Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 116.92 Billion |

| Market Size (2026) | USD 120.5 Billion |

| Market Size (2031) | USD 140.03 Billion |

| Growth Rate (2026 - 2031) | 3.06% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Compound Feed Market Analysis by Mordor Intelligence

The Europe compound feed market size is expected to grow from USD 116.92 billion in 2025 to USD 120.5 billion in 2026 and is forecast to reach USD 140.03 billion by 2031 at 3.06% CAGR over 2026-2031. Regulatory pressure on carbon intensity, the green-light for novel proteins, and stricter antibiotic rules are reshaping ingredient procurement, processing technology, and digital oversight across the region. Poultry dominated the 2024 value, and aquaculture is growing more than twice as fast, thanks in part to Norway, Scotland, and Spain, which have a high demand for micro-pellets with precise nutrient density. Cereals remained the largest input, although insect meal is scaling rapidly following European Food Safety Authority approvals for Tenebrio molitor and Hermetia illucens. Pellets dominate the feed form, but micro-pellets are posting the quickest gains as hatcheries look to cut waste and improve conversion. Spain led revenue in 2024, while Italy is the fastest riser through 2030, driven by renewed dairy herd expansion.

Key Report Takeaways

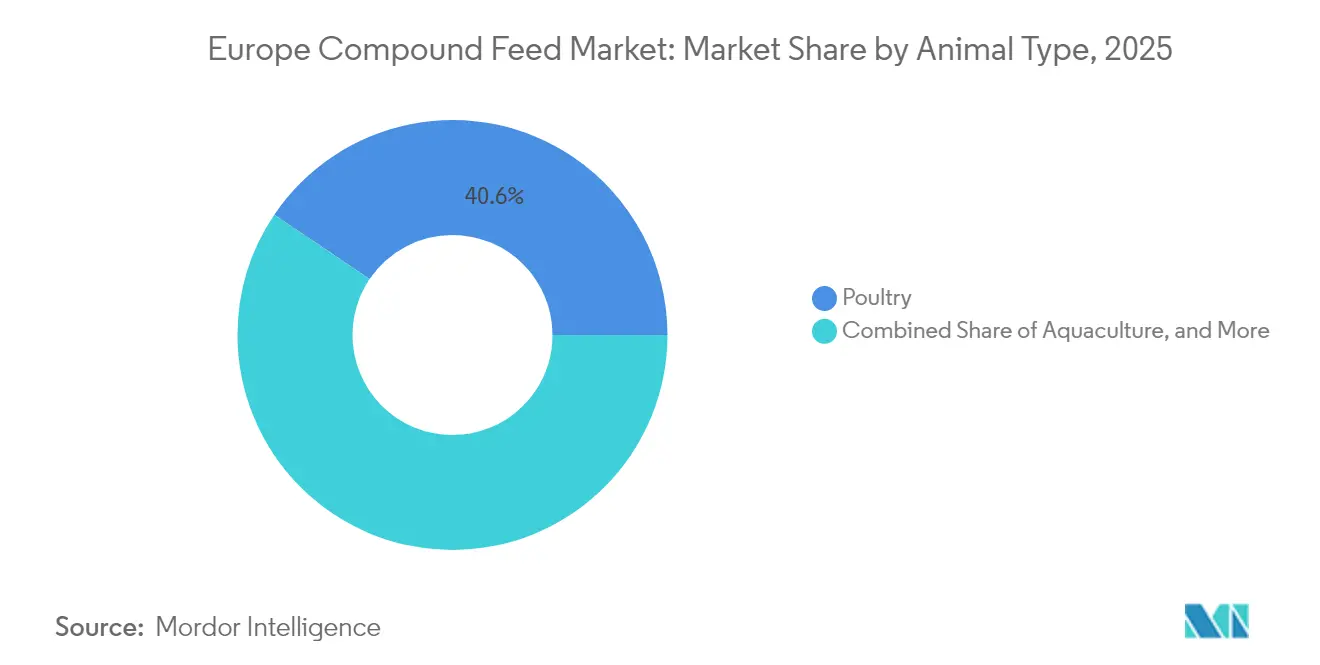

- By animal type, poultry held 40.55% of Europe compound feed market share in 2025, while aquaculture is forecast to expand at a 5.82% CAGR to 2031.

- By ingredient type, cereals captured 45.85% of the Europe compound feed market size in 2025, while cakes and meal are advancing at an 10.94% CAGR through 2031.

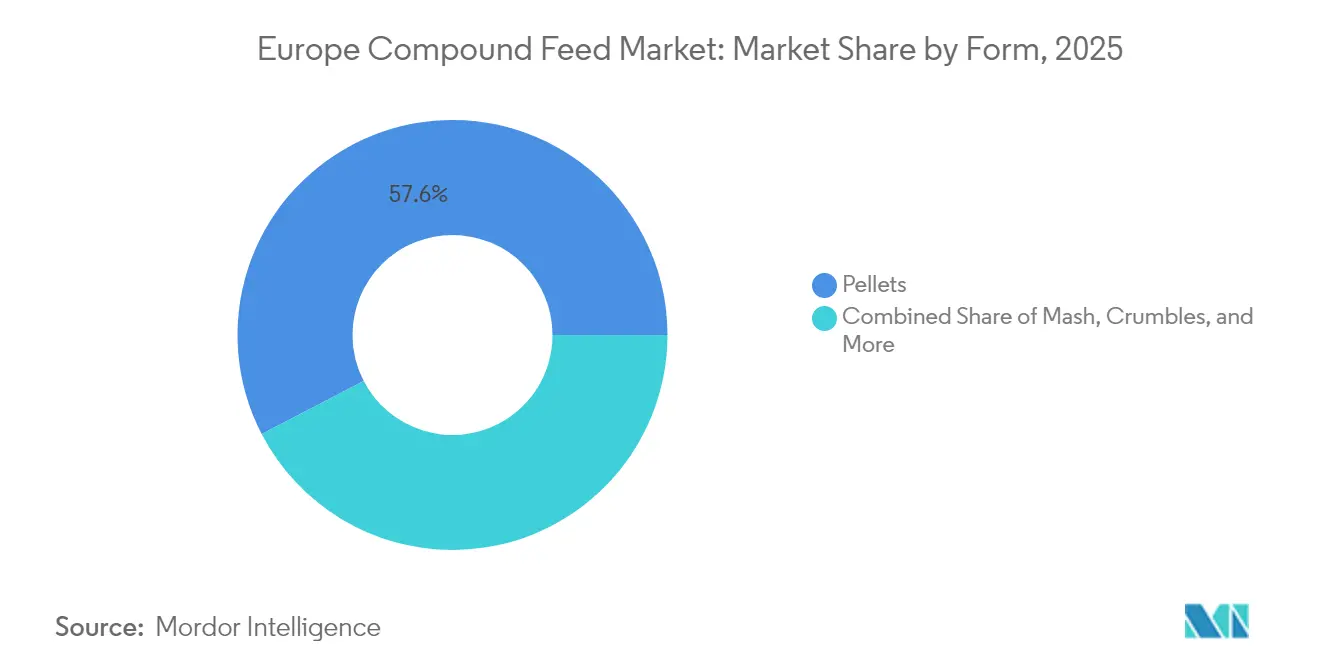

- By form, pellets led the market with a 57.62% market share in 2025, and micro-pellets are projected to grow at an 8.17% CAGR through 2031.

- By geography, Spain accounted for 18.62% of the revenue share in 2025, and Italy is projected to post the fastest growth of 4.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Compound Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising meat consumption and animal protein demand | +0.8% | Spain, Poland, Germany, and France, with the strongest growth in Eastern European markets | Medium term (2-4 years) |

| Strategic production capacity investments by integrators | +0.6% | Spain, Germany, France, and the Netherlands, with concentrated activity in poultry and swine corridors | Short term (≤ 2 years) |

| Increasing focus on feed efficiency and gut-health additives | +0.7% | Western Europe is leading the adoption, with gradual diffusion to Central and Eastern Europe | Medium term (2-4 years) |

| European Union Green Deal pushes for low-carbon livestock production | +0.5% | European Union-wide, with early implementation in Netherlands, Denmark, and Germany | Long term (≥ 4 years) |

| Digital twin adoption in feed formulation | +0.3% | Netherlands, Denmark, Germany, and France, driven by large Cooperatives and integrators | Medium term (2-4 years) |

| Expansion of insect-meal inclusion in compound feed | +0.4% | France, the Netherlands, Belgium, and Spain, following European Food Safety Authority authorizations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Meat Consumption and Animal Protein Demand

Poultry intake climbed to 24.8 kilograms per capita in 2024 while pork remained steady at 32.4 kilograms, together safeguarding basal demand for Europe compound feed market supplies despite urban shifts toward plant alternatives. Rising incomes in Poland and Romania are shifting consumption from processed meats toward fresh poultry and value-added pork, both of which rely on higher amino acid densities and enzyme enrichment to meet tight feed conversion targets. Spain lifted broiler output 4.2% in 2024 on export gains to North Africa and the Middle East, offsetting a 2.1% decline in German pork linked to African swine fever containment[1]Source: FEFAC (European Feed Manufacturers' Federation), "Feed and Food Statistical Yearbook 2024." fefac.eu.. Aquaculture is acting as a third anchor, with salmon and trout volumes reaching 2.8 million metric tons in 2024 and demanding premium marine-ingredient rations that cost 20 to 30% more than terrestrial formulas. The pivot toward higher value proteins is forcing mills in the Europe compound feed market to invest in micro-ingredient dosing and liquid application equipment so that enzymes, organic acids, and essential oils are dispersed at below 0.5% inclusion with uniformity that commodity producers struggle to match. Those upgrades increase capital intensity, yet enable suppliers to defend their margins through demonstrated performance improvements, reinforcing the market’s transition toward quality-led competition.

Strategic Production Capacity Investments by Integrators

During 2024, integrators commissioned eighteen new feed mills across Spain, Poland, and Germany, adding 3.2 million metric tons of annual throughput aimed at securing margins and enhancing biosecurity. Cargill’s upgrade in Krefeld introduced precision grinding and encapsulated butyric acid, targeting a 1.85 feed conversion ratio and lowering grow-out costs by USD 0.09 (EUR 0.08) per kilogram of liveweight. ForFarmers followed with a 240,000 metric tons Polish plant equipped with near-infrared analyzers that trim nutrient variance by 40%. Independent mills are attempting to remain relevant by forming purchasing pools and installing modular extrusion lines that are capable of switching quickly between poultry, swine, and aquaculture diets. Most new brick-and-mortar investments are clustered in wheat and barley belts, such as the Beauce plain in France and Lower Saxony in Germany, which cuts inbound grain logistics costs. These strategic moves underscore how Europe compound feed market participants are racing to secure quality grain pipelines and build flexible capacity that can reformulate quickly.

Increasing Focus on Feed Efficiency and Gut-Health Additives

European broiler feed conversion improved from 1.58 in 2020 to 1.52 in 2024 following widespread uptake of multi-enzyme complexes that unlock an extra 4 to 6% metabolizable energy from wheat diets[2]Source: European Food Safety Authority, “Feed Additives,” efsa.europa.eu. The use of probiotics in starter diets doubled as the European Commission cleared Bacillus subtilis and Enterococcus faecium strains, supporting a 1.2- to 1.8-point decline in early mortality. Organic acids, such as formic and propionic, are now standard inclusions in Danish and Dutch weaner pig rations, resulting in 35 to 50 grams of daily gain during the vulnerable post-weaning window. Encapsulation processes that shield volatile oils during pellet heat treatment are quickly becoming table stakes, and mills without the technology risk losing contracts with integrators who benchmark on gut health. Premium customers in the European compound feed market are willing to pay a surcharge for additive-rich blends because the delta in performance offsets the higher cost, thereby widening the competitiveness gap with budget feeds that sacrifice supplements to maintain headline pricing. The ongoing pivot toward functional ingredients, therefore, exerts a structural pull on formulation practices and capital spending plans.

European Union Green Deal Pushes for Low-Carbon Livestock Production

The Farm to Fork objective of cutting nutrient losses in half by 2030 is forcing mills to match protein and phosphorus to animal needs more precisely, resulting in a 12 to 18% reduction in nitrogen runoff. Conditional approvals for 3-nitrooxypropanol in dairy diets reduced methane by up to 30% but increased formulation costs. Carbon-footprint labels, piloted in Denmark and Germany, reveal that imported soybean meal can account for half of feed carbon intensity, increasing the appeal of regional rapeseed and faba beans, although they deliver less protein. The Industrial Emissions Directive 2.0 tightened ammonia caps in 2024, accelerating the use of low-crude-protein diets supplemented with crystalline amino acids, which reduce nitrogen excretion by up to one-fifth. Large players are adopting life cycle assessment and blockchain traceability to back sustainability claims, while small mills struggle with added compliance expenses that undermine their price position within the Europe compound feed market. The policy mix, therefore, tilts competitive advantage toward operators able to document and monetize emissions cuts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in cereal and oilseed prices | -0.5% | European Union-wide, with acute pressure in France, Germany and Poland due to drought and geopolitical supply disruptions | Short term (≤ 2 years) |

| Stricter antibiotic-free regulations | -0.4% | European Union-wide, with the highest compliance costs in Denmark, Netherlands, and Germany | Medium term (2-4 years) |

| Accelerating shift toward plant-based diets | -0.3% | Western Europe, particularly the United Kingdom, Germany, and the Netherlands, urban centers | Long term (≥ 4 years) |

| Slow harmonization of European Union novel-feed approvals | -0.2% | European Union-wide, with bottlenecks in cross-border commercialization of insect proteins and algae-based ingredients | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Cereal and Oilseed Prices

European wheat averaged USD 262.1 per metric ton (EUR 245 per metric ton) in 2024 after drought cut French and German harvests by 8.2 million metric tons, while soybean meal peaked at USD 518.9 per metric ton (EUR 485 per metric ton) before easing to USD 449.4 per metric ton (EUR 420 per metric ton) as South American supply stabilized[3]European Commission, “Market Price Data,” ec.europa.eu . Smaller plants, lacking hedging tools, were hit hardest, amplifying the structural shift toward large cooperatives that operate grain desks and storage silos. Formulators responded by increasing the shares of rapeseed and sunflower meal, yet the lower amino-acid density required additional synthetic lysine and methionine, thereby increasing supplement expenditure. The need to carry higher safety stocks tied up working capital at a time when interest rates were already elevated. Feed buyers in the European compound feed market, therefore, are confronted with a trade-off between price volatility and nutrient risk, prompting greater interest in locally grown cereals, despite the need for more enzymes to unlock wheat energy. Until Black Sea logistics normalize and climate volatility subsides, raw material swings will continue to weigh on near-term growth.

Stricter Antibiotic-Free Regulations

Rules issued in 2022 limited the use of prophylactic antibiotics, obliging producers to demonstrate a therapeutic need through veterinary prescriptions. Compliance costs increased as mills added organic acids, essential oils, and probiotics to their products. Denmark’s antibiotic-free swine phase initially raised weaner mortality by 3.2%, which only normalized once encapsulated butyric acid and Bacillus probiotics were supplied at 2.5 to 3.5 kilograms per metric ton. The Netherlands then banned zinc oxide above 150 parts per million, forcing new gut-health strategies and extra lab tests. Large integrators with in-house veterinarians adjusted quickly, while small, independent farms experienced wider performance variations, making premium markets harder to access. Retail chains tightened residue checks, raising the stakes for mills that were unable to document their additive programs. The transition highlights how antibiotic-free mandates, although beneficial for public health, can compress margins for operators lacking capital and technical expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Aquaculture Widens The Growth Gap

Poultry preserved a 40.55% share of the Europe compound feed market size in 2025. Poultry blends benefit from finer grinding, as well as the addition of xylanase and amylase, which enhance starch digestibility and offset the higher inclusion of wheat. Swine recovers modestly while ruminant tonnage contracts 1.2% amid herd reductions driven by methane and ammonia targets. Aquaculture feeds are projected to grow at the fastest 5.82% CAGR through 2031, driven by the demand for fishmeal-rich formulas, which are required for Norwegian and Scottish salmon, as well as Mediterranean seabass and seabream, which typically contain 25 to 35% marine protein. Shrimp diets add even more momentum, as the Netherlands and Spain expand recirculating systems that need high digestibility and astaxanthin pigmentation.

Rising demand for micro-pellets measuring less than one millimeter, with two-hour water stability, is reshaping equipment orders across mills that serve salmon smolt and shrimp hatcheries. Swine producers in Germany and Denmark are transitioning to liquid feeding systems that combine dry feed with whey and bakery co-products, reducing costs. In ruminant feed, methane blockers such as 3-nitrooxypropanol are being incorporated at an additional cost, while also providing access to carbon credit payments. As a result, species diversification is influencing capital investments, with feed mills installing flexible production lines that can alternate between high-density fish feed and traditional pellets to maintain utilization rates.

By Ingredient Type: Cakes and Meal Challenges Cereal Dominance

Cereals still represented 45.85% of of Europe compound feed market share in 2025, with wheat often climbing above 60% in poultry rations. Cakes and meals, primarily made from soybeans and rapeseed, show an 10.94% CAGR, with rapeseed gaining market share as deforestation due diligence regulations reduce the appeal of South American soy. Supplements account for a notable portion of expenditure despite their low tonnage, as synthetic amino acids are priced at a premium.

Supplement growth outpaces bulk ingredients because xylanase, phytase, probiotics, and acidifiers help mills offset high cereal prices and stricter nutrient-loss caps. Insect protein adoption is concentrated in France, the Netherlands, and Belgium, where twenty-two plants already produce 28,000 metric tons, and forward contracts with salmon farmers secure financing. Wheat’s share may slip as integrators diversify toward sorghum and barley, but enzyme adoption ensures stability in digestibility. Ingredient sourcing is thus fragmenting into commodity versus specialty tiers that allow mills to tailor the Europe compound feed market supply for both price-sensitive and premium sustainability channels.

By Form: Micro-Pellets Take Premium Share

Pellets accounted for 57.62% of the 2025 market size, as they reduce dust and boost feed efficiency. Micro-pellets measuring less than two millimeters are increasing at an annual rate of 8.17%, driven by hatchery demand that values minimal fines. Crumbles occupy a significant share, especially in broiler starters, where birds need an intermediate particle. Mash, popular on small farms and layer units that tolerates 4 to 6% poorer conversion but saves on pelleting costs.

Technological upgrades include steam conditioning at temperatures of up to ninety degrees Celsius and hold times of one minute, which raises pellet durability and reduces fines to below five percent, resulting in a reduction of wastage by up to twelve percent. Micro-pellet production lines operate at a lower capacity compared to standard pellet lines, which explains the higher premiums per metric ton. Additionally, crumble production incurs an extra cost per metric ton but delivers measurable benefits in starter performance. The Europe compound feed market, therefore, bifurcates into large integrated mills focused on high-volume pellets and niche plants that switch rapidly among forms to serve specialty contracts.

Geography Analysis

Spain accounted for 18.62% of the revenue share of the Europe compound feed market in 2025, representing the largest single-country share in the Europe compound feed market. Increased broiler exports to North Africa and the Middle East, along with a recovery in swine herds, are driving domestic demand in these regions. Additionally, six Hermetia illucens plants now produce 8,500 metric tons of insect meal for organic feed formulations. The aquaculture feed segment is supported by seabass and seabream farms adopting marine-lipid diets with 1.2-1.8% omega-3 inclusion, sourced from Norwegian fish oil.

Italy is projected to achieve the fastest CAGR of 4.62% through 2031. This growth is fueled by the expansion of dairy herds in Lombardy and Emilia Romagna, which require high-energy maize-silage blends fortified with 12-15% soybean meal. Automated milking systems, now implemented on 18% of Italian farms, optimize concentrate delivery and improve feed efficiency by 6-9%, contributing additional tonnage to the Europe compound feed market.

Germany generated significant revenue but is growing at a modest rate of 2.32%, as swine inventories decline due to stricter welfare regulations. Despite this, eighteen mills have adopted digital twin technology, resulting in a reduction of USD 4-6 per metric ton in formulation costs. Poultry feed volumes remain stable at 1.6 million metric tons, while the early adoption of 3-nitrooxypropanol in dairy diets has reduced methane emissions by 28%, despite increasing feed costs by USD 23.5 per metric ton. The diverse growth trajectories across countries are projected to sustain the overall expansion of the Europe compound feed market by 2031. Geographic diversification mitigates risks and ensures aggregate demand remains resilient, even when individual countries face challenges such as adverse weather conditions or policy changes.

Regulatory Landscape

The Europe compound feed market operates under a harmonized EU framework led by Regulation (EC) No 1831/2003 for additives in animal nutrition and Regulation (EC) No 767/2009 for placing feed on the market and feed labelling. EFSA provides the scientific risk assessment and efficacy opinions that underpin European Commission Implementing Regulations, which in practice shapes the authorization pathway for additives (including enzymes, probiotics, amino acids, and acidifiers) and affects formulation choices and cross-border commercialization.

In 2026, multiple Commission Implementing Regulations refreshed the compliance baseline for commonly used additive categories, including renewals for fumaric acid (January 2026) and thiamine forms (February 2026), and authorizations such as L-lysine sulphate produced with Corynebacterium glutamicum (January 2026) and Duddingtonia flagrans (March 2026). These updates raise the bar for mills and premix suppliers to keep dossiers and usage conditions aligned with current EFSA guidance, while maintaining documentation and labelling discipline under Regulation (EC) No 767/2009 as customers and auditors increase scrutiny on ingredient disclosure and claim substantiation.

Competitive Landscape

Competition in the Europe compound feed market is moderate, with global integrators such as Cargill, Incorporated, Archer Daniels Midland Company, and Nutreco N.V. investing in backward links to raw materials as well as forward links into livestock production to control margin under volatile grain prices. Regional cooperatives, including ForFarmers N.V., Agrifirm Group, and Danish Agro a.m.b.a., provide farmer members with bulk ingredient discounts, technical advice, and flexible payment terms, which help lock in loyalty despite price competition.

Digital twin software represents a clear line of demarcation, as early adopters can trim procurement costs by up to five percent and reposition resources on a weekly basis rather than quarterly. Patent activity is increasing for encapsulation methods that preserve volatile acids during 90°C pelleting, as seen with Cargill, Incorporated, which filed four patents in 2024 covering lipid matrix delivery systems. Independent mills respond by forming purchasing clubs and installing modular extrusion that switches among poultry, swine, and aquaculture recipes within a single shift, thereby protecting utilization and keeping working capital low.

Competitive intensity peaks in poultry and swine corridors where integrators internalize feed production to secure biosecurity, leaving independents to serve organic, non-Genetically Modified Organism (non-GMO), and insect-enriched niches that bring 15% to 25% price upside once third-party certifications are documented. Larger cooperatives utilize sustainability dashboards that track Scope 3 emissions from soybeans to barns, a prerequisite for shelf placement under retailer carbon labels. As sustainability metrics move from marketing to compliance, scale, and data fluency will tilt bargaining power toward technology leaders across the Europe compound feed market.

Europe Compound Feed Industry Leaders

-

Cargill, Incorporated

-

Alltech

-

Archer Daniels Midland Company

-

Kemin Industries, Inc.

-

Nutreco N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity centers on specialty nutrition and process upgrades that help customers meet tighter antibiotic, nutrient-loss, and carbon-intensity constraints, especially in poultry and aquaculture where performance sensitivity supports premium pricing. In Southern Europe aquaculture, platforms such as Skretting 360+ connect on-farm performance data with feeding strategy and formulation decisions, creating room for micro-pellets, higher-precision dosing, and additive programs that improve conversion and reduce waste across hatchery and grow-out systems.

Ingredient sourcing and protein diversification also create commercial space as customers respond to sustainability and supply-security pressures, including the operational impact of the EU deforestation agenda on soybean-linked supply chains. Industry signals in 2026 point to a high-volume but flat production environment (FEFAC cited 152 million tonnes of EU-27 industrial compound feed production for 2026), which shifts emphasis toward product differentiation (functional additives, verified claims, and traceability) and toward localized processing routes that increase access to regionally produced meals and alternative proteins for compound formulations.

Recent Industry Developments

- June 2026: Cargill invested EUR 5.4 million in a new extrusion pilot plant at its Innovation Center in Vilvoorde, Belgium, expanding R&D capability for feed and pet food applications. The added piloting capacity is intended to support faster scale-up of new formulations and processing parameters, reinforcing the shift toward higher-value, performance-led compound feed and aquafeed specifications in Europe.

- September 2025: ADM unveiled a new dairy feed solution positioned to improve nutrient utilization and animal performance, expanding its specialty offering for ruminant diets. The release supports the broader move toward additive-enabled efficiency gains as producers manage tighter nutrient-loss and emissions requirements while protecting milk yield economics.

- September 2024: ForFarmers and DLG subsidiary team, agrar agreed to consolidate their German feed activities under a new entity, ForFarmers team agrar, subject to regulatory approval. The combination aims to strengthen scale in one of Europe’s more regulated livestock markets and sharpen competitive positioning through a broader portfolio across swine, cattle, and poultry feed.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the European compound feed market is defined as the value of manufactured feed that is formulated and sold as complete or complementary feed for livestock and aquaculture across Europe.

Scope exclusions: We exclude on-farm feed mixing that is not commercially sold, and we also exclude standalone feed additives and premixes that are traded as ingredients rather than finished compound feed.

Segmentation Overview

-

By Animal Type

-

Ruminants

- Beef Cattle

- Dairy Cattle

- Other Ruminants

-

Poultry

- Broiler

- Layer

- Other Poultry

- Swine

-

Aquaculture

- Fish

- Shrimp

- Other Aquaculture Species

- Other Animal Types

-

Ruminants

-

By Ingredient Type

- Cereals

- Cakes and Meals

- By-products

-

Supplements

- Vitamins

- Amino Acids

- Enzymes

- Prebiotics and Probiotics

- Acidifiers

- Other Supplements

-

By Form

- Mash

- Pellets

- Crumbles

- Micro-Pellets

-

By Geography

- Spain

- United Kingdom

- France

- Germany

- Russia

- Italy

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model and to collect consistent, repeatable inputs that can be checked year over year. We relied on public and official sources such as Eurostat for livestock and trade series, FAOSTAT for production context, and European Commission materials for policy signals that affect feed demand and formulation needs.

To keep the sizing grounded in real operating conditions, association publications such as FEFAC were reviewed for compound feed output and animal category trends, then cross-checked with national statistics and industry press coverage. Company annual reports, investor presentations, and regulatory updates were used to validate capacity expansion, pricing pressure, and formulation shifts. Where the public trail was thin, our analysts used paid subscriptions for company financials and intelligence, shipment-level trade views, and patent databases to confirm whether a change was local or more Europe-wide. These examples are illustrative, and other sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on checking what drives purchasing and production decisions across animal feed lines, and then confirming how quickly those drivers are changing. We spoke with a mix of feed manufacturers, ingredient suppliers, distributors, and downstream commercial farms across key European markets to validate demand shifts, pricing behavior, and the practical split between compound feed and adjacent products.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 16% | APAC: 46% |

| Mid tier: 52% | Functional/Unit leaders: 31% | EMEA: 30% |

| Smaller Players: 18% | Managers: 53% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where livestock population and production patterns are translated into feed demand pools, then reconciled with reported compound feed output at the regional and country level. To keep the totals realistic, the model uses a small set of measurable inputs such as animal headcount by species, meat and milk production trends, compound feed output by animal category, import and export flows for key feed ingredients, and observed price movement for common formulations.

Once the demand pool is reconstructed, selective bottom-up approximations are used as checks, including sampling manufacturer revenue exposure to compound feed, sanity-checking average selling prices against raw material cost direction, and reviewing channel feedback on volume growth by poultry, ruminant, swine, and aquaculture feed. When company-level disclosures do not split revenues cleanly, gaps are handled through proxy splits based on product mix statements and country production footprints, then adjusted after interview feedback.

For forecasting, we use scenario analysis supported by simple regression-style relationships between animal production indicators and compound feed demand, followed by expert validation on price pass-through timing. In periods where disease events or policy shifts can distort a single variable, assumptions are stress-tested so the final outlook reflects a practical range rather than one fragile trajectory.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, then reviewed for breaks that do not match known livestock cycles or input cost movements. We compare the implied feed intensity and pricing to reference statistics, trade direction, and field feedback, and then track any large variance back to a specific assumption before it is accepted.

Before sign-off, a second analyst reviews the model logic, the year-to-year deltas, and internal consistency between value and volume. If a major revision in livestock numbers, regulation, or raw material pricing is observed, experts are re-contacted to confirm whether it is a short disruption or a structural change. Reports are refreshed annually, with interim updates for material events, and a final pre-delivery pass is done so the client receives the latest aligned view.

Mordor Intelligence's European Compound Feed Market Market Size Compared With Other Published Estimates

It is normal to see different market sizes published for European compound feed because each study draws the boundary differently and also picks different base years. The totals can shift even when the same countries are covered, since value can be built from production volumes, from farm demand pools, or from revenue proxies.

By tracking production-linked demand indicators and refreshing scope checks, Mordor Intelligence keeps compound feed limited to commercially manufactured formulations across Europe, which reduces inflation from adjacent premix or additive-only revenue treatment. Differences also show up when one estimate leans more on aggressive price uplift assumptions, when currency conversion timing is not consistent, or when EU-only production metrics are extended to all of Europe without a clear adjustment for non-EU markets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 120.5 B (2026) | |

| Global Consultancy A | USD 96.2 B (2024) | Uses an earlier base year and a broader, less explicit product boundary, which can mix compound feed value with adjacent nutrition products while applying higher growth from a different cycle point. |

| Industry Publisher B | USD 103.02 B (2025) | Definition language can extend into companion animal feed and does not clearly separate finished compound feed from premix or additive packs, which changes what is counted and how prices are applied. |

Looking across the three values, most of the spread is explained by year selection and what gets counted as compound feed versus neighboring product buckets. The approach used here stays traceable to livestock demand signals and production reality, and it can be repeated each year with the same checks, which makes the final number easier to use for planning.

Key Questions Answered in the Report

What is the projected value of the Europe compound feed market by 2031?

The market is forecast to reach USD 140.03 billion by 2031 at a 3.06% CAGR.

Which animal category shows the fastest feed demand growth across Europe?

Aquaculture feeds are expanding at a 5.82% CAGR owing to salmon, trout, and shrimp expansion.

Why is insect meal attracting among European feed formulators?

European Food Safety Authority approvals enable Tenebrio molitor and Hermetia illucens to supply high-protein organic and aquaculture diets at price premiums that lift mill margins.

What role does the European Union Green Deal play in feed formulation trend?

New nutrient-loss and methane targets are accelerating adoption of precision protein diets, 3-nitrooxypropanol, and certified low-carbon ingredient sourcing.

Page last updated on: