Security Assessment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

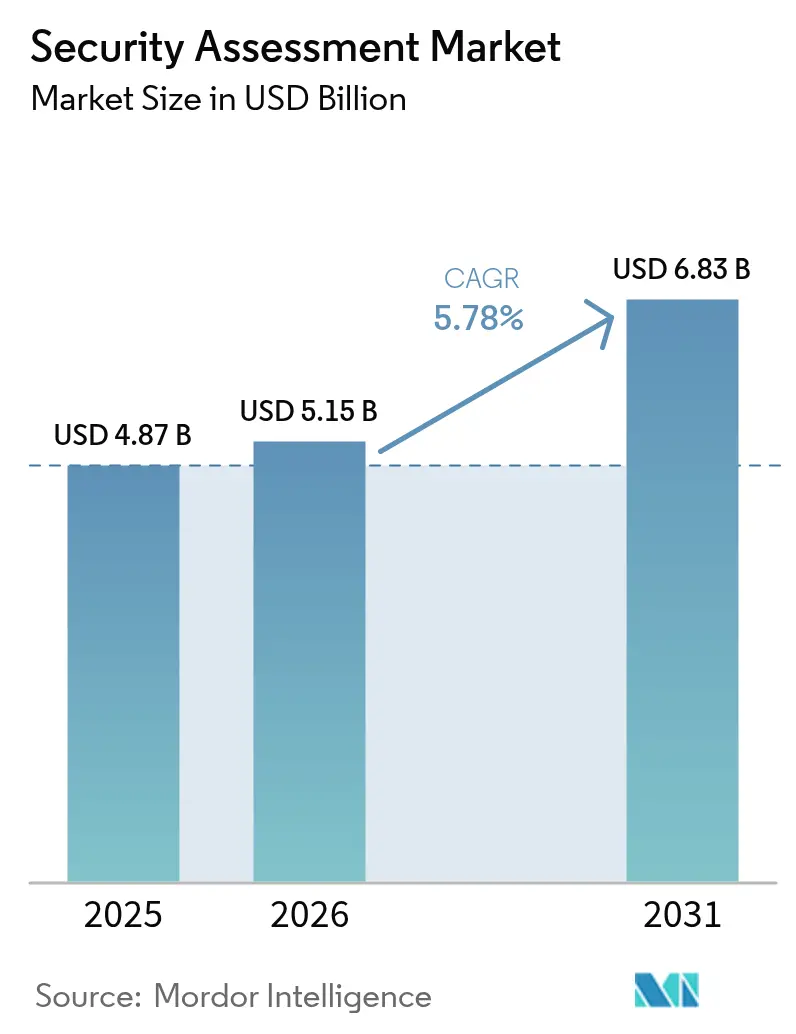

| Market Size (2026) | USD 5.15 Billion |

| Market Size (2031) | USD 6.83 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Security Assessment Market Analysis by Mordor Intelligence

The security assessment market size is expected to grow from USD 4.87 billion in 2025 to USD 5.15 billion in 2026 and is forecast to reach USD 6.83 billion by 2031 at 5.78% CAGR over 2026-2031. Wider adoption stems from enterprises validating cyber-posture against ever-richer attack techniques and expanding regulatory rules. Automated, AI-enabled testing trims assessment cycle times and raises detection accuracy, prompting firms to shift from annual audits to continuous validation. Demand also benefits from cloud migration, DevSecOps integration, and a need to secure hybrid work architectures that blur traditional perimeter controls.

Key Report Takeaways

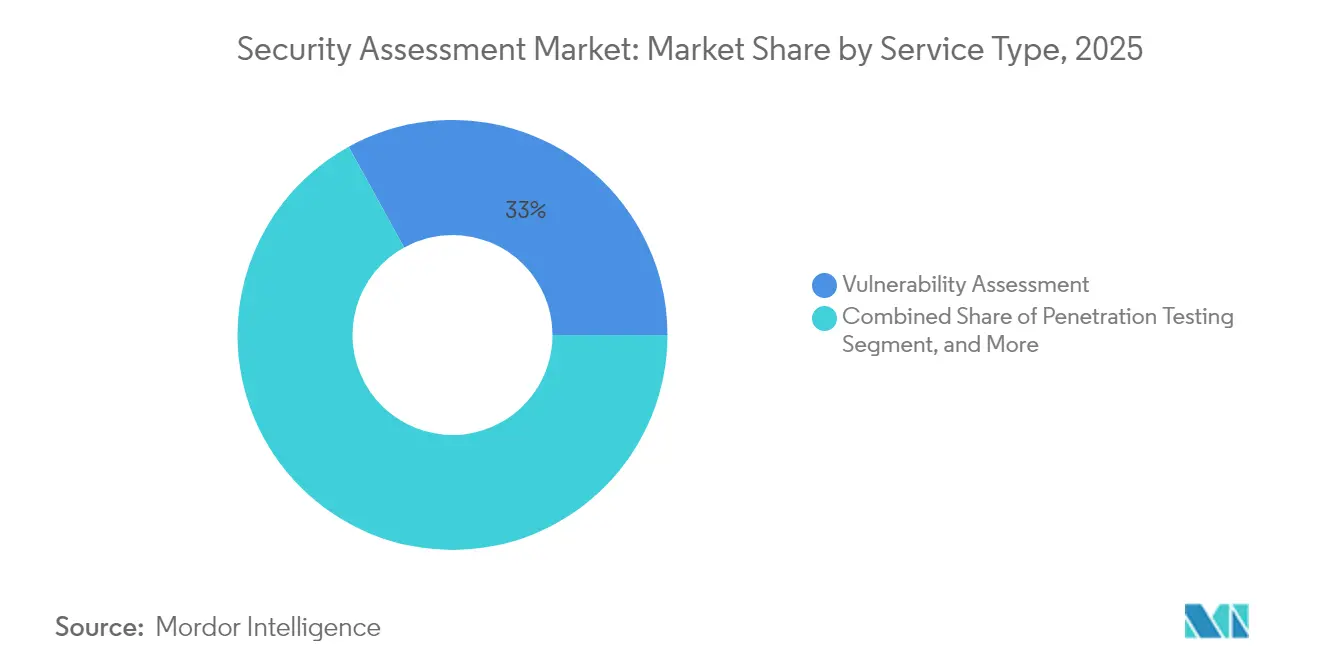

- By service type, vulnerability assessment captured 33.02% of the security assessment market share in 2025; PTaaS is forecast to expand at a 7.18% CAGR through 2031.

- By deployment model, on-premise retained 51.65% share of the security assessment market size in 2025, whereas cloud-based solutions will post an 7.97% CAGR to 2031.

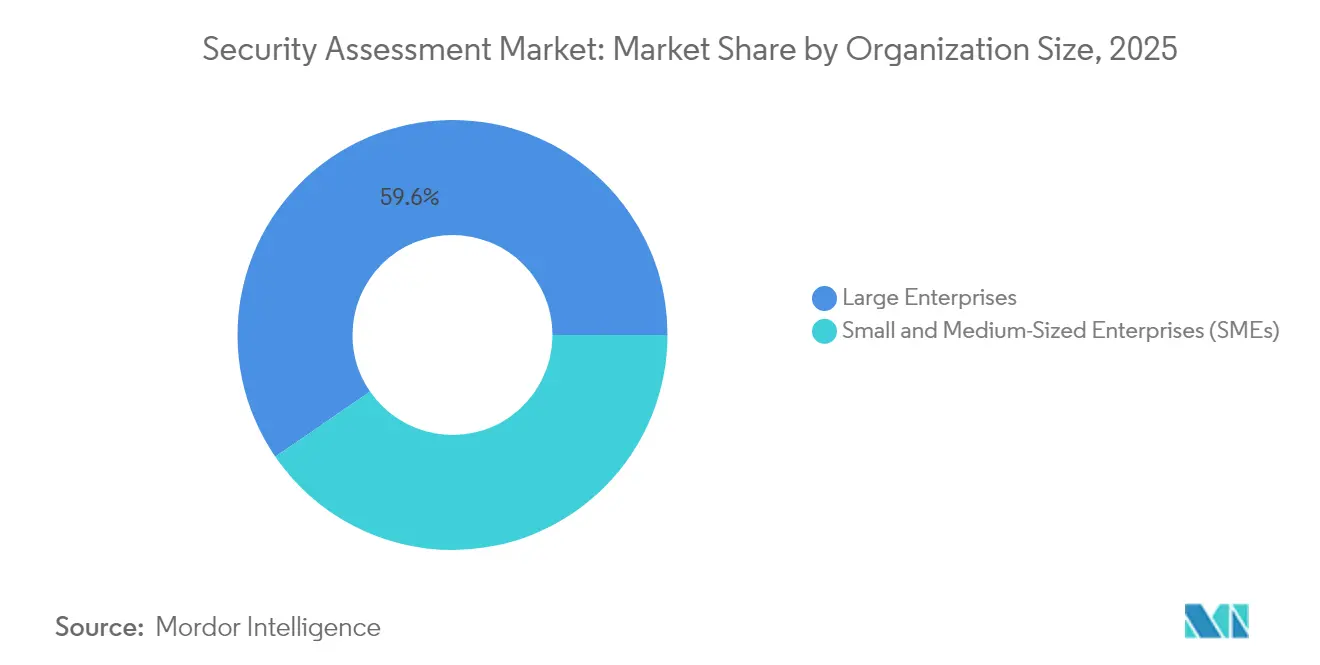

- By organization size, large enterprises commanded 59.58% revenue in 2025; SMEs register the highest expected CAGR at 6.63% for 2026-2031.

- By end-user industry, BFSI led with 27.85% revenue in 2025, while Healthcare and Life Sciences will record the fastest 5.92% CAGR through 2031.

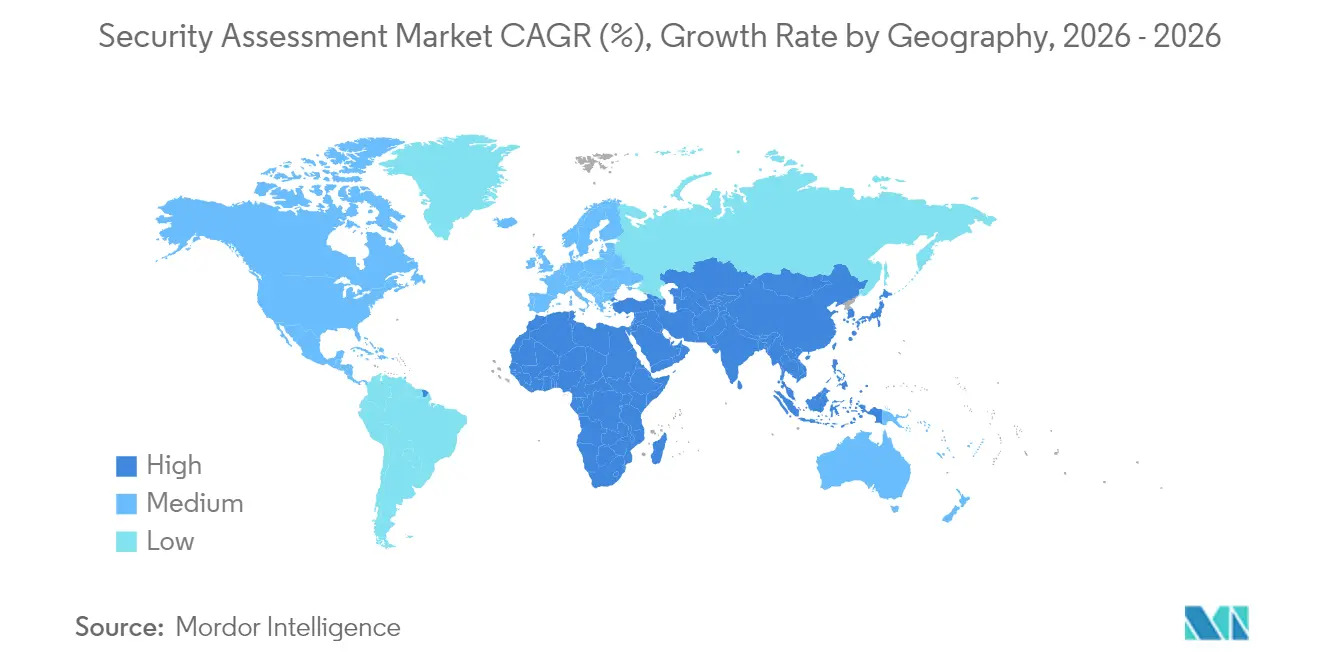

- By geography, North America contributed 40.88% revenue in 2025; Asia-Pacific is the fastest-expanding region with an 8.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Security Assessment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing volume and sophistication of phishing/malware attacks | +1.2% | Global | Short term (≤ 2 years) |

| Regulatory compliance mandates expanding to mid-market | +0.8% | North America & EU | Medium term (2-4 years) |

| Surging cloud migration creating demand for continuous validation | +0.6% | Global | Medium term (2-4 years) |

| AI-enabled automated testing platforms lowering cost and cycle time | +0.4% | North America & APAC | Long term (≥ 4 years) |

| Pen-Testing-as-a-Service uptake among SaaS vendors | +0.3% | Global | Medium term (2-4 years) |

| Convergence of DevSecOps with shift-left testing | +0.2% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Volume and Sophistication of Phishing/Malware Attacks

Ransomware strikes on healthcare providers jumped 137% within 18 months, compelling firms to rethink assessment methods beyond annual checklists. Attackers now pivot tactics within days of patch releases, so enterprises are deploying continuous breach simulation that mirrors adversary behavior instead of static scans. Asia-Pacific records the highest median dwell times globally, exposing response gaps that specialized assessment services must close. Providers delivering AI-backed threat emulation and red-team exercises see rising engagement as clients demand realistic validation over routine vulnerability sweeps.

Regulatory Compliance Mandates Expanding to Mid-Market

The Digital Operational Resilience Act, live since January 2025, obliges more than 22,000 EU financial firms to run regular resilience testing, extending obligations from major banks to mid-tier entities.[1]Digital Operational Resilience Act Editorial Team, “EU Banks Must Enhance Cyber Resilience as DORA Takes Effect,” Banking Exchange, bankingexchange.com In the United States, regulators signal baseline resilience requirements that incorporate third-party risk programs, pushing fresh demand for assessment among regional banks. Proposed HIPAA security updates further require multi-factor authentication and yearly audits, projecting USD 9 billion first-year compliance costs.[2]Federal Register Staff, “HIPAA Security Rule To Strengthen the Cybersecurity of Electronic Protected Health Information,” Federal Register, federalregister.gov These broadening mandates stabilize service demand by transforming compliance from episodic to ongoing.

Surging Cloud Migration Creating Demand for Continuous Validation

FedRAMP 20x streamlines U.S. federal cloud authorizations with infrastructure-as-code and nonstop monitoring, illustrating an industry move from point-in-time tests to ever-running assessment. The Cloud Security Alliance flags identity weaknesses as top cloud threats, pulling attention toward configuration assessment across AWS, Azure, and Google Cloud. Providers that embed assessments into DevOps pipelines thus gain competitive ground.

AI-Enabled Automated Testing Platforms Lowering Cost and Cycle Time

The National Security Agency’s autonomous penetration testing prototypes highlight how AI trims weeks-long engagements to hours.[3]Beryllium Security Research Unit, “AI-Powered Penetration Testing: Nebula in Focus and How It Stacks Up Against the Rest,” berylliumsec.com Solutions such as Nebula automatically map vulnerabilities and generate exploits, democratizing advanced testing for organizations lacking deep internal resources. The Cloud Security Alliance emphasizes that AI augments human experts, freeing them for strategic analysis while automation handles repetitive discovery tasks.[4]loud Security Alliance Press Office, “Cloud Security Alliance Issues Top Threats to Cloud Computing Deep Dive 2025,” cloudsecurityalliance.org Vendors pairing AI with expert validation address concerns over false positives and ethics.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget constraints in SMB segment | –0.4% | Global; APAC & MEA | Short term (≤ 2 years) |

| Shortage of skilled red-team/pentest talent | –0.3% | Global | Medium term (2-4 years) |

| Tool sprawl creating assessment fatigue | –0.2% | North America & EU | Short term (≤ 2 years) |

| Accuracy concerns over Gen-AI assessment engines | –0.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Budget Constraints in SMB Segment

Small firms devote near 4% of revenue to security yet face disproportionate breach rates, with 56% of Asia-Pacific SMEs reporting incidents and 75% suffering customer data loss. Full-spectrum testing often exceeds available budgets, pushing many toward basic scanners and leaving gaps in threat coverage. Affordability concerns therefore cap near-term expansion, but they also spur innovation in automated, subscription-priced platforms that lower delivery costs.

Shortage of Skilled Red-Team/Pentest Talent

Asia-Pacific alone requires 2.1 million additional cybersecurity professionals, and 64% of firms plan budget increases to attract talent. Scarcity inflates wages, elevates service pricing, and creates scheduling delays for advanced assessments. Providers respond by centralizing scarce expertise into managed services and augmenting analysts with AI to extend capacity, yet near-term supply shortfalls still temper growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Continuous Validation Recasts Priorities

Vulnerability assessment held 33.02% of 2025 revenue, underscoring its foundational role in compliance programs. PTaaS, however, will scale fastest at 7.18% CAGR, mirroring a market pivot to ongoing validation aligned with DevOps. Many enterprises transition from yearly pentests to monthly or sprint-driven exercises. Risk and compliance audits sustain steady uptake thanks to DORA and HIPAA revisions.

Demand for cloud configuration assessment is rising as multi-cloud estates proliferate. Vendors embedding APIs into CI/CD pipelines create durable advantage, replacing lengthy consulting cycles with real-time dashboards. Mainstream adoption of AI-assisted exploit generation further shifts buyer expectations toward speed over labor hours. Providers offering hybrid models-automated discovery plus analyst validation-balance efficiency and accuracy, appealing to risk-averse sectors like BFSI and healthcare.

By Deployment Model: Cloud Momentum Builds

On-premise testing environments, mandatory for certain financial and government clients, delivered 51.65% revenue in 2025. Nonetheless, cloud-delivered assessment platforms will post an 7.97% CAGR to 2031. Elastic scale, remote collaboration, and integration with cloud-native workloads drive uptake. The FedRAMP 20x roadmap shows public-sector appetite for continuous cloud monitoring, and private enterprises follow suit. Multi-tenant SaaS assessment reduces infrastructure overhead for clients and accelerates updates.

Providers differentiating through multi-cloud visibility and API openness secure longer-term contracts. Conversely, purely on-premise tools risk obsolescence as hybrid workforces and edge deployments expand. Where data-sovereignty regulations persist, vendors increasingly position sovereign SaaS regions rather than hard-air-gapped appliances to retain regulated customers.

By Organization Size: SMEs Close the Gap

Large enterprises contributed 59.58% revenue in 2025, reflecting complex estates requiring layered assessments. They commission red-team simulations, social-engineering tests, and regulatory audits in parallel, creating high average deal sizes. Yet SMEs are poised for 6.63% CAGR as cloud platforms flatten entry barriers. Automated SaaS assessment bundled with managed remediation guidance fits smaller IT teams. Vendors offering modular subscriptions rather than six-figure projects penetrate this segment.

Awareness is climbing as insurers tighten cyber-policy conditions, often mandating annual scans even for modest firms. Government grant programs in several countries subsidize SME security upgrades, indirectly bolstering demand for assessment services. These conditions gradually chip away at enterprise dominance, broadening the security assessment industry client base.

By End-User Industry: Healthcare Accelerates

BFSI led with 27.85% revenue in 2025 owing to stringent reporting rules and high monetary stakes. DORA enforces continuous resilience testing, while US regulators eye similar baselines, ensuring steady spend. Telecommunications and IT services remain heavy users to protect backbone infrastructure. Healthcare and Life Sciences will rise fastest at 5.92% CAGR through 2031, propelled by HIPAA rule changes that impose multi-factor authentication and annual audits. Rising ransomware on hospitals magnifies urgency.

Retail, energy, and utilities also enlarge budgets as payment compliance and critical-infrastructure mandates evolve. Industrial control system testing emerges as a niche requiring domain-specific expertise, creating room for specialists. Collectively these verticals keep the security assessment market on a growth trajectory through the decade.

Geography Analysis

North America produced 40.88% of 2025 revenue owing to deep budgets and far-reaching regulations. FedRAMP 20x and potential federal resilience baselines spur federal and banking sectors to adopt continuous monitoring. Canada aligns breach-notification rules with its USMCA partners, while Mexico’s 2024 data-protection statute elevates demand for standardized assessment across supply chains.

Asia-Pacific is the growth engine with an 8.27% CAGR through 2031. Rapid cloud adoption, e-commerce expansion, and heightened geopolitical tensions lift spending. Australia’s five-year cybersecurity accord with Microsoft and Japan’s defense-oriented cyber build-out illustrate capital infusion. The region’s 2.1 million talent gap and prolonged dwell times create appetite for managed and automated services that offset staffing deficits. SMEs particularly favor subscription-delivered testing platforms to close exposure gaps without heavy capex.

Europe remains sizable through sweeping legislation. DORA reaches thousands of financial entities, while NIS2 widens compulsory security controls across utilities and digital providers. The region’s strict data-sovereignty stance directs demand toward localized cloud nodes and encrypted data storage within assessments. United Kingdom operational-resilience rules converge with EU statutes, simplifying pan-European compliance roadmaps for multinational banks.

Latin America, Middle East, and Africa show nascent yet accelerating uptake as cyber incidents escalate and governments draft national strategies. Gulf Cooperation Council states invest in sovereign cloud zones, driving local assessment demand. South American power utilities prioritize critical-infrastructure audits following headline ransomware incidents. Budget limitations still temper immediate revenue, but vendor partnerships with regional integrators lay groundwork for mid-term expansion.

Competitive Landscape

Market dynamics reflect fragmentated with consulting giants, security specialists, and AI start-ups vying for wallet share. IBM, Accenture, and Deloitte leverage broad client footprints and vertical expertise. CrowdStrike, Rapid7, and Qualys focus on cloud-based platforms offering integrated vulnerability, compliance, and threat-hunting modules. Consolidation accelerates: Cisco’s USD 28 billion Splunk buy and CyberArk’s USD 1.54 billion Venafi deal underline a platform race. Investment intensity is high-Accenture spent USD 6.6 billion on acquisitions and USD 1.2 billion on R&D in FY 2024.

Differentiation hinges on AI-driven automation, multi-cloud visibility, and DevSecOps workflow integration. Application Security Posture Management tools address alert fatigue by correlating findings and prioritizing fixes, an angle that appeals to over-tooled enterprises. PTaaS players disrupt traditional consulting by offering on-demand pentests via web portals with flat pricing. White-space exists in quantum-safe cryptography assessments, industrial control testing, and AI model security audits-areas with rising regulatory scrutiny yet scant service depth.

Strategic moves continue: Zscaler bought Red Canary in May 2025 to bolster AI-powered security operations. Palo Alto Networks’ plan to buy Protect AI and launch Cortex XSIAM 3.0 highlights email-security enhancement via AI CRN. Sophos closed an USD 859 million Secureworks purchase to build managed detection capacity. Arctic Wolf’s Cylance acquisition enriches endpoint coverage, and Mastercard’s Recorded Future deal shows non-security firms acquiring threat intelligence for core operations.

Overall, leading five vendors account for roughly 28% of global revenue, indicating a moderately fragmented environment that encourages continuous innovation and acquisition.

Security Assessment Industry Leaders

IBM Corporation

Qualys Inc

Trustwave Holdings, Inc (Singapore Telecommunications Limited)

AO Kaspersky Lab

Trellix

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Zscaler acquired Red Canary to advance AI-powered security operations capabilities, underscoring platform consolidation in managed security.

- April 2025: Palo Alto Networks unveiled plans to buy Protect AI and introduced Cortex XSIAM 3.0 with AI-driven email security at RSAC 2025.

- March 2025: Sophos finalized its USD 859 million Secureworks acquisition, expanding managed detection and response offerings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the global security assessment market as fees paid for structured evaluations that probe an organization's cyber-defense posture, including vulnerability assessments, penetration testing, red/purple-team simulations, configuration reviews, and compliance audits performed across on-premise and cloud environments. The valuation covers fresh contracts, retainer renewals, and platform-driven assessment subscriptions delivered by commercial providers to all industry verticals in 2019-2030.

Scope exclusion: hardware sales for scanners, firewalls, or broader managed security operations are not counted.

Segmentation Overview

- By Service Type

- Vulnerability Assessment

- Penetration Testing

- Risk and Compliance Audit

- Red-/Purple-Team Simulation

- Cloud Configuration Assessment

- By Deployment Model

- On-Premise

- Cloud

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises (SMEs)

- By End-user Industry

- BFSI

- IT and Telecom

- Healthcare and Life Sciences

- Retail and eCommerce

- Energy and Utilities

- Government and Defense

- Others (Education, Media, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- South East Asia

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed security consultants, CISOs at banks, cloud architects in Asia-Pacific, and assessment platform product leads in North America and Europe. Discussions clarified prevailing pricing bands, average assessment frequency, and regional regulation triggers, helping us validate desk findings and refine growth assumptions.

Desk Research

We sifted through publicly available datasets such as ENISA threat landscape bulletins, US-CERT incident statistics, NIST vulnerability repositories, and regional privacy-fine trackers, which anchor attack frequency, breach cost, and regulatory cadence. Complementary inputs came from company 10-Ks, investor decks, and trade association whitepapers that quantify enterprise security budgets. For deeper company intelligence, we tapped D&B Hoovers and news flows inside Dow Jones Factiva. These sources illustrate adoption rates by sector and typical contract values; yet they are illustrative only and not exhaustive of every secondary reference consulted.

Market-Sizing & Forecasting

A top-down model converts worldwide IT services spend into a security-testing addressable pool, using penetration-rate curves that vary by region, firm size, and vertical. Supplier roll-ups and sample average-selling-price × project counts act as bottom-up cross-checks, with gaps bridged through weighted averaging. Key drivers in the model include: (1) number of reported CVEs, (2) cloud migration share of enterprise workloads, (3) average cost per breach, (4) frequency of mandated third-party audits, and (5) hiring shortfalls in cyber talent. Multivariate regression links these indicators to historical revenue; then ARIMA smoothing projects forward while scenario analysis stresses optimistic and downside demand.

Data Validation & Update Cycle

Outputs pass anomaly checks against independent spend trackers, and variances above five percent trigger analyst review. Findings go through two internal peer reviews before sign-off. We refresh every twelve months, with interim adjustments when material regulations or flagship breaches occur, ensuring clients always receive an up-to-date baseline.

Why Our Security Assessment Baseline Commands Reliability

Published figures diverge because firms choose different service bundles, currency bases, and update cadences. We openly frame scope around assessment revenues only, previewing drivers and exclusions so users can reconcile numbers quickly.

Key gap drivers stem from rivals bundling broader advisory, vulnerability management platforms, or incident response retainers, applying aggressive roll-ups, or carrying forward pre-pandemic baselines with limited refresh. Currency conversion methods and ASP inflation curves further widen spreads.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.87 B (2025) | Mordor Intelligence | - |

| USD 4.54 B (2024) | Global Consultancy A | Uses fixed US-only contract data and projects globally without regional mix adjustment |

| USD 20.41 B (2025) | Global Consultancy B | Bundles broader security advisory services and managed remediation fees, inflating base |

The comparison shows how differing scope and refresh logic explain most variance. By centering on clearly defined assessment activities, using current-year indicators, and balancing top-down with selective bottom-up checks, Mordor delivers a transparent, repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

How is AI changing security assessment delivery?

AI-driven platforms cut testing time from weeks to hours, automate exploit generation, and enable continuous monitoring, while human experts remain essential for contextual validation.

What impact will DORA have on service demand in Europe?

The act mandates ongoing resilience testing for over 22,000 financial entities, creating long-term demand for operational resilience assessments and third-party risk reviews.

How large is the North American security assessment market today?

North America contributed 40.88% of 2025 global revenue, keeping the region in the lead thanks to stringent regulations and mature budgets.

Which industry segment will grow fastest through 2031?

Healthcare and Life Sciences is projected at a 5.92% CAGR as new HIPAA rules require annual audits, multi-factor authentication, and updated inventories.

Why are SMEs expected to increase spending despite budget constraints?

Cloud-delivered, automated platforms reduce entry costs, and insurers plus regulators now demand baseline assessments, driving a 6.63% CAGR in SME uptake.

How large is the Security Assessment market in 2026?

The security assessment market is expected to grow from USD 4.87 billion in 2025 to USD 5.15 billion in 2026 and is forecast to reach USD 6.83 billion by 2031 at 5.78% CAGR over 2026-2031.

Page last updated on: