Foundation Model Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 31.20 Billion |

| Market Size (2031) | USD 119.29 Billion |

| Growth Rate (2026 - 2031) | 30.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Foundation Model Market Analysis by Mordor Intelligence

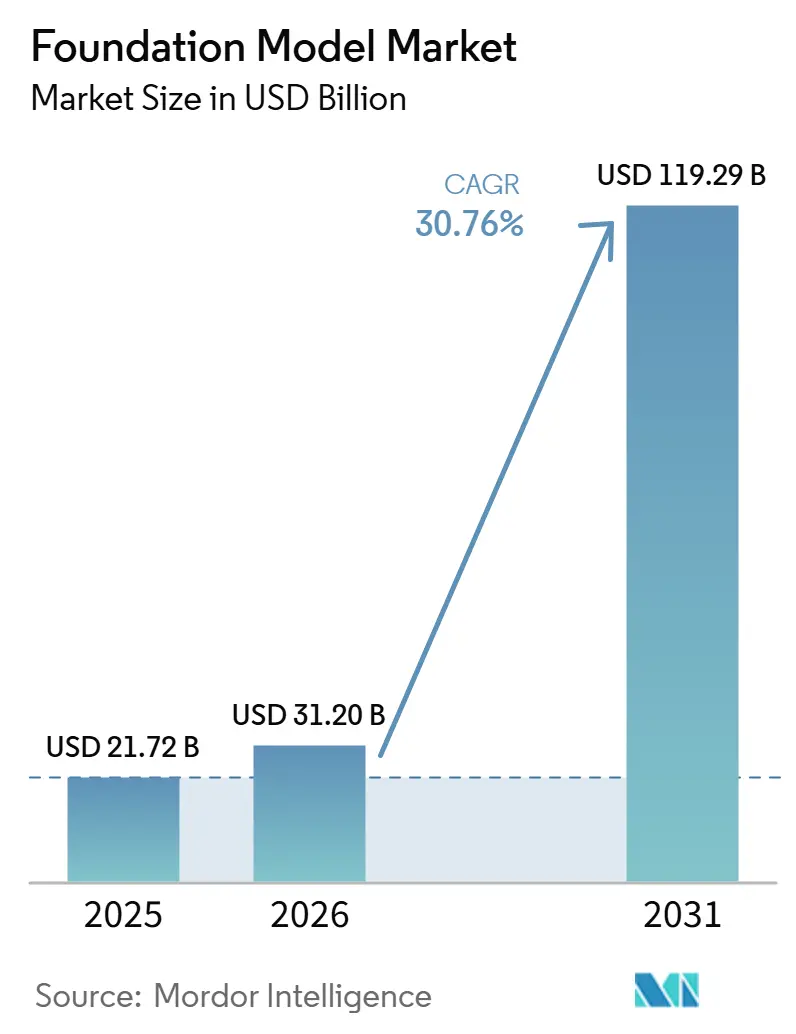

The Foundation Model Market size is projected to expand from USD 21.72 billion in 2025 and USD 31.20 billion in 2026 to USD 119.29 billion by 2031, registering a CAGR of 30.76% from 2026 to 2031. The market is moving beyond early text-generation use cases because enterprises now want models that can support reasoning, automation, and decision support within daily workflows. Demand is also widening as multimodal systems, open-weight ecosystems, and managed deployment platforms make adoption more practical across a broader range of operating environments. Competitive positioning is increasingly shaped by a provider’s ability to combine model performance with access to infrastructure, fine-tuning support, and compliance readiness. At the same time, the market still faces structural pressure from concentrated compute access, high training costs, and stricter reliability expectations in regulated sectors. These conditions continue to create room for vendors that can offer secure deployment options, domain-specific performance, and flexible hosting models across regions.

Key Report Takeaways

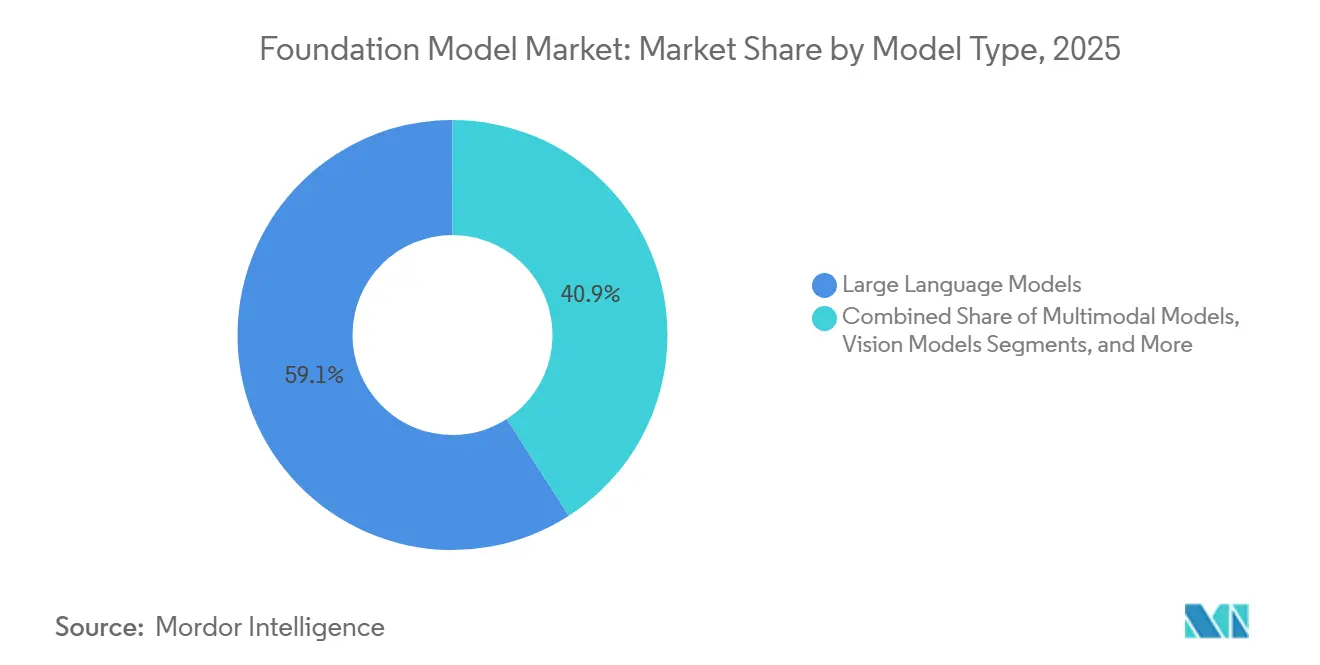

- By model type, large language models led with 59.11% of revenue share in the foundation model market in 2025, while multimodal models are projected to expand at a 31.34% CAGR through 2031.

- By deployment mode, cloud-based deployment held 66.39% of revenue share in the foundation model market in 2025, while on-premises deployment is projected to expand at a 39.90% CAGR through 2031.

- By enterprise size, large enterprises held 68.48% of revenue share in the foundation model market in 2025, while SMEs are expected to expand at a 35.21% CAGR through 2031.

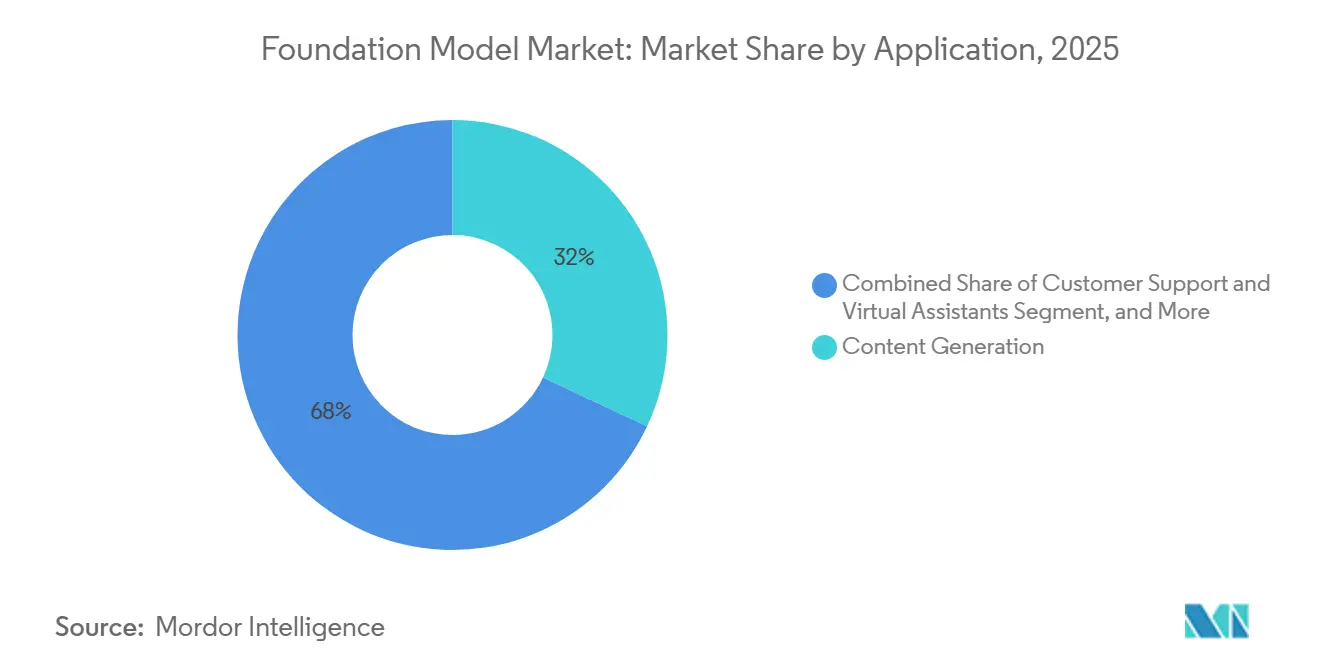

- By application, content generation held 31.98% of revenue share in the foundation model market in 2025, while the business intelligence and analytics segment is projected to expand at a 37.57% CAGR through 2031.

- By end user, IT and telecommunications held 28.56% of revenue share in the foundation model market in 2025, while the government and defense segment is projected to expand at a 39.76% CAGR through 2031.

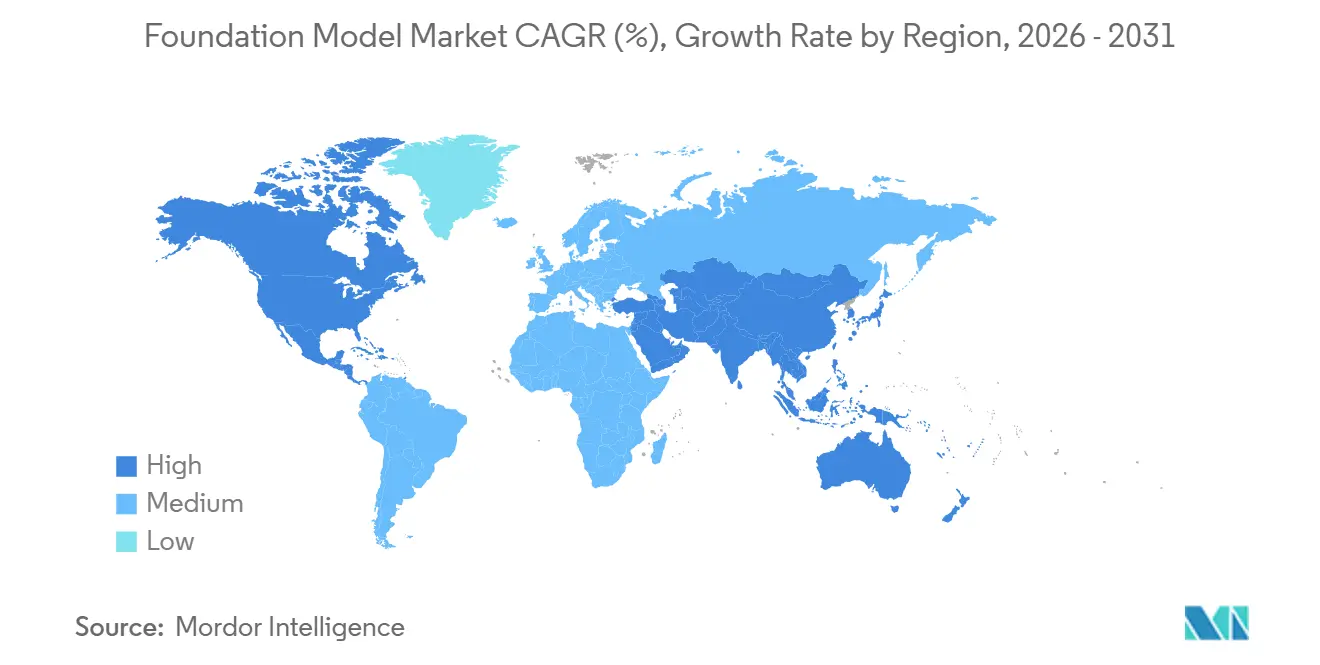

- By geography, North America held 39.37% of revenue share in the foundation model market in 2025, while Asia-Pacific is projected to expand at a 32.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Foundation Model Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise Demand for Multimodal and Reasoning Models | +6.5% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid Shift to Domain-Tuned Foundation Models | +5.8% | Global, with high intensity in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Inference Cost Compression from Open-Weight Ecosystems | +4.9% | Global, particularly impactful in Asia-Pacific, South America, and Africa | Short term (≤ 2 years) |

| AI Agent Deployment Across Core Business Workflows | +4.2% | North America and Europe core, spill-over to Asia-Pacific and Middle East and Africa | Short term (≤ 2 years) |

| Cloud-Native Model Hosting and Managed AI Platforms | +3.6% | Global, highest intensity in North America and Europe | Short term (≤ 2 years) |

| Demand for Model Fine-Tuning, Guardrails, and Governance Layers | +2.8% | North America and Europe, with early gains in Saudi Arabia and Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Demand for Multimodal and Reasoning Models Drives Architecture Upgrades

Enterprises are no longer buying models mainly for draft generation, because they now want systems that can process documents, images, audio, and structured records inside the same workflow. This is changing procurement standards across the foundation model market, where buyers increasingly expect models to support multi-step reasoning and dependable task execution. Multimodal capability matters more in sectors such as healthcare, defense, and media, where input data arrives in multiple formats and cannot be handled effectively by text-only systems. It also strengthens use cases that depend on connecting records, visuals, and instructions before producing an action or recommendation. Apple’s third-generation foundation model family reflects this direction by combining on-device and server-based variants for language and image understanding in hardware-constrained environments.[1]Apple Machine Learning Research, “Introducing the Third Generation of Apple’s Foundation Models,” Apple Machine Learning Research, machinelearning.apple.com As these architectures mature, the foundation model market is shifting toward broader reasoning systems rather than standalone content tools.

Rapid Shift to Domain-Tuned Foundation Models Changes Buying Priorities in High-Stakes Verticals

General-purpose models trained on broad internet data are becoming less effective in workflows that need precision, traceability, and domain context. In finance, research presented through IEEE CSCloud showed that domain-adaptive post-training with modular LoRA on financial datasets enabled compact 7-billion-parameter models to outperform GPT-4 on selected financial benchmarks. In healthcare, EHR foundation models fine-tuned on HL7 FHIR-standardized clinical data have demonstrated progress across 6 major clinical forecasting tasks, underscoring why specialized architectures are gaining ground.[2]University of Toronto Authors, “EHRMamba, Towards Generalizable and Scalable Foundation Models for Electronic Health Records,” Proceedings of Machine Learning Research, proceedings.mlr.press This is pushing enterprises in regulated settings to prefer smaller, more targeted systems over broader models that require greater supervision. It also lowers total operating cost when a fine-tuned model can run inside controlled infrastructure instead of sending every task through a premium frontier API. In the foundation model market, that shift is moving value toward vendors that support fine-tuning, integration, and governance rather than only raw model access.

Inference Cost Compression from Open-Weight Ecosystems Reshapes Deployment Economics

Open-weight ecosystems are changing the economics of the foundation model market by widening access to capable model families. Enterprises now have a larger pool of reusable architectures to evaluate, adapt, and host, which reduces dependence on a narrow set of proprietary API providers. Alibaba reported in April 2025 that the Qwen open-source ecosystem had exceeded 300 model versions, 300 million downloads, and 100,000 derivative fine-tuned models, which shows how quickly open-weight distribution can scale.[3]Alibaba Group, “Tongyi Qwen Open-Source Ecosystem, 300+ Models, 300M+ Downloads,” Alibaba Group, qwenlm.github.io Capital is also following this shift, as Together AI raised USD 800 million in July 2026 to expand open-source AI inference infrastructure.[4]Together AI, “Announcing Our USD 800M Series C to Accelerate the Shift to Open-Source AI,” Together AI, together.ai This broader tool base lets more organizations test, fine-tune, and deploy models without committing to frontier-level infrastructure from the start. That wider affordability is expanding the foundation model market's demand base, especially among smaller enterprises that were outside the first wave of adoption.

AI Agent Deployment Across Core Business Workflows Embeds Models in Revenue-Critical Systems

AI agents are giving the foundation model market a much stronger link to revenue-critical work by enabling them to plan and act across multi-step tasks rather than just generate responses. This changes enterprise buying behavior, since the model becomes part of task execution rather than a separate assistant used for isolated prompts. Agent deployments are especially relevant in customer operations, internal knowledge workflows, and process-heavy back-office environments where coordination matters as much as content generation. The general availability of Claude Sonnet 5 in Microsoft Foundry on NVIDIA GB300 systems in Azure shows how vendors are packaging models with enterprise deployment stacks for agentic use. That packaging matters because production use depends on orchestration, monitoring, and secure access as much as on raw model quality. As a result, the foundation model market is drawing more spending into workflow tools, control layers, and implementation services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High GPU Dependency and Frontier Training Costs | -3.2% | Global, most acute for North America and Asia-Pacific frontier labs | Long term (≥ 4 years) |

| Hallucination Risk in Regulated Workflows | -2.4% | Global, highest compliance burden in North America and Europe | Medium term (2-4 years) |

| Data Sovereignty and Cross-Border Model Hosting Constraints | -1.8% | Europe, Asia-Pacific, Middle East, spill-over to South America | Medium term (2-4 years) |

| Fragmented Compliance Burden Across Model, Data, and Deployment Layers | -1.4% | Europe and North America core, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High GPU Dependency and Frontier Training Costs Compress the Competitive Field

High GPU dependency remains one of the clearest structural restraints on the foundation model market, as frontier model training still requires substantial capital commitments. Current-generation frontier training runs now regularly exceed USD 100 million, and the largest single run in 2024 reached nearly USD 390 million.[5]Epoch AI, “Trends in Artificial Intelligence,” Epoch AI, epoch.ai This keeps true frontier development concentrated among a very small group of hyperscaler-backed organizations with the capital and infrastructure to absorb repeated training cycles. The effect is not limited to training, because access to advanced hardware also shapes inference scale, release timing, and long-term service economics. Export controls on advanced semiconductors add another layer of uneven access across jurisdictions, which affects who can scale at the leading edge. In the foundation model market, that combination narrows the field of firms that can sustain model-performance leadership over time.

Hallucination Risk Slows Adoption in Regulated Workflows Despite Wider Deployment

The risk of hallucination is still slowing the foundation model market in regulated workflows, even as adoption continues to broaden elsewhere. In pharmacovigilance, research published in Nature Scientific Reports found that large language model hallucinations can generate false-positive adverse event signals, diverting safety resources from legitimate investigations. Financial institutions face a related problem: model outputs may appear fluent even when unsupported or outside valid operating conditions. Research on model risk management for generative AI in financial institutions identified hallucination and toxicity as major new risks that require stronger validation and oversight. This does not stop adoption, but it does extend procurement timelines and raises demand for human review, monitoring, and guardrail layers. As a result, the foundation model market is moving faster in lightly regulated use cases than in clinical or financial decision systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Model Type: Multimodal Reasoning Expands Enterprise Expectations

Large language models accounted for 59.11% of the foundation model market share in 2025 by model type, maintaining text-centric deployments as the primary commercial base. Multimodal models are projected to expand at a 31.34% CAGR through 2031, as buyers increasingly seek a single system that can process text, images, audio, and structured data across connected workflows. Vision models remain a focused but important category in the foundation model market, especially in inspection, radiology triage, and visual search environments where image understanding is central. Other model types, including speech, audio, and domain-specific models, are also gaining traction where voice interfaces, latency, or technical vocabularies create a poor fit for broad architectures. The segment mix shows that the foundation model market is moving from single-modality tools toward broader reasoning systems that can operate across more complex enterprise contexts.

The boundary between large language models and multimodal models is already becoming less clear, as many leading releases now support documents, images, and code within the same workflow. Apple’s third-generation foundation model family reflects this trend with on-device and server-based variants that combine language and image understanding for hardware-constrained environments. The foundation model industry is therefore likely to reward vendors that can combine model breadth with more efficient inference and simpler deployment.

By Deployment Mode: Local Control Rises Alongside Cloud Scale

Cloud-based deployment accounted for 66.39% of the foundation model market in 2025, as managed services from AWS, Azure, and Google Cloud reduce the operational burden of model hosting. On-premise deployment is projected to expand at a 39.90% CAGR through 2031, reflecting stronger demand for security, control, and locally managed infrastructure in sensitive environments. This pattern shows that the foundation model market is not simply favoring one mode over another, because buyer priorities now differ by data sensitivity, workload type, and internal governance needs. The open-weight ecosystem supports that shift by giving enterprises more freedom to deploy models without tight vendor lock-in or fixed cloud-only operating models. In practice, cloud remains the default for many organizations, but local deployment has become a strategic requirement for an increasing share of high-value use cases.

Cloud and on-premise setups are also not replacing each other in a clean line, because many large organizations now use hybrid architectures that split workloads by risk and data class. Sensitive inference often runs on internal infrastructure, while non-sensitive, high-volume tasks continue to run through external APIs. Apple’s third-generation foundation model family, spanning on-device and server-based variants, shows that hybrid deployment is becoming a practical design choice rather than an edge case. This means reported cloud leadership can understate the importance of internal deployment capability in the foundation model market. Government and defense adoption reinforces that point, because secure, air-gapped environments often require hardware-resident models and tailored support for them.

By Enterprise Size: SME Adoption Improves as Access Barriers Fall

Large enterprises held 68.48% of the foundation model market share in 2025 by enterprise size, because they had the budgets, data resources, and technical teams needed for integration and governance. SMEs are projected to expand at a 35.21% CAGR through 2031 as managed platforms and open-weight options reduce several of the barriers that initially limited adoption. The shift is not only about lower model pricing, because smaller organizations also benefit when deployment tools become easier to manage and require less in-house engineering. In the foundation model market, usable infrastructure is becoming almost as important as model quality for expanding the addressable customer base. The segment is therefore moving from a first wave dominated by large enterprises toward a broader adoption profile with more mid-sized operational buyers.

Together AI closed a USD 800 million Series C in July 2026 to expand its open-source AI inference infrastructure, signaling confidence that accessible deployment platforms will continue to widen the customer base. Even so, cost is not the only barrier for SMEs, because data governance, evaluation discipline, and internal approval processes still slow the move from pilot work to production use. That gap between experimentation and scaled deployment creates steady demand in the foundation model market for integration support, packaged tooling, and vertical solutions that reduce setup friction. Vendors that simplify onboarding, monitoring, and model updates are likely to benefit more than those that compete only on benchmark performance. The foundation model industry is therefore expanding not just through better models, but through easier access to dependable operational workflows.

By Application: Analytics Use Cases Gain Ground Against Content-Led Adoption

Content generation accounted for 31.98% of the foundation model market in 2025, making it the first major commercial entry point for enterprise deployments. Business intelligence and analytics are projected to expand at a 37.57% CAGR through 2031 as organizations use models to interpret structured and unstructured internal data with more context. Customer support, virtual assistants, and knowledge management remain established areas in the foundation model market because they fit well with retrieval, summarization, and contextual response generation. The application mix now shows a gradual move away from simple drafting use cases toward workflows that connect model output to measurable business actions. This matters because applications with clear operational outcomes tend to support more durable spending and deeper internal integration.

Research in Nature Medicine showed that a generalist medical language model could support disease diagnosis, reflecting how vertical fine-tuning is broadening the role of advanced applications in professional settings. Cybersecurity and fraud detection are gaining strategic weight in the foundation model market because models trained on domain data can recognize patterns that rule-based tools may miss. Drug discovery and software development are also scaling as secondary use cases, especially where models shorten discovery cycles or speed repetitive coding tasks. That broadening use base means the foundation model market is increasingly defined by workflow depth, data integration, and task completion quality rather than by content automation alone. The segment is still anchored in early communication use cases, but future expansion is increasingly driven by decision support and process execution.

By End User: Sovereign and Regulated Demand Changes Deployment Priorities

IT and telecommunications captured 28.56% of the foundation model market share in 2025, reflecting their role as both early adopters and delivery layers for adjacent sectors. Government and defense are projected to expand at a 39.76% CAGR through 2031, supported by sovereign AI programs, secure inference requirements, and a stronger preference for controlled deployment environments. Healthcare is also advancing in the foundation model market as domain-tuned models build stronger evidence for clinical support, workflow coordination, and data interpretation use cases. These end-user patterns are gradually shifting product demand toward secure deployment, monitoring, traceability, and domain control rather than only generic API consumption. Vendors that can support sensitive environments are therefore gaining relevance beyond the traditional cloud-first model delivery approach.

Financial services remain a high-value segment, but hallucination risk and model validation requirements continue to extend procurement timelines and raise oversight needs. Manufacturing, retail, and e-commerce represent large addressable groups in the foundation model market, where process optimization, quality control, and forecasting use cases are becoming more practical as fine-tuning gets easier. China National Petroleum had scaled its Kunlun foundation model to 152 application scenarios across the oil and gas value chain by May 2026, which shows how sector-specific deployment can move from pilots to broad operational coverage. That breadth of use suggests the foundation model market is expanding through domain execution as much as through general model availability. The foundation model industry is therefore increasingly shaped by end-user operating needs rather than a single cross-sector adoption pattern.

Geography Analysis

North America accounted for 39.37% of the foundation model market in 2025, making it the largest regional revenue pool. The region benefits from the co-location of frontier AI labs, hyperscaler headquarters, and a deep enterprise software base that helps commercialize new models quickly. The United States remains the main anchor of this position because it combines model development leadership with strong cloud distribution and enterprise procurement activity. Canada adds depth through research strength linked to the Toronto and Montreal AI ecosystems, which continue to support talent supply and academic influence. In the foundation model market, South America remains earlier in adoption and more dependent on cloud APIs from U.S. and European providers than on local frontier model development.

Europe presents the most compliance-heavy operating environment in the foundation model market, because documentation, transparency, and testing obligations shape how providers launch and maintain models. That does not stop demand, as financial services and industrial manufacturing remain important buying centers across Germany, the United Kingdom, France, Italy, and Spain. The result is a two-track regional pattern in which deployment moves ahead, while governance spending also rises to meet new operating rules. The Middle East is also gaining relevance, as sovereign AI infrastructure plans and local hosting ambitions create a clearer role for regional deployment hubs.

Asia-Pacific is projected to expand at a 32.89% CAGR through 2031, making it the fastest-growing regional block in the foundation model market. China’s open-weight ecosystem is scaling quickly, and Alibaba reported that the Qwen series had exceeded 300 model versions, 300 million downloads, and 100,000 derivative fine-tuned models by April 2025. China National Petroleum’s Kunlun foundation model had reached 152 deployment scenarios by May 2026, which shows how the foundation model market in Asia-Pacific is linking model development with large industrial use cases. South Korea’s Framework Act on Artificial Intelligence Development took effect in January 2026 and added a formal compliance layer for foreign AI companies operating in the country. India and Japan are also scaling quickly, while Africa, led by South Africa, remains at an earlier stage where multilingual design and mobile-first delivery are important for broader deployment.

Competitive Landscape

The foundation model market remains moderately concentrated at the frontier tier, where a small group of hyperscaler-backed labs still sets the pace in model performance. At the same time, the broader revenue base is more fragmented across cloud services, inference platforms, fine-tuning vendors, and application specialists. This split means leadership in raw model capability does not automatically translate into control over enterprise deployment or downstream monetization. In the foundation model market, providers compete through managed APIs, open-weighted releases, and direct implementation support within customer organizations. The common pattern is that recurring revenue increasingly depends on who can reduce deployment complexity, rather than on who can publish the biggest model alone.

Together AI’s USD 800 million Series C in July 2026 showed how investors are backing open-source inference infrastructure as a competitive layer in its own right. EXL Service Holdings announced a definitive agreement to acquire iMerit for up to USD 310 million in June 2026, which strengthened its position in model training, evaluation, and reinforcement learning services. Apple’s July 2026 release of the third-generation Apple Foundation Models showed another route to advantage, as it tied model capabilities more closely to endpoint hardware and on-device experiences. These moves suggest the foundation model market is rewarding firms that connect models to infrastructure, services, and installed platforms rather than treating model access as a standalone product.

Open frameworks also remain a strong competitive tool, because they help vendors build developer ecosystems faster than closed API models can. NVIDIA and Hugging Face integrated Isaac GR00T 1.7 and Cosmos 3 into the LeRobot platform in July 2026, which linked model tooling more closely to GPU-optimized robotics workflows. Domain-specific compliance tooling is still less mature than model availability, which leaves space for vendors focused on guardrails, monitoring, and documentation. In the foundation model market, that gap matters most in regulated sectors where deployment approvals take longer, and support burdens are heavier. Competitive outcomes, therefore, depend not only on benchmark strength but also on whether vendors can deliver secure, maintainable, and auditable systems at scale.

Foundation Model Industry Leaders

OpenAI LLC

Microsoft Corporation

Google LLC

Amazon Web Services, Inc.

Anthropic PBC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Tencent officially launched the full version of Hunyuan Hy3, a 295-billion-parameter Mixture-of-Experts foundation model released under the Apache 2.0 license, with a 90% task-completion rate reported across internal agent applications. The model was immediately integrated into the Yuanbao consumer AI assistant, reducing developer usage fees and marking a significant open-source competitive move targeting global developer ecosystems.

- June 2026: Anthropic's Claude Sonnet 5 became generally available in Microsoft Foundry on NVIDIA GB300 Blackwell Ultra infrastructure via Azure, clearing a key enterprise procurement barrier by enabling production-grade agentic AI deployments inside Microsoft 365 environments on the latest accelerator architecture.

- June 2026: OpenAI previewed the GPT-5.6 model suite, comprising Sol, Terra, and Luna variants, with Sol priced at USD 5 per million input tokens and USD 30 per million output tokens, representing improved cost efficiency relative to prior-generation frontier models. Initial access was restricted to government-approved partners pending cybersecurity review.

Global Foundation Model Market Report Scope

The Foundation Model Market comprises the development, deployment, licensing, and commercialization of large-scale pre-trained AI models, including large language, multimodal, vision, speech, audio, and domain-specific foundation models, that serve as the underlying intelligence for a wide range of enterprise AI applications. The market's revenue is generated through model licensing and subscriptions, API and inference usage fees, cloud-hosted and on-premise deployments, model customization and fine-tuning services, enterprise support, and managed AI services provided to organizations across industries such as BFSI, healthcare, IT and telecommunications, manufacturing, government, and other end-user sectors.

The Foundation Model Market Report is Segmented by Model Type (Large Language Models, Multimodal Models, Vision Models, and Other Model Types (Speech and Audio Models, Domain-Specific Models, etc.)), Deployment Mode (Cloud-Based and On-Premise), Enterprise Size (Large Enterprises and Small and Medium Enterprises), Application (Content Generation, Customer Support and Virtual Assistants, Knowledge Management, Cybersecurity and Fraud Detection, Business Intelligence and Analytics, and Other Applications (Software Development, Drug Discovery, etc.)), End User (BFSI, Healthcare, IT and Telecommunications, Manufacturing, Government and Defense, and Other End Users (Retail and E-Commerce, Media and Entertainment, Education, etc.)), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Large Language Models |

| Multimodal Models |

| Vision Models |

| Other Model Types (Speech and Audio Models, Domain-Specific Models, etc.) |

| Cloud-Based |

| On-Premise |

| Large Enterprises |

| Small and Medium Enterprises |

| Content Generation |

| Customer Support and Virtual Assistants |

| Knowledge Management |

| Cybersecurity and Fraud Detection |

| Business Intelligence and Analytics |

| Other Applications (Software Development, Drug Discovery, etc.) |

| BFSI |

| Healthcare |

| IT and Telecommunications |

| Manufacturing |

| Government and Defense |

| Other End Users (Retail and E-Commerce, Media and Entertainment, Education, etc.) |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of the Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Model Type | Large Language Models | |

| Multimodal Models | ||

| Vision Models | ||

| Other Model Types (Speech and Audio Models, Domain-Specific Models, etc.) | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application | Content Generation | |

| Customer Support and Virtual Assistants | ||

| Knowledge Management | ||

| Cybersecurity and Fraud Detection | ||

| Business Intelligence and Analytics | ||

| Other Applications (Software Development, Drug Discovery, etc.) | ||

| By End User | BFSI | |

| Healthcare | ||

| IT and Telecommunications | ||

| Manufacturing | ||

| Government and Defense | ||

| Other End Users (Retail and E-Commerce, Media and Entertainment, Education, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the foundation model space?

The foundation model market was valued at USD 21.72 billion in 2025, stands at USD 31.2 billion in 2026, and is forecast to reach USD 119.29 billion by 2031 at a 30.76% CAGR.

Which region leads revenue generation for foundation models?

North America led with a 39.37% share in 2025, supported by its concentration of frontier labs, hyperscalers, and enterprise software buyers.

Which region is expanding the fastest through 2031?

Asia-Pacific is the fastest-growing region with a projected 32.89% CAGR, helped by strong domestic model development and large industrial deployment bases.

Which model type is growing the fastest?

Multimodal models are projected to record the highest CAGR at 31.34%, as enterprises increasingly want systems that can reason across text, images, audio, and structured data.

Why is on-premise deployment gaining traction?

On-premise deployment is projected to grow at 39.90% CAGR because regulated sectors and sovereign use cases need tighter control over data, hosting, and model governance.

Which end-user group is creating the strongest growth momentum?

Government and defense is projected to expand at a 39.76% CAGR, driven by sovereign AI programs and demand for secure inference in controlled environments.

Page last updated on: