Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

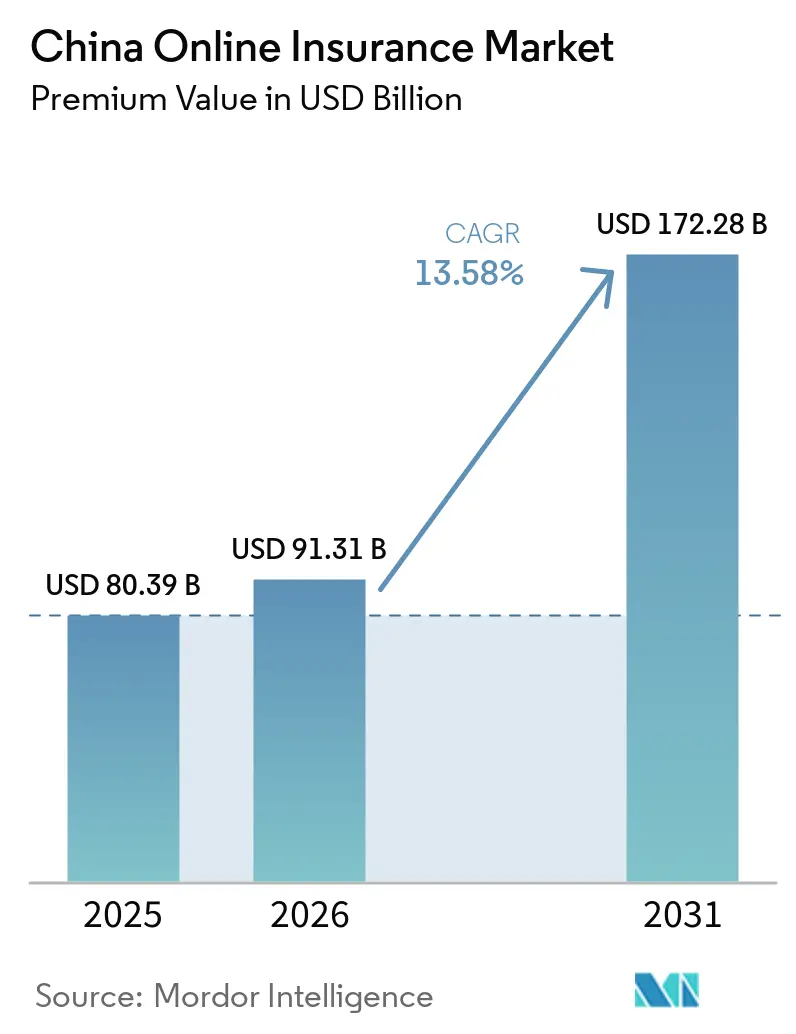

| Base Year Market Size (2025) | USD 80.39 Billion |

| Market Size (2026) | USD 91.31 Billion |

| Market Size (2031) | USD 172.28 Billion |

| Growth Rate (2026 - 2031) | 13.58% CAGR |

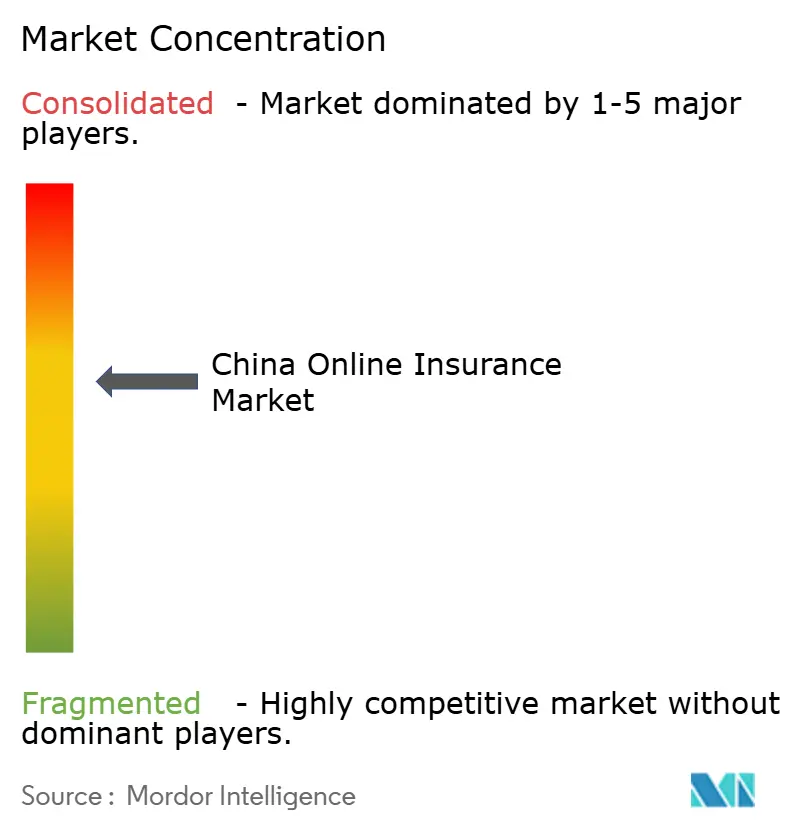

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Online Insurance Market Analysis by Mordor Intelligence

The China Online Insurance Market size in terms of premium value is expected to grow from USD 80.39 billion in 2025 to USD 91.31 billion in 2026 and is forecast to reach USD 172.28 billion by 2031 at 13.58% CAGR over 2026-2031.

Growing regulatory support, super-app distribution, and AI-enabled operations collectively reinforce double-digit momentum for the China online insurance market. Property & Casualty products lead digital conversion because mandatory motor coverage now issues, renews, and settles claims entirely online. Retail buyers dominate policy volumes, but small-business demand is accelerating as SMEs seek cyber and professional liability cover. Competitive intensity is rising as state-owned giants modernize platforms to defend share against pure-play digital insurers, while rising compliance costs and platform commissions compress margins.

Key Report Takeaways

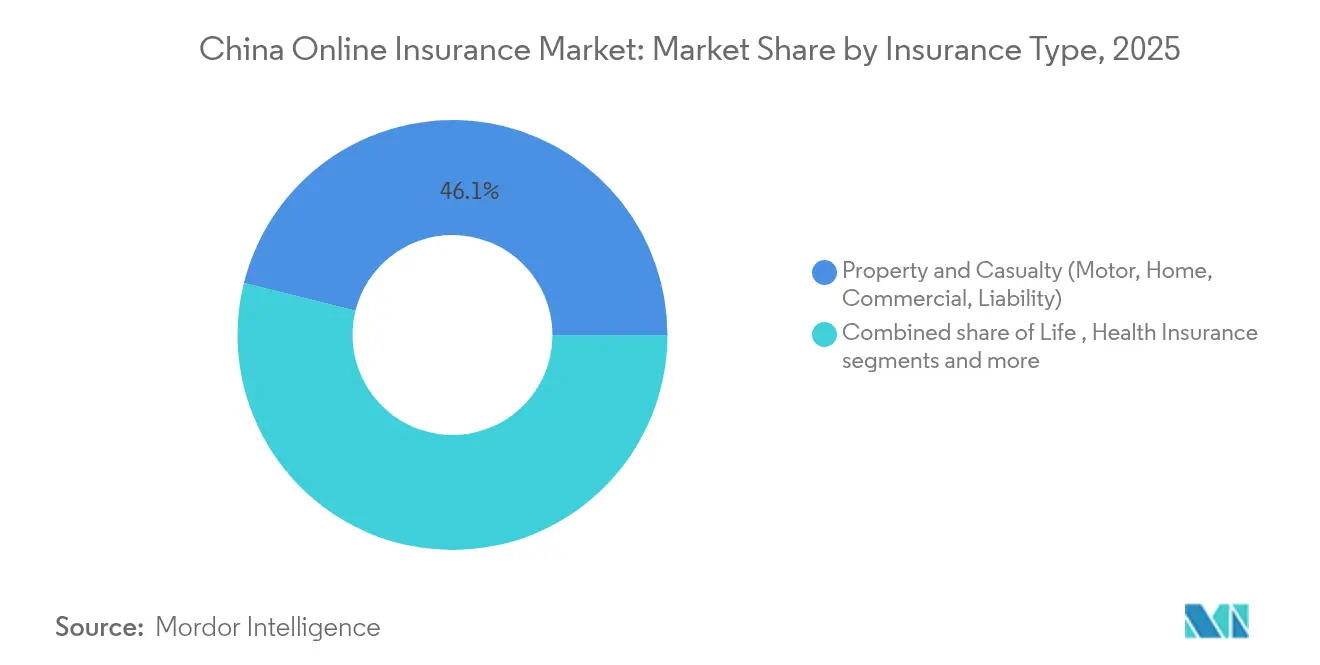

- By insurance type, property & casualty held 46.12% of the China online insurance market share in 2025, whereas specialty lines are projected to post an 8.05% CAGR through 2031.

- By customer segment, retail captured 69.45% revenue share in 2025, and SME & commercial accounts are set to grow at a 7.21% CAGR to 2031.

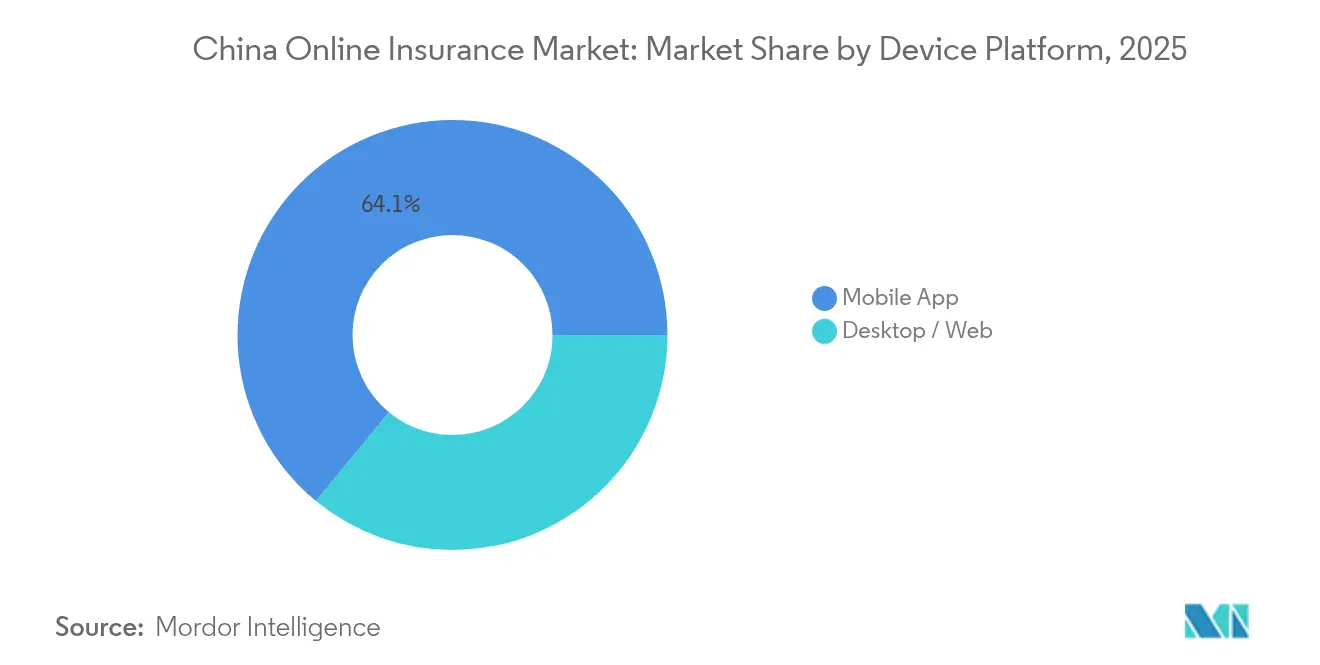

- By device platform, mobile applications contributed 64.05% of transaction value in 2025 and continue to record the highest 8.68% CAGR over the outlook period.

- By geography, Tier-1 and Tier-2 cities generated 34.62% of premiums in 2025, while central and western provinces are forecast to be the fastest-expanding cluster at a double-digit CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Online Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-only insurance licenses | +2.8% | National, early gains in Tier-1 cities | Medium term (2-4 years) |

| Rising middle-class demand | +3.2% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Super-app conversion uplift | +2.1% | National, strongest in mobile-first demographics | Short term (≤ 2 years) |

| AI-powered underwriting & claims | +1.9% | National, led by insurtech hubs | Medium term (2-4 years) |

| Usage-based motor coverage | +1.6% | Urban centers with high EV penetration | Medium term (2-4 years) |

| Hainan cross-border data reforms | +0.8% | Hainan, spillover to mainland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Mandated Expansion of Digital-Only Insurance Licenses

The 2025 NFRA framework grants streamlined digital-only charters, lowering capital hurdles and enabling technology-native firms to enter the China online insurance market quickly[1]Norton Rose Fulbright, “China’s Digital-Only Insurance Licenses: Regulatory Update 2025,” nortonrosefulbright.com. Applicants focus on cyber, pet, and usage-based motor products that incumbents have historically overlooked. Uniform conduct rules now bind digital carriers to heightened disclosure, but lean virtual operations still deliver cost advantages that translate into competitive pricing. The policy explicitly encourages embedded distribution through super-apps and mandates transparent AI model governance. Consequently, more entrants intensify product innovation and widen consumer choice, sustaining growth momentum across the China online insurance market.

Rising Middle-Class Demand for Protection Products

Urban disposable income gains and lifestyle upgrades lift appetite for comprehensive health, life, and property cover across the China online insurance market. Eighty percent of metro households prefer mobile management of insurance, driving digital adoption. Commercial health policies grow swiftly as employer-funded benefits become a talent magnet. Greater home and vehicle ownership pushes motor, home, and liability uptake, while cross-border travel boosts demand for travel and marine policies. The demographic’s readiness to share data for personalized pricing accelerates usage-based product penetration over the medium term.

Super-App Ecosystems Boosting Insurance Conversion

WeChat and Alipay embed micro-insurance offers within daily payments, pushing the China online insurance market toward friction-free purchase journeys. Conversion rates surpass 15%, well above traditional banner ads, because contextual triggers align coverage with real-time user actions[2]Ant Group, “WeSure Growth Metrics 2025,” antgroup.com. Mini-programs eliminate sign-up steps, while native payments automate premium collection and claim payouts. Cross-selling of travel, device, and wellness policies inside these ecosystems strengthens retention and increases policy per customer metrics. As super-apps refine AI recommendation engines, embedded insurance is expected to deepen market penetration, especially among Gen-Z users.

AI-Powered Instant Underwriting & Claims

Ping An and ZhongAn deploy machine-learning engines that underwrite 90% of standard proposals in under 30 minutes and settle most motor claims within 3 hours[3]Ping An Group, “Annual Report 2025,” pingan.com. Image-recognition and telematics data enhance risk pricing accuracy, reduce fraud, and improve loss ratios, making AI central to the operational economics of the Chinese online insurance market. Virtual assistants powered by natural-language processing cut human service workloads by 60%, yet deliver 24/7 support. Regulators now require audit trails for algorithms, pushing carriers to invest in explainable AI and bias detection frameworks that safeguard consumer interests.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer trust deficit | -1.4% | National, notably rural & elderly markets | Short term (≤ 2 years) |

| Stricter solvency capital rules | -0.9% | National, hits smaller insurers hardest | Medium term (2-4 years) |

| Platform-driven margin pressure | -1.2% | National, centered in mobile-first urban clusters | Medium term (2-4 years) |

| Cyber-security & data-localization costs | -0.8% | National, intense on cross-border operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer Trust Deficit After Mis-Selling Cases

Regulators fined multiple carriers for false advertising and data misuse in 2024, souring sentiment among older and rural consumers[4]DLA Piper, “China Consumer Protection Enforcement Review 2024-2025,” dlapiper.com. New rules ban incentive-driven reviews and enforce cooling-off periods, lengthening sales cycles and lifting compliance costs. Insurers respond with transparent policy wording, real-time complaint dashboards, and financial-literacy outreach to rebuild confidence. Short-term growth slows, yet sustained adherence to consumer-protection norms is expected to restore adoption rates across the China online insurance market by 2027.

Stricter CBIRC Solvency Capital Rules

July 2025 measures reclassify asset risk weights and mandate quarterly stress tests, tightening capital buffers across the China online insurance market. Small regional players face disproportionate strain, triggering exit or merger scenarios that reshape competitive dynamics. Some carriers pause new-business intake or shed high-capital products, tempering near-term premium expansion. Well-capitalized market leaders exploit the turmoil, using balance-sheet strength to capture vacated share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Digital P&C Scale Leads While Specialty Lines Accelerate

The Property & Casualty segment delivered 46.12% of total premiums in 2025 within the China online insurance market share, benefiting from mandatory e-motor certificates and rapid commercial-risk digitization. Motor remains the largest sub-line as 320 million registered vehicles renew coverage online, aided by image-based claims that shorten settlement cycles. Homeowners in urban towers increasingly buy bundled contents and earthquake protection through smartphone apps. Commercial property and liability demand rises as exporters seek supply-chain coverage aligned with global standards. Meanwhile, specialty lines post an 8.05% forecast CAGR, making them the fastest-growing slice of the China online insurance market through 2031. Cyber breaches, pet adoption, marine logistics, and post-pandemic travel fuel uptake, with micro-duration and event-based products delivered through super-apps. Regulatory sandboxes in Shanghai and Shenzhen support experimentation, accelerating speed-to-market for niche covers.

Digital broker APIs simplify quotation, while AI underwrite curbs loss ratios, positioning specialty insurers for long-run profitability. Partnerships between ZhongAn and logistics platforms automate marine cargo protection, ensuring real-time risk assessment on transit data. Pet insurers partner with vet chains to bundle medical services, embedding policies at checkout. The high-growth trajectory attracts foreign reinsurers that supply capacity and actuarial expertise. Continuous product refresh cycles and granular data feedback loops sustain innovation and cement the China online insurance market as a testbed for next generation covers.

By Customer Segment: Retail Dominance Sustains, SMEs Emerge as Growth Catalyst

Retail clients commanded 69.45% of premiums in 2025, affirming the consumer-centric core of the Chinese online insurance market. Simpler products, transparent pricing, and instant issuance fit smartphone scroll behavior, while gamified wellness programs build stickiness. Digital term-life and critical-illness offerings gain traction among millennials wary of long-term policies. Personal-property and device cover monetize China’s gadget-rich lifestyle, with one-click extensions at the point of sale. Repeating purchase and renewal automation boost lifetime value, offsetting platform commission costs. SMEs, however, are projected to outpace retail at a 7.21% CAGR, reaching a sizable share of China's online insurance market by 2031. Supply-chain disruptions, cyber threats, and labor-law liabilities push small firms to adopt coverage once reserved for large corporations.

Insurers introduce modular bundles, letting owners scale limits as business grows. Digital underwriting reduces documentation, letting SMEs bind policies in minutes. Credits linked to safe-behavior analytics lower premiums, incentivizing risk-management upgrades. Government procurement portals now accept e-financial-guarantee bonds, unlocking fresh demand. As SMEs spread westward, carriers partner with regional fintechs to deepen penetration, ensuring balanced portfolio mix across the China online insurance market.

By Device Platform: Mobile Supremacy Shapes Experience, Web Remains Critical for Complex Covers

Mobile apps generated 64.05% of 2025 policy value and recorded the highest 8.68% CAGR, guaranteeing their primacy in the China online insurance market. Super-app ecosystems let users buy travel covers during ticket booking and renew motor policies via push reminders tied to vehicle registration. Photo-upload claims, GPS accident validation, and biometric log-in enrich convenience. Seamless payments speed premium collection, curbing lapse rates.

Regulatory APIs embedded in apps ensure pre-contract disclosures and consent logs, aligning with NFRA rules. Despite mobile dominance, desktop portals retain importance for enterprise accounts and policy comparisons that require wider display. Businesses exploit bulk-upload dashboards for fleet and employee-benefit management. Responsive web design ensures cross-platform continuity, allowing users to initiate on phones and finalize on PCs, enhancing engagement across the China online insurance market.

Geography Analysis

Tier-1 clusters, Beijing, Shanghai, Guangzhou, and Shenzhen, together supplied 34.62% of premiums in 2025, reflecting high internet saturation, affluent demographics, and concentration of corporates. These hubs pilot AI claims bots, embedded-finance co-launches, and insurance NFTs, seeding innovations later scaled nationwide. Policy density is highest among young professionals whose digital wallet usage exceeds 95%, sustaining premium recycling within the China online insurance market. Provincial regulators in these zones also deploy sandboxes, easing product testing and accelerating approval cycles.

The Yangtze River Delta and Pearl River Delta industrial belts underpin robust growth in commercial P&C lines. Exporters ensure cargo, credit, and manufacturing facilities via online platforms that sync with customs records. Usage-based motor policies flourish as EV adoption climbs, particularly in Shenzhen, where municipal subsidies catalyze EV fleet expansion. Western and central provinces now present the fastest-growing frontier, driven by government infrastructure spending and 5G rollout. Local fintechs cooperate with national insurers to onboard rural consumers through mini-program tutorials and agricultural-insurance subsidies. As broadband reaches villages, crop and livestock policies distributed via e-commerce widen the China online insurance market’s addressable base.

Rural penetration nonetheless trails urban uptake due to lower digital literacy and trust concerns. Insurers collaborate with village co-ops and postal banks for omnichannel service, blending online enrollment with on-ground claim surveys. Cultural nuances require Mandarin and dialect content, along with simplified visuals. Remote-sensing and drones verify crop loss, expediting payouts in disaster-prone areas.Over time, rising rural income and smartphone ownership are expected to narrow the urban-rural gap, enabling balanced geographic distribution of premiums within the Chinese online insurance market..

Competitive Landscape

In 2024, the top five carriers command a significant share of the market, indicating a landscape of moderate competition. Ping An, harnessing its universal-banking ecosystem, adeptly cross-sells policies spanning wealth management, loans, and healthcare services. ZhongAn, a frontrunner in pure online distribution, swiftly rolls out micro-duration covers in mere days, due to its cloud-native architecture. Ant Insurance Services, capitalizing on Alipay's vast user base of 1 billion, drives the Chinese online insurance market towards a focus on contextual, event-based products. Meanwhile, traditional powerhouses like PICC and China Pacific, in a bid to safeguard their market share, are modernizing their legacy systems in collaboration with AI partners. Foreign players, AIA and Allianz, are strategically positioning themselves in high-value life and specialty commercial lines, leveraging their global underwriting expertise and established brand trust.

Strategic partnerships are pivotal in shaping industry dynamics. In a notable collaboration, Ping An teams up with FAW Hongqi to develop intelligent-driving motor policies, harnessing the power of vehicle telemetry. Cheche Technology, in partnership with Nio, is fine-tuning EV telematics pricing, establishing new benchmarks for green-mobility insurance. Reinsurers, Munich Re and Swiss Re, bolster domestic insurtechs with their capacity and analytics, especially those focusing on cyber and pandemic-risk covers. These partnerships are driving innovation and setting new standards across the market.

As solvency regulations tighten, smaller carriers feel the pinch, leading to a wave of consolidation. Larger groups, seizing the opportunity, are acquiring licenses to broaden their geographic footprint. Looking ahead, the trajectory of the China online insurance market will be shaped by technological prowess, data governance, and an unwavering commitment to customer experience. These factors will play a critical role in determining market share shifts over the forecast period.

China Online Insurance Industry Leaders

Ping An Insurance

ZhongAn Online P&C Insurance

Ant Insurance Services

Tencent WeSure

PICC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Ant Group introduced the AI-driven AQ healthcare app integrating insurance with telemedicine, expanding digital health-insurance distribution among urban families.

- December 2024: Zhibao Technology partnered with PICC and Munich Re to launch AI-based medical products tailored to middle-class needs, combining local data with global reinsurance capacity.

- October 2024: AXA rebranded its Chinese reinsurance arm to focus resources on digital channels and specialty lines.

- June 2024: Cheche Technology allied with a Nio subsidiary to co-develop usage-based motor policies powered by EV telematics.

China Online Insurance Market Report Scope

Online insurance allows the customer to buy an insurance product through online mediums from their homes without any hassles to submit physical documents. Buying insurance online is expedient, fast, and cost-effective.

China's online insurance market report aims to provide a detailed analysis of the online insurance market in China. It focuses on the market dynamics, recent trends, and insights into the online insurance market in China. It also analyses the major players and the competitive landscape. China's online insurance market is segmented by product type and by type of provider. By product, the market is further segmented into life insurance and non-life insurance. By type of provider, the market is further segmented into insurance companies, third-party administrators, and brokers.

The report offers market size and forecasts for the China online insurance market in value (USD) for all the above segments.

By Insurance Type (Value)

| Life Insurance |

| Health Insurance |

| Property & Casualty (Motor, Home, Commercial, Liability) |

| Specialty Lines (Cyber, Pet, Marine, Travel) |

By Customer Segment (Value)

| Retail / Individual |

| SME / Commercial |

| Large Enterprise / Corporate |

By Device Platform (Value)

| Mobile App |

| Desktop / Web |

| By Insurance Type (Value) | Life Insurance |

| Health Insurance | |

| Property & Casualty (Motor, Home, Commercial, Liability) | |

| Specialty Lines (Cyber, Pet, Marine, Travel) | |

| By Customer Segment (Value) | Retail / Individual |

| SME / Commercial | |

| Large Enterprise / Corporate | |

| By Device Platform (Value) | Mobile App |

| Desktop / Web |

Key Questions Answered in the Report

How large is the China online insurance market in 2026?

The China online insurance market size is USD 91.31 billion in 2026.

What is the expected growth rate through 2031?

Premiums are projected to rise at a 13.58% CAGR to reach USD 172.28 billion by 2031.

Which insurance line currently leads digital sales?

Property & Casualty products, particularly motor coverage, hold the largest share at 46.12% of premiums in 2025.

Why are super-apps critical in insurance distribution?

WeChat and Alipay embed contextual insurance offers, driving conversion rates above 15% and accounting for two-thirds of mobile transactions.

How will stricter solvency rules affect smaller insurers?

Higher capital buffers raise compliance costs, likely accelerating consolidation as under-capitalized regional carriers seek mergers or exits.

Which customer segment shows the highest forecast growth?

SME and commercial customers are expected to expand policy uptake at a 7.21% CAGR between 2026 and 2031.

Page last updated on: