Starter Feed Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 33 Billion |

| Market Size (2030) | USD 44.5 Billion |

| Growth Rate (2025 - 2030) | 6.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

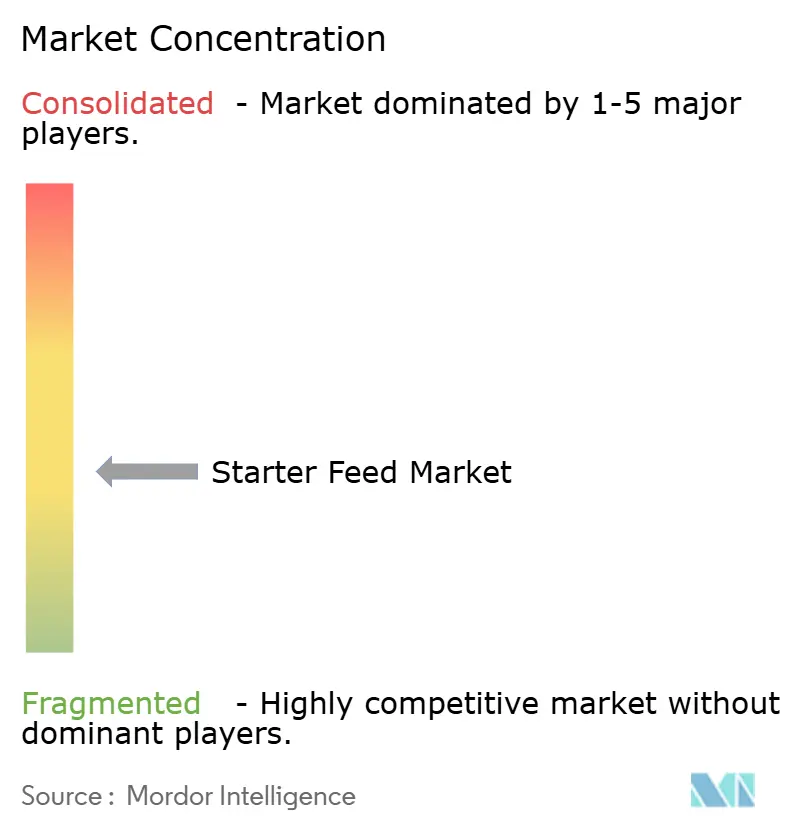

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Starter Feed Market Analysis by Mordor Intelligence

The starter feed market size is valued at USD 33 billion in 2025 and is forecast to reach USD 44.5 billion by 2030 at a 6.2% CAGR. Robust poultry expansion in Asia-Pacific, rapid intensification of Southeast Asian aquaculture, and the worldwide shift away from antibiotic growth promoters collectively underpin this trajectory. Feed form innovations such as precision micro-pellets, wider use of probiotics and phytogenics, and blockchain-enabled traceability premiums are allowing suppliers to protect margins even as commodity prices fluctuate. At the same time, starter feed manufacturers are broadening revenue streams by serving functional protein supply chains for infant formula and sports nutrition, while farm-level precision feeding systems curb waste and optimize feed conversion.

Key Report Takeaways

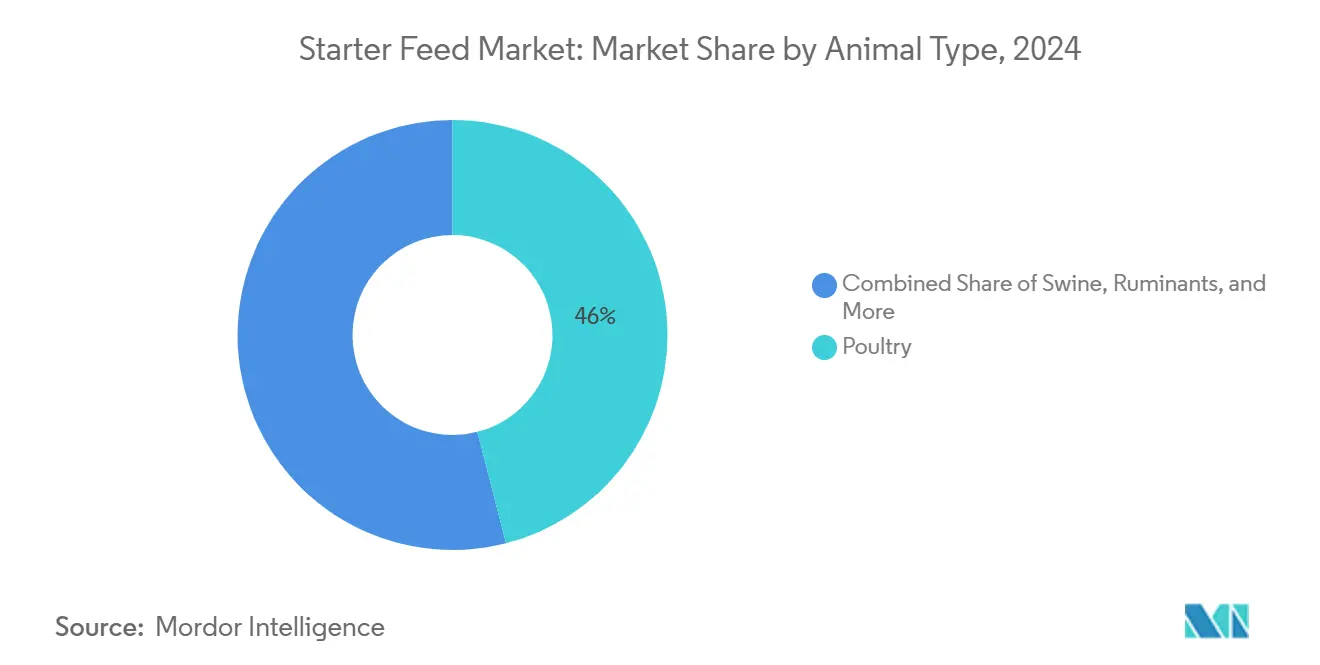

- By animal type, poultry led with 46% of the starter feed market share in 2024, and aquaculture is projected to register the fastest 9.5% CAGR through 2030.

- By product type, non-medicated formulations held 68% share of the starter feed market size in 2024, and the medicated segment is advancing at a 7.8% CAGR to 2030.

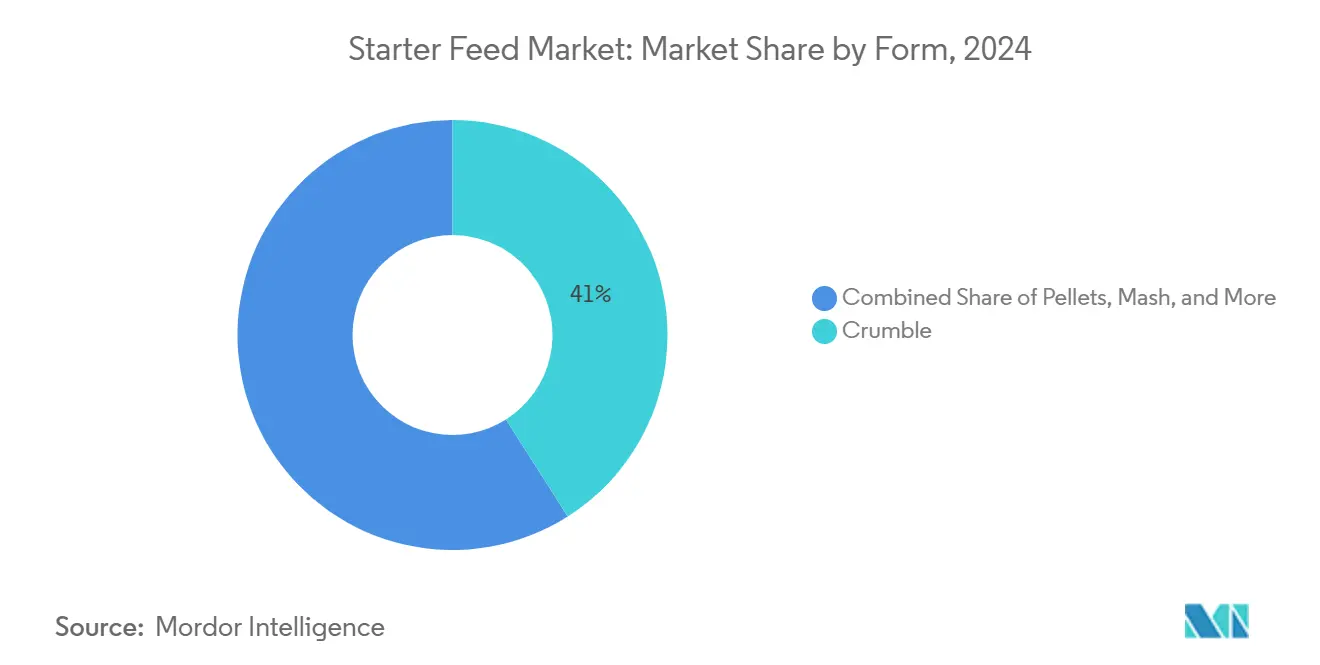

- By form, traditional crumble accounted for 41% of the starter feed market size in 2024, and the pellets segment is expanding at an 8.2% CAGR over the same timeframe.

- By geography, Asia-Pacific captured 37% revenue share in 2024 and is forecast to grow at a 7.3% CAGR to 2030.

- Cargill, Incorporated, ADM, Nutreco, Charoen Pokphand Foods PCL, and Land O'Lakes, Inc. collectively commanded around 40.2% of the starter feed market share in 2024.

Global Starter Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating commercial poultry production in Asia-Pacific | +1.8% | Asia-Pacific core and spill-over to Middle East and Africa | Medium term (2-4 years) |

| Ban on antibiotic growth promoters in Europe and the United States | +1.2% | North America and European Union, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rising demand for functional animal proteins in infant formula and sports nutrition | +0.9% | Global, with premium markets leading | Long term (≥ 4 years) |

| Rapid expansion of commercial aquaculture in Southeast Asia | +1.1% | Asia-Pacific core and emerging in South America | Medium term (2-4 years) |

| Farm-level adoption of precision micro-pellet dosing systems | +0.7% | North America and European Union, pilot Asia-Pacific | Medium term (2-4 years) |

| Blockchain-enabled feed-to-fork traceability premiums | +0.5% | European Union and North America, selective Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Commercial Poultry Production in Asia-Pacific

Industrial broiler capacity additions across China, India, and Southeast Asia are dramatically lifting starter feed demand. Global chicken meat output is set to rise 2.5-3% in 2025, with Asia-Pacific responsible for the bulk of extra volume [1]Source: United States Department of Agriculture, "World Agricultural Supply and Demand Estimates", usda.gov. South and Southeast Asia are anticipated to sustain 4-5% annual poultry growth through 2030, fueled by rising incomes and consumer preference for affordable lean protein. Larger integrators are financing automated facilities that require precision starter diets delivering tight feed conversion ratios during the first two weeks of growth. The economics are compelling, wherein feed accounts for roughly 75% of total broiler costs in Mexico, underscoring why optimized starter rations directly influence profitability. As commercial operators scale, they also adopt biosecurity protocols that heighten demand for pathogen-free starter feed, amplifying opportunity for suppliers that can validate quality at volume.

Ban on Antibiotic Growth Promoters in Europe and the United States

Regulators removed antibiotic growth promoters (AGPs) from poultry and livestock diets in the European Union and the United States, pushing producers to redesign early-phase nutrition. Peer-reviewed literature shows that more than 65% of current poultry nutrition studies focus on alternatives such as probiotics, prebiotics, and phytogenics[2]Source: K.A. Alayande et al., “Alternatives to Antibiotic Growth Promoters for Poultry,” ScienceDirect, sciencedirect.com. Innovation is spreading, and Trouw Nutrition and AgroCares are deploying mobile Near-infrared (NIR) scanners that allow real-time nutrient profiling and on-farm feed reformulation. Because producers can no longer rely on AGPs to offset hygiene lapses, they now place a premium on starter feeds with enhanced shelf stability, low pathogen load, and bioactive ingredients that modulate gut health. The same regulatory logic is moving into Asian jurisdictions, ensuring sustained global growth for specialty non-medicated starter feeds.

Rising Demand for Functional Animal Proteins in Infant Formula and Sports Nutrition

Human nutrition brands are sourcing poultry, dairy, and aquaculture proteins with specific amino acid and bioactive profiles. Early-stage feed, therefore, becomes a strategic lever for downstream product differentiation. Cargill’s partnership with Nestlé Purina on regenerative agriculture illustrates how starter feed specifications are being linked to sustainability narratives that enable premium consumer pricing. Dairy and poultry integrators are paying for starter diets fortified with micronutrients that later translate into improved protein functionality in whey powders and chicken isolate ingredients. Clean-label rules that discourage synthetic additives in sports nutrition reinforce the preference for natural starter feed components, while blockchain traceability helps verify adherence to stringent ingredient protocols.

Rapid Expansion of Commercial Aquaculture in Southeast Asia

Southeast Asia leads global aquaculture volume, and hatcheries there rely on micro-pellet starter feeds with precise buoyancy and nutrient density. Food and Agriculture Organization (FAO) projections show aquaculture maintaining higher growth than any terrestrial protein segment, powered by shrimp and tilapia systems that increasingly adopt recirculating technologies. Nutreco’s full takeover of aquaculture tech firm Eruvaka underscores the market’s appetite for sensor-enabled feeding that cuts waste and boosts survival. Technical barriers favor suppliers with extrusion and micro-encapsulation know-how, safeguarding margins amid volume growth. Sustainability concerns over marine-based raw materials encourage plant and single-cell alternatives, further expanding formulation complexity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in soybean and corn prices | -1.4% | Global and acute in import-dependent regions | Short term (≤ 2 years) |

| Stringent medicated-feed approvals and residue limits | -0.8% | European Union and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Mycotoxin contamination in Asia-Pacific supply chains | -1.1% | Asia-Pacific core and seasonal in tropics | Short term (≤ 2 years) |

| Competition from on-farm home-mix formulations in South America | -0.6% | South America and large operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Soybean and Corn Prices

Starter feed formulations derive between 60% and 70% of their cost from soybean meal and corn. University of Illinois forecasts corn at USD 4.40 per bushel and soybeans at USD 11.20 per bushel for 2024-2025, but uncertainty remains around biofuel demand, Argentine harvest swings, and Black Sea freight premiums[3]Source: Hongxia Jiao, “Corn and Soybeans Economics in 2024 and 2025,” farmdoc daily, illinois.edu. Hedging is challenging for small mills lacking financial capacity, creating margin compression and occasionally forcing ration reformulation that can upset animal performance.

Stringent Medicated-Feed Approvals and Residue Limits

The European Union, the United States, and now parts of Asia-Pacific require separate licensing for each active pharmaceutical ingredient included in medicated starter feeds. The approval process often takes 24-36 months and mandates residue studies, cold storage protocols, and batch-level documentation. These requirements raise compliance costs, deter new entrants, and restrict the number of approved compounds, limiting formulation flexibility. Producers facing region-specific disease outbreaks can find themselves without legal medicated options, creating supply shocks and reliance on emergency import allowances that are both costly and bureaucratically complex.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Aquaculture Gains Speed Amid Poultry Scale

The poultry category sustained 46% of the starter feed market size in 2024, a testament to its industrialized supply chain and uniform performance standards. Aquaculture, though smaller, is slated to expand at 9.5% CAGR, the fastest of all categories, as micro-pellet starter feeds enable higher larval survival in intensive shrimp and tilapia systems. In value terms, aquaculture’s share of the starter feed market is projected to rise, supported by advances in extrusion technology that enhance water stability and nutrient density. Innovations in swine starter formulations targeting post-weaning gut health are reducing mortality and enhancing feed efficiency, while calf starters enriched with rumen-specific probiotics are gaining traction among dairy enterprises focused on improving lifetime milk yield.

Technical demands vary widely. Aquaculture requires the tightest control over pellet floatability, crumble dust, and water solubility, pushing barriers to entry higher than for poultry or swine. Poultry remains the volume anchor, giving suppliers scale economies that trickle down into other species lines. Niche segments such as equine or rabbit feed offer customized opportunities but lack the throughput to interest major multinationals, leaving regional specialists to dominate.

By Product Type: Precision Medicated Formulas Edge Forward

Non-medicated starter feeds constituted 68% market share in the starter feed market, yet medicated products are advancing faster at 7.8% CAGR owing to selective applications in disease-prone geographies. In aquatic hatcheries, for example, oxytetracycline micro-encapsulated pellets are deployed during specific pathogen outbreaks, commanding prices up to 35% above non-medicated equivalents. Within poultry, coccidiostat-embedded crumble remains prevalent where vaccination coverage is incomplete.

Regulation is steering composition where Europe endorses probiotics, organic acids, and essential oils, while many Asia-Pacific countries still permit low-level antimicrobial inclusion. Multinationals hedge exposure by maintaining diversified ingredient portfolios that can toggle between functional additives and approved pharmaceuticals as laws evolve. Encapsulation and slow-release technologies are increasingly critical, as they enable precise dosage while meeting residue limits and minimizing off-target environmental impact.

By Form: Pellets Disrupt the Traditional Crumble Stronghold

Crumble retained a 41% share in 2024 on the strength of global poultry adoption, and the micro-pellet volumes are rising fastest with an 8.2% CAGR. Micro-pellets typically range from 0.5 mm to 1.2 mm in diameter, delivering higher bulk density and reduced segregation in automated feeders. Extrusion lines such as the ANDRITZ Micro Fluid System allow post-pellet liquid inclusion, enhancing vitamin stability and enzyme activity. Mash persists among cost-focused producers who possess on-farm pelleting capacity, while standard 2-3 mm pellets serve ruminant starters where chewing behavior facilitates mechanical breakdown.

Automation trends heavily influence form choice. Automated nurseries and hatcheries favor consistent pellet geometry to prevent hopper bridging. Consequently, suppliers capable of producing uniform micro-pellets with narrow size distribution and low fines gain preferred-vendor status among integrators shifting toward total precision feeding.

Geography Analysis

Asia-Pacific leads with 37% of the starter feed market size in 2024 and is projected to expand at a 7.3% CAGR to 2030, which is also the fastest-growing region in the market. Starter feed uptake benefits from rising disposable income, urban diet shifts to animal protein, and aggressive expansion of commercial poultry and aquaculture complexes. China’s New Hope Group leads production at 28 million metric tons annually, illustrating scale benefits in ingredient purchasing and research and development. Yet mycotoxin prevalence remains a structural risk, and 88% of regional samples tested positive for at least one toxin, necessitating costly mitigation.

North America ranks second in value, as precision feeding and sustainability certifications take hold. Cargill’s new Animal Nutrition and Health division reflects a pivot toward higher-margin health solutions rather than bulk tonnage. Europe follows, but faces rising compliance costs, and poultry reached USD 3.0 per kg wholesale in March 2025, squeezing feed budgets.

South America posts strong growth, underpinned by Brazil’s projected 5.4 million metric tons poultry export volume in 2025 and feed grain cost advantages. On-farm mixing growth among large integrators limits commercial feed penetration. Middle East and Africa, though smaller in absolute terms, exhibit steady expansion, enabled by government protein self-sufficiency programs and greenfield hatchery investments, albeit tempered by infrastructural and geopolitical challenges.

Competitive Landscape

Market concentration in the starter feed market was moderate, with the major players holding around 40.2% combined share in 2024. Cargill, Incorporated leads with an expansive raw-material network and proprietary digestibility models. ADM follows and faces scrutiny over its Nutrition segment’s accounting practices, potentially limiting near-term investment capacity. Nutreco is leveraging microbiome research through its stake in BiomEdit to deliver differentiated additives. Regionally, Charoen Pokphand Foods PCL and JAPFA Ltd capitalize on local distribution and blockchain traceability to command premiums, while mid-tier players such as De Heus Animal Nutrition expand through targeted plant rollouts in Indonesia.

New Hope Liuhe Co., Ltd, which started its business focusing on animal feed, is now one of China's largest animal feed companies. Selling 15 million metric tons of feeds to 250,000 users annually, it boasts the largest market share and enjoys a tremendous competitive edge in technology and marketing.

Technology adoption is the emerging battleground. Players investing in extrusion, sensor-enabled dosing, and traceability platforms are commanding higher EBITDA multiples than volume-centric peers. M&A activity centers on specialty additive firms and regional producers with established distribution but lacking advanced R&D, indicating ongoing consolidation balanced by localized innovation.

Starter Feed Industry Leaders

-

Cargill, Incorporated

-

ADM

-

Nutreco

-

Chareon Pokphand Foods PCL

-

Land O'Lakes, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: AgroCares and Trouw Nutrition have renewed their NutriOpt On-site Adviser partnership. The collaboration combines Trouw's species-specific nutrient data for swine, ruminants, and poultry with AgroCares' portable NIR scanning technology. This integration enables rapid, on-farm analysis of raw materials and finished feed. The combined database and scanning capabilities support real-time decision-making, improving operational efficiency, sustainability, and financial performance for farmers and feed mills worldwide.

- October 2024: De Heus Animal Nutrition opened its fifth production facility in Purwodadi, Central Java, increasing its monthly production capacity to 15,000 metric tons. The facility strengthens the company's capabilities to provide livestock and aquaculture feed in Central Java and surrounding areas.

- April 2024: Kalmbach Feeds announces over USD 12 million warehouse expansion investment in Ohio, enhancing distribution capabilities and production capacity to meet growing demand for commercial feed. This expansion reflects the company's commitment to regional market leadership and operational efficiency improvements.

Global Starter Feed Market Report Scope

| Poultry | Broiler |

| Layer | |

| Other Poultry | |

| Swine | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Other Animals |

| Medicated |

| Non-medicated |

| Mash |

| Crumble |

| Pellets |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Animal Type | Poultry | Broiler |

| Layer | ||

| Other Poultry | ||

| Swine | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Aquaculture | Fish | |

| Shrimp | ||

| Other Aquaculture Species | ||

| Other Animals | ||

| By Product Type | Medicated | |

| Non-medicated | ||

| By Form | Mash | |

| Crumble | ||

| Pellets | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Thailand | ||

| Vietnam | ||

| Philippines | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected size of the global starter feed market by 2030?

The starter feed market size is projected to reach USD 44.5 billion by 2030.

Which animal segment will grow the fastest through 2030?

Aquaculture starter feeds are forecast to grow at a 9.5% CAGR, the highest among all animal types.

How is regulation affecting medicated starter feeds?

Stringent residue limits and longer approval timelines in the European Union and United States are restricting routine use, yet precision medicated formulations are still expanding at a 7.8% CAGR for targeted disease control.

Which region currently dominates the starter feed market?

Asia-Pacific holds 37% of global revenue and is projected to maintain leadership with a 7.3% CAGR through 2030.

Page last updated on: