North America Lipid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

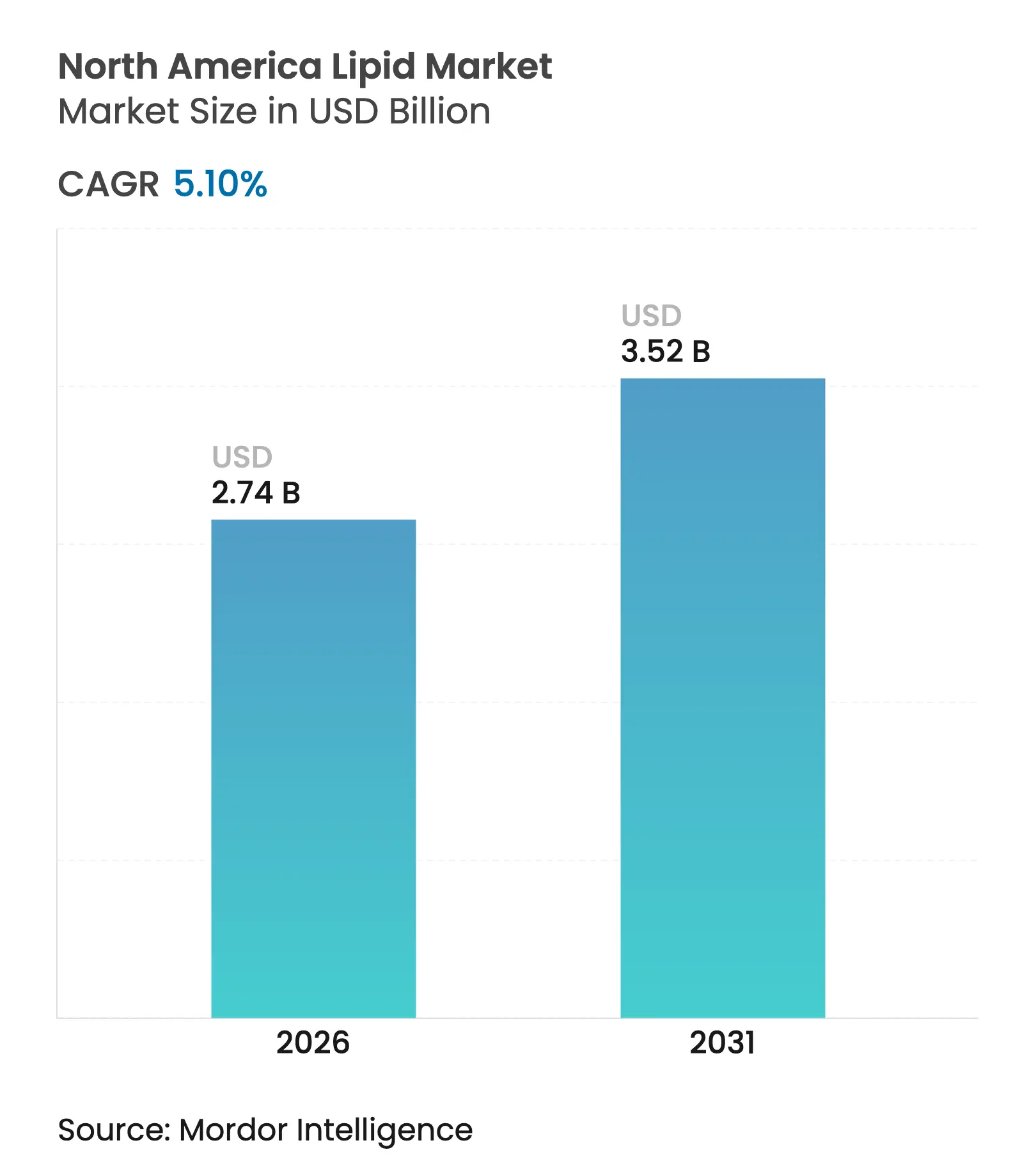

| Market Size (2026) | USD 2.74 Billion |

| Market Size (2031) | USD 3.52 Billion |

| Growth Rate (2026 - 2031) | 5.10 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

North America Lipid Market Analysis by Mordor Intelligence

The North American lipid market size was valued at USD 2.61 billion in 2025 and estimated to grow from USD 2.74 billion in 2026 to reach USD 3.52 billion by 2031, at a CAGR of 5.10% during the forecast period (2026-2031). The market expansion is driven by increased lipid usage across various industries. Growth is supported by advancements in lipid applications, changing consumer preferences, improvements in lipid delivery systems, and supportive regulatory frameworks for health-focused product development. Consumer awareness of functional lipids' health benefits, including omega-3 fatty acids, medium-chain triglycerides (MCTs), phytosterols, and phospholipids, contributes significantly to market growth. The market is also experiencing increased adoption of plant-based and algae-derived lipid sources, aligned with sustainability initiatives and clean-label demands.

Key Report Takeaways

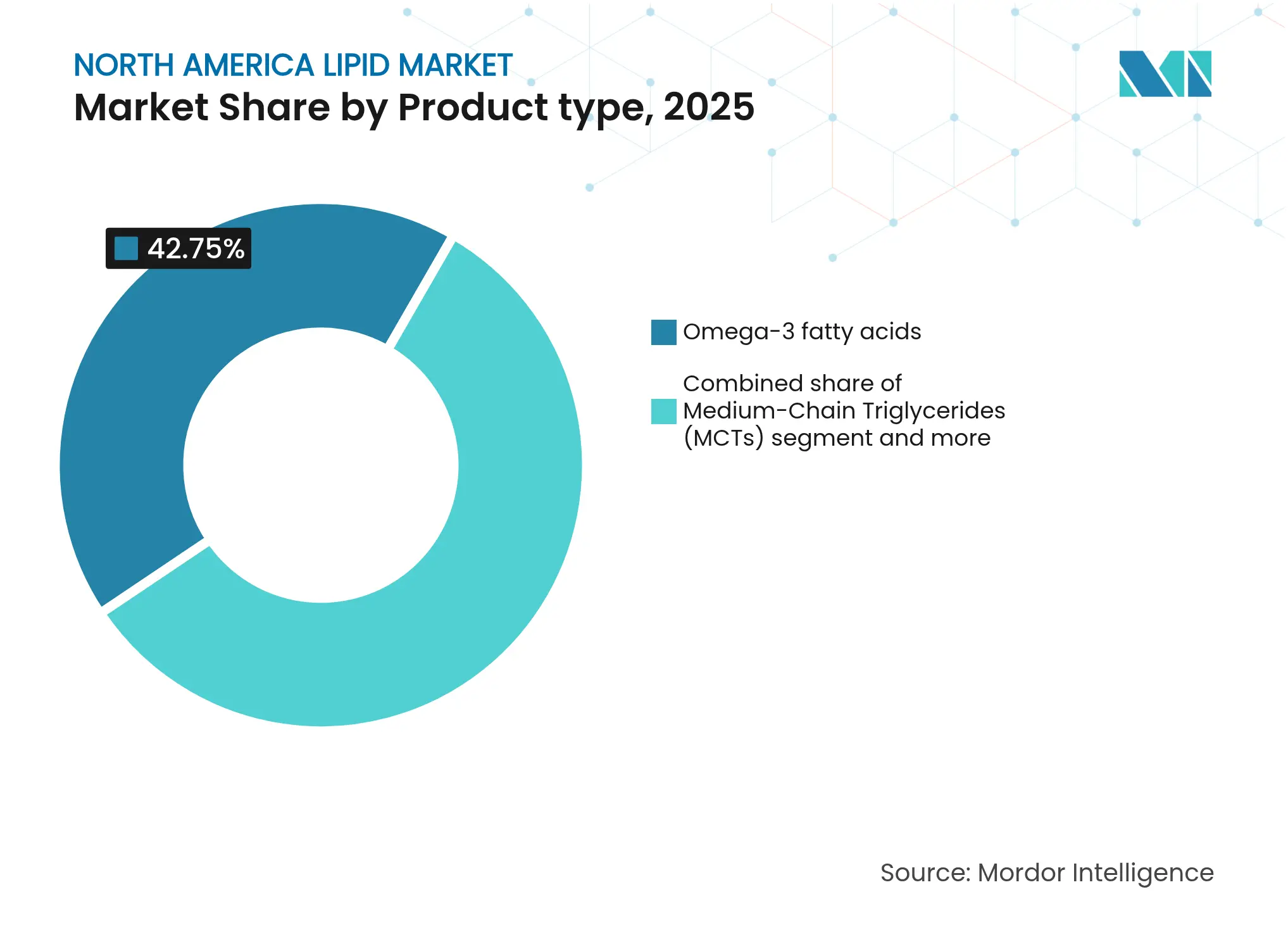

- By product type, omega-3 fatty acids led with 42.75% revenue share in 2025, while medium-chain triglycerides registered the fastest 6.55% CAGR to 2031.

- By source, plant-based inputs held 54.70% of the North America lipid market share in 2025 and are forecast to advance at 7.10% CAGR.

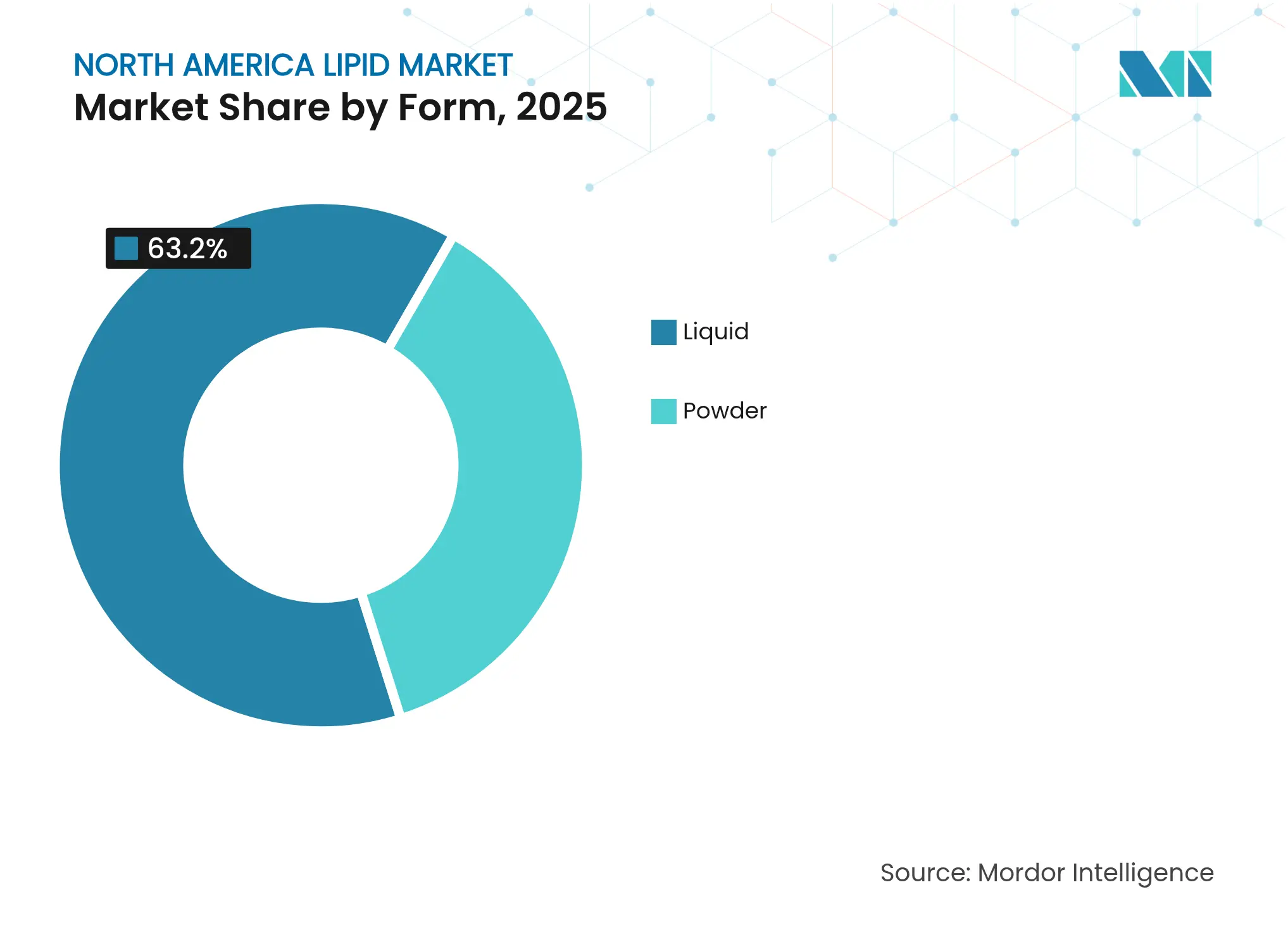

- By form, liquid formats commanded 63.20% share of the North America lipid market size in 2025; powder formats are projected to rise at 7.25% CAGR.

- By application, dietary supplements accounted for 45.20% share of the North America lipid market size in 2025; animal feed applications are expanding at 7.15% CAGR to 2031.

- By country, the United States represented 73.10% of 2025 revenue, while Canada is set to record a 6.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Lipid Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising popularity of fortified functional foods and beverages Rising popularity of fortified functional foods and beverages | +1.2% | North America, with strongest gains in United States and Canada | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:North America, with strongest gains in United States and Canada | Impact Timeline:Medium term (2-4 years) |

Expanding adoption of omega-3 and functional lipids in dietary supplements and nutraceuticals Expanding adoption of omega-3 and functional lipids in dietary supplements and nutraceuticals | +1.5% | Global, with North America leading premium segment adoption | Long term (≥ 4 years) | |||

Widening use of MCTs in weight management diets Widening use of MCTs in weight management diets | +0.8% | North America, particularly United States consumer markets | Short term (≤ 2 years) | |||

Growing demand for plant-based and algae-derived lipids Growing demand for plant-based and algae-derived lipids | +1.1% | North America and EU, with spillover to emerging markets | Long term (≥ 4 years) | |||

Pharmaceutical innovation using lipids in drug delivery systems Pharmaceutical innovation using lipids in drug delivery systems | +0.7% | North America, concentrated in biotech hubs | Medium term (2-4 years) | |||

Increasing investment in algae-based lipid production technologies Increasing investment in algae-based lipid production technologies | +0.9% | North America, with focus on United States Gulf Coast and Canada | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Popularity of Fortified Functional Foods and Beverages

The North American lipid market is experiencing growth due to increased demand for functional foods and beverages that contain health-promoting lipids. Consumers in the United States and Canada are becoming increasingly health-conscious, leading to a greater consumption of foods and beverages that offer specific health benefits, including improved heart health, enhanced cognitive performance, effective weight management, and anti-inflammatory properties. The Food and Drug Administration (FDA)'s new "healthy" food definition, effective February 2025, provides opportunities for lipid-fortified products by allowing higher levels of healthy fats while maintaining limits on added sugars and sodium [1]Source: Food and Drug Administration (FDA), "FDA Finalizes Updated “Healthy” Nutrient Content Claim", www.fda.gov. This regulatory change is expected to affect formulation strategies in the functional food industry. Moreover, Health Canada's approval of vitamin D fortification in yogurt and kefir responds to the needs of 19% of Canadians with vitamin D deficiency, demonstrating regulatory support for nutrition enhancement.

Expanding Adoption of Omega-3 and Functional Lipids in Dietary Supplements and Nutraceuticals

The North American lipid market is experiencing significant growth due to increased adoption of omega-3 and other functional lipids in dietary supplements and nutraceuticals. This expansion stems from consumers' growing health awareness and their search for preventive solutions to manage chronic conditions, including cardiovascular disease, cognitive decline, metabolic disorders, and inflammatory conditions. Manufacturers are incorporating various functional lipids - omega-3 fatty acids (EPA and DHA), medium-chain triglycerides (MCTs), phytosterols, and conjugated linoleic acid (CLA) - into nutraceutical products for their proven benefits in brain function support, cholesterol reduction, weight management, and energy metabolism enhancement. According to the Council for Responsible Nutrition (CRN), 74% of United States adults used dietary supplements in 2023 [2]Source: Council for Responsible Nutrition (CRN), "2023 CRN Consumer Survey on Dietary Supplements", www.crnusa.org. In response to this demand, manufacturers offer diverse lipid-based delivery formats, including softgels, gummies, powders, and emulsified liquids, targeting specific life stages and health needs such as prenatal care, aging, sports performance, and immune support.

Widening Use of MCTs in Weight Management Diets

Medium-chain triglycerides (MCTs) have distinct metabolic properties that promote fat oxidation and energy metabolism. Clinical studies indicate that MCTs reduce body weight and fat more effectively than long-chain triglycerides, particularly in individuals with specific health conditions. MCTs are rapidly absorbed and converted to energy, making them beneficial for managing obesity, malnutrition, and cognitive decline. They also support exercise performance and endurance improvement. Medium- and long-chain triacylglycerol (MLCT) formulations support weight management and lipid metabolism. These ingredients have received regulatory approval in several countries as healthy food ingredients, establishing their position in the functional lipid market. As consumers become more aware of ingredient processing methods, MCT manufacturers can highlight their natural sourcing and minimal processing practices.

Growing Demand for Plant-Based and Algae-Derived Lipids

The North American lipid market is experiencing transformation driven by increased demand for plant-based and algae-derived lipids. Environmental and health considerations are prompting consumers to choose plant-based alternatives like flaxseed oil, chia oil, sunflower lecithin, and algae-derived omega-3s (EPA/DHA) over traditional animal-based fats and marine-sourced lipids. These alternatives complement the increasing adoption of plant-based diets, personalized nutrition, and environmentally conscious consumption patterns. Government research and policies in North America support the expansion of plant-based and algae-derived lipids. The United States Department of Energy (DOE) estimates that microalgae cultivation in the United States has an annual potential of 152 million tons, with production costs averaging USD 674 per ton [3]Source: United States Department of Energy, "Microalgae, Macroalgae and Point-Source Carbon Dioxide Waste Streams", www.energy.gov. This assessment demonstrates the commercial viability of algae for both renewable energy and high-value biochemicals, including omega-3 fatty acids. The government's support aligns with broader initiatives to decrease reliance on marine resources and fossil fuels while promoting circular bioeconomies and alternative protein and lipid development.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatility in raw material prices Volatility in raw material prices | -0.9% | Global, with particular impact on North American processors | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.9% | Geographic Relevance:Global, with particular impact on North American processors | Impact Timeline:Short term (≤ 2 years) |

Stringent purity and safety regulations Stringent purity and safety regulations | -0.6% | North America, with varying compliance costs across regions | Medium term (2-4 years) | |||

Negative consumer perception of highly processed lipids Negative consumer perception of highly processed lipids | -0.4% | North America, concentrated in health-conscious demographics | Medium term (2-4 years) | |||

Limited algal fermentation infrastructure Limited algal fermentation infrastructure | -0.7% | North America, with capacity constraints in specialized facilities | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatility in Raw Material Prices

The vegetable oil market is experiencing significant changes as soyoil gains prominence due to palm oil reaching near-record price premiums. This shift creates price volatility that affects lipid manufacturers' cost structures and margin predictability. In North America, supply chain dynamics are shifting after the United States Customs and Border Protection ruled that Norwegian-origin omega-3-acid ethyl esters encapsulated in China do not qualify as substantially transformed products. The industry is adopting nutrient Fifo (nFifo) measurements to track omega-3 retention from wild fish to final products, supporting improved byproduct utilization and sustainability, though this may affect pricing structures. Archer Daniels Midland Company has implemented sustainability measures, achieving a 14.7% reduction in Scope 1+2 greenhouse gas emissions and expanding regenerative agriculture programs to 2.8 million acres, reflecting the industry's environmental commitment while managing associated costs.

Stringent Purity and Safety Regulations

Health Canada's modernization of regulations for special dietary foods and infant foods (Divisions 24 and 25 of the Food and Drug Regulations) aims to improve safety and nutritional standards while addressing global supply shortages. The Canadian Food Inspection Agency enforces specific labeling requirements for fats and oils, including accurate common names and ingredient declarations, with detailed rules for modified or hydrogenated oils. Mexico's NOM-051-SCFI/SSA1-2010 standard mandates front-of-package warning labels for products containing high levels of sugars, fats, or sodium, with non-compliance resulting in significant penalties. Canada's updated regulations on food additives and compositional standards streamline existing frameworks while eliminating redundancies. The regulatory differences between the United States dietary supplements (regulated as foods) and Canadian natural health products present compliance challenges for companies operating across both markets.

Segment Analysis

By Product Type: Omega-3 Dominance Faces MCT Disruption

Omega-3 fatty acids hold a 42.75% market share in 2025, maintaining their dominant position through established applications in cardiovascular health and cognitive function. Medium-chain triglycerides (MCTs) represent the fastest-growing segment with a 6.55% CAGR through 2031, driven by increasing demand in weight management and ketogenic diet applications. The omega-3 segment receives regulatory support, as the Food and Drug Administration (FDA)'s review of infant formula nutrient requirements may expand DHA and EPA requirements in early nutrition applications. Phospholipids and glycolipids find specialized uses in pharmaceutical drug delivery systems, where liposomal technology improves therapeutic efficacy through targeted delivery mechanisms.

MCTs offer distinct metabolic benefits through quick absorption and energy conversion, with clinical studies demonstrating notable weight reduction effects compared to long-chain triglycerides, especially in patients with metabolic disorders. The omega-3 segment faces supply constraints from limited marine sources. The "Others" category includes emerging lipid developments, such as structured lipids and specialty fatty acid derivatives used in industrial applications.

Note: Segment shares of all individual segments available upon report purchase

By Source: Plant-Based Revolution Accelerates

Plant-based sources hold a 54.70% market share in 2025 and are projected to grow at a 7.10% CAGR through 2031. This dominance stems from increasing consumer demand for sustainable and ethical lipid sources, particularly as concerns rise about the environmental impacts of marine harvesting. Marine-based sources experience sustainability challenges and supply limitations, while animal-based sources remain focused on specialized nutrition and pharmaceutical applications.

Technological advancements support this transition to plant-based alternatives. Corbion's AlgaVia platform employs microalgae cultivation with minimal resource requirements and renewable energy, providing traceable omega-3 sources for aquaculture applications. Marine sources maintain their position in premium applications requiring specific fatty acid profiles, despite supply chain instability. In agricultural innovation, Yield10 Bioscience has received USDA approval for genetically modified Camelina crops that produce 10% EPA and 10% DHA, demonstrating progress in plant-based omega-3 production.

By Form: Liquid Leadership Challenged by Powder Innovation

Liquid forms hold 63.20% market share in 2025 through established applications in food processing and direct supplementation. The powder formulations segment grows at 7.25% CAGR through 2031, supported by its stability, shelf life, and bioavailability advantages. Evonik's AvailOm omega-3 lysine complexes showcase powder innovation with 5 times higher bioavailability than traditional softgels and 4-year potency retention without additives. The powder segment offers formulation flexibility for various dosage forms and applications where liquid stability is challenging. Liquid forms remain dominant in bulk applications like food manufacturing and aquaculture feeds, where processing requirements favor liquid integration.

Nano-encapsulation technologies improve powder formulations by addressing oxidation issues and increasing bioavailability, with metal-organic framework nanoparticles showing potential for targeted delivery. The powder segment growth reflects consumer demand for convenient, stable supplementation formats that maintain potency during storage. Liquid forms maintain advantages in industrial applications requiring immediate solubility and processing compatibility, particularly in aquaculture feeds and food manufacturing. Spray-drying and microencapsulation technologies enable manufacturers to address traditional stability limitations while providing enhanced functionality in finished products.

Note: Segment shares of all individual segments available upon report purchase

By Application: Dietary Supplements Lead While Animal Feed Surges

Dietary supplements hold a 45.20% market share in 2025, driven by increased health awareness and regulatory frameworks supporting omega-3 health claims. Animal feed applications are expected to grow at a 7.15% CAGR through 2031, primarily due to aquaculture's shift toward sustainable lipid sources. The infant nutrition segment is expanding through regulatory updates, including Health Canada's proposed revisions to foods for special dietary use, which focus on safety, nutritional adequacy, and addressing supply shortages. In pharmaceuticals, lipid-based drug delivery systems are advancing, supported by the United States government.

The functional food and beverage segment is growing due to clean label trends and the FDA's updated "healthy" food definition that accommodates higher healthy fat content. The animal feed sector is adopting innovative approaches through algae-based omega-3 integration, exemplified by BioMar's Blue Impact feed program that combines cultivated algal oil, fish trimmings, and insect meal to decrease dependence on wild fish stocks. In infant nutrition, lipid developments focus on structured triglycerides, algae-derived DHA, and MFGM components to replicate breast milk fat composition and enhance cognitive and immune development.

Geography Analysis

The United States holds a 73.10% share of the North American lipid market in 2025, driven by pharmaceutical innovation, established dietary supplement distribution networks, and government investments in manufacturing capabilities. Lonza's USD 1.2 billion acquisition of Roche's Vacaville biologics site strengthens the country's large-scale manufacturing capacity for lipid-based therapeutics. The Food and Drug Administration (FDA)'s ongoing infant formula nutrient review process, with comments due September 2025, may expand omega-3 requirements in early nutrition products

Canada projects the highest regional growth rate at 6.75% CAGR through 2031, supported by favorable regulations and strategic marine lipid processing capabilities. Health Canada's approval of phosphatidylserine as a supplemental ingredient, with a 300 mg daily intake limit, demonstrates regulatory support for market expansion. The country's supplemented foods regulations framework balances safety and innovation through specific labeling requirements and cautionary statements.

Mexico offers developing opportunities in the North American lipid market. The Canadian Food Inspection Agency outlines export requirements for meat and poultry products to Mexico, including various by-products containing lipid components, with emphasis on proper labeling and documentation. The Rest of North America comprises smaller markets with distinct regulatory environments and specialized applications, though market analysis remains limited due to data constraints.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

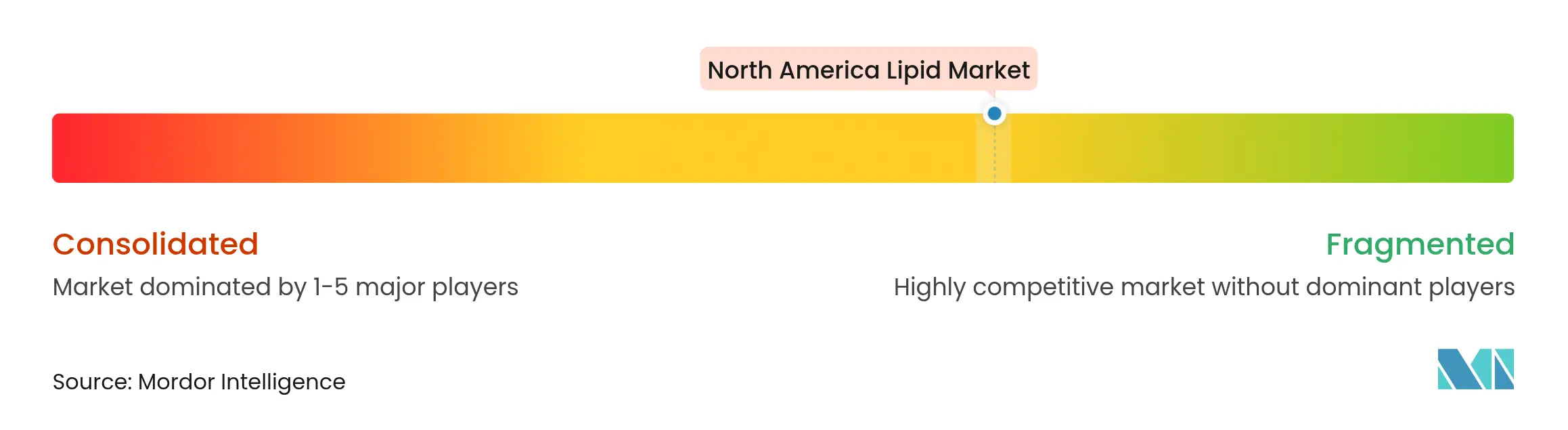

Market Concentration

The North America lipid market demonstrates a moderate level of fragmentation. This market structure facilitates strategic consolidation opportunities while fostering competitive dynamics that enhance innovation and maintain pricing efficiency. The market's competitive environment is dominated by established organizations, including Cargill Incorporated, BASF SE, Kerry Group plc, Croda International Plc, and Bunge Ltd, each contributing significantly to market development and technological advancement.

Market leaders are implementing comprehensive vertical integration strategies to strengthen their competitive positions. A notable example is KD Pharma's strategic acquisition of DSM-Firmenich's marine lipids business in October 2024, which included the MEG-3 brand and production facilities in Canada and Peru. This acquisition exemplifies the industry trend toward consolidation and technological advancement in pharmaceutical and dietary supplement applications.

The competitive landscape presents significant opportunities in sustainable production technologies and pharmaceutical applications, with emerging companies introducing innovative production methods to gain market share. Regulatory compliance requirements serve as a critical differentiator among market participants, while established companies such as Archer Daniels Midland maintain their market positions through robust governance frameworks and operational transparency in their Nutrition segment. This competitive environment encourages continuous innovation and operational excellence among market participants.

North America Lipid Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Croda International Plc opened a new lipids manufacturing facility in Lamar, Pennsylvania, United States. The 23,680 square foot, multi-purpose facility strengthens Croda's production capabilities for drug delivery system components, including lipids.

- October 2024: Ahlstrom Corporation introduced Lipid Saver, a specialized solution developed for the collection, transportation, and storage of fatty acids derived from whole blood samples.

- December 2023: Lipoid introduced a new product quality for LIPOID PE 18:1 that enables quick and complete dissolution in ethanol, simplifying customer processing operations. This enhancement aligns with the company's continuous improvement of production processes and product offerings.

- March 2023: Evonik opened a new GMP facility to manufacture lipids for advanced pharmaceutical drug delivery applications. The lipid launch facility, located at the company's site in Hanau, Germany, provides customers with lipid quantities needed for clinical and small-scale commercial manufacturing.

Table of Contents for North America Lipid Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising popularity of fortified functional foods and beverages

- 4.2.2Expanding adoption of omega-3 and functional lipids in dietary supplements and nutraceuticals

- 4.2.3Widening use of MCTs (medium-chain triglycerides) in weight management diets

- 4.2.4Growing demand for plant-based and algae-derived lipids

- 4.2.5Pharmaceutical innovation using lipids in drug delivery systems

- 4.2.6Increasing investment in algae-based lipid production technologies

- 4.3Market Restraints

- 4.3.1Volatility in raw material prices

- 4.3.2Stringent purity and safety regulations

- 4.3.3Negative consumer perception of highly processed lipids

- 4.3.4Limited algal fermentation infrastructure

- 4.4Supply Chain Analysis

- 4.5Regulatory Outlook

- 4.6Porter’s Five Forces

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers/Consumers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Product Type

- 5.1.1Omega-3

- 5.1.2Medium-Chain Triglycerides (MCTs)

- 5.1.3Phospholipids and Glycolipids

- 5.1.4Others

- 5.2By Source

- 5.2.1Marine-based

- 5.2.2Plant-based

- 5.2.3Animal-based

- 5.3By Form

- 5.3.1Powder

- 5.3.2Liquid

- 5.4By Application

- 5.4.1Functional Food and Beverages

- 5.4.2Infant Nutrition

- 5.4.3Pharmaceuticals

- 5.4.4Dietary Supplements

- 5.4.5Animal Feed

- 5.4.6Others

- 5.5By Country

- 5.5.1United States

- 5.5.2Canada

- 5.5.3Mexico

- 5.5.4Rest of North America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Ranking Analysis

- 6.4Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1Cargill Incorporated

- 6.4.2BASF SE

- 6.4.3Kerry Group plc

- 6.4.4Croda International Plc

- 6.4.5Bunge Ltd.

- 6.4.6KD Pharma Group SA

- 6.4.7Merck KGaA

- 6.4.8Solutex GC, S.L.

- 6.4.9Epax Norway AS

- 6.4.10GC Rieber Oils AS

- 6.4.11Archer Daniels Midland Company

- 6.4.12Golden Omega S.A.

- 6.4.13Omega Protein Corporation

- 6.4.14Plant Lipids Pvt Ltd

- 6.4.15Aker BioMarine ASA

- 6.4.16Lonza Group Ltd.

- 6.4.17Nissui Corporation

- 6.4.18Associated British Foods

- 6.4.19Lonza Group

- 6.4.20Stepan Company

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

North America Lipid Market Report Scope

North American Lipid Market is segmented by product type, application, and geography. On the basis of product type, the market is segmented into omega 3 and omega 6, medium-chain triglycerides (MCTs), and other product types. On the basis of application, the market is segmented into functional food and beverages, infant nutrition, pharmaceuticals, dietary supplements, animal feed, and pet food, and cosmetics., Based on geography, the report provide a regional analysis, which includes United States, Mexico, Canada, and rest of North America.