Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

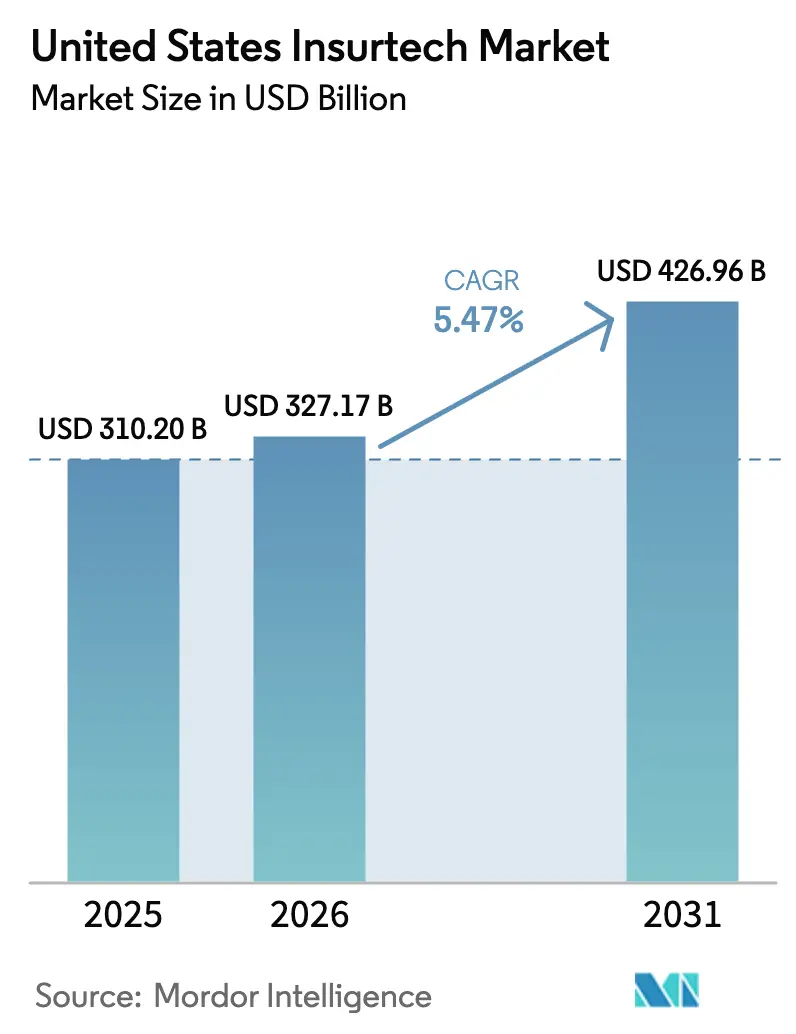

| Base Year Market Size (2025) | USD 310.2 Billion |

| Market Size (2026) | USD 327.17 Billion |

| Market Size (2031) | USD 426.96 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

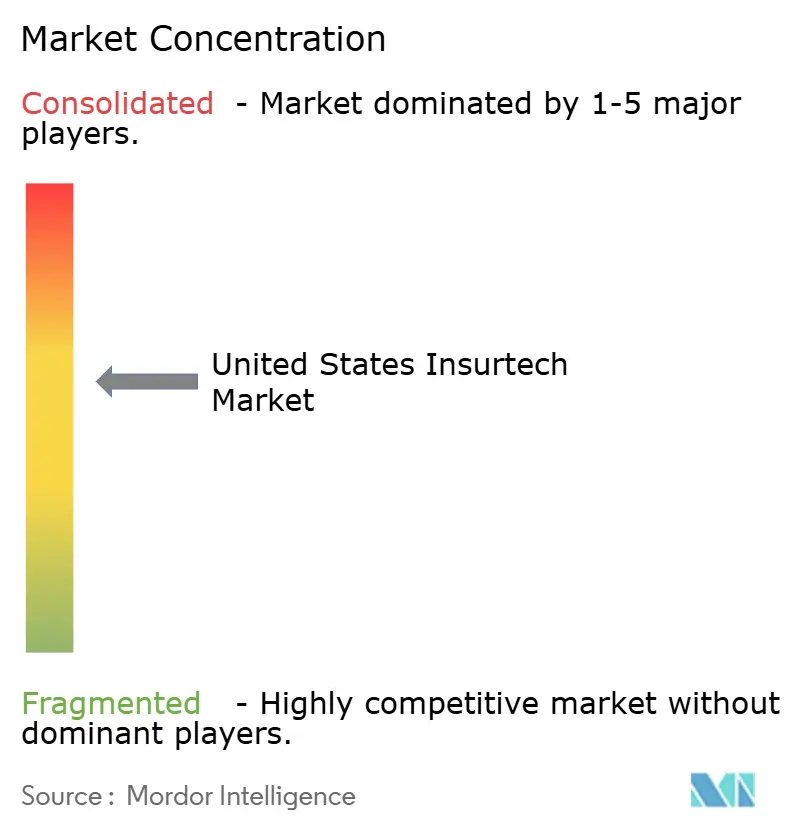

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Insurtech Market Analysis by Mordor Intelligence

The United States insurtech market size was valued at USD 310.2 billion in 2025 and estimated to grow from USD 327.17 billion in 2026 to reach USD 426.96 billion by 2031, at a CAGR of 5.47% during the forecast period (2026-2031). Robust venture funding, a widening network of regulatory sandboxes across 12 states, and the National Association of Insurance Commissioners (NAIC) Model Bulletin on artificial intelligence (AI) governance underpin this steady expansion. Carrier modernization agendas, although hampered by legacy platforms, continue to accelerate as open-API mandates facilitate seamless data exchange with fintech partners. Meanwhile, embedded-insurance partnerships are reshaping distribution economics, enabling contextual cover to be offered inside everyday financial journeys. Consolidation among reinsurers and full-stack digital carriers is redefining competitive boundaries, while climate-risk parametric products and usage-based pricing fuel product innovation speaks to evolving customer risk profiles.

Key Report Takeaways

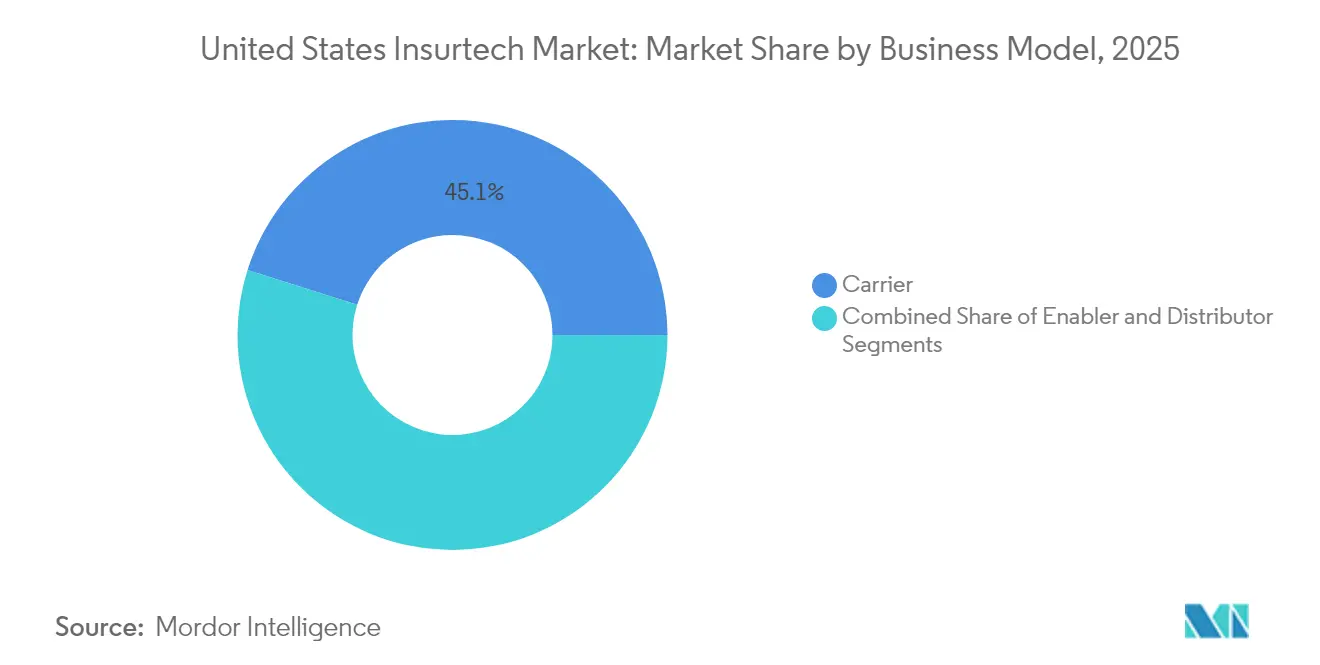

- By business model, carrier operations led with 45.12% of the United States insurtech market share in 2025; Enabler models record the highest projected CAGR at 5.74% through 2031.

- By insurance line, non-Life lines accounted for 71.65% of the United States insurtech market size in 2025 and are expanding at 6.34% CAGR through 2031.

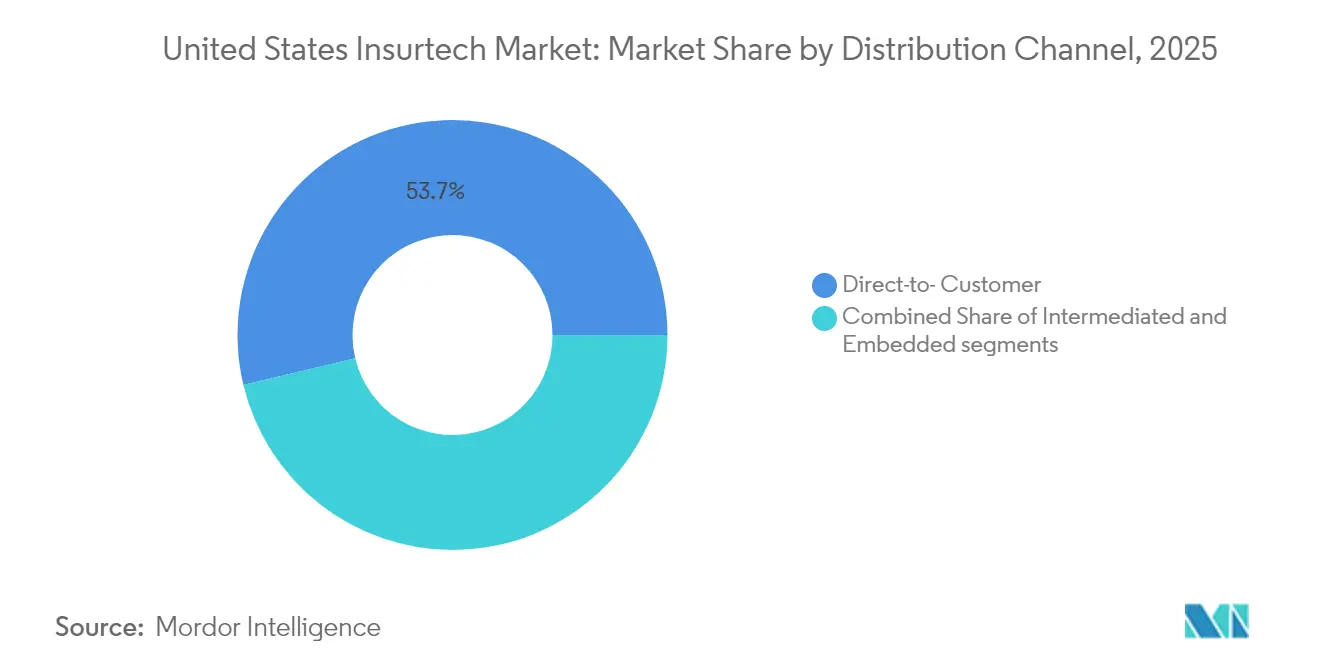

- By distribution channel, direct-to-consumer captured 53.74% revenue share in 2025, while embedded distribution is projected to grow at 5.52% CAGR to 2031.

- By geography, the Northeast region held 42.86% revenue share in 2025 and is advancing at a 6.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Insurtech Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for data analytics & AI | +1.8% | National, concentrated in Northeast & West Coast | Medium term (2–4 years) |

| Digital-first consumer purchasing | +1.2% | National, strongest in urban markets | Short term (≤ 2 years) |

| Regulatory sandbox & open-API mandates | +0.9% | State-specific, led by Kentucky, Vermont, West Virginia | Long term (≥ 4 years) |

| Embedded-insurance via open banking | +1.1% | National, early adoption in fintech hubs | Medium term (2–4 years) |

| Climate-risk parametric products | +0.7% | Regional, catastrophe-prone zones | Long term (≥ 4 years) |

| Usage-Based & Behavior-Based Pricing (UBI/BBI) | +0.8% | National, higher penetration in auto-centric regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for Data Analytics & AI

88% of US auto insurers and 70% of home insurers already deploy or pilot AI tools for loss triage and fraud prevention, prompting the NAIC to form a Third-Party Data and Models Task Force in 2024[1]National Association of Insurance Commissioners, “Third-Party Data and Models Task Force,” naic.org. Real-time risk assessment compresses quote-to-bind cycles from weeks to minutes, sharpening underwriting precision. Commercial carriers seek “agentic” AI to cope with rising claim severity and talent shortages, targeting operational expense ratios below 25%. However, Colorado’s algorithmic-bias statute and similar bills increase compliance costs, favoring well-capitalized platforms able to audit model fairness. The United States insurtech market, therefore, rewards firms that can prove explainability while sustaining predictive accuracy.

Digital-First Consumer Purchasing

Mobile-optimised journeys now dictate insurer relevance: policyholders under 40 finalise 72% of new covers on smartphones. Telematics-driven auto policies price risk dynamically, making usage-based insurance attractive as vehicle premiums rise. Fleet operators integrate GPS diagnostics with carrier APIs to negotiate real-time premiums, pushing direct-to-consumer channels toward self-service experiences. Embedded checkout flows let retailers bundle parcel protection or travel cover in a single click, reducing acquisition costs by as much as 60%. These shifts elevate customer-experience metrics above price alone and reinforce direct digital strategies within the United States insurtech market.

Regulatory Sandbox & Open-API Mandates

Kentucky, Vermont, and West Virginia administer waivers that let innovators test products on up to 10,000 customers for limited periods. Simultaneously, the Centers for Medicare & Medicaid Services’ 2024 final rule compels Medicare Advantage and Medicaid carriers to publish Patient- and Provider-Access APIs, harmonizing data standards[2]Centers for Medicare & Medicaid Services, “CMS Interoperability and Prior Authorization Final Rule,” federalregister.gov. Such openness slashes integration timelines and broadens the addressable base for policy-as-code concepts. Yet a patchwork of state requirements forces multistate players to juggle disparate approval cycles, raising legal spend and slowing nationwide rollouts.

Embedded-Insurance via Open Banking

Open-banking integrations allow credit-card issuers and neobanks to embed micro-cover in checkout flows, elevating total addressable property-and-casualty premiums. One Inc’s partnership with U.S. Bank illustrates how payment gateways and real-time premium funding converge, improving claims disbursement speed. Chubb Studio’s more than 150 embedded alliances reach over 100 million users, showcasing the scale advantage of API-first architectures[3]Chubb, “Chubb Studio Embedded Insurance Platform,” chubb.com . Channel conflicts persist as agents resist disintermediation, but early adopters view embedded distribution as a means to broaden protection without layering additional sales friction.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & cyber-breach risk | -1.4% | National, heightened scrutiny in California & New York | Short term (≤ 2 years) |

| Legacy-system integration costs | -1.1% | National, acute for established carriers | Medium term (2–4 years) |

| Actuarial data-science talent gap | -0.8% | National, centred in metro areas | Long term (≥ 4 years) |

| Scrutiny on algorithmic bias | -0.6% | State-specific, led by Colorado & California | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & Cyber-Breach Risk

The Change Healthcare intrusion compromising 100 million individuals underscores the vulnerability of interconnected claims workflows. Similar incidents at Globe Life’s customer portal prompted swift regulatory review under California’s Consumer Privacy Act, highlighting the possibility of multimillion-dollar fines. Heightened scrutiny obliges insurtechs to implement zero-trust architectures, multi-factor authentication, and annual penetration testing that can absorb up to 10% of operating expenditure. Investor sentiment remains positive toward cyber-resilience leaders, but valuation discounts emerge for platforms perceived as lagging on privacy assurance.

Legacy-System Integration Costs

Roughly three-quarters of large carriers still run policy and billing cores installed before 2010, complicating API orchestration. Modernization programs frequently exceed USD 200 million and stretch three-plus years, diluting near-term returns. Data migration obstacles and skills gaps prolong payback horizons; insurers unable to harmonize historical data see analytics benefits delayed. Consequently, enabler-model vendors flourish by delivering cloud microservices that interoperate with COBOL-based systems, providing a pragmatic bridge from legacy to digital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Carriers Drive Scale While Enablers Accelerate Innovation

Carrier platforms accounted for 45.12% of the United States insurtech market share in 2025, reflecting the enduring importance of capital strength and claims infrastructure. Enabler vendors, though smaller in absolute revenue, register the fastest progress with a 5.74% CAGR, suggesting that asset-light SaaS toolkits resonate with incumbents seeking rapid modernisation. The United States insurtech market size attributed to Enablers is projected to advance from roughly USD 14.4 billion today to more than USD 20.1 billion by 2031, as API orchestration, low-code product factories, and fraud analytics engines become plug-and-play essentials.

Strategic deals validate the trend: Munich Re entered full-stack operations by announcing a USD 2.6 billion purchase of Next Insurance in March 2025, while Travelers moved into cyber-specialty with its agreement to acquire Corvus. Such moves blur the carrier-enabler divide, shifting focus toward control of customer data and underwriting algorithms. Enablers leverage multi-tenant architecture to serve numerous carriers simultaneously, yielding superior marginal economics and positioning them as indispensable partners throughout the United States insurtech market.

By Insurance Line: Non-Life Dominance Reflects Digital Transformation Readiness

Non-Life products accounted for 71.65% of the U.S. insurtech market in 2025 and are projected to grow at a 6.34% CAGR through 2031, largely fueled by property-and-casualty offerings that leverage telematics, IoT-enabled devices, and parametric triggers for real-time claims automation. These technologies not only reduce fraud but also enable more precise risk pricing. As automation deepens, carriers are investing in API-driven distribution models that improve quote-to-bind times and enhance user experience. In contrast, life and annuity segments—though smaller in market share—are gaining traction through faster, tech-enabled underwriting and the rising appeal of instant-issue policies that resonate with digital-first consumers.

Product innovation is reshaping insurance architecture: parametric solutions for wildfires, hurricanes, and event cancellations now offer instant payouts once pre-agreed conditions are met, streamlining processes and easing pressure on claims teams. This model also supports faster capital recycling for insurers, enhancing overall operational agility. On the life side, insurers are piloting simplified underwriting for policies up to USD 3 million without requiring medical exams, lowering acquisition costs by double digits while meeting the preferences of younger, tech-savvy policyholders. Together, these trends are expanding insurability, broadening market access, and reinforcing long-term growth in the United States insurtech ecosystem.

By Distribution Channel: Direct Models Lead While Embedded Approaches Gain Momentum

Direct-to-Consumer sales maintained a 53.74% share of the United States insurtech market in 2025 as mobile quoting, instant payment, and digital claims continue to resonate with customers seeking convenience. API-driven funnels create frictionless onboarding and transparent pricing to differentiate carriers competing primarily on experience rather than solely on rate. Personalization tools, such as AI-powered recommendation engines, further enhance D2C channels by tailoring coverage to individual risk profiles. Additionally, digital self-service portals and chatbots have reduced service costs while increasing engagement, reinforcing customer preference for direct, tech-enabled interactions.

Embedded distribution, however, posts the fastest 5.52% CAGR, illustrating how insurance becomes an unobtrusive component of broader retail, travel, and lending journeys. Cross-selling potential is significant: grocery-delivery customers can activate parcel-protection cover, or ride-hail drivers can toggle on-demand auto policies from the same wallet application. Fintechs and e-commerce platforms are increasingly acting as insurance conduits, integrating products at natural decision points to improve conversion rates. As ecosystem partners prioritize seamless UX, the embedded route is poised to enlarge its imprint on the United States insurtech market by blending protection into everyday digital experiences.

Geography Analysis

The Northeast commands 42.86% of all United States insurtech market revenues, fuelled by dense fintech clusters in New York and Massachusetts and supportive regulatory frameworks such as New York’s Department of Financial Services cybersecurity rule. Venture-capital flows into Boston and New York doubled between 2022 and 2024, enabling early-stage proofs of concept that quickly migrate into production pilots with incumbent carriers. Rapid adoption of AI-enabled underwriting bolsters regional momentum, lifting forecast CAGR to an above-average 6.61%.

Although California garners more than one-quarter of the national deal count, its share of the United States insurtech market size remains lower than the Northeast due to a higher prevalence of early-stage firms with modest premium volumes. Nonetheless, Silicon Valley’s deep engineering talent and proximity to Big-Tech cloud providers sustain a pipeline of innovative risk-scoring, imagery-analysis, and blockchain pilots that often scale eastward. State privacy statutes such as the California Consumer Privacy Act shape product design and data-governance blueprints later adopted nationwide.

The South and Midwest collectively represent a growing opportunity pool. Kentucky’s innovation sandbox and Texas’ openness to managing-general-agency (MGA) formations encourage regional entrepreneurship. Clearcover’s launch of a non-standard auto MGA in Texas exemplifies the ability of digital challengers to address niche coverage gaps. Embedded insurance delivered through community banks and credit unions may further democratize access, enabling the United States insurtech market to penetrate rural segments historically underserved by traditional distribution.

Competitive Landscape

Market structure balances fragmentation and consolidation: the five largest digital-first carriers account for slightly less than one-third of written premium, while hundreds of MGAs and software providers compete on specialised niches. Recent transactions underscore a scramble for scale and data ownership. Munich Re’s Next Insurance acquisition grants a reinsurer direct access to small-business underwriting pipelines, while Travelers’ bid for Corvus adds proprietary cyber-risk scoring tools to a mainstream carrier portfolio.

Profitability remains elusive for many direct-only brands, yet Root reported its first full-year net profit in 2024 by trimming marketing spend and refining telematics pricing. Lemonade narrowed quarterly losses as its customer count approached 2.5 million. Technology enablers such as Duck Creek and Guidewire continue to expand core platform footprints inside tier-1 insurers, bundling claims-AI, digital-billing, and low-code product-assembly modules. Competitive advantage is increasingly defined by explainable-AI documentation and Model Governance maturity, a requirement formalized by the NAIC bulletin adopted in 24 states.

White-space opportunities persist in cyber protection for small-and-medium enterprises, parametric agriculture coverage, and integrated health-payment ecosystems. Players able to combine actuarial depth with cloud-native microservices command premium valuations. Incumbents counter by forming venture-capital arms and sponsoring joint development agreements, positioning themselves to absorb or partner with innovators rather than cede ground within the United States insurtech market.

United States Insurtech Industry Leaders

Root Insurance

Lemonade

Hippo

Next Insurance

Oscar Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Munich Re agreed to acquire Next Insurance for USD 2.6 billion, accelerating its direct digital-carrier capabilities. The deal strengthens Munich Re’s footprint in the U.S. SME insurance market and supports its long-term strategy to expand embedded and digitally distributed coverage solutions.

- March 2025: Ethos announced plans to explore an initial public offering with Goldman Sachs as adviser after reporting 50% revenue growth in 2024.

- January 2025: Nationwide agreed to purchase Allstate’s employer stop-loss unit for USD 1.25 billion, expanding group-benefits scale. The acquisition enhances Nationwide’s position in the self-funded health benefits space and diversifies its overall employee benefits portfolio.

- October 2024: Liberty Mutual Reinsurance and AIR Parametric introduced Milkshake™ heat-stress cover for US dairy producers.

United States Insurtech Market Report Scope

Insurtech refers to technological innovations that are created and implemented to improve the efficiency of the insurance industry. Insurtech powers the creation, distribution, and administration of the insurance business. Macro trends have been driving change in the insurance risk landscape. And along with coping with new and emerging risks, the industry began to shift, in recent years, to include new business models and disruptive newcomers. The United States insurance market can be segmented by the types of insurance provided, which include life and non-life, and by a business model, which includes enabler, carrier, and distributor.

The report offers the value (in USD) for the above segments.

By Business Model

| Carrier |

| Enabler |

| Distributor |

By Insurance Line

| Life |

| Non-Life |

By Distribution Channel

| Direct to Consumer |

| Intermediate |

| Embedded |

By Geography

| South |

| West |

| Midwest |

| NorthEast |

| By Business Model | Carrier |

| Enabler | |

| Distributor | |

| By Insurance Line | Life |

| Non-Life | |

| By Distribution Channel | Direct to Consumer |

| Intermediate | |

| Embedded | |

| By Geography | South |

| West | |

| Midwest | |

| NorthEast |

Key Questions Answered in the Report

How large is the United States insurtech market in 2026?

The United States insurtech market is valued at USD 327.17 billion in 2026 and is on track to reach USD 426.96 billion by 2031.

Which business model is growing fastest in the United States insurtech industry

Enabler-model vendors, which sell API-driven technology to incumbent carriers, are expanding at a 5.74% CAGR, outpacing both full-stack carriers and distribution-only models.

Why is the Northeast region so dominant?

The Northeast commands 42.86% revenue share because of dense fintech clusters, strong venture funding, and progressive regulatory frameworks that accelerate product pilots.

What are the top restraints on United States insurtech market growth?

Heightened cybersecurity risks and high legacy-system integration costs together subtract roughly 2.5 percentage points from potential CAGR.

Page last updated on: