Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

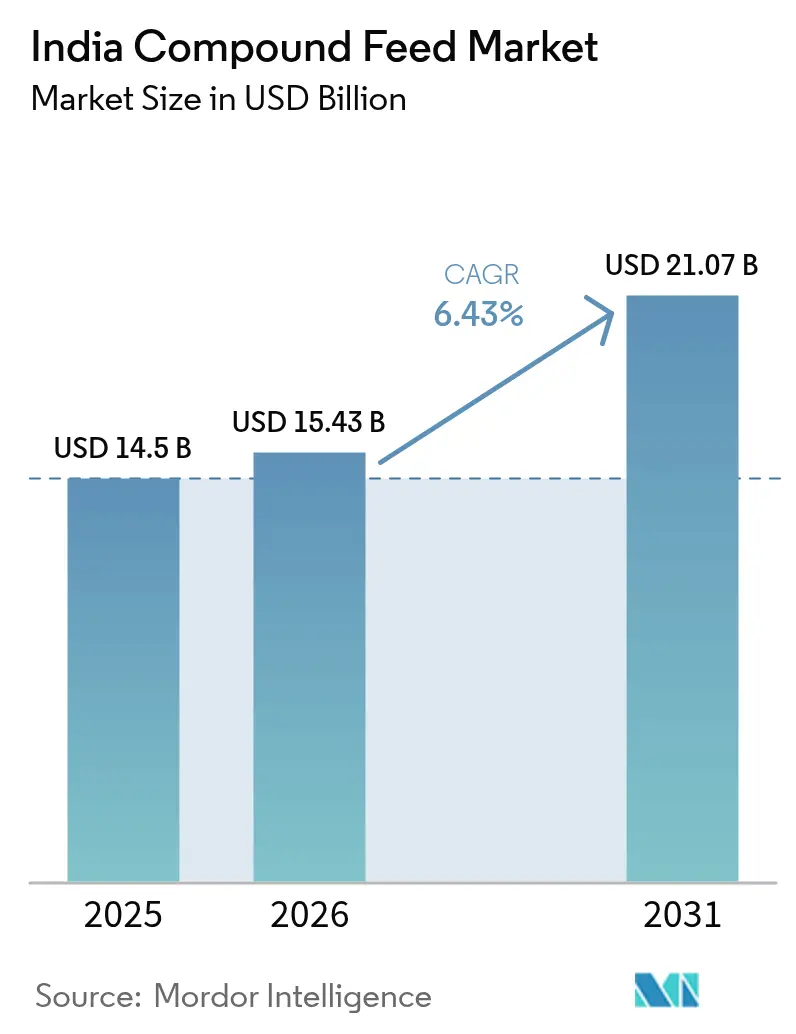

| Base Year Market Size (2025) | USD 14.5 Billion |

| Market Size (2026) | USD 15.43 Billion |

| Market Size (2031) | USD 21.07 Billion |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Compound Feed Market Analysis by Mordor Intelligence

India compound feed market size in 2026 is estimated at USD 15.43 billion, growing from 2025 value of USD 14.5 billion with 2031 projections showing USD 21.07 billion, growing at 6.43% CAGR over 2026-2031. Livestock population growth, rising urban demand for meat and dairy, and supportive policy incentives are steering producers away from farm mixed rations toward industrial formulations. Maize price inflation and stricter feed safety norms are reshaping ingredient strategies, while the proliferation of precision‐feeding technologies offers measurable efficiency gains. Consolidation momentum is visible as larger players leverage scale, technology, and integrated supply chains to defend margins and capture new customers. Export-oriented aquaculture and branded poultry products add further upside by broadening the scope of value-added nutrition solutions.

Key Report Takeaways

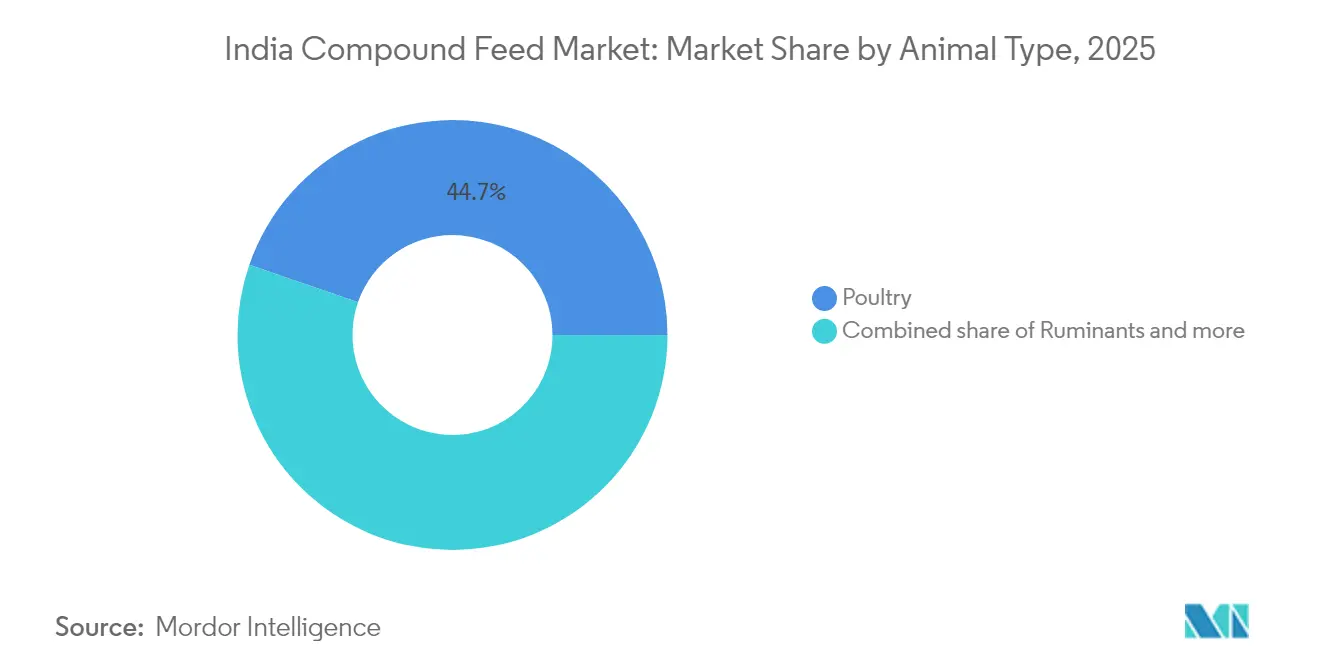

- By animal type, poultry held 44.70% of the India compound feed market share in 2025, and aquaculture feed is projected to expand at a 9.12% CAGR to 2031.

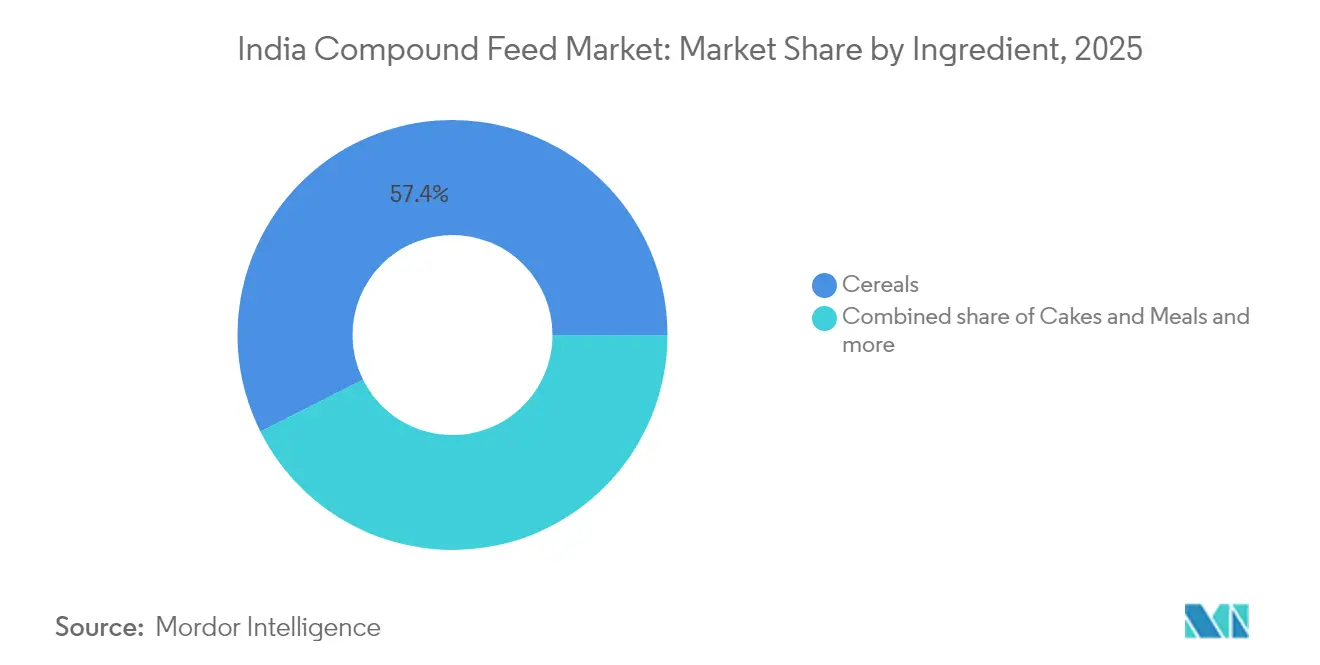

- By ingredient, cereals accounted for 57.40% of the India compound feed market size in 2025, while supplements are advancing at an 8.05% CAGR through 2031.

- The top five manufacturers together accounted for a significant share of the India compound feed market in 2024, reflecting a moderately concentrated market structure

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Compound Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising livestock population | +1.2% | Uttar Pradesh, West Bengal,and Bihar | Medium term (2-4 years) |

| Increasing demand for animal-based products | +1.5% | South and West India urban hubs | Short term (≤ 2 years) |

| Government support and initiatives | +0.8% | AHIDF beneficiary states nationwide | Long term (≥ 4 years) |

| Growth of organized retail meat and dairy in tier-II cities | +0.9% | Maharashtra, Karnataka, and Tamil Nadu | Medium term (2-4 years) |

| Adoption of precision feeding technologies (IOT-enabled) | +0.6% | Punjab, Haryana, and Gujarat | Long term (≥ 4 years) |

| Expansion of domestic oilseed processing capacity | +0.7% | Madhya Pradesh, Maharashtra, and Karnataka | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Livestock Population

The growth of India's livestock population, particularly in poultry and dairy cattle, drives the demand for compound feeds as traditional grazing and crop residue feeding cannot meet nutritional requirements. The poultry sector anticipates 8-10% annual revenue growth, driven by broiler flock expansion and layer productivity improvements that require scientifically formulated feeds. This transition is prominent in states like Uttar Pradesh and West Bengal, where smallholder farmers are moving from subsistence to commercial livestock operations. The shift intensifies as urbanization reduces grazing land availability, compelling producers to adopt intensive feeding systems. Government livestock census data shows consistent herd growth across multiple species, with dairy cattle and poultry demonstrating the highest expansion rates. The combination of higher stocking densities and improved genetic potential in modern livestock breeds requires precision nutrition that compound feeds provide.

Increasing Demand for Animal-Based Products

The increasing protein consumption in India, particularly in urban and tier-II markets, is driving the demand for compound feeds as livestock producers aim to increase animal productivity. India's per capita egg availability rose to 103 eggs per person per year in 2023-24, an increase from 101 eggs in 2022-23[1]Source: National Egg Coordination Committee, “Egg Industry Overview 2024,” NECC, neccegg.com . Total egg production grew to 142.77 billion eggs in 2024, showing a 3.18% increase from the previous year 2023 [2]Source: U.S. Department of Agriculture Foreign Agricultural Service, “India Livestock and Products Annual 2024,” fas.usda.gov. South and West India demonstrate strong demand growth, supported by organized retail networks and cold-chain infrastructure that facilitate animal product distribution. Younger consumers show increased preference for animal proteins, indicating a shift from traditional consumption patterns. The export market for processed meat and dairy products contributes to higher domestic production requirements. Rising disposable income in tier-II cities has created consumer segments prioritizing food quality and safety, leading to increased adoption of quality compound feeds among commercial producers.

Government Support and Initiatives

The India government's policy frameworks, including the Animal Husbandry Infrastructure Development Fund (AHIDF) and reduced import duties on feed ingredients, support the compound feed market's growth through improved access to capital and raw materials. The AHIDF has facilitated the establishment of 372 registered feed manufacturing facilities across India, particularly in states focused on livestock development. The Bureau of India Standards (BIS) codes ensure uniform labeling standards, enabling buyers to evaluate nutritional quality effectively. The Food Safety and Standards Authority of India's (FSSAI) implementation of strict contaminant limits has led feed mills to establish in-house laboratories and implement hazard analysis protocols. These regulatory measures reduce operational barriers, facilitate technology adoption, and support expansion strategies in the India compound feed market[3]Source: Food Safety and Standards Authority of India, “Advisories / Orders,” FSSAI, fssai.gov.in .

Growth Of Organized Retail Meat and Dairy In Tier-II Cities

Emerging metro clusters such as Coimbatore and Indore are witnessing rapid cold-chain deployments that lengthen product shelf life and widen sourcing radii. Retail chains issue supplier scorecards on parameters such as feed traceability, residue compliance, and animal welfare, encouraging smallholders to adopt commercial rations. Milk cooperatives are rolling out bonus schemes for higher fat and protein percentages achievable only with balanced dairy concentrates. Poultry integrators contract local broiler farmers on cost-plus terms, embedding feed protocols into grow-out contracts and guaranteeing offtake. As organized retail deepens penetration, uniform feed standards transition from optional to mandatory across supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High costs of raw materials | -1.8% | Grain-deficit states nationwide | Short term (≤ 2 years) |

| Limited awareness among small-scale farmers | -1.2% | Eastern and Central India | Long term (≥ 4 years) |

| Stricter antibiotic-free regulations are elevating formulation cost | -0.9% | Export-oriented clusters | Medium term (2-4 years) |

| Climate-linked supply chain volatility | -0.7% | Rain-fed crop belts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Costs of Raw Materials

The volatile pricing of key feed ingredients, particularly maize and soybean meal, creates margin pressure for feed manufacturers and affordability challenges for livestock producers. This volatility potentially limits compound feed adoption among price-sensitive segments. Maize prices have exceeded Rs 26 per kg compared to historical ranges of Rs 20-22 per kg, representing a 20-25% cost increase that directly impacts feed formulation economics and end-user adoption rates. Feed producers must either absorb costs or transfer them to farmers with limited resources. While some mills attempt to reformulate using broken rice and sorghum, the reduced digestibility often negates any cost savings. Dairy cooperatives implement price caps on compound feed to retain members, forcing manufacturers to operate on reduced margins. Additionally, spot shortages lead to speculative hoarding, which causes further price increases and reduces confidence among smallholder farmers.

Limited Awareness Among Small-Scale Farmers

Limited understanding of compound feed benefits and proper feeding practices among small-scale livestock farmers restricts market growth, especially in areas where traditional feeding methods prevail and agricultural support services are limited. Many farmers prefer using farm-mixed feeds or crop residues, perceiving compound feeds as costs rather than investments in productivity. This knowledge gap is significant in Eastern and Central India, where agricultural support systems have minimal reach, and demonstrating compound feed advantages requires continuous education initiatives. Small, scattered farm operations make individual farmer education costly for feed manufacturers. Rural literacy levels and language differences also hinder the spread of technical information about feed formulations and usage. These factors result in reduced livestock productivity and restrict the potential market for compound feed manufacturers, particularly in regions with substantial livestock populations but low commercial feed usage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Poultry Maintains Top Billing, Aquaculture Accelerates

The poultry segment captured 44.70% of the India compound feed market share in 2025, reflecting its dominance in organized protein supply chains. Feed manufacturers offer breed-specific starter, grower, and finisher rations, each fortified with enzymes and synthetic amino acids to optimize feed conversion. Consumption growth aligns with quick-service restaurant expansion, prompting integrators to secure long-term grain contracts.

The India compound feed market size for aquaculture is projected to surge at a 9.12% CAGR through 2031 on the back of shrimp export momentum and government subsidies for pond aeration equipment. Rising disease pressures in intensive ponds are steering farmers toward floating extruded pellets enriched with immune boosters. Technologically advanced mills nowadays produce micro-pellets tailored for larval stages, improving survival rates in hatcheries. Dairy feed adoption remains mixed, organized cooperatives procure compound concentrates, but many smallholders in milk belts still rely on green fodder and oil-cake mixes. Swine feed demand stays regional, concentrated in northeastern states where pork is culturally accepted. Niche growth pockets include meat goat feed in Rajasthan and sheep fattening pellets in Telangana, each reflecting the adaptive breadth within the India compound feed market.

By Ingredient: Cereals Foundation with Supplements on the Fast Track

Cereals contributed 57.40% to the 2025 ingredient mix, with maize as the primary energy source thanks to favorable starch profiles. High spot prices, however, prompt rations to incorporate broken rice and sorghum to defend gross margins. Cakes and meals stand as the second-largest category owing to soybean meal’s high lysine content, and domestic crushers are upgrading facilities to deliver low-urease, high-protein variants. Supplements, although a smaller volume slice, log the fastest 8.05% CAGR, fueled by phytogenic additives and encapsulated vitamins that align with antibiotic-free positioning.

Alternative proteins are emerging. Arthro Biotech’s European Union-certified black soldier fly meal offers a digestible, sustainable option for the aqua and pet segments. Enzyme blends targeted at non-starch polysaccharides are gaining traction as mills reformulate to include higher fiber cereals. By-products such as rice bran and wheat offal hold relevance for ruminant rations, particularly where cost sensitivities curtail inclusion of premium ingredients. Ingredient diversification hedges against climatic shocks and currency swings, strengthening supply resilience across the India compound feed market.

Geography Analysis

North India remains the single largest territory for compound feeds, thanks to dense dairy cooperatives in Uttar Pradesh and large broiler integrators in Punjab. Proximity to grain belts ensures steady maize availability, while strong road networks facilitate inter-state trade. West India is expanding the fastest, with Maharashtra’s organized dairy and Gujarat’s shrimp feed operations lifting regional CAGR to 7.18%. Port access through Mumbai and Kandla eases soybean meal and additive imports, bolstering feed quality standards.

South India’s Andhra Pradesh and Tamil Nadu combine sizable aquaculture zones with vibrant poultry clusters, generating a balanced demand mix. Biotechnology hubs in Bengaluru supply enzymes and probiotics, fostering innovation and local sourcing efficiencies. East India lags in per-animal feed adoption due to fragmented landholdings. West Bengal’s sizable livestock base signals growth potential once awareness programs and credit lines deepen. Climate vulnerability runs highest in rain-fed eastern states, where supply disruptions during heavy monsoons often push feed costs upward.

Regional competition is intensifying as new mills spring up closer to consumption centers, reducing freight costs and enhancing pellet freshness. State government incentives, such as electricity tariff concessions and capital subsidies, are spurring capacity additions in Odisha and Rajasthan. Consequently, the India compound feed market is evolving into a mosaic of regional hubs, each capitalizing on local crop patterns, livestock densities, and policy levers to reinforce feed security.

Regulatory Landscape

India’s compound feed sector works under a mix of food safety oversight and product standards, with the Food Safety and Standards Authority of India (FSSAI) directing animal feed businesses toward Bureau of Indian Standards (BIS) specifications for quality and contaminant control. BIS standards such as IS 2052:2023 for compounded cattle feed set formulation and safety expectations, including limits on contaminants such as aflatoxin B1 (20 ppb), and these requirements are reinforced by feed mills building in-house testing and hazard-control protocols to meet residue and contaminant expectations.

Beyond national standards, state-level regulation is becoming more explicit. The Karnataka Animal Feed (Regulation of Manufacture and Quality Control) Act, 2025 (assented on April 5, 2025) establishes a licensing and inspection framework for animal feed manufacturers in the state, increasing compliance focus for companies selling into or operating facilities within Karnataka. Separately, court scrutiny around the mandatory nature of BIS compliance for feed, including litigation such as Godrej Agrovet Ltd v. Union of India, adds an execution variable, and manufacturers are responding by keeping documentation, testing, and traceability systems ready for tighter enforcement scenarios.

Value Chain Analysis

The India compound feed value chain begins with procurement of cereals and protein meals, where cereals form the core of rations, and it is supported by vitamins, enzymes, amino acids, and other additives. Higher-purity inputs, including those routed through major gateways such as Mumbai/Nhava Sheva and Chennai, feed into formulation and processing at specialized mills that produce pelleted formats and, increasingly for aquaculture, extrusion. From there, product reaches poultry, dairy, aquaculture, and niche livestock producers through direct-to-integrator supply, dealer networks, and cooperative channels.

Key bottlenecks are tied to ingredient price volatility and availability, particularly for maize and soybean meal, which can tighten working capital and increase the premium on storage, sourcing diversification, and formulation flexibility through alternative cereals or by-products. Downstream, integrated poultry and organized dairy chains are embedding feed protocols into contracting and procurement scorecards, which rewards mills that can provide consistent pellet quality, contaminant testing, and batch traceability. Capacity additions and footprint optimization are also visible in North India, where companies expand closer to large dairy and poultry clusters to reduce freight costs and improve service reliability for time- and freshness-sensitive feeds.

Competitive Landscape

India compound feed market demonstrates moderate concentration. Godrej Agrovet leverages vertically integrated operations spanning oilseed crushing to processed chicken retail, enabling tight control over feed quality and margins. Cargill India focuses on high-performing poultry and aqua diets, banking on global R&D capabilities to localize formulations rapidly. Regional challenger Suguna Foods differentiates through contract farming models that bundle feed, chicks, and veterinary support into turnkey packages.

Mergers and acquisitions underscore consolidation dynamics. The India Poultry Alliance’s March 2025 takeover of Kwality Animal Feeds for Rs 300 crore (USD 36 million) expanded captive capacity in northern states and unlocked cross-selling opportunities. Precision feeding startups partner with established mills, integrating cloud analytics into existing extrusion lines to enhance formulation accuracy. Compliance with the Food Safety and Standards Authority of India's (FSSAI) residue norms and Bureau of Indian Standards (BIS) creates entry barriers that favor capital-rich incumbents while elevating industry professionalism.

Competitive thrust now centers on functional additives, eco-friendly packaging, and on-farm advisory services that embed suppliers deeper into customer value chains. Blockchain pilots for feed traceability attract premium buyers in export corridors. Mills that can guarantee mycotoxin-safe corn and antibiotic-free status stand to gain retail shelf space and export contracts, raising the bar for market participation across the India compound feed market.

India Compound Feed Industry Leaders

Godrej Agrovet Limited

Cargill Incorporated

Suguna Group

PT Japfa Comfeed Indonesia Tbk

Nutreco N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The most tangible opportunities in India compound feed lie in formalization and quality differentiation, as tighter standards and buyer requirements shift demand toward branded, tested, and traceable feed. BIS specifications such as IS 2052:2023 for compounded cattle feed, alongside FSSAI-led enforcement of contaminant controls, are pushing mills to build laboratory capability for mycotoxin risk management and to strengthen documented quality systems. This creates room for suppliers of premixes, enzymes, probiotics, and toxin binders that align with antibiotic-free positioning. In aquaculture, Coastal Aquaculture Authority (CAA) standards on effluent and antibiotic restrictions raise the value of specialized, performance-oriented formulations and compliance-ready production.

Investment-backed capacity and infrastructure programs offer a clearer route for expansion, particularly for players able to translate credit and subsidy access into localized manufacturing and procurement hubs. Policy support through Department of Animal Husbandry and Dairying programs such as the National Livestock Mission, and financing routes such as the Animal Husbandry Infrastructure Development Fund, links feed growth with fodder development, silage, and modern storage, improving raw material resilience. Recent corporate actions reinforce how modern capacity near consumption belts is becoming central to competitive positioning, including Cargill’s dairy feed expansion in Punjab, which increases competition and service-level expectations in organized dairy regions and encourages adjacent players to respond with regional plants, distribution upgrades, and differentiated dairy concentrates.

Recent Industry Developments

- February 2026: Cargill inaugurated a dairy feed plant in Wazirabad, Punjab, with annual capacity of 400,000 metric tons and an investment reported around INR 300 crore. The commissioning strengthens localized supply for dairy clusters in North India and raises the competitive benchmark on scale, quality systems, and service levels in commercial cattle feed.

- March 2025: Indian Poultry Alliance completed the acquisition of Kwality Animal Feeds for Rs 300 crore (USD 36 million), adding 0.4 million metric tons of annual pelleting capacity and a distribution footprint across 12 states. The deal increased consolidation momentum and improved the acquirer’s ability to balance raw-material procurement with captive manufacturing and cross-selling across poultry feed channels.

- August 2024: Godrej Agrovet acquired the remaining 49% stake in Godrej Tyson Foods, tightening integration from feed through processed poultry. The move supports closer alignment between feed specifications and branded poultry requirements, reinforcing demand for consistent, traceable formulations in organized supply chains.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers commercially produced compound feed sold in India for livestock and aquaculture, where multiple ingredients are blended to match species and growth-stage nutrition needs.

Scope exclusions: It does not count on-farm feed mixing, raw grains and oilseed meals sold as single ingredients, or veterinary supplements sold as standalone products.

Segmentation Overview

- By Animal Type

- Ruminants

- Poultry

- Swine

- Aquaculture

- Other Animal Types

- By Ingredient

- Cereals

- Cakes and Meals

- By-Products

- Supplements

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping how feed is produced and consumed in India, and by listing the demand pools that drive compound feed purchases across species. We used public datasets and references such as Department of Animal Husbandry and Dairying releases, FAOSTAT time series, APEDA trade statistics, the Directorate General of Commercial Intelligence and Statistics (DGCIS) import-export tables, and peer-reviewed animal nutrition journals to anchor production and raw material signals.

To translate those signals into market value, we also reviewed company annual reports, investor presentations, and credible press coverage for capacity additions, pricing commentary, and product-mix cues. In parallel, we used a paid subscription that aggregates company financials and another that tracks shipment-level trade flows selectively to cross-check the direction of revenue and commodity-linked cost movements that affect feed pricing. These examples are not exhaustive, and we used other public references as well for collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were used to test what desk research cannot show clearly, especially the split between organized feed sales and informal feeding, and how prices move when corn and soymeal change. We spoke with manufacturers, distributors, integrators, and large farm operators to confirm usage patterns, typical feed forms, and procurement behavior across key producing states and demand clusters.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | |

| Mid tier: 52% | Functional/Unit leaders: 33% | |

| Smaller Players: 14% | Managers: 55% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where livestock output and feed demand indicators were reconstructed into a yearly compound feed consumption pool, then valued using representative price bands by species and form. To keep the model grounded, we checked results using selective bottom-up approximations, such as rolling up a sample of supplier revenues, and running volume x average selling price checks at the species level before final totals.

Key inputs (illustrative) included poultry and milk output trends, aquaculture production signals, feed conversion and inclusion rates shared by industry practitioners, shifts in pellet versus mash usage, and raw material price direction for major inputs like corn and oilseed meals. Where data was patchy, we filled gaps using bounded assumptions that were confirmed in interviews, then stress-tested using alternate price and adoption cases. Forecasting relied on scenario analysis supported by short series smoothing for pricing, and it was adjusted with expert views on protein demand, integration levels, and policy and quality compliance trends that influence organized feed penetration.

Data Validation & Update Cycle

Outputs were validated in multiple steps, starting with consistency checks against independent signals like livestock production, trade flows for key feed inputs, and capacity announcements. Outliers were reviewed, assumptions were revisited, and follow-up calls were triggered when pricing, penetration, or volume narratives did not align across sources.

Before sign-off, the model is reviewed by another analyst focusing on year-over-year movements, unit logic, and boundary conditions so the numbers remain explainable. Reports are refreshed annually, and interim updates are done when a material event changes feed demand or pricing direction, followed by a final pre-delivery check to ensure clients receive the latest view.

Mordor Intelligence's India Compound Feed Market Estimate Compared With Other Published Estimates

Published numbers for India compound feed can differ because the boundary is not always the same, and the value can shift depending on whether informal feeding is counted, how feed additives are treated, and which year and currency timing are used.

Trade-linked raw material movement, livestock output trends, and cross-checks from manufacturer capacity and revenue direction are the evidence points that tie Mordor Intelligence's estimate to a defined demand pool, rather than letting mixed scopes inflate or compress the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.5 B (2025) | |

| Global Consultancy A | USD 14.8 B (2026) | Uses a different reference year and a wider scope that can bundle additives and broader feed forms, which can lift value even if underlying volume growth is similar. |

| Publisher B | USD 14.34 B (2024) | Reported under an animal feed umbrella where category boundaries can mix compound feed with adjacent feed products, and the base-year choice can pull the value down or up versus a 2025 starting point. |

The spread across the three figures is mainly explained by year selection and what gets counted as compound feed versus neighboring categories. By keeping the scope tied to commercial compound feed sold in India and by using repeatable checks on demand and pricing drivers, the final number stays transparent and easier to reconcile when new data points arrive.

Key Questions Answered in the Report

How fast is the India compound feed market anticipated to grow through 2031?

The India compound feed market is projected to register a 6.43% CAGR, advancing from USD 15.43 billion in 2026 to USD 21.07 billion by 2031.

Which animal type currently uses the largest share of compound feed?

Poultry accounts for 44.70% of feed sales thanks to intensive broiler and layer operations across major producing states.

Why are supplement ingredients gaining traction in feed formulations?

Supplements log an 8.05% CAGR because probiotic, enzyme, and vitamin additives help producers comply with antibiotic-free regulations while boosting feed efficiency.

How are government policies influencing the feed sector?

Subsidized credit under the Animal Husbandry Infrastructure Development Fund and duty relief on select inputs encourage mill expansion and lower production costs, supporting broader market growth.

Page last updated on: