Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

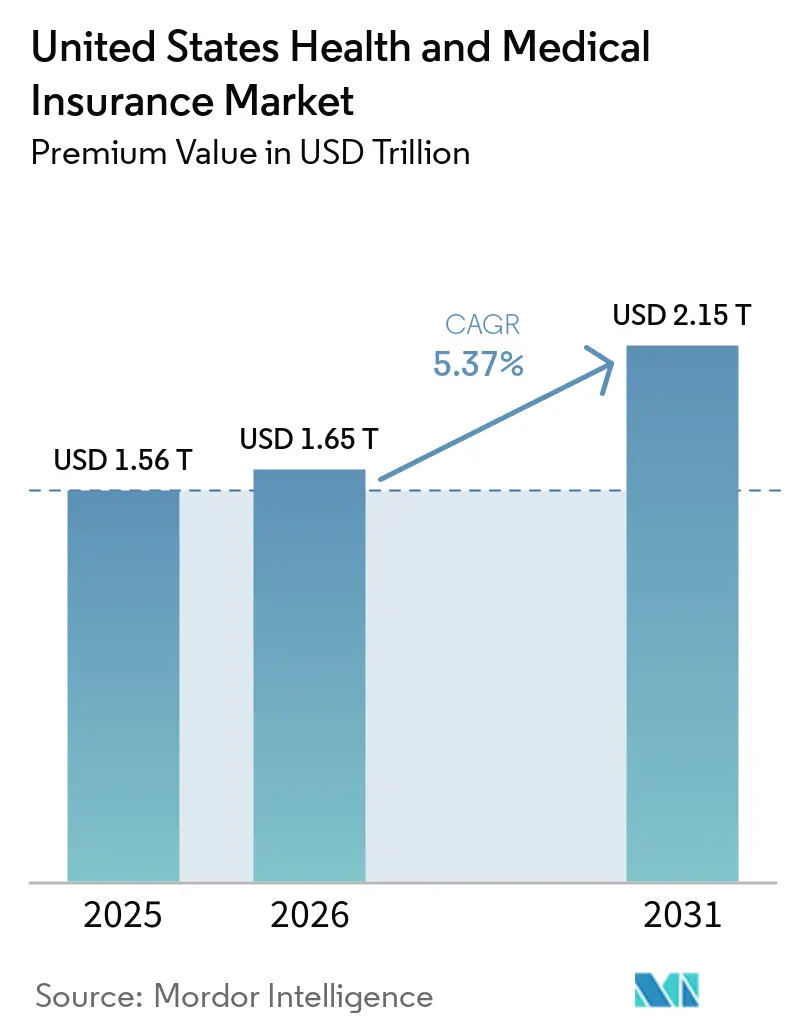

| Base Year Market Size (2025) | USD 1.56 Trillion |

| Market Size (2026) | USD 1.65 Trillion |

| Market Size (2031) | USD 2.15 Trillion |

| Growth Rate (2026 - 2031) | 5.37% CAGR |

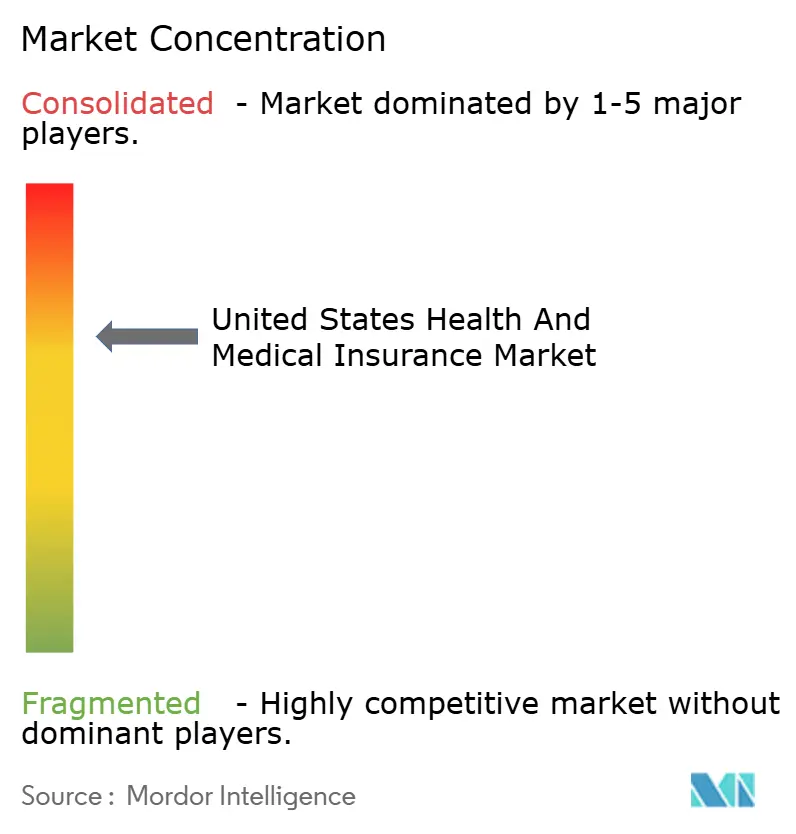

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Health and Medical Insurance Market Analysis by Mordor Intelligence

The United States Health And Medical Insurance Market size in terms of premium value is expected to increase from USD 1.56 trillion in 2025 to USD 1.65 trillion in 2026 and reach USD 2.15 trillion by 2031, growing at a CAGR of 5.37% over 2026-2031.

Growth is reinforced by large-scale marketplace enrollment under the Affordable Care Act, as well as the structural shift of Medicare beneficiaries into Medicare Advantage plans, which has tightened competition on pricing and benefit design across the United States' health and medical insurance market. National carriers are consolidating in profitable lines while exiting weaker geographies, creating openings for regionally focused not-for-profit plans and provider-sponsored entrants that target service gaps with niche product designs in the United States' health and medical insurance market. Employers are pushing more consumer cost sharing through high-deductible designs and HSA-enabled strategies, while public programs continue to test rate containment and selective contracting. Plan economics are being reshaped by medical trends led by GLP-1 drug utilization and specialty pharmacy, which is moving faster than premium increases and pushing carriers toward tighter utilization management and narrower networks. Regulatory updates on HIPAA security, telehealth reimbursement, and potential changes to tax credits add short-term volatility to demand, especially in individual coverage and small group segments, where the United States health and medical insurance market is more price sensitive.

Key Report Takeaways

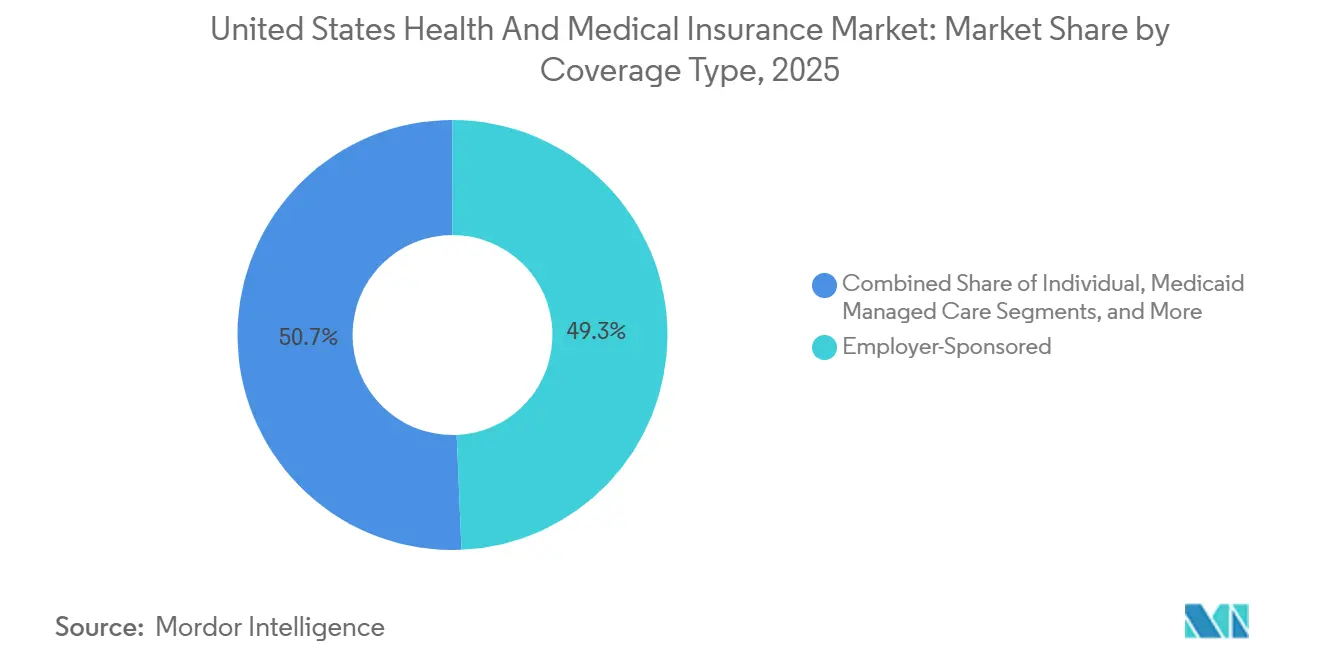

- By coverage type, employer-sponsored insurance led with 49.33% market share in 2025, while Medicare Advantage is forecasted to expand at a 9.73% CAGR from 2026 to 2031.

- By plan type, preferred provider organizations held a 48.35% share in 2025, while high-deductible health plans paired with HSAs are projected to grow at an 11.38% CAGR through 2031.

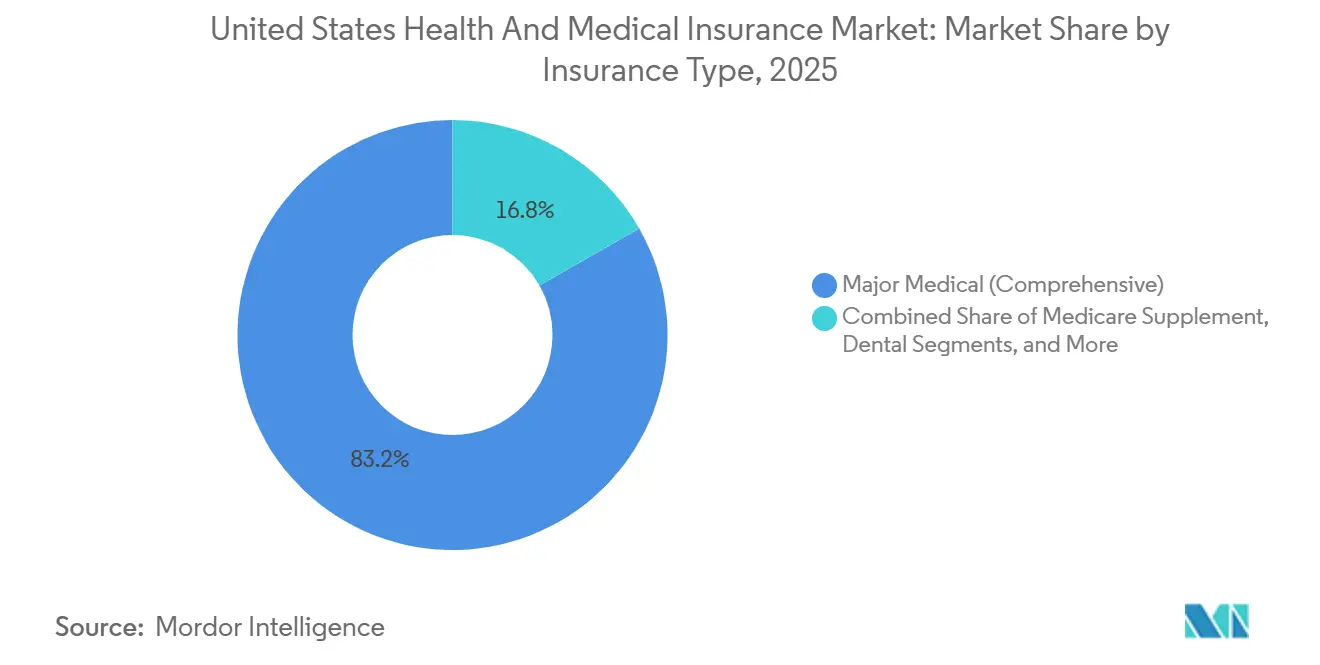

- By insurance type, comprehensive major medical accounted for an 83.24% share in 2025, and other ancillary products are expected to register a 12.24% CAGR from 2026 to 2031.

- By distribution channel, traditional brokers and agents controlled a 57.39% share in 2025, while online marketplaces and exchanges are projected to scale at a 14.78% CAGR through 2031.

- By geography, the South held a 38.35% share in 2025, and the West is forecasted to be the fastest-growing region at an 8.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Health and Medical Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising healthcare costs & aging population | +1.8% | National, with acute pressure in the Northeast and West coastal markets | Long term (≥ 4 years) |

| Expansion of ACA subsidies & Marketplace enrollment | +1.2% | National, with early gains in non-expansion states including TX, FL, GA | Medium term (2-4 years) |

| Growth in Medicaid managed care adoption by states | +0.9% | The South region, with spill-over to the Midwest expansion states | Medium term (2-4 years) |

| Employers, ICHRAs, and QSEHRAs shifting coverage to the individual market | +0.7% | National, concentrated in mid-market employers with 50-199 employees | Long term (≥ 4 years) |

| AI-driven risk stratification enabling micro-insurance offerings | +0.5% | North America and EU early adopters, with initial deployment in MA and commercial segments | Long term (≥ 4 years) |

| Permanent telehealth reimbursement parity expanding virtual-care coverage | +0.6% | National, with pronounced impact in rural and underserved geographies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Healthcare Costs & Aging Population Fuel Coverage Expansion

Medical trend remains elevated in 2026, with carriers pointing to GLP-1 uptake and specialty drug costs that supported the largest ACA rate filings since 2018, reflected in a median requested increase for 2026 Marketplace plans. This demographic shift intersects with sustained medical cost inflation-insurers reported an 18% median proposed rate increase for 2026 ACA Marketplace plans, the largest since 2018, driven by GLP-1 drug utilization, specialty medication proliferation, and provider consolidation that elevates contracted reimbursement rates[2]Matt McGough et al., “How Much and Why ACA Marketplace Premiums Are Going Up in 2026,” Peterson-KFF Health System Tracker, healthsystemtracker.org. If enhanced premium tax credits do not extend, modeling points to higher gross benchmark premiums in 2026 and a multi-year trajectory of premium growth as healthier individuals exit, which reshapes the risk pool in the United States health and medical insurance market. In Medicare Advantage, carriers are moving members toward HMO structures to strengthen referral controls and align cost management with narrower networks, an approach reflected in broad HMO access for beneficiaries in 2026. Plans are also adjusting supplemental benefits and product features to absorb revenue headwinds from the V28 risk-adjustment transition and are reallocating dollars from lower-value benefits to sustain actuarial balance under the new model.

ACA Marketplace Enrollment Doubling Creates Individual Market Momentum

ACA Marketplace enrollment more than doubled from 11 million in 2020 to over 24 million in 2025, powered by the American Rescue Plan's elimination of the 400% federal poverty level subsidy cliff and the reduction of maximum premium contributions to 8.5% of income[3]Meredith Freed et al., “Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings,” KFF, kff.org. A large share of enrollees now falls within the 100% to 150% FPL range, which increases sensitivity to premium changes if temporary credits lapse in 2026 and may compress the United States health and medical insurance market in the individual segment[4]Bernadette Fernandez, “Enhanced Premium Tax Credit and 2026 Exchange Premiums: Frequently Asked Questions,” Congressional Research Service, congress.gov. State-based exchanges are using reinsurance and Section 1332 waiver strategies to stabilize premiums and reduce federal pass-through spending, as seen in Nevada’s public option that is expected to generate material pass-through savings over its early years. Similar initiatives in Colorado and Washington show how state-led designs that cap reimbursement levels and set premium targets can build enrollment in products that compete on price without eroding network adequacy. These strategies underpin a more resilient individual market if federal support becomes intermittent, although the near-term adjustment to the subsidy cliff remains a headwind in the United States health and medical insurance market.

Medicaid Managed Care Reaches Saturation as States Navigate Post-PHE Acuity Mismatch

Most states now rely on Medicaid managed care to deliver benefits to the majority of enrollees, and capitation frameworks are adapting to changing acuity profiles following the end of continuous coverage under the PHE, which reshaped the remaining membership risk mix. State budget managers expect higher outlays in FY 2026 driven by rate adjustments, specialty pharmacy costs, and behavioral health needs, even as overall Medicaid enrollment stabilizes. Contracting decisions reflect pressure on plan performance and network standards, as seen in Louisiana’s decision to end one large carrier’s contract ahead of 2026 and redistribute members across remaining MCOs[5]Louisiana Department of Health, “LDH Announces Update to Medicaid Managed Care Contracts for 2026,” Louisiana Department of Health, ldh.la.gov. Federal policy changes included in recently enacted legislation will add new program rules such as work requirements and more frequent redeterminations for expansion adults, which may push enrollment down and raise the uninsured rate after 2026. These shifts contribute to operational complexity in the United States health and medical insurance market and keep managed care rate adequacy in focus through the forecast period.

Employer ICHRAs & QSEHRAs Shifting Coverage to Individual Market

Individual Coverage HRAs offer fixed allowances that employees apply to marketplace plans, delivering predictable employer expense and broad plan choice that boosts satisfaction, per early adopters in professional services and tech sectors. Adoption remains in early stages but is scaling as platforms simplify compliance and enrollment, potentially re-routing a meaningful slice of group lives into the individual exchange by decade-end. Insurers are adapting with portable network designs and concierge navigation to preserve experience and control risk.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty around ACA subsidy extension | -0.8% | National, with acute pressure in states without state-level subsidies | Short term (≤ 2 years) |

| Rising medical loss ratios are squeezing insurer margins | -0.6% | National, with concentrated pressure in the MA, Medicaid, and ACA segments | Medium term (2-4 years) |

| State-level public-option initiatives are intensifying price competition | -0.3% | Western states, including CA, NV, WA, and CO, with possible Midwest expansion | Medium term (2-4 years) |

| Escalating cybersecurity and data-privacy compliance costs | -0.4% | National, with a disproportionate burden on smaller regional carriers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ACA Subsidy Cliff Threatens to Reverse Individual Market Gains

The scheduled lapse of enhanced ACA premium tax credits as of January 1, 2026, restores the 400% FPL eligibility cap and increases required premium contributions across income bands, which raises out-of-pocket premiums for subsidized households and pressures retention in the United States health and medical insurance market. Pricing for 2026 exchange plans reflects expectations of higher adverse selection if the credits are not extended and incorporates broader medical trend pressures observed in rate filings for 2026. Surveys show many enrollees have limited ability to absorb higher monthly payments, a factor that could reduce take-up among middle-income households if offsets are not available. Some state-based exchanges have contingency measures funded through Section 1332 pass-through dollars, but states on the federal platform lack such backstops, which may widen geographic disparities in affordability. The near-term risk is a smaller and less balanced risk pool in individual coverage, with downstream effects on plan design, network composition, and pricing strategies across the United States health and medical insurance market.

Medical Loss Ratio Pressure Forces Plan Design Austerity Across Segments

Aggregate medical loss ratios moved higher through 2025, which narrowed administrative margins and limited headroom for care management investments and distribution expense in regulated lines. Carriers have increased focus on vertical integration and alignment with affiliated providers because that structure can redirect claims dollars to owned entities while remaining within MLR requirements, although this approach draws scrutiny from regulators and consumer advocates. Public data show MLR rebates remain a discipline mechanism in individual lines, while administrative ratio pressures are tighter in group and MA segments due to minimum thresholds and quality bonus dynamics. Cost inflation from specialty drugs and new therapeutics like GLP-1s has outpaced premium growth in recent periods, which further compresses margins unless utilization controls and formulary strategies are tightened. These conditions keep plan sponsor premiums on an upward trajectory and sustain pressure on benefit designs across the United States health and medical insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: Medicare Advantage Velocity Reshapes Government Program Economics

Employer-sponsored insurance led with a 49.33% share in 2025 of the United States health and medical insurance market, reflecting large employer inertia, Section 125 tax treatment, and the use of broad networks to support workforce retention despite rising plan costs. Medicare Advantage is projected as the fastest-growing coverage type at a 9.73% CAGR from 2026 to 2031, which cements MA as a core growth engine within the United States health and medical insurance market size as older adults shift from fee-for-service Medicare into coordinated products. Growth aligns with benefit stability under 2026 payment updates, continued access to behavioral health telehealth, and the expansion of chronic and dual-eligible special needs plans that target higher-acuity cohorts with care coordination models. The ACA individual market doubled membership from 2020 to 2025 under enhanced subsidies, but pending policy shifts introduce uncertainty in retention if subsidies remain lapsed beyond 2026. Medicaid managed care holds a stable enrollment base after the end of continuous coverage, with state capitation approaches adjusting to revised acuity and utilization profiles.

Medicare Advantage’s momentum is supported by the demographic shift and by the share of beneficiaries enrolled in MA surpassing half of eligible Medicare members, a threshold that reinforces competitive intensity in plan design and quality performance. Carriers are leaning toward HMO structures to reinforce utilization controls through primary care gatekeeping and to align network economics with lower premiums for price-sensitive members. Star Ratings changes for 2026, and risk-adjustment model updates are prompting targeted investments in HEDIS measures and experience scores to sustain quality bonus payments over the medium term. Military, government, and other public programs continue steady enrollment linked to statutory eligibility and appropriations, with limited volatility relative to commercial lines. These dynamics collectively sustain a mixed demand profile across the United States health and medical insurance market, where government programs set the pace of growth while employer groups carry the largest premium base.

By Plan Type: Consumer-Driven Models Surge as Employers Shift Financial Risk

Preferred provider organizations held 48.35% of 2025 enrollment, underscoring member preference for broader access and the willingness of employers to fund flexibility when the labor market is tight, even as PPO offerings shrink in MA lines where carriers favor HMO designs for cost control. High-deductible health plans with HSAs are expected to post the fastest growth at an 11.38% CAGR through 2031, supported by higher statutory HSA contribution limits for 2026, expanded use of price transparency tools, and employer adoption of defined-contribution philosophies that cap premium growth in the United States health and medical insurance market. HMO access in Medicare Advantage remains widespread in 2026 and aligns with benefit management strategies that emphasize primary care alignment and referral pathways. EPO and POS products serve niche preferences for network structure and price, balancing narrower networks against premium advantages in selected geographies. The United States health and medical insurance market continues to support a spectrum of plan types as carriers match benefit designs to employer and beneficiary cost-sharing preferences.

HDHP adoption has grown within employer-sponsored coverage, correlating with long-running trends in benefit cost shifting and increased availability of employer contributions to HSAs that support out-of-pocket expenses. The United States health and medical insurance industry is also adapting to state mandates for behavioral health and other categories that must be embedded into compliant plan designs, which may narrow the premium gap between HDHP and traditional plans in some states. Within Medicare Advantage, carriers are consolidating plan portfolios into structures that allow tighter formulary management and focused networks to align with MLR requirements and quality performance goals. Direct coordination with provider organizations supports plan designs that balance utilization controls with access for high-need members. As employer and MA plan portfolios evolve, the United States health and medical insurance market presents a diversified set of options that align with different price and access trade-offs.

By Insurance Type: Ancillary Products Capitalize on Consumer Out-of-Pocket Anxiety

Comprehensive major medical accounted for an 83.24% share in 2025, anchoring the core risk-bearing products regulated under federal and state rules that define benefits, actuarial value, and rating practices. Premiums filed for 2026 show heightened pressure from specialty pharmaceuticals and GLP-1 utilization, which is driving benefit adjustments and intensified utilization management in order to maintain affordability in the United States health and medical insurance market. Other ancillary products, including accident, critical illness, and hospital indemnity, are forecast to be the fastest-growing category at a 12.24% CAGR from 2026 to 2031, as employers expand voluntary benefit menus and employees seek targeted financial protection. Dental and vision continue to scale in both employer and Medicare contexts, and Medicare Supplement remains stable among higher-income retirees who value predictable cost sharing. These product dynamics illustrate how consumers are seeking layered financial protection in the United States health and medical insurance market as medical bills rise faster than wages.

Product innovation is emerging around condition-specific coverage that aligns incentives with member needs, as seen in the introduction of menopause-focused plan designs with targeted benefits and $0 cost sharing for key services in 2026. Such designs leverage data to refine benefit structures and improve perceived value for specific cohorts without broadening networks or adding unrelated benefits. Short-term medical offerings continue to face a constrained regulatory landscape at the state level, which limits their addressable market and shifts demand toward compliant ACA plans where subsidies are available. Medicare Supplement remains a stable option for traditional Medicare beneficiaries who prefer unrestricted provider choice in exchange for higher monthly premiums. Together, these shifts underscore the role of supplemental and niche products in relieving out-of-pocket exposure within the United States health and medical insurance market.

By Distribution Channel: Digital Platforms Disrupt Traditional Broker Dominance

Brokers and agents held 57.39% of distribution in 2025, reflecting the complexity of benefit design decisions for employers and Medicare beneficiaries and the continued value of human-led guidance across plan selection and year-round service. Online marketplaces and exchanges are projected to grow at a 14.78% CAGR through 2031, driven by improved decision support on state-based platforms, better integration with EDI and payroll systems, and rising ICHRA adoption that steers more households into the individual market within the United States health and medical insurance market. Emerging AI-enabled member service agents in individual plans can resolve benefit and care navigation queries using records and plan documents, which raises the standard for digital self-service. Direct-to-consumer channels remain a strong option for vertically integrated payers that own delivery assets and have no need for intermediaries, while employer benefit consultants retain a prominent role in large group segments. The United States health and medical insurance market is therefore moving toward a hybrid distribution landscape where human and digital channels coexist.

Platforms that serve ICHRA and small group employers are embedding plan recommendation engines and compliance checks to streamline enrollment, which reduces friction and improves plan matching for heterogeneous workforces. Medicare Advantage distribution continues to support agent-assisted enrollment, given the complexity of plan features, with carriers updating incentives and plan lineups to direct members into designs that align with margin targets and network strategy. State public option programs are testing lower broker fee structures to meet premium reduction targets, which introduces new dynamics for distribution economics as more states assess those models. Online exchange tools and navigators remain important for underserved communities and for populations with complex needs who require assistance beyond a single enrollment transaction. As these shifts take hold, the United States health and medical insurance market will see more specialized roles for brokers, digital vendors, and payer-owned channels.

Geography Analysis

The South region held 38.35% share in 2025 of the United States health and medical insurance market, led by population scale in Texas and Florida, high managed care penetration in Medicaid, and strong Medicare Advantage adoption in retiree-heavy counties. State Medicaid programs in the South have leveraged managed care structures extensively, with national MCOs anchoring enrollment under Section 1115 and other authorities that direct members into comprehensive plans. Medicare Advantage penetration is among the highest in large Southern states, supported by broad HMO access and dense provider networks, which stabilize pricing while supporting narrow-network products. The United States health and medical insurance market in the South also benefits from individual market participation, where premium subsidies have drawn households into exchange plans, with trend risk tied to the permanence of credit enhancements. Competitive dynamics include national carriers and Blues plans balancing portfolio breadth with targeted exits from less profitable counties to align with network and medical cost realities.

The West is projected as the fastest-growing region at an 8.66% CAGR for 2026 to 2031 in the United States health and medical insurance market, supported by state policy measures that focus on rate containment and exchange competition. California sustains significant membership through Medi-Cal and exchange coverage, supported by state-level subsidy and enrollment policies that limit disruption from federal program changes. Nevada, Washington, and Colorado have adopted public option frameworks that tie premium targets to reimbursement controls, which have spurred enrollment and federal pass-through savings in early years of implementation. Western markets also feature prominent integrated delivery systems that align plan and provider operations, which support HMO-led MA strategies with controlled cost structures. These structural attributes support sustained growth in the United States health and medical insurance market across Western states through the forecast period.

The Midwest and Northeast present mixed patterns that reflect regulatory intensity and provider market structure in the United States health and medical insurance market. The Midwest exhibits stability anchored by Blues plans with strong employer and individual presence, with Medicaid expansion and managed care frameworks that continue to evolve under state budget constraints. The Northeast registers higher average exchange benchmark premiums, which mirror concentrated provider markets, community rating rules, and certificate-of-need regulations that add cost pressure. Robust oversight, such as independent external review programs, can shift claims outcomes in favor of members more often, which affects carrier utilization management strategies and appeals processes. In both regions, the United States health and medical insurance market depends on careful rate setting and differentiated plan designs to balance affordability with network adequacy requirements.

Competitive Landscape

The United States health insurance market demonstrates high concentration with moderate fragmentation in local segments where regional Blues plans and provider-led health systems maintain a strong share. UnitedHealth Group and Humana together hold a large portion of MA enrollment, and the broad top tier of national carriers, including CVS Health, Elevance, and Centene, retain scale across government and commercial lines while rationalizing county footprints for 2026. Competitive intensity diverges by line of business, with the ACA Marketplace showing strong price competition in multi-carrier counties, while MA dynamics are shaped by annual payment updates, Star Ratings, and risk-adjustment changes. State public option initiatives in the West introduce a new competitive axis where premium reduction targets guide benefit and reimbursement structures and reshape distribution economics. Vertical integration remains a core strategy to balance MLR requirements with care delivery alignment, while selective exits and plan consolidations are used to manage underperforming product lines.

Digital-native insurers are scaling technology-enabled models to capture underserved niches in the United States health and medical insurance market. Oscar Health expanded for plan year 2026 across 573 counties in 20 states and launched an AI-enabled support agent and menopause-focused plan design that offers targeted benefits with $0 copays for key services. Clover Health continues to deploy its clinical decision support platform in primary care to raise diagnosis and care initiation rates in MA, with supporting evidence that technology-enabled workflows can improve risk capture and chronic disease management. Integrated delivery systems continue to expand regionally, as seen in Kaiser Permanente’s joint venture in Nevada that adds a new geography to its coordinated care footprint, which supports HMO-led strategies and aligned pharmacy and lab services. These models increase the diversity of approaches to benefit design, network, and service that define the United States health and medical insurance market.

Technology investment is a key differentiator as payers upgrade utilization management, prior authorization, and claims adjudication to address rising denials and higher clinical complexity. The NAIC’s 2025 survey reported that a large majority of health insurers already use AI or ML, with deployment concentrated in utilization management and prior authorization, while full automation of denial decisions remains limited due to governance and oversight expectations. Policy frameworks continue to evolve, with sector guidance emerging on responsible AI use and risk management that will shape vendor selection and internal governance in 2026. Carriers are applying these tools to move from retrospective review toward prepayment clinical validation and straight-through processing where appropriate, which aims to lower administrative costs and accelerate accurate payment. As adoption expands, the United States health and medical insurance market will likely see measured gains in efficiency and improved member service where AI supports clear and explainable decisions. The net effect is a slow but steady modernization of payer operations to keep pace with medical trends and regulatory scrutiny.

United States Health and Medical Insurance Industry Leaders

UnitedHealth Group

CVS Health (Aetna)

Elevance Health (Blue Cross Blue Shield)

Cigna Group

Humana

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Health Net and Centene announced expanded Medicare Advantage and PDP options for 2026 in California, increasing available plans and access for seniors and boosting plan choices across multiple counties.

- November 2025: Wellcare by Centene and Health Net launch expanded Medicare Advantage and Prescription Drug Plans for 2026, offering coverage to more than 51 million beneficiaries nationwide with enhanced benefits and plan options.

- October 2025: Oscar Health expanded its health insurance coverage to 573 counties across 20 U.S. states for the 2026 open enrollment period and introduced new AI-enabled member support tools, including the Oswell personal AI agent and the HelloMeno menopause-focused plan.

- August 2025: UnitedHealth Group completed its USD 3.3 billion acquisition of home health provider Amedisys, making Amedisys a wholly owned subsidiary of UnitedHealth’s Optum division after resolving antitrust concerns and regulatory reviews.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the United States health and medical insurance market as all written premiums, public or private, covering medically necessary services delivered inside the fifty states, the District of Columbia, and U.S. territories. Benefits considered include inpatient and outpatient care, prescription drugs, preventive services, long-term managed care, and supplemental gap products that attach to major medical plans.

Scope Exclusions: stand-alone discount cards, excepted benefit indemnity plans, and international travel policies are excluded from our sizing.

Segmentation Overview

- By Coverage Type

- Employer-Sponsored

- Individual (ACA / Non-Group)

- Medicaid Managed Care

- Medicare Advantage

- Military / Government (TRICARE, VA, FEHBP)

- By Plan Type

- HMO

- PPO

- EPO

- POS

- HDHP / Consumer-Driven

- By Insurance Type

- Major Medical (Comprehensive)

- Medicare Supplement

- Dental

- Hospital Indemnity / Limited Benefit

- Vision

- Short-Term Medical

- Other Ancillary (Accident, Critical Illness)

- By Distribution Channel

- Direct to Consumer

- Brokers & Agents

- Employer Benefit Consultants

- Online Marketplaces / Exchanges

- By Region

- Northeast

- Midwest

- South

- West

Detailed Research Methodology and Data Validation

Primary Research

Multiple semi-structured interviews with carrier actuaries, brokers, hospital finance leaders, and state regulators helped us pressure test loss ratio assumptions, enrollment elasticity, and average premium paths across regions. These conversations, spanning all four census regions, also verified early findings on Medicare Advantage penetration and employer contribution strategy shifts.

Desk Research

Analysts begin with authoritative public datasets such as CMS National Health Expenditure Accounts, NAIC statutory premium filings, U.S. Census Current Population Survey, and Bureau of Labor Statistics medical inflation indices. We enrich these baselines with insights from trade bodies like AHIP, Kaiser Family Foundation, and state insurance department dashboards, while corporate 10-Ks and investor decks clarify carrier level trends. Select paid repositories, notably D&B Hoovers for company revenue splits and Dow Jones Factiva for deal flow, fill remaining gaps. This source list is illustrative; numerous additional outlets were tapped for validation and nuance.

Market-Sizing & Forecasting

Our model starts with a top-down roll-up of premium collections by segment (employer, individual, Medicare Advantage, Medicaid managed care, military), adjusted to gross written terms. Selective bottom-up carrier sampling, premium and enrollment dashboards from the ten largest insurers, checks segment totals. Key variables driving the forecast include medical cost inflation, population aged 65 plus, Medicaid enrollment volumes, employer-sponsored coverage counts, and average deductible levels. Values feed a multivariate regression and scenario analysis framework that projects premiums through 2030 while accounting for policy changes and economic swings. Data voids, for instance, limited transparency in self-funded stop-loss rates, are bridged through benchmark ratios derived from primary interviews and CMS trend factors.

Data Validation & Update Cycle

Outputs undergo variance checks against CMS and NAIC time series, followed by peer review by a senior analyst team. Any anomaly above a three percent threshold triggers re-contact with domain experts. Reports refresh annually, and material events, large mergers, federal rule changes, and public health emergencies prompt interim model updates before client delivery.

Why Mordor's United States Health and Medical Insurance Baseline Commands Reliability

Published market estimates often diverge because firms pick different benefit scopes, enrollment bases, and premium definitions.

Key gap drivers include whether short-term and supplemental products are counted, how aggressively discounted ASPs are applied to Medicaid managed care, and the cadence at which data feeds are refreshed. Our analysts report a balanced base case tied to the most recent NAIC and CMS releases, whereas other publishers may adopt earlier snapshots or rely on untested carrier surveys.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.59 trillion (2025) | Mordor Intelligence | - |

| USD 1.54 trillion (2025) | Regional Consultancy A | Excludes Medicare Advantage premium flows |

| USD 1.23 trillion (2024) | Trade Journal B | Omits employer self-funded ASO equivalents and applies pre-2023 NAIC filings |

| USD 0.66 trillion (2025) | Industry Association C | Counts only individual ACA compliant and group risk business, ignoring government programs |

Taken together, the comparison shows that once scope, data timeliness, and premium definitions are equalized, Mordor's disciplined blend of public micro data and targeted bottom-up checks delivers a dependable, decision ready baseline.

Key Questions Answered in the Report

What is the current size and growth outlook for the United States health and medical insurance market in 2026?

The United States health and medical insurance market stands at USD 1.65 trillion in 2026 and is projected to reach USD 2.15 trillion by 2031, reflecting a 5.37% CAGR.

Which coverage types are leading and growing fastest in 2026-2031?

Employer-sponsored insurance leads by share at 49.33% in 2025, and Medicare Advantage is projected as the fastest-growing at a 9.73% CAGR to 2031.

How will the expiration of enhanced ACA premium credits affect enrollment and premiums?

The lapse raises required contributions and risks lower retention among subsidized enrollees, with 2026 filings reflecting higher premiums and adverse selection expectations in the individual segment.

What are the main drivers shaping demand in the United States health and medical insurance market?

Aging demographics, rising specialty drug utilization, increased Marketplace enrollment under recent subsidies, and telehealth reimbursement parity are the key drivers influencing growth.

Which distribution channels are gaining traction among employers and individuals?

Brokers and agents remain dominant by share, while online exchanges and ICHRA-enabled platforms are the fastest-growing due to better decision support and payroll integration.

How are payers deploying technology to manage costs and member experience?

Carriers are expanding AI use in utilization management and prior authorization while testing prepayment clinical validation to improve accuracy and speed of adjudication.

Page last updated on: