Endpoint And Cloud Managed Security Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

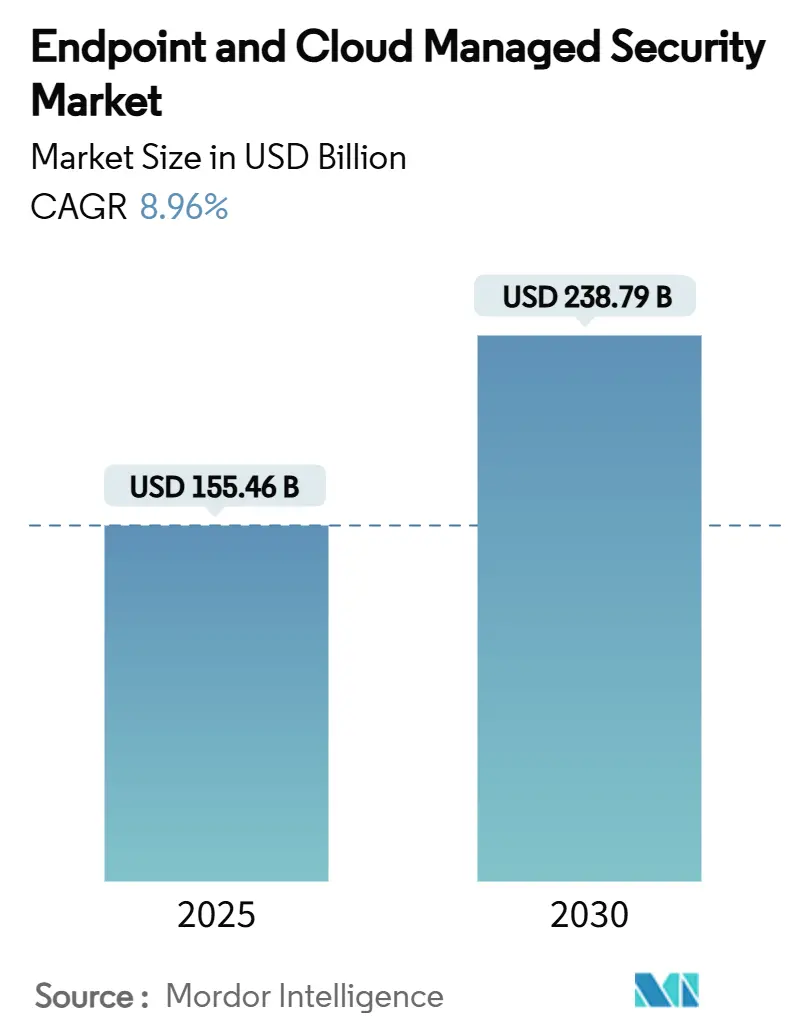

| Market Size (2025) | USD 155.46 Billion |

| Market Size (2030) | USD 238.79 Billion |

| Growth Rate (2025 - 2030) | 8.96% CAGR |

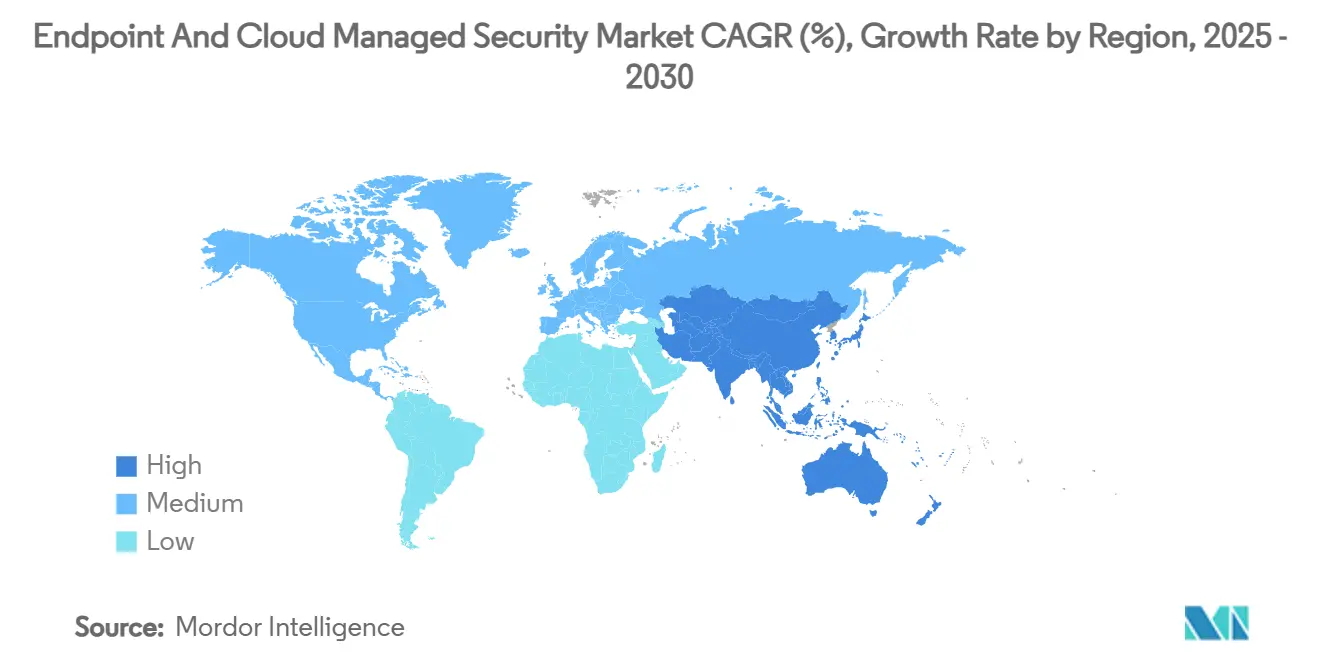

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endpoint And Cloud Managed Security Market Analysis by Mordor Intelligence

The Endpoint and Cloud Managed Security Market reached a current market size of USD 155.46 billion in 2025 and is forecast to attain USD 238.79 billion by 2030, registering an 8.96% CAGR over the period. Rapid enterprise migration to outsourced cyber-operations, hybrid workforce expansion, and cloud-native application growth are steering this trajectory. Heightened cyber-insurance conditions, AI-driven threat-hunting, and geopolitical supply-chain incidents are also intensifying demand for managed detection and response. Consolidation among platform vendors is reshaping provider strategies, while unified security stacks are helping buyers curb tool sprawl and lower total cost of ownership.

Key Report Takeaways

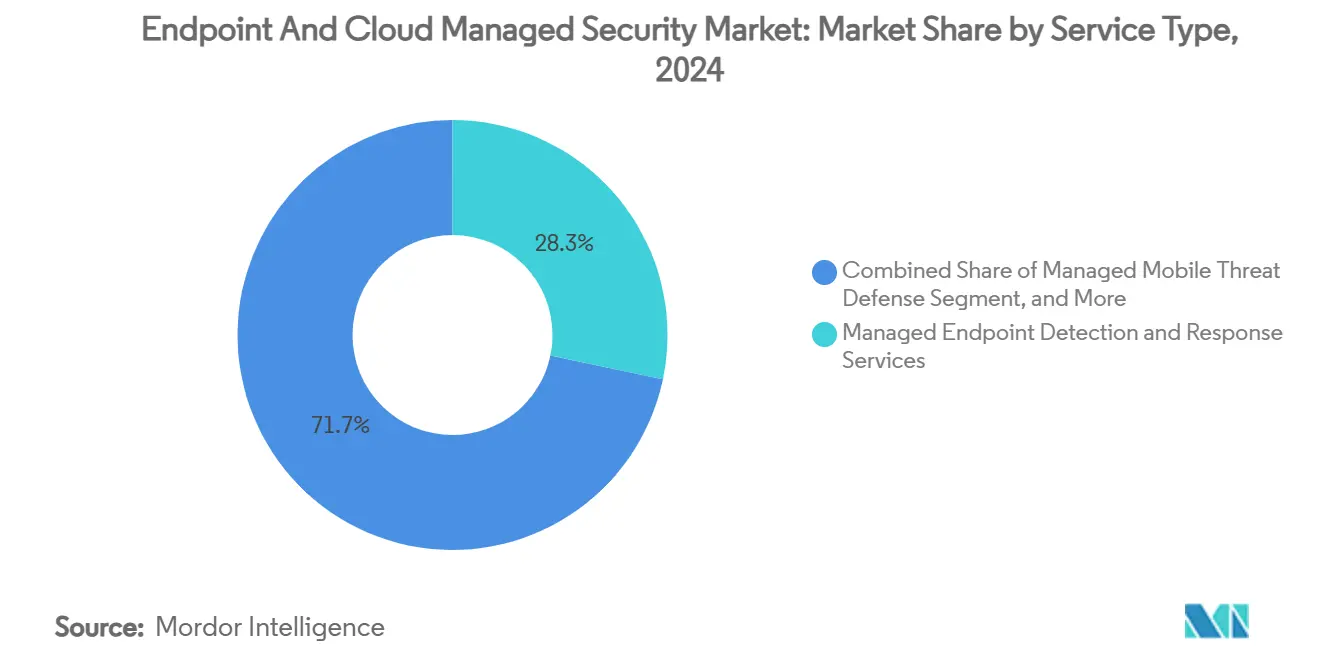

- By service type, Managed Endpoint Detection and Response Services led with 28.3% of the Endpoint and Cloud Managed Security market share in 2024; Managed Unified Endpoint Management Services is projected to compound at a 14.8% CAGR through 2030.

- By deployment mode, cloud-based solutions commanded 66.1% share of the Endpoint and Cloud Managed Security market size in 2024 and are advancing at a 10.6% CAGR through 2030.

- By security type, endpoint security contributed 35.5% to the Endpoint and Cloud Managed Security market size in 2024, while cloud workload security is set to expand at a 13.4% CAGR to 2030.

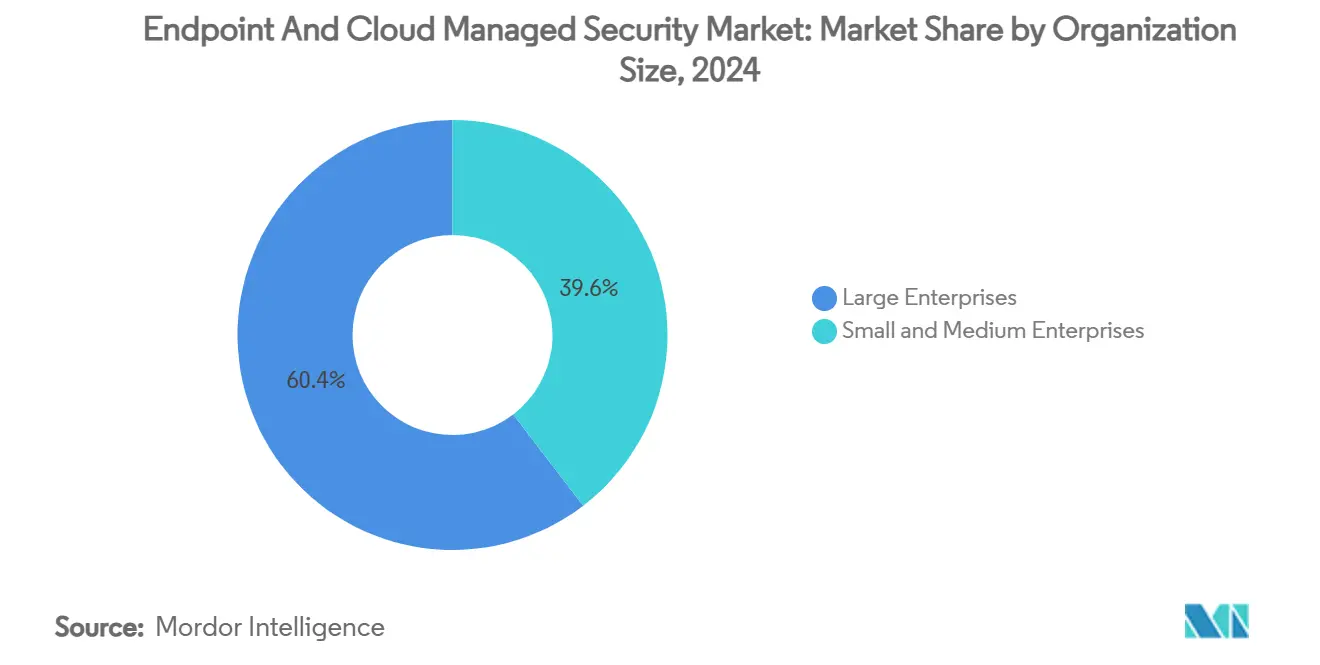

- By organization size, large enterprises captured 60.4% of the Endpoint and Cloud Managed Security market share in 2024; small and medium enterprises are pacing ahead at 11.9% CAGR over the forecast horizon.

- By end-user industry, BFSI held 20.3% revenue share in 2024, whereas healthcare is forecast to rise at a 12.7% CAGR to 2030.

- By geography, North America accounted for 38.7% of the Endpoint and Cloud Managed Security market size in 2024, whereas Asia-Pacific is expanding fastest at 14.2% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Endpoint And Cloud Managed Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of hybrid-work endpoints | +1.8% | Global, with concentration in North America and the EU | Medium term (2-4 years) |

| Surging cloud-native application adoption | +2.1% | Global, led by Asia-Pacific and North America | Long term (≥ 4 years) |

| Cyber-insurance prerequisites for MDR | +1.4% | North America and the EU, expanding to the Asia-Pacific | Short term (≤ 2 years) |

| XDR platform unification demand | +1.6% | Global, enterprise-focused markets | Medium term (2-4 years) |

| AI-driven threat-hunting advances | +1.9% | Global, technology-mature regions | Long term (≥ 4 years) |

| Geo-political supply-chain attacks escalation | +1.2% | Global, critical infrastructure sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Hybrid-Work Endpoints

Organizations now manage triple the endpoint devices compared to pre-2020 levels, increasing attack-surface complexity. Unified monitoring over corporate, personal, and IoT hardware is stretching in-house resources, steering spending toward managed security partners. Microsoft’s Security Copilot integration with Intune shows how AI-guided administration helps sustain visibility at scale.[1]Microsoft Corporation, “What Is XDR? (Extended Detection and Response),” Microsoft, microsoft.com Enterprises report a 40% jump in cybersecurity complexity from hybrid models and admit only 23% possess adequate internal capabilities. Managed services thus deliver consistent policies, identity validation, and compliance without ballooning headcount, reinforcing the Endpoint and Cloud Managed Security Market’s growth arc.

Surging Cloud-Native Application Adoption

Seventy-eight percent of enterprises now operate hybrid or multi-cloud environments, with container, serverless, and microservice workloads proliferating. Fortinet indicates cloud security budgets are expanding 25% annually to 2027, and managed providers are capturing the lion’s share as skills gaps widen. DevSecOps convergence demands expertise spanning legacy endpoints and modern clouds, driving unified outsourcing contracts that embed continuous workload posture management.

Cyber-Insurance Prerequisites for MDR

Insurers increasingly list managed detection and response as a baseline for coverage, akin to former multi-factor authentication mandates. Policyholders without MDR have faced 30-50% premium hikes, prompting compliance-driven procurement even when discretionary budgets tighten. Coalition identifies MDR as a stabilizing risk-reduction pillar for underwriters.

XDR Platform Unification Demand

Average security stacks top 80 tools from nearly 30 vendors, creating operational drag. Consolidated XDR platforms cut deployment overhead by 65% and enhance detection efficacy by 30%, according to Cisco. Managed providers that operate multi-domain telemetry in a single console help enterprises retire redundant licenses and curb alert fatigue, intensifying consolidation momentum within the Endpoint and Cloud Managed Security Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High alert-fatigue and skill shortage | -1.3% | Global, acute in developed markets | Medium term (2-4 years) |

| Data-sovereignty compliance hurdles | -0.9% | EU, Asia-Pacific regulatory regions | Long term (≥ 4 years) |

| Budget squeeze from macro headwinds | -1.7% | Global, cyclical impact | Short term (≤ 2 years) |

| MSP vendor lock-in concerns | -0.8% | Global, enterprise segment focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Budget Squeeze from Macro Headwinds

Economic slowdowns have stalled many security budgets even as threat volume rises. Corporate boards question incremental spend, believing existing controls should suffice. Regulatory mandates such as NIS2 still force minimum investments, creating a split market where compliance-bound sectors sustain spending while discretionary sectors defer projects. Managed security vendors that quantify ROI and consolidate tools earn preference as buyers seek value over breadth.[2]European Union Agency for Cybersecurity (ENISA), “NIS Investments 2024,” enisa.europa.eu

MSP Vendor Lock-in Concerns

Platform bundling by major vendors raises switching costs, pushing enterprises to weigh interoperability against efficiency. Proprietary data models within cloud-security suites can tether customers beyond contract terms. Buyers increasingly request data-portability guarantees and platform-agnostic architectures before signing multiyear deals, tempering some growth prospects for fully integrated offers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: EDR Dominance Drives Consolidation

Managed Endpoint Detection and Response Services held a commanding 28.3% share of the Endpoint and Cloud Managed Security market size in 2024, anchored by cyber-insurance mandates and real-time telemetry gains. Compliance-driven uptake supports steady revenue even when other discretionary categories decelerate. Managed Unified Endpoint Management Services, expanding at 14.8% CAGR, reflect enterprise appetites for single-pane device governance spanning laptops, mobiles, and IoT endpoints.

Functional convergence is blurring the lines between endpoint management and security. Providers now package device administration, threat detection, and policy compliance in a unified subscription, reducing the total vendor count. Traditional antivirus services have commoditized, prompting vendors to emphasize behavioral analytics and tailored response playbooks. Identity, DLP, and emerging mobile-threat defense services round out portfolios as clients broaden protection layers.

By Deployment Mode: Cloud-First Transformation Accelerates

Cloud-based delivery captured 66.1% Endpoint and Cloud Managed Security market share in 2024 and is on track for a 10.6% CAGR to 2030. Organizations favor elastic, API-driven controls over fixed hardware, particularly as AI analytics workloads need continuous model refreshes. On-premise installations persist in highly regulated sectors, yet many adopt hybrid overlays where local sensors feed cloud analytics.

Security service edge adoption further tilts uptake toward cloud, combining network access control and threat inspection within managed offerings.[3]Hewlett Packard Enterprise, “Simplify Zero Trust from Edge to Cloud with a Holistic SASE Platform,” HPE, community.hpe.com Total cost of ownership studies show 40-60% savings compared with equivalent in-house setups after factoring in infrastructure depreciation, staff, and patching overheads.

By Security Type: Endpoint Security Leads Platform Integration

Endpoint security retained 35.5% m arket share in 2024, underscoring its role as the first line of enterprise defense. Meanwhile, cloud workload security is rising at a 13.4% CAGR as containerized and serverless workloads proliferate across public clouds. CASB, email, web, and identity controls mature in parallel, driven by zero-trust frameworks.

Unified XDR consoles are collapsing previously siloed telemetry, enabling managed partners to correlate endpoint and cloud-workload events within seconds. Microsoft reports 30-40% false-positive reduction after integrating endpoint and cloud signals. Providers with AI-fused analytics attract clients seeking faster mean-time-to-respond and leaner staffing models.

By Organization Size: SME Growth Outpaces Enterprise Adoption

Large enterprises commanded 60.4% Endpoint and Cloud Managed Security market share in 2024 due to their sprawling digital estates and regulatory scrutiny. Their multi-business-unit complexity often necessitates outsourced 24/7 SOC coverage. Small and medium enterprises, however, clock an 11.9% CAGR through 2030 as cloud-delivered security democratizes enterprise-grade defenses.

SMEs cite cost-effectiveness and skills scarcity as primary drivers. Fortified by cyber-insurance checkpoints, many adopt managed services to satisfy baseline control frameworks without staffing their analysts. Total cost studies show managed SOCs delivering equivalent coverage at up to 70% lower ownership cost for firms with fewer than 1,000 employees.

By End-User Industry: Healthcare Transformation Drives Fastest Growth

BFSI retained 20.3% revenue share in 2024, given its high-value data troves and mature regulation. Healthcare, forecast to rise at a 12.7% CAGR, faces connected-device proliferation and stringent patient-privacy rules. Ransomware-prone manufacturing and critical OT environments follow closely behind, requiring dual IT-OT controls.

Government and defense maintain steady demand, anchored by national-security imperatives and sovereign-cloud mandates. Energy and utilities continue to invest in OT visibility after several high-profile grid incidents. Retail and e-commerce uptake accelerates on payment-card compliance and brand-reputation concerns linked to breach headlines.

Geography Analysis

North America accounted for 38.7% of the Endpoint and Cloud Managed Security market size in 2024, buoyed by early cloud-security adoption, mature cyber-insurance markets, and sizable government outsourcing frameworks. The U.S. Treasury’s USD 20 billion support contract illustrates federal appetite for long-term managed partnerships. Canadian organizations align with U.S. standards, while cross-border providers leverage shared language and regulatory commonalities to streamline service delivery.

Asia-Pacific, forecast to expand at a 14.2% CAGR, benefits from explosive digital-service uptake and widening regulatory frameworks. Google Cloud’s Indonesia BerdAIa initiative, which deploys AI-enabled SOC capabilities within local data centers, demonstrates provider localization strategies. Rising cybercrime and skill shortages amplify demand for turnkey managed offerings across ASEAN and South Asian economies.

Europe sustains growth through NIS2, GDPR, and upcoming AI regulations, driving compliance-centric outsourcing. ENISA notes that security now consumes 9% of EU IT budgets, reflecting year-on-year elevation. Providers boasting local-data processing, multi-language SOC support, and EU-certified hosting attract enterprises balancing sovereignty with operational agility.

Competitive Landscape

The Endpoint and Cloud Managed Security Market remains moderately fragmented, yet high-value acquisitions signal accelerating concentration. Sophos’ USD 859 million takeover of Secureworks added Taegis XDR to its stack, deepening endpoint-to-cloud coverage. Palo Alto Networks’ pursuit of SentinelOne (valuation near USD 7 billion) points to similar endpoint reinforcement motives. Cloud providers likewise seek cyber depth; Google’s unsuccessful approach for Wiz underscores the strategic value placed on unified workload security capabilities.

Start-ups wield AI to shorten mean-time-to-detect. Exaforce raised USD 75 million to automate SOC processes, while Tenable acquired Apex Security to embed AI model governance into its Tenable One suite.[4]Channel Futures, “Tenable Buying AI Cybersecurity Startup Apex Security for ‘Next Frontier of AI Security,’” channelfutures.com Vertical specialists focus on healthcare, manufacturing, and OT, leveraging domain expertise to counterbalance broad-spectrum giants.

Differentiation hinges on telemetry fusion, automation depth, and measurable resilience gains. Providers capable of cutting false positives and compressing response windows secure multi-year renewals. Platform unification also raises switching costs, heightening retention yet amplifying lock-in concerns that favor modular, standards-based approaches in regulated industries.

Endpoint And Cloud Managed Security Industry Leaders

CrowdStrike Holdings, Inc.

Palo Alto Networks, Inc.

Microsoft Corp.

Trend Micro Incorporated

SentinelOne, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Google Cloud launched the Indonesia BerdAIa for Security program to deliver AI-enabled cyber defense with in-country data residency.

- July 2025: Compliance platform Vanta closed a USD 150 million funding round, reaching a USD 4 billion valuation through expansion of automated security audits.

- July 2025: Israel’s cybersecurity ecosystem secured 40% of U.S. venture inflows, with private funding doubling year-on-year.

- June 2025: Tenable acquired Apex Security to integrate AI usage risk management within Tenable One.

Global Endpoint And Cloud Managed Security Market Report Scope

| Managed Endpoint Detection and Response Services |

| Managed Antivirus/Antimalware Services |

| Managed Identity and Access Management Services |

| Managed Data Loss Prevention Services |

| Managed Mobile Threat Defense |

| Managed Unified Endpoint Management Services |

| Others |

| On-premise |

| Cloud-based |

| Hybrid |

| Endpoint Security |

| Cloud Workload Security |

| Cloud Access Security Broker (CASB) |

| Cloud Email Security |

| Cloud Web Security |

| Cloud Identity Security |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| IT and Telecom |

| Healthcare |

| Retail and E-commerce |

| Manufacturing |

| Government and Defense |

| Energy and Utilities |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Managed Endpoint Detection and Response Services | ||

| Managed Antivirus/Antimalware Services | |||

| Managed Identity and Access Management Services | |||

| Managed Data Loss Prevention Services | |||

| Managed Mobile Threat Defense | |||

| Managed Unified Endpoint Management Services | |||

| Others | |||

| By Deployment Mode | On-premise | ||

| Cloud-based | |||

| Hybrid | |||

| By Security Type | Endpoint Security | ||

| Cloud Workload Security | |||

| Cloud Access Security Broker (CASB) | |||

| Cloud Email Security | |||

| Cloud Web Security | |||

| Cloud Identity Security | |||

| By Organization Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By End-User Industry | BFSI | ||

| IT and Telecom | |||

| Healthcare | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Government and Defense | |||

| Energy and Utilities | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the Endpoint and Cloud Managed Security Market by 2030?

It is expected to reach USD 238.79 billion, reflecting an 8.96% CAGR over 2025-2030.

Which service type currently generates the largest revenue?

Managed Endpoint Detection and Response Services lead with 28.3% share in 2024.

Why are SMEs adopting managed security faster than large enterprises?

Cloud-delivered SOC services offer enterprise-grade protection at up to 70% lower total cost, easing skills and budget constraints.

Which region is expanding at the highest rate through 2030?

Asia-Pacific is growing at a 14.2% CAGR, supported by rapid digitalization and new regulatory frameworks.

How are cyber-insurance requirements influencing buying patterns?

Insurers increasingly mandate MDR, driving organizations to outsource detection and response to qualify for affordable coverage.

What technological factor is most reshaping provider competition?

Unified XDR platforms combining endpoint and cloud telemetry allow vendors to cut false positives and accelerate automated response.

Page last updated on: