Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

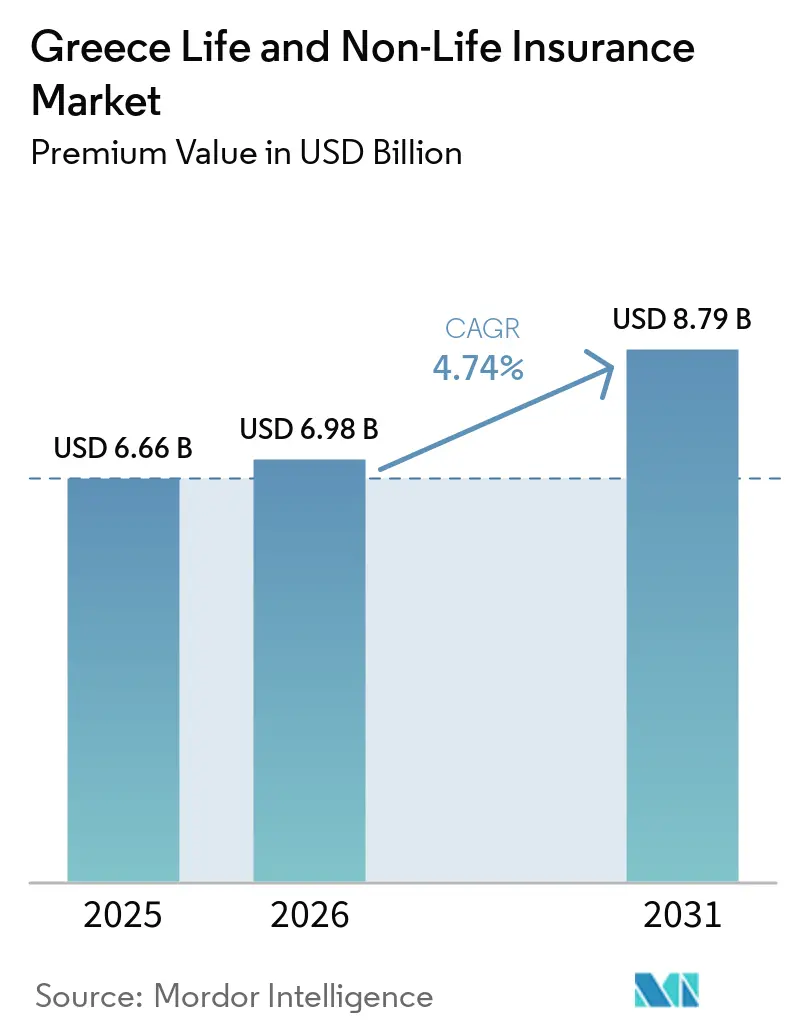

| Base Year Market Size (2025) | USD 6.66 Billion |

| Market Size (2026) | USD 6.98 Billion |

| Market Size (2031) | USD 8.79 Billion |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

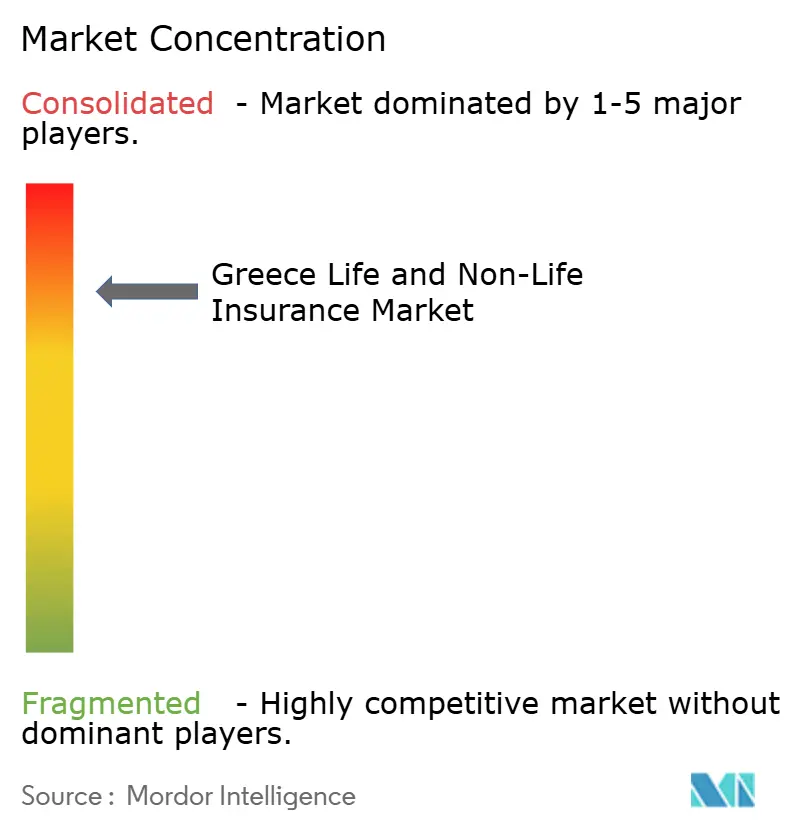

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Greece Life and Non-Life Insurance Market Analysis by Mordor Intelligence

The Greece Life And Non-Life Insurance Market size in terms of premium value is expected to increase from USD 6.66 billion in 2025 to USD 6.98 billion in 2026 and reach USD 8.79 billion by 2031, growing at a CAGR of 4.74% over 2026-2031.

The expansion reflects a shift from post-crisis stagnation to steady growth as regulatory modernization, pension reform, and digital distribution deepen risk awareness and drive product uptake. Non-life business retained a slim majority of written premiums, but life insurance accelerated on the back of funded pension accounts. Meanwhile, the rollout of compulsory electronic motor liability verification tightened compliance, adding hundreds of thousands of formerly uninsured vehicles and stabilizing motor loss ratios. Elsewhere, EU Recovery and Resilience Facility (RRF) disbursements totalling USD 35.95 billion are lifting household income and corporate investment appetite, supporting health, property, and specialty lines.

Key Report Takeaways

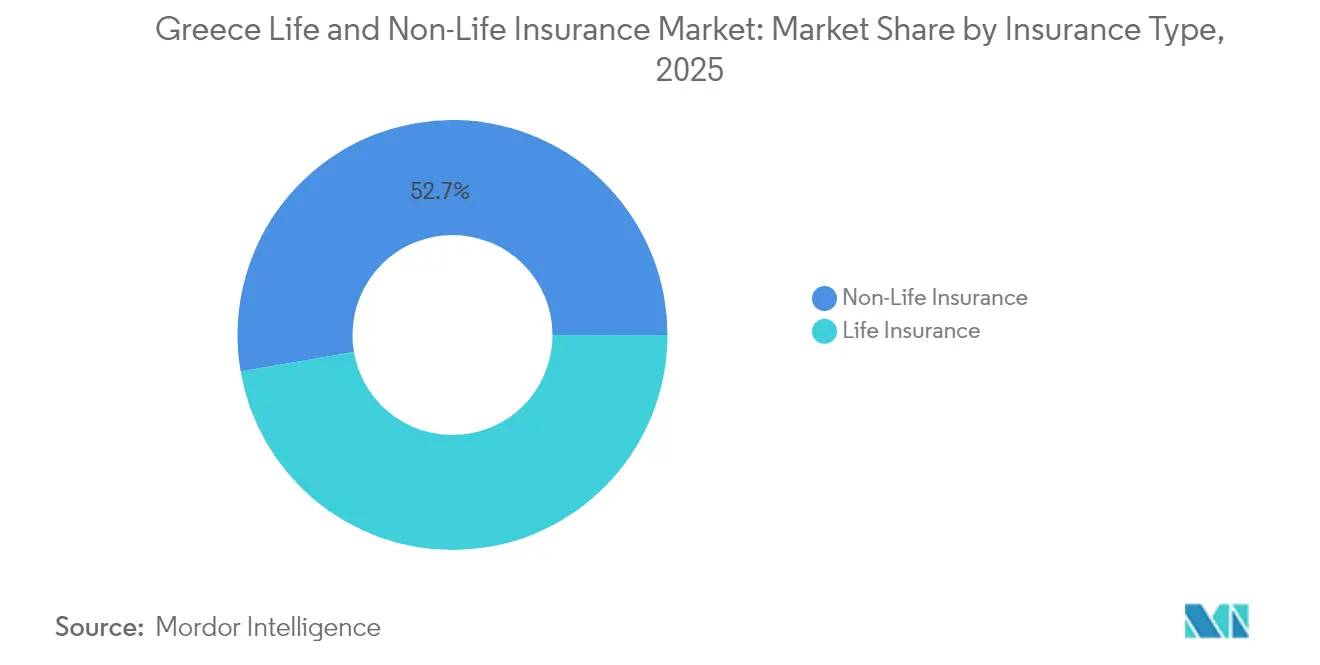

- By insurance type, non-life policies led with 52.72% of Greece life and non-life insurance market share in 2025; life insurance is projected to grow the fastest at a 6.95% CAGR between 2026-2031.

- By distribution channel, insurance agents retained 39.05% revenue share in 2025, while bancassurance is on track for the highest 8.05% CAGR to 2031.

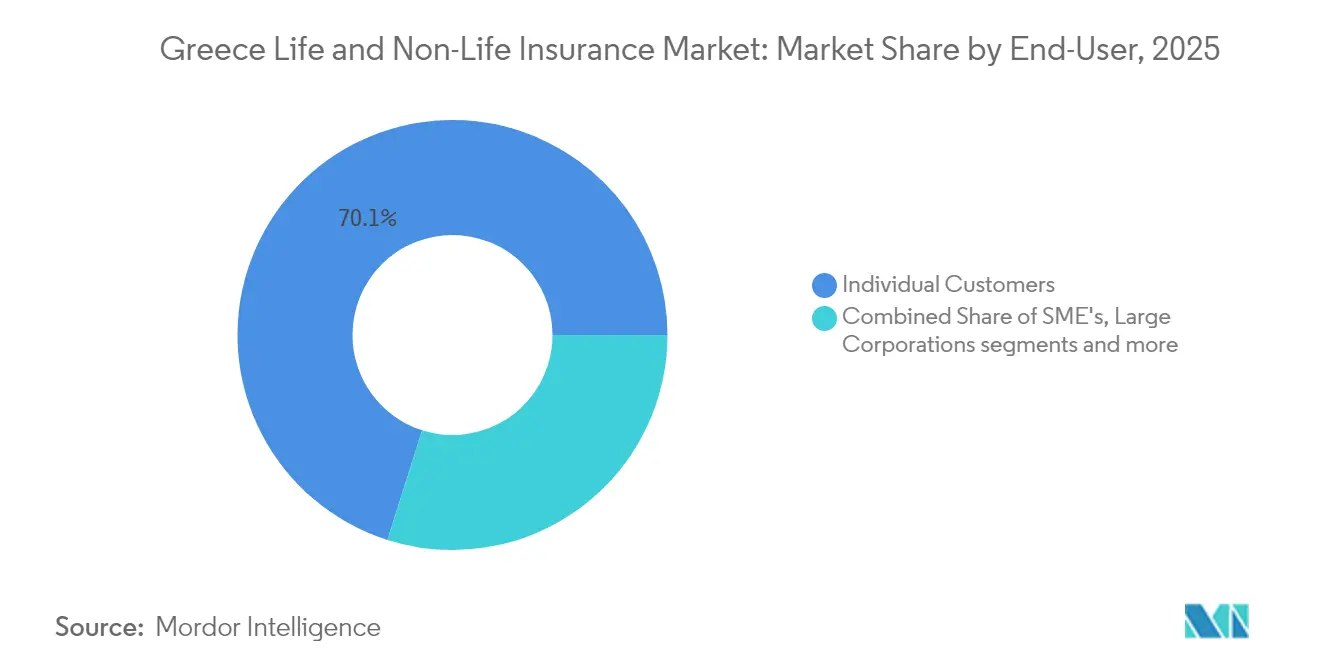

- By end user, individuals accounted for 70.10% of the Greece life and non-life insurance market size in 2025; small and medium enterprises are poised for a 6.03% CAGR through 2031.

- By premium type, regular premium products dominated with a 67.05% share in 2025, whereas single-premium products are expected to advance at a 6.72% CAGR to 2031.

- By region, Attica held 47.25% of the Greece life and non-life insurance market size in 2025; Central Macedonia is forecast to expand at a 5.45% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Greece Life and Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pension reform redirecting savings toward private life & annuity products | +1.2% | Attica, Thessaloniki | Medium term (2-4 years) |

| Residential construction and tourism infrastructure revival | +0.8% | Attica, Crete, Central Macedonia | Short term (≤ 2 years) |

| Electronic motor liability verification boosting compliance | +0.6% | Nationwide, urban focus | Short term (≤ 2 years) |

| Digital bancassurance integration with systemic banks | +0.7% | Financial hubs | Medium term (2-4 years) |

| EU RRF income lift for households and corporates | +0.5% | Nationwide | Long term (≥ 4 years) |

| Uptake of usage-based telematics motor policies | +0.4% | Major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated pension reform shifting retirement savings toward private life & annuity products

In Greece, accelerated pension reforms are driving growth in both life and non-life insurance markets. The 2024 reforms introduced funded defined-contribution auxiliary accounts, diverting an estimated EUR 1.5 billion annually from the public first-pillar system to private insurers[1]European Commission, “Recovery and Resilience Plan – Greece Amendments,” ec.europa.eu. With new tax incentives and contribution-matching mechanisms in place, voluntary participation in these reforms is on the rise. This uptick is especially pronounced given concerns over retirement adequacy, amplified by Greece’s ageing demographic, projected to see 67 retirees for every 100 workers by 2030. Capitalizing on this trend, life insurers reported a 7.9% premium increase in 2024, outpacing the broader market's growth. In a bid to attract talent, employers, especially in finance and tech-centric regions like Attica, are increasingly integrating life and pension benefits into their compensation packages. Insurers, in turn, are innovating their product offerings, spotlighting unit-linked plans, lifetime income guarantees, and coverage for longevity risks. As assets transition from the traditional pay-as-you-go (PAYG) state system to private portfolios, these reforms are poised to further deepen and diversify Greece's insurance landscape in the coming years.

Resurgence of residential construction and tourism infrastructure fueling property & casualty premium growth

Greece's life and non-life insurance market is witnessing a boost, largely fueled by a revival in residential construction and a surge in tourism infrastructure. In 2024, a 15% spike in residential investment, buoyed by a surge in building permits, was evident. Concurrently, significant tourism projects in areas like Crete and Central Macedonia heightened the demand for commercial property insurance. Property insurance premiums, driven predominantly by commercial lines, saw a 9.4% uptick. This rise is attributed to a growing emphasis on insurance-linked sustainability compliance for new projects. Moreover, public works in the EU, with budgets surpassing EUR 1 million, now come with a stipulation for builders’ liability coverage, amplifying the insured volumes. The revamped Golden Visa scheme has steered foreign investments towards premium real estate, spiking the demand for upscale property policies. In Attica, which accounts for 35% of Greece’s building permits, there's a noticeable surge in the uptake of contractor all-risk and project-specific insurance. These developments in real assets are not just channeling fresh premium inflows into the non-life segment but are also bolstering risk diversification within the Greek insurance landscape.

Mandatory electronic motor liability verification increasing compliance and premium uptake

The nationwide electronic verification platform connected to police databases removed a 15% uninsured vehicle gap by mid-2024, adding roughly 224,000 policies and lifting written motor premiums to EUR 1.24 billion. Automated number-plate recognition has shortened claims handling by 30% and eliminated historic fraud tied to uninsured motorists. The legal foundations—Presidential Decree 237/1986 and Law 489/76—gained real-time enforcement teeth, turning theoretical compliance into enforceable reality. Discussions are underway to replicate the model in other compulsory lines, potentially widening compliance-driven premium pools.

Rapid bancassurance digital integration with Greek systemic banks expanding distribution reach

Greece's systemic banks are rapidly integrating digital solutions into bancassurance, broadening their distribution reach and propelling growth in both life and non-life insurance markets. A prime example is Piraeus Bank's EUR 469 million acquisition of Ethniki Insurance, which combines Piraeus's 28% share of the deposit market with Ethniki's 14% stake in composite insurance premiums[2]Piraeus Bank, “Completion of Acquisition of Ethniki Insurance,” piraeusbankgroup.com. Thanks to digital tools, cross-selling now accounts for 65% of new policies, slashing acquisition costs by 25% and enhancing insurance uptake among retail banking clients. Strategic moves, like NN Hellas's renewed pact with Piraeus Bank and Alpha Bank's extended collaboration with Generali through 2040, are solidifying a bank-insurer ecosystem that seamlessly blends savings, protection, and investment products. These trends are driving a projected 8.24% CAGR for bancassurance, transforming Greece's insurance distribution landscape and underscoring its pivotal role in the market's growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural reliance on family and welfare dampening insurance penetration | -0.9% | Rural areas nationwide | Long term (≥ 4 years) |

| Catastrophic risk exposure inflating reinsurance costs and retail premiums | -0.7% | Seismic and wildfire zones | Medium term (2-4 years) |

| Macroeconomic drag from high sovereign debt servicing | -0.5% | Urban households | Medium term (2-4 years) |

| Price-sensitive motor market compressing underwriting margins | -0.3% | Competitive urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistently low insurance penetration owing to cultural reliance on extended family and welfare support

In Greece, a deep-rooted cultural reliance on extended family networks and state welfare support has led to persistently low insurance penetration, stifling the growth of both life and non-life insurance markets. From 1990 to 2019, a mere 8% of natural disaster losses were insured in Greece, starkly trailing the EU average of 25%. This discrepancy underscores a prevalent dependence on public aid and informal support systems. Such reliance fosters a moral hazard: when government-funded disaster relief acts as a stand-in for private insurance, it diminishes households' motivation to seek coverage. Surveys indicate a persistent distrust of insurers and a limited understanding of products, especially in rural regions where multigenerational living is common. Although a government mandate set for 2025 will require large businesses to insure against natural disaster risks, household adoption of insurance remains sluggish. Initiatives like awareness campaigns and micro-insurance trials strive to bridge the protection gap, yet deeply ingrained cultural attitudes are likely to continue hindering the market's long-term expansion.

Elevated catastrophic risk exposure driving up reinsurance costs and premium rates

Greece's life and non-life insurance markets are grappling with rising costs and premium rates, largely due to heightened exposure to catastrophic risks. In 2023, wildfires led to insured losses of EUR 300 million[3]World Bank, “Managing Disaster Risk in Greece,” worldbank.org. Meanwhile, damages from a rare 1-in-200-year earthquake could surpass EUR 22 billion, underscoring the need for substantial reinsurance and pushing policy prices up by 15–20%. As climate volatility intensifies, reinsurers are responding by tightening terms, implementing higher retentions, and enforcing regional exclusions. This shift compels primary insurers to either reduce their underwriting or pass on increased costs to policyholders. While there's been a proposal for a National Earthquake Insurance Scheme to distribute risk more evenly, legislative holdups have hindered its rollout. Without a robust public-private risk-sharing framework, the rising exposure to catastrophes will likely keep insurance unaffordable for many, particularly lower-income families in areas beyond urban hubs like Attica.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Life acceleration amid non-life dominance

Non-life business retained a 52.72% share of Greece life and non-life insurance market size. The life segment is projected to compound at 6.95%, far ahead of non-life, due to funded pension accounts and ageing demographics. Motor remains the biggest non-life class, yet property and health are expanding faster on the back of natural-disaster awareness and medical inflation. Within life, unit-linked products are gaining traction as consumers seek combined protection and capital-market returns in a low-rate environment.

The accelerating life trajectory also reflects EU RRF-led income growth and employers’ shift to group life schemes. Conversely, non-life players face margin erosion from surging catastrophe claims even as they diversify into cyber and specialty lines. Health premiums are set to jump 14% in 2025 as loss ratios surpass 100%, while traditional endowment policies are giving way to transparent, market-linked propositions that align with investor preferences. Overall, life’s higher CAGR will gradually erode non-life’s majority share, but the latter will remain the primary volume anchor of Greece life and non-life insurance market.

By Distribution Channel: Digital bancassurance disrupts agent networks

Insurance agents accounted for 39.05% of premium flows in 2025, supported by 1,600 corporate agencies and entrenched local relationships. Yet, bancassurance is projected to post the segment-leading 8.05% CAGR, propelled by systemic banks integrating policy journeys into mobile and online banking. The omnichannel model lowers friction and exploits vast customer datasets for cross-selling, particularly in life and savings. Brokers maintain a stronghold in complex commercial lines, and direct online players capture price-sensitive retail customers through aggressive digital marketing.

Piraeus Bank’s takeover of Ethniki Insurance exemplifies bancassurance’s disruptive momentum, promising a seamless bank-assurance super-app that could materially re-rank distribution shares. Meanwhile, Alpha Bank and Generali’s 15-year extension underscores a long-run commitment to the model. Regulatory upgrading under the Bank of Greece demands professional certification and capital adequacy for all intermediaries, raising compliance costs that may crowd out smaller agents. Consequently, Greece life and non-life insurance market is moving toward a hybrid distribution architecture in which bank-owned digital channels lead customer acquisition, and specialised brokers provide value-added advisory on complex risks.

By End User: SME growth outpaces individual dominance

Individuals supplied 70.10% of 2025 written premiums, a pattern anchored in compulsory motor insurance and expanding life protection. Nonetheless, SMEs are forecast to record the fastest 6.03% CAGR as EU funds spur entrepreneurial investment and regulations broaden mandatory covers such as professional liability. Large corporations and public entities already maintain sophisticated captives and international programs, limiting incremental growth potential, but new ESG and cyber obligations create selective upside.

SME demand extends beyond property and liability to cyber, environmental impairment, and business interruption, reflecting stricter supply-chain resilience requirements. Public procurement rules increasingly insist on evidence of insurance before awarding EU-funded contracts, effectively driving quasi-compulsory uptake. On the retail side, rising disposable income and digital customer experiences are nudging households toward bundled auto-home-life packages with loyalty discounts and streamlined claims. These dynamics progressively diversify the Greece life and non-life insurance industry risk pool.

By Premium Type: Single-premium growth challenges regular dominance

Regular-payment contracts comprised 67.05% of 2025 premiums, dovetailing with monthly salary cycles and smoothing cash flow for policyholders. Single-premium products, however, are projected to accelerate at 6.72% CAGR. Pension reforms enable lump-sum transfers from auxiliary accounts into annuities and investment-linked policies that offer estate-planning advantages and tax benefits. Higher-income retirees in Attica are especially predisposed to one-off premium outlays that secure lifetime income or bequest provision.

Regulation now favours transparent unit-linked designs over opaque guaranteed products, encouraging insurers to package single-premium offers that combine market participation with downside buffers. Non-life single-premium business is growing too: commercial property and project covers adopt upfront payments to simplify accounting and strengthen insurer cash flow. Regular-premium motor and property retains volume leadership, but competitive pricing and cost-of-living pressure weigh on margins. Overall, the rising single-premium share may gradually reshape liquidity and investment strategies across the Greece life and non-life insurance market.

Geography Analysis

Attica’s commanding 47.25% market share stems from its role as the nation’s economic nerve centre, home to 18 of 34 licensed insurers and a concentration of high-income households. The abundance of corporate headquarters fuels demand for specialty lines such as cyber, D&O, and multinational employee benefits. Digital adoption outstrips all other regions, with online sales and mobile claims functionality reinforcing customer experience leadership. Elevated property values and high vehicle density ensure motor and home insurance remain volume mainstays, though catastrophe-model adjustments for urban wildfire risk are becoming more prevalent.

Central Macedonia posts the fastest future trajectory, projected at a 5.45% CAGR through 2031. Thessaloniki’s port expansion and Belt-and-Road logistics projects require marine, hull, and cargo covers, while manufacturing investors seek comprehensive industrial packages aligned with EU ESG codes. Tourism growth in Halkidiki increases liability exposure for hotel and leisure operators, stimulating tailored solutions. Crop-insurance demand is rising too, as mechanised farming increases asset values and financing partners insist on risk transfer.

Thessaly, Crete and the Rest of Greece contribute diversified demand patterns. Thessaly’s seismic profile drives higher earthquake premium rates, yet EU-subsidised agritech investments are contingent on robust insurance. Crete’s seasonal tourism generates cyclicality requiring flexible cover periods, and island territories facing logistical constraints benefit from simplified, digital-first policy servicing. In less densely populated regions, cultural reliance on family risk-sharing and lower disposable income suppress uptake, sustaining a sizeable protection gap that regulatory and educational initiatives are only slowly narrowing.

Competitive Landscape

The top 5 players controlled the majority of 2024 written premiums, signaling a high concentration. Piraeus Bank’s purchase of Ethniki Insurance for EUR 469 million exemplifies escalating M&A. NN Hellas, Generali, Allianz, and Interamerican leverage long-term bancassurance alliances and aggressive digital investment to defend their share.

Digital-first challengers such as Hellas Direct deploy AI customer service and instant claim settlement to erode incumbents’ retail footholds, forcing legacy players to accelerate IT modernization. ERGO Greece rolled out its ‘Chara’ virtual assistant and ‘ERGO forMe’ portal, reflecting the hybrid approach of combining human agents with self-service tech. Regulatory tightening continues to shape competition: Law 5193/2025 transposes DORA cybersecurity standards, favoring larger firms with sophisticated resilience frameworks. Risk-based capital regimes also incentivize operational scale, encouraging further consolidation among Greece life and non-life insurance industry participants.

White-space growth prospects include telematics-based motor policies, SME cyber, parametric natural disaster covers, and ESG-linked underwriting solutions. Incumbents are exploring partnerships with insurtechs to accelerate time-to-market in these niches while controlling acquisition costs. Price competition remains intense in motor, compressing technical margins, but insurers aim to offset pressure through ancillary service bundles and cross-selling life or health riders. Overall, the competitive outlook points to continuing consolidation balanced by innovation-driven niche entrants.

Greece Life and Non-Life Insurance Industry Leaders

Ethniki Hellenic General Insurance Co.

Interamerican Hellenic Insurance (Achmea Group)

Generali Hellas Insurance Company

NN Hellenic Life Insurance Company

Allianz Hellas Insurance Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Piraeus Bank completed its EUR 469 million acquisition of a 70% stake in Ethniki Insurance, creating Greece’s largest integrated banking-insurance group with assets above EUR 4 billion

- February 2025: Reale Mutua di Assicurazioni acquired 75% of Ydrogios Insurance, signaling renewed foreign interest in the consolidating Greek market.

- January 2025: Law 5116/2024 introduced mandatory natural disaster insurance for large companies, unlocking an estimated EUR 200 million in annual premiums.

- December 2024: ERGO Greece expanded its ‘Chara’ AI virtual assistant and customer portal feature set.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every gross written premium generated by licensed insurers that underwrite life risk covers, pension-linked savings, and non-life policies such as motor, property, liability, accident, and health within Greece's borders. Reinsurance receipts stay outside this boundary. According to Mordor Intelligence, figures are stated in constant 2024 US dollars after translating euro denominated filings with the yearly average rate.

Scope Exclusions: credit insurance written by export guarantee agencies and offshore captives are not included.

Segmentation Overview

- By Insurance Type

- Life Insurance

- Endowment Insurance

- Term Life Insurance

- Whole-Life Insurance

- Unit-Linked Insurance

- Group Life Insurance

- Non-Life Insurance

- Motor Insurance

- Third-Party Liability

- Land Vehicle

- Property Insurance

- Fire and natural disasters

- Property Insurance

- Commercial Property

- Health Insurance

- Individual Health

- Group Health

- Marine, Aviation & Transport Insurance

- General Liability Insurance

- Motor Insurance

- Life Insurance

- By Distribution Channel

- Insurance Agents

- Brokers

- Bancassurance

- Direct (Online & Company Owned)

- Affinity Partners & Retailers

- By End User

- Individual Customers

- Small & Medium Enterprises

- Large Corporations & Public Sector

- By Premium Type

- Single Premium

- Regular Premium

- By Region

- Attica

- Central Macedonia

- Thessaly

- Crete

- Rest of Greece

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed underwriting managers, bancassurance heads, and independent agents across Attica, Central Macedonia, and Crete. They then ran an online questionnaire among policy-holders and SME finance heads. These dialogues clarified pricing drifts, digital distribution uptake, and the likely take-up of the new natural-catastrophe mandate, allowing us to refine growth assumptions and lapse rates that raw desk data could not reveal.

Desk Research

We started with regulatory filings and statistical yearbooks from the Hellenic Association of Insurance Companies, Bank of Greece solvency reports, and Eurostat household income dashboards, which provided the foundational premium, penetration, and demographic series. Public databases such as IMF Financial Access Survey, Swiss Re sigma world insurance tables, and the OECD pension outlook helped benchmark long-run ratios and macro sensitivities. Paid intelligence from D&B Hoovers and Dow Jones Factiva was tapped to cross-verify corporate premium splits, M&A deal values, and channel strategies. This list illustrates the breadth of documentary evidence consulted; many additional public and subscription sources informed narrower datapoints and sanity checks.

Market-Sizing & Forecasting

A top-down reconstruction of total premiums starts with audited 2024 sector GWP, which is then segmented by line and channel using regulator and association shares. Results are corroborated with selective bottom-up approximations built from sampled average premium multiplied by policy volumes for motor, property, and term life, ensuring material lines reconcile within a +/-3 % tolerance. Key variables driving the model include insurance penetration versus disposable income, new vehicle registrations, mortgage issuance, population age mix, and statutory reform timelines. Multivariate regression with ARIMA error correction projects each driver to 2030, while scenario analysis captures macro shock sensitivities. Gaps in bottom-up inputs, especially for specialty covers, are bridged through weighted averages drawn from disclosed retention ratios and reinsurer cessions.

Data Validation & Update Cycle

Outputs pass automated variance flags, peer review, and senior analyst sign-off. Mordor refreshes every twelve months, with interim updates triggered by material events such as tax law changes or large catastrophe losses.

Why Mordor's Greece Life & Non-Life Insurance Baseline Commands Reliability

Published estimates often differ because firms pick dissimilar premium classes, currency bases, and forecast cadences.

Our disciplined scoping, annual refresh, and dual-track modeling lessen those distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.66 B (2025) | Mordor Intelligence | - |

| EUR 7.5 B (2023) | Global Consultancy A | Includes reinsurance and health riders, uses pre-COVID trend extrapolation |

| EUR 5.68 B (2024) | Trade Journal B | Reports gross euro value only, omits unit-linked life savings, no currency adjustment |

These comparisons show that, by selecting a clearly stated scope and validating euro data through both top-down and bottom-up lenses, Mordor delivers a balanced, traceable baseline that decision-makers can replicate and stress-test with confidence.

Key Questions Answered in the Report

What is the current size of the Greece life and non-life insurance market

Greece life and non-life insurance market reached USD 6.98 billion in 2026 and is forecast to advance at a 4.74% CAGR, lifting total premium income to USD 8.79 billion by 2031

Which insurance segment is growing the fastest?

Life insurance premiums are projected to grow at 6.95% CAGR during 2026-2031 due to pension reform and ageing demographics.

Why is bancassurance gaining traction in Greece?

Systemic banks are digitising insurance sales, giving bancassurance an 8.05% projected CAGR and lowering distribution costs by 25%.

How concentrated is the competitive landscape?

The top ten insurers command dominant share of premiums, indicating a moderately high level of market concentration.

Page last updated on: