Pulse Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

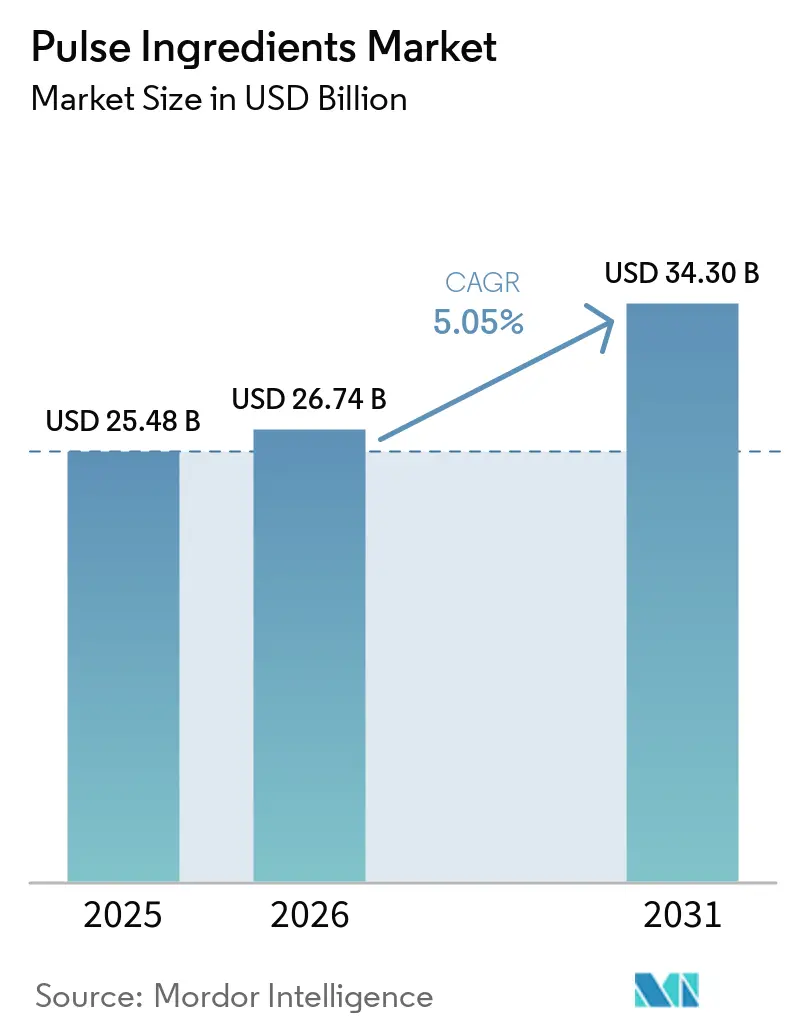

| Market Size (2026) | USD 26.74 Billion |

| Market Size (2031) | USD 34.30 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pulse Ingredients Market Analysis by Mordor Intelligence

The pulse ingredients market size was valued at USD 25.48 billion in 2025 and is estimated to grow from USD 26.74 billion in 2026 to reach USD 34.30 billion by 2031, at a CAGR of 5.05% during the forecast period. Escalating consumer interest in plant-based diets, retailer-driven clean-label mandates, and manufacturing advances that resolve solubility and flavor gaps are enabling pea, chickpea, lentil, and bean derivatives to displace both animal and soy proteins in dairy alternatives, meat analogs, ready-to-mix beverages, and fortified bakery products. Asia-Pacific processors are scaling capacity on supportive agri-policy, the European Union is tightening pesticide-residue and traceability standards that reward certified suppliers, and North American firms are leveraging GRAS and EFSA novel-food clearances to accelerate launches. For instance, data from the Ministry of Agriculture and Farmers Welfare (India) indicate that India’s tur (pigeon pea) production reached approximately three million metric tons in FY 2024, reflecting an increase compared to the preceding fiscal year[1]Source: Ministry of Agriculture and Farmers Welfare (India), "Final estimate of production of foodgrains for 2023-24", www.agriwelfare.gov.in.

Key Report Takeaways

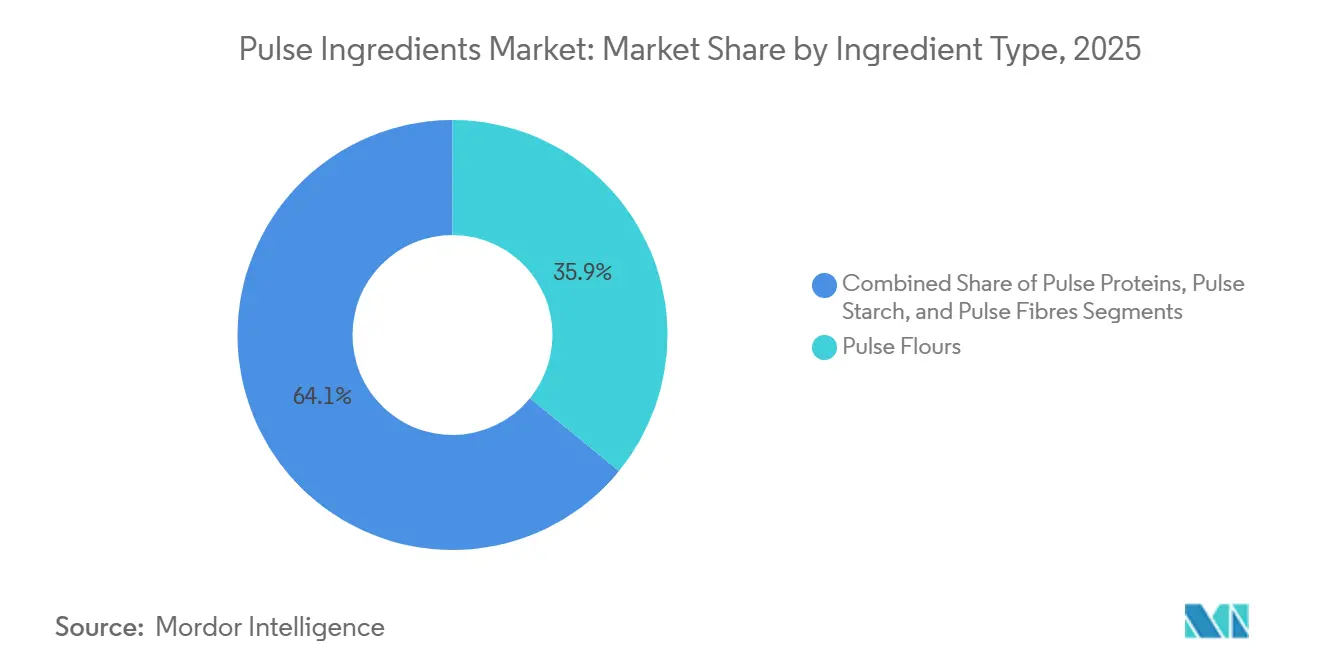

- By ingredient type, pulse flours secured 35.90% revenue share in 2025; pulse proteins are forecast to register the fastest 5.85% CAGR to 2031.

- By source, peas held 34.70% of the pulse ingredients market share in 2025, while chickpeas are set to expand at a 5.60% CAGR through 2031.

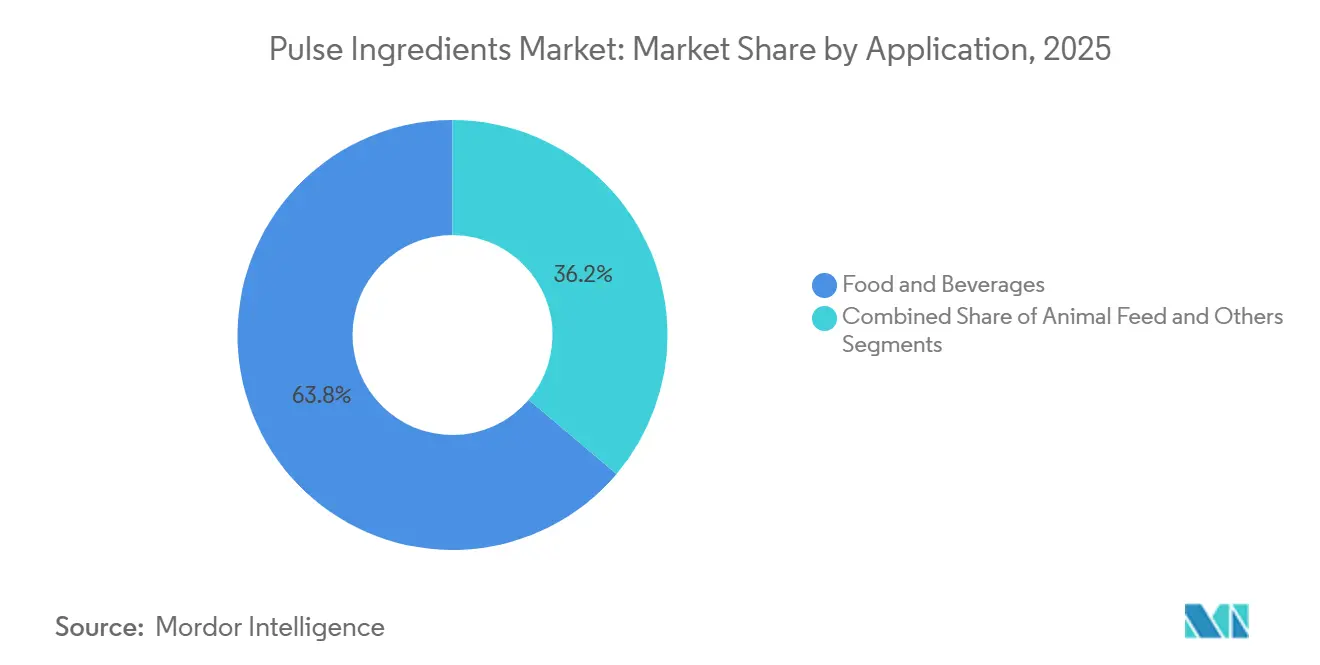

- By application, food and beverages accounted for 63.80% of the pulse ingredients market size in 2025, and animal feed is on track for a 6.05% CAGR to 2031.

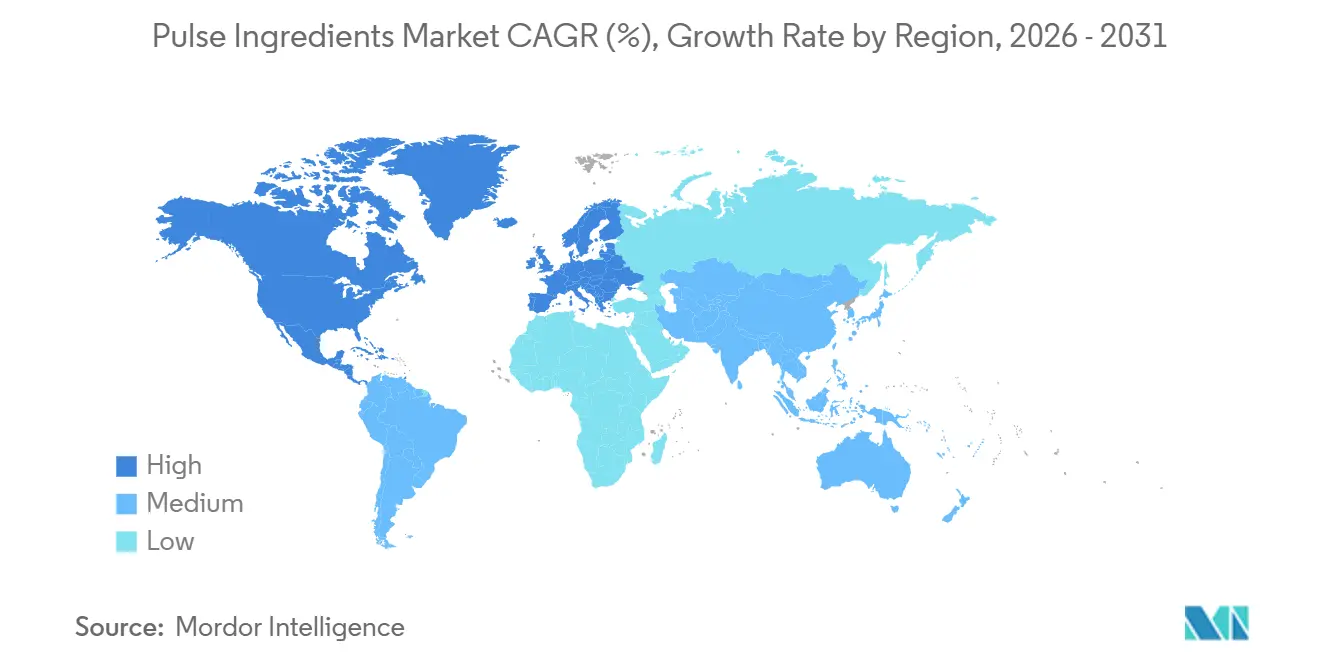

- By geography, Asia-Pacific commanded a 39.10% share of the pulse ingredients market in 2025 and is projected to record a 6.70% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pulse Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Shift Toward Plant-Based and Clean-Label Product Demand | +1.2% | Global, with the strongest uptake in North America & Europe | Medium term (2-4 years) |

| Strong Value Proposition of Pulses Driven by High Protein Content and Nutritional Profile | +0.8% | Global, particularly Asia-Pacific and North America | Long term (≥ 4 years) |

| Rapid Expansion of Foodservice Channels and Processed Food Applications | +0.9% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Advancements and Innovation in Pulse Processing Technologies | +1.1% | Global, led by Europe and North America | Medium term (2-4 years) |

| Favorable Regulatory Landscape Supporting Allergen-Free and Gluten-Free Product Development | +0.7% | North America & Europe, with Asia-Pacific adoption | Long term (≥ 4 years) |

| Accelerating Adoption of Protein Ingredients, Concentrates, and Isolates in Food Formulations | +0.6% | Global, with premium applications in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Shift Toward Plant-Based and Clean-Label Product Demand

Shifting consumer preferences toward transparent, clean-label ingredient lists are accelerating the adoption of pulse-based ingredients across mainstream food categories, with nearly 70% of consumers indicating a willingness to pay a premium for high-protein offerings. According to the International Food Information Council, high-protein and mindful eating emerged as the most widely followed dietary patterns in the United States in 2024, with 18% and 17% of respondents, respectively, adopting these approaches over the past year[2]Source: International Food Information Council, "Food & Health Survey 2024", www.ific.org. This demand is extending beyond traditional meat alternatives into bakery, dairy, and snack segments, where pulse ingredients deliver functional benefits while maintaining clean-label appeal. Regulatory alignment is further reinforcing this trajectory, with updated guidance from the U.S. Food and Drug Administration on allergen labeling providing clearer compliance pathways for pulse-based formulations that exclude major allergens while maintaining strong nutritional profiles. Similarly, the convergence of rising health awareness and sustainability priorities is positioning pulse ingredients as viable alternatives to synthetic additives, particularly in premium segments, where clean-label transparency supports greater pricing power.

Strong Value Proposition of Pulses Driven by High Protein Content and Nutritional Profile

Pulse proteins deliver 80-84% protein content on a dry basis, comparable to whey isolates, while offering intrinsic fiber, potassium, and essential amino acids that appeal to formulators targeting satiety, blood-sugar management, and cardiovascular health[3]Source: FDA, “GRAS Notice No. 1098, Chickpea Protein Concentrate,” fda.gov. The WHO reaffirmed dietary guidance in early 2025, highlighting global fiber insufficiency, and cohort updates from Harvard T.H. Chan School of Public Health linked higher habitual fiber intake to improved cardiometabolic markers and lower inflammation, creating a commercial tailwind for pulse flours and fibers in bakery, snacks, and ready-to-eat meals. Pulse ingredients are uniquely positioned to address this gap because they combine protein density with intrinsic fiber, reducing the need for synthetic fiber additives and enabling clean-label claims. Innova Market Insights reported in 2025 that new product launches with high-fiber claims are growing faster than protein-only claims across categories, signaling a shift in formulator priorities toward multi-functional ingredients.

Rapid Expansion of Foodservice Channels and Processed Food Applications

Foodservice operators are integrating pulse ingredients into menu offerings to meet sustainability commitments and appeal to health-conscious diners, with lentils, chickpeas, and peas increasingly featured in snacks, baked goods, plant-based burgers, and ready-to-eat applications. Processed food manufacturers are reformulating legacy products to incorporate pulse flours and proteins, driven by regulatory pressure to reduce sodium, saturated fat, and added sugars while maintaining texture and mouthfeel. U.S. and EU authorities issued 2025 compliance updates requiring precise fiber quantification for fiber-related claims, compelling suppliers and manufacturers to increase laboratory testing and specify soluble and insoluble fiber breakdowns in sourcing specifications. This regulatory shift is elevating fiber from a marketing claim to a commercial specification, with pulse ingredients benefiting because their intrinsic fiber content can be documented through compositional analysis without reliance on synthetic additives.

Advancements and Innovation in Pulse Processing Technologies

Dry fractionation, wet extraction, and hybrid methods are converging to deliver pulse proteins with improved solubility, emulsification, and neutral flavor profiles, addressing the sensory limitations that have historically constrained adoption. Pulsed electric field processing, air classification, and ultrafiltration are enabling processors to achieve higher protein yields and lower antinutrient levels without organic solvents, aligning with clean-label requirements and reducing production costs. DSM-Firmenich launched two textured vegetable protein (TVP) pea-protein variants in April 2026, Vertis TVP P55m (55% protein) and P65m (65% protein), integrating ModulaSENSE taste-modulation technology embedded during extrusion to reduce bitter, beany, and earthy off-notes, aiming to minimize or replace separate flavor masking systems. This innovation signals a shift from post-formulation flavor masking to in-process taste modulation, simplifying ingredient decks and reducing formulation costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensory Limitations Including Off-Flavors and Suboptimal Texture Profiles | -0.9% | Global, particularly in premium applications | Short term (≤ 2 years) |

| Intensifying Competitive Pressure from Alternative Protein Sources | -0.7% | Global, with intensity in developed markets | Medium term (2-4 years) |

| Risk Exposure to Allergen Cross-Contamination in Production and Supply Chains | -0.4% | North America & Europe, expanding globally | Long term (≥ 4 years) |

| Technical and Functional Constraints in Processing and Product Formulation | -0.6% | Global, concentrated in specialized applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sensory Limitations Including Off-Flavors and Suboptimal Texture Profiles

Persistent sensory limitations, particularly beany, earthy, and bitter off-notes, continue to represent a key adoption barrier for pulse proteins in applications such as dairy alternatives, ready-to-mix beverages, and ready-to-eat meals, where flavor neutrality is a critical purchase driver. Pea protein, in particular, is associated with green and grassy flavor profiles linked to lipoxygenase activity and lipid oxidation during processing, necessitating the use of masking agents (e.g., vanilla, cocoa, or fruit flavors). This increases formulation complexity and cost, while potentially diluting clean-label positioning. Chickpea protein offers a comparatively improved sensory profile; however, residual earthy and nutty notes still constrain its applicability in neutral-flavored formats such as plant-based milks and protein-enhanced beverages. In parallel, texture-related challenges, including grittiness, chalkiness, and suboptimal mouthfeel, persist in liquid systems, primarily due to limited solubility and particle aggregation under standard formulation pH conditions.

Intensifying Competitive Pressure from Alternative Protein Sources

Pulse proteins are encountering intensifying competitive pressure from a broadening set of alternative protein sources, including soy, whey, algae, insect, and cultured proteins, many of which offer advantages in amino acid completeness, sensory neutrality, or differentiated sustainability positioning. Soy protein isolates, with protein concentrations of ~90% and complete amino acid profiles, continue to benefit from decades of regulatory acceptance and entrenched use in sports and clinical nutrition, sustaining their market leadership despite ongoing allergen considerations. In parallel, whey proteins remain the industry benchmark for solubility, emulsification, and clean flavor delivery in applications such as ready-to-mix beverages and protein bars, supported by mature supply chains and cost efficiencies that are difficult for pulse proteins to replicate. Emerging categories, including algae- and insect-based proteins, are progressing toward commercialization with strong sustainability narratives, particularly around reduced land use, water consumption, and greenhouse gas emissions, which resonate with environmentally focused brands and investors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Proteins Gain Share Despite Flour Dominance

Pulse flours accounted for approximately 35.90% of total revenue in 2025, driven by their widespread use in staple bakery and snack applications, where moderate protein levels (20–30%) and inherent fiber content provide cost-effective functionality. However, higher-value segments, namely proteins, concentrates, and isolates, are projected to register a stronger growth trajectory, with an estimated CAGR of 5.85%, as they gain traction in premium applications such as sports nutrition and dairy alternatives that require protein concentrations of 80% and above. Growth in protein derivatives is expected to align closely with ongoing capital investments in advanced processing technologies, including wet extraction and ultrafiltration, which enhance purity, solubility, and overall performance characteristics. Early-stage momentum is exemplified by innovations such as VITESSENCE Pea 200 D from Ingredion Incorporated, where reduced particle size distribution contributes to improved dispersion and lower sedimentation in powdered beverage applications.

By Source: Peas Lead, Chickpeas Accelerate on Functionality

Peas commanded 34.70% of source-type share in 2025, reflecting decades of agronomic optimization, processing infrastructure, and regulatory acceptance in North America and Europe. Chickpeas are forecast to grow at 5.60% CAGR through 2031, driven by superior emulsification properties, neutral-to-mild flavor profiles, and rising adoption in Mediterranean and Middle Eastern cuisine applications such as hummus, dairy alternatives, and plant-based protein products. The pulse ingredients market size contribution from chickpea concentrates is poised to climb as FDA GRAS clearance (GRN 1098) enables inclusion up to 90% in diverse categories. Diverse source portfolios hedge agronomic risk and help processors address allergen and sustainability preferences, solidifying peas’ leadership while creating headroom for chickpeas and faba beans to expand pulse ingredients market share.

By Application: Animal Feed Outpaces Food as Aquaculture Scales

Food and beverages absorbed 63.80% of demand in 2025, spanning dairy alternatives, meat analogs, bakery, snacks, beverages, and fortified products where pulse proteins and flours deliver protein density, fiber content, and clean-label credentials. Animal feed is accelerating at 6.05% CAGR through 2031, driven by aquaculture and poultry producers replacing fishmeal and soy with pulse proteins to lower feed costs, meet sustainability benchmarks, and mitigate supply-chain risk. Pulse proteins in aquaculture diets improve feed conversion ratios, reduce nitrogen excretion, and support gut health in shrimp and finfish, with field trials demonstrating performance comparable to fishmeal at lower cost. Dairy alternatives are a key growth driver, with pea and chickpea proteins replacing soy and almond in milk, yogurt, cheese, and frozen desserts to capture flexitarian and vegan consumers. Meat analogs are adopting textured pulse proteins to improve juiciness, texture, and protein density, with dsm-firmenich's Vertis TVP pea proteins integrating taste-modulation technology to reduce beany off-notes and simplify ingredient decks

Geography Analysis

Asia-Pacific captured 39.10% of global revenue in 2025 and is forecast to grow at 6.70% CAGR through 2031, outpacing all other regions as China, India, and Japan scale domestic pulse processing capacity and regulatory frameworks for novel plant proteins mature. China is expanding industrial-scale pulse ingredient production to serve domestic food processing and export markets, with government support for agricultural modernization and protein self-sufficiency driving investment in fractionation infrastructure. India combines extensive pulse cultivation with rising urban protein demand, positioning the country as both a major producer and consumer of pulse ingredients, with domestic processors targeting bakery, snacks, and dairy alternatives for middle-class consumers. Japan is demanding precision, high-quality pulse derivatives for ready-to-eat and nutritional foods, with strict pesticide residue limits and allergen labeling requirements creating barriers to entry but also premium pricing opportunities for compliant suppliers.

North America held the second-largest share in 2025, driven by mature food processing infrastructure, high plant-protein demand, and favorable regulatory frameworks, including FDA GRAS determinations for pea, chickpea, and faba bean proteins. Roquette doubled its Manitoba facility's pea protein capacity to 125,000 tonnes per year in 2024, reflecting North American demand for high-purity isolates in sports nutrition and clinical nutrition applications.

Europe is navigating regulatory complexity, with the EU omnibus regulation on food and feed safety tightening maximum residue levels to 0.01 mg/kg for many active substances and mandating a 50% increase in import controls, compelling exporters to invest in plot-level traceability and pesticide-residue management.

South America, led by Brazil, Argentina, and Chile, is expanding pulse cultivation and processing to serve domestic markets and export to North America and Europe, with domestic agricultural output and export-focused processing creating growth opportunities. The Middle East and Africa are emerging markets with rising pulse ingredient demand driven by population growth, urbanization, and government initiatives to improve food security and nutrition, though infrastructure gaps and regulatory fragmentation constrain near-term growth.

Competitive Landscape

The pulse ingredients market exhibits a moderately consolidated structure, with the top five players accounting a major revenue. Ingredion Incorporated continues to strengthen its leadership position through capacity expansion at its Nebraska facility, coupled with the integration of localized innovation centers focused on optimizing beverage-grade protein isolates. Roquette Frères is advancing its Nutralys portfolio via proprietary debittering technologies for fava-based proteins, enabling deeper penetration into high-protein dairy alternative segments. Meanwhile, Archer Daniels Midland Company is leveraging its origination capabilities to deliver fully traceable supply chains, particularly for European infant nutrition applications.

Emerging players such as Puris and Sunnydale Foods are differentiating through proprietary low-energy extraction technologies, targeting niche, high-growth segments including sports nutrition and aquaculture.

Strategic activity across the sector is increasingly oriented toward vertical integration and value-chain expansion. In 2024, Roquette Frères raised approximately EUR 600 million in senior notes to support the acquisition of IFF’s Pharma Solutions business, combining excipient capabilities with plant-based protein platforms. BENEO GmbH’s EUR 50 million investment in a faba bean processing facility highlights a strategic focus on regionalized sourcing, while DSM-Firmenich is expanding its footprint in Italy to integrate flavor systems with pulse protein carriers, addressing persistent formulation challenges around taste masking.

In Parallel, equipment and technology partnerships are gaining importance. Collaborations such as ProteinDistillery’s agreement with NETZSCH Group to enhance micro wet-milling processes are improving emulsion stability and product performance. Collectively, these developments underscore a shift toward process innovation and differentiated capabilities, rather than scale alone, as key drivers of competitive advantage in the evolving pulse ingredients market.

Pulse Ingredients Industry Leaders

-

Ingredion Incorporated

-

Roquette Frères S.A.

-

AGT Food and Ingredients Inc.

-

Cargill, Incorporated

-

Archer-Daniels-Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ingredion Incorporated expanded its pulse-derived ingredient lineup by launching new pulse fiber blends designed for gut health and clean-label food formulations. These fibers are targeted for applications in baked goods, snacks, and nutritional bars, offering improved textural benefits and prebiotic functionality.

- April 2025: BENEO inaugurated a EUR 50 million pulse-processing plant in Germany to produce high-quality, plant-based ingredients from locally sourced faba beans for food and feed applications.

- August 2024: Archer Daniels Midland entered into a strategic partnership with Pulse Canada focused on integrating cutting-edge pulse extraction and processing technologies. This partnership aimed to increase production efficiency and reduce waste by maximizing the yield and purity of pulse proteins and starches.

- January 2024: AGT Food and Ingredients unveiled a new proprietary processing technology that improves the texture, solubility, and overall functional properties of pulse-based ingredients, such as pulse protein isolates and flours. This technology enables their pulse ingredients to be used more flexibly across various food applications, including bakery, meat alternatives, dairy substitutes, and beverages.

Global Pulse Ingredients Market Report Scope

Pulse ingredients are value-added food components derived from pulses, edible dry seeds of leguminous crops such as peas, chickpeas, lentils, and beans. These ingredients are produced through mechanical or biochemical processing methods (e.g., milling, fractionation, or protein extraction) to isolate or enhance specific functional and nutritional properties.

The global pulse ingredients market is evaluated across multiple key dimensions, including ingredient type, source, application, and geography. By ingredient type, the market is segmented into pulse flours, starches, proteins, and fibers. Based on the source, it encompasses lentils, peas, beans, chickpeas, and others. In terms of application, the market is categorized into food and beverages, animal feed, and other end uses. Geographically, the analysis covers major regions such as North America, Europe, Asia-Pacific, South America and Middle East, and Africa. Market size and forecasts for each segment are presented in terms of both value (USD million) and volume (tons), enabling a comprehensive assessment of market dynamics.

| Pulse Flours |

| Pulse Starch |

| Pulse Proteins |

| Pulse Fibers |

| Lentils |

| Peas |

| Beans |

| Chickpeas |

| Others |

| Food and Beverages | Bakery and Confectionery |

| Dairy and Dairy Alternatives | |

| Snack Foods | |

| Meat Analogues | |

| Beverages | |

| Others | |

| Dietary Supplements | |

| Animal Feed | |

| Pharmaceuticals | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Italy | |

| Sweden | |

| Norway | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Ingredient Type | Pulse Flours | |

| Pulse Starch | ||

| Pulse Proteins | ||

| Pulse Fibers | ||

| By Source | Lentils | |

| Peas | ||

| Beans | ||

| Chickpeas | ||

| Others | ||

| By Application | Food and Beverages | Bakery and Confectionery |

| Dairy and Dairy Alternatives | ||

| Snack Foods | ||

| Meat Analogues | ||

| Beverages | ||

| Others | ||

| Dietary Supplements | ||

| Animal Feed | ||

| Pharmaceuticals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Norway | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of pulse ingredients?

The pulse ingredients market is valued at USD 25.48 billion in 2025 and is expected to reach USD 34.30 billion by 2031.

Which ingredient type is growing fastest?

Pulse proteins are forecast to rise at a 5.85% CAGR through 2031 thanks to purity improvements and neutral flavor profiles.

Why does Asia-Pacific hold the largest share?

The region combines extensive pulse cultivation with modern processing plants, securing 39.10% of 2025 revenue and a 6.70% CAGR outlook.

How are pulse ingredients used in animal nutrition?

Inclusion rates of up to 30% in poultry and aquaculture diets replace fishmeal or soy while maintaining growth performance.

What are the main sensory challenges?

Residual beany flavors and grittiness limit usage in clear beverages and premium dairy alternatives, though enzymatic treatments are improving profiles.

Page last updated on: