Broiler Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

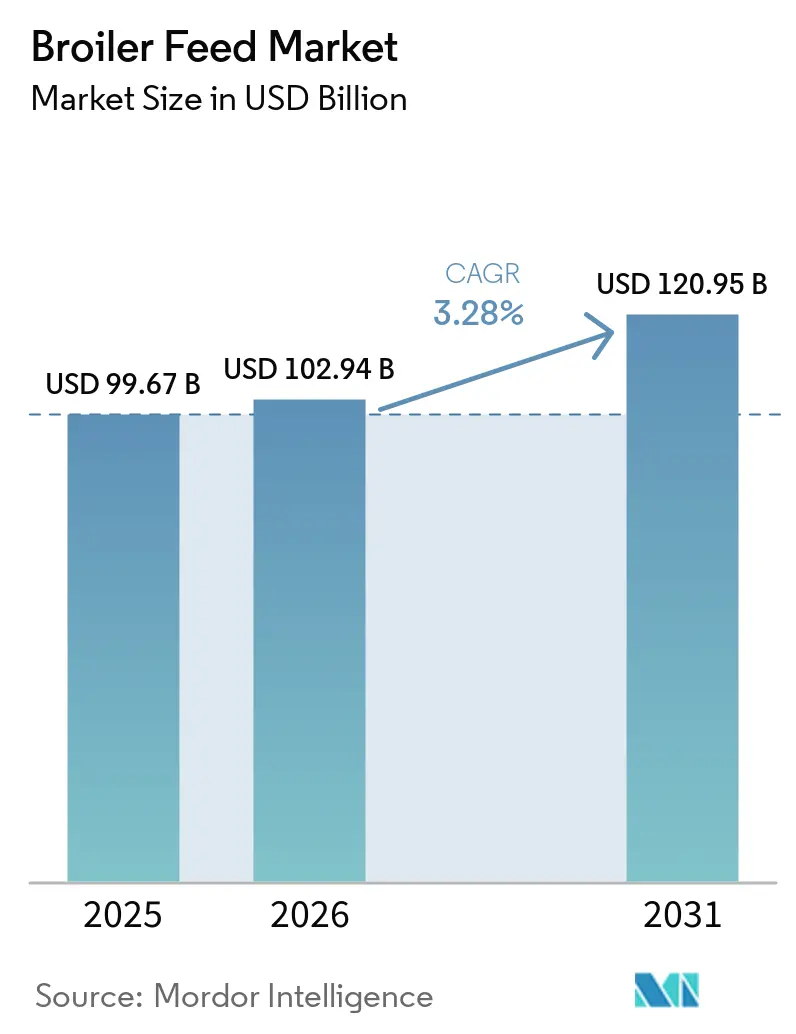

| Market Size (2026) | USD 102.94 Billion |

| Market Size (2031) | USD 120.95 Billion |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Broiler Feed Market Analysis by Mordor Intelligence

The broiler feed market size is anticipated to grow from USD 99.67 billion in 2025 to USD 102.94 billion in 2026 and is forecast to reach USD 120.95 billion by 2031 at 3.28% CAGR over 2026-2031. The broiler feed market remains closely tied to poultry production economics because feed accounted for 60-70% of total broiler production costs, keeping efficiency gains central to supplier selection and farm profitability [1]Source: Frontiers in Animal Science, “Broiler Feed Costs and Production Efficiency,” Frontiers Media SA, frontiersin.org. Global poultry demand continues to support the broiler feed market, as the Organization for Economic Co-operation and Development and the Food and Agriculture Organization's Agricultural Outlook 2025-2034 stated that poultry will account for 62% of additional global meat consumption through 2034 [2]Source: Organisation for Economic Co-operation and Development and Food and Agriculture Organization, “OECD-FAO Agricultural Outlook 2025-2034 – Meat,” OECD Publishing, oecd.org. The broiler feed market is also separating more clearly between suppliers that can deliver measurable performance and those that still compete primarily on commodity pricing, as the adoption of precision nutrition technologies is enabling improvements in feed efficiency, production performance, and feed cost optimization. Recent company actions in 2025 and 2026 show that producers are still investing in scale, integration, and depth of nutrition, with Koninklijke De Heus Voeders B.V., ForFarmers N.V., Coöperatie Koninklijke Agrifirm U.A., and Cargill, Incorporated each making strategic moves across feed and nutrition platforms. At the same time, the broiler feed market faces tighter regulatory pressure on soy sourcing and growing quality risks from climate-linked mycotoxin exposure, pushing buyers toward traceable ingredients, stronger quality control, and higher-value additive programs.

Key Report Takeaways

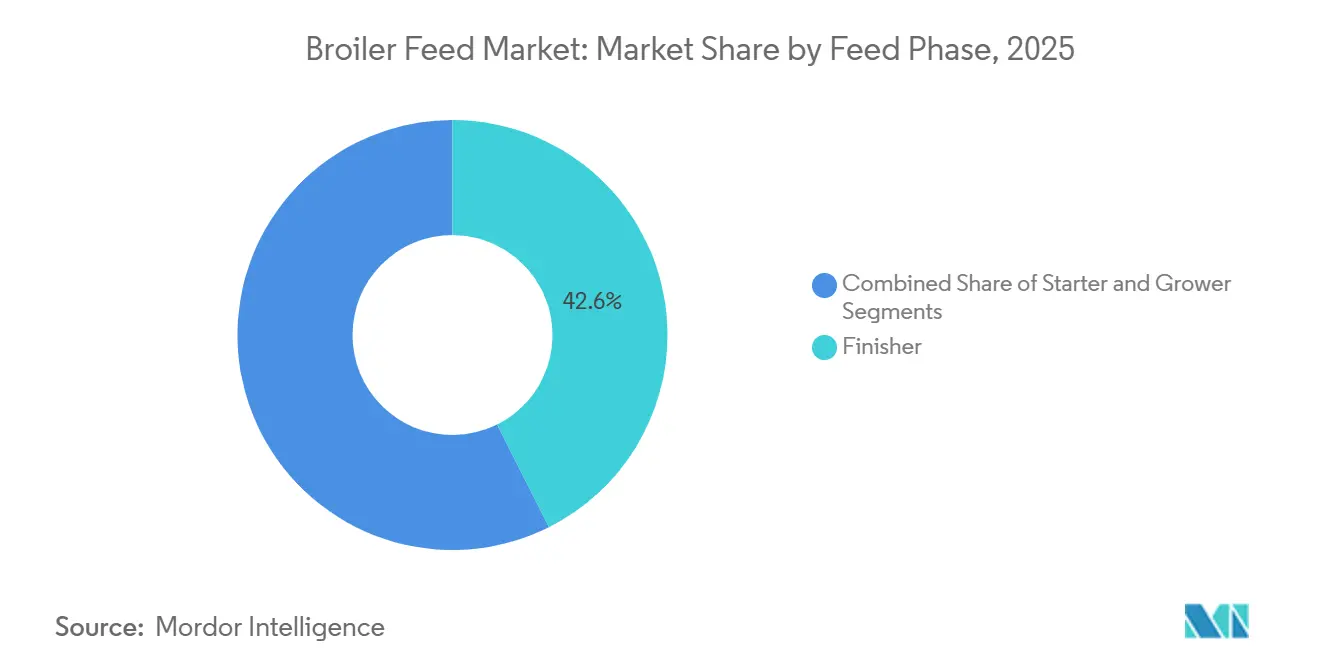

- By feed phase, finisher held the largest share of the broiler feed market with 42.6% in 2025, while starter is projected to register the fastest growth at a 4.1% CAGR during 2026-2031.

- By form, pellets accounted for 55.7% of the broiler feed market size in 2025, whereas crumbles are forecast to expand at a 4.6% CAGR through 2031.

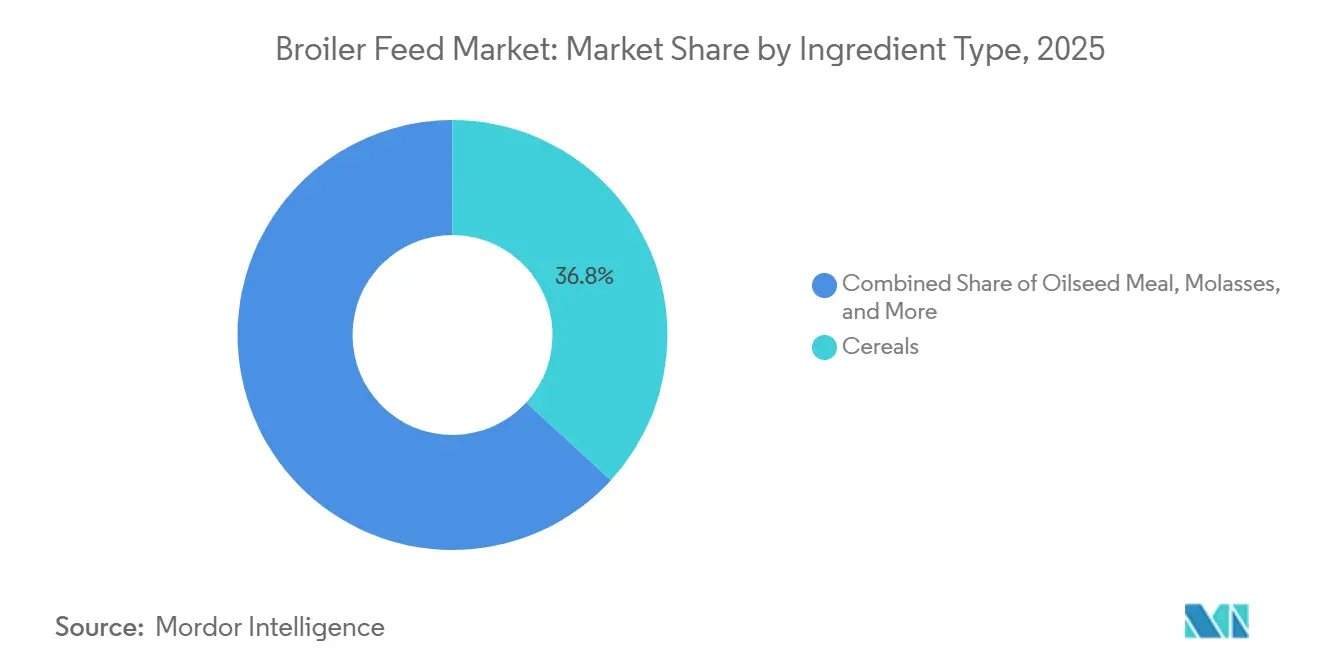

- By ingredient type, cereals emerged as the leading segment with a 36.8% market share in 2025, while additives are anticipated to grow the fastest at a 5.4% CAGR over 2026-2031.

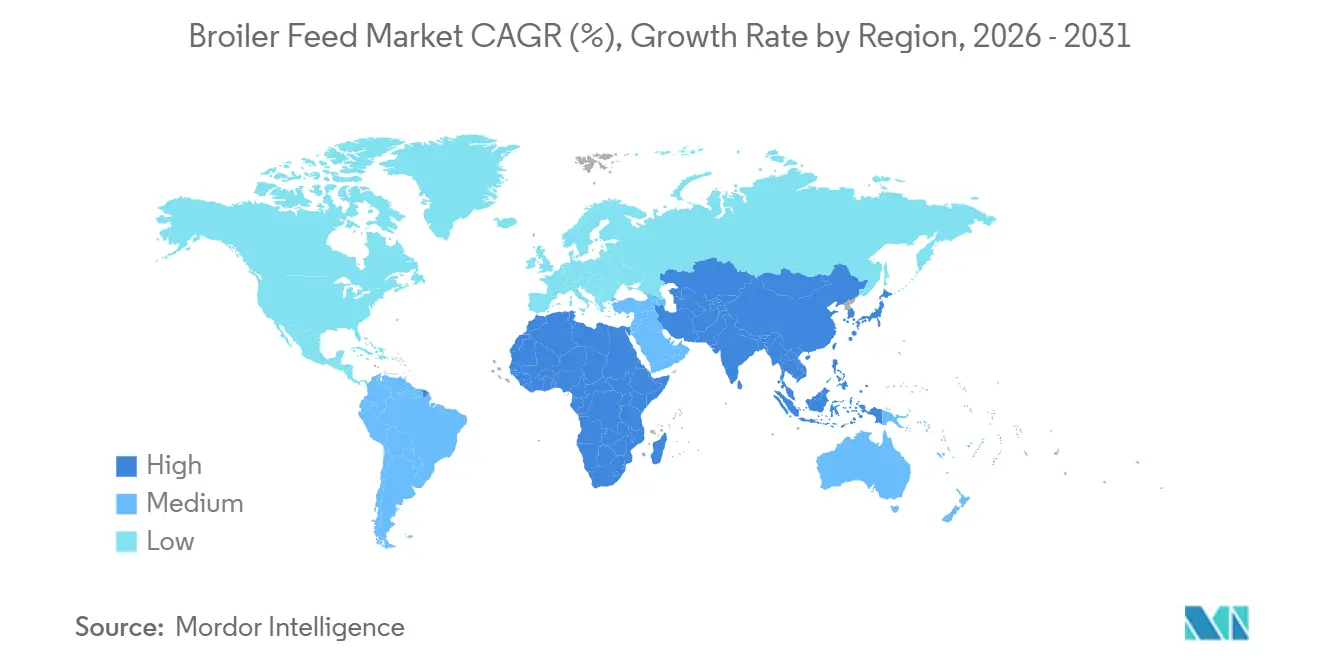

- By geography, Asia-Pacific dominated the broiler feed market in 2025 with a 46.5% share, and it is also projected to remain the fastest-growing regional market at a 4.3% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Broiler Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising poultry meat consumption and protein affordability | +1.20% | Broad global relevance, with stronger pull in Asia-Pacific, Africa, and South America where poultry remains a more affordable animal protein option | Long term (≥ 4 years) |

| Commercial broiler farming expansion and feed outsourcing | +0.90% | Strongest in Asia-Pacific, the Middle East, Africa, and parts of South America as organized poultry farming expands | Medium term (2-4 years) |

| Higher focus on feed conversion and cost efficiency | +0.70% | Global relevance across both mature and developing broiler-producing regions because feed remains the main cost center | Short term (≤ 2 years) |

| Shift toward antibiotic-free and additive-led feed programs | +0.60% | Most visible in Europe and North America, with growing adoption in Asia-Pacific as stewardship frameworks tighten | Medium term (2-4 years) |

| AI-enabled precision nutrition in broiler feed formulation | +0.30% | Higher relevance in markets with stronger technical adoption, including North America, China, Brazil, and Western Europe | Long term (≥ 4 years) |

| Heat-stress mitigation demand for functional feed | +0.20% | Most relevant in hot-climate broiler regions across Asia-Pacific, the Middle East, Africa, and tropical parts of South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Poultry Meat Consumption and Protein Affordability

Poultry meat is expanding its role in global diets, which directly supports demand for broiler feed. The Organization for Economic Co-operation and Development and the Food and Agriculture Organization projected that poultry will account for 62% of additional global meat consumption through 2034, with much of that increase concentrated in developing regions. Poultry also remains one of the more affordable animal proteins, which helps sustain consumption when household food budgets come under pressure. Affordability matters for the broiler feed market because stable meat demand protects feed volumes, even when other proteins face a sharper substitution risk. MHP SE reported nine-month 2025 revenue of USD 2.64 billion, representing a 16% year-on-year increase. The growth was supported by strong poultry demand, stable market pricing, and the consolidation of Spanish poultry producer Grupo UVESA. This trend supports sustained demand for broiler feed, as growing poultry output and capacity expansion require consistent increases in commercial feed consumption.

Commercial Broiler Farming Expansion and Feed Outsourcing

The broiler feed market grows more steadily when poultry production shifts from backyard systems to commercial and contract-based farming. Larger broiler operations depend on standardized compound feed because growth targets, flock uniformity, and processor requirements leave little room for inconsistent farm mixing. Once growers move to integrated or contract models, they usually remain tied to formal feed supply because financing, veterinary support, and buyer agreements are tied to that system. ForFarmers N.V. formed ForFarmers Polska in 2026 by combining feed production with poultry farming and processing, demonstrating how feed is being drawn deeper into organized poultry chains. Koninklijke De Heus Voeders B.V. also widened its position in Asia in March 2026 through the acquisition of CJ Feed and Care, adding 17 feed mills and extending its reach in major poultry-producing markets. These developments support the view that the broiler feed market benefits most when poultry farming becomes larger, more formal, and more dependent on outsourced feed.

Higher Focus on Feed Conversion and Cost Efficiency

Feed efficiency remains one of the most important commercial drivers in the broiler feed market because feed still accounts for the largest share of production cost. Peer-reviewed research published in 2026 in the Frontiers Animals Science showed that feed accounted for 60-70% of total broiler production costs, indicating that even small changes in feed conversion can significantly affect farm profitability. This cost pressure keeps buyers focused on formulations that can convert nutrients into live weight with less waste and more consistency. Research published in Applied Sciences (MDPI) in 2026 also found that phytase, xylanase, amylase, and protease, when used at full matrix specifications, improved nutrient use and enabled lower-cost formulations in broiler diets [3]Source: MDPI Applied Sciences, “Effects of Phytase, Xylanase, Amylase and Protease Inclusion at Full Matrix Specifications in Diets for Broiler Chickens,” MDPI, mdpi.com. That evidence helps explain why the broiler feed market is moving toward products backed by trial data rather than simple ingredient claims. Suppliers that can show better feed conversion ratio performance are in a stronger position to defend pricing and retain larger commercial accounts.

Shift toward Antibiotic-Free and Additive-Led Feed Programs

The broiler feed industry is moving toward more additive-led formulations as antimicrobial controls become stricter across key poultry-producing regions. The European Medicines Agency reported that antimicrobial consumption in food-producing animals in Europe reached its lowest level on record in 2024, confirming the strength of the stewardship shift [4]Source: European Medicines Agency, “Consumption of Antimicrobials in Animals Reaches Lowest Level Ever in Europe,” European Medicines Agency, europa.eu. As antibiotic growth promoters are phased out of routine use, feed formulators need additional tools to maintain gut health, growth, and flock consistency. That change raises the commercial importance of enzymes, probiotics, plant extracts, organic acids, and related functional ingredients in the broiler feed market. The additives segment growth shows that this shift is already becoming visible in spending patterns. The result is a broader move away from simple commodity feed blends toward more specialized nutrition programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corn and soybean meal price volatility | -0.60% | Global relevance because these ingredients remain core to most broiler feed formulas across major producing regions | Short term (≤ 2 years) |

| Tighter antimicrobial-use regulation | -0.20% | Strongest in Europe and North America, with growing spillover into Asia-Pacific as compliance standards expand | Medium term (2-4 years) |

| European Union Deforestation Regulation(EUDR)-linked soy traceability premiums | -0.10% | Highest relevance for Europe-facing feed manufacturers and soy export corridors serving the European Union | Medium term (2-4 years) |

| Climate-driven mycotoxin and ingredient-quality risk | -0.20% | More severe in humid and heat-exposed crop zones, including tropical and subtropical broiler-producing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

European Union Deforestation Regulation (EUDR)-Linked Soy Traceability Premiums

The European Union Deforestation Regulation (EUDR) adds a new compliance layer to the broiler feed market, especially for supply chains with heavy soybean meal exposure. The regulation mandates plot-level traceability for covered commodities and products, with large and medium-sized operators required to comply by December 30, 2026. Non-compliance can result in penalties of up to 4% of an operator's annual European Union turnover. The European Feed Manufacturers' Federation reported disruption risk in the soy trade due to compliance systems that were still not fully ready, creating a tighter, less flexible sourcing environment. These requirements increase documentation costs for exporters and compounders that serve Europe-linked demand. They also make soy procurement less straightforward for mills that lack strong traceability systems. In practical terms, this raises sourcing premiums and encourages the broiler feed market to examine more diversified protein inputs.

Climate-Driven Mycotoxin and Ingredient-Quality Risk

Mycotoxin exposure is becoming a more serious restraint for the broiler feed market as weather volatility affects crop quality across more producing regions. This problem is not limited to visible spoilage, as multiple toxins can be present simultaneously and still reduce flock performance. A 2025 peer-reviewed study published in Poultry Science found that multi-mycotoxin exposure in broilers can impair gut health, weaken immunity, reduce vaccine response, and worsen feed conversion performance. That combination creates hidden cost pressure because birds may perform below target even when ingredient prices look manageable on paper. It also reduces confidence in standard formulations when ingredient quality is inconsistent. As a result, the broiler feed market is putting more commercial value on screening, binders, documentation, and tighter supplier control.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feed Phase: Early-Life Formulations Drive Above-Average Growth

The largest feed phase segment was finisher, which held 42.6% of the broiler feed market share in 2025. This lead reflects the high feed intake during the final growth window, when producers focus on carcass yield and feed efficiency. Commercial broiler systems place strong emphasis on finisher diets because the last stage directly affects saleable output and processing returns. The fastest-growing feed phase segment is the starter, projected to grow at a 4.1% CAGR during 2026-2031. That faster pace shows that more producers now treat early-life nutrition as a performance foundation rather than a basic opening ration.

Starter diets are gaining more attention because gut development, immunity, and nutrient uptake are set early in the production cycle. The grower phase still plays a key balancing role because it connects early development with the high-volume finisher stage. Research published in Poultry Science in 2026 found that β-mannanase supplementation in reduced-energy broiler diets improved nutrient utilization and growth performance, highlighting continued industry interest in enzyme-enabled feed reformulation strategies to maintain productivity while reducing feed costs. This means value growth in the broiler feed market is not limited to higher volumes, but also reflects more precise feeding decisions across each phase. Coöperatie Koninklijke Agrifirm U.A. agreed to acquire Hamlet Protein in March 2026, underscoring that early-life and specialty nutrition remain attractive areas for commercial expansion.

By Form: Pellet Dominance Persists While Crumbles Gain Starter-Phase Momentum

Pellets were the largest form segment, accounting for 55.7% of the broiler feed market in 2025. Their leading position reflects lower waste, stronger feed-handling efficiency, and broader use in large commercial broiler systems. Pellets also fit well with producers' focus on feed conversion ratio because they support more uniform intake and more consistent nutrient delivery. Crumbles are the fastest-growing segment and are projected to advance at 4.6% CAGR during 2026-2031. This faster growth is closely linked to the rising focus on starter nutrition, where a smaller particle size better suits younger birds.

Mash remains relevant in smaller commercial systems and in areas with less developed pelleting infrastructure. It also continues to serve farms that still rely on simpler feed handling practices or mixed feeding approaches. The broiler feed market for crumbles is growing as buyers place greater value on early intake and chick accessibility. Research published in Frontiers in Veterinary Science in 2026 showed that combined lysophospholipid and lipase supplementation maintained broiler performance under energy-restricted feeding conditions, supporting cost control without forcing a change away from established feed forms. Over time, the form mix in the broiler feed market is likely to keep shifting toward pellets and crumbles as commercial farming becomes more standardized.

By Ingredient Type: Additive-Led Value Growth Outpaces Base Ingredients

Cereals accounted for the largest ingredient segment with 36.8% share of the broiler feed market in 2025, reflecting the fundamental role of corn and other grains as primary energy sources in broiler feed formulations. Oilseed meals remained another major ingredient group because soybean meal still provides a large share of protein in commercial rations. The fastest-growing ingredient segment is additives, projected to grow at a 5.4% CAGR during 2026-2031. That pace is well above the overall market rate and shows that value growth in the broiler feed market size is shifting toward performance support rather than just bulk ingredients. This development is reinforcing demand for functional feed additives such as enzymes, probiotics, phytogenics, and organic acids, which are increasingly used to improve digestive performance and optimize nutrient absorption.

Molasses continues to play a niche role in improving feed palatability and binding properties, particularly in certain mash formulations. Fish oil and fish meal remain part of the ingredient mix, although cost and supply constraints continue to drive interest in alternative sources. Emerging proteins and specialty ingredients are also gaining selective adoption as producers seek greater formulation flexibility. Consequently, ingredient selection is increasingly driven by functional performance and production outcomes, reinforcing the shift toward more targeted, value-oriented broiler feed formulations.

Geography Analysis

Asia-Pacific was the largest regional segment with 46.5% of the broiler feed market share in 2025, and it is also the fastest regional segment with a projected 4.3% CAGR during 2026-2031. This position reflects strong poultry demand, rising commercial production, and the broad affordability of chicken across many large population centers. The Organization for Economic Co-operation and Development and the Food and Agriculture Organization outlook support this direction, as much of the added poultry consumption through 2034 is projected to come from Asia and other developing regions. Koninklijke De Heus Voeders B.V. has expanded its Asian platform in March 2026 through CJ Feed and Care, reinforcing that the broiler feed market in the region remains attractive for long-term investment.

South America remains an important region in the broiler feed market because poultry production and feed demand are closely connected to grain and oilseed availability. Brazil remains especially influential because it combines a strong poultry base with a major role in agricultural raw materials tied to feed formulation. Cargill, Incorporated, announced in 2025 a binding offer to acquire Mig-Plus in Brazil, indicating that nutrition companies still see room to deepen their footprint in major producing markets. North America is more mature by volume, so competition there centers more on efficiency, formulation upgrades, and additive performance than on large jumps in feed tonnage. This means the broiler feed market in the Americas combines scale-driven demand in South America with performance-led differentiation in North America.

Europe remains a lower-growth but higher-compliance part of the broiler feed market. The European Union Deforestation Regulation is pushing feed manufacturers to build more traceable soy sourcing systems before the December 30, 2026, deadline. Africa and the Middle East show stronger room for expansion because poultry remains a practical protein source in markets with fast population growth and changing food demand patterns. Hotter climate conditions also make functional and heat-support feed solutions more relevant in these regions, especially where flock performance is exposed to sustained temperature stress. As a result, the broiler feed market exhibits distinct regional priorities, with Asia-Pacific emphasizing production scale, Europe focusing on regulatory compliance, and Africa and the Middle East prioritizing market access, supply chain resilience, and industry formalization.

Competitive Landscape

The broiler feed market remains highly fragmented in 2025, with global manufacturers, regional feed mills, integrated poultry companies, and specialist nutrition players all competing for different buyer groups. No single company defines the field on its own, and competition still depends heavily on local distribution, feed performance, ingredient sourcing, and technical support. Leading participants in the broiler feed market include New Hope Liuhe Co., Ltd., Charoen Pokphand Foods Public Company Limited, Cargill, Incorporated, Koninklijke De Heus Voeders B.V., and Land O'Lakes, Inc. The presence of both multinational suppliers and strong domestic operators keeps pricing and customer loyalty highly regional. This is why the broiler feed market still rewards operational reach and product consistency as much as raw scale.

Recent strategic moves show that leading companies are strengthening their positions through acquisitions and integrated operating models. Koninklijke De Heus Voeders B.V. completed its acquisition of CJ Feed and Care in March 2026, adding 17 mills and expanding access across several important Asian livestock markets. Coöperatie Koninklijke Agrifirm U.A. agreed to acquire Hamlet Protein in March 2026, thereby strengthening its specialty nutrition capabilities in young-animal feeding. ForFarmers N.V. formed ForFarmers Polska in February 2026 through a transaction that more closely linked compound feed with poultry farming and food processing in Poland. Cargill, Incorporated also moved to expand in Brazil in 2025 through its binding offer for Mig-Plus, showing that product depth and geographic reach remain central themes in the broiler feed market.

The next layer of competition is forming around measurable nutrition outcomes rather than simple ingredient supply. Suppliers that can pair compound feed with feed conversion data, early-life support, traceability, and regulatory readiness are better placed to defend margins. This matters even more as artificial intelligence-enabled formulation, antibiotic-free feeding, and mycotoxin control become more important purchasing criteria in the broiler feed market. Large players have an advantage because they can spread research, compliance, and technical service costs across wider networks. Smaller firms can still compete effectively when they are strong in local relationships, phase-specific nutrition, or specialty additives. Overall, the broiler feed market is staying competitive because buyer needs vary sharply by region, farm scale, and production model.

Broiler Feed Industry Leaders

New Hope Liuhe Co., Ltd.

Charoen Pokphand Foods Public Company Limited

Cargill, Incorporated

Koninklijke De Heus Voeders B.V.

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Koninklijke De Heus Voeders B.V. completed the acquisition of CJ Feed and Care, gaining 17 feed mills and livestock operations across Vietnam, Indonesia, and Cambodia, and marking new market entries into Korea and the Philippines. This is among the largest single feed-sector acquisitions in Asia in recent years and materially expands De Heus's position in the broiler feed segment of the region's fastest-growing markets.

- March 2026: Coöperatie Koninklijke Agrifirm U.A. agreed to acquire Hamlet Protein, a global leader in specialty soy-based protein ingredients for young animal nutrition, with production facilities in Denmark and the United States and a sales presence in China. The deal strengthens Agrifirm's Specialties business by introducing early-life nutrition concepts that directly address premiumization trends in starter feed across the global broiler feed market.

- February 2026: ForFarmers N.V. formed ForFarmers Polska through a joint venture with KPS Food Group, merging its Tasomix affiliate with KPS's poultry production, slaughtering, and food processing business. The combined entity carries an enterprise value of USD 558 million (PLN 2,192 million), with ForFarmers holding a 50.5% controlling stake and full consolidation. The venture integrates compound feed production, poultry farming, and processing into a single entity, reflecting a shift toward vertical integration in the Polish poultry feed market.

Global Broiler Feed Market Report Scope

Broiler feed refers to nutritionally balanced feed formulations for chickens raised for meat, including starter, grower, and finisher diets in pellet, crumble, mash, and other forms.

The Broiler Feed Market Report is Segmented by Feed Phase (Starter, Grower, and Finisher), by Form (Pellets, Crumbles, Mash, and Others), by Ingredient Type (Cereals, Oilseed Meal, Molasses, Fish Oil and Fish Meal, Additives, and Other Ingredient Types), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Starter |

| Grower |

| Finisher |

| Pellets |

| Crumbles |

| Mash |

| Others |

| Cereals |

| Oilseed Meal |

| Molasses |

| Fish Oil and Fish Meal |

| Additives |

| Other Ingredient Types |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Feed Phase | Starter | |

| Grower | ||

| Finisher | ||

| By Form | Pellets | |

| Crumbles | ||

| Mash | ||

| Others | ||

| By Ingredient Type | Cereals | |

| Oilseed Meal | ||

| Molasses | ||

| Fish Oil and Fish Meal | ||

| Additives | ||

| Other Ingredient Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the market size of the broiler feed market in 2026, and what value is it projected to reach by 2031?

The broiler feed market is forecast to reach USD 120.95 billion by 2031, rising from USD 102.94 billion in 2026.

Which feed phase leads revenue generation in broiler nutrition?

Finisher is the largest feed phase segment, with 42.6% share of the broiler feed market in 2025, because birds consume the highest feed volumes during the final growth stage.

Which form is expanding the fastest in broiler diets?

Crumbles are the fastest form segment, with a projected 4.6% CAGR during 2026-2031, largely due to stronger use in starter feeding.

Why are additives growing faster than other ingredient groups?

Additives are projected to grow at 5.4% CAGR during 2026-2031 because producers need more gut health, efficiency, and antibiotic-free performance support.

Which region leads global demand for broiler feed?

Asia-Pacific is the largest region with 46.5% share of the broiler feed market in 2025 and is also the fastest regional segment, with a projected 4.3% CAGR during 2026-2031.

What are the main risks affecting feed manufacturers and broiler producers?

The main risks are corn and soybean meal price volatility, tighter antimicrobial rules, soy traceability costs linked to the European Union Deforestation Regulation, and climate-driven mycotoxin exposure.

Page last updated on: