Market Overview

| Study Period | 2021 - 2031 |

|---|---|

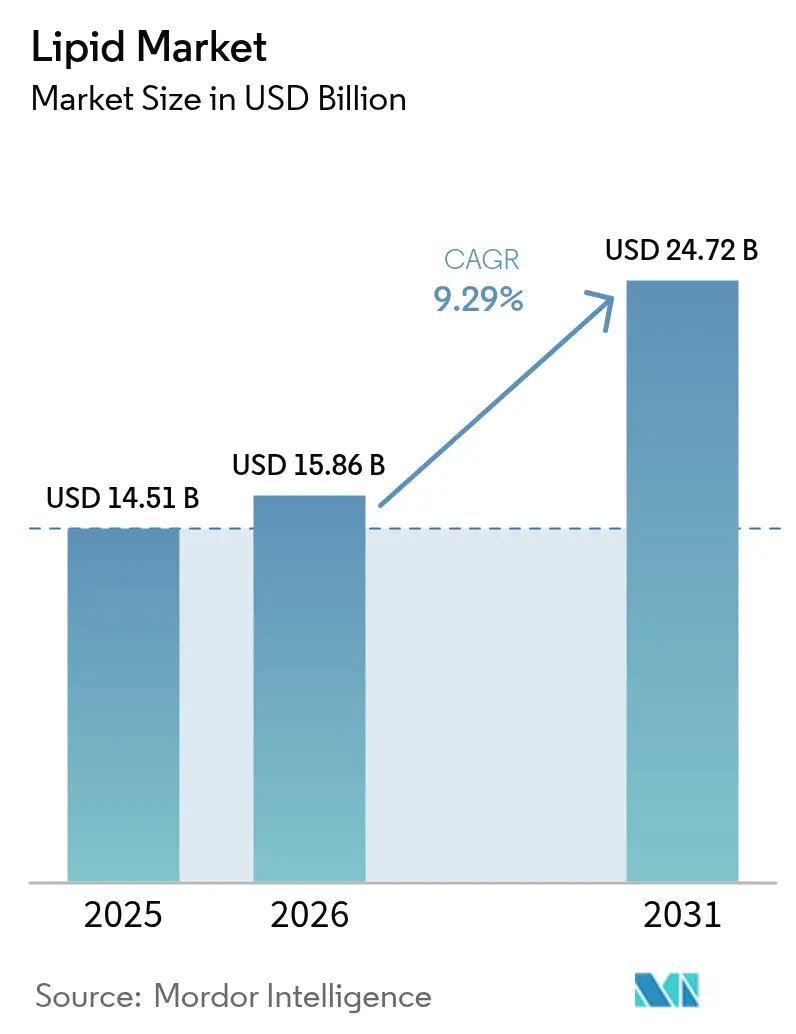

| Market Size (2026) | USD 15.86 Billion |

| Market Size (2031) | USD 24.72 Billion |

| Growth Rate (2026 - 2031) | 9.29% CAGR |

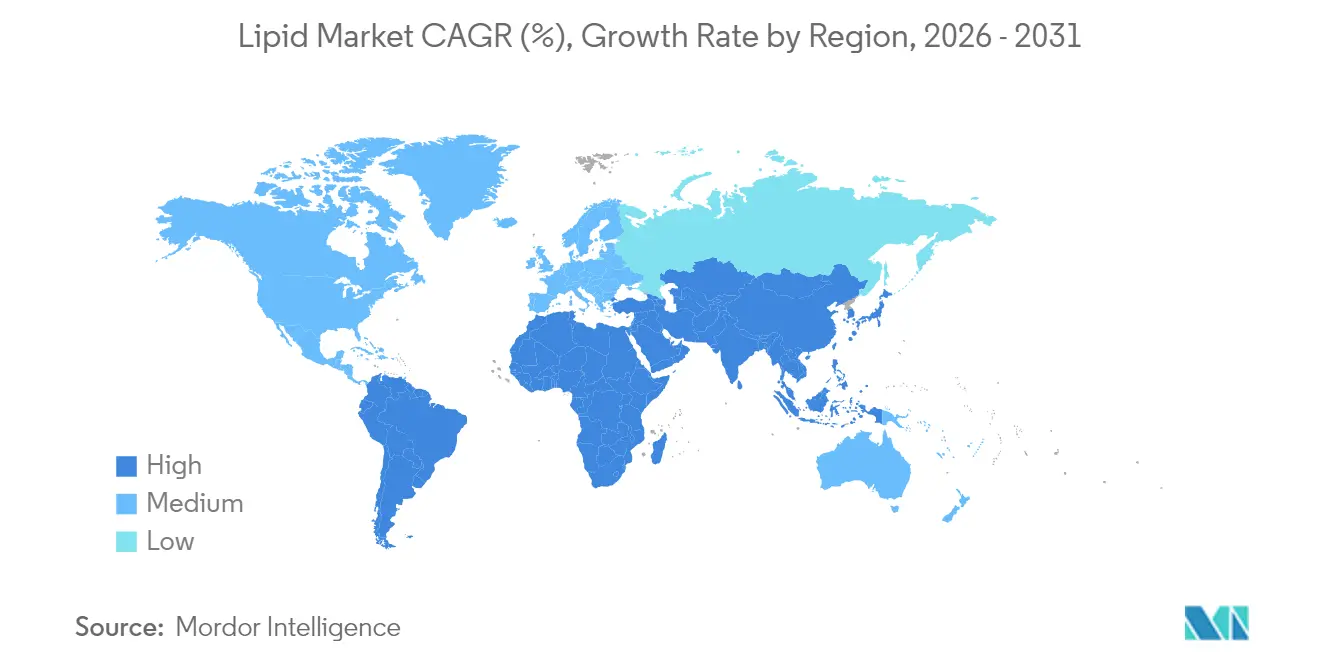

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

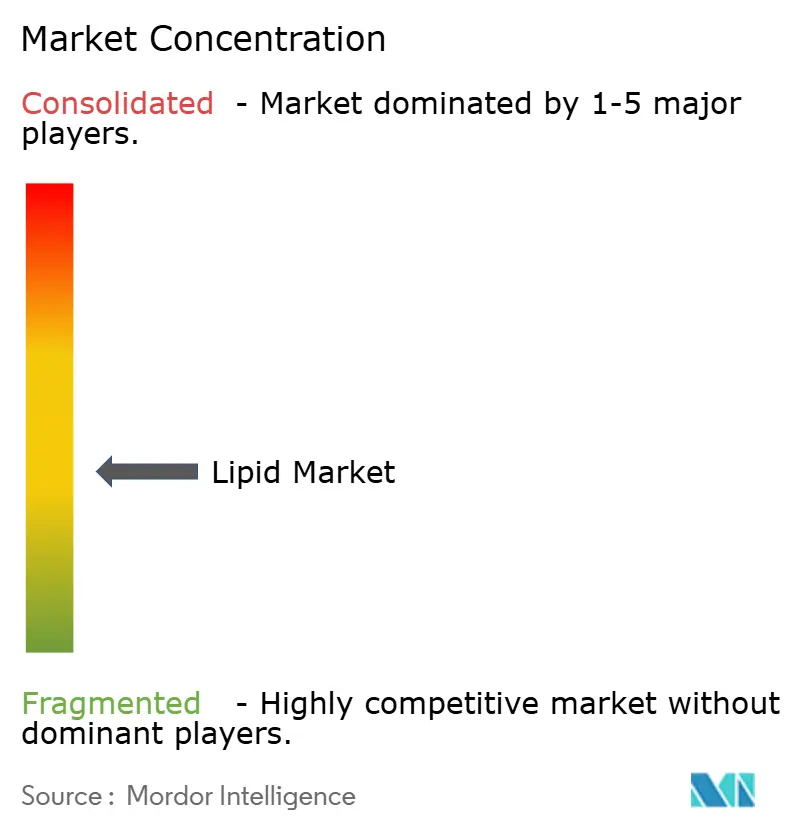

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lipid Market Analysis by Mordor Intelligence

The lipids market size is expected to grow from USD 14.51 billion in 2025 to USD 15.86 billion in 2026 and is forecast to reach USD 24.72 billion by 2031 at 9.29% CAGR over 2026-2031. By 2030, it's set to grow to an estimated USD 22.75 billion, marking a notable CAGR of 9.41%. This optimistic forecast is driven by heightened awareness of cardiovascular health, biotechnological advancements reducing reliance on marine sources, and evolving regulations endorsing healthy fats in diets. As metabolic disorders become more prevalent, consumers increasingly associate lipid intake with cellular health, cognitive function, and disease prevention. On the supply side, fermentation platforms are emerging as key players, offering high-purity fatty acids independent of marine stock limitations. Companies emphasizing traceable sourcing, tailored nutrition, and sustainability are reaping premium prices in food, feed, and pharmaceutical markets. The lipids market is now prioritizing science-driven differentiation over sheer commodity scale, especially in niches like personalized nutrition, athletic performance, and advanced drug delivery systems.

Key Report Takeaways

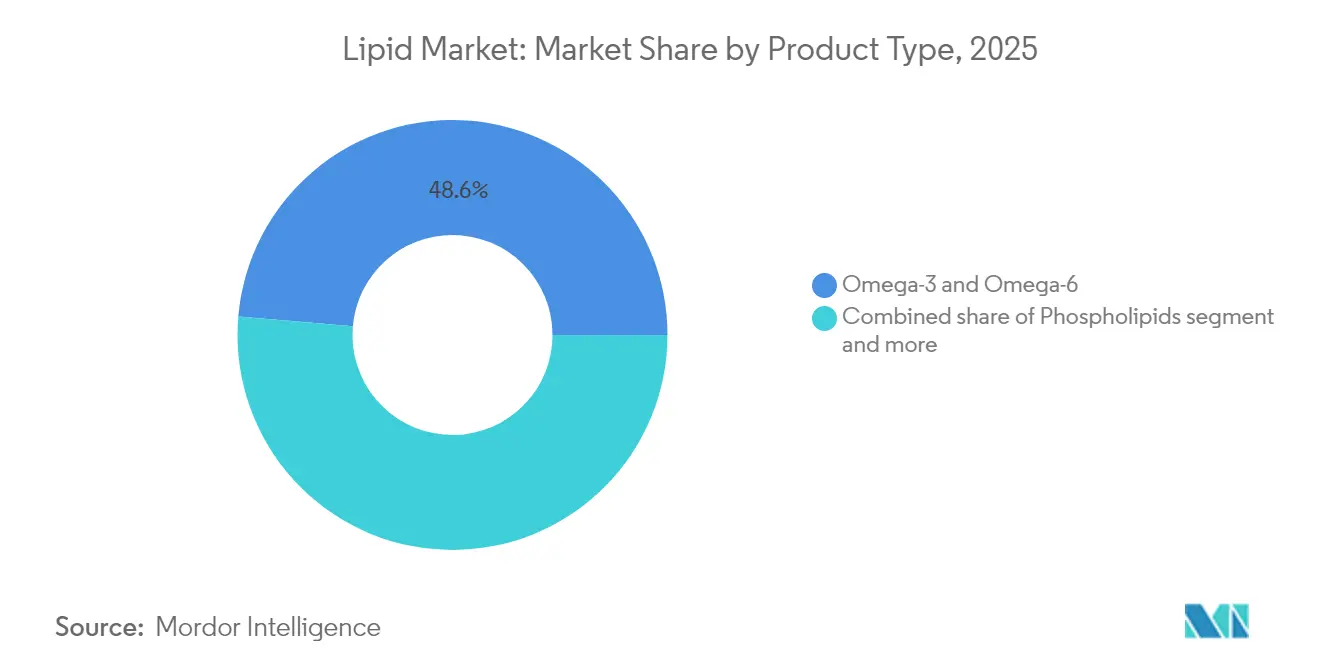

- By product type, omega-3 and omega-6 fatty acids led with 48.62% of the lipids market share in 2025, while medium-chain triglycerides are forecast to grow at an 11.42% CAGR to 2031.

- By source, plant-derived ingredients commanded 61.92% revenue share of the lipids market in 2025; the same segment is projected to expand at a 11.96% CAGR through 2031.

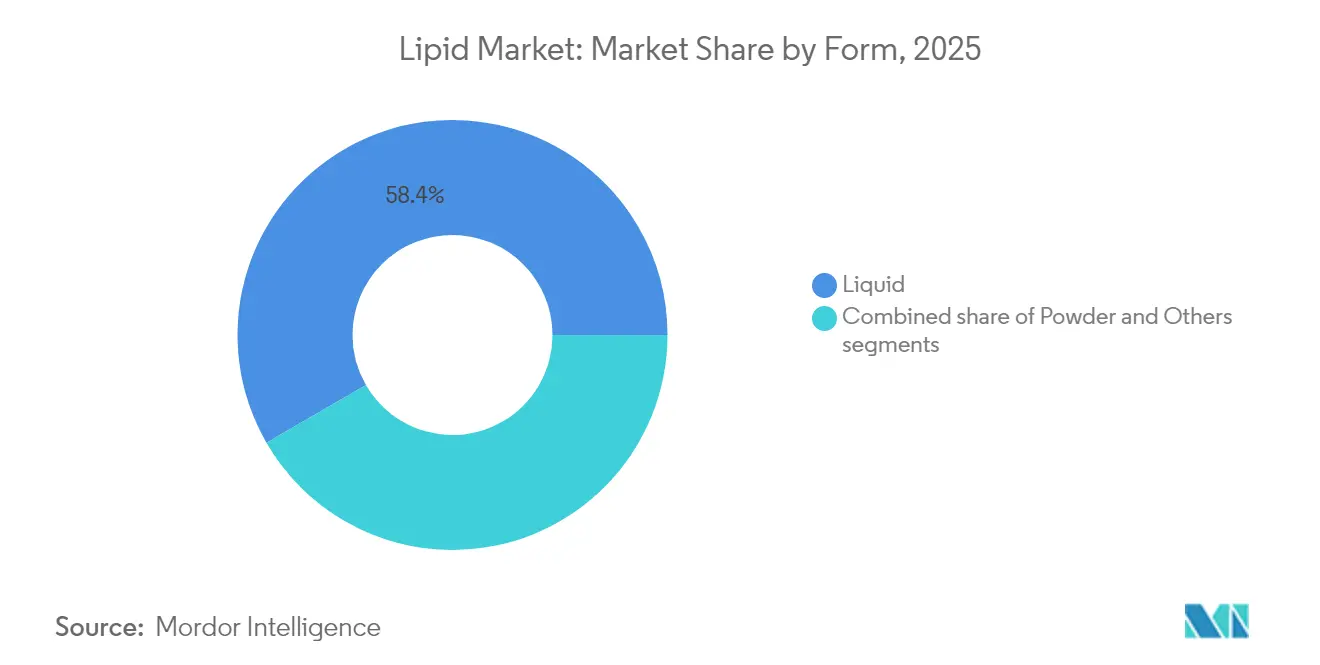

- By form, liquid formulations accounted for 58.35% share of the lipids market size in 2025 and are advancing at a 10.78% CAGR to 2031.

- By application, pharmaceutical uses are set to register the fastest 10.49% CAGR, and dietary supplements continue to hold 46.74% of the lipids market size in 2025.

- By geography, Europe dominated with a 37.32% share of the lipids market in 2025, whereas Asia-Pacific is pacing ahead at 11.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lipid Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for lipid-based dietary supplements | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Increasing prevalence of cardiovascular and metabolic disorders | +1.8% | Global, particularly Asia-Pacific and North America | Long term (≥ 4 years) |

| Rising use of lipids in functional health foods | +1.5% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| The animal feed and aquafeed industries demonstrate growing lipid utilization | +1.3% | Global, with emphasis on Asia-Pacific aquaculture markets | Long term (≥ 4 years) |

| Expanding lipid use in nutritional food fortification | +1.2% | Global, led by developed markets | Medium term (2-4 years) |

| Surging popularity of personalized dietary solutions | +0.9% | North America and Europe, early adoption markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for lipid-based dietary supplements

The dietary supplements sector's lipid consumption surge reflects a fundamental shift from generic multivitamins to targeted metabolic interventions. Omega-3 supplementation protocols now emphasize EPA-to-DHA ratios for specific health outcomes, with the International Society of Sports Nutrition establishing that athletes require higher omega-3 intake due to increased oxidative stress. This precision approach drives premium pricing and creates barriers for commodity suppliers. The Office of Dietary Supplements' 2025 guidance recommending 250 mg/day DHA plus EPA for women of childbearing age, with an additional 100-200 mg/day DHA during pregnancy, establishes new baseline consumption standards [1]Source: National Institute of Health, "New guidance from Office of Dietary Supplements on omega-3s for pregnancy health", ods.od.nih.gov. Medium-chain triglyceride (MCT) supplements capitalize on ketogenic diet adoption and cognitive enhancement trends, while phospholipid formulations target cellular membrane optimization. The regulatory clarity around omega-3 health claims enables direct-to-consumer marketing strategies that bypass traditional retail channels.

Increasing prevalence of cardiovascular and metabolic disorders

Cardiovascular disease prevalence in Asia-Pacific creates the world's largest untapped lipid intervention market. According to the American Heart Foundation data from 2025, one in 6 people in Australia are suffering from cardiovascular diseases [2]Source: American Heart Foundation, "Prevalence of Cardiovascular Diseases in Australia", heartfoundation.org.au. This geographic disparity reflects dietary transition patterns and healthcare infrastructure gaps that favor preventive nutrition strategies. Merck's successful late-stage cholesterol drug trials in 2025 validate lipid metabolism as a pharmaceutical target, potentially expanding prescription omega-3 usage beyond current triglyceride indications. The REDUCE-IT trial's cardiovascular benefits with purified EPA contrast with mixed results from combination formulations, suggesting product differentiation opportunities based on fatty acid composition. Metabolic syndrome's rising incidence drives demand for lipid interventions that address insulin sensitivity and inflammatory markers simultaneously. Healthcare cost pressures favor nutritional interventions over pharmaceutical treatments, creating market expansion opportunities for evidence-based lipid formulations.

Rising use of lipids in functional health foods

Functional food fortification with omega-3 fatty acids transforms commodity food categories into premium health platforms, with yogurt, bread, and beverage applications demonstrating successful commercial implementation. Microencapsulation technologies enable omega-3 integration without sensory compromise, addressing the primary barrier to consumer acceptance. The FDA's updated "healthy" claim criteria (2025) that emphasize nutrient density over fat restriction create regulatory tailwinds for lipid-fortified products [3]Source: U.S. Food and Drug Administration, “Updated Definition of ‘Healthy’ Claims,” fda.gov. Plant-based beverage fortification addresses omega-3 deficiencies in dairy alternatives, with algal oils providing sustainable sourcing that aligns with environmental consumer preferences. The convergence of clean label demands and functional nutrition creates opportunities for naturally-derived lipid ingredients that replace synthetic alternatives.

The animal feed and aquafeed industries demonstrate growing lipid utilization

In January 2025, global fishmeal production surged by 75% year-over-year, largely due to a rebound in Peruvian output. However, this uptick in supply volatility underscores the growing strategic significance of plant-based alternatives, as highlighted by data from the IFFO, Marine Ingredients Organization in 2024. The reliance on traditional fishmeal sources continues to face challenges, emphasizing the need for sustainable and stable alternatives. Different fish species have varying phospholipid needs, paving the way for tailored lipid blends that enhance growth and bolster stress resilience. The development of customized lipid formulations offers significant potential for improving aquaculture efficiency and productivity. Meanwhile, trends in alternative proteins for human nutrition are propelling aquaculture production, further intensifying the demand for specialized lipid formulations. The growing focus on sustainable protein sources in human diets is driving innovation in aquaculture, creating opportunities for advanced lipid solutions to meet evolving market demands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High costs associated with lipid synthesis and production | -1.4% | Global, particularly affecting emerging markets | Short term (≤ 2 years) |

| Volatility in raw material supply and prices | -1.1% | Global, with acute impact on marine-sourced lipids | Short term (≤ 2 years) |

| Challenges with oxidative stability and shelf life | -0.8% | Global, affecting all lipid categories | Medium term (2-4 years) |

| Strict regulatory requirements for lipid manufacturing and quality standards | -0.6% | Primarily North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High costs associated with lipid synthesis and production

According to data from the Royal Society of Chemistry, the production cost of microbial lipid is 1.60 per kilogram. This pricing positions single-cell oils as economically viable alternatives to conventional sources, but primarily in high-value applications. The cost structure is influenced by pricey fermentation substrates and energy-heavy downstream processing, which in turn restricts scalability for broader commodity applications. These challenges highlight the need for advancements in fermentation technology and downstream processing to reduce costs and improve scalability. Meanwhile, traditional marine lipid extraction grapples with challenges: rising vessel fuel costs and dwindling fish stocks introduce price volatility. Additionally, the environmental impact of overfishing and fuel consumption is driving the search for sustainable alternatives. Furthermore, the capital-intensive nature of lipid refinement facilities poses entry barriers for smaller players, inadvertently favoring integrated operations. This dynamic underscores the importance of innovation and investment in cost-effective and sustainable lipid production methods.

Volatility in raw material supply and prices

Weather patterns, including rainfall variability, temperature fluctuations, and extreme climate events, significantly impact oilseed crop yields throughout growing seasons. These environmental factors make it challenging for suppliers to establish stable, long-term pricing contracts with buyers. The marine lipid supply chain faces substantial constraints from government-imposed fishing quotas, seasonal fish migration patterns, and limited harvesting windows, which concentrate production activities in specific coastal regions. The growing demand for lipids across multiple sectors - food products, animal feed formulations, and biofuel production - creates intense competition and upward price pressures in the market. Exchange rate fluctuations in major producing countries introduce additional cost uncertainties for international suppliers managing cross-border transactions and long-term supply agreements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Medium-Chain Triglycerides (MCTs) Drive Premium Growth

The medium-chain triglycerides segment is expected to grow at a CAGR of 11.42% through 2031, while the omega-3 and omega-6 segment held a 48.62% market share in 2025. The growth in MCTs reflects their expanding applications beyond sports nutrition into pharmaceutical drug delivery and ketogenic therapeutic protocols. Omega-3 and omega-6 fatty acids maintain their market position through established cardiovascular health benefits and regulatory approvals, despite facing price pressure from increased competition. Phospholipids continue to grow due to their use in pharmaceutical applications, particularly in liposome drug delivery systems.

Biotechnology advancements in lipid production enable the development of fatty acid profiles for specific therapeutic purposes, expanding beyond traditional omega-3 supplements into precision nutrition. Product categories such as structured lipids and specialty phospholipids serve specific applications in infant nutrition and pharmaceutical ingredients. The segmentation of products now reflects technological capabilities rather than the availability of natural sources, indicating ongoing innovation in product differentiation.

By Source: Plant-Based Dominance Accelerates

Plant-based sources held a 61.92% market share in 2025 and are projected to grow at a CAGR of 11.96% through 2031. This dominance reflects the market's transition toward sustainable sourcing practices. Consumer preferences increasingly align with environmental sustainability, while concerns about marine supply chain reliability further strengthen the position of plant-based sources. The marine lipids segment faces supply constraints from depleting fish stocks and strict fishing quotas, resulting in price fluctuations that enhance the appeal of plant-based alternatives.

Animal-based sources remain important in pharmaceutical excipients and infant nutrition due to regulatory approval of established ingredients. However, synthetic lipids produced through fermentation technologies provide precise control over fatty acid compositions while addressing sustainability concerns associated with traditional sourcing methods. The industry's increasing adoption of biotechnology platforms indicates a shift where technological capabilities may become more valuable than access to natural resources.

By Form: Liquid Maintains Processing Advantages

In 2025, liquid formulations command a 58.35% share of the market and are projected to maintain a 10.78% CAGR through 2031. This preference for liquids is attributed to their superior bioavailability and greater manufacturing flexibility over powders. Liquids can be directly incorporated into food and beverage applications, eliminating the need for extra processing steps. On the other hand, powders are tailored for specific uses, such as dietary supplement tablets and capsules, where an extended shelf life and ambient storage are paramount.

Beyond liquids and powders, other formats like emulsions and encapsulated systems cater to specialized delivery needs in pharmaceuticals and functional foods. As technology advances, the industry is witnessing a shift: form segmentation is now more about application-specific optimization than mere processing constraints. Notably, liposomal delivery systems are emerging as a groundbreaking innovation, boosting bioavailability and tackling stability challenges.

By Application: Pharmaceuticals Outpace Traditional Supplements

Pharmaceutical applications are projected to grow at a CAGR of 10.49% through 2031, while dietary supplements maintained a dominant 46.74% market share in 2025. This growth trajectory reflects the increasing adoption of lipid-based drug delivery systems and prescription omega-3 formulations for medical conditions. The food and beverage segment expands due to functional nutrition trends and established regulatory frameworks for health claims. Animal feed applications continue to grow, driven by aquaculture development and the demand for sustainable protein sources.

The pharmaceutical segment maintains high prices due to complex manufacturing processes and clinical validation requirements, which create barriers to entry. Applications in cosmetics and industrial sectors represent niche markets with distinct performance needs. The market's shift toward regulated therapeutic applications indicates ongoing price premiumization and market consolidation among companies with regulatory compliance capabilities.

Geography Analysis

Europe held a 37.32% share of the market in 2025, reflecting its established regulatory framework and consumer awareness of functional nutrition. While the region's mature market shows limited growth potential compared to emerging economies, regulatory developments continue to strengthen its position. The European Food Safety Authority's 2025 approval of Schizochytrium limacinum oil for infant formula applications exemplifies this ongoing regulatory progress . The region's focus on sustainability and clean label products has increased demand for plant-based and biotechnology-derived lipids over traditional marine sources. While Brexit has created supply chain challenges, it has also enhanced regional production capabilities. Europe's aging population and rising healthcare costs support the continued adoption of premium products, despite the overall market maturity.

Asia-Pacific is growing at 11.02% CAGR through 2031, driven by varying cardiovascular disease rates across countries that require specific interventions. China's economic growth and expanding healthcare system support the adoption of preventive nutrition approaches. India's pharmaceutical manufacturing capabilities establish the region as a key production center. Japan's aging demographics and developed healthcare infrastructure increase the consumption of premium omega-3 supplements. Australia's regulatory framework, aligned with global standards, enables market access for international suppliers. The expanding aquaculture sector increases the demand for specialized lipid formulations in feed products. South Korea's technological advancement supports the development of innovative delivery systems and personalized nutrition solutions.

North America's market growth is supported by clear FDA regulations and established health claim pathways, which enable direct marketing to consumers and premium pricing for scientifically validated formulations. The United States dominates prescription omega-3 sales through healthcare system integration and insurance coverage for specific conditions. Canada's natural health product regulations offer alternative approval routes beneficial for smaller companies. Mexico presents growth opportunities for functional nutrition products due to its expanding middle class and improved healthcare access. The region's developed sports nutrition market increases the consumption of MCTs and specialized lipids beyond cardiovascular applications. North America maintains its position as a global innovation hub for lipid-based therapeutics through its advanced research infrastructure and clinical trial capabilities.

Competitive Landscape

In the lipids market, food-ingredient manufacturers, marine oil specialists, and biotech firms compete for market share, leading to moderate fragmentation. Major players utilize global refining networks, integrated logistics, and comprehensive regulatory knowledge to secure contracts with large consumer packaged goods (CPG) companies and pharmaceutical firms. Meanwhile, biotech newcomers are reshaping supply chains by offering single-cell oils. These oils maintain consistent profiles, unaffected by seasonal catch fluctuations, making them attractive for sustainability-driven contracts.

As the market evolves, established companies are increasingly acquiring niche startups specializing in fermentation or encapsulation. This strategy grants them access to unique strains and intellectual property. Additionally, collaborations are forming between agricultural commodity firms and synthetic biology companies. The pharmaceutical excipients segment sees heightened competition. Here, the demand for clinical-grade purity and adherence to Good Manufacturing Practices (GMP) creates high entry barriers, limiting the number of suppliers. On another front, digital nutrition platforms are innovating by combining genetic testing with tailored lipid packages. This strategy not only strengthens consumer loyalty but also pushes traditional bulk suppliers to explore value-added services.

Commodity exchanges are promoting price transparency, which in turn limits profit margins. As a response, companies are seeking differentiation through branded concentrates, sustainability certifications, and patented delivery mechanisms. To navigate the complexities of the lipid market, successful players are adopting a dual approach: they emphasize innovation while simultaneously managing risks. By diversifying their sources to include marine, plant, and microbial inputs, they're ensuring a steady supply and continuity in the market.

Lipid Industry Leaders

-

Cargill, Incorporated

-

BASF SE

-

Archer Daniels Midland Company

-

DSM-Firmenich

-

Croda International Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Natac, through its omega-3 division Innovaoleo, has unveiled Omega 3 Star, a premium fish oil tailored for the food, nutraceutical, and pet nutrition sectors. The oil is rich in essential fatty acids like EPA and DHA.

- October 2024: DSM-Firmenich has unveiled its latest addition to the life's omega-3 nutraceutical lineup: life's DHA B54-0100. DSM touts that Life's DHA B54-0100 packs a punch, offering 545mg of DHA and 80mg of EPA per gram, translating to a robust 620mg of omega-3s in a single serving. This concentrated oil empowers dietary supplement manufacturers to craft smaller, cost-effective capsules without compromising on bioactivity.

- June 2024: In Norway, GC Rieber VivoMega inaugurated a state-of-the-art omega-3 manufacturing facility. This USD 75 million investment is set to double the company's production of premium triglyceride forms of marine omega-3s, namely EPA and DHA, alongside vegan alternatives sourced from algal oils.

- March 2024: Epax launched Omega 3-9-11, promoting benefits for brain and heart health while also enhancing skin vitality. Omega 3-9-11 boasts the highest concentration of an oil that merges EPA and DHA, both long-chain polyunsaturated fatty acids (LC-PUFAs), with the lesser-known long-chain monounsaturated fatty acids (LC-MUFAs).

Global Lipid Market Report Scope

The global lipid market is segmented based on product type, application, and geography. In the product type segment, the market has omega 3 & omega 6, medium-chain triglycerides (MCTS), and others. Based on the application, the market is segmented into food & beverage, nutrition & supplements, feed, pharmaceuticals, and others. The nutrition & supplements segment, followed by the food & beverage segment, is the leading market in terms of segmentation by the application.

By Product Type

| Omega-3 and Omega-6 |

| Medium-Chain Triglycerides (MCTs) |

| Phospholipids |

| Others |

By Source

| Plant-based |

| Marine-based |

| Animal-based |

| Synthetics |

By Form

| Liquid |

| Powder |

| Others |

By Application

| Dietary Supplements |

| Food and Beverage |

| Animal Feed |

| Pharmaceuticals |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Omega-3 and Omega-6 | |

| Medium-Chain Triglycerides (MCTs) | ||

| Phospholipids | ||

| Others | ||

| By Source | Plant-based | |

| Marine-based | ||

| Animal-based | ||

| Synthetics | ||

| By Form | Liquid | |

| Powder | ||

| Others | ||

| By Application | Dietary Supplements | |

| Food and Beverage | ||

| Animal Feed | ||

| Pharmaceuticals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the lipids market?

The lipids market reached USD 15.86 billion in 2026 and is forecast to hit USD 24.72 billion by 2031.

Which product category leads the lipids market?

Omega-3 and omega-6 fatty acids hold 48.62% of 2025 revenue, making them the largest product segment.

Which region is growing fastest in the lipids market?

Asia-Pacific is advancing at an 11.02% CAGR to 2031 due to rising healthcare access and dietary awareness.

Why are liquid lipid formulations so dominant?

Liquid formats offer superior bioavailability and easy incorporation in food, beverage, and pharmaceutical products, which secured 58.35% market share in 2025.

Page last updated on: