Accelerates Despite ICE Dominance

Internal-combustion powertrains still command 72.74% of the ride-hailing market size in 2025, reflecting legacy vehicle pools. Yet battery-electric rides accelerate at 16.55% CAGR on the back of regulatory sticks and charging carrots. California’s 90% electric-mile rule for 2030 compels platforms to amass EV fleets, while NYC’s Gravity Mobility hubs provide 2,400 mi/h turnaround, minimizing downtime. Hybrid models bridge infrastructure gaps in markets where DC fast-chargers remain scarce, and CNG/LPG fleets sustain relevance in South Asia due to abundant supply chains. Uber’s plan to deploy 100,000 BYD EVs across Europe and Latin America signals a near-term volume spike, supported by app-based driver incentives that offset higher lease rates.

Brazil’s consumer survey showed stable ride-hail usage despite concerns about upfront EV prices, indicating that cost parity is not a binary prerequisite for mass adoption when platform-level subsidies close TCO gaps. Predictive dispatch shortens queue times for battery vehicles, mitigating range anxiety. With renewable energy penetration growing, the emissions advantage of EV fleets widens and feeds back into corporate sustainability reporting, generating a pull from enterprise riders.

By Service Type: E-Hailing Leadership Challenged by Robo-Taxi Innovation

E-hailing retained 73.62% of 2025 revenue, but robo-taxis posted a 16.60% CAGR, hinting at an inflection beyond manual driver models. Waymo now logs 100,000 weekly rides across multiple U.S. cities and has embedded into Uber’s interface, letting users toggle between human and autonomous cars. Car-sharing and peer-to-peer rentals meet asset-light traveler needs yet remain marginal at a sub-10% share. Subscription ride bundles emerge through corporate plans, locking recurring volume at predictable margins.

Uber’s USD hundreds-of-millions stake in Lucid-Nuro will introduce 20,000 autonomous SUVs within six years, affirming a multimodal future instead of binary human-versus-robot substitution. Wuhan regulators approve the large-scale rollout of driverless vehicles, highlighting confidence in the technology's readiness. While commercial rollout remains city-specific, learnings on rider trust, remote-assist protocols, and mapping will diffuse quickly, compressing lead times for the broader ride-hailing market.

By Booking Channel: App-Based Dominance Reinforces Digital Transformation

App-based orders accounted for 87.21% of 2025 bookings and sustain a 16.47% CAGR, mirroring the ubiquity of smartphones in target demographics. In-app algorithms predict fares, suggest pickup spots, and integrate digital wallets, streamlining the customer journey. Voice and phone lines linger for seniors or in patchy-coverage zones, serving as redundancy rather than primary channels. Grab’s speech interface achieves more than four-fifth accent accuracy, blending accessibility with mainstream functionality. Future iterations may leverage generative AI to parse real-time rider intent, suggesting multimodal itineraries that combine ride-hail with transit or e-scooters.

Importantly, channel dominance does not foreclose inclusivity; WhatsApp-based ordering pilots in India extend reach to users with limited data plans. Across emerging economies, operator chatbots handle trip status and dispute resolution, shrinking support overhead. The stickiness of app ecosystems underpins the ride-hailing market’s recurring-revenue logic and cross-sell pathways.

By End-User: Corporate Adoption Accelerates Amid Personal Market Maturity

Personal riders still produce 61.12% of turnover, yet corporate accounts post the highest 16.36% CAGR as business travel resumes and ESG reporting tightens. Mobility budgets rebundle transport spending into a unified wallet, letting employees claim ride-hail receipts without paper clutter.

Sustainability directives nudge corporations to log Scope 3 emissions, and Ride-hailing APIs feed granular trip data into carbon dashboards. Tiered loyalty programs reward frequent business riders with upgrades and lower surge multipliers, differentiating service levels. Meanwhile, personal user growth in mature cities plateaus, steering operator focus toward high-margin enterprise segments where predictable peak-hour demand improves fleet utilization and driver earnings.

Geography Analysis

Asia-Pacific contributed 38.44% of the ride-hailing market size in 2025. China, propelled by its dense urban landscapes, widespread smartphone penetration, and favorable mobility policies, is at the forefront of the autonomous vehicle revolution. Baidu's Apollo Go has rolled out a significant fleet of driverless cars in various cities, racking millions of completed rides. In India, two-wheelers, particularly through platforms like Rapido, are the go-to choice for commuters looking to sidestep long traffic jams without breaking the bank. In Southeast Asia, the patchwork nature of public transit is giving rise to super-apps, with companies such as Grab leading the charge in ride bookings. Its proposed merger with GoTo stands to forge a dominant regional entity potentially.

South America is the velocity leader with a 16.43% CAGR through 2031, anchored by Brazil, where Uber’s drivers form the company’s largest national fleet. Regional revenue grew exponentially by 2027, buoyed by rapid urbanization and cultural comfort with shared rides. Argentina and Colombia show early signs of regulatory openness, while UBS polling records stable rider loyalty despite inflationary stress. Platforms tailor low-bandwidth app versions to tap prepaid-phone segments, sustaining double-digit trip growth.

North America remains the technology crucible. Waymo's extensive autonomous trips, coupled with California's vigorous promotion of electric vehicles, are establishing pivotal benchmarks that influence global standards for sustainable and intelligent mobility. New York City's swift embrace of electric vehicle rides underscores the pivotal role of robust infrastructure, like fast-charging corridors, in propelling greener urban transport. Europe grapples with regulatory harmonization; the European Commission’s review aims to converge taxi and ride-share licensing, potentially unlocking pan-EU scaling.

Competitive Landscape

Oligopolistic dynamics define the ride-hailing market, with Uber, Didi, and Grab carving regional strongholds rather than any single player commanding monopoly power. In 2024, Uber's robust financial results drive significant investments in cutting-edge technologies, notably a hefty investment in robo-taxis through collaborations such as Lucid-Nuro. Grab, reigning as a super-app, fosters strong customer loyalty across its services. Its prospective merger with GoTo promises to consolidate hundreds of millions of users, potentially establishing a formidable regional powerhouse in Southeast Asia. On another front, Lyft's takeover of FREENOW marks a notable expansion into Europe, hinting that such consolidations might be a tactical maneuver against the rising tide of autonomous mobility.

AI differentiation eclipses basic ride-matching. Uber’s GPT-4o-powered driver assistant answers EV transition queries, while Lyft’s predictive ETA engine trims idle minutes, boosting driver earnings. Niche services gain traction as white-space plays: Grab’s voice interface for visually impaired riders and Lyft’s Silver segment for older adults illustrate demographic specialization. OEM alliances tighten, evidenced by Uber-BYD and Didi-SAIC tie-ups, securing preferential vehicle supply amid chip shortages.

Market entry barriers rise through data scale, regulatory expertise, and capital needs. Yet regional newcomers still surface in protected markets such as Iran and Nigeria. Ultimately, the top five operators control about three-fifth of global gross bookings, a level signaling healthy competition without fragmenting network effects.

Ride-Hailing Industry Leaders

Uber Technologies, Inc.

Lyft, Inc.

Grab Holdings Inc.

Bolt Technology OÜ

SUOL Innovations Ltd (inDrive)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Uber signs a global deal with Baidu to launch thousands of Apollo Go autonomous cars on the Uber network outside mainland China, first in select Asian and Middle Eastern cities.

- July 2025: Lyft completes the EUR 175 million acquisition of FREENOW, gaining coverage in 180 European cities and extending addressable trips to 300 billion annually.

- July 2025: Uber invests hundreds of millions in Lucid and Nuro to roll out more than 20,000 robotaxis over six years, each based on the Lucid Gravity SUV running Nuro’s self-drive stack.

Global Ride-Hailing Market Report Scope

A ride-hailing service refers to ridesharing services that, via website and mobile applications, match passengers with drivers of vehicles for hire that, unlike taxicabs, cannot be legally hailed from the street.

The ride-hailing market is segmented by vehicle type, propulsion type, and geography. By vehicle type, the market is segmented into motorcycles, cars, vans, and buses. By propulsion type, the market is segmented into internal combustion engine (ICE) and electric. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market size and forecast are provided in terms of value (USD).

By Vehicle Type

| Two-Wheelers |

| Three-Wheelers |

| Passenger Cars |

| Vans & MPVs |

| Buses & Shuttles |

By Propulsion Type

| ICE |

| Hybrid |

| Battery-Electric |

| CNG / LPG |

By Service Type

| E-Hailing |

| Car-Sharing (Peer-to-Peer) |

| Robo-Taxi |

| Subscription-Based Ride Packages |

By Booking Channel

| App-Based |

| Voice / Phone |

By End-User

| Personal |

| Corporate / Institutional |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Two-Wheelers | |

| Three-Wheelers | ||

| Passenger Cars | ||

| Vans & MPVs | ||

| Buses & Shuttles | ||

| By Propulsion Type | ICE | |

| Hybrid | ||

| Battery-Electric | ||

| CNG / LPG | ||

| By Service Type | E-Hailing | |

| Car-Sharing (Peer-to-Peer) | ||

| Robo-Taxi | ||

| Subscription-Based Ride Packages | ||

| By Booking Channel | App-Based | |

| Voice / Phone | ||

| By End-User | Personal | |

| Corporate / Institutional | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Ride-Hailing Market in 2026?

It totals USD 184.49 billion and is forecast to grow at a 16.29% CAGR to USD 392.27 billion by 2031 (2026-2031).

Which region grows fastest through 2031?

South America posts the highest 16.43% CAGR, led by Brazil’s strong driver network.

What share do electric rides hold nowadays?

Battery-electric trips are a minority but expanding fastest, with EV miles mandated to reach 90% in California by 2030.

Who leads autonomous deployments?

Waymo has surpassed 100,000 weekly rides, and Uber plans 20,000 Lucid-Nuro robotaxis, signaling leadership in commercial scale.

Why are corporate accounts important?

Employer-funded mobility budgets are rising at a 16.36% CAGR, offering higher margins and reliable demand compared with personal riders.

Page last updated on: