Nutraceutical Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 116.36 Billion |

| Market Size (2031) | USD 152.32 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nutraceutical Ingredients Market Analysis by Mordor Intelligence

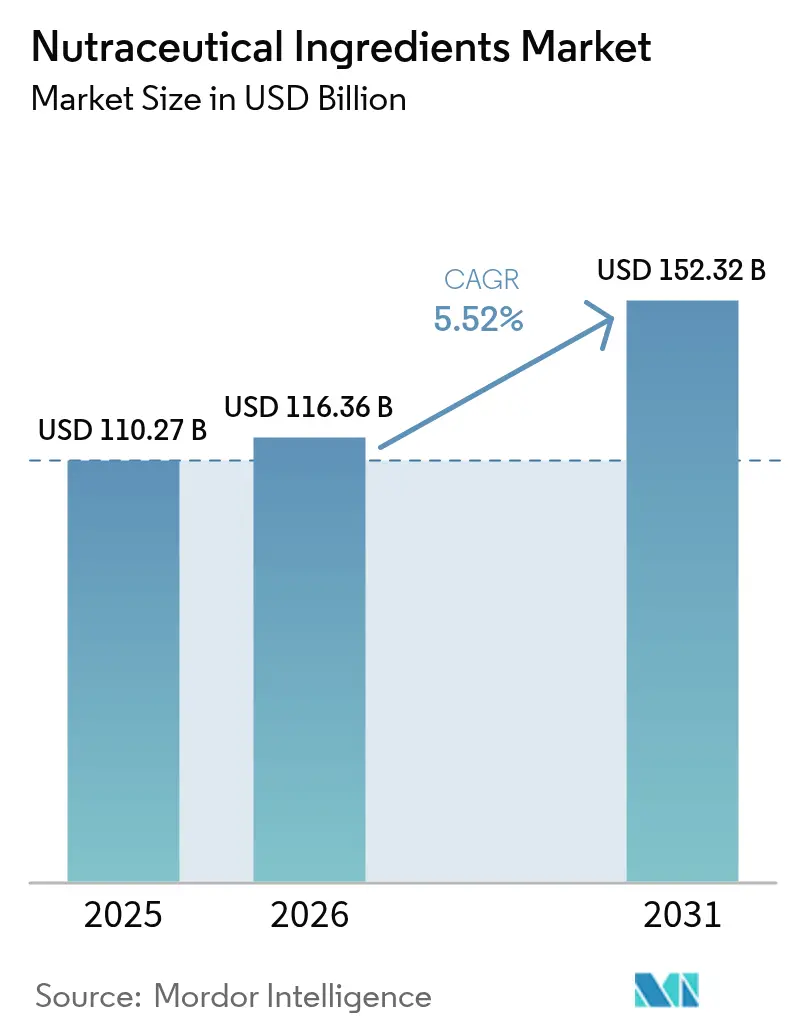

The nutraceutical ingredients market size is expected to grow from USD 110.27 billion in 2025 to USD 116.36 billion in 2026 and is forecast to reach USD 152.32 billion by 2031 at 5.52% CAGR over 2026-2031. This growth highlights a significant consumer preference for foods that provide specific health benefits. Key areas of focus include improving immunity, maintaining digestive health, and enhancing cognitive functions. The increasing emphasis on preventive nutrition, advancements in micro-encapsulation technologies, and the development of clean-label extraction methods are driving this demand. Additionally, the consistent introduction of ready-to-drink nutraceutical products is contributing to market expansion across various regions. Research and development efforts are intensifying, particularly in improving bioavailability and mainstreaming plant-based proteins. Furthermore, the incorporation of nutraceutical science into everyday food categories is broadening the consumer base, making these products more accessible to a wider audience. However, stricter regulatory requirements for evidence-based claims are prompting manufacturers to invest in clinical validation. This trend is raising technical barriers to entry, especially for smaller players, as the market becomes increasingly competitive.

Key Report Takeaways

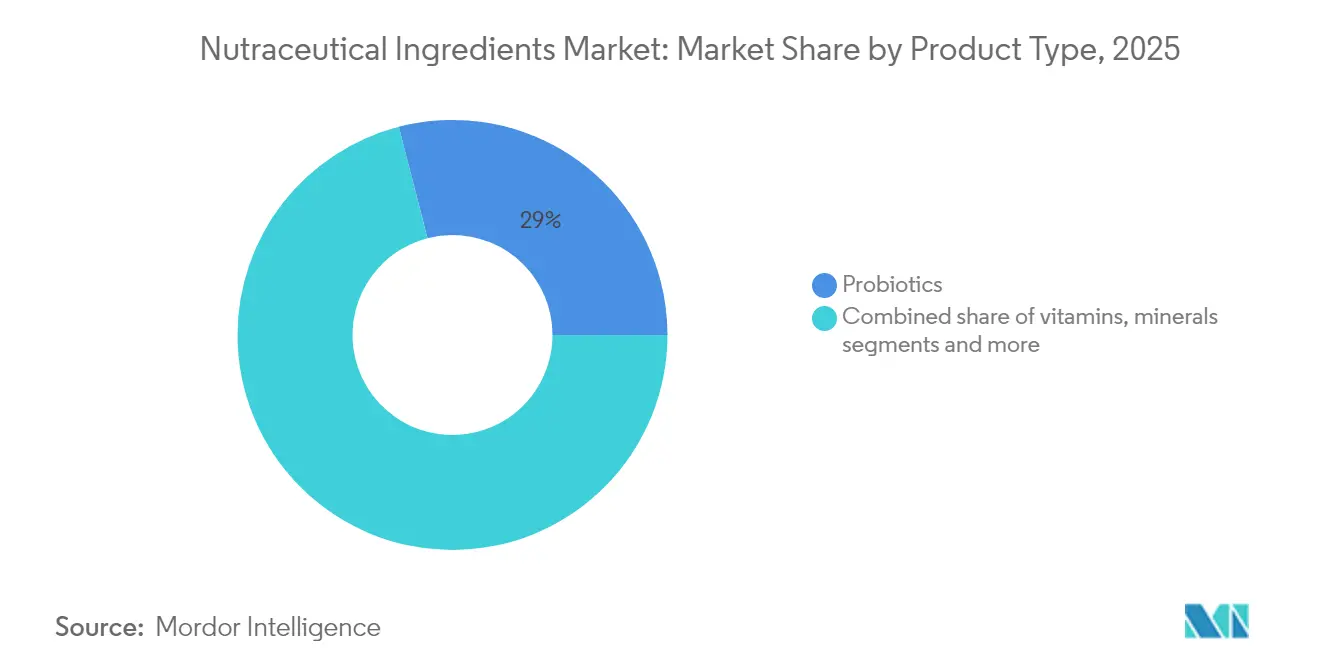

- By product type, probiotics led with 29.02% of the nutraceutical ingredients market share in 2025; omega-3 ingredients are projected to expand at a 9.12% CAGR to 2031.

- By form, powder formats commanded 67.13% share of the nutraceutical ingredients market size in 2025, while liquids are set to advance at an 8.27% CAGR through 2031.

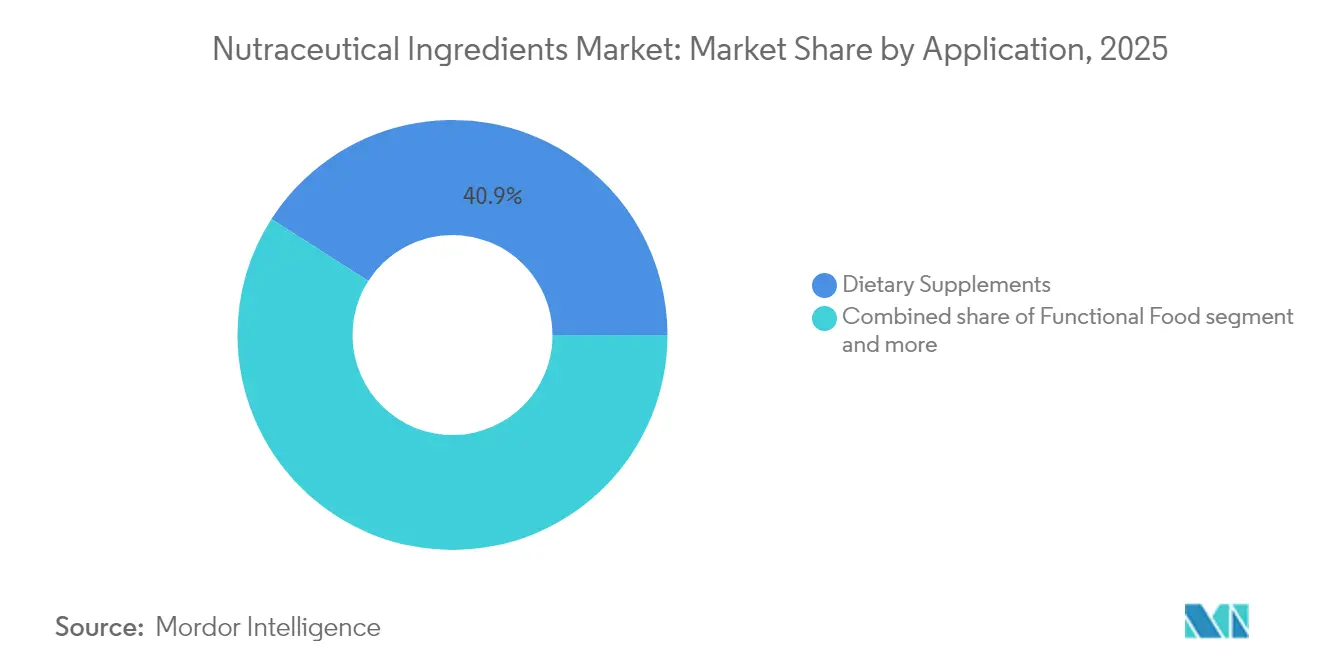

- By application, dietary supplements accounted for a 40.94% share of the nutraceutical ingredients market size in 2025, and functional beverages are forecast to grow at a 9.48% CAGR between 2026-2031.

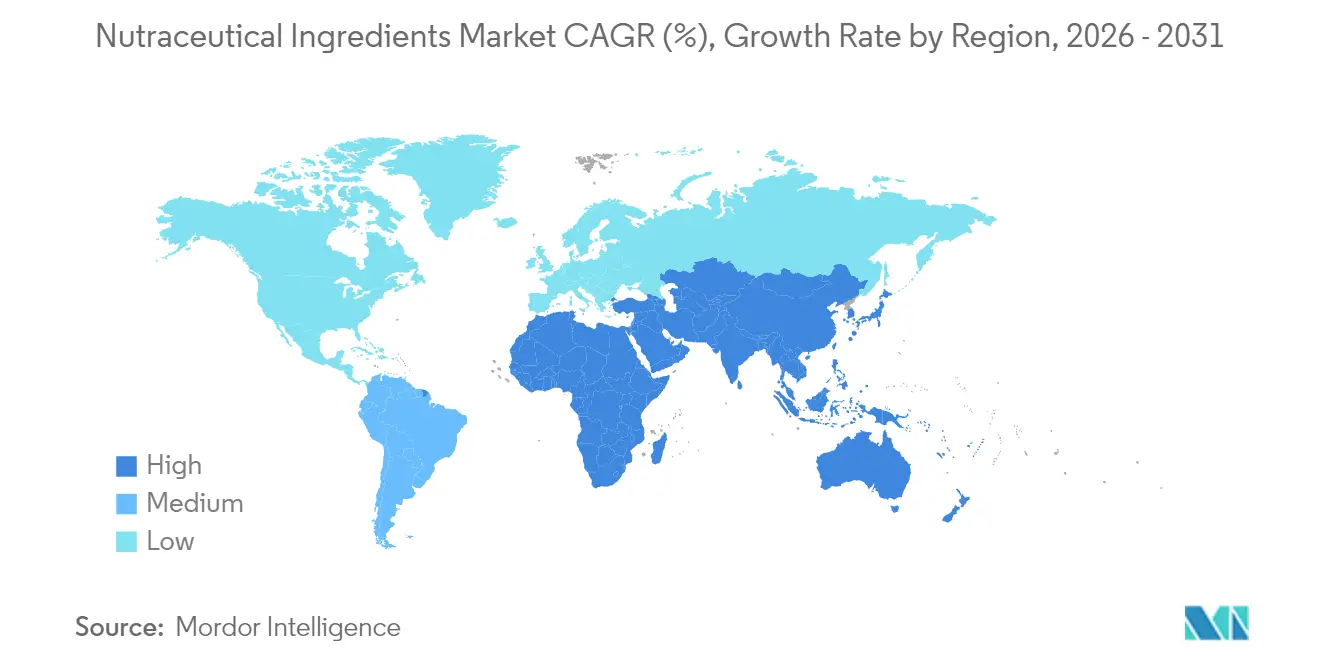

- By geography, Asia-Pacific held 35.79% revenue share in 2025; the Middle East and Africa region is expected to record the fastest CAGR of 9.31% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nutraceutical Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for preventive healthcare solution | +1.7% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| High demand for plant-based protein fortification | +1.2% | North America, Europe, with growing influence in Asia-Pacific | Medium term (2-4 years) |

| Probiotics-infused beverage gaining mainstream appeal | +0.9% | Global, with higher adoption in Asia-Pacific | Short term (≤ 2 years) |

| Adoption of omega-3s in mental and heart health regimens | +0.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Technological advancements in extraction and formulation | +0.6% | Global, with innovation centers in Europe and North America | Long term (≥ 4 years) |

| Growing demand for personalized nutrition solutions | +0.5% | North America, Europe, high-income Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging demand for preventive healthcare solution

The surging demand for preventive healthcare solutions is fueling the market growth. Governments and health organizations worldwide are increasingly promoting preventive healthcare to reduce the burden of chronic diseases. For instance, the World Health Organization (WHO) emphasizes the importance of nutrition in preventing non-communicable diseases (NCDs) such as diabetes and cardiovascular conditions. According to the WHO, NCDs account for 74% of all global deaths, highlighting the critical need for preventive measures [1]Source: World Health Organization, "Noncommunicable Diseases Report- December 2024", who.int. Similarly, the United States Department of Agriculture (USDA) and the Food and Drug Administration (FDA) have implemented guidelines and regulations to encourage the consumption of fortified foods and dietary supplements. Additionally, initiatives like India's National Nutrition Mission (POSHAN Abhiyaan) aim to improve nutritional outcomes, further boosting the demand for nutraceutical ingredients. The European Food Safety Authority (EFSA) also plays a pivotal role in regulating health claims on food products, ensuring consumer trust and driving market growth. These efforts underscore the growing recognition of preventive healthcare as a critical component of public health strategies, further propelling the nutraceutical ingredients market.

High demand for plant-based protein fortification

The increasing demand for plant-based protein fortification is a key driver of the market. According to the Food and Agriculture Organization (FAO), plant-based proteins are gaining popularity due to their health benefits, sustainability, and lower environmental impact compared to animal-based proteins. Additionally, the Plant Based Foods Association (PBFA) reported a 27% growth in plant-based food sales in the United States in 2023, highlighting the rising consumer preference for such products [2]Source: Plant-Based Foods Association, "Plant-Based Foods Association Report 2023", plantbasedfoods.org. Governments worldwide are also actively promoting plant-based diets to address environmental concerns, reduce greenhouse gas emissions, and improve public health. The European Union has introduced initiatives under its Farm to Fork Strategy, which supports the transition to sustainable food systems, including the promotion of plant-based alternatives. Furthermore, the Indian government has launched programs to support the production of plant-based proteins, aligning with its focus on sustainable agriculture and nutrition security. These factors collectively contribute to the growing adoption of plant-based protein fortification in the nutraceutical industry, as manufacturers increasingly incorporate these ingredients to meet evolving consumer demands and regulatory guidelines.

Probiotics-infused beverage gaining mainstream appeal

The increasing popularity of probiotics-infused beverages is a significant driver of the market. For instance, the World Health Organization and the Food and Agriculture Organization have emphasized the health benefits of probiotics in improving gut health, reducing the risk of gastrointestinal disorders, and enhancing immunity. According to the International Probiotics Association (IPA), the global probiotics market has witnessed consistent growth, with probiotics-infused beverages emerging as a key segment due to their convenience and health benefits. Furthermore, the United States Food and Drug Administration (FDA) has been actively regulating and approving probiotics-based products, ensuring their safety and efficacy, which has boosted consumer confidence [3]Source: U.S. Food and Drug Administration, "FDA Raises Concerns About Probiotic Products Sold for Use in Hospitalized Preterm Infants", fda.gov. These efforts, combined with increasing consumer awareness and scientific backing, are driving the demand for probiotics-infused beverages, solidifying their position as a mainstream choice among health-conscious individuals.

Adoption of omega-3s in mental and heart health regimens

The adoption of omega-3 fatty acids is increasingly recognized as a significant driver in the market. Governments and health organizations worldwide are emphasizing the inclusion of omega-3s in dietary guidelines due to their proven benefits for mental and heart health. For instance, the American Heart Association (AHA) recommends the consumption of omega-3-rich foods, such as fish, at least twice a week to support cardiovascular health [4]Source: American Heart Association, "Fish and Omega-3 Fatty Acids", heart.org. Similarly, the National Institutes of Health (NIH) highlights the role of omega-3s in reducing symptoms of depression and anxiety, further underlining their importance in mental health regimens. Additionally, initiatives like the European Commission's funding for research on omega-3s and their health benefits demonstrate the growing institutional support for these nutrients. Such endorsements and research-backed findings are driving consumer awareness and demand, thereby bolstering the growth of the nutraceutical ingredients market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex supply chain for bioactive ingredients | -0.7% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Allergen risks in protein and amino acid products | -0.5% | Global, with stricter regulations in North America and Europe | Short term (≤ 2 years) |

| Quality variation in omega-3 sourcing | -0.3% | Global, with particular impact on marine-sourced products | Medium term (2-4 years) |

| High cost of premium ingredients | -0.9% | Global, with stronger effect in price-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex supply chain for bioactive ingredients

The complex supply chain for bioactive ingredients acts as a significant restraint in the nutraceutical ingredients market. The production and distribution of these ingredients involve multiple stages, including sourcing raw materials, processing, quality control, and final delivery to manufacturers. Each stage requires stringent regulatory compliance, which increases operational challenges and costs. Additionally, the reliance on diverse suppliers and the need for consistent quality further complicate the supply chain. The sourcing of raw materials, often from geographically dispersed regions, adds another layer of complexity due to varying regulations, logistical challenges, and potential supply disruptions. Furthermore, maintaining the bioactivity and efficacy of these ingredients during processing and transportation demands advanced technologies and specialized handling, which can escalate costs. These factors collectively hinder the seamless flow of bioactive ingredients, impacting the overall growth of the nutraceutical ingredients market. The intricate nature of the supply chain also limits the ability of smaller players to compete effectively, as they may lack the resources to navigate these challenges efficiently.

Allergen risks in protein and amino acid products

Allergen risks pose a significant restraint in the nutraceutical ingredients market, particularly in protein and amino acid products. These products often contain ingredients derived from common allergens such as soy, milk, eggs, and nuts, which can trigger adverse reactions in sensitive individuals. Addressing these risks is crucial for manufacturers to maintain consumer trust and expand their market presence in the nutraceutical ingredients sector. Furthermore, the growing demand for clean-label and allergen-free products has intensified the pressure on manufacturers to innovate and reformulate their offerings. This often requires sourcing alternative ingredients, which may not only increase production costs but also affect the taste, texture, and nutritional profile of the final product. The complexity of supply chains in the nutraceutical ingredients market further complicates the management of allergen risks, as cross-contamination can occur at various stages, from raw material procurement to final product packaging. Regulatory bodies across different regions have implemented strict guidelines for allergen labeling and traceability, which manufacturers must adhere to in order to avoid legal penalties and product recalls. These factors collectively hinder the growth potential of protein and amino acid products within the nutraceutical ingredients market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product type: Probiotics Lead While Omega-3s Accelerate

Probiotics seize 29.02% of the market share in 2025, solidifying their role as the linchpin of the nutraceutical ingredients arena. This stronghold is bolstered by growing scientific validation of the gut's pivotal role in overall health. Probiotics are now recognized not just for gut health, but as essential players in immune function, mental well-being, and metabolic balance. Manufacturers are shifting from broad gut health assertions to crafting strain-specific solutions, targeting diverse health issues from stress relief to athletic recovery. The increasing consumer awareness regarding the benefits of probiotics, coupled with advancements in research and development, is further driving the segment's growth.

On the rise, omega-3 ingredients are set to be the fastest-growing segment, boasting a projected CAGR of 9.12% from 2026-2031. Their surge is fueled by broadening applications, now spanning cognitive and joint health alongside traditional heart benefits. Owing to technological advancements in encapsulation, omega-3s are finding their way into food matrices once deemed challenging, broadening their application horizon. The vitamins and minerals segment continues to grow steadily, supported by the standardization of fortification across various food categories to combat nutritional deficiencies. Meanwhile, proteins and amino acids ride the wave of the fitness and active nutrition trend, as consumers increasingly prioritize muscle health and recovery. Prebiotics are emerging as valuable partners to probiotics, with new studies underscoring their enhanced effects when used together in formulations, creating synergistic benefits for gut health and overall well-being.

By Form: Powder Dominates While Liquid Formats Surge

Powders command a dominant 67.13% market share in the market in 2025, owing to their adaptability and enhanced stability. Recent advancements in particle engineering have improved powders' dissolution, flowability, and sensory traits, overcoming past consumer acceptance hurdles. Innovations in spray drying now allow manufacturers to safeguard sensitive ingredients, ensuring they're easily integrated into end products. Spanning a range of ingredient categories, from proteins and fibers to probiotics and botanical extracts, the powder segment underscores its pivotal role in product development. Its universal applicability across diverse nutraceutical formulations further solidifies its market leadership, as manufacturers continue to leverage its versatility to meet evolving consumer demands.

Meanwhile, liquids are on a rapid ascent, eyeing an 8.27% CAGR from 2026 to 2031, driven by a consumer shift towards ready-to-consume items and breakthroughs in liquid stability. Innovations in liquid formulations are addressing challenges such as ingredient separation, shelf-life, and nutrient degradation. These advancements enable manufacturers to deliver high-quality, convenient products that align with modern lifestyles while ensuring the retention of nutritional value and product integrity over time. The growing demand for functional beverages and liquid supplements further propels the segment's growth trajectory.

By Application: Dietary Supplements Maintain Lead While Beverages Surge

Dietary supplements command the largest application segment, holding a 40.94% market share in 2025. Their success stems from a concentrated delivery of functional ingredients and a strong consumer acceptance, which has been built over years of consistent usage and trust among consumers. This dominance is especially pronounced in North America and Europe, where supplements are deeply embedded in health and wellness routines. The supplement category is witnessing a surge in innovation, expanding from traditional pills to more diverse formats like gummies, powders, and liquid shots. These new formats not only cater to consumers' desires for convenience but also enhance the overall consumption experience, making them more appealing to a broader audience, including younger demographics.

Functional beverages are on the rise, emerging as the fastest-growing application segment. With a projected CAGR of 9.48% from 2026-2031, their growth is fueled by their easy integration into daily routines, such as replacing traditional drinks with healthier alternatives. This category is undergoing a wave of innovation, with manufacturers crafting beverages that offer multiple functional benefits, such as energy boosting, immunity support, and stress relief, while maintaining appealing taste profiles. The ability to combine health benefits with enjoyable flavors is driving their popularity among health-conscious consumers and those seeking convenient, on-the-go solutions.

Geography Analysis

In 2025, the Asia-Pacific region solidifies its status as the leading market for nutraceutical ingredients, commanding a 35.79% share. This dominance is a result of blending age-old wellness traditions with contemporary nutritional science. While Japan and China anchor this leadership with their culturally ingrained nutraceutical ingredients, emerging markets like India and Indonesia are rapidly bolstering the region's stature. Factors such as urbanization, rising disposable incomes, and heightened health awareness, especially among the youth, fuel this growth. Notably, there's a surge in innovation, with traditional Asian botanicals being modernized for contemporary uses. The beverage sector thrives, with energy drinks and functional waters becoming favorites among urban professionals.

The Middle East and Africa are on the fast track, eyeing a robust CAGR of 9.31% from 2026-2031. This growth, especially pronounced in the United Arab Emirates, Saudi Arabia, and South Africa, is spurred by a blend of expatriate demand and escalating chronic disease rates. As consumers become more health-conscious and premium products become more accessible, the region's nutraceutical ingredients market is rapidly evolving. Manufacturers are responding strategically, as demonstrated by DSM-Firmenich's announcement of a new premix and additives plant in Sadat City, scheduled for September 2024. This highlights Egypt's potential in the region. Also, beauty-focused nutraceutical ingredients are gaining momentum, especially in Turkey, Morocco, and the GCC, highlighting a rising consumer interest in the link between nutrition and aesthetics. While the region's regulatory landscape is adapting to this growth, aligning standards across its diverse nations poses a challenge.

North America and Europe remain pivotal players in the nutraceutical ingredients arena. Both regions are characterized by advanced regulatory frameworks that ensure product safety and efficacy, fostering consumer trust. High levels of health awareness among consumers drive demand for innovative and premium nutraceutical products. Additionally, these regions benefit from well-established research and development ecosystems, enabling the continuous introduction of cutting-edge products. The growing focus on personalized nutrition and the increasing adoption of plant-based and clean-label ingredients further strengthen the market in these regions. Strategic collaborations between manufacturers and research institutions are also contributing to sustained growth and innovation.

Competitive Landscape

The Global Nutraceutical Ingredients Market demonstrates a moderately fragmented competitive landscape. This score reflects a dynamic environment where both established corporations and emerging startups actively compete for market share. Leading companies such as Cargill, ADM, and DSM-Firmenich dominate the market by leveraging their extensive ingredient portfolios and robust global distribution networks. These players capitalize on their scale, operational efficiency, and global reach to maintain a strong foothold. On the other hand, smaller, specialized firms focus on innovation and expertise in niche ingredient categories, such as plant-based proteins, probiotics, and omega-3 fatty acids, to secure premium positions. This dual dynamic fosters healthy competition, drives innovation, and ensures a diverse range of offerings for end-users across the nutraceutical industry.

The competitive landscape is further shaped by significant mergers and acquisitions (M&A) activity, which has become a key strategy for market players to strengthen their positions. Companies are increasingly pursuing vertical integration strategies to secure raw material supplies, reduce dependency on third-party suppliers, and enhance supply chain resilience. Simultaneously, horizontal expansion efforts are gaining momentum as firms diversify their product portfolios to cater to evolving consumer demands for functional and health-focused ingredients. For instance, the rising consumer preference for clean-label and sustainable products has prompted companies to invest in plant-based and organic ingredient categories. These strategic moves not only enhance operational efficiency but also enable companies to expand their market presence and address emerging trends. The ongoing consolidation trend underscores the importance of scale, specialization, and adaptability in maintaining a competitive edge in this rapidly evolving market.

A surge in specialty ingredient acquisitions is anticipated as companies strive to enhance their competitive positioning and address the growing consumer focus on health and wellness. This "frenzy" of acquisitions is expected to reshape the market, creating opportunities for both established players and new entrants. Additionally, advancements in technology, such as precision fermentation and bioengineering, are likely to play a pivotal role in driving innovation and differentiation in the market. As the nutraceutical ingredients market continues to evolve, companies that prioritize strategic partnerships, research and development investments, and adaptability to consumer trends will likely emerge as leaders, setting the stage for sustained growth and innovation in the forecast period.

Nutraceutical Ingredients Industry Leaders

-

BASF SE

-

Archer Daniels Midland Company

-

International Flavors & Fragrances, Inc

-

Cargill, Incorporated

-

DSM- Firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Ajinomoto Co has teamed up with LabCentral, backing biotech startups that specialize in amino acids and protein sciences. This alliance not only amplifies innovation in nutraceutical ingredients, especially those derived from amino acids, but also empowers Ajinomoto to steer developments in health and wellness applications.

- November 2024: Balchem, a manufacturer of specialty ingredients, has unveiled its latest offering: Vital Trio, a three-in-one formula. This innovative formula boasts K2Vital Delta, a double-microencapsulated ingredient featuring 99.7% all-trans vitamin K2 MK-7. Complementing this are Albion Minerals’ chelated magnesium bisglycinate and vitamin D3, all aimed at promoting immune, cardiovascular, and bone health.

- July 2024: Kaneka launched its Naturally Smart Probiotic line, Floradapt. The company also announced a USD 150,000 product giveaway as a part of its Innovation Awards program. According to the company, it provides highly efficacious effects for various stages of life. Floradapt has an extensive bank of over 1,000 acid-resistant clinical probiotic strains for targeted health conditions, including Cardio, Intensive Gastrointestinal (GI), Digestive, and Oral Health.

- May 2024: Kerry launched a digital innovation hub, positioning it as a comprehensive resource for supplement consumers. This hub offers insights into consumer preferences, covering categories such as gummies and functional beverages. Additionally, it showcases proprietary global research on supplement preferences and key health platforms.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the nutraceutical ingredients market as the total manufacturer-level sales of bioactive compounds, including probiotics, prebiotics, proteins, amino acids, omega-3 lipids, vitamins, minerals, and botanical extracts, supplied to food, beverage, supplement, feed, and personal-care formulators worldwide. We capture value at the first commercial transfer of the ingredient, before any further blending or retail conversion.

Scope Exclusion: Pharmaceutical-grade active pharmaceutical ingredients and finished consumer nutraceutical products fall outside this assessment.

Segmentation Overview

-

By Type

- Prebiotics

- Probiotics

- Vitamin

- Mineral

- Proteins and Amino Acids

- Omega-3 Ingredients

- Others

-

By Form

- Powder

- Liquid

-

By Appilcation

- Functional Food

- Functional Beverage

- Dietary Supplements

- Animal Nutrition

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts held structured discussions with formulation scientists, ingredient distributors, contract manufacturers, and food-safety officials across North America, Europe, and Asia-Pacific. These interviews clarified inclusion rates, emerging demand for synbiotic blends, and live price movements that refined our desk inputs.

Desk Research

We assembled baseline volumes and prices from open datasets such as FAOSTAT, USDA GAIN, UN Comtrade, EFSA novel-food opinions, and WHO nutrition tables; these sources anchor regional production, trade, and regulatory uptake. Annual reports and investor decks, mined via D&B Hoovers, plus real-time news on Dow Jones Factiva, allowed us to cross-check corporate revenue trails against macro totals. The sources listed are illustrative; many additional public references informed data collection and verification.

Market-Sizing & Forecasting

A top-down model reconstructs ingredient demand from functional food, beverage, supplement, and feed output using penetration rates, average inclusion levels, and prevailing prices. Supplier roll-ups and channel checks provide selective bottom-up validation, reconciling gaps. Key variables like global fish-oil price indices, probiotic CFU capacity, per-capita supplement spend, novel-food approvals, and plant-protein extrusion capacity feed a multivariate regression supported by ARIMA for short-term shocks. Region-weighted averages bridge sparse bottom-up data, and every adjustment is logged for audit.

Data Validation & Update Cycle

Outputs pass a two-step analyst review where anomalies versus historical series or peer signals are flagged, re-tested, and approved. Reports refresh annually, with interim updates triggered by material events such as major regulatory shifts or capacity expansions. A final pre-delivery sweep ensures clients receive the latest vetted view.

Why Mordor's Nutraceutical Ingredients Baseline Inspires Confidence

Published estimates for 2024 span USD 88 billion to USD 105 billion, yet figures diverge because providers vary ingredient scope, price assumptions, and refresh cadence. By transparently disclosing inclusions, variables, and update rhythm, we give decision-makers a baseline they can trace and replicate.

Key Gap Drivers: Several studies omit personal-care and feed usage, depressing totals. Others back-calculate from finished supplement sales, inflating numbers. Static price decks and multiyear refresh gaps widen spreads further.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 110.27 B (2025) | Mordor Intelligence | |

| USD 105.15 B (2024) | Global Consultancy A | Excludes personal-care and feed channels; 2022 price baseline |

| USD 87.76 B (2024) | Global Consultancy B | Infers value from finished product rebates, leading to conservative totals |

These contrasts show how Mordor's disciplined scoping, live price tracking, and yearly refresh cycle create a balanced, transparent baseline that end-users can rely on.

Key Questions Answered in the Report

What is the current size of the nutraceutical ingredients market?

The market is valued at USD 116.36 billion in 2026 and is projected to reach USD 152.32 billion by 2031, growing at a 5.52% CAGR.

Which product segment holds the largest functional food ingredients market share?

Probiotics lead with 29.02% revenue share in 2025, reflecting strong consumer interest in gut-health solutions.

Which application is expanding fastest?

Functional beverages are forecast to grow at a 9.48% CAGR between 2026-2031 as consumers seek health benefits in everyday drinks.

Why are powder formats dominant?

Powders account for 67.13% of demand owinf to superior stability and versatility across bakery, beverage and supplement applications.

Page last updated on: