Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 613.9 Billion |

| Market Size (2031) | USD 748.27 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

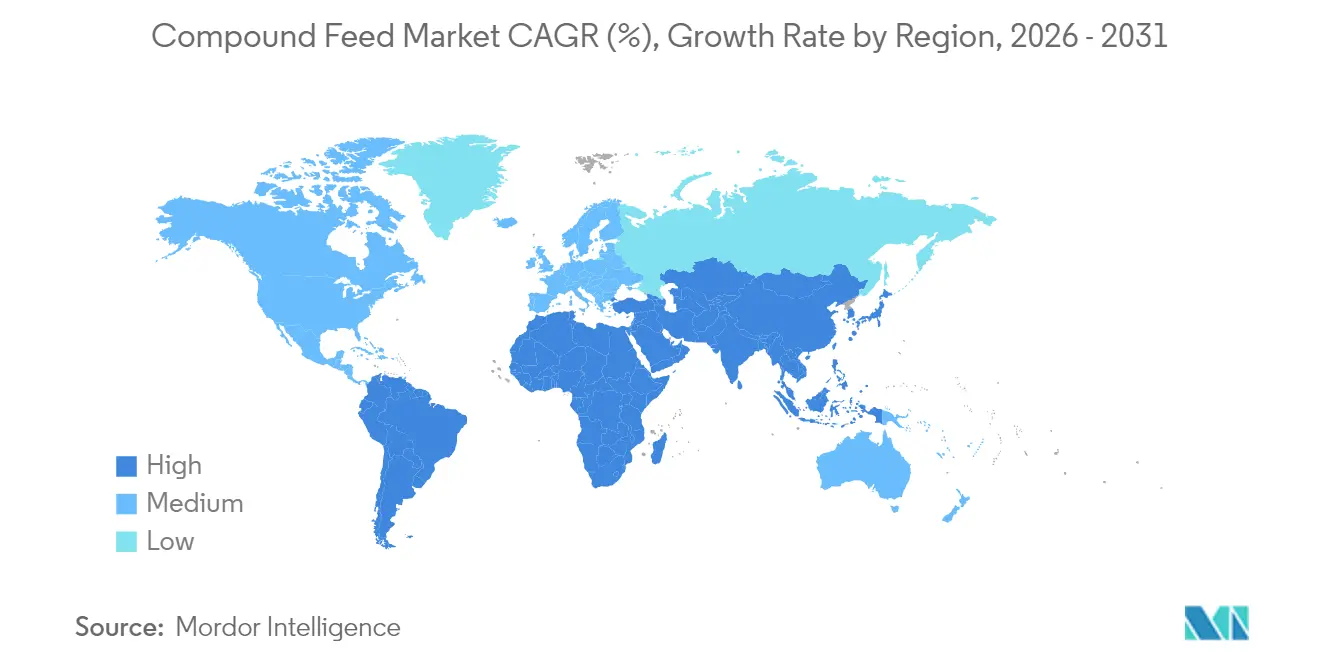

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

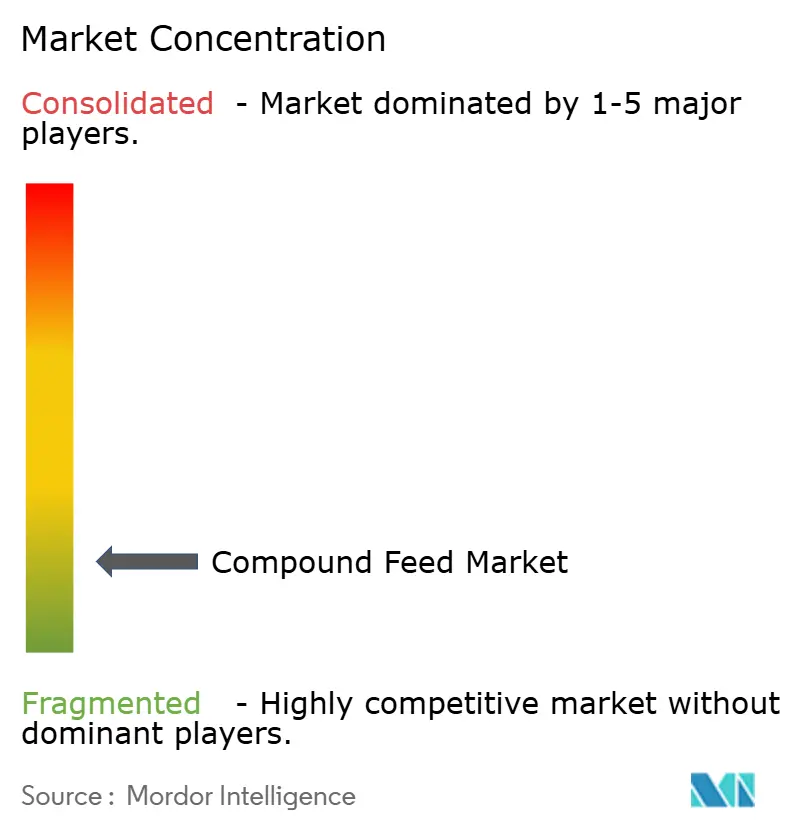

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compound Feed Market Analysis by Mordor Intelligence

The compound feed market size was valued at USD 590 billion in 2025 and estimated to grow from USD 613.9 billion in 2026 to reach USD 748.27 billion by 2031, at a CAGR of 4.05% during the forecast period (2026-2031). Demand is buoyed by rising global meat and fish consumption, rapid industrialization of livestock, and the spread of precision nutrition technologies that reduce waste and boost profits. The increasing use of artificial intelligence in formulation and government programs that promote sustainable farming practices is reinforcing growth among major manufacturers. Ingredient diversification toward functional supplements and upcycled by-products is also reshaping supply chains, while tighter rules on antibiotics and carbon labeling push producers toward natural additives. Together, these forces underpin a robust outlook for the compound feed market despite periodic raw-material cost swings.

Key Report Takeaways

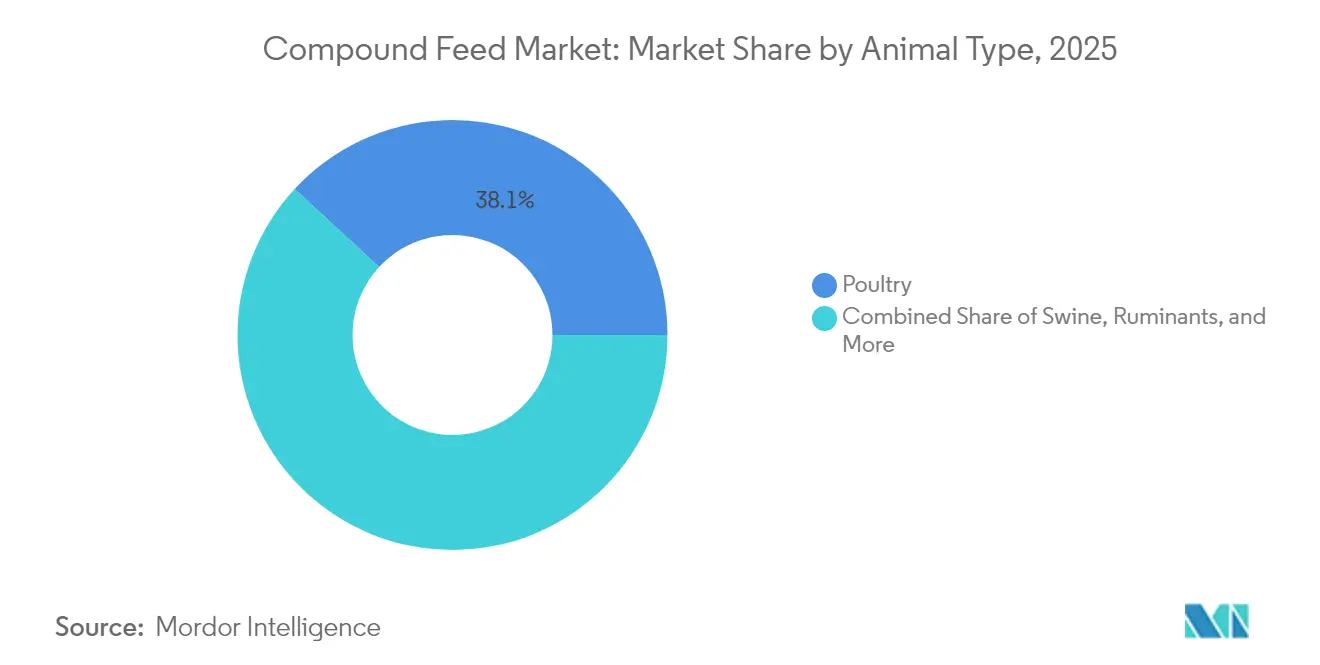

- By animal type, poultry held 38.12% of the compound feed market share in 2025, while aquaculture is set to expand at a 5.55% CAGR through 2031.

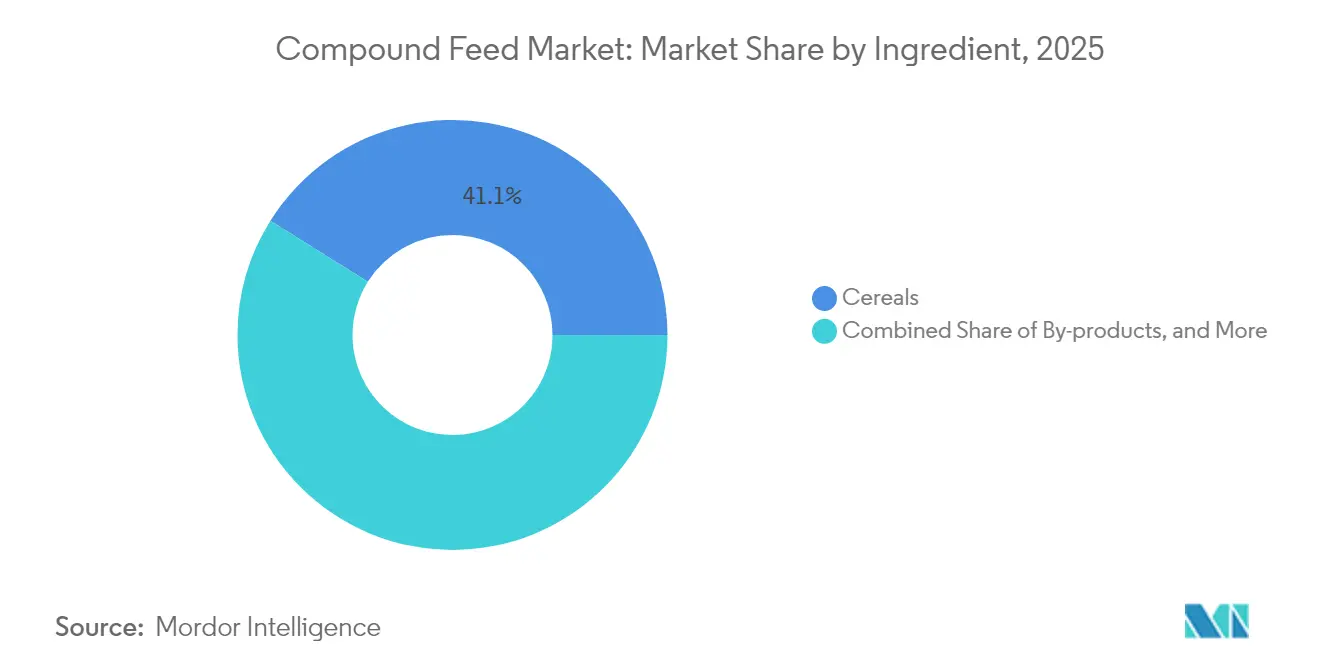

- By ingredient, cereals accounted for 41.08% of the compound feed market size in 2025, while supplements are projected to register the fastest 6.38% CAGR to 2031.

- By form, pellets led with a 45.62% revenue share in 2025, whereas liquid feeds are forecast to grow at a 5.95% CAGR over the same horizon.

- By geography, the Asia-Pacific region commanded 39.22% of 2025 revenue, and the Middle East is poised for the highest 5.62% CAGR from 2025 to 2031.

- The top five players controlled 26.2% of global sales in 2024, indicating a fragmented market and room for regional entrants to scale.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Compound Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for animal-based protein | +1.2% | Global, strongest in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Expanding global livestock population | +0.8% | Developing regions worldwide | Long term (≥4 years) |

| Industrialization of poultry and swine farming | +0.9% | Asia-Pacific core, spillover to South America | Medium term (2-4 years) |

| Adoption of precision-nutrition software in feed mills | +0.6% | North America and European Union, growing in Asia-Pacific | Short term (≤2 years) |

| Upcycling agri-waste into feed | +0.5% | Europe first, spreading globally | Long term (≥4 years) |

| Carbon-footprint labeling pressures on feed formulators | +0.3% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Animal-Based Protein

Urbanization and income gains in emerging economies are driving larger servings of meat, milk, and seafood, prompting feed manufacturers to expand capacity and refine nutrient density. Shrimp output alone surpassed 5 million metric tons in 2024, stimulating specialized functional diets rich in peptides and nucleotides that enhance growth and immunity. Precision amino-acid balancing technologies such as Skretting’s AmiNova line are also reducing nitrogen discharge in aquaculture ponds, helping producers meet environmental benchmarks.

Industrialization of Poultry and Swine Farming

Integrated corporations now deploy sensor networks and automated feeders that adjust rations in real time. Charoen Pokphand Foods’ AI FarmLab in Thailand uses computer vision and climate mapping to maintain uniform bird weights and cut feed conversion ratios, while large Chinese operators have partnered with Huawei Cloud to roll out edge-computing modules that track barn conditions continuously. These platforms translate to leaner inventories and lower disease risk, strengthening profitability.

Adoption of Precision-Nutrition Software in Feed Mills

Digital twins and algorithm-driven formulation platforms are reshaping mill economics. ADM's EQUADVICE model predicts the nutrient contribution of more than 420 raw materials with batch-level accuracy, lowering formulation costs by 1-3% and improving margins by up to 75% through tighter inventory control. BinSentry’s silo-mounted sensors further slash out-of-feed events by 75%, saving fuel and labor across truck fleets.

Carbon-Footprint Labeling Pressures on Feed Formulators

Retailers and quick-service chains increasingly request verified climate impacts on livestock products. Feed makers respond with phytogenic additives, enzymes, and probiotic blends that lift digestibility and cut methane or nitrous oxide emissions. United States Department of Agriculture (USDA) guidelines issued in 2024 emphasize third-party certification for any low-carbon label, accelerating the adoption of life-cycle analysis tools among premix suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in cereal and soybean prices | -0.7% | Import-dependent economies worldwide | Short term (≤2 years) |

| Grain diversion to bio-ethanol and bio-chemicals | -0.4% | North America and Brazil | Medium term (2-4 years) |

| Stringent caps on antibiotic usage in feed | -0.3% | Europe, North America, global spread | Long term (≥4 years) |

| Climate-driven variability in feed-crop yields | -0.5% | Weather-sensitive regions globally | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility in Cereal and Soybean Prices

Corn futures softened from USD 187 per metric ton in 2023 to USD 173.20 in 2024, while soybeans slipped from USD 494 to USD 441, reflecting shifting acreage and freight disruption around the Black Sea. Feed formulators hedge through diversified ingredient matrices, yet cost swings still pressure margins, especially in regions that rely on imports. The Ukraine-Russia conflict continues to influence global grain markets, with low stocks-to-use ratios affecting distillers-to-corn price relationships and creating uncertainty in feed ingredient procurement strategies.

Stringent Caps on Antibiotic Usage in Feed

Regulatory restrictions on antibiotic growth promoters necessitate substantial reformulation investments as the FDA's (Food and Drug Administration) Veterinary Feed Directive requires veterinarian prescriptions for medicated feeds, while the European Union implements strict cross-contamination limits for antimicrobial substances at 1% maximum levels.[1]Source: European Commission, “Delegated Regulation 2024/1229,” eur-lex.europa.eu Alternative feed additives, including essential oils, probiotics, prebiotics, and herbal formulations, require extensive validation and higher per-unit costs, though they offer improved animal health outcomes and reduced antimicrobial resistance risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Faster growth in aquaculture amid poultry dominance

Poultry represented 38.12% of the compound feed market share in 2025, confirming its anchor position within the compound feed market. Robust demand for chicken protein and established industrial infrastructures keep volumes high. In contrast, aquaculture posted the strongest 5.55% CAGR outlook to 2031, signaling its rising strategic weight. Functional shrimp diets fortified with beta-glucans, carotenoids, and single-cell proteins now command premiums, elevating the compound feed market size for aquatic species. Precision nutrition platforms paired with water-quality sensors trim feed conversion ratios and reduce nitrogen loading, enhancing farm profitability and reinforcing environmental compliance.

Ruminant operators adopt radio-frequency identification (RFID) tags and facial-recognition cameras that track individual intake, allowing millers to offer custom concentrates that limit refusals and bolster daily gains. Swine integrators follow circular models that incorporate bakery waste, distillers' dried grains with solubles, and insect meal to offset soybean imports. Together, these shifts widen formulation complexity and create new niches for specialized premix blends across the compound feed market.

By Ingredient: Supplements outpace staples as health focus intensifies

Cereals still commanded 41.08% of the compound feed market share in 2025, but growth is flattening as cost volatility steers nutritionists toward alternative energy sources. Supplements are projected to rise 6.38% annually to 2031, the sharpest among ingredient categories. Adoption is fueled by zero-antibiotic programs and retailer sustainability scorecards that value feed efficiency. Cakes and meals derived from oilseeds retain importance yet face price swings linked to biofuel demand.

Circular economy initiatives accelerate the uptake of by-products such as citrus pulp, brewers' grains, and feather-derived keratin hydrolysate, offering fiber and functional peptides at competitive prices. Emerging proteins from algae, black soldier fly larvae, and methane-fed single-cell biomass also diversify supply. These innovations expand supplier pools, intensify quality-control demands, and transform procurement patterns within the compound feed market.

By Form: Liquid feed gains momentum while pellets stay dominant

Pellets captured the largest slice at 45.62% in 2025 due to durability, low dust, and compatibility with automated feeders. Moisture-controlled conditioning and post-pellet liquid application systems improve nutrient stability and cut pathogen load, reinforcing pellet appeal. Yet liquid feed is forecast to grow 5.95% annually, driven by fish and nursery-pig diets that benefit from higher digestibility and uniform additive dispersion.

Crumbles and mash retain roles in starter and layer diets where beak size or gut development demands specific textures. High-moisture extrusion is opening hybrid formats that blend plant and animal proteins without chemical binders, broadening formulation options and sustaining product innovation cycles across the compound feed market.

Geography Analysis

Asia-Pacific generated 39.22% of compound feed market revenue in 2025, anchored by China’s massive poultry and aquaculture complexes. Government grants that promote the use of enzymes and antibiotic reduction, combined with the adoption of smart farming, give regional players a competitive edge. Vietnam, Indonesia, and Thailand are magnets for European joint ventures that introduce functional additives and cloud-based formulation services, extending market sophistication. The Middle East, though smaller in absolute terms, is on track for a 5.62% CAGR through 2031. Subsidized credit for feed plants, expanding dairy and poultry operations, and tighter food-safety mandates catalyze investment. Countries such as Saudi Arabia and the United Arab Emirates now require mycotoxin certificates for imported raw materials, thereby increasing demand for certified premixes.

South America’s compound feed market benefits from merger and partnership deals that blend local distribution reach with European or North American technology. Brazil produced more than 81 million metric tons of compound feed in 2024, and new mineral-based toxin binders are entering swine and poultry diets to address mycotoxin hotspots in tropical storage environments. Europe shapes global policy through stringent residue limits and the Good Manufacturing Practice Plus (GMP+) Feed Safety Assurance scheme, pushing mills toward hazard analysis and risk-based auditing. North America leads digital transformation, cloud analytics platforms integrating mill-sensor data with enterprise resource planning systems, cutting downtime and scaling multi-site control. Africa’s feed sector remains fragmented yet is pivoting toward climate-smart crops and drought-resistant sorghum and millet. Development agencies sponsor modular mill installations and mobile testing labs to ensure quality in remote regions. These initiatives, combined with fertilizer and seed subsidies, are raising feed reliability and lifting livestock yields, broadening the customer base for the compound feed market.

Regulatory Landscape

Feed regulation is tightening across ingredient approvals, medicated-feed controls, and traceability, which is pushing compound feed producers toward more documentation-heavy, audited operations. In Canada, the Feeds Regulations, 2024 (registered June 17, 2024) introduced updated registration and approval requirements covering mixed feeds, medicated feeds, and single ingredient feeds, lifting compliance expectations for formulations and labels. In the United Kingdom, the Feed Additives (Authorisations) and Uses of Feed Intended for Particular Nutritional Purposes (Amendment) (England) Regulations 2024 entered into force on December 20, 2024, reinforcing governance on additive authorizations and uses.

In the European Union, additive authorization decisions continue to shape permissible formulation options, including the April 2025 authorization of L-valine produced with Escherichia coli CGMCC 22721 for all animal species. The EU has also moved to restrict use of certain antimicrobial medicinal products for animals and animal-derived products exported into the EU from third countries, with application starting September 3, 2026 under the amended implementing framework, adding compliance requirements for exporters and across the feed and livestock supply chain.

Competitive Landscape

The compound feed market exhibits fragmentation, with the top five manufacturers, Cargill, Incorporated, ADM, Nutreco (SHV Holdings), ForFarmers Group, and Charoen Pokphand Foods PCL (Charoen Pokphand Group), holding a significant portion of the combined revenue in 2024. Cargill, Incorporated, divested its Malaysian feed unit for RM 231 million (USD 49.3 million) to streamline its Asian operations, while acquiring two United States mills to strengthen its domestic network depth. ADM acquired PT Trouw Nutrition Indonesia for USD 15 million to enhance local premix capacity and meet Halal-certified demand.

Nutreco’s management shake-up coincides with alliances focused on novel proteins and data services, signaling a pivot toward agile Research and Development. ForFarmers recorded a 7% volume growth in 2024, driven by acquisitions in Poland and the Netherlands, alongside a push for climate-aligned feeds. Charoen Pokphand Foods layers digital twins across its vertically integrated pork and poultry systems, translating sensor data into feed reformulations that lift feed conversion efficiency. Innovative challengers are ascending. Novonesis agreed to acquire DSM-Firmenich’s stake in the Feed Enzyme Alliance for EUR 1.5 billion (USD 1.61 billion), creating an integrated enzyme platform that accelerates product development and cycling[3]Source: Novozymes Press Office, “Novonesis to Acquire dsm-firmenich’s Share of the Feed Enzyme Alliance,” ft.com.

Calysta commercialized a methane-derived protein that displaces fish meal in shrimp diets, while BinSentry and other sensor firms monetize software-as-a-service models by guaranteeing mill uptime. Regional producers gain traction by blending imported know-how with local raw materials, intensifying competition and pressuring incumbents to localize quickly in growth hotspots.

Compound Feed Industry Leaders

Charoen Pokphand Foods PCL (Charoen Pokphand Group)

ForFarmers Group

ADM

Nutreco (SHV Holdings)

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity additions and localization of premix and additives are standing out as a practical whitespace as manufacturers respond to faster professionalization in livestock and aquaculture systems and to the need for formulations tailored to local raw materials and regulations. In 2026, ADM opened a new premix and feed additives facility in Apucarana, Brazil (40,000 tonnes per year), while Cargill commissioned a new dairy feed plant in Wazirabad, Punjab, India (400,000 metric tonnes per year). These moves support higher-value product mixes (premixes, functional supplements, and performance additives) and shorter lead times, which is increasingly relevant where commercial feed is displacing on-farm mixing.

Operational digitalization and sustainability-linked formulations are also expanding the scope for differentiated compound feeds. AI-based batching and plant control systems have been in commercial adoption since 2025, improving dosing accuracy, throughput optimization, and quality consistency, especially for supplements, which are the fastest-growing ingredient category in the report. On the policy front, the pending US Innovative Feed Enhancement and Economic Development (FEED) Act to modernize the FDA framework for feed ingredient approvals and the EU focus on circular bioeconomy pathways (including by-products and former foodstuffs) align with the report trend toward upcycled by-products and functional supplementation, supporting a clearer path for new ingredients and claims when paired with validated data.

Recent Industry Developments

- June 2026: ADM opened a new premix and feed additives production facility in Apucarana, Brazil, with annual capacity of 40,000 tonnes. The site strengthens local availability of higher-margin nutrition solutions and supports faster customization for regional poultry, swine, and ruminant producers.

- July 2025: Cargill, Incorporated reached an agreement to sell its Malaysian animal feed subsidiary, Cargill Feed Sdn Bhd, to Cakaran Corporation Berhad (CAB). The deal shifts manufacturing ownership toward an integrated poultry operator, tightening farm-to-feed alignment and reshaping competitive positioning in Malaysia.

- September 2024: Cargill, Incorporated acquired two United States feed mills to enhance production and distribution capabilities. Expanding the domestic mill network improves service levels and logistics resilience for its Animal Nutrition and Health business across key livestock regions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the compound feed market is measured as the value of manufactured, formulated feed sold for farmed animals, where multiple ingredients are mixed to meet nutrition needs and delivered through organized feed channels.

Scope exclusions: We exclude on-farm mixing of single raw grains and forage, as well as standalone feed additives sold separately from complete compound feed.

Segmentation Overview

- By Animal Type

- Ruminants

- Poultry

- Swine

- Aquaculture

- Other Animal Types (Equine, etc.)

- By Ingredient

- Cereals

- Cakes and Meals

- By-products

- Supplements

- By Form

- Pellets

- Mash

- Crumbles

- Liquid

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Spain

- United Kingdom

- France

- Germany

- Russia

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Thailand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market context and lock down practical inputs that drive compound feed demand across regions and animal categories. We reviewed public production and livestock statistics, then aligned them with trade flows and input-cost signals so the model reflects real-world feed output and pricing patterns.

Typical references included sources such as FAOSTAT, USDA reports, Eurostat datasets, and UN Comtrade, alongside trade association publications such as global and regional feed federation releases. Patent and standards databases were also checked to understand formulation shifts and additive substitution. Company annual reports and investor presentations were used to validate capacity additions and plant utilization language. Where needed, paid subscriptions for company financials and a shipment-level trade database were used to cross-check revenues, export mixes, and major commodity movements. These examples are illustrative, and many other public and paid sources were also consulted during data collection and validation.

Primary Interviews and Surveys

Primary work focused on validating what changes spend per ton of compound feed and the actual demand pull across species. We spoke with feed manufacturers, ingredient distributors, integrators, and downstream livestock and aquaculture stakeholders across APAC, EMEA, and the Americas. The goal was to confirm operating rates, formulation changes, and pricing pass-through behavior, then use that input to refine assumptions and close gaps left by public data.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 14% | APAC: 46% |

| Mid tier: 48% | Functional/Unit leaders: 29% | EMEA: 30% |

| Smaller Players: 20% | Managers: 57% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where feed demand is reconstructed from livestock and aquaculture production intensity, feed conversion patterns, and commercially supplied feed penetration by region. That demand pool is translated into value using observed pricing signals and ingredient cost movements, then adjusted for form mix (pellets, mash, crumbles, and liquid) and species mix so the total stays consistent with how feed is bought and sold.

To keep the model practical, we track a few market fingerprints closely, including compound feed output in metric tons, poultry and swine inventory and production trends, aquaculture output growth, corn and soybean meal price cycles, and the share shift toward higher-protein formulations. Results are corroborated with selective bottom-up approximations, such as sampled price-per-ton checks and revenue sanity checks for a set of producers and regions. These are used to correct potential overstatement that can come from uneven reporting. For forecasting, scenario analysis is used around grain and oilseed cost bands and animal output growth, and those scenarios are aligned to the outlook shared by primary experts so the final curve is not driven by a single assumption.

Data Validation & Update Cycle

Outputs are triangulated against independent signals such as feed production totals, trade flows for key inputs, and region-level livestock and aquaculture growth rates. We also check for unrealistic price or volume jumps. When a variance looks large, we re-check the underlying driver, and if needed we re-contact contributors to confirm whether it is a real shift, such as a disease event, policy change, or a sharp ingredient cost swing.

Before sign-off, the model and assumptions go through multi-step analyst review so the numbers match the defined scope and remain consistent across regions and animal types. Reports are refreshed annually, with interim updates when material events move demand or pricing, and a final pre-delivery pass is completed so clients receive the latest adjusted view.

Mordor Intelligence's Global Compound Feed Market Market Estimate Compared With Other Published Estimates

It is normal to see different market sizes for compound feed because publishers do not always count the same items, even when the title looks identical. The biggest swings usually come from whether the number is tied to manufactured feed sales only, or it includes adjacent items. Differences also show up in how pricing is built from input costs and inflation timing.

Some published figures fold in feed additives or broader animal nutrition revenues, and they also tend to apply a generic price per ton across regions. Mordor Intelligence counts formulated compound feed sold into livestock and aquaculture diets, and it keeps separate tallies for form and species mixes. This helps avoid overstating value when additives or non-commercial feed are blended into the same total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 613.9 B (2026) | |

| Global Consultancy A | USD 497.69 B (2025) | Uses a factory-gate revenue framing and a different base year, and the lower figure can also reflect narrower capture of commercial feed sales and service revenue treatment across countries. |

| Industry Publisher B | USD 611.25 B (2025) | Uses 2025 as the base year and may apply different price progression assumptions by region, which can shift the value even when volumes and species coverage look similar on the surface. |

The spread in the table is mainly explained by scope packaging and timing, not by a single demand driver. By tying value to species-led demand pools and checking the price build against ingredient cycles and regional mix, our estimate stays traceable to repeatable inputs instead of broad averages.

Key Questions Answered in the Report

How large is the compound feed market in 2026?

The compound feed market size hit USD 613.9 billion in 2026 and is on course to reach USD 748.27 billion by 2031.

Which animal type is projected to grow fastest to 2031?

Aquaculture feed is forecast to post the highest 5.55% CAGR, driven by functional diets and sustainable protein initiatives.

What share of revenue do the top five feed manufacturers hold?

Industry leaders hold roughly 26.2% of worldwide sales, signaling fragmentation.

Which ingredient category is expanding quickest?

Supplements including enzymes and amino acids are projected to grow 6.38% yearly as producers focus on animal health and regulatory compliance.

Page last updated on: