Cybersecurity For AI Models and LLMs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

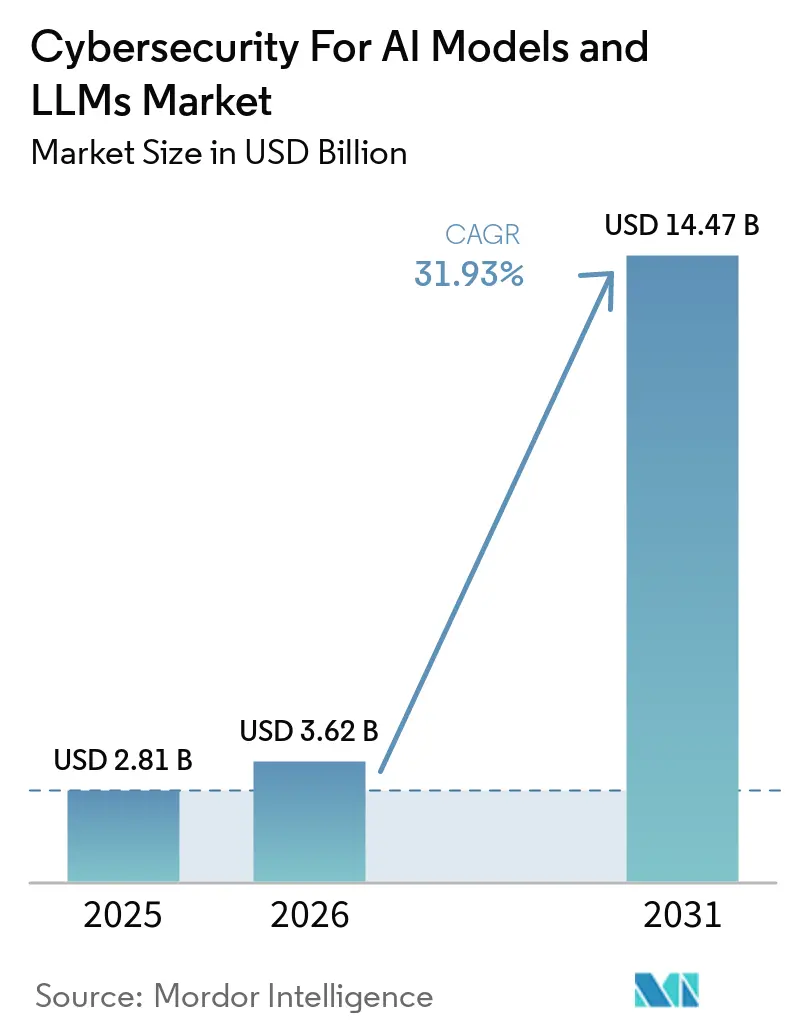

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 14.47 Billion |

| Growth Rate (2026 - 2031) | 31.93% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

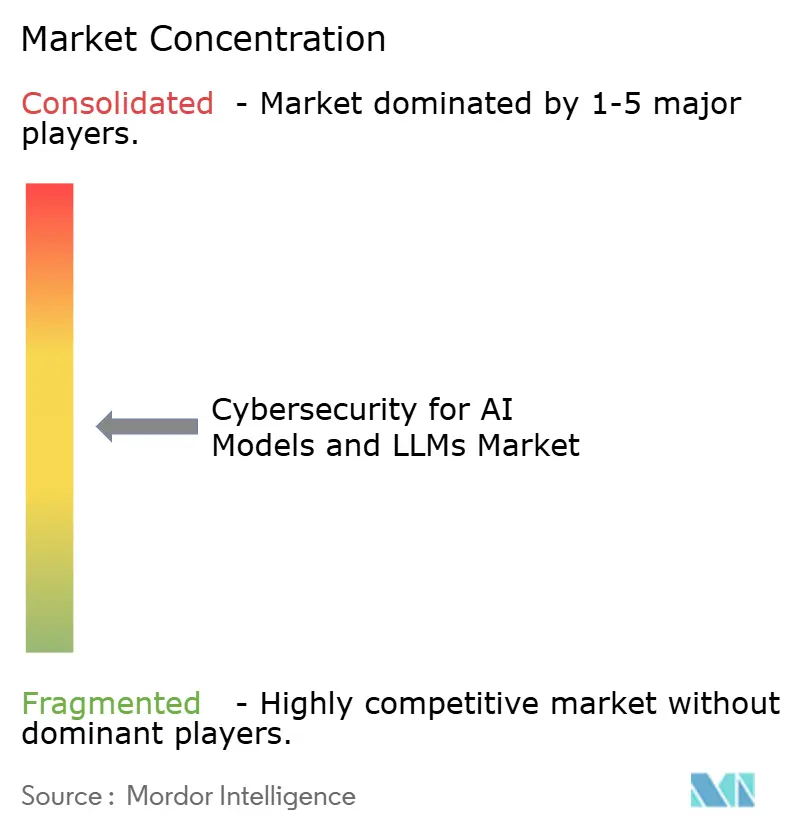

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cybersecurity For AI Models and LLMs Market Analysis by Mordor Intelligence

The Cybersecurity for AI Models and LLMs Market size is projected to be USD 2.81 billion in 2025, USD 3.62 billion in 2026, and reach USD 14.47 billion by 2031, growing at a CAGR of 31.93% from 2026 to 2031. The Cybersecurity for AI Models and LLMs Market is expanding because AI tools now sit at the core of workflows, and each model interaction creates a new point of exposure. Enterprise AI adoption moved faster than security tooling, which left many organizations with production deployments but weak prompt, runtime, and governance controls. The Cybersecurity for AI Models and LLMs Market is also benefiting from buyer preference for platforms that combine prompt protection, runtime monitoring, and governance in a single environment rather than across disconnected tools. Large companies still account for most current spending, but the demand base is widening as smaller firms also use third-party AI services without mature controls. The Cybersecurity for AI Models and LLMs Market still faces pressure from rapid model changes, uneven standards, and skills gaps, yet these same frictions are also pushing organizations to invest earlier in durable controls and external expertise.

Key Report Takeaways

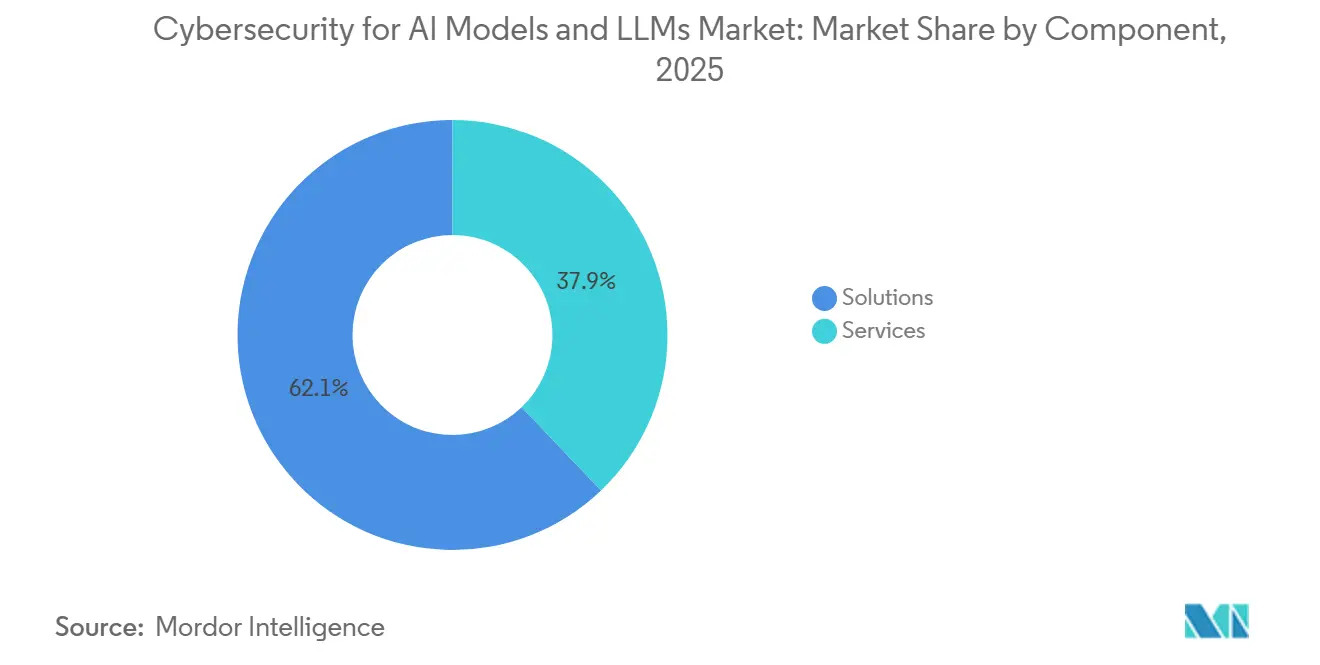

- By component, solutions held 62.14% share of the Cybersecurity for AI Models and LLMs Market in 2025, while services are projected to expand at a 32.98% CAGR through

- By security type, model security held 28.21% share in 2025, while governance, risk, and compliance is projected to expand at a 33.09% CAGR through 2031.

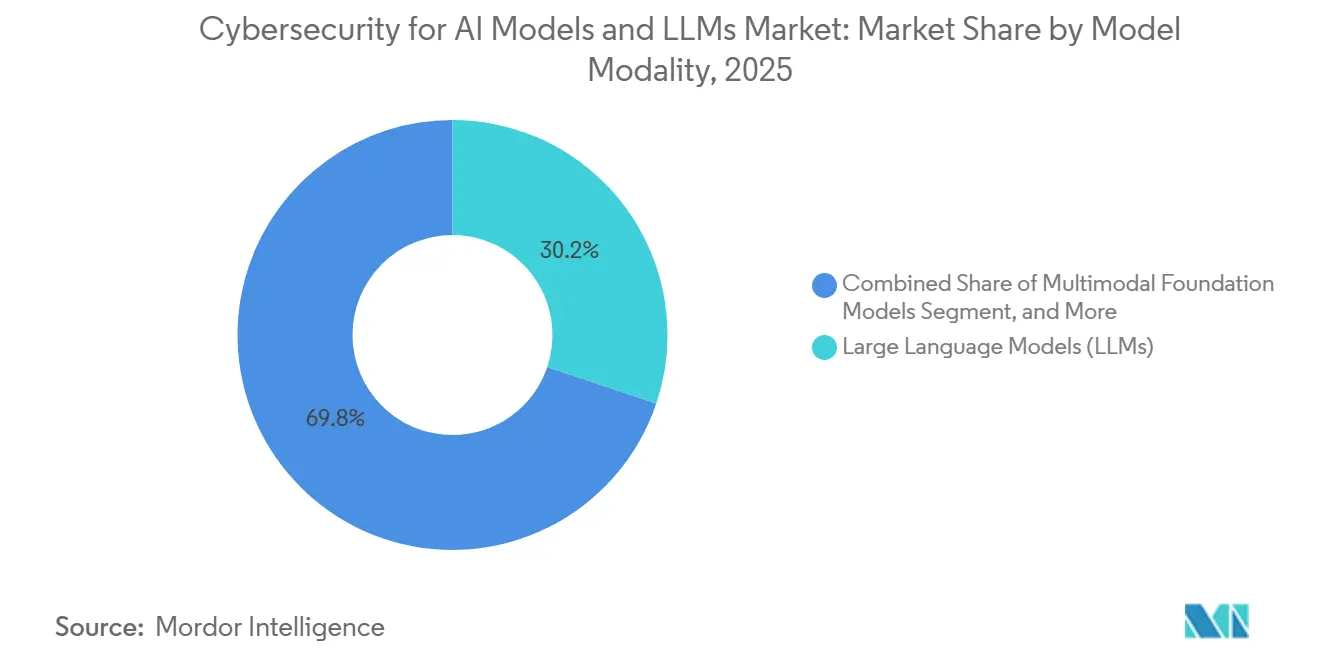

- By model modality, large language models held 30.17% share of the Cybersecurity for AI Models and LLMs Marketin 2025, while multimodal foundation models are projected to expand at a 33.20% CAGR through 2031.

- By deployment, cloud held 55.18% share in 2025, while hybrid deployment is projected to expand at a 33.31% CAGR through 2031.

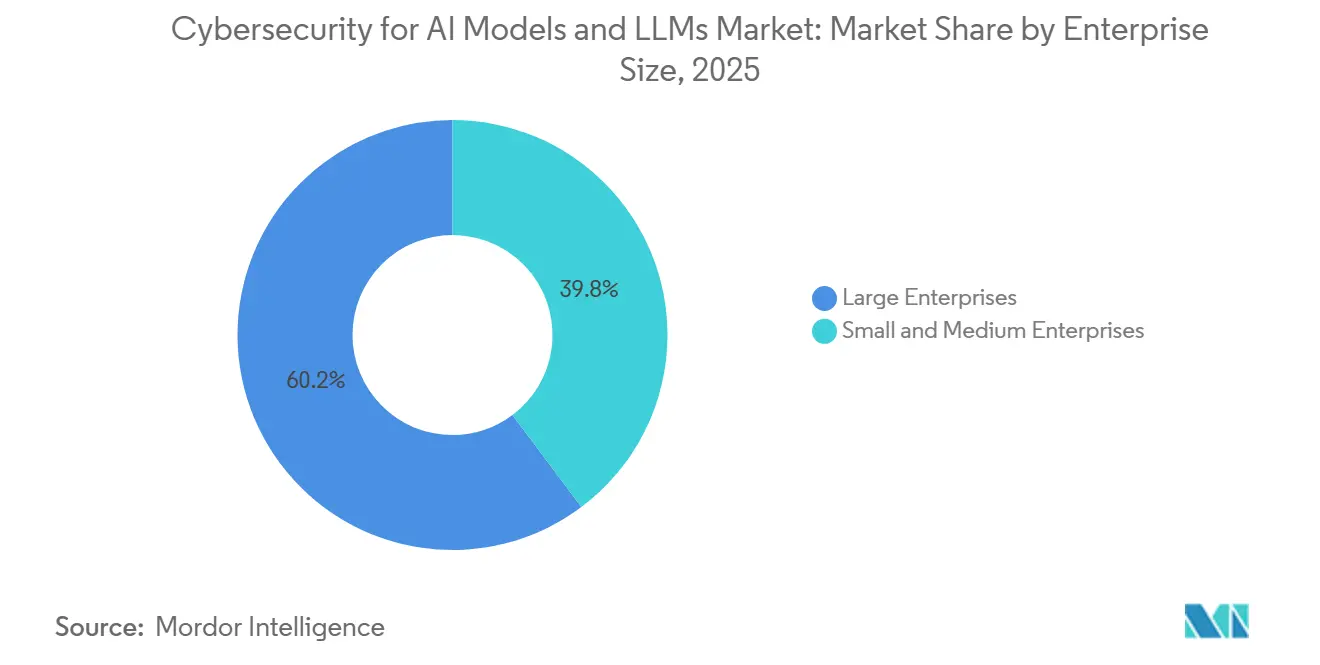

- By enterprise size, large enterprises held 60.23% share of the Cybersecurity for AI Models and LLMs Market in 2025, while SMEs are projected to expand at a 33.42% CAGR through 2031.

- By end-user industry, BFSI held 17.19% share in 2025, while healthcare and life sciences are projected to expand at a 33.53% CAGR through 2031.

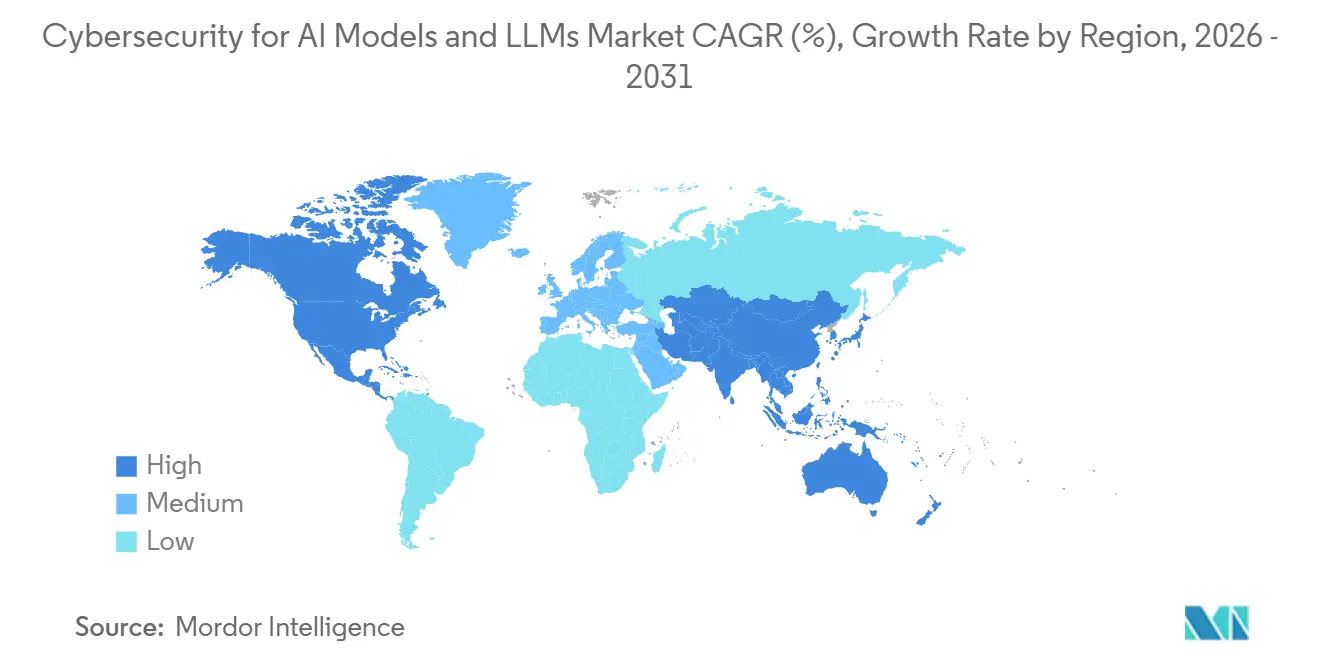

- By geography, North America held 33.14% share in 2025, while Asia-Pacific is projected to expand at a 33.64% CAGR through 2031 in the Cybersecurity for AI Models and LLMs Market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cybersecurity For AI Models and LLMs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prompt Injection and Jailbreak Attempts | +5.2% | Global, with highest incidence in North America and Asia-Pacific | Short term (≤ 2 years) |

| Expanding AI Model Attack Surface Across Enterprise Workflows | +4.8% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Regulatory Pressure for AI Governance and Model Accountability | +4.5% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Adversarial Use of GenAI for Automated Social Engineering | +3.8% | Global, with high exposure in BFSI and government sectors | Short term (≤ 2 years) |

| Model Supply Chain Risk Across APIs, Plugins, and Open-Source Weights | +3.2% | Asia-Pacific core, North America, spillover to Europe | Medium term (2-4 years) |

| Demand for Continuous AI Red-Teaming and Runtime Policy Enforcement | +2.9% | North America and Europe, with early adoption in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prompt Injection and Jailbreak Attempts

Prompt injection has become the most visible weakness in deployed generative AI systems, and the exposure is widening as enterprises connect models to data stores, tools, and agents. OWASP ranked prompt injection as LLM01 for 2025 and noted that 53% of enterprise AI deployments rely on retrieval-augmented generation or agentic pipelines, which are particularly vulnerable to indirect injection via retrieved content.[1]OWASP Gen AI Security Project, “LLM01 2025 Prompt Injection,” OWASP, genai.owasp.org A 2026 review described a June 2025 disclosure of a GitHub Copilot Chat CVSS 9.6 flaw that enabled the exfiltration of secrets and source code from private repositories via indirect prompt injection. Research circulated in January 2026 also described prompt injection as a multistep malware delivery mechanism that now extends into persistence and lateral movement in a large share of observed incidents. This is why the Cybersecurity for AI Models and LLMs Market is seeing steady demand for prompt firewalls, runtime guardrails, and adversarial red-teaming tools that can test how attacks evolve across chained workflows.

Expanding AI Model Attack Surface Across Enterprise Workflows

AI models are now embedded in code generation, legal review, customer support, and financial analysis, so the attack surface now stretches across every process that sends information into a model or acts on its output. CrowdStrike said its platform telemetry identified more than 1,800 AI applications across customer environments in 2026, covering nearly 160 million unique application instances.[2]CrowdStrike Holdings, Inc., “CrowdStrike Establishes the Endpoint as the Epicenter for AI Security,” CrowdStrike Investor Relations, ir.crowdstrike.com A 2026 Check Point report stated that only 17% of organizations had broadly deployed runtime LLM controls such as input validation, output filtering, and tool-use authorization across AI-connected applications. As agentic systems start routing actions through Model Context Protocol servers, each third-party connection adds another supply chain point that many asset inventories still do not track. The Cybersecurity for AI Models and LLMs Market is therefore gaining from rising demand for AI asset discovery, shadow AI governance, and endpoint-level runtime protection.

Regulatory Pressure for AI Governance and Model Accountability

Regulatory deadlines are turning AI governance from a policy topic into a direct trigger for software and services buying. The European Commission stated that high-risk obligations under the EU AI Act will become enforceable from August 2, 2026, with penalties that can reach EUR 35 million or 7% of global annual turnover.[3]European Commission, “AI Act Shaping Europe’s Digital Future,” European Commission, digital-strategy.ec.europa.eu In India, advisories issued in April 2026 and June 2026 called for controls over prompt injection, data poisoning, model manipulation, and documented AI governance across banks and payment operators. China also put amended cybersecurity provisions into effect on January 1, 2026, and added explicit focus on AI system risks, while national standards for generative AI security had already entered into force in late 2025. The Cybersecurity for AI Models and LLMs Market is moving higher because organizations now need auditable controls that can withstand regulatory review, even when models operate through tools and agents.

Adversarial Use of GenAI for Automated Social Engineering

Generative AI is changing social engineering by eliminating the effort required to create large volumes of convincing lures. Microsoft Threat Intelligence reported in June 2026 that threat actors were running AI brand impersonation campaigns that distributed up to 100,000 phishing emails a day, and one Claude-themed operation targeted more than 2,000 organizations across 62% in the United States.[4]Microsoft Security Blog, “AI Brands as Bait How Threat Actors Are Using the AI Hype in Social Engineering,” Microsoft, microsoft.com Academic research published in 2025 found that recipients rated LLM-generated spear-phishing emails built from public social media data as more persuasive and less suspicious than genuine phishing across five models and nearly 18,000 emails. Attackers are also using employee demand for new AI tools as a lure, turning trusted model brands into a path for malware delivery. This supports the Cybersecurity for AI Models and LLMs Market because enterprises need stronger controls over AI application access, browser-level prompt inspection, and workforce simulation programs tied to AI-branded phishing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly Changing Model Architectures Outpacing Security Controls | -3.6% | Global | Short term (≤ 2 years) |

| Limited Standardization for AI Security Benchmarks and Testing | -2.8% | Global, with higher friction in Europe and Asia-Pacific | Medium term (2-4 years) |

| High False Positive Rates in Output Filtering and Detection | -2.1% | Global | Short term (≤ 2 years) |

| Talent Shortage in AI Security, MLops, and Threat Research | -3.2% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapidly Changing Model Architectures Outpacing Security Controls

Security tools that worked for one model generation often need major adjustment when the architecture changes. The move from text-only systems to multimodal models introduced image-based prompt injection, adversarial audio, and cross-modality jailbreaks that text-focused scanners were not built to detect. Research published in March 2026 also identified weaknesses in a unified multimodal model, in which generation and understanding functions create bidirectional attack paths within the same system. Frequent model updates also shorten the shelf life of red-team findings, because a test against one version may no longer hold after the next release. This slows the Cybersecurity for AI Models and LLMs Market because buyers hesitate when tool requirements keep shifting with model design, model behavior, and new modalities.

Talent Shortage in AI Security, MLops, and Threat Research

The shortage of people who can secure AI systems is growing faster than normal hiring channels can fill. Fortinet reported in 2026 that 60% of organizations named AI-specific cybersecurity talent as their primary recruiting challenge, while 71% said the broader skills gap posed a material risk to their organizations. The Linux Foundation stated in 2026 that security concerns had risen sharply as a barrier to AI adoption, and 57% of organizations reported a significant capacity gap in AI security and risk management. AI red-teaming, MLops security, and adversarial ML work require a mix of engineering, data, and offensive security skills that formal pipelines still do not produce at scale. This limits the speed at which the Cybersecurity for AI Models and LLMs Market can convert software demand into full operational adoption, because many buyers still need outside help to run the tools they purchase.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Set To Outpace Solutions In Growth Rate

Solutions held 62.14% of the Cybersecurity for AI Models and LLMs market share in 2025, indicating that buyers initially focused on deploying dedicated prompt security, runtime monitoring, output filtering, and governance products. That early spending pattern also reflected the urgency of closing visible control gaps before enterprises built long service relationships around AI security operations. AI red-teaming and validation platforms, along with AI governance and compliance tools, attracted strong demand because organizations need repeated testing rather than one-time checks. The solutions side of the Cybersecurity for AI Models and LLMs Market also benefited from buyers wanting fast deployment and direct policy control. This kept solutions in the lead even as service demand continued to rise.

Services are projected to expand at a 32.98% CAGR through 2031, surpassing solutions in growth as customers seek external expertise they cannot hire internally. The work required here differs from traditional managed security, as teams need to craft adversarial prompts, assess output drift, and map model behavior to AI risk taxonomies in live enterprise settings. SplxAI reported 127% quarter-over-quarter growth after launching in August 2024, and followed that performance with a USD 7 million seed round in March 2025 to scale its capabilities. A 2026 SANS research summary also pointed to a sharp rise in demand for specialist AI security roles from 2025 to 2026. For that reason, the Cybersecurity for AI Models and LLMs Market is likely to see managed red-teaming, governance advisory, and AI incident response grow faster than many buyers expected at the start of large-scale LLM adoption.

By Security Type: GRC Moves From Compliance Task To Operating Layer

Model security held the largest share at 28.21% in 2025, reflecting immediate buyer concern about prompt injection, model integrity, and adversarial manipulation. Those controls were the most urgent because they sat closest to the model and directly addressed visible failure modes in deployed applications. The Cybersecurity for AI Models and LLMs Market also saw steady demand for data security and application security, because retrieval-augmented generation ties data access and application behavior together in the same workflow. As a result, buyers increasingly treated the model boundary, the application layer, and the data path as a single risk surface rather than separate procurement tracks. This supported a broader mix of controls across the security type stack.

Governance, risk, and compliance is projected to grow at a 33.09% CAGR through 2031, making it the fastest-growing security type in the Cybersecurity for AI Models and LLMs Market. The shift is tied to procurement behavior because boards, legal teams, and risk functions now want evidence that AI systems were tested, documented, and monitored before wide deployment. India’s 2026 advisory described AI agents as privileged non-human identities, which pushed identity, access, and governance concerns closer together in enterprise control design. Enterprises are also asking vendors for adversarial testing evidence, AI incident playbooks, and alignment with NIST AI RMF functions before moving forward with purchase decisions. This is why GRC has moved from a back-office requirement into a central operating layer for enterprise AI security programs.

By Model Modality: LLMs Keep The Lead While Multimodal Risk Widens

Large language models held 30.17% of the market in 2025, supported by broad enterprise use in customer support, coding assistance, summarization, and internal knowledge tools. LLMs also remained the most researched modality, so buyers had a clearer view of prompt injection, jailbreaks, and output filtering risks than they had for other model types. That clarity helped the Cybersecurity for AI Models and LLMs Market build around practical controls for text-based deployments first. It also meant vendors could package and sell more defined protection features into enterprise budgets. The LLM base, therefore, continued to anchor current spending even as other modalities gained ground.

Multimodal foundation models are projected to expand at a 33.20% CAGR through 2031, driven by use cases in imaging, financial document analysis, and agentic systems that process text, images, and audio together. The Cloud Security Alliance reported in 2025 that tested multimodal systems were 18 to 40 times more likely to generate harmful information under adversarial conditions than single-modality models. Research from 2026 also showed that multimodal architectures introduce attack paths that do not exist in pure text systems, which raises control complexity at the point of deployment. Image, audio, speech, and video generation models are still a small part of the Cybersecurity for AI Models and LLMs Market, but they offer room for vendors that can scan across modalities rather than protect only text inputs. That gives cross-modal detection and policy enforcement an advantage as enterprise AI portfolios diversify.

By Deployment: Hybrid Adoption Rises As Governance Needs Deepen

Cloud deployment accounted for 55.18% of the market in 2025, reflecting the fact that most enterprise AI applications first went live via APIs and cloud-native software stacks. Major hyperscaler ecosystems hosted a large share of these workloads, but infrastructure security at the host level did not eliminate the need for application-level model security, prompt inspection, or output filtering. This left cloud customers with clear responsibility at the model interaction layer, which supported near-term software spending in the Cybersecurity for AI Models and LLMs Market. On-premises deployments remained important for regulated use cases where data residency, latency, or internal policy limited cloud use. The cloud segment, therefore, led in installed demand, even as architectural choices continued to evolve.

Hybrid deployment is projected to expand at a 33.31% CAGR in the Cybersecurity for AI Models and LLMs market size through 2031, making it the fastest-growing deployment model. Many organizations now keep sensitive, fine-tuned models or data-heavy workloads on-premises while still connecting to cloud APIs for general inference and broader functionality. That design increases flexibility, but it also creates policy and logging challenges because input controls and output reviews must work the same way across both environments. Cisco said its February 2026 AI Defense expansion added AI supply chain governance, agentic guardrails, and broader control features aimed at this mixed deployment reality. As a result, the Cybersecurity for AI Models and LLMs Market is shifting toward tools that can enforce a single policy fabric across cloud, on-premises, and hybrid deployments.

By Enterprise Size: SMEs Become The Next Adoption Wave

Large enterprises held 60.23% of the market in 2025 because they adopted AI earlier, had internal security teams, and could fund point solutions before platform consolidation took hold. These companies also faced greater regulatory and reputational exposure in sectors such as banking, healthcare, and government, making AI security spending hard to defer. Their buying activity gave the Cybersecurity for AI Models and LLMs Market an early revenue base and helped define feature priorities for vendors. In many cases, large buyers also demanded more evidence around testing, monitoring, and response readiness than smaller firms did. That kept enterprise accounts at the center of current vendor roadmaps.

SMEs are projected to expand at a 33.42% CAGR through 2031, indicating a wider addressable base for the Cybersecurity for AI Models and LLMs Market over the next few years. Many smaller firms use AI through third-party APIs and SaaS products, but they often do so without prompt inspection, output filtering, or dedicated leakage controls. A 2025 BigID study said only 6% of organizations had deployed an advanced AI security strategy, with readiness skewed heavily toward larger enterprises. Vendors are responding with simpler onboarding, API-native integrations, and usage-based pricing that fits below heavy enterprise procurement thresholds. This lowers adoption friction and turns SMEs into a meaningful source of incremental demand rather than a distant secondary segment.

By End-User Industry: Healthcare And Life Sciences Builds The Fastest Momentum

BFSI accounted for 17.19% of the Cybersecurity for AI Models and LLMs Market in 2025, making it the largest end-user vertical. Banks, insurers, and payment firms were early users of AI in know-your-customer workflows, anti-money laundering screening, credit models, and fraud systems, and each of those use cases requires auditable outputs and tested controls. The regulated institution also remains accountable for the outcome, even if a model vendor supplied the tool, which keeps the business case for model security direct and immediate. This accountability structure helped BFSI become a stable demand anchor in the Cybersecurity for AI Models and LLMs industry. It also explains why financial buyers continue to ask for evidence of governance, testing, and response discipline before scaling production use.

Healthcare and life sciences are projected to grow at a 33.53% CAGR through 2031, which gives it the fastest pace among end-user groups in the Cybersecurity for AI Models and LLMs Market. Clinical LLM use introduces a different problem because retrieval workflows can pull full patient records into context windows, which cuts against the minimum necessary standard for protected health information. A 2026 review in Frontiers in Artificial Intelligence identified retrieval-augmented generation pipelines and reliance on third-party AI services as the two highest-risk exposure points for PHI leakage in healthcare LLM deployments. Information technology and telecom, retail and e-commerce, industrial manufacturing, and government are also moving higher as they add AI to customer interfaces, operations, and service delivery. Even so, healthcare is moving faster because the cost of weak controls can quickly combine privacy risks, clinical risks, and regulatory liability in a single deployment.

Geography Analysis

North America held 33.14% of the Cybersecurity for AI Models and LLMs market share in 2025, making it the largest regional revenue base. The United States remained the core market because it combines dense enterprise AI adoption, major platform vendors, and active sector guidance across financial and public institutions. Canada added support through strong adoption in healthcare and financial services, while Mexico remained a smaller but developing market. Europe followed, with demand shaped by compliance urgency, and Germany led regional spending through active guidance from the Federal Office for Information Security and its work on AI design principles and AI software bill of materials. The Cybersecurity for AI Models and LLMs Market in Europe is also being boosted by the EU AI Act, DORA, and national cyber rules that are integrating AI security into broader IT risk budgets.

Asia-Pacific is projected to expand at a 33.64% CAGR in the Cybersecurity for AI Models and LLMs market through 2031, making it the fastest-growing region. China is a major reason, because amended cybersecurity rules that took effect on January 1, 2026, explicitly addressed AI system risks, while generative AI security standards had already entered force in late 2025. India is also moving quickly after the Reserve Bank of India issued sector-level advisories in 2026 that covered prompt injection, model manipulation, and governance documentation. Japan and South Korea are adding momentum through industrial AI deployments that require stronger security controls as usage broadens across enterprise workflows. This combination of regulation and deployment scale gives Asia-Pacific a faster growth path than more mature regions.

South America remained a smaller regional market for Cybersecurity for AI Models and LLMs in 2025, with Brazil as the clear leader due to its fintech base and established data protection framework. Argentina contributed to regional awareness through an active technology community, even though broader economic conditions stayed difficult. The Middle East and Africa were still at an earlier stage, but the United Arab Emirates and Saudi Arabia moved ahead through national AI strategies that include cybersecurity-by-design requirements for sovereign AI efforts. South Africa and Nigeria remained nascent markets, where demand is tied to wider use of cloud-hosted AI applications in financial services and other service-led sectors.

Competitive Landscape

The Cybersecurity for AI Models and LLMs Market remains moderately fragmented, with large platform vendors and AI-native specialists competing across overlapping control layers. Established cybersecurity companies are expanding through product development and tighter platform packaging, while younger firms are focusing on deep model-layer or agentic system use cases. Palo Alto Networks used this approach when it launched Prisma AIRS 3.0 in March 2026, combining agent discovery, risk assessment, adversarial red-teaming, runtime governance, and an AI Agent Gateway into a single architecture. That move showed that buyers increasingly want fewer tools and broader coverage across the full AI lifecycle. It also reinforced the shift in the Cybersecurity for AI Models and LLMs Market toward platform consolidation rather than isolated point products.

CrowdStrike pushed a similar strategy in March 2026, adding endpoint-focused AI runtime protection, shadow AI discovery, and prompt-layer protection for desktop AI applications, including ChatGPT, Gemini, Claude, and Microsoft Copilot. Cisco also expanded AI Defense in February 2026 with AI supply chain governance, algorithmic red-teaming, real-time agentic guardrails, and an AI-aware SASE layer. These moves matter because they position existing infrastructure footprints as control planes for AI risk, giving large vendors a channel advantage as enterprise budgets tighten. At the same time, the Cybersecurity for AI Models and LLMs Market still leaves room for specialists who can solve narrower problems better than broad platforms can. That is why new entrants remain visible despite growing consolidation.

White space still exists in areas such as MCP server security, multi-agent trust verification, and AI-specific forensic readiness, where deeper technical coverage is still limited. SplxAI is one example, focusing on offensive security for agentic AI systems and a commercial model built around automated red-teaming and governance needs. Palo Alto Networks Unit 42 also documented the Model Namespace Reuse attack in 2025, demonstrating how supply chain weaknesses can expose remote code execution across AI development environments. Vendors that align product design with OWASP LLM risks and adversarial ML taxonomies are gaining procurement traction because they can link product features to recognized control frameworks. This keeps the Cybersecurity for AI Models and LLMs Market competitive, but it also favors companies that can combine technical depth with enterprise-ready governance and deployment scale.

Cybersecurity For AI Models and LLMs Industry Leaders

Microsoft Corporation

Amazon Web Services, Inc.

Google LLC

International Business Machines Corporation

Palo Alto Networks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Reserve Bank of India (RBI) expands AI cyber advisory to payment system operators. Following its April 2026 advisory to all commercial banks, the RBI issued AI-Accelerated Cyber Threats and Related Safeguards (AI-ACT&RS) guidelines to all authorised non-bank payment system operators on June 1, 2026, mandating controls for prompt injection, data poisoning, model manipulation, AI agent governance, and third-party AI risk management. This makes India the first major emerging market to impose sector-wide binding AI model security requirements on both banking and payments institutions.

- June 2026: EU AI Act high-risk obligations and AI omnibus political agreement take effect. High-risk AI system rules under Annex III of the EU AI Act became enforceable from August 2, 2026. A political agreement on the "AI omnibus" simplification package was reached on May 7, 2026, following adoption of the proposal by the European Commission on November 19, 2025. Penalties for prohibited practices reach EUR 35 million (USD 39.5 million) or 7% of global annual turnover. This regulatory milestone represents the largest single compliance-driven procurement event in the history of the AI security market.

- March 2026: Palo Alto Networks launches Prisma AIRS 3.0 with full AI agent lifecycle security. The platform includes agent discovery, risk assessment, adversarial red-teaming mapped to the OWASP Top 10 for Agentic Applications (2026), runtime governance, and an AI Agent Gateway. Capabilities include over 50 attack techniques aligned to OWASP and NIST AI RMF, with multi-turn red-teaming and support for autonomous and multi-agent systems.

Global Cybersecurity For AI Models and LLMs Market Report Scope

The Cybersecurity for AI Models and LLMs market covers solutions and services that protect large language models (LLMs) and other foundation AI models from adversarial attacks, misuse, and systemic vulnerabilities. It includes prompt security, runtime monitoring, output moderation, data leakage prevention, AI red teaming, and governance frameworks to ensure the integrity, reliability, and compliance of advanced AI systems across text, image, audio, and video modalities. The market is driven by the rapid adoption of generative AI, rising risks such as prompt injection, model theft, data poisoning, and synthetic content misuse, along with growing demand for regulatory compliance and trustworthy AI governance. Organizations across BFSI, healthcare, IT, manufacturing, retail, and government are deploying these solutions to secure AI pipelines, protect sensitive data, and maintain resilience. Its primary goal is to enable secure, transparent, and trustworthy AI ecosystems by integrating proactive defenses, continuous monitoring, and governance frameworks that mitigate risks while supporting safe innovation and deployment of advanced AI technologies.

The Cybersecurity for AI Models and LLMs market report is segmented by Component (Solutions [Prompt Security Solutions, Runtime Security and Monitoring, Output Security and Content Moderation, Data Security and Leakage Prevention, AI Red Teaming and Validation Platforms, AI Governance and Compliance Platforms] and Services), Security Type (Model Security, Data Security, Application Security, Identity and Access Security, Governance, Risk and Compliance (GRC)), Model Modality (Large Language Models (LLMs), Multimodal Foundation Models, Image Generation Models, Audio and Speech Models, Video Generation Models), Deployment (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Prompt Security Solutions |

| Runtime Security and Monitoring | |

| Output Security and Content Moderation | |

| Data Security and Leakage Prevention | |

| AI Red Teaming and Validation Platforms | |

| AI Governance and Compliance Platforms | |

| Services |

| Model Security |

| Data Security |

| Application Security |

| Identity and Access Security |

| Governance, Risk and Compliance (GRC) |

| Large Language Models (LLMs) |

| Multimodal Foundation Models |

| Image Generation Models |

| Audio and Speech Models |

| Video Generation Models |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | Prompt Security Solutions | |

| Runtime Security and Monitoring | |||

| Output Security and Content Moderation | |||

| Data Security and Leakage Prevention | |||

| AI Red Teaming and Validation Platforms | |||

| AI Governance and Compliance Platforms | |||

| Services | |||

| By Security Type | Model Security | ||

| Data Security | |||

| Application Security | |||

| Identity and Access Security | |||

| Governance, Risk and Compliance (GRC) | |||

| By Model Modality | Large Language Models (LLMs) | ||

| Multimodal Foundation Models | |||

| Image Generation Models | |||

| Audio and Speech Models | |||

| Video Generation Models | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Information Technology and Telecom | |||

| Retail and E-commerce | |||

| Industrial Manufacturing | |||

| Government and Public Sector | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 value of the Cybersecurity for AI Models and LLMs Market?

The Cybersecurity for AI Models and LLMs Market is projected at USD 3.62 billion in 2026 and is forecast to reach USD 14.47 billion by 2031 at a 31.93% CAGR.

What is driving adoption of cybersecurity tools for AI models and LLMs?

The strongest drivers are rising prompt injection attempts, wider AI use across enterprise workflows, tighter governance rules, and the use of generative AI in social engineering attacks.

Which component is leading revenue and which is growing faster?

Solutions led with 62.14% share in 2025, while services are projected to expand faster at a 32.98% CAGR through 2031.

Which region is growing the fastest for cybersecurity in AI deployments?

Asia-Pacific is projected to record the fastest growth at a 33.64% CAGR through 2031, supported by tighter rules in China and India and broader enterprise AI adoption.

Which end-user group is expanding the fastest?

Healthcare and life sciences is projected to grow at a 33.53% CAGR because clinical LLM deployments create high privacy and governance exposure, especially around PHI handling.

How competitive is the vendor environment for securing AI models and LLMs?

The field is moderately fragmented. Large vendors such as Palo Alto Networks, CrowdStrike, and Cisco are broadening platform coverage, while specialists still hold room in model-layer and agentic security use cases.

Page last updated on: