Application Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

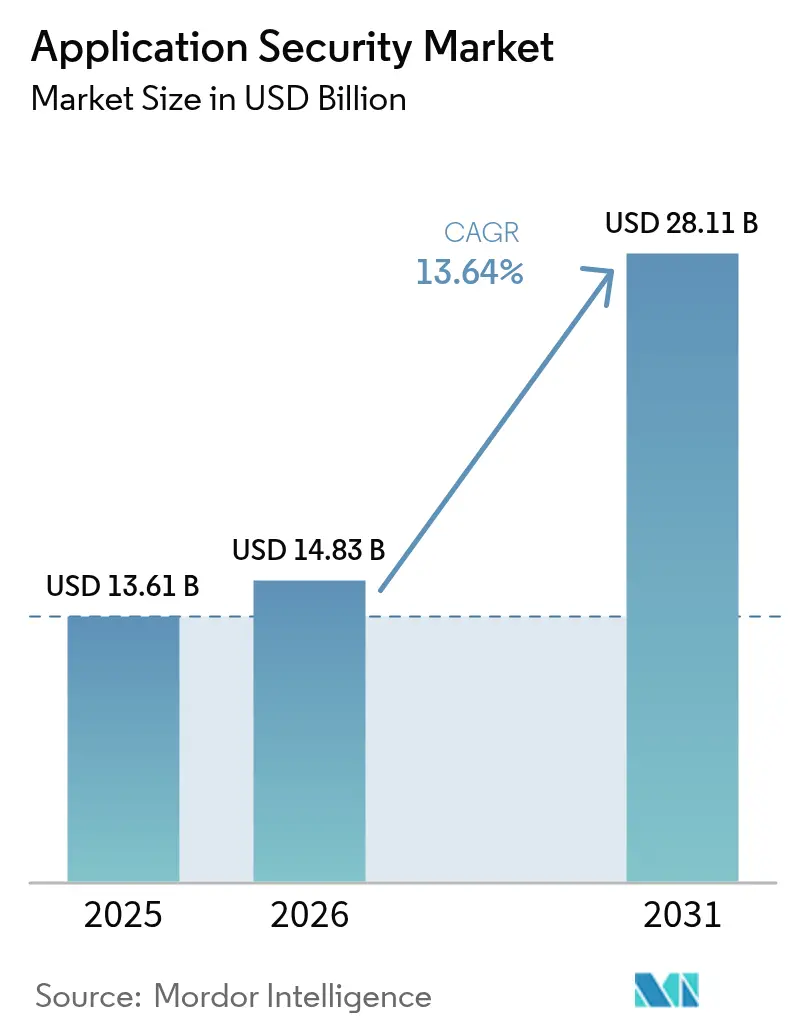

| Market Size (2026) | USD 14.83 Billion |

| Market Size (2031) | USD 28.11 Billion |

| Growth Rate (2026 - 2031) | 13.64% CAGR |

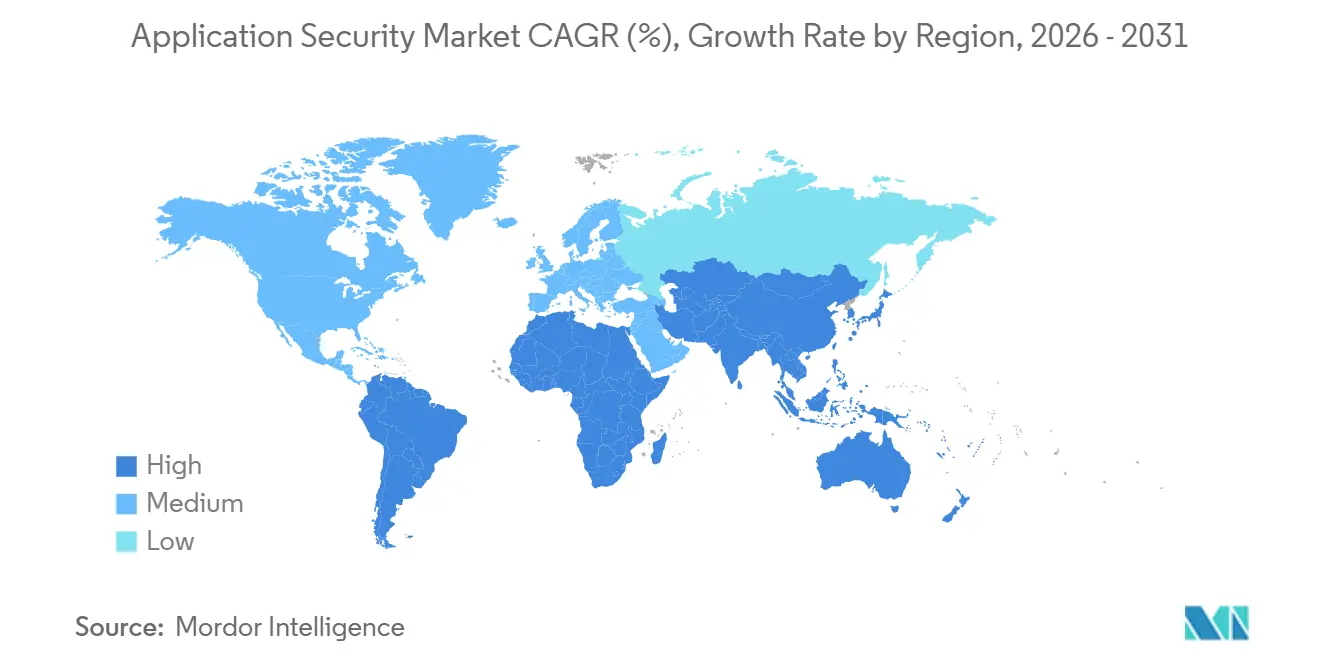

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Application Security Market Analysis by Mordor Intelligence

The application security market size is expected to increase from USD 13.61 billion in 2025 to USD 14.83 billion in 2026 and reach USD 28.11 billion by 2031, growing at a CAGR of 13.64% over 2026-2031. Continuous integration pipelines now embed code scanning at every commit, multiplying tool usage across development, staging and production layers. Enterprises are pivoting toward API-aware testing after United States regulators highlighted that 42% of 2025 web incidents involved insecure interfaces. Deadlines such as the March 2025 mandate for full PCI-DSS 4.0 compliance compressed buying cycles, accelerating adoption of software composition analysis and runtime protection. Meanwhile, dynamic and interactive testing suites are displacing stand-alone static analyzers as organizations seek to detect business-logic flaws during live execution. Mergers, especially by large platform vendors buying niche API, container and supply-chain specialists, are reshaping competitive dynamics and expanding bundled DevSecOps suites.

Key Report Takeaways

- By component, solutions commanded 61.48% of 2025 revenue, while services are advancing at a 13.67% CAGR through 2031.

- By deployment mode, cloud platforms held 57.81% of spending in 2025, and the segment is expanding at a 13.77% CAGR to 2031.

- By organization size, large enterprises captured 60.58% of 2025 outlays, whereas small and medium enterprises are set to grow at a 13.72% CAGR during 2026-2031.

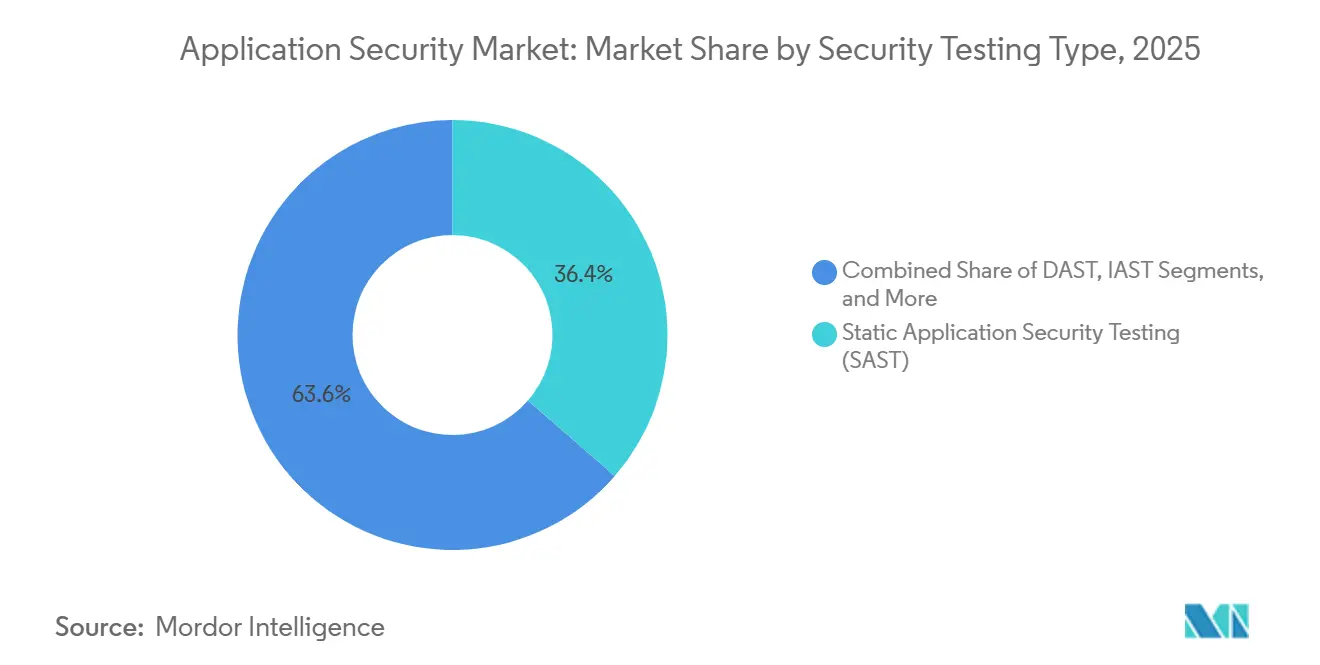

- By security testing type, static application security testing secured 36.38% of 2025 revenue, while interactive application security testing is projected to grow at a 13.69% CAGR to 2031.

- By end-user industry, banking, financial services and insurance led with 24.83% share in 2025, whereas healthcare is forecast to expand at a 13.79% CAGR through 2031.

- By geography, North America accounted for 40.91% of 2025 revenue, while Asia-Pacific records the highest 13.83% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Application Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Volume and Sophistication of Web-, Mobile- and API-Based Attacks | +2.8% | Global, with acute pressure in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rapid Adoption of DevSecOps Toolchains | +2.5% | North America and Europe lead; Asia-Pacific following | Medium term (2-4 years) |

| Expanding Regulatory Mandates (PCI-DSS 4.0, GDPR, DORA, etc.) | +2.3% | Europe and North America; spillover to APAC financial hubs | Medium term (2-4 years) |

| Growth in Third-Party SaaS and API Integrations | +1.9% | Global, especially North America and Europe | Long term (≥ 4 years) |

| Mandatory SBOM Disclosure Post-US Executive Order 14028 | +1.6% | United States federal contractors; expanding to commercial sector | Medium term (2-4 years) |

| AI-Generated Code Inflating Unknown Vulnerabilities | +1.4% | Global, concentrated in tech hubs adopting generative AI tools | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Volume And Sophistication Of Web, Mobile And API-Based Attacks

Attackers increasingly bypass perimeter controls by exploiting poorly authenticated API endpoints, broken object-level authorization and excessive data exposure, vulnerabilities flagged in the 2024 OWASP API Security Top 10. Financial services firms logged a 67% jump in API-driven fraud attempts during 2025 as adversaries manipulated unchecked input parameters in mobile banking apps.[1]Financial Services Information Sharing and Analysis Center, “API Fraud Trends Report 2025,” FSISAC.com Enterprises consequently deploy dynamic and interactive testing that replay malicious payloads inside running applications, combined with real-time gateways inspecting every request. Mobile software faces similar scrutiny because regulators now mandate biometric authentication and encrypted local storage, forcing agile teams to schedule security scans within each sprint. The immediate business risk of data exfiltration and account takeover makes this driver the single largest catalyst for new spending across the application security market.

Rapid Adoption Of DevSecOps Toolchains

Automated security scans built into continuous integration and continuous delivery pipelines reduced median time to vulnerability detection from 21 days in 2023 to 4 days in 2025, as reported by GitLab’s global survey.[2]GitLab Inc., “2025 Global DevSecOps Report,” about.gitlab.com Kubernetes clusters now enforce policy engines that block containers containing critical flaws, pushing remediation upstream before code can merge. Cloud providers supply native dashboards highlighting application-layer weaknesses alongside infrastructure misconfigurations, giving developers an end-to-end risk posture within familiar consoles. Nevertheless, the average organization already runs seven distinct scanners, creating alert fatigue and integration overhead that vendors address through unified orchestration platforms. Overall, embedding security controls directly inside developer workflows expands addressable usage moments and fuels compounding license growth across the application security market.

Expanding Regulatory Mandates (PCI-DSS 4.0, GDPR, DORA)

PCI-DSS 4.0 added 53 new checkpoints effective March 2025, including compulsory software composition analysis for any application touching card data.[3]Payment Card Industry Security Standards Council, “PCI DSS v4.0 Summary of Changes,” pcisecuritystandards.org Europe’s Digital Operational Resilience Act obliges quarterly threat-led penetration tests and immutable audit logs of every code commit for financial entities. GDPR’s privacy-by-design principle drives adoption of static analyzers that flag insecure data handling at commit time. Auditors now demand continuous evidence rather than annual attestations, rewarding cloud testing platforms that stream machine-readable compliance artifacts. Similar rules emerge in Asia-Pacific and the Middle East, turning once voluntary safeguards into non-negotiable procurement criteria. This regulatory cascade steadily expands baseline purchasing across the application security market.

Growth In Third-Party SaaS And API Integrations

Modern software relies on an average of 23 external APIs for payment, identity verification and analytics, each extending the attack surface. United States guidance in 2024 now obligates SaaS vendors to declare upstream dependency risk, hastening adoption of supply-chain scanning. High-profile exploits, notably the SolarWinds compromise, highlighted how poisoned libraries enable wide breach blast radiuses, encouraging enterprises to run continuous software composition analysis. API gateways increasingly meld runtime self-protection functions, shutting down anomalous calls before they reach business logic. Automated dependency mapping and binary provenance tracking become mandatory capabilities, advancing the market toward holistic software supply-chain security.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership and Tool Complexity | -1.2% | Global, acute for SMEs in cost-sensitive markets | Short term (≤ 2 years) |

| Global Shortage of Secure-Coding Talent | -1.0% | North America and Europe; emerging in Asia-Pacific | Long term (≥ 4 years) |

| False-Positive Overload Eroding Developer Trust | -0.9% | Global, especially in organizations with legacy SAST deployments | Medium term (2-4 years) |

| Shift-Left Fatigue and Tool Sprawl | -0.7% | North America and Europe; early signs in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost Of Ownership And Tool Complexity

National Cyber Security Alliance research showed that 62% of small firms cited cost as the top barrier to automated testing in 2025. Beyond license fees, teams must allocate scarce engineers to configure scan rules, integrate outputs into ticketing systems and triage thousands of findings, roles commanding salaries above USD 120,000 in major hubs. Migration projects toward unified platforms can span 12-18 months, disrupting release cadences and prompting some businesses to defer modernization. Consumption-based cloud pricing introduces budget volatility, further complicating planning for cash-constrained organizations. As a result, potential buyers, particularly SMEs, may postpone full coverage, tempering short-term growth across the application security market.

Global Shortage Of Secure-Coding Talent

The United States anticipates a 15% annual shortfall of application security engineers through 2026. Universities internationally graduate fewer than 10,000 students annually versed in secure software, while demand exceeds 50,000 new positions in North America alone. Enterprises therefore lean on managed security providers for code review, penetration testing and remediation guidance, services that inflate operational cost yet only partially fill knowledge gaps. Generative AI-based coding assistants add complexity because unskilled programmers may unknowingly accept insecure snippets, raising remediation workload downstream. Persistent labor scarcity slows enterprises’ ability to operationalize advanced testing modalities, constraining the achievable pace of adoption, especially across regulated verticals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain As Enterprises Outsource Triage

Solutions maintained 61.48% of 2025 revenue, confirming entrenched demand for platforms that integrate seamlessly with source control and continuous integration flows. The services segment is growing at a 13.67% CAGR because organizations delegate penetration testing, alert triage and developer upskilling to global consulting firms, mitigating in-house talent shortages. Professional advisers negotiate complex seat-based licenses, configure rule sets and deliver audit-ready evidence, freeing product teams to ship features faster.

Managed services also combine automated scans with 24/7 human validation, ranking exploitable findings over theoretical flaws, a model prized by payment processors and healthcare systems under strict breach-notification laws. Solutions vendors bundle advisory hours into enterprise agreements, blurring lines between software and services and locking clients into long-term contracts. This convergence keeps platform spending steady while accelerating uptake of add-on incident-response and training offerings across the application security market.

By Deployment Mode: Cloud Platforms Embed Security Natively

Cloud deployment held 57.81% of revenue in 2025 and is projected to compound at 13.77% through 2031, buoyed by Amazon, Microsoft and Google integrating scanners inside developer consoles. Real-time feedback delivered within code editors eliminates context switching, encouraging continuous scanning and facilitating pay-as-you-go economics ideal for startups and small teams.

On-premise solutions remain indispensable for banks and defense agencies operating air-gapped environments that prohibit external code processing. Hybrid models are rising, with containerized testing engines deployed behind firewalls for sensitive modules, while less critical microservices run in public clouds. Vendors now ship identical feature sets across both modes, allowing customers gradual migration without tooling disruption. As regulatory data-sovereignty clauses tighten, flexible deployment remains a competitive differentiator within the application security market.

By Organization Size: SMEs Embrace Cloud-Native Security

Large enterprises captured 60.58% of 2025 spending, reflecting sizable portfolios and compliance overhead. Small and medium enterprises, however, are expanding at a 13.72% CAGR, empowered by consumption pricing and developer-centric interfaces. SMEs integrating IDE plug-ins detect vulnerabilities 40% faster than peers relying on stand-alone portals, shrinking remediation loops.

Fortune 500 companies grapple with polyglot stacks accumulated through acquisitions, necessitating broad language coverage and policy-as-code governance engines to enforce uniform thresholds. Conversely, SMEs typically standardize on modern frameworks, reducing configuration complexity. Cloud-hosted dashboards further democratize access by abstracting away scanner maintenance. As licensing tiers scale with active users, cost aligns closely with headcount, attracting budget-constrained founders and fueling grassroots expansion of the application security market.

By Security Testing Type: IAST Bridges Static And Dynamic Gaps

Static application security testing commanded 36.38% share in 2025, valued for scanning proprietary code at rest. Interactive application security testing is forecast to climb at a 13.69% CAGR because embedded agents observe live execution paths, pinpointing reachable vulnerabilities and cutting false positives. This context-rich insight appeals to teams fatigued by unverified SAST alerts and tight sprint schedules.

Dynamic scanners remain vital for black-box assessments of third-party packages lacking source access, while software composition analysis mitigates open-source supply-chain risk post-Log4Shell. Vendors orchestrate all modalities from unified dashboards, correlating risk scores so security teams can prioritize defects exploitable in production. The intersection of these techniques anchors multiproduct expansions, reinforcing vendor lock-in even as specialized startups drive innovation across the application security market.

By End-User Industry: Healthcare Accelerates Post-Breach

Banking, financial services and insurance preserved 24.83% of 2025 outlays, under relentless regulatory scrutiny demanding quarterly penetration tests and immutable audit trails. Healthcare is on track for a 13.79% CAGR through 2031 after 725 breach disclosures in 2025 cited application vulnerabilities as 38% of entry points. Ransomware incidents targeting electronic health records catalyze investment in automated scanning and runtime self-protection.

Retail and e-commerce prioritize API and DAST coverage to shield payment data during seasonal traffic surges, whereas government agencies favor on-premise SAST arrays due to classified data constraints. Education boards migrate student-information systems to SaaS, adopting lightweight cloud scanners to satisfy FERPA safeguards. Industrial manufacturers integrate scanners into operational technology projects as web interfaces proliferate across factory floors. Collectively, vertical-specific pressures diversify demand patterns while broadening the total addressable application security market size.

Geography Analysis

North America accounted for 40.91% of 2025 revenue, propelled by Executive Order 14028, which obliges vendors to supply software bills of materials for federal procurement. The United States Cybersecurity and Infrastructure Security Agency published baseline secure-software standards in 2024, effectively making application security controls contractual requirements for public-sector deals. Venture capital funding fosters constant startup formation, intensifying competition among incumbents and open-source challengers while driving rapid feature innovation.

Asia-Pacific delivers the fastest 13.83% CAGR through 2031 as India’s digital lending rules and Indonesia’s banking modernization require independent security audits and secure-by-design lifecycles. China’s Multi-Level Protection Scheme 2.0 enforces application-layer encryption and vulnerability disclosure, causing domestic platforms to embed SAST and DAST tooling from the earliest sprint. Compliance changes across Japan, South Korea and Australia further unify regional demand, prompting global vendors to add local data residency and language packs.

Europe benefits from the Digital Operational Resilience Act effective January 2025, mandating quarterly penetration testing for finance and pushing adoption of version-control-level audit trails. The forthcoming Cyber Resilience Act will extend secure-by-design duties to all software sold inside the single market, broadening scope beyond traditional regulated verticals. Middle East and Africa markets remain nascent but accelerate as sovereign-cloud mandates in Saudi Arabia and the United Arab Emirates require local hosting paired with certified security tooling. South America witnesses gradual uptake as financial regulators in Brazil and Mexico harmonize guidance with PCI-DSS 4.0, nudging banks and fintechs toward continuous testing. Collectively, compliance harmonization converges regional trajectories, enlarging the global application security market.

Competitive Landscape

The application security market remains moderately fragmented because the top five vendors held roughly 35% of 2025 global revenue. Synopsys, Checkmarx and Veracode differentiate by delivering unified SAST, DAST, IAST and SCA within a single license. Synopsys accelerated consolidation with three acquisitions between 2024-2025, most recently Apiiro, to fold risk-based prioritization and software supply-chain analytics into its Coverity platform.

Open-source-centric challengers, notably Snyk and GitLab, embed scanners inside commit workflows, winning developer mindshare and lowering switching costs. Cloud hyperscalers leverage control of CI/CD infrastructure to bundle scanning as value-add, threatening traditional license models. Meanwhile, API-focused startups such as Salt Security and Traceable AI carve niches by providing real-time behavioral analytics specialized for interface abuse patterns, a gap only partially addressed by multipurpose suites.

Artificial-intelligence-assisted triage emerges as white space; machine-learning engines analyze historical fix data to flag exploitable defects, trimming false positive noise that erodes developer trust. Vendors owning large proprietary vulnerability databases will wield an advantage in model training. Patent activity underscores vibrant innovation: the United States granted 127 testing-related patents in 2025, covering ML-based classification, automated remediation pull requests and runtime threat correlation. Competitive intensity is likely to remain high as market leaders balance acquisitions with organic R&D to preserve share across the expanding application security market.

Application Security Industry Leaders

IBM Corporation

Oracle Corporation

Veracode (Thoma Bravo)

Synopsys Inc.

Qualys Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Synopsys acquired Apiiro to add risk-based prioritization and supply-chain analytics to Coverity SAST.

- December 2025: Palo Alto Networks launched Prisma Cloud Code Security 3.0, introducing AI-driven remediation pull requests.

- November 2025: Snyk raised USD 200 million in Series G funding, valuing the company at USD 7.4 billion to expand into infrastructure-as-code scanning.

- October 2025: IBM integrated watsonx Code Assistant with Application Security on Cloud for in-editor guidance.

Global Application Security Market Report Scope

Application security encompasses measures taken to improve the security of an application, often by finding, fixing, and preventing security vulnerabilities. Different techniques surface security vulnerabilities at various stages of an application's lifecycle, such as design, development, deployment, upgrade, and maintenance.

The Application Security Market Report is Segmented by Component (Solutions, Services), Deployment Mode (Cloud, On-Premise), Organization Size (Small and Medium Enterprises, Large Enterprises), Security Testing Type (SAST, DAST, IAST, RASP, SCA), End-User Industry (BFSI, Healthcare, Retail and E-Commerce, Government and Defense, IT and Telecom, Education, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Cloud |

| On-Premise |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Static Application Security Testing (SAST) |

| Dynamic Application Security Testing (DAST) |

| Interactive Application Security Testing (IAST) |

| Run-Time Application Self-Protection (RASP) |

| Software Composition Analysis (SCA) |

| BFSI |

| Healthcare |

| Retail and E-Commerce |

| Government and Defense |

| IT and Telecom |

| Education |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Solutions | |

| Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By Organization Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Security Testing Type | Static Application Security Testing (SAST) | |

| Dynamic Application Security Testing (DAST) | ||

| Interactive Application Security Testing (IAST) | ||

| Run-Time Application Self-Protection (RASP) | ||

| Software Composition Analysis (SCA) | ||

| By End-User Industry | BFSI | |

| Healthcare | ||

| Retail and E-Commerce | ||

| Government and Defense | ||

| IT and Telecom | ||

| Education | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected revenue for the application security market by 2031?

The sector is forecast to reach USD 28.11 billion by 2031.

Which deployment mode is growing fastest?

Cloud deployment is advancing at a 13.77% CAGR through 2031 as platforms embed native scanners.

Why are services gaining share within application security?

Organizations outsource vulnerability triage and developer training to managed providers, driving services at a 13.67% CAGR.

Which testing type is expected to outpace the rest?

Interactive application security testing leads growth with a 13.69% CAGR because it validates runtime exploitability.

Which region posts the highest growth rate?

Asia-Pacific records the top 13.83% CAGR, driven by digital banking and stricter data-protection rules.

What is the main restraint hampering adoption?

High total cost of ownership and tool complexity deter especially small and medium enterprises.

Page last updated on: