Insurance BPO Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

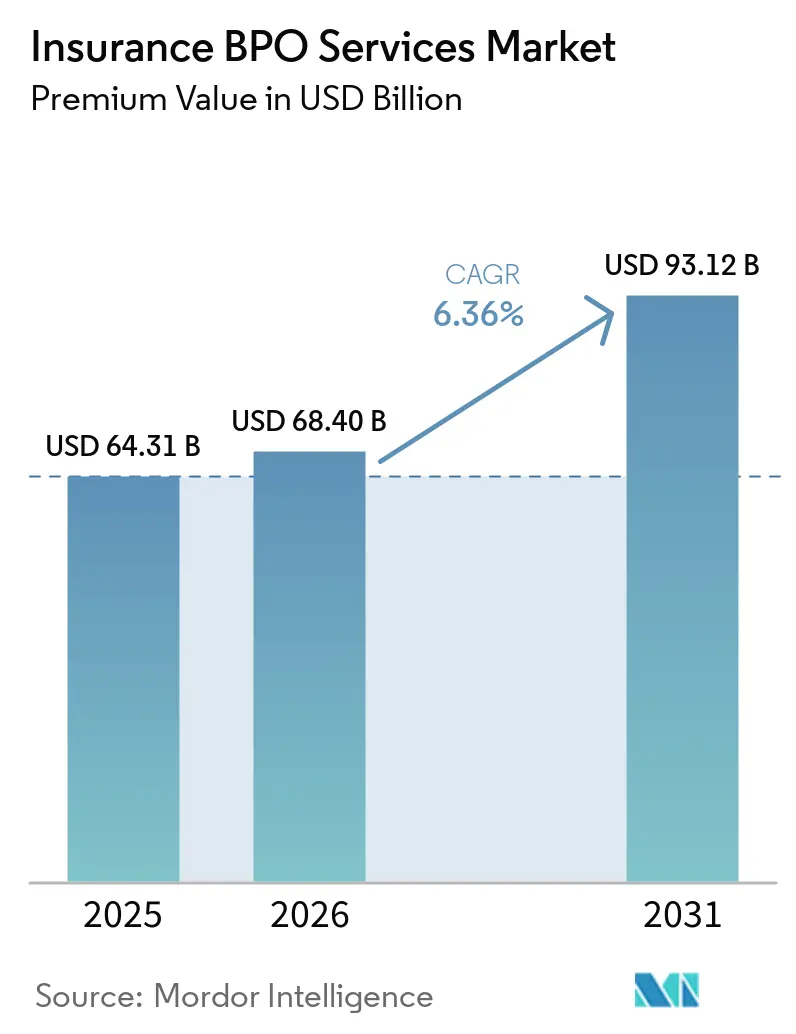

| Market Size (2026) | USD 68.40 Billion |

| Market Size (2031) | USD 93.12 Billion |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

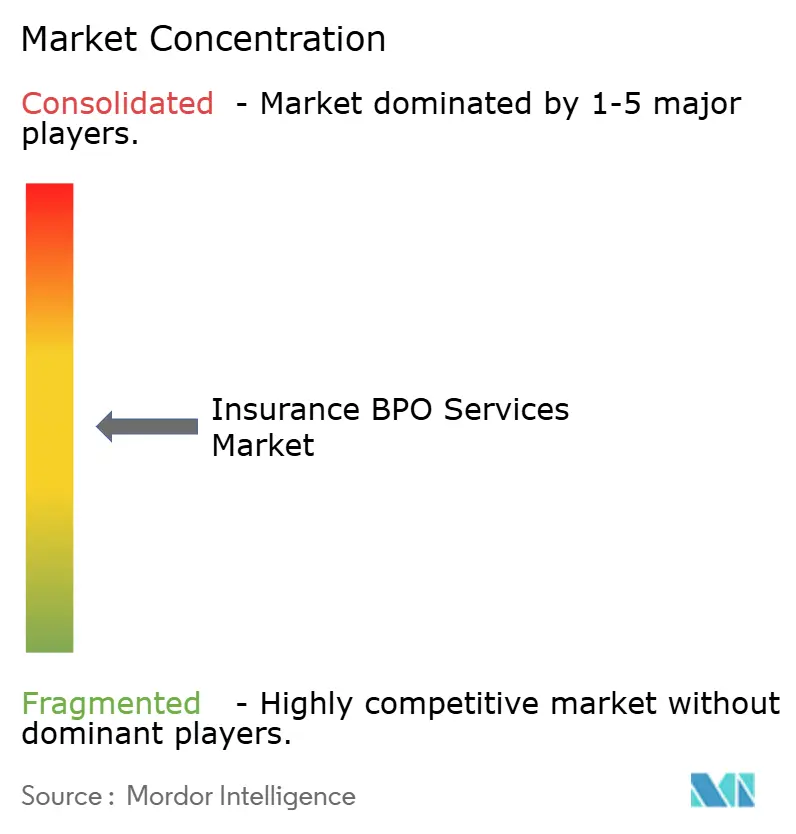

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insurance BPO Services Market Analysis by Mordor Intelligence

The Insurance BPO Services Market size in terms of premium value is projected to expand from USD 64.31 billion in 2025 and USD 68.40 billion in 2026 to USD 93.12 billion by 2031, registering a CAGR of 6.36% between 2026 to 2031.

The insurance BPO services market is propelled by carriers that are modernizing claims adjudication, policy administration, and fraud detection through automation and analytics to offset margin pressure and labor gaps. North America remains the largest buyer ecosystem given the concentration of global carriers and complex multi-state compliance needs, while Asia-Pacific is the fastest growing delivery and demand hub due to multilingual talent, expanding regulatory clarity, and maturing digital infrastructure. Vendors are embedding robotic process automation and AI decisioning into high-volume workflows to lower the total cost of ownership and improve cycle times in claims, billing, and customer support. Rising cybersecurity and privacy oversight, including third-party risk controls and mandated audits, is elevating the role of certified BPO partners that can meet encryption, access control, and incident reporting requirements while maintaining audit-ready documentation for insurers. The insurance BPO services market is also influenced by fraud-related cost exposure and the need to cut false positives, which is accelerating investment in machine learning models embedded at first notice of loss and policy servicing stages.

Key Report Takeaways

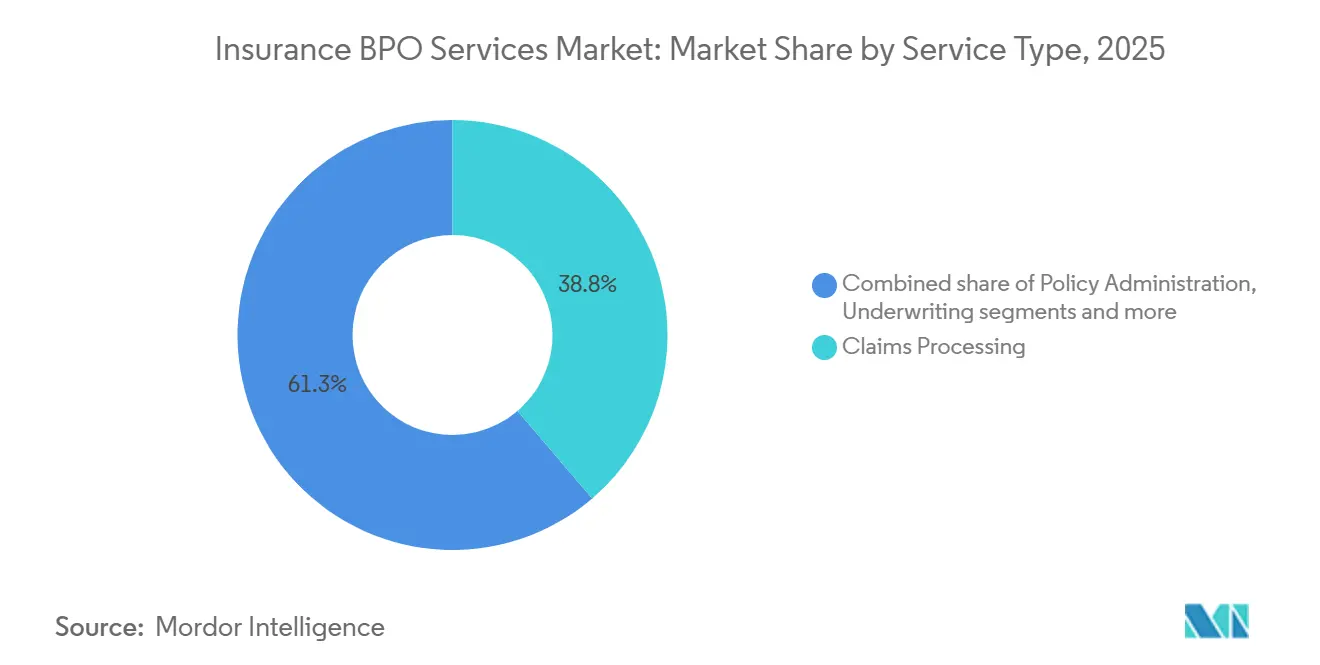

- By service type, claims processing led with 38.75% of the insurance BPO services market share in 2025, while fraud detection & analytics is projected to expand at a 7.64% CAGR through 2031.

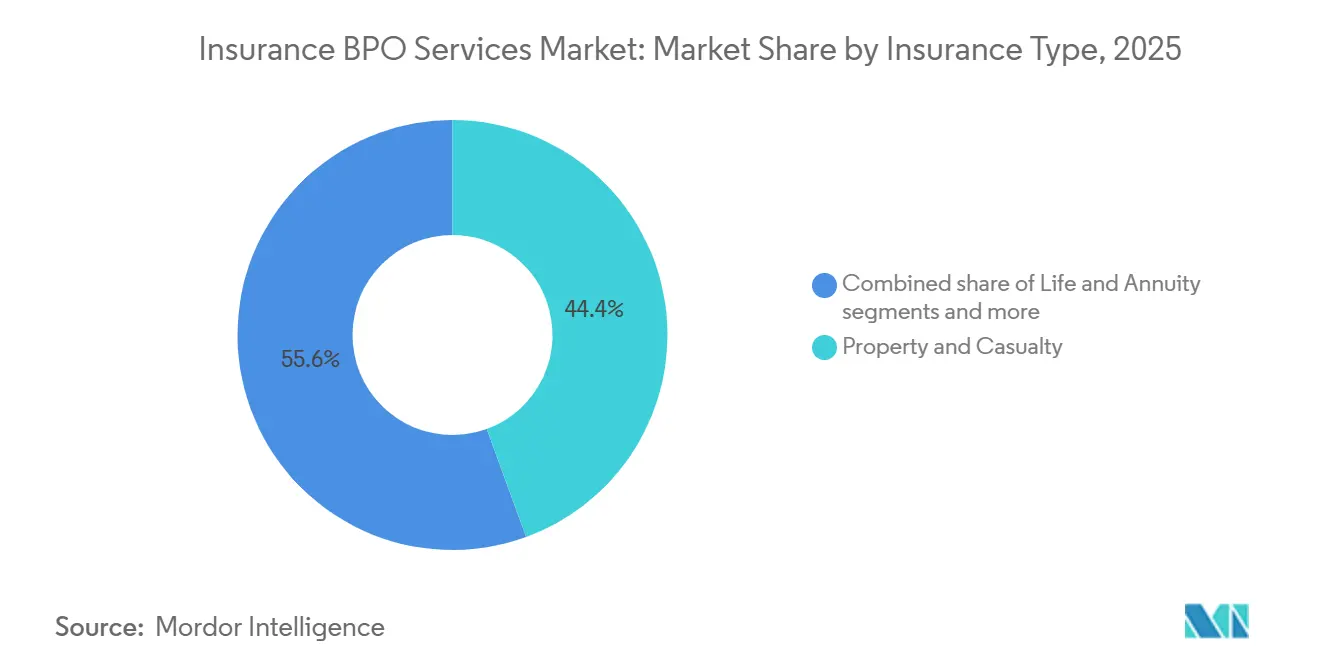

- By insurance type, property & casualty accounted for 44.43% of the insurance BPO services market share in 2025, and health is forecast to advance at an 8.27% CAGR to 2031.

- By organization size, large enterprises represented 78.32% of the insurance BPO services market share in 2025, while small & mid-sized enterprises are set to grow at a 7.57% CAGR through 2031.

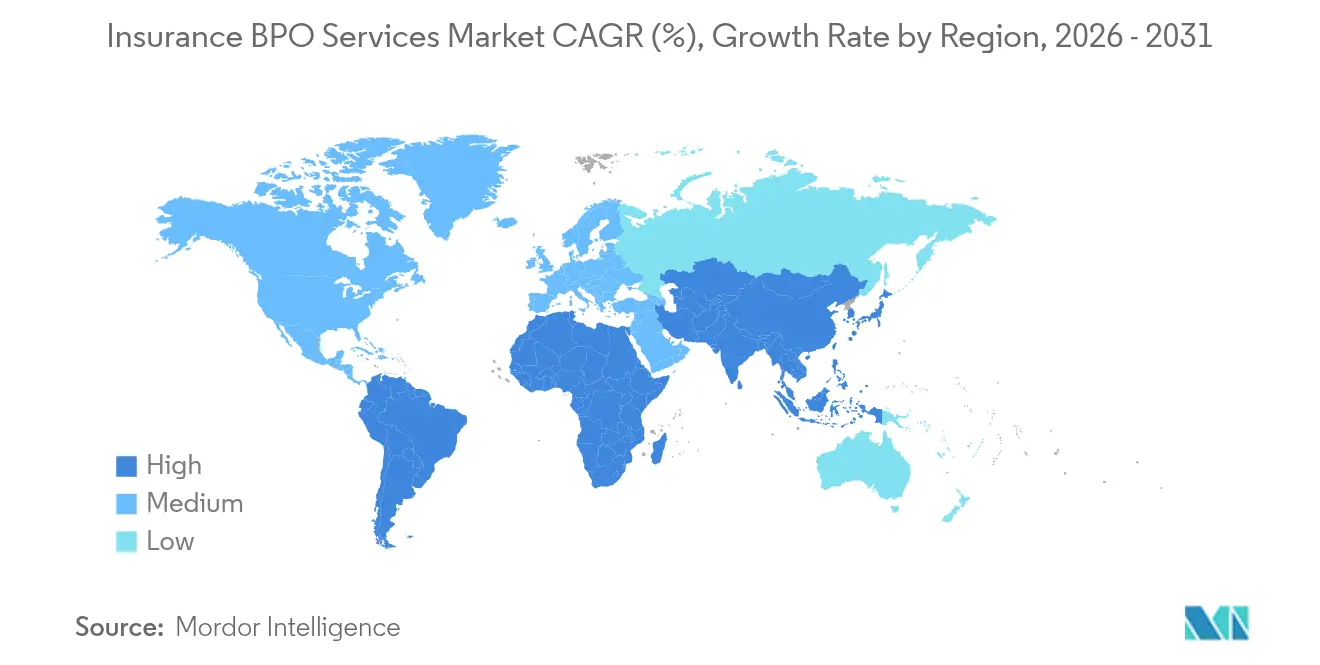

- By geography, North America held 41.19% of the insurance BPO services market share in 2025, and Asia-Pacific is projected as the fastest-growing region at a 9.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insurance BPO Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-reduction pressure & efficiency focus | +1.8% | Global, concentrated in North America & Western Europe, where carrier SG&A ratios exceed 25% | Short term (≤ 2 years) |

| Digital transformation (RPA, AI, analytics) adoption | +2.1% | Global, APAC leading adoption in greenfield centers; North America retrofitting legacy stacks | Medium term (2-4 years) |

| Core-versus-context outsourcing trend | +0.9% | North America & EMEA mature markets are rationalizing internal headcount | Medium term (2-4 years) |

| Reg-tech & compliance complexity escalation | +1.1% | North America (NAIC, state AGs), EU (GDPR, Solvency II), Asia (data localization mandates) | Long term (≥ 4 years) |

| Surge in annuity block & PRT administration volumes | +0.7% | North America & the United Kingdom, driven by defined‑benefit pension de-risking | Medium term (2-4 years) |

| Severe licensed-talent shortage in mature markets | +1.3% | North America & Western Europe (actuarial, underwriting roles aging out) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation (RPA, AI, analytics) Adoption

Insurers continue to invest in automation across document intake, policy servicing, and claims, which raises the technology baseline that BPO partners must meet to win and renew contracts in the insurance BPO services market. Straight-through processing for low complexity claims is improving through computer vision and natural language models that classify and extract unstructured content from forms, reports, and emails, which reduces manual touchpoints and handoffs in adjudication [1]Decerto Editorial Team, “Claims Processing Software: Automate FNOL to Payout in 2026,” Decerto, decerto.com. In Asia-Pacific, greenfield centers often embed AI from day one, while legacy operations in North America retrofit decisioning into existing case management stacks, creating differences in tooling and delivery models that shape partner selection. Examples from digital leaders show underwriting and claims reaching high automation rates when models are trained on insurance-specific language and patterns, which BPO vendors increasingly offer through domain-tuned platforms and secure data pipelines. Fraud detection remains a priority because it reduces false positives and improves investigator productivity, and industry estimates for fraud-linked losses continue to drive adoption of anomaly detection at first notice of loss and during payment authorization. Payments modernization and richer messaging standards like ISO 20022 also reshape billing and reconciliation workflows that BPO vendors support, improving data quality, audit trails, and exception handling in finance operations for carriers and intermediaries.

Core-Versus-Context Outsourcing Trend

Insurers are segmenting activities into core and context, retaining pricing and underwriting authority while shifting repeatable processes like certificate issuance, loss run compilation, and endorsement processing to partners that standardize and scale them across portfolios. The insurance BPO services market benefits when buyers unbundle process families and contract for outcomes like faster quote turnaround and cleaner reconciliation, which depend on playbooks and platforms that vendors refine across many clients. Managing General Agents and program administrators, which have leaner operating models, are frequent adopters of outsourced policy and claims support to preserve focus on distribution and product, especially in commercial and specialty lines reported as growth areas by trade sources. A 2024 partnership between a specialty carrier and a global BPO set up multi-tower, multi-location delivery for underwriting, reinsurance processing, finance, technology services, and an automation Center of Excellence, which illustrates how buyers blend domain and technology capabilities through managed services to accelerate modernization without large internal buildouts. As carriers shift to outcome-based pricing models, vendors accept performance risk tied to leakage reduction, cycle time, or customer experience, which moves relationships from staff augmentation toward managed transformation. This trend expands the insurance BPO services market by repositioning vendors as long-term partners embedded in target operating models rather than transactional suppliers.

Reg-Tech & Compliance Complexity Escalation

Third-party risk management rules, privacy mandates, and cybersecurity requirements are expanding in scope, and they now drive vendor selection and oversight practices that favor certified, audit-ready partners in the insurance BPO services market. New York’s Department of Financial Services has issued guidance requiring insurers to ensure third party providers implement strong cybersecurity programs aligned with Part 500, including multi factor authentication, encryption of nonpublic information, and timely incident notification, with explicit expectations for due diligence and ongoing monitoring [2]Department of Financial Services, “Industry Letter - Guidance on Managing Risks Related to Third-Party Service Providers,” dfs.ny.gov, dfs.ny.gov. In the European Union and the United Kingdom, GDPR and financial sector rules make data governance and cross-border transfers central to any outsourcing arrangement, which elevates the importance of ISO 27001 and SOC 2 certifications, penetration testing, and strict subcontractor controls managed through the vendor’s governance program. In the United States, updated California Consumer Privacy Act provisions effective in 2026 introduce mandatory cybersecurity audits for certain businesses, which will raise documentation and control expectations that BPO partners must support across systems and processes that touch insured or claimant data. South Africa’s regulators also advanced new outsourcing and cybersecurity standards for insurers, requiring board approved frameworks, annual training, incident reporting, and secure data return or destruction in vendor contracts, which strengthens compliance baselines across English language hubs that serve Europe and Africa. These developments make compliance a competitive differentiator as buyers seek partners that can operationalize privacy by design, maintain evidence for audits, and adjust workflows quickly as regulations evolve across jurisdictions.

Surge in Annuity Block & PRT Administration Volumes

Growing pension risk transfer activity and larger in-force annuity books are reshaping back office requirements for participant services, recordkeeping, payment operations, and tax reporting, which expands addressable volumes for specialized providers in the insurance BPO services market. Transferring decades-long payment and beneficiary management obligations onto life insurers requires scalable administration with strict controls for identity verification and exception handling that many carriers increasingly co-source. As life insurers scale through acquisitions and partnerships, they inherit heterogeneous systems and reporting obligations that intensify the need for standardized processes executed by partners fluent in reinsurance accounting and regulatory capital reporting. Market moves in 2025 involving pension and retirement platforms highlighted the scale and cross-border operational footprints needed to serve millions of beneficiaries, which can catalyze demand for outsourced operations to harmonize data and reporting across jurisdictions. BPO partners that combine policy administration, customer service, and finance controls on secure platforms are positioned to absorb incremental work as annuity writers add new cohorts, integrate acquired books, and redesign service metrics. The insurance BPO services market gains when life and retirement businesses prioritize operational resilience, multilingual service coverage, and audit-ready financial controls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security & privacy concerns | -1.4% | Global, acute in EU (GDPR penalties) and North America (state AG enforcement, FTC actions) | Short term (≤ 2 years) |

| Attrition & knowledge-loss risk in delivery hubs | -0.9% | APAC core (Philippines, India), spill‑over to South America nearshore centers | Medium term (2-4 years) |

| Low-code / no-code automation displacing manual tasks | -0.6% | Global, early adoption in North America and APAC tech‑forward insurers | Long term (≥ 4 years) |

| On-shoring political pressure in key buyer nations | -0.5% | National, with shifts in major economies driving hybrid delivery choices | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Security & Privacy Concerns

Escalating privacy and cybersecurity oversight requires robust controls and demonstrable compliance, which can slow new outsourcing programs and add cost for both buyers and providers in the insurance BPO services market. Insurers must verify that third-party providers implement strong cybersecurity programs aligned with regulatory frameworks, including multi-factor authentication, encryption of nonpublic information, vendor risk assessments, and incident notification protocols. Updated California privacy regulations, effective in 2026, further introduce mandatory cybersecurity audits for certain businesses, raising the bar for evidence, record retention, and executive accountability that may extend to outsourced processes. These requirements can lengthen procurement cycles and reduce the pool of qualified vendors able to meet encryption, access, logging, and data retention standards at scale. Providers that cannot produce independent attestations such as ISO 27001 or SOC 2 may be excluded from consideration in regulated lines like health, life, and retirement services, which concentrates demand among certified players. The insurance BPO services market continues to expand, but privacy obligations shape scope, location, and technology configurations to ensure compliance by design.

Attrition & Knowledge-Loss Risk in Delivery Hubs

High turnover in large delivery centers raises replacement and training costs while risking inconsistency in service quality, which can limit scaling speed in the insurance BPO services market. While attrition has improved from earlier peaks, maintaining stable tenure remains a challenge requiring targeted retention, career development, and hybrid work plans to reduce commuting friction and improve engagement. Knowledge capture practices, such as codified standard operating procedures, AI-assisted knowledge bases, and structured shadowing, are essential to mitigate the impact of churn on complex processes like subrogation or specialty claims. Buyers often require explicit succession and staffing continuity measures within managed services agreements to reduce service risk. As demand grows in nearshore markets, competition for bilingual talent can intensify attrition, which underscores the value of robust training academies and certification tracks within vendor operations. The insurance BPO services market addresses these risks through governance, shared services centers of excellence, and technology that standardizes routine decision-making at scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Automation Propels Niche Analytics

Claims Processing commanded 38.75% of the insurance BPO services market share in 2025, reflecting the priority to speed settlements and control leakage in high-volume lines while maintaining regulatory and audit integrity. The insurance BPO services industry is increasingly using document AI to extract facts from police reports, medical records, and invoices so that low-severity claims route to straight-through processing with fewer handoffs and lower error rates, which supports better customer experience and faster cycle time. Fraud Detection & Analytics is projected as the fastest riser, with the insurance BPO services market size for this service expected to expand at a 7.64% CAGR between 2026 and 2031 as anomaly detection and network analysis reduce false positives, lighten investigator queues, and improve recovery rates. Policy Administration remains a core bundle of tasks ripe for automation, including endorsement processing, billing, and renewal documents, while Underwriting Support teams offshore perform submission triage and data enrichment that allow onshore experts to focus on pricing judgments and broker engagement. Customer Service & Contact Center outsourcing operations are segmenting routine policy inquiries for AI chat and voice bots while reserving complex or empathy-intensive interactions for skilled agents aided by AI copilots that surface next best actions and knowledge snippets in real time.

Billing, Accounting & Reconciliation workstreams are also modernizing as payments standards and richer messaging, such as ISO 20022, increase data availability for reconciliations and exception handling that used to depend on manual spreadsheets and email chains [3]Duck Creek Team, “What 2025 Taught Insurance Carriers About Payments—And How to Win in 2026,” Duck Creek, duckcreek.com. The insurance BPO services market continues to favor providers that can combine domain expertise, secured platforms, and analytics that quantify leakage reduction and straight-through rates. Providers are codifying best practices in reusable playbooks and initial operating capability kits that shorten transition times for new lines of business and books of business. As buyers increasingly adopt outcome-based pricing tied to accuracy and speed, service lines with clearer quality metrics, like claims or reconciliations, are advancing more quickly than ambiguous or ad hoc tasks. This service mix dynamic sustains Claims Processing at scale while allowing Fraud Detection & Analytics to outpace category averages as data sources and ML tools multiply.

By Insurance Type: Health Segment Rides Digitization Wave

Property & Casualty accounted for 44.43% in 2025, underpinned by heavy claim volumes in auto and homeowners, catastrophe response complexity, and specialty lines that require depth in policy servicing and subrogation. The insurance BPO services industry aligns P&C delivery around high-throughput claims, first notice of loss capture, repair network coordination, and payment operations that respond to line-specific regulations and consumer protection rules. Health is the fastest growing use case, with the insurance BPO services market size for Health projected to advance at an 8.27% CAGR through 2031 as telemedicine claim volumes and value-based care reconciliation increase the need for coding, prior authorization, and coordination of benefits that specialized partners manage with HIPAA controls. Life & Annuity outsourcing spans policy servicing, beneficiary support, and annuity payments, which require long-horizon accuracy and robust identity and tax reporting capabilities that BPOs can provide through standardized workflows. Specialty and Workers’ Compensation lines need tailored expertise and state-by-state rule familiarity, which favors either boutique providers or specialized practices within large vendors that maintain jurisdictional expertise and medical management capabilities.

Carriers are recalibrating make versus buy decisions for each product family based on business priorities, regulatory requirements, and internal platform modernization timetables. P&C teams partner for scale in claims intake and adjudication during catastrophe events, where surge capacity and standardized quality checks protect outcomes for policyholders and regulators. Health payers increasingly rely on partners to manage member services, provider inquiries, coding compliance, and payment integrity while their internal teams address plan design and network strategy. Life & Annuity teams use partners for policy changes, beneficiary updates, and customer communications at key life events, supplemented by analytics that identify exceptions and at-risk interactions requiring human intervention. The insurance BPO services market continues to be segmented by product complexities, with P&C sustaining the largest base and Health showing the steepest growth curve because of digitization and regulatory documentation demands.

By Organization Size: SMEs Embrace Cloud-Enabled Solutions

Large Enterprises represented 78.32% of demand in 2025, driven by global carriers and major brokers that manage thousands of seats across multi-tower programs for claims, policy servicing, finance, and technology operations. The insurance BPO services industry has matured frameworks for large buyers that prefer end-to-end process accountability, strong governance, and outcome-aligned pricing that ties fees to quality and speed metrics rather than seat counts. Small & Mid-Sized Enterprises are the faster risers, with the insurance BPO services market size for SMEs projected to grow at 7.57% CAGR through 2031 as cloud native platforms lower entry barriers, modularize service bundles, and enable pay-per-transaction economics suited to regional carriers and MGAs. Smaller buyers prioritize pre-integrated workflow, compliance, and analytics capabilities, often delivered through subscription bundles that scale up or down with premium cycles and product launches. These dynamics broaden access to modernized operations for organizations that historically could not justify captive offshore centers or long multi-year transformations.

SMEs also benefit from standard operating procedures and best practice libraries developed through large enterprise programs that vendors now provide in right-sized formats. Low-code orchestration and pre-built integrations with claim intake, policy administration, and payments systems allow SMEs to deploy operating improvements without burdensome IT projects, while vendors supply compliance documentation and audit evidence by default. Large buyers continue to anchor the insurance BPO services market with complex multi-geography books that require integration depth and rigorous controls, but SME momentum is reshaping the go-to-market model toward smaller, faster pilots that expand into multi-process engagements. Outcome-based pricing is attractive across sizes because it aligns spend with realized value, and it encourages deeper technology enablement that reduces rework and leakage over time. These shifts raise the importance of reference architectures and domain-specific AI that vendors tune for both enterprise and SME contexts.

Geography Analysis

North America held 41.19% of the insurance BPO services market share in 2025, supported by the presence of large Property & Casualty carriers, life insurers, and health payers that contract for multi-tower, multi-year solutions with vendors capable of combining domain knowledge and secure platforms. The United States features a patchwork of state regulations for licensing, claims handling, and data protection that requires structured playbooks, strong third-party risk management, and well-documented controls across vendor networks. New York’s 2025 guidance for managing risks related to third-party service providers reinforced expectations for due diligence, multi-factor authentication, encryption, and oversight, which vendors must evidence through policies, logs, and independent assessments to remain eligible for regulated lines of business. Canada mirrors many of these trends and maintains high standards for access control and data handling in financial services and insurance, which sustains demand for certified operations partners. The insurance BPO services market in North America also emphasizes outcome-based pricing, surge capacity, and bilingual support for cross-border programs, all delivered within governance frameworks that reflect heightened scrutiny by supervisors and attorneys general.

Asia-Pacific is the fastest growing region with a projected 9.32% CAGR through 2031 as delivery ecosystems scale in India, the Philippines, Malaysia, and Vietnam, while domestic insurance markets expand in South and Southeast Asia. Delivery hubs are investing in multilingual talent, domain certifications, and AI-enabled workflows that serve global carriers and regional insurers seeking cost-effective, resilient service. Multinational providers are adding capabilities across the region, and ecosystem players have opened new multilingual centers that complement established hubs, which support broader language coverage for European and Asian buyers. Payments modernization and data residency rules shape architecture decisions that vendors implement with secure in-country processing and audited controls, which help carriers meet privacy laws while maintaining scale from global delivery. The insurance BPO services market in Asia-Pacific is also marked by greenfield operations that embed automation and analytics from inception rather than retrofitting legacy systems, which can produce step-change productivity in claims and policy servicing.

Europe’s demand spans Western markets with mature insurers and growing nearshore locations such as Poland, Romania, and Portugal that offer multilingual coverage aligned with GDPR. United Kingdom regulatory developments, including new safeguarding rules for payment and e-money firms and the Bank of England’s ISO 20022 adoption for large value payments, are reshaping billing and reconciliation processes that BPO partners often operate for carriers and intermediaries. The region values data privacy, encryption, and vendor oversight with granular evidence, which narrows the provider pool to those with audited certifications and mature governance models that meet European documentation expectations. The insurance BPO services market in Europe remains competitive, with hybrid onshore nearshore designs balancing cost, language coverage, and regulatory comfort. In South America and the Middle East & Africa, adoption is smaller but growing, with South America’s nearshore advantage supporting United States programs, and South Africa’s Joint Standards on cybersecurity and outsourcing improving regulatory clarity that favors English language delivery to European and African insurers.

Competitive Landscape

The insurance BPO services market features moderate consolidation among the top ten vendors, which together account for majority of activity, and a long tail of regional and functional specialists. Large multi-tower firms deepen industry focus by investing in insurance platforms, AI enablement, and certifications, while contact center leaders move up the value chain into specialized claims and policy workflows supported by AI copilots. Strategic moves in 2025 included targeted acquisitions to expand capabilities in insurance consulting and cybersecurity that strengthen delivery for regulated clients, with reported investments across dozens of transactions to scale high-growth offerings and talent bases. Partnerships between specialty insurers and global providers demonstrate how co-sourced models can stand up underwriting support, reinsurance processing, finance operations, and automation centers under unified governance in a multi-tower framework. The insurance BPO services market continues to reward providers that blend domain expertise with secure platforms and measurable outcomes.

Technology differentiation centers on agent assist and document automation that shrinks backlogs in claims and underwriting by raising straight through rates, with vendors productizing domain-tuned solutions for faster deployments. Examples include underwriting intake suites built to triage submissions at scale and case management add-ons that summarize unstructured content for human review, which shorten time to quote and improve compliance in audit trails. Customer experience specialists have added AI-based guidance and autonomous document readers that feed core systems, which aligns service delivery with outcome-based pricing that rewards fewer touches and higher accuracy. The insurance BPO services market also values secure identity and access management capabilities that align with third-party risk rules, prompting acquisitions of cybersecurity specialists to support clients in financial services and insurance with privileged access and identity governance. Vendors that can demonstrate strong controls, independent assessments, and rapid remediation practices are advantaged in bids with carriers facing frequent audits.

Competitive intensity is also shaped by in-house automation programs at carriers and the rise of low-code platforms that let buyers assemble workflows internally, which nudges providers toward higher-value analytics, model monitoring, and exception handling. Nonetheless, the complexity of the insurance domain logic and regulatory documentation creates durable advantages for partners that have codified process knowledge and validated controls at scale. Regional expansion by ecosystem players is broadening multilingual capacity and adding redundancy across APAC and EMEA, which improves resiliency and risk diversification for global insurers. The insurance BPO services market also benefits from alliances that integrate generative AI with customer service platforms to guide agents in real time, raise first contact resolution, and improve satisfaction metrics in regulated environments. As buyers seek measurable value, the ability to quantify leakage reduction, speed gains, and audit readiness remains central to awarding multi-year, multi-tower programs.

Insurance BPO Services Industry Leaders

Accenture

Cognizant

Genpact

EXL Service

WNS Global Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Teleperformance has expanded its operations in Davao City with the launch of a second site, increasing its total locations in the Philippines to 26. The new facility, TP Davao Uprise, represents the company's fourth site on Mindanao. Strategically situated at The Uprise within Felcris Centrale mall, this expansion underscores the company's commitment to strengthening its presence in the region.

- June 2026: EXL Service intends to open two new delivery centers in Tier 2 and Tier 3 cities in India this year, reflecting the global shift toward the adoption of artificial intelligence (AI) and data analytics.

- July 2025: Athora Holding Ltd. announced the acquisition of Pension Insurance Corporation Group for USD 7.69 billion (GBP 5.7 billion), with closing expected in early 2026, subject to approvals. PIC will operate as Athora’s United Kingdom platform, representing a substantial portion of combined assets and supporting millions of pensioners with long-term payment obligations. The transaction underscores continued consolidation and scale economics in pension risk transfer and retirement services.

- June 2025: Trucordia, formerly PCF, secured a USD 1.3 billion investment from Carlyle, valuing the brokerage at USD 5.7 billion, and raised USD 2.5 billion in debt, including a USD 400 million revolving credit facility. The funding supports acquisitions and organic investments to expand distribution capabilities. The move indicates sustained investor interest in scaled distribution and servicing platforms.

Global Insurance BPO Services Market Report Scope

The Insurance Business Process Outsourcing (BPO) market refers to the delegation of non-core functions, including claims processing, policy administration, customer support, billing, and data management, to external providers, enabling insurers to reduce costs, improve efficiency, and prioritize core operations.

The insurance BPO services market report is segmented by service type (claims processing, policy administration, underwriting support, customer service & contact center, billing, accounting & reconciliation, fraud detection & analytics), insurance type (life & annuity, property & casualty (P&C), health, specialty/workers' compensation), organization size (large enterprises, small & mid-sized enterprises (SMEs)), and geography (North America, South America, Europe, Asia-Pacific, Middle East & Africa). The market forecasts are provided in terms of value (USD).

| Claims Processing |

| Policy Administration |

| Underwriting Support |

| Customer Service & Contact Center |

| Billing, Accounting & Reconciliation |

| Fraud Detection & Analytics |

| Life & Annuity |

| Property & Casualty (P&C) |

| Health |

| Specialty / Workers' Compensation |

| Large Enterprises |

| Small & Mid-Sized Enterprises (SMEs) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia (SG, MY, TH, ID, VN, PH) | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Service Type | Claims Processing | |

| Policy Administration | ||

| Underwriting Support | ||

| Customer Service & Contact Center | ||

| Billing, Accounting & Reconciliation | ||

| Fraud Detection & Analytics | ||

| By Insurance Type | Life & Annuity | |

| Property & Casualty (P&C) | ||

| Health | ||

| Specialty / Workers' Compensation | ||

| By Organization Size | Large Enterprises | |

| Small & Mid-Sized Enterprises (SMEs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia (SG, MY, TH, ID, VN, PH) | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the size and growth outlook for the Insurance BPO services market through 2031?

The Insurance BPO services market size is expected to rise from USD 64.31 billion in 2025 to USD 68.40 billion in 2026 and reach USD 93.12 billion by 2031, reflecting a 6.36% CAGR over 2026-2031.

Which service lines and insurance products are leading or growing fastest in Insurance BPO?

Claims Processing led service lines with 38.75% in 2025, while Fraud Detection & Analytics shows the fastest trajectory at a 7.64% CAGR; by insurance type, Property & Casualty held 44.43% in 2025, and Health is poised to grow fastest at an 8.27% CAGR.

Which regions lead demand and expansion for Insurance BPO?

North America led with 41.19% in 2025 due to large carriers and complex compliance, while Asia-Pacific is projected as the fastest?growing region at a 9.32% CAGR to 2031 on the strength of multilingual hubs and greenfield AI-enabled operations.

How is regulation shaping outsourcing decisions in insurance?

Third-party risk rules and privacy mandates require strong cybersecurity programs, encryption, MFA, incident notification, and independent assessments, with New York DFS and updated California privacy audits influencing vendor selection and oversight.

How is AI transforming Insurance BPO delivery?

AI improves document ingestion, triage, and analytics across claims and policy servicing, raising straight-through rates and reducing false positives in fraud detection, while agent copilots enhance customer service and exception handling quality.

What is the competitive dynamic among leading Insurance BPO providers?

The top 10 providers account for most of the activity with deep domain platforms, certified controls, and AI enablement, while a fragmented tail offers specialized or regional capabilities under outcome-based pricing models.

Page last updated on: