LLM and Foundation Model Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

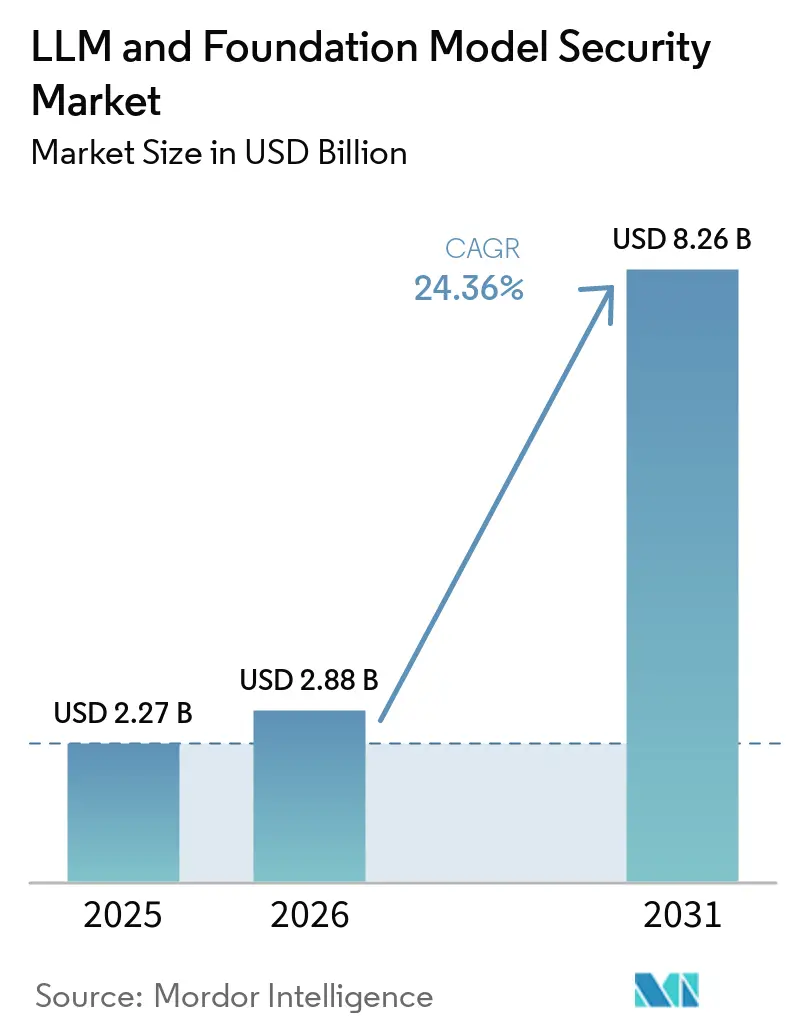

| Market Size (2026) | USD 2.88 Billion |

| Market Size (2031) | USD 8.26 Billion |

| Growth Rate (2026 - 2031) | 24.36% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LLM and Foundation Model Security Market Analysis by Mordor Intelligence

The LLM and Foundation Model Security Market size is expected to increase from USD 2.27 billion in 2025 to USD 2.88 billion in 2026 and reach USD 8.26 billion by 2031, growing at a CAGR of 23.5% over 2026-2031. The LLM and Foundation Model Security Market is expanding as enterprise AI moves out of pilot environments and into production systems that handle real content, user actions, and business workflows. A major shift came when EchoLeak demonstrated that a production enterprise assistant could be exploited for zero-click data exfiltration, pushing model-layer risk into mainstream security planning. The LLM and Foundation Model Security Market is also benefiting from the fact that prompt injection, unsafe outputs, and model misuse sit outside the normal coverage of many legacy applications and cloud security tools. Governance pressure is adding another layer of demand because enterprises now need audit records, policy controls, and risk documentation for AI systems that touch sensitive data or regulated workflows. The LLM and Foundation Model Security Market is therefore attracting investment from both established cybersecurity vendors and specialized AI security providers expanding into agent controls, gateways, monitoring, and managed services.

Key Report Takeaways

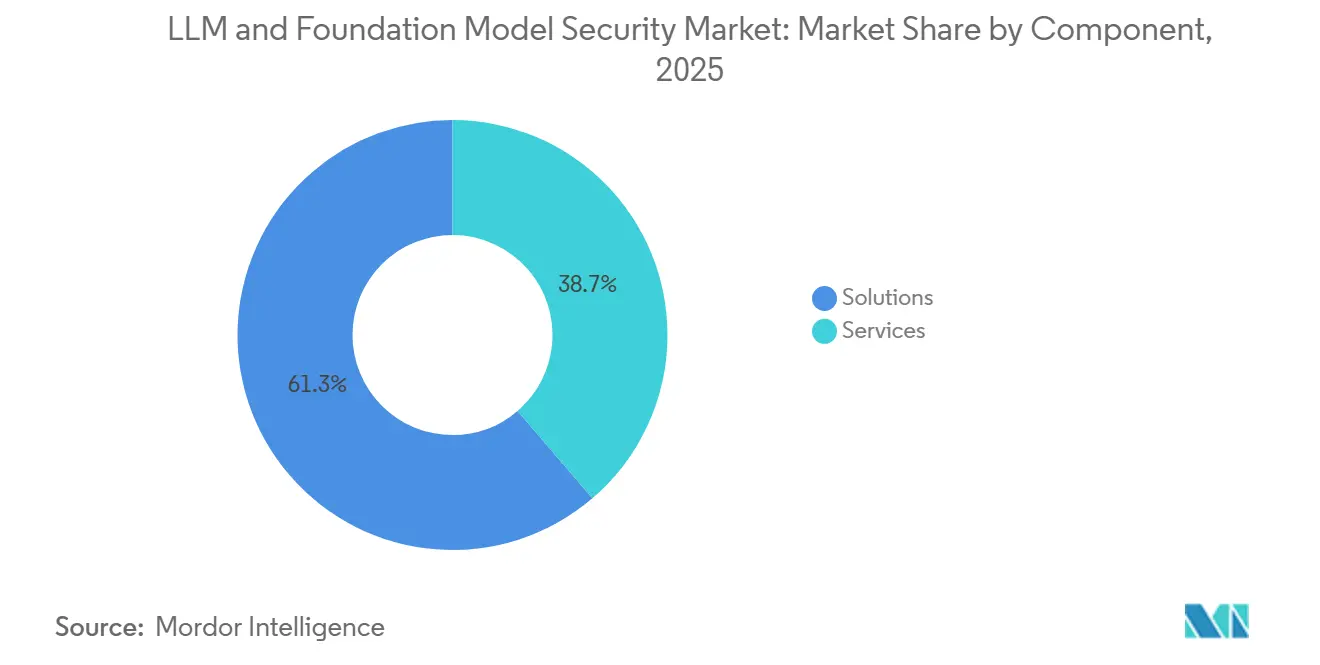

- By component, Solutions led with 61.3% revenue share in LLM and Foundation Model Security Market 2025, while Services is projected to expand at 24.6% CAGR through 2031.

- By security type, Model Security held the largest share at 28.1% in 2025, while GRC is forecast to grow at 24.7% CAGR through 2031.

- By deployment, Cloud accounted for a 54.2% share in 2025, while Hybrid is projected to grow at a 24.8% CAGR through 2031.

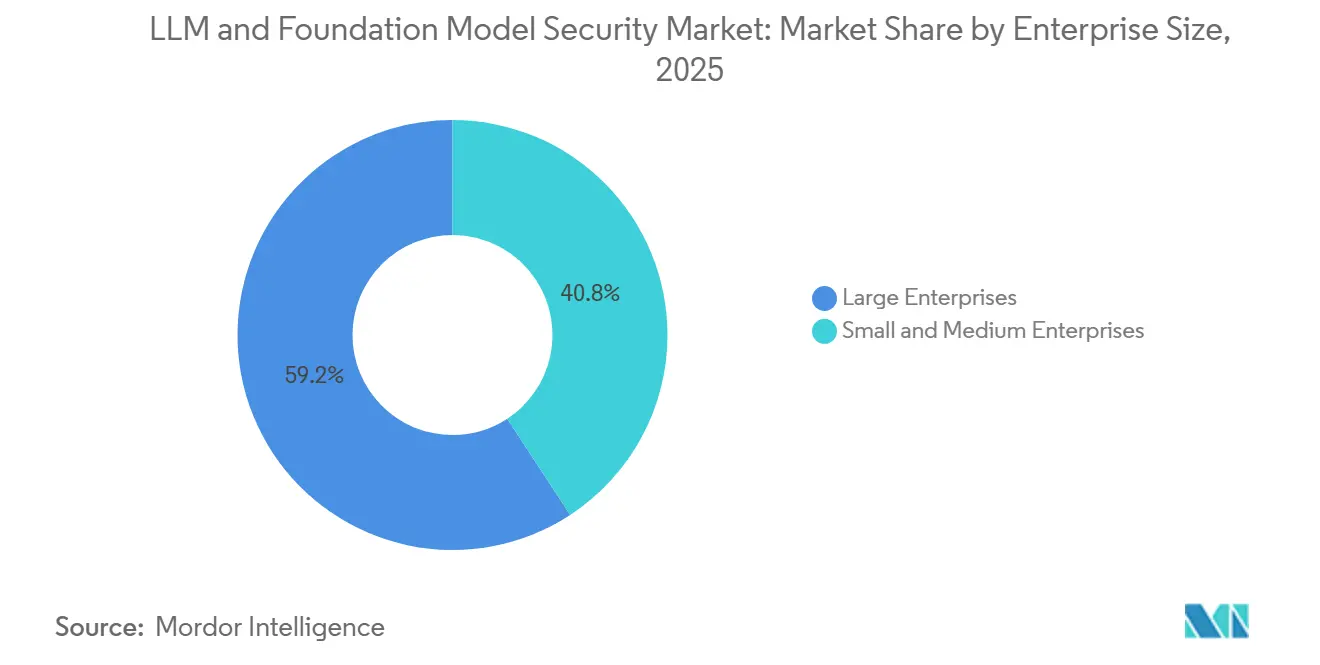

- By enterprise size, Large Enterprises held 59.2% share in 2025, while SMEs are forecast to grow at 24.9% CAGR through 2031.

- By end-user industry, BFSI accounted for 17.2% of the LLM and Foundation Model Security Market size in 2025, while Healthcare and Life Sciences are projected to expand at 25.1% CAGR through 2031.

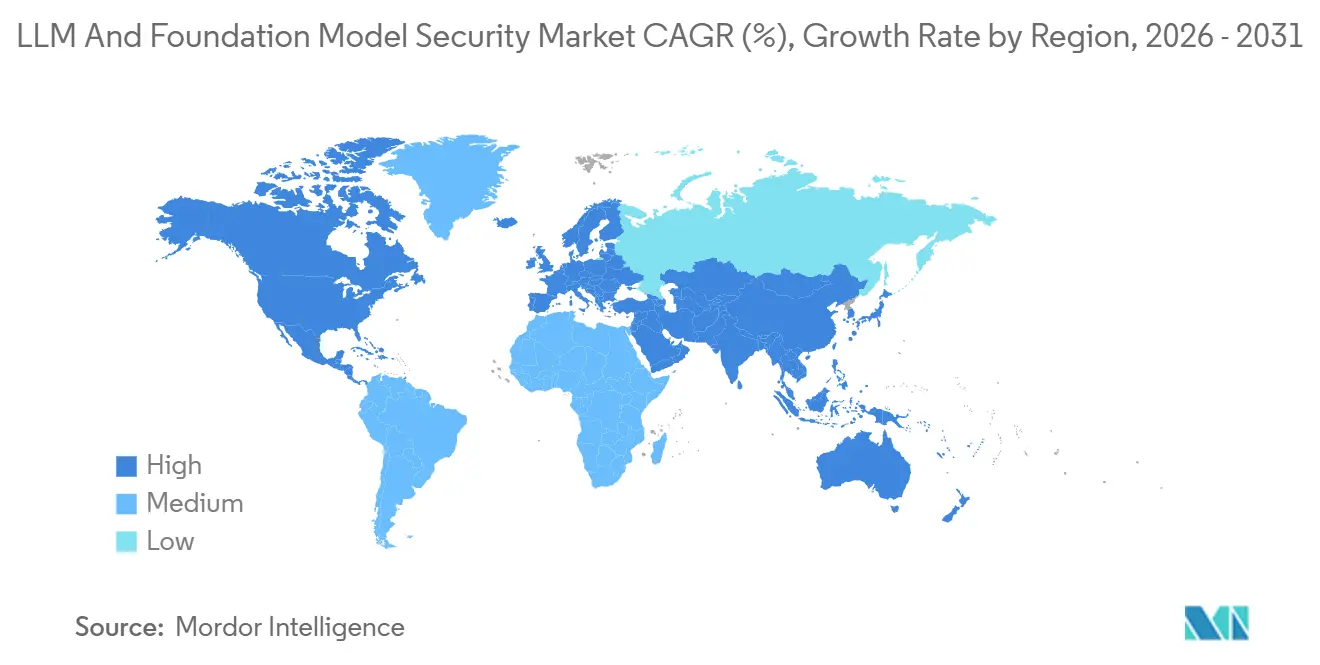

- By geography, North America held 32.2% of the LLM and Foundation Model Security Market share in 2025, while Asia-Pacific is forecast to grow at 25.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global LLM and Foundation Model Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prompt Injection and Data Exfiltration Exposure | +4.5% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Rising Scrutiny of Model Governance and AI Risk Controls | +4.0% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Expansion of Multi-Model AI Stacks Requiring Centralized Security | +3.5% | Global, particularly North America, Asia-Pacific, and Europe | Medium term (2-4 years) |

| Commercialization of Customer-Facing LLM Applications | +3.0% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Shift Toward Secure AI Development Lifecycles in Regulated Industries | +2.5% | North America and Europe, with spillover into Asia-Pacific | Medium term (2-4 years) |

| Growing Need for Runtime Monitoring of Hallucinations and Unsafe Outputs | +2.0% | Global, concentrated in BFSI and healthcare | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Enterprise Exposure to Prompt Injection and Data Exfiltration

The LLM and Foundation Model Security Market is moving faster because prompt injection is no longer a theoretical issue. OWASP ranked indirect prompt injection as LLM01:2025, indicating its growing centrality in production systems.[1]OWASP Foundation, “OWASP Top 10 for Large Language Model Applications,” OWASP Foundation, owasp.org Microsoft documented EchoLeak as a zero-click attack path against Microsoft 365 Copilot, demonstrating that attackers can target enterprise assistants without requiring direct user action. Cloud Security Alliance research also showed that many promptware incidents span multiple attack stages, indicating that model abuse now resembles broader multi-step security campaigns rather than isolated prompts. As a result, the LLM and Foundation Model Security Market is seeing stronger demand for prompt inspection, runtime guardrails, and output validation that can sit close to the model and the application layer.[2]Microsoft Security Response Center, “How Microsoft Defends Against Indirect Prompt Injection Attacks,” Microsoft, microsoft.com

Accelerating Regulatory Scrutiny on Model Governance and AI Risk Controls

The LLM and Foundation Model Security Market is also supported by a broader shift away from optional AI governance toward formal control frameworks. NIST AI guidance provides enterprises with a practical framework for mapping, measuring, managing, and governing AI risk in operational settings.[3]National Institute of Standards and Technology, “IR 8596, Cybersecurity Framework Profile for Artificial Intelligence, NIST Community Profile,” NIST, csrc.nist.gov In healthcare, the FDA guidance for adaptive AI devices and the HHS HIPAA Security Rule changes have pushed AI-specific monitoring and control needs into active compliance workstreams. This is changing procurement because buyers now want security tools that can produce records, policy evidence, workflow controls, and audit trails, rather than just alerts. The LLM and Foundation Model Security Market is therefore gaining recurring demand from GRC-led deployments as organizations build AI oversight into normal audit and supplier review processes.

Expansion of Multi-Model Enterprise AI Stacks Requiring Centralized Security

The LLM and Foundation Model Security Market is benefiting from the growing distribution of enterprise AI stacks across models, tools, and environments. When organizations add more model endpoints, they also add more credentials, prompt pipelines, access rules, and output review paths that must be monitored together. This makes point products harder to manage because they cannot always provide one policy view across cloud APIs, internal tools, and agent workflows. Vendors are responding with centralized control layers, and CrowdStrike expanded Falcon AI Detection and Response through a gateway ecosystem that connects policy and telemetry across several AI environments. Microsoft also positioned Agent 365 around centralized agent identity, shadow AI discovery, and policy enforcement, which reflects the same buyer need for unified oversight in the LLM and Foundation Model Security Market.[4]Censinet, “FDA, FTC, and Beyond, Multi-Agency Compliance for Healthcare AI,” Censinet, censinet.com

Mainstream Commercialization of Customer-Facing LLM Applications

The broader adoption of customer-facing assistants and workflow agents is also driving forward the LLM and Foundation Model Security Market. Once a model is exposed to customers, the cost of unsafe outputs, leaked information, or unauthorized actions becomes immediate and visible. Skyhigh Security reported that 94% of surveyed AI services were exposed to at least 1 LLM threat vector, while the average enterprise used more than 320 unsanctioned AI applications, highlighting how quickly shadow AI can widen risk. That risk is pushing organizations to add stronger controls around approved use cases, data handling, and real-time monitoring before scaling broader deployments. The LLM and Foundation Model Security Market is benefiting from this shift because customer-facing AI programs tend to elevate security from a technical concern to a business, legal, and reputational priority.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Availability of LLM Security Engineering Talent | -2.5% | Global, most acute in emerging markets and mid-market enterprises | Short term (≤ 2 years) |

| Fragmented Threat Taxonomy Slowing Standardized Buying Decisions | -2.0% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Difficulty Proving ROI Before a Material Security Incident | -1.5% | Global, most pronounced among SMEs | Short term (≤ 2 years) |

| Model Access Constraints and Black-Box Vendor Limitations | -1.0% | Global, concentrated where closed-source models dominate | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Availability of LLM Security Engineering Talent

The LLM and Foundation Model Security Market still faces a clear talent gap that slows deployment quality and speed. AI security work needs a mix of model understanding, red teaming discipline, application security, and prompt behavior analysis, and that mix remains hard to find in 2026. The IIF-EY survey in financial services found that AI oversight and governance remain difficult for many institutions, suggesting limited internal capacity to test vendor claims or run deep assurance programs. This pushes many buyers toward vendor-led implementation and managed support, which can stretch rollout timelines and reduce the amount of control they build internally. The LLM and Foundation Model Security Market therefore grows alongside demand, but not every buyer can operationalize tools at the same pace.

Fragmented Threat Taxonomy Slows Standardized Buying Decisions

The LLM and Foundation Model Security Market also faces slower buying cycles because AI threat language is still fragmented across frameworks and vendor categories. OWASP, NIST, and other AI risk frameworks do not describe every problem in the same way, making internal evaluation more difficult for procurement and security teams. Buyers often need to translate one framework into another before they can compare tools, which adds extra review steps for already cautious organizations. Smaller buyers face an even harder problem because they may not know which framework will matter most for their own sector or geography. Until a narrower set of buyer standards becomes dominant, the LLM and Foundation Model Security Market will continue to see some friction in early-stage evaluations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Anchor Spend, Services Emerge as the Growth Engine

Solutions accounted for 61.3% of revenue in 2025, making them the largest component of the LLM and Foundation Model Security Market. Buyers have generally preferred platforms because subscription software is easier to standardize across model teams than consulting-heavy engagements. Prompt security tools and model monitoring have moved to the front of deployment plans because production AI now needs active checks on inputs, outputs, and model behavior. Data leakage prevention and governance layers also matter because many enterprise assistants touch internal content repositories, documents, and communication tools. This keeps software platforms central to how the LLM and Foundation Model Security Market is being implemented in large accounts.

Services are projected to grow at a 24.6% CAGR through 2031, making them the fastest-expanding component of the LLM and Foundation Model Security Market. The talent shortage is a direct reason, as many organizations cannot build in-house red teaming, adversarial testing, and AI incident response capabilities quickly enough. Managed monitoring is also gaining ground as buyers try to keep pace with evolving prompts, new agents, and post-deployment policy tuning needs. Services are therefore becoming a practical extension of software adoption rather than a one-time implementation add-on. This is expanding the addressable market for the LLM and Foundation Model Security industries, especially among buyers who need operational support from the start.

By Security Type: Model Security Leads, GRC Signals the Next Phase

Model Security held the largest share at 28.1% in 2025, which placed it at the center of the LLM and Foundation Model Security Market. Enterprises are prioritizing it because fine-tuned models, weights, and inference pathways now hold direct business value and can become targets for extraction or manipulation. Data Security and Application Security remain close behind because the context pipeline and the prompt interface are frequent entry points for sensitive information exposure and unsafe interactions. Identity and Access Security is also rising because agentic systems increasingly receive permissions, tokens, and the ability to take actions on behalf of users. This means the LLM and Foundation Model Security Market is broadening from pure model defense into a wider stack of surrounding controls.

GRC is projected to expand at a 24.7% CAGR through 2031, making it the fastest-growing security type in the LLM and Foundation Model Security Market. The growth is being driven by the need to document AI risks, assign controls, preserve evidence, and support internal reviews or external audits. Healthcare rules and enterprise AI governance programs are making those documentation needs more immediate in 2026. Buyers also value GRC spending because it gives a clearer budget case than purely reactive categories that depend on visible incidents. That makes governance software a durable growth layer within the LLM and Foundation Model Security Market as AI use moves into controlled business processes.

By Deployment: Cloud Leads, Hybrid Captures Regulated Workloads

Cloud accounted for 54.2% of 2025 spend, making it the leading deployment mode in the LLM and Foundation Model Security Market. Organizations continue to favor cloud AI services because they speed up rollouts and embed baseline controls into the deployment environment. Even so, cloud-first rollouts still need separate prompts, outputs, and policy protections because provider safeguards do not fully eliminate model misuse risks. Cloud also suits teams that want faster experimentation and easier access to multiple model providers within a single commercial environment. This keeps Cloud Central focused on the LLM and Foundation Model Security Market, especially in less restrictive deployment scenarios.

Hybrid is projected to grow at a 24.8% CAGR through 2031, making it the fastest-growing deployment model in the LLM and Foundation Model Security Market. Regulated enterprises are increasingly combining on-premises inference or sensitive data handling with cloud-native monitoring and governance layers. That design allows buyers to more tightly protect critical workflows while still using scalable external security services. It also creates a policy consistency problem because controls must work across different infrastructure layers and operating teams. Vendors are responding with gateway and control-plane models, reinforcing hybrid demand in the LLM and Foundation Model Security industry.

By Enterprise Size: Large Enterprises Anchor Revenue, SMEs Accelerate Fastest

Large Enterprises accounted for 59.2% of revenue in 2025, giving them the leading position in the LLM and Foundation Model Security Market. They tend to run broader AI estates, face more jurisdictions, and manage more internal stakeholders around security and governance. That makes them more likely to purchase multi-module platforms that combine prompt controls, model protections, identity oversight, and governance capabilities in one contract. Their scale also increases the value of standardization because fragmented AI security tools become difficult to manage across business units and regions. As a result, large accounts remain the revenue anchor of the LLM and Foundation Model Security Market.

SMEs are projected to grow at a 24.9% CAGR through 2031, making them the fastest-growing segment in the LLM and Foundation Model Security Market. Low-code builders and easier access to packaged AI tools have allowed smaller organizations to launch assistants and workflow agents without large engineering teams. The security burden arises immediately, even when the internal staff responsible for managing model behavior and policy tuning is still limited. Vendors are answering this with embedded controls, simpler deployment paths, and more managed support around rollout and operations. This is expanding the buyer base of the LLM and Foundation Model Security Market and gradually changing sales models from highly customized deals to more repeatable adoption patterns.

By End-user Industry: BFSI Sets the Risk Standard, Healthcare Scales Fast

BFSI held the largest share at 17.2% in 2025, which made it the leading vertical in the LLM and Foundation Model Security Market. Financial institutions handle sensitive customer data, regulated decisions, and high-value workflows, so the cost of weak model controls is unusually high. The IIF-EY survey showed that AI third-party oversight and governance remain major concerns in this sector, underscoring the need for continued spending on validation, monitoring, and control frameworks. Customer-facing assistants also make governance more urgent because output quality, access controls, and data handling all sit close to consumer trust. This keeps BFSI as a benchmark buyer group within the LLM and Foundation Model Security Market.

Healthcare and Life Sciences is projected to grow at a 25.1% CAGR through 2031, making it the fastest-growing vertical in the LLM and Foundation Model Security Market. The FDA guidance on adaptive AI devices and the HHS HIPAA changes are pushing runtime monitoring, reviewability, and AI-specific safeguards to the forefront of active procurement priorities. The Health Sector Coordinating Council added further structure by guiding AI bill-of-materials tracking, auditability, and fail-safe expectations for vendor relationships. That combination is expanding demand beyond basic model protection into supply chain visibility and third-party assurance. It also makes healthcare one of the clearest examples of how regulation and operational risk are expanding the LLM and Foundation Model Security industry at the same time.

Geography Analysis

North America held 32.2% of the LLM and Foundation Model Security Market share in 2025, which made it the largest regional market. The region benefits from a high concentration of regulated financial institutions, cloud AI infrastructure, and mature enterprise security budgets. It also has a strong base of vendors that are actively shaping the category with new products and integrations. NIST AI guidance has become an important anchor for AI governance programs in the region, especially for enterprises that want a structured framework for model oversight and operational controls. Product moves from Microsoft and CrowdStrike also show that North America remains the main launch ground for centralized agent and gateway controls in the LLM and Foundation Model Security Market.

Europe was the second-largest regional market in 2025 within the LLM and Foundation Model Security Market. Demand is being shaped by organizations that increasingly treat AI governance as a required operating discipline rather than a discretionary layer. Financial services, public institutions, and other regulated sectors continue to support buying activity focused on policy controls, documentation, and supplier assurance. Europe also remains important because buyers there tend to place heavy weight on traceability, depth of governance, and evidence that security controls can withstand formal review. That preference supports steady demand for platforms that can connect model protection with governance workflows across the LLM and Foundation Model Security Market.

Asia-Pacific is projected to expand at a 25.2% CAGR, making it the fastest-growing regional segment of the LLM and Foundation Model Security Market through 2031. The region combines large-scale enterprise AI adoption with a wide range of domestic implementation paths across China, India, Japan, and South Korea. Public sector and enterprise governance activity is also becoming more structured, which supports demand for model, data, and application controls. Since dedicated AI security tooling still has lower penetration in many Asia-Pacific deployments than in North America, the LLM and Foundation Model Security Market has more room to expand from a lower installed base.

Competitive Landscape

The LLM and Foundation Model Security Market remains moderately fragmented, with large cybersecurity vendors and focused AI security specialists competing on different strengths. Incumbents usually bring stronger distribution, broader customer access, and easier integration into existing enterprise stacks. Specialists usually bring deeper expertise across model layers, especially in prompt abuse, adversarial testing, and runtime guardrails. Check Point strengthened its position in Q4 2025 by acquiring Lakera and integrating runtime protection and pre-deployment assessment into the Infinity platform, demonstrating that incumbents are buying AI-specific depth rather than waiting to build everything internally. That pattern is pushing the LLM and Foundation Model Security Market toward broader platform competition over time.

The move toward centralized control planes is also shaping the LLM and Foundation Model Security Market. Microsoft launched Agent 365 as a generally available platform for agent identity governance, shadow AI discovery, runtime blocking, and policy enforcement across first-party and third-party ecosystems. CrowdStrike expanded Falcon AI Detection and Response across multiple AI gateways, underscoring the growing value of cross-model visibility and shared policy enforcement. These launches show that vendors are competing less on isolated features and more on how much of the AI workflow they can control within a single operating layer. That shift is making platform completeness more important in the LLM and Foundation Model Security Market.

Managed and service-led strategies are becoming another clear line of competition in the LLM and Foundation Model Security Market. IBM joined the OpenAI Daybreak Cyber Partner Program and committed USD 5 billion through Project Lightwell, which adds scale to the category for managed vulnerability discovery and remediation. SentinelOne also opened Purple AI Agentic Investigation to all customers and launched Wayfinder Frontier AI Services, which shows demand for both automated investigation and expert-led security support. Palo Alto Networks added native support for Anthropic's Claude Sonnet 4.6, Claude Opus 4.8, and Gemini 3.5 Flash across Cortex, reflecting the breadth of competitive support now including more models and operational contexts. The result is an LLM and Foundation Model Security Market where vendor count remains broad, but the center of gravity is shifting toward platforms that combine model protection, identity control, observability, and services.

LLM and Foundation Model Security Industry Leaders

Palo Alto Networks, Inc.

Microsoft Corporation

Alphabet Inc.

Amazon.com, Inc.

CrowdStrike Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: IBM joined the OpenAI Daybreak Cyber Partner Program and committed USD 5 billion through Project Lightwell to integrate frontier AI into enterprise application security services, launching a new managed vulnerability discovery service that uses OpenAI models to identify and validate software vulnerabilities across large-scale codebases with broader coverage than traditional scanning tools.

- June 2026: CrowdStrike extends Falcon AI Detection and Response (AIDR) across an open gateway partner ecosystem including Databricks Unity AI Gateway, Google Cloud Apigee, Microsoft Azure API Management, Kong, LiteLLM, Maxim AI Bifrost, JetStream Security, and TrueFoundry, establishing the Falcon platform as a unified AI security control plane for multi-model enterprise deployments.

- June 2026: SentinelOne opens Purple AI Agentic Investigation to all customers, providing zero-click autonomous threat detection that investigates, renders verdicts, and stops AI-enabled threats without human dependencies, while simultaneously introducing Singularity Credits as a unified currency for AI-powered security operations across the Singularity Platform

- May 2026: Microsoft launched Agent 365 as generally available to commercial customers at USD 15 per user per month, providing a centralized control plane for agent identity governance, shadow AI discovery, runtime blocking, and policy enforcement across Microsoft and third-party agent ecosystems including AWS Bedrock and Google Gemini Enterprise Agent Platform

Global LLM and Foundation Model Security Market Report Scope

The LLM and Foundation Model Security market encompasses platforms and services designed to safeguard large language models (LLMs) and foundation AI models against adversarial attacks, misuse, and systemic vulnerabilities. These solutions include prompt security, output moderation, runtime monitoring, data leakage prevention, governance frameworks, and AI red teaming to ensure the integrity, reliability, and trustworthiness of advanced AI systems. The market is fueled by the rapid adoption of generative AI across industries, rising risks such as prompt injection, data poisoning, model theft, and misuse of synthetic content, as well as the growing demand for compliance with global AI governance and security standards. Organizations in BFSI, healthcare, IT, manufacturing, government, and retail are deploying these solutions to protect sensitive data, secure AI pipelines, and maintain operational resilience. Its primary objective is to enable secure, transparent, and trustworthy AI ecosystems by integrating proactive defenses, continuous monitoring, and governance frameworks that mitigate risks while supporting innovation and safe deployment of advanced AI technologies.

The LLM and Foundation Model Security market report is segmented by Component (Solutions [Prompt Security Solutions, Output Security and Content Moderation, Model Monitoring and Runtime Protection, Data Leakage Prevention and Data Governance, AI Red Teaming and Validation Platforms, Other Solutions], and Services), Security Type (Model Security, Data Security, Application Security, Identity and Access Security, Governance, Risk and Compliance (GRC)), Deployment (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Prompt Security Solutions |

| Output Security and Content Moderation | |

| Model Monitoring and Runtime Protection | |

| Data Leakage Prevention and Data Governance | |

| AI Red Teaming and Validation Platforms | |

| Other Solutions | |

| Services |

| Model Security |

| Data Security |

| Application Security |

| Identity and Access Security |

| Governance, Risk and Compliance (GRC) |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | Prompt Security Solutions | |

| Output Security and Content Moderation | |||

| Model Monitoring and Runtime Protection | |||

| Data Leakage Prevention and Data Governance | |||

| AI Red Teaming and Validation Platforms | |||

| Other Solutions | |||

| Services | |||

| By Security Type | Model Security | ||

| Data Security | |||

| Application Security | |||

| Identity and Access Security | |||

| Governance, Risk and Compliance (GRC) | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Information Technology and Telecom | |||

| Retail and E-commerce | |||

| Industrial Manufacturing | |||

| Government and Public Sector | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and projected size of the LLM and generative AI energy optimization software market?

The market was valued at USD 1.28 billion in 2025, rose to USD 1.58 billion in 2026, and is forecast to reach USD 5.07 billion by 2031 at a 26.26% CAGR.

Which solution category leads revenue in this space?

AI Energy Analytics and Observability led with 29.85% share in 2025 because most operators first need accurate circuit-level and facility-level visibility before they automate optimization actions.

Why are hybrid deployments growing faster than cloud-only models?

Hybrid deployments are projected to grow at a 26.92% CAGR because operators want local control over power and cooling systems while still using cloud-scale analytics across sites.

Which end-user group is expanding fastest?

Enterprise Data Centers are expected to grow at a 27.05% CAGR through 2031 as more firms bring LLM inference in-house for stronger control over cost, privacy, and performance.

Which region is expanding fastest for energy optimization software tied to AI infrastructure?

Asia-Pacific is forecast to grow at a 27.45% CAGR through 2031, supported by national AI infrastructure programs, energy efficiency standards, and data center policy updates.

What is the main buyer priority beyond energy savings?

Reliability and Availability Optimization is the fastest-growing objective at a 26.87% CAGR, which shows that operators are increasingly focused on avoiding failures that disrupt expensive GPU workloads.

Page last updated on: