Layer Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 85.84 Billion |

| Market Size (2031) | USD 116.5 Billion |

| Growth Rate (2026 - 2031) | 6.30% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Layer Feed Market Analysis by Mordor Intelligence

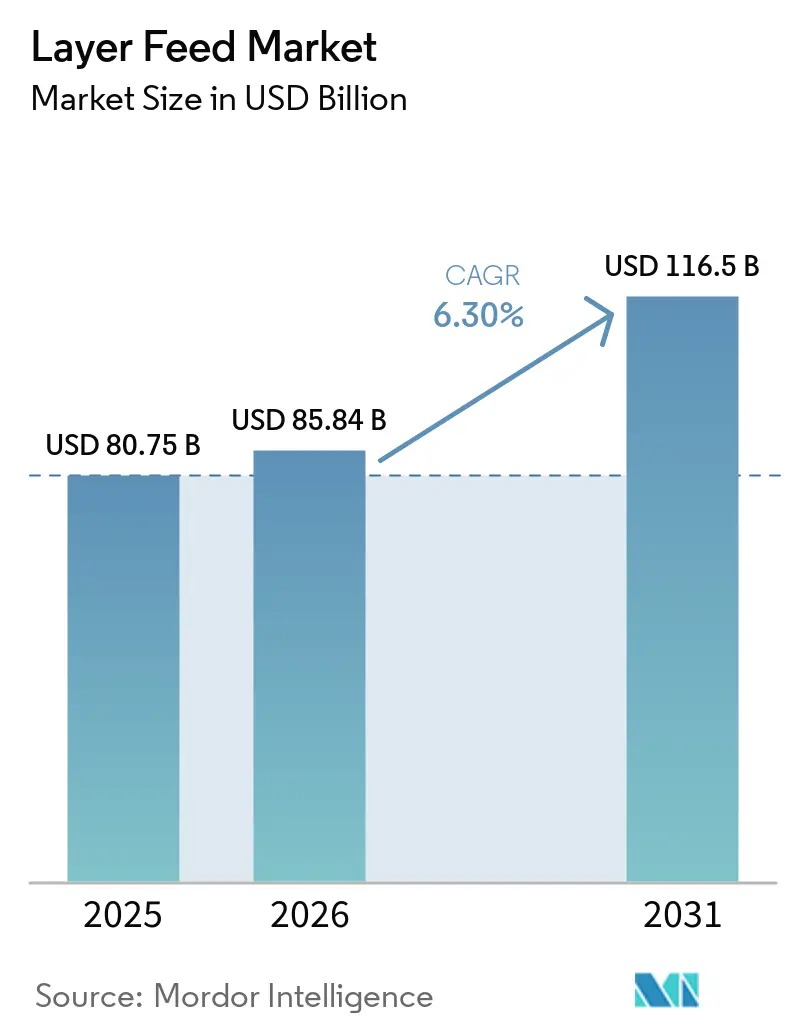

The layer feed market size is projected to increase from USD 80.75 billion in 2025 to USD 85.84 billion in 2026 and reach USD 116.50 billion by 2031, registering a CAGR of 6.3% during 2026–2031. The market is advancing along two parallel trends, feed volumes are increasing alongside flock expansion, while feed value is rising faster as producers shift toward specialty formulations supporting omega-3 eggs, cage-free production systems, and extended laying cycles. Asia-Pacific remains the largest demand center, supported by China’s laying hen population of approximately 1.29 billion birds in 2026, while Brazil continues benefiting from strong soybean availability, and Europe is recording comparatively slower volume growth, led by Germany and Poland. The layer feed market also reflects a broader shift in producer purchasing behavior, as integrated poultry operations increasingly prioritize feed efficiency, egg mass, shell quality, and flock persistence over feed cost alone. This transition is supporting greater formulation differentiation, technical service integration, and additive-enriched feeding programs that are comparatively more resilient than standard commodity feed offerings. However, disease outbreaks and raw material price volatility continue to constrain the pace of premium nutrition adoption, underscoring the need to maintain execution discipline and a procurement strategy central to long-term growth across the layer feed market.

Key Report Takeaways

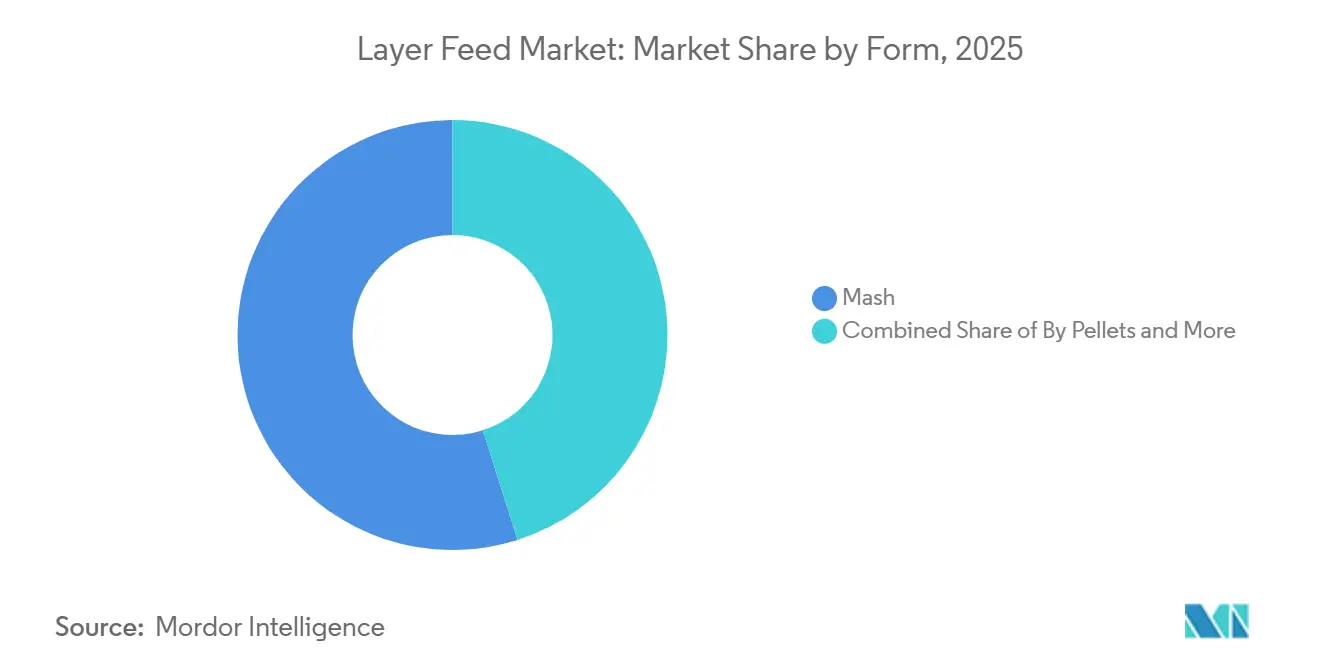

- By form, mash accounted for 54.9% of the layer feed market share in 2025, and pellets were the fastest-growing segment, with a 5.0% CAGR over 2026-2031.

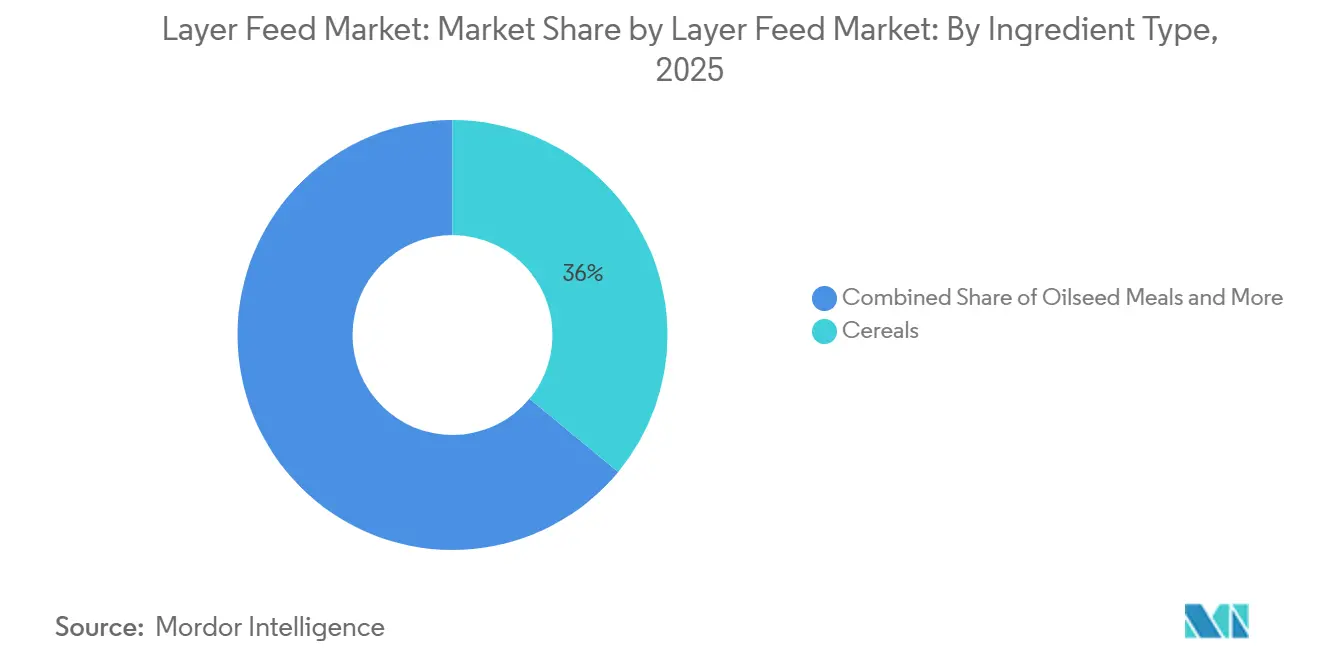

- By ingredient type, cereals were the largest segment with a 52.5% share in 2025, while additives were the fastest-growing segment at an 8.4% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Layer Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing shell egg consumption and commercial layer flock expansion | +2.1% | Global, with concentrated gains in Asia-Pacific, Middle East, and Sub-Saharan Africa | Short term (≤ 2 years) |

| Feed conversion and egg yield optimization focus | +1.5% | Global, most impactful in North America, Europe, and Asia-Pacific where integrated production dominates | Medium term (2-4 years) |

| Rising demand for fortified, omega-3, and premium eggs | +1.2% | North America and Europe core, expanding into Asia-Pacific and Middle East as premium retail channels broaden | Medium term (2-4 years) |

| Antibiotic-free production increasing additive-rich feed adoption | +1% | North America and European Union core, with spillover into Asia-Pacific through export-chain requirements | Medium term (2-4 years) |

| Longer laying cycles requiring sustained nutritional precision | +0.9% | Global, with early commercial adoption in North America, Europe, and parts of Asia-Pacific | Long term (≥ 4 years) |

| Heat-stress and shell-strength management demand | +0.8% | Asia-Pacific core, Middle East, Africa, with spillover into South America and Southern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Shell Egg Consumption and Commercial Layer Flock Expansion

Persistent egg demand is giving the layer feed market a durable volume base across both mature and developing poultry systems. Germany’s Federal Statistical Office recorded 13.7 billion consumer eggs in 2025 from a flock of around 44.6 million hens, with an average of 304 eggs per laying hen. Saudi Arabia is also adding new commercial egg capacity from late 2025, supported by food security programs and related infrastructure spending that reduce import dependence, which keeps local feed demand on a firmer base. In Southeast Asia and Sub-Saharan Africa, the formal shift from on-farm mixing to compound feed purchasing is widening the addressable customer base, even as flock numbers are not rising at the same pace. This pattern keeps the layer feed market closely linked to both flock expansion and the commercial formalization of egg production.

Feed Conversion and Egg Yield Optimization Focus

Feed represents 60% to 75% of total laying hen production cost, so performance improvement remains one of the strongest commercial drivers in the layer feed market. Producers are increasingly judging nutrition programs by cost per egg rather than by cost per kilogram of feed, which shifts buying decisions toward higher precision formulation. That has increased the appeal of amino acid balancing, digestible phosphorus programs, and tighter energy-density control in commercial layer diets. Cargill presented its REVEAL Layers near-infrared (NIR) body-condition monitoring platform at VIV Asia 2025 and the International Production and Processing Expo (IPPE) 2026, demonstrating how feed adjustments can be tied to flock condition over a 100-week cycle. As a result, the layer feed market is moving further away from simple ration supply and closer to a technical service model with higher switching costs.

Rising Demand for Fortified, Omega-3, and Premium Eggs

The layer feed market is gaining from the spread of premium egg categories, because these products require more specialized feed formulas than standard shell egg production. Fortified and omega-3 eggs enable producers to achieve better retail margins, which supports spending on flaxseed-based diets, specialty fats, and other differentiated inputs. This is important in countries where standard egg pricing is tightly managed, because producers can use product differentiation to protect value rather than competing only on base volume. The layer feed market, therefore, benefits when consumer demand moves beyond basic eggs and starts rewarding nutritional attributes, cage-free systems, and branded quality claims. Premium formats also raise the average revenue per metric ton for feed producers, since specialty diets usually carry a higher formulation value than standard feed. Over time, this pushes the layer feed market toward a more mixed structure, where value growth can outpace pure volume growth.

Antibiotic-Free Production Increasing Additive-Rich Feed Adoption

The shift away from antibiotic growth promoters is changing formulation economics across the layer feed market. European Union Regulation 2019/6 made the use of antimicrobials for growth promotion or routine disease prevention in healthy animals unacceptable across member states, pushing producers toward more additive-supported diets. Similar stewardship expectations in the United States are shaping commercial purchasing standards among large egg buyers, so feed programs now need clearer health support that relies less on routine antibiotic inclusion. In April 2025, Cargill launched Biostrong C-Protect, and in March 2026, it released field data from an 11 million bird cage-free operation showing more than 60% lower APEC (Avian Pathogenic Escherichia coli-challenged)-related mortalities when the product was used in pullet and production diets. International Organization for Standardization 22000 (ISO 22000) certification also reinforces demand for auditable formulations, which gives the layer feed market a steady pull toward postbiotics, phytogenics, and other documented feed health tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corn and soybean meal price volatility | -0.50% | Global, most acute in import-dependent Middle East and Africa | Short term (≤ 2 years) |

| Avian influenza and disease-led flock disruption | -0.40% | North America and Asia-Pacific core, with spillover into Europe | Short term (≤ 2 years) |

| Traceability and deforestation-linked soy compliance costs | -0.20% | European Union 27 primarily, with spillover into North America | Medium term (2-4 years) |

| Egg price compression limiting premium feed uptake | -0.20% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Corn and Soybean Meal Price Volatility

Corn and soybean meal volatility remains the most direct margin restraint in the layer feed market because those inputs dominate the cost of standard rations. Corn and soybean meal together account for more than 70% of a standard layer diet by weight, and Brazil’s animal nutrition sector consumed around 60 million metric tons of corn and 20 million metric tons of soybean meal in 2025[1]Source: Sindirações, “Produção de ração animal no Brasil crescerá 3% em 2025,” Poder360, poder360.com.br. Brazil also recorded a 171.8 million metric ton soybean harvest in the 2024-25 season, but prices still remained exposed to export demand, biofuel pull, and geopolitically driven trade shifts. Soy origin also affects digestibility, so procurement shifts can change formulation value even when headline price moves look manageable. That uncertainty slows premium feed adoption and keeps the layer feed market highly sensitive to raw material purchasing discipline.

Avian Influenza and Disease-Led Flock Disruption

Disease remains a major restraint on the layer feed market because flock losses immediately reduce feed demand, while repopulation takes time and capital. The Congressional Research Service reported that highly pathogenic avian influenza accounted for 75% of domestic poultry losses in the latest major United States outbreak cycle, and recovery from depopulation to full restocking usually takes 20 weeks. [2]Source: Congressional Research Service, “Highly Pathogenic Avian Influenza (HPAI): Domestic Poultry Impact,” Congressional Research Service, everycrsreport.com That disruption creates a direct volume shock for the layer feed market and makes mill utilization harder to manage during outbreak periods. Disease risk also slows investment in premium housing and higher-specification feed programs, since producers may postpone upgrades until biological risk becomes easier to manage. Even after flock recovery begins, feed demand does not return in a straight line because replacement birds move through different nutrition stages before reaching full lay. This makes disease-led volatility one of the most difficult short-term constraints for the layer feed market to absorb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Mash Build Share in Layer Systems

Mash accounted for 54.9% of the layer feed market share in 2025, establishing itself as the leading feed form in the global layer industry. Its extensive adoption is attributed to lower manufacturing costs, formulation flexibility, and its applicability to both commercial and small-scale egg production systems. Mash is particularly prevalent in Asia-Pacific, Africa, and other cost-sensitive regions, where producers prioritize minimizing feed processing costs while maintaining nutritional efficiency. Despite the increasing use of automated feeding systems in modern integrated farms, mash remains the preferred feed format in much of the global layer industry due to its cost-effectiveness and established role in commercial egg production.

Crumbles are anticipated to be the fastest-growing feed form in the layer feed market, with a projected CAGR of 5.0% during 2026–2031. This growth is primarily driven by their application during pullet and transition feeding stages, where uniform particle size enhances feed intake and supports early bird development. The ongoing modernization of poultry production systems, particularly in emerging markets, is driving the adoption of feed formats that ensure consistent flow characteristics and efficient distribution via mechanized feeding equipment. While pellets are gaining traction among some large-scale integrated producers due to their handling and feed management advantages, mash is anticipated to retain its position as the dominant feed form throughout the forecast period.

By Ingredient Type: Additive-Led Value Growth Outpaces Base Ingredients

Cereals accounted for 36.0% of the layer feed market share in 2025, maintaining their position as the largest ingredient group in standard formulations. Corn and wheat remain the energy base of most commercial diets, so cereal demand stays closely linked to overall flock feeding requirements and the structure of local grain markets. Even so, the layer feed market is gradually becoming more balanced by value as protein sources, functional ingredients, and specialty inputs capture a larger share of diet economics. Oilseed meals remain central to protein supply, and the quality of soybean meal has become more important as producers pursue tighter control over egg output and feed conversion. Molasses also plays a useful role in pelleted formulas, helping support palatability and improve pellet quality in high-throughput production systems.

Additives are the fastest-growing ingredient segment, and the layer feed market size for additives is projected to expand at an 8.4% CAGR during 2026-2031. This reflects a broad move away from antibiotic growth promoters and toward programs that support gut health, livability, shell quality, and resilience under stress. Enzymes, probiotics, phytogenics, organic acids, and postbiotics are gaining ground because they serve both performance and compliance needs in modern commercial systems. Fish oil and fish meal remain important in premium egg applications, especially where producers want to support omega-3 enrichment and stronger nutritional positioning at retail. Other ingredient types, including by-products, minerals, and fermented inputs, continue to serve cost control and targeted performance roles as the layer feed market develops into a more formulation-driven business.

Geography Analysis

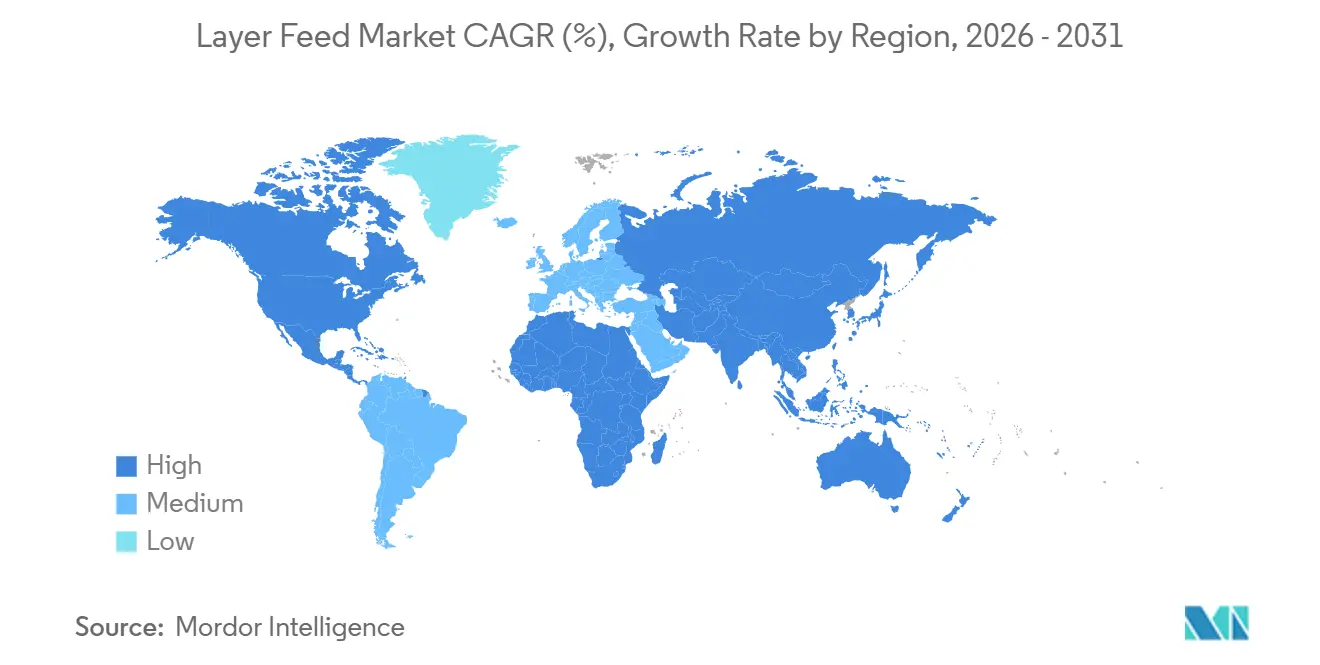

Asia-Pacific held 44% of the global layer feed market in 2025 and is the fastest-growing region during 2026-2031, with a CAGR of 4.4%. China, India, Indonesia, Vietnam, and the Philippines support this position as urbanization, rising egg consumption, and the shift from on-farm mixing to purchased compound feed continue to expand the commercial demand base. In China, the scale of the laying hen population means that even small gains in formulation precision can translate into significant increases in feed demand for manufacturers. India and Southeast Asia are showing the strongest momentum, as a growing middle class continues to lift egg demand and support investment in commercial feed capacity. Heat stress also remains a built-in demand driver across tropical markets, which supports steady spending on functional additives and specialty nutrition.

North America remained a mature but active regional market, with feed demand shaped more by housing transitions and flock recovery than by new structural volume surges. In the United States, post-Highly Pathogenic Avian Influenza (HPAI) recovery normalized feed purchasing, while the shortage of cage-free layers, against corporate buying commitments, continued to support demand for higher-value diets. Canada is growing faster than the broader region because cage-free standards in retail procurement and premium egg channels are expanding. South America is led by Brazil, where integration between feed manufacturing and domestic soy crushing gives producers a clear raw material cost advantage. Smaller Andean and Southern Cone markets are also moving more farms from on-farm ration preparation to purchasing commercial compound feed, gradually broadening the regional customer base.

Europe remained a mature regional market in 2026, with European Union 27 poultry feed production reaching 51.6 million metric tons[3]Source: European Feed Manufacturers’ Federation, “EU Feed Production Forecast Remains Stable Despite Mounting Regulatory and Disease Pressures,” Aquafeed.com, aquafeed.com, up 1.2% from the prior year. Germany and Poland recorded the strongest gains within Europe, while the United Kingdom is moving faster on barn conversion as retailer cage-free commitments pull demand toward higher-value formulations. The Middle East is expanding quickly as Gulf states invest in domestic egg production for food security, and heat-stress additives remain a recurring cost line for regional feed producers. Africa is also becoming a stronger growth cluster, particularly in Nigeria, Egypt, and South Africa, where urbanization and lower protein prices are boosting commercial egg demand and shifting more buyers into formal feed channels.

Competitive Landscape

The layer feed market remains highly fragmented, with hundreds of regional millers, domestic cooperatives, integrated poultry companies, and multinational suppliers operating without meaningful structural pricing power. No single company holds a dominant global position, which keeps competition centered on formulation performance, customer relationships, and operating reach rather than on scale alone. That structure favors companies that can deliver both commodity feed at local cost and premium nutrition services where customers are willing to pay for measurable outcomes. It also leaves room for region-specific strategies because feed demand is still tied closely to local grain supply, flock density, regulation, and disease conditions. In practical terms, the layer feed market rewards execution depth more than brand visibility.

De Heus Animal Nutrition reported 2025 revenue of EUR 6.22 billion (USD 6.78 billion) and, in 2025, completed the acquisition of CJ Feed and Care from CJ CheilJedang, adding 17 feed mills across Vietnam, Indonesia, Cambodia, Korea, and the Philippines. In 2025, De Heus also opened a USD 23.2 million plant in Kenya and expanded its Western European footprint through the acquisition of Voeders Huys, demonstrating a dual focus on emerging-market capacity and mature-market depth. ForFarmers reported 2025 revenue of EUR 3.15 billion (USD 3.44 billion) and identified Poland’s poultry market as a core expansion priority after strengthening its position through a joint venture with KPS. These moves show that growth in the layer feed market is still being pursued through local manufacturing access and regional poultry concentration rather than through global pricing control. They also show that the most active companies are trying to build positions close to the flock rather than rely on export-led feed models.

Cargill has taken a different route by building out a stronger technical services layer around nutrition, health, and digital monitoring. In March 2025, the company introduced its Micronutrition and Health Solutions portfolio at VIV Asia, and in January 2026 it highlighted integrated poultry solutions at International Production & Processing Expo (IPEE) with a focus on longer laying cycles and body-condition monitoring. In April 2025, it launched Biostrong C-Protect, and in March 2026 it released commercial field data that strengthened the case for postbiotic and phytogenic solutions in cage-free layers. This approach matters because the layer feed market is increasingly separating into standard feed supply and feed-plus-service relationships, with the second model offering better margin protection. Smaller specialist mills and alternative protein suppliers can still gain share in premium and antibiotic-free niches, but they usually compete through formulation focus rather than broad geographic spread.

Layer Feed Industry Leaders

Charoen Pokphand Foods Public Company Limited

Cargill, Incorporated

Land O'Lakes, Inc.

De Heus Animal Nutrition B.V.

ForFarmers N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Cargill, Incorporated, released field performance data from a large cage-free commercial layer operation with 11 million birds, confirming that Biostrong C-Protect reduced mortalities in APEC-challenged flocks by more than 60% when integrated into pullet and production diets. The data established a commercial-scale performance benchmark for postbiotic and phytogenic combinations in cage-free layer production.

- January 2026: Cargill, Incorporated showcased its integrated layer poultry solutions at IPPE 2026 in Atlanta, presenting nutrition strategies for laying cycles of up to 100 weeks and demonstrating how REVEAL Layers NIR body-condition monitoring reduces feed costs while sustaining laying persistency across late-cycle production.

- October 2025: De Heus Animal Nutrition B.V. completed the acquisition of CJ Feed and Care from CJ Cheil Jedang, adding 17 feed mills across Vietnam, Indonesia, Cambodia, Korea, and the Philippines. The transaction significantly extended De Heus's direct layer feed production network into 5 Asian markets.

Global Layer Feed Market Report Scope

Layer feed market covers complete diets formulated specifically for commercial egg-laying poultry. The Layer Feed Market is Segmented by Form (Mash, Pellets, Crumbles, and Others), Ingredient Type (Cereals, Oilseed Meal, Molasses, Fish Oil and Fish Meal, Additives, and Other Ingredient Types), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). Forecasts are Provided in Terms of Value (USD).

| Mash |

| Pellets |

| Crumbles |

| Others |

| Cereals |

| Oilseed Meals |

| Molasses |

| Fish Oil and Fish Meal |

| Additives |

| Other Ingredient Types |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Form | Mash | |

| Pellets | ||

| Crumbles | ||

| Others | ||

| By Ingredient Type | Cereals | |

| Oilseed Meals | ||

| Molasses | ||

| Fish Oil and Fish Meal | ||

| Additives | ||

| Other Ingredient Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the layer feed market through 2031?

The layer feed market was valued at USD 80.75 billion in 2025, is estimated at USD 85.84 billion in 2026, and is projected to reach USD 116.50 billion by 2031 at a 6.3% CAGR during 2026-2031.

Which feed form leads the layer feed market?

Mash accounted for 54.9% of the layer feed market share in 2025, establishing itself as the leading feed form in the global layer industry. Its extensive adoption is attributed to lower manufacturing costs, formulation flexibility, and its applicability to both commercial and small-scale egg production systems.

Which ingredient group is growing the fastest in layer feed market?

Additives are the fastest-growing ingredient group with an 8.4% CAGR during 2026-2031. Growth is being driven by antibiotic-free production, heat-stress management, and higher demand for flock health and shell-quality support.

What are the biggest risks for feed manufacturers serving egg producers?

The two main risks are raw material price volatility and disease-led flock disruption. Corn and soybean meal cost swings affect formulation economics, while highly pathogenic avian influenza can remove feed demand for many weeks after depopulation.

Page last updated on: