Phospholipids Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.24 Billion |

| Market Size (2031) | USD 3.18 Billion |

| Growth Rate (2026 - 2031) | 7.26% CAGR |

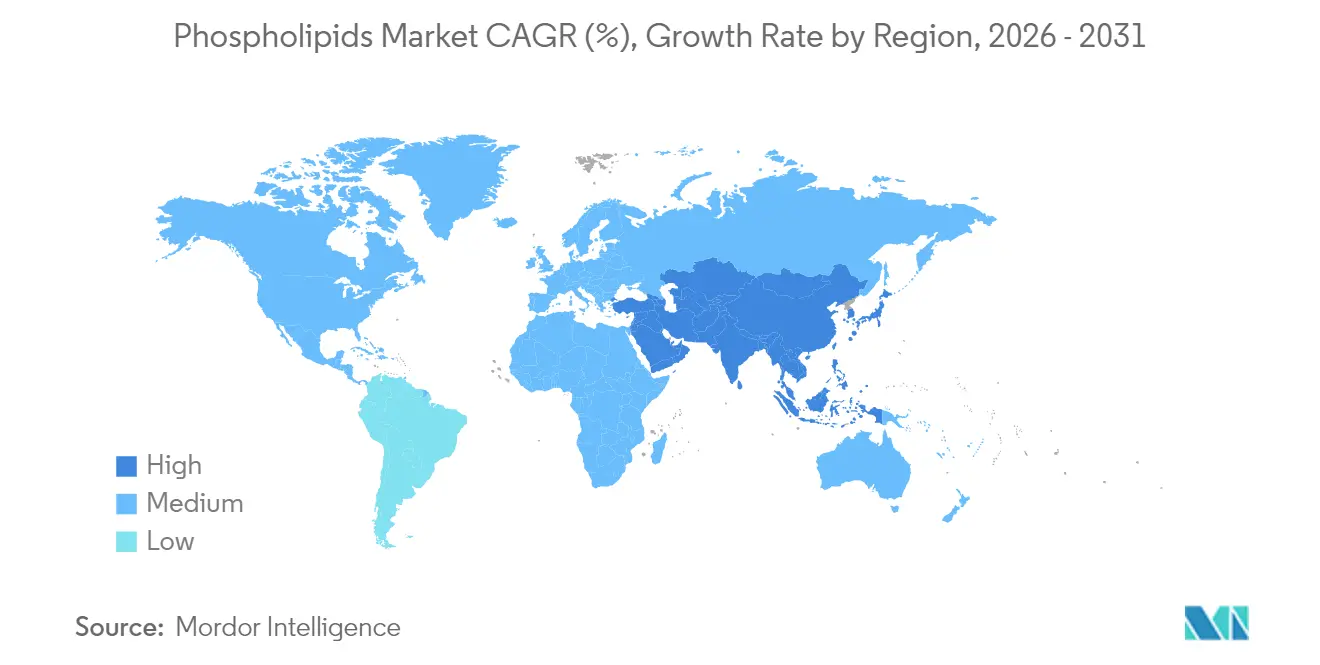

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Phospholipids Market Analysis by Mordor Intelligence

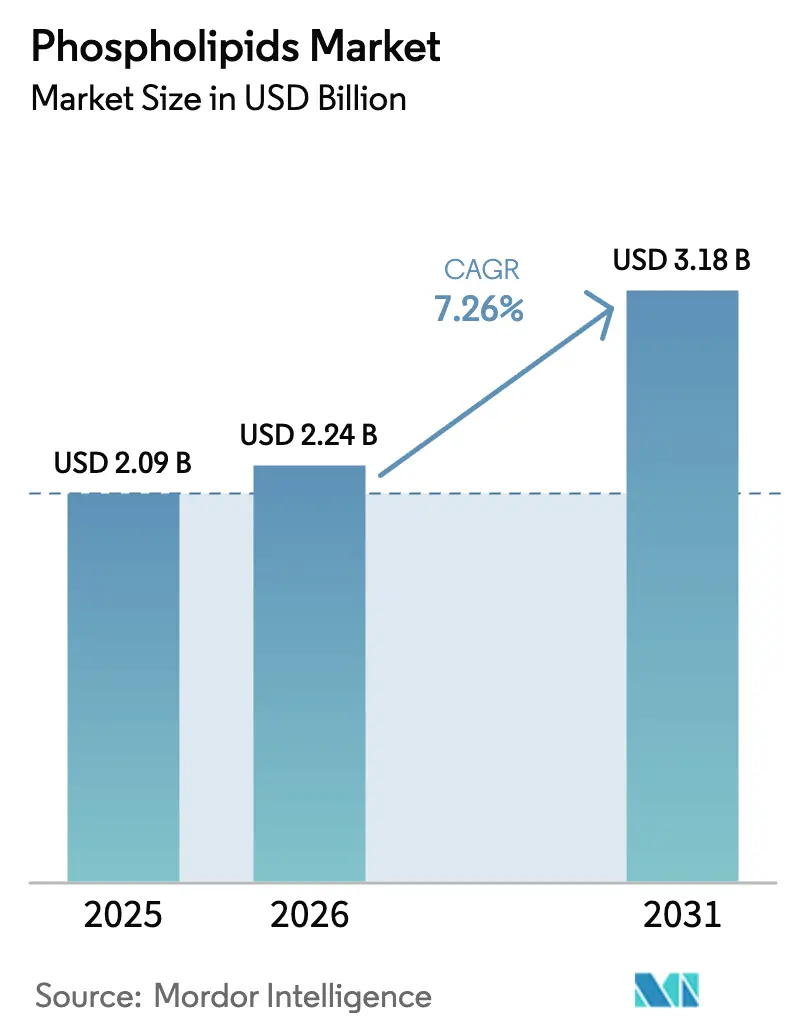

The phospholipids market size was valued at USD 2.09 billion in 2025 and estimated to grow from USD 2.24 billion in 2026 to reach USD 3.18 billion by 2031, at a CAGR of 7.26% during the forecast period (2026-2031). This growth is driven by increasing demand in nutraceuticals and pharmaceuticals, evolving regulatory frameworks, and advancements in lipid-based delivery systems. The European Commission's 2024 regulation on infant formula, limiting phospholipid content to 2 g/L, establishes safety standards while creating opportunities for high-purity phospholipid products [1]Source: European Union, “Commission Delegated Regulation 2024/225,” ec.europa.eu Moderna, “Annual Report 2024,” eur-lex.europa.eu. The market expansion is supported by research demonstrating phospholipids' role in cognitive function and their application in lipid nanoparticles for mRNA therapeutics. The industry is shifting toward non-GMO sunflower and marine-sourced phospholipids in response to sustainability and allergen concerns. Improvements in supercritical and ethanol-based extraction methods are reducing production costs and enhancing product purity, narrowing the quality gap between food and pharmaceutical grades.

Key Report Takeaways

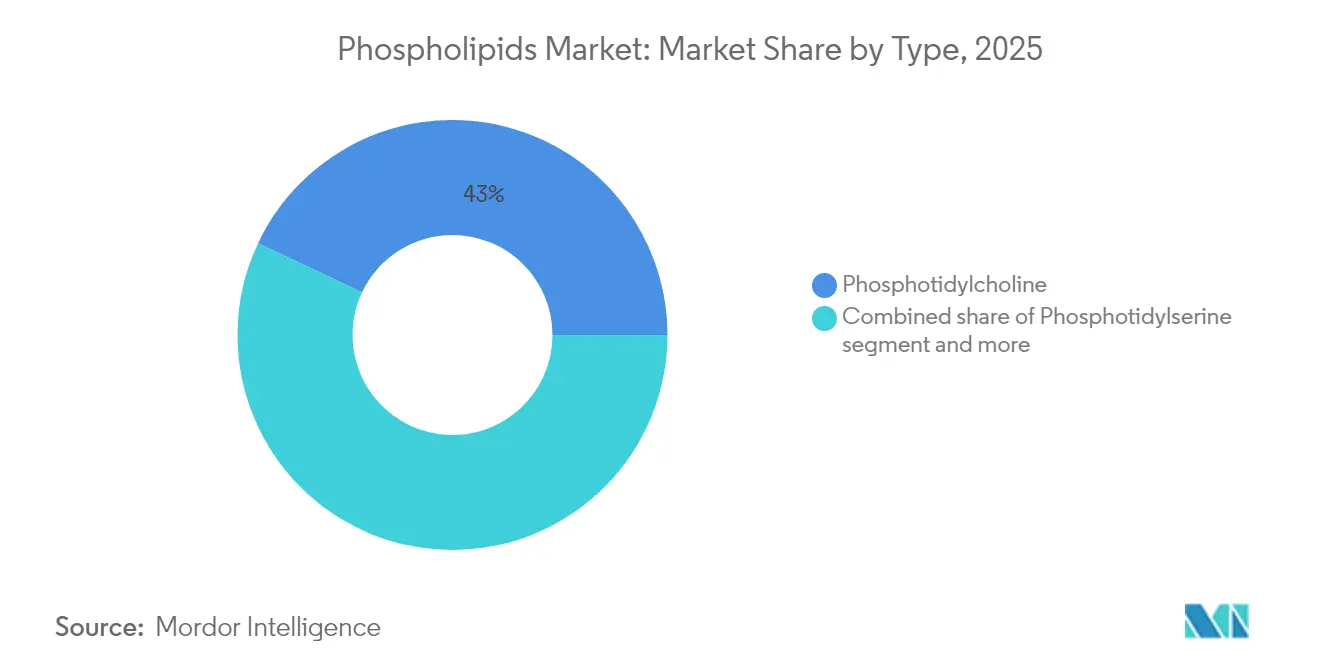

- By type, phosphotidylcholine led with 42.98% phospholipids market share in 2025, while phosphotidylserine is projected to climb at an 7.78% CAGR to 2031.

- By source, soy accounted for 61.02% of the phospholipids market in 2025; sunflower-derived grades exhibit the fastest growth at an 8.49% CAGR through 2031.

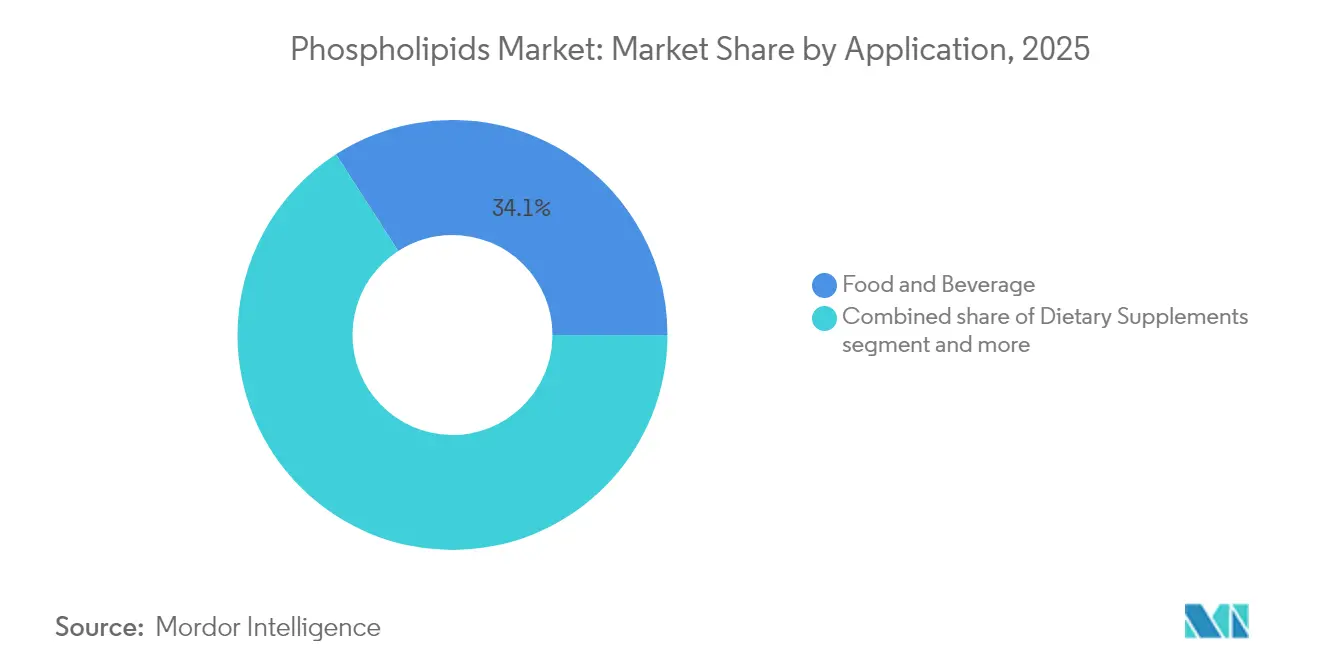

- By application, food and beverage held 34.12% revenue share in 2025, whereas pharmaceutical use is advancing at an 7.95% CAGR between 2026-2031.

- By geography, North America commanded 32.10% share of the phospholipids market in 2025; Asia-Pacific is expanding at a 7.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Phospholipids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand in nutraceuticals for cognitive health support | +1.8% | Global, with a concentration in North America and Europe | Medium term (2-4 years) |

| Surging vegan and plant-based phospholipid sources | +1.2% | Global, particularly strong in Europe and North America | Long term (≥ 4 years) |

| High demand in infant nutrition products | +1.5% | Global, with regulatory leadership in Europe and North America | Short term (≤ 2 years) |

| Rising demand of phospholipids in drug delivery systems | +2.1% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Technological advancements in extraction and purification | +0.9% | Global, with innovation centers in North America and Europe | Medium term (2-4 years) |

| Emerging application in tissue engineering and cell culture | +0.7% | North America and Europe, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand in Nutraceuticals for Cognitive Health Support

The growing recognition of cognitive health importance and changing consumer lifestyles are driving demand for brain health nutraceuticals. Phospholipids have become essential ingredients due to their role in neural function and structure. The European Food Safety Authority recommends a daily choline intake of 400 mg, which is higher than typical dietary consumption, indicating a significant market opportunity for phospholipid supplements. Companies are developing specialized formulations to address various cognitive health requirements. In 2024, Indena introduced Virtiva Plus, which combines Ginkgo biloba extract with phosphatidylserine, illustrating the market's shift toward premium, specialized products. The phospholipids market is expanding into stress management and sports nutrition segments, as younger consumers seek cognitive performance enhancement through phospholipid supplements. This trend strengthens phospholipids' position as high-value, multifunctional ingredients in the global nutraceutical market.

Surging Vegan and Plant-Based Phospholipid Sources

The increasing preference for plant-based phospholipid sources is driven by sustainability concerns and allergen avoidance requirements, which are changing supply chain patterns. The non-GMO foods market is projected to experience significant growth in the forecast period through the end of this decade, supporting the demand for sunflower-derived phospholipids. The adoption of ethanol-based extraction methods instead of hexane extraction aligns with current EU regulations on food processing solvents. This transition in extraction methodology demonstrates the industry's adaptation to regulatory requirements while maintaining production efficiency and product quality. The market continues to evolve as manufacturers invest in sustainable practices and alternative processing methods to meet consumer demands and regulatory standards.

High Demand in Infant Nutrition Products

Infant nutrition is a highly regulated segment where phospholipids play a crucial role in cognitive and immune development. The incorporation of phospholipids in infant formula has gained significant attention due to their proven benefits in brain development, immune system function, and overall infant health. In 2024, Food Standards Australia New Zealand approved milk fat globule membrane (MFGM) as a nutritive substance in infant formula, acknowledging phospholipids' developmental benefits[2]Source: Food Standards, “Food Standards Australia New Zealand,” foodstandards.gov.au. This regulatory approval represents a significant milestone in the infant nutrition industry, as MFGM-WPC contains glycerophospholipids and sphingolipids at concentrations of 4-7 g/L. The approval also demonstrates the growing recognition of phospholipids' importance in early childhood development and sets a precedent for similar regulatory changes in other regions. Moreover, several clinical trials demonstrate that phospholipid-supplemented infant formulas produced significantly higher cognitive, language, and motor scores at 12 months compared to control formulas, providing evidence-based support for premium positioning

Rising Demand of Phospholipids in Drug Delivery Systems

Pharmaceutical applications represent the fastest-growing segment for phospholipids due to their essential role in advanced drug delivery systems, particularly in gene therapy and precision medicine. Evonik's lipid-based delivery technology supports the encapsulation and cellular uptake of nucleic acid therapies, providing stability and targeted release profiles. Cellectar Biosciences' phospholipid drug conjugate (PDC) platform demonstrates the technology's effectiveness by delivering therapeutic agents to cancer cells while reducing exposure to healthy tissues. The expansion of personalized medicine and biologics increases the demand for phospholipids in pharmaceutical formulations. The rise in regulatory approvals for lipid-enabled therapeutics and vaccine platforms has prompted pharmaceutical manufacturers to increase investments in specialized phospholipid systems, highlighting their importance in targeted drug delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of pharmaceutical grade phospholipids | -1.1% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Complex extraction and refining process | -0.8% | Global, with higher impact in regions with limited technical infrastructure | Medium term (2-4 years) |

| Regulatory variability across geography | -0.6% | Global, with particular challenges in emerging markets | Medium term (2-4 years) |

| Low stability in high-temperature food processing | -0.4% | Global, particularly affecting food processing applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Pharmaceutical Grade Phospholipids

High prices of pharmaceutical-grade phospholipids significantly constrain market growth, particularly in emerging economies where cost concerns restrict their widespread adoption across various therapeutic applications. Croda's Life Sciences segment reported sales of EUR 504.3 million in 2024, representing a 16% decline, with phospholipids contributing only 1% of total sales, demonstrating the substantial challenges in maintaining profitability for high-specification products. The stringent quality-by-design requirements for pharmaceutical lipid formulations impose substantial regulatory compliance costs, which smaller manufacturers find increasingly difficult to manage, ultimately driving consolidation trends among suppliers in the market.

Complex Extraction and Refining Process

The technical complexity of phospholipid extraction and purification processes creates significant production bottlenecks, affecting manufacturing scalability and product quality consistency across various feedstock sources. While ethanol-based extraction methods improve environmental sustainability, they demand precise temperature and pressure control throughout the process to maintain phospholipid molecular integrity. Extraction yields fluctuate considerably based on critical processing parameters such as solvent concentration, contact time, and agitation speed. The industry's mandatory transition from hexane-based extraction to alternative solvents, primarily driven by stringent EU regulations, requires manufacturers to make substantial capital investments in specialized processing equipment and comprehensive operator training programs. This widespread operational transformation has resulted in temporary supply chain constraints as manufacturers systematically modify their production facilities and adapt to new extraction methodologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Phosphotidylcholine Dominance Faces Emerging Competition

Phosphotidylcholine holds 42.98% of the market share in 2025, primarily due to its use in cognitive health supplements and pharmaceutical formulations. Its function as a choline source for acetylcholine synthesis, which supports memory and learning, has been validated through extensive research. The segment's market position is strengthened by regulatory approvals across multiple regions, making it difficult for alternative phospholipid types to gain significant market share.

Phosphotidylserine is projected to grow at 7.78% CAGR through 2031, driven by increased adoption in sports nutrition products and new research demonstrating its stress management benefits. The compound's growing popularity in athletic performance supplements and mental wellness products has created new opportunities for manufacturers and suppliers in the phospholipid market .

By Source: Soy Leadership Challenged by Sunflower Innovation

Soy-derived phospholipids hold a 61.02% market share in 2025, supported by established supply chains and efficient extraction processes. This dominance stems from mature soybean processing infrastructure and the availability of phospholipid-rich byproducts from oil refining. The extensive processing network and consistent supply of raw materials create economies of scale, enabling manufacturers to maintain competitive pricing in the global market.

Sunflower-derived phospholipids are growing at an 8.49% CAGR through 2031, driven by demand for non-GMO alternatives and higher phosphatidylcholine content. The increasing consumer preference for natural and non-genetically modified ingredients has positioned sunflower phospholipids as a premium alternative. Their superior phosphatidylcholine content enhances functional performance in food applications, making them particularly attractive for manufacturers focused on product quality and clean-label formulations.

By Application: Food Dominance Shifts Toward Pharmaceutical Innovation

The food and beverage segment holds 34.12% market share in 2025, as phospholipids serve as natural emulsifiers in processed foods, baked goods, and plant-based alternatives. These compounds improve texture and stability in food products. Consumer demand for clean-label ingredients and widespread regulatory approval across global markets sustains the demand for lecithin-based formulations. The increasing adoption of phospholipids in food processing, coupled with their natural origin and functional benefits, continues to drive their use across various food applications.

The pharmaceutical segment is projected to grow at 7.95% CAGR through 2031, primarily due to advancements in drug delivery systems. The growth is particularly notable in lipid nanoparticles used for mRNA vaccines and gene therapy applications, where phospholipids facilitate targeted therapeutic delivery. The expanding research in pharmaceutical applications and the development of novel drug formulations further strengthen the segment's growth potential in the coming years.

Geography Analysis

North America holds a dominant 32.10% market share in 2025, driven by advanced pharmaceutical research and development infrastructure, supportive regulatory frameworks, and established nutraceutical markets. The region's prominence is reinforced by investments in mRNA vaccine technologies and drug delivery systems, as evidenced by Moderna's USD 3.1 billion net product sales in 2024, validating the commercial success of phospholipid-based therapeutics. The region's leadership position is further strengthened by its robust supply chain infrastructure, established research institutions, and strong collaboration between industry and academia in developing innovative phospholipid applications.

Asia-Pacific exhibits the highest growth rate at 7.66% CAGR through 2031. This growth stems from expanding middle-class populations, rising health awareness, and improved regulatory frameworks that support market entry for new phospholipid ingredients. China's National Health Commission's 2024 approval of L-alpha-Glycerylphosphorylcholine as a food raw material demonstrates regulatory support that enhances market opportunities. The streamlined approval process in China, featuring reduced review periods and higher acceptance rates, presents significant expansion opportunities for international phospholipid suppliers. The region's rapid industrialization, increasing healthcare expenditure, and growing focus on preventive healthcare further accelerate market growth.

Europe maintains consistent growth despite complex regulations. The European Commission's revised infant formula regulations influence phospholipid applications, while regional sustainability initiatives increase demand for plant-based phospholipid sources that meet environmental standards. The region's mature market characteristics, combined with stringent quality standards and emphasis on sustainable production methods, create a stable but competitive environment for phospholipid manufacturers and suppliers.

Competitive Landscape

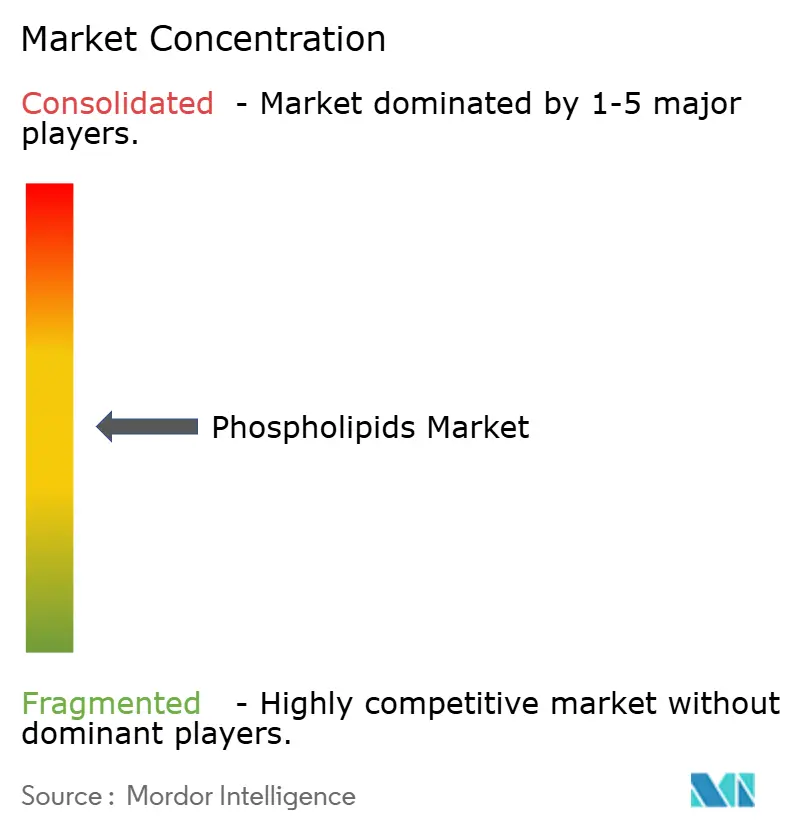

The market maintains moderate fragmentation, with vertically integrated companies optimizing margins through control of soybean crushing, fractionation, and downstream formulation processes. Companies with diverse portfolios across food, feed, and pharmaceutical segments demonstrate resilience against market fluctuations in individual channels. The major players in the market include Cargill Incorporated, VAV Life Sciences, Lipoid GmbH, Kemin Industries, and DSM-Firmenich.

Technological capabilities increasingly determine market position. Companies with patents in zwitterionic phospholipids and microfluidic continuous-flow systems establish competitive advantages in high-value therapeutic applications. Cellectar Biosciences demonstrates this trend through its phospholipid drug conjugate platform, which is currently exploring strategic alternatives, showing how specialized suppliers can evolve into licensors of drug-delivery technologies. Companies focusing on marine and upcycled sources attract sustainability-focused investors but must address scale-up costs and regulatory compliance challenges.

Strategic collaborations continue to shape the market. Lipid manufacturers form partnerships with Contract Development and Manufacturing Organizations (CDMOs) to secure sterile fill-finish capabilities. Food ingredient companies invest in low-solvent or solvent-free extraction technologies to comply with EU regulations. Merger and acquisition discussions focus on international partnerships that combine research and development capabilities with raw material access, particularly as global conflicts affect sunflower oil availability.

Phospholipids Industry Leaders

Cargill, Incorporated

VAV Life Sciences

Lipoid GmbH

DSM-Firmenich

Kemin Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Lipoid GmbH introduced non-GMO soybean phospholipids, positioning them as an optimal solution for clean-label supplements.

- November 2024: Cellectar Biosciences partnered with SpectronRx to manufacture iopofosine I 131, a cancer therapy utilizing phospholipid drug conjugate delivery platform technology. This partnership enhances global supply network capabilities for phospholipid-based therapeutics

- March 2024: India-based VAV Lipids expanded into Latin America to supply high-purity lipids and phospholipids to pharmaceutical, nutraceutical, and cosmetic manufacturers in Mexico, Brazil, Argentina, Peru, and Colombia. The EU-GMP-certified company will distribute its complete product portfolio through local networks, including plant-derived lecithins (LECIVA), egg lecithins (LIPOVA), synthetic phospholipids, and neutral lipids, along with technical and marketing support.

Global Phospholipids Market Report Scope

A phospholipid is a type of lipid molecule that contain two fatty acids, a phosphate group, and a glycerol molecule. The global phospholipids market (henceforth referred to as the market studied) is segmented by type, source, application, and geography. By type, the market is segmented into phosphatidylserine, phosphatidylcholine, and others. Based on the source, the market is segmented into soy, sunflower, egg, and others. Based on the application, the market studied is segmented into food & beverages, nutraceutical supplements, pharmaceuticals, and others. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Phosphotidylserine |

| Phosphotidylcholine |

| Others |

| Soy |

| Sunflower |

| Egg |

| Others |

| Food and Beverage |

| Dietary Supplements |

| Pharmaceutical |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Phosphotidylserine | |

| Phosphotidylcholine | ||

| Others | ||

| By Source | Soy | |

| Sunflower | ||

| Egg | ||

| Others | ||

| By Application | Food and Beverage | |

| Dietary Supplements | ||

| Pharmaceutical | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the value of the phospholipids market today and how fast will it grow by 2031?

The global phospholipids market stands at USD 2.24 billion in 2026 and is projected to reach USD 3.18 billion by 2031, reflecting a 7.26% CAGR

Which phospholipid type currently leads global sales?

Phosphotidylcholine accounts for 42.98% of 2025 revenue, the highest share among all phospholipid types.

Which end-use segment is expanding the quickest?

Pharmaceutical applications show the fastest momentum, advancing at an 7.95% CAGR from 2026-2031

Which region will post the highest growth through 2031?

Asia-Pacific is projected to increase at a 7.66% CAGR, propelled by regulatory approvals.

Page last updated on: