Feed Adaptogens Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 3.10 Billion |

| Growth Rate (2026 - 2031) | 9.50% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Adaptogens Market Analysis by Mordor Intelligence

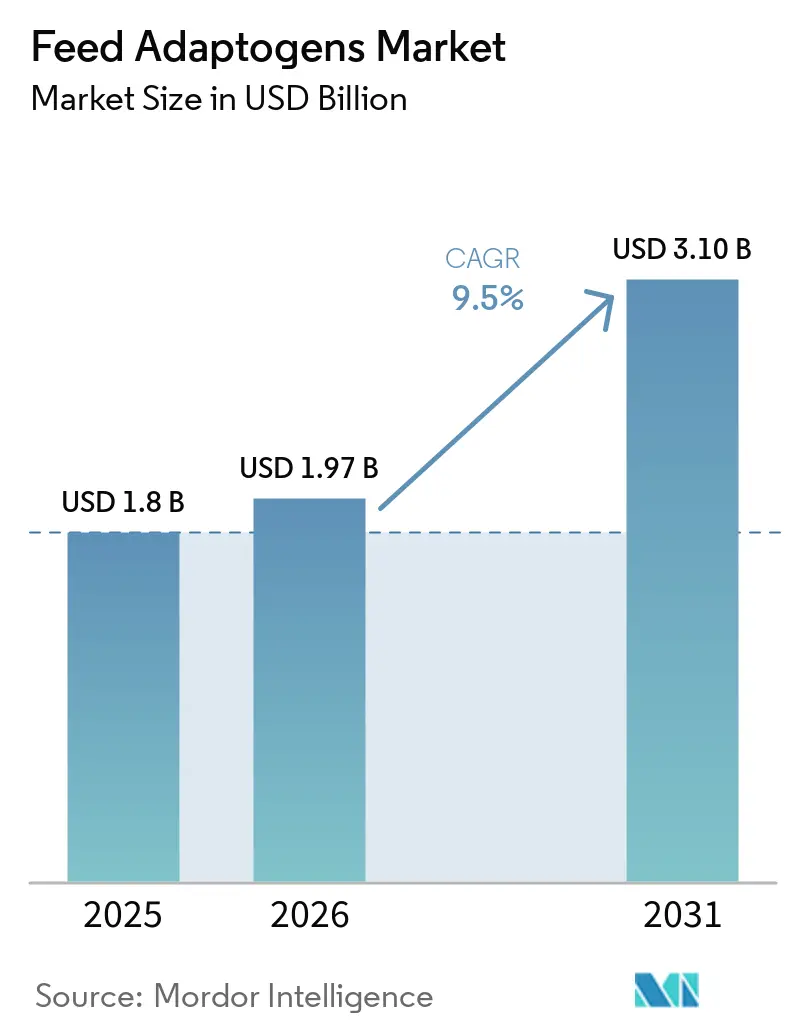

The Feed Adaptogens Market size is projected to increase from USD 1.80 billion in 2025 to USD 1.97 billion in 2026 and reach USD 3.10 billion by 2031, growing at a CAGR of 9.50% over 2026-2031. The feed adaptogens market is being shaped by the steady replacement of antibiotic growth promoters (AGPs) with botanical and fungal additives across major livestock systems, especially where regulation and export standards now favor antibiotic-free production. Heat stress is also moving from a seasonal issue to a regular operating constraint, pushing feed formulators to use adaptogenic ingredients to support stress response, gut integrity, and recovery in poultry, dairy, and ruminant diets. Aquaculture is opening a new demand path for the feed adaptogens market, as immune support and stress control are becoming increasingly important in shrimp and salmonid production, while global farmed aquatic output continues to rise. The feed adaptogens market is also splitting by product quality, with standardized and encapsulated blends gaining ground in mature systems and lower-cost herbal extracts still expanding in cost-sensitive regions, which is shaping pricing, sourcing, and formulation choices.

Key Report Takeaways

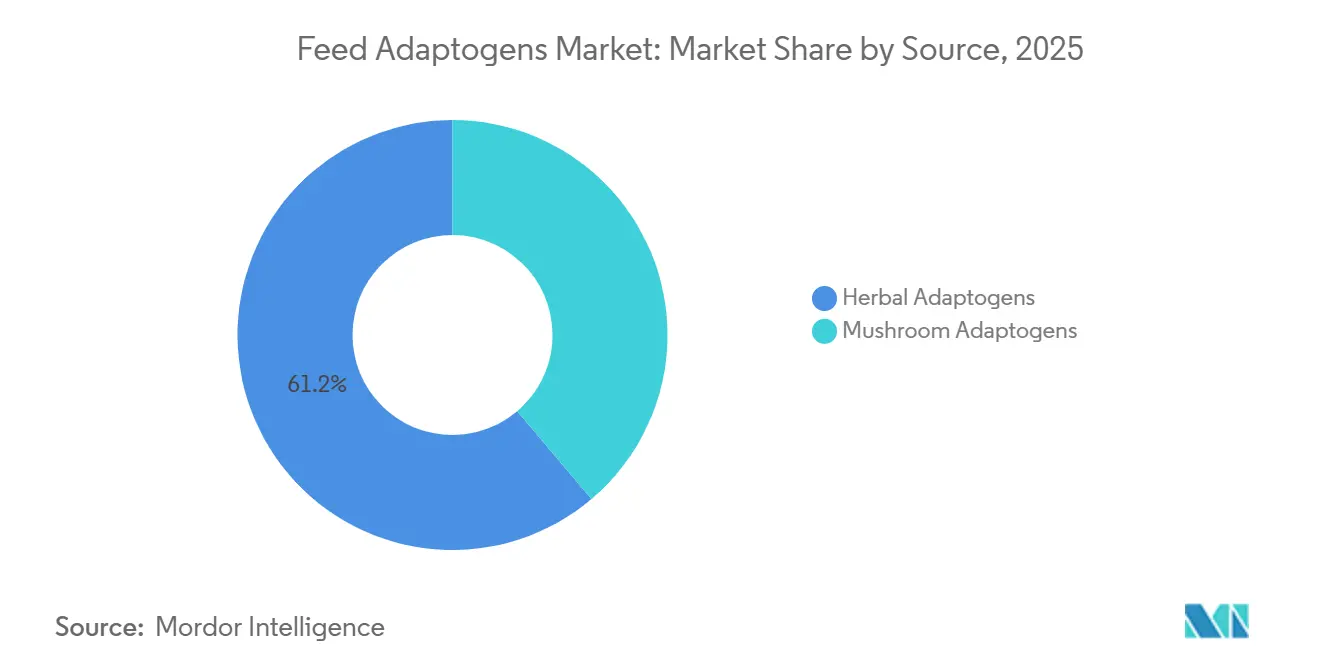

- By source, herbal adaptogens were the largest segment, with a 61.2% share in 2025, while mushroom adaptogens are the fastest-growing segment, with a projected 9.8% CAGR through 2031.

- By form, powder was the largest segment, accounting for 52.3% of the feed adaptogens market size in 2025, while liquid are the fastest-growing segment, with a projected 8.5% CAGR through 2031.

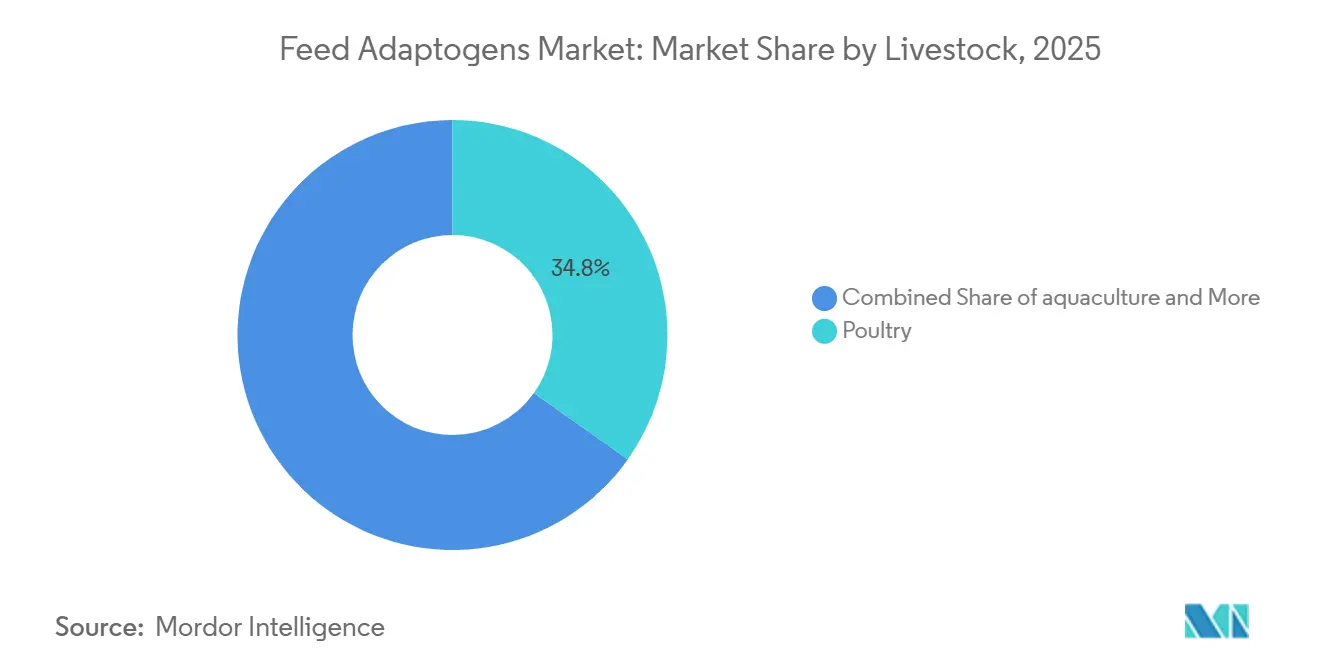

- By livestock, poultry was the largest segment with 34.8% share in 2025, while aquaculture are the fastest segment with a forecasted 7.2% CAGR through 2031.

- By function, stress mitigation was the largest segment with 46.1% share in 2025, while immune enhancement is the fastest segment, which post a 8.6% CAGR through 2031.

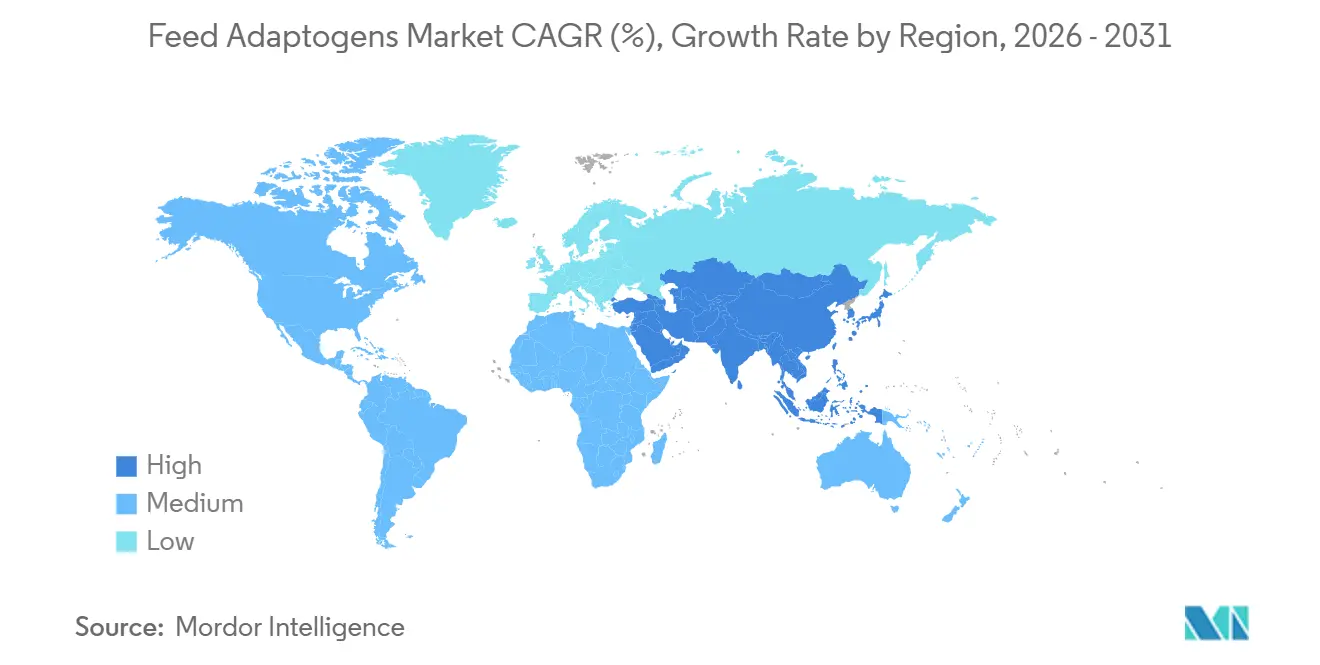

- By geography, Asia-Pacific held 35.4% of the feed adaptogens market share in 2025, while the Middle East are the fastest regional segment with an 8.9% CAGR projected through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Feed Adaptogens Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ban on antibiotics as growth promoters | +2.5% | Global, concentrated in European Union, North America, China, and Asia-Pacific | Short term (≤ 2 years) |

| Rising demand for natural and herbal livestock products | +2.0% | Global, high intensity in North America, European Union, and Australia | Medium term (2-4 years) |

| Heat-stress management in commercial livestock | +1.5% | Asia-Pacific core, with spillover to the Middle East and Africa | Medium term (2-4 years) |

| Rapid growth of global aquaculture sector | +1.0% | Asia-Pacific dominant, with secondary gains in South America and the Middle East | Long term (≥ 4 years) |

| Feed-cost optimization through adaptogen supplementation | +0.8% | Global, strongest in South America and Africa | Medium term (2-4 years) |

| Adoption of precision livestock farming practices | +0.7% | North America and European Union, with early gains in China and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ban on Antibiotics as Growth Promoters

The ban on antibiotic growth promoters has become the clearest structural support for the feed adaptogens market, as it removed the most established, low-cost growth tool from several major livestock economies. The United States ended the production and use of medically important antimicrobials, China eliminated antibiotic growth promoters, and Canada removed growth-promotion claims from antimicrobial labels, thereby shifting procurement toward non-antibiotic feed solutions. The feed adaptogens market is also benefiting from export pressure in middle-income producer countries, where antibiotic use remains more flexible, as exporters increasingly need to comply with buyer requirements in destination markets.

Rising Demand for Natural and Herbal Livestock Products

The feed adaptogens market is gaining support from buyers seeking meat, milk, eggs, and seafood from systems with lower antibiotic use and greater input transparency. Food retailers, restaurant chains, and importers are asking suppliers to document antibiotic-free production, which brings feed decisions into procurement audits rather than leaving them as farm-level preferences. A 2026 review published by researchers of the Slovak University of Agriculture in Nitra found that phytogenic feed additives improved feed conversion ratio, intestinal integrity, and antioxidant status across poultry, swine, and ruminants, strengthening the commercial case for herbal adaptogens in production systems seeking to move away from routine antibiotic support[1]Source: Francesco Vizzarri et al., “Literature Review of Phytogenic Feed Additives for Sustainable Livestock Production,” mdpi.com. This change matters beyond North America and the European Union because export-oriented producers in Brazil, India, and Thailand are adopting natural feed programs earlier than local policy alone would require. As a result, the feed adaptogens market is expanding not only in regions with strict regulation but also in those where access to premium export channels depends on cleaner production claims and traceable feed practices.

Heat-Stress Management in Commercial Livestock

Heat stress is becoming a stable demand driver for the feed adaptogens market because producers now treat thermal pressure as a regular productivity issue rather than an occasional climate event. The pressure appears in poultry, where sharp heat events reduce growth rates and worsen feed efficiency over short exposure periods, making rapid nutritional intervention more valuable. Much of the work also shows that herbal compounds such as ashwagandha, astragalus polysaccharides, and flavonoid-rich blends support antioxidant activity and stress response pathways in livestock under thermal challenge. This is helping the feed adaptogens market move into dedicated budget lines in intensive poultry and dairy systems, especially in tropical and subtropical regions where repeated heat events are now part of annual planning.

Rapid Growth of Global Aquaculture Sector

Aquaculture is creating a new channel for the feed adaptogens market because demand is no longer limited to poultry, swine, and ruminants. The Organization for Economic Co-operation and Development and Food and Agriculture Organization Agricultural Outlook 2025-2034 projects that global aquaculture production will reach 118 million metric tons by 2034, which is 20% above the 2022-2024 base period, while shrimp and prawn volumes are projected to rise 38%[2]Source: Organisation for Economic Co-operation and Development and Food and Agriculture Organization, “Fish and Other Aquatic Products, OECD-FAO Agricultural Outlook 2025-2034,” OECD, oecd.org. Aquaculture systems operate under high stocking densities, disease pressure, and growing scrutiny of antibiotic use, so immune-modulating and stress-control additives meet current operational needs. The Food and Agriculture Organization also reported that aquaculture produced 104.1 million metric tons in 2025, which confirms the scale of the channel now opening to natural feed inputs[3]Source: Food and Agriculture Organization of the United Nations, “Food Outlook – Biannual Report on Global Food Markets,” FAO, fao.org. Botanical extracts from garlic, turmeric, and morinda, along with mushroom beta-glucans, are gaining attention in shrimp and salmonid feeding, which gives the feed adaptogens market a growth path that is not tied only to antibiotic replacement in land-based animal systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory barriers and complex approval processes for botanical feed additives | -1.5% | European Union and North America most constrained, with growing influence in Asia-Pacific | Medium term (2-4 years) |

| Mycotoxin contamination risk in botanical raw materials | -1.0% | Global, acute for wildcrafted herbs concentrated in Asia-Pacific and South Asia | Short term (≤ 2 years) |

| Volatile scalability of herbal adaptogen production | -0.8% | Global, strongest effect on small and mid-size formulators | Medium term (2-4 years) |

| Limited supply and price volatility of botanical raw materials | -0.7% | Global, elevated in Asia-Pacific, Africa, and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Barriers and Complex Approval Processes for Botanical Feed Additives

Regulation remains one of the clearest limits on the feed adaptogens market because botanical additives face a more detailed approval process than many conventional feed inputs. Under Regulation (EC) No. 1831/2003, the European Food Safety Authority requires complete dossiers that cover target species safety, consumer safety, user safety, and environmental safety before a product can move through review. The European Food Safety Authority states that scientific assessment begins only after a complete submission, and additional data requests can lengthen the process beyond the minimum review window, which delays commercialization and increases compliance expense. Its 2025 opinions on rosemary, lavender, peppermint, and wild thyme tinctures show how specific this process can become, including species-based inclusion limits, methyleugenol controls, and hazard analysis and critical control point quality expectations.

Mycotoxin Contamination Risk in Botanical Raw Materials

Mycotoxin exposure remains a significant restraint on the feed adaptogens market because many herbal raw materials pass through fragmented sourcing and post-harvest systems before entering formal feed channels. A 2025 scientific opinion from the European Food Safety Authority on peppermint tincture also noted that mycotoxin testing by some manufacturers is conducted irregularly and outside hazard analysis and critical control point plans, indicating a quality gap in parts of the botanical supply chain. The issue is harder to control in wildcrafted or smallholder-sourced botanicals such as ashwagandha, astragalus, and several adaptogenic mushrooms, where drying, storage, and traceability vary widely across origin markets. For the feed adaptogens market, this makes certified sourcing and vertical control more valuable, and it shifts demand toward suppliers that can demonstrate consistent testing, clean material flows, and documented batch quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Herbal Adaptogens Lead While Mushroom Science Rapidly Matures

Herbal adaptogens held the largest market share at 61.2% in 2025, keeping them firmly ahead in the feed adaptogens market because they already fit established poultry and swine feed programs. Commercial use has been built over many years around essential oil blends, tinctures, and dry extracts from oregano, thyme, turmeric, ashwagandha, and astragalus, so buyers are more familiar with their handling, inclusion rates, and performance role. This established base is reinforced by sourcing depth and by the wider set of documented efficacy studies available for herbal materials than for newer functional categories.

The feed adaptogens market for mushroom adaptogens is projected to expand at a 9.8% CAGR through 2031, making them the fastest-growing source segment in the current forecast period. The feed adaptogens industry is giving mushroom-derived inputs more attention because species such as Ganoderma lucidum, Hericium erinaceus, Cordyceps militaris, and Agaricus bisporus now have a stronger research base across poultry and ruminant diets. Sustainability also supports this segment, as spent mushroom substrate and controlled cultivation models better align with circular production goals than some wild-harvested botanicals.

By Form: Powder Dominates as Liquid Delivery Accelerates in Intensive Systems

Powder accounted for the largest market share at 52.3% in 2025, reflecting how closely this format aligns with the dominant feed manufacturing systems used in commercial poultry and swine production. Dry premixes and pelleted feed lines are already designed to handle powders efficiently, which lowers changeover costs and keeps the format easy to integrate into existing routines. Powder also performs well in large-scale milling because many botanical extracts and mushroom polysaccharides can tolerate conditioning and pelleting temperatures when properly prepared.

The feed adaptogens market size for liquid formats is projected to grow at an 8.5% CAGR through 2031, making liquid the fastest-growing segment as intensive housing systems expand. Liquid delivery is attractive in broiler and layer operations because drinking water systems allow uniform dosing and a much faster response during heat stress events or disease pressure than a normal feed production cycle can provide. Water-soluble ashwagandha extracts and essential oil emulsions are becoming more relevant in these settings because farm managers can change dose levels quickly without waiting for a new feed batch.

By Livestock: Poultry Anchors Volume While Aquaculture Drives Incremental Demand

Poultry held the largest market share at 34.8% in 2025, making it the leading position in the feed adaptogens market due to the species’ scale, rapid turnover, and sensitivity to antibiotic restrictions. Broiler and layer operations consume large volumes of oregano and thyme blends, garlic extracts, and immune-support polysaccharides across starter, grower, and finisher programs, providing poultry with the broadest commercial base. Swine remained the next major outlet because post-weaning stress, enteric stability, and feed efficiency have become more pressing since the removal of routine antibiotic growth support in many systems. Ruminants still represent a smaller share, but they are becoming increasingly important for dairy and beef producers who need support with heat stress management and reproductive performance.

The feed adaptogens market size for aquaculture is forecast to grow at a 7.2% CAGR through 2031, making it the fastest livestock segment during the period. This growth is tied to immune stimulation in shrimp systems facing White Spot Syndrome and Early Mortality Syndrome, and to stress mitigation in salmonid farming, where density and temperature pressures can affect performance. Structural shift gives the feed adaptogens market a durable route into aquafeed, especially for botanical beta-glucans, morinda extracts, and astragalus polysaccharides. Suppliers that can generate species-specific efficacy data for shrimp and salmon feeds are likely to gain an advantage, as this market still requires more validation than poultry and swine applications.

By Function: Stress Mitigation Leads as Immune Enhancement Gains Formulation Priority

Stress mitigation held the largest market share at 46.1% in 2025, making it the leading function, as this use case has the broadest commercial relevance across livestock systems. Producers already understand the economic effect of heat stress, handling stress, transport pressure, and early-life stress, so products that target cortisol response and antioxidant defense are easier to justify in purchasing decisions. This demand base spans poultry, dairy, swine, cattle, and aquaculture, providing the segment with greater volume stability than narrower functional niches.

The feed adaptogens market size for immune enhancement is projected to grow at an 8.6% CAGR through 2031, making it the fastest-growing function as producers invest more in biosecurity and disease resilience. Beta-glucans from mushroom species, astragalus polysaccharides, and ginsenosides from Panax derivatives are among the most active compounds in this tier, and the feed adaptogens industry is using that functional focus to position higher-value products. The result is a clearer split between broad health-support formulas and more targeted immunity products that can be marketed around vaccine response and disease pressure management.

Geography Analysis

Asia-Pacific held the largest regional market share at 35.4% in 2025, keeping it at the center of the feed adaptogens market, as the region combines large livestock volumes with deep herbal raw material traditions. China remains the main anchor because its ban on antibiotic growth promoters shifted one of the world’s largest animal production systems toward alternative feed tools. India adds a second growth base through its expanding compound feed sector and through established Ayurvedic veterinary practice that now supports more industrial-scale product development. Japan and Australia are smaller in total volume, but both influence premium aquafeed innovation and biosecurity-led formulation standards. The feed adaptogens market in Asia-Pacific is therefore driven by both scale and quality progression, with Southeast Asian poultry and shrimp systems also upgrading feed specifications.

The Middle East is the fastest regional segment, with the feed adaptogens market projected to expand at an 8.9% CAGR through 2031 as food security policies drive livestock and aquaculture intensification. Saudi Arabia, the United Arab Emirates, and Turkey are using state-backed development programs and long-term supply arrangements to bring modern feed additives into poultry and fish production faster than many emerging regions. That shortens the standard adoption cycle and provides international suppliers with clearer entry points through organized procurement. Africa remains the smallest regional segment, but it offers a longer-term opportunity, as governments in South Africa, Egypt, and Nigeria work to boost livestock productivity amid rising urban demand for animal protein.

North America and Europe formed the next major demand bloc, supported by regulation, large integrated livestock systems, and buyer preference for cleaner animal production models. The United States leads North American demand because its poultry and swine industries already operate through large commercial networks that can quickly absorb validated non-antibiotic additives. Europe remains more regulated than any other region in the feed adaptogens market, since botanical additives must pass a strict authorization process that slows launches but raises confidence in approved products. Germany, France, and the United Kingdom are the main European demand centers, where retailer sourcing standards and sustainability requirements influence additive selection.

Competitive Landscape

The feed adaptogens market is moderately concentrated, with a leading group of multinational nutrition companies controlling important positions through broad phytogenic portfolios, while many specialized suppliers compete through narrower botanical expertise and regional reach. Cargill Incorporated stands out because Delacon Biotechnik GmbH provides it with an established phytogenic platform, recognized product lines, and integrated access to larger animal nutrition channels. DSM-Firmenich AG also remains influential through its natural additives and sensory compounds portfolio, even as its Animal Nutrition and Health business is in a divestiture process. This structure means a single dominant cluster does not control the feed adaptogens market, but the larger companies still shape standards in quality, scale, and route to market.

Competition in the feed adaptogens market is being defined by manufacturing expansion, portfolio broadening, and a move toward more defensible formulation platforms. In November 2025, Cargill, Incorporated completed a 50% capacity expansion at its Engerwitzdorf, Austria micronutrition facility, integrating Delacon Biotechnik GmbH production with Diamond V postbiotics and Provimi micronutrition capabilities. In August 2025, DSM-Firmenich AG opened a new Animal Nutrition and Health plant in Jadcherla, Hyderabad, India, which strengthened its regional footprint in Asia-Pacific. In February 2026, DSM-Firmenich AG also announced an agreement to divest its Animal Nutrition and Health business to CVC Capital Partners, while retaining a 20% stake, demonstrating that natural feed additive platforms still hold strategic value even during portfolio reshaping.

White space in the feed adaptogens market remains strongest in aquafeed-specific adaptogen products and in mushroom-derived ingredients produced to tighter quality and contamination standards. Companies such as Phytobiotics Futterzusatzstoffe GmbH, Ayurvet Limited, and Indian Herbs Specialties Private Limited remain relevant because they can serve narrower formulation needs that large multinationals may not address efficiently. The market is also moving toward more digitally linked delivery models, as precision livestock systems connect farm data with targeted feeding decisions, creating a better fit for specialized stress and immunity products.

Feed Adaptogens Industry Leaders

DSM-Firmenich AG

Cargill, Incorporated

Archer Daniels Midland Company

Alltech, Inc.

Novus International, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The European Commission issued Implementing Regulation (EU) 2026/178, authorizing eucalyptus tincture from Eucalyptus globulus Labill as a sensory feed additive for cattle, poultry, pigs, rabbits, and finfish under Regulation (EC) No. 1831/2003, expanding the commercially available herbal adaptogen roster in the European Union market.

- August 2025: DSM-Firmenich AG inaugurated a new Animal Nutrition and Health manufacturing plant in Jadcherla, Hyderabad, India, covering 11,200 square meters and incorporating a production line for mycotoxin risk management solutions alongside a new warehouse facility, strengthening the company's footprint for the India and Asia-Pacific feed adaptogens market.

- October 2024: DSM-Firmenich AG has opened a new Animal Nutrition and Health facility in Minas Gerais, Brazil. The plant, which includes adaptogens, has an annual production capacity of 100,000 metric tons of supplements for beef and dairy cattle. It aims to serve South American livestock producers seeking locally manufactured natural nutrition solutions.

Global Feed Adaptogens Market Report Scope

Adaptogens are non-toxic, plant-derived substances, such as herbs, roots, and mushrooms, that help the body resist and adapt to physical, chemical, and emotional stress. They work by regulating stress hormones like cortisol to restore overall physiological balance and homeostasis without causing crashes or side effects.

The Feed Adaptogens Market Report is segmented by source, herbal adaptogens, and mushroom adaptogens, form, powder, liquid, and encapsulated, livestock, poultry, swine, ruminants, aquaculture, and pets, function, stress mitigation, immune enhancement, and feed conversion, and geography, North America, South America, Europe, Asia-Pacific, Middle East, and Africa. The market forecasts are provided in terms of Value (USD).

| Herbal Adaptogens |

| Mushroom Adaptogens |

| Powder |

| Liquid |

| Encapsulated and Beadlet |

| Poultry |

| Swine |

| Ruminants |

| Aquaculture |

| Pets |

| Stress Mitigation |

| Immune Enhancement |

| Feed Conversion Improvement |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Source | Herbal Adaptogens | |

| Mushroom Adaptogens | ||

| By Form | Powder | |

| Liquid | ||

| Encapsulated and Beadlet | ||

| By Livestock Species | Poultry | |

| Swine | ||

| Ruminants | ||

| Aquaculture | ||

| Pets | ||

| By Function | Stress Mitigation | |

| Immune Enhancement | ||

| Feed Conversion Improvement | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is driving demand for feed adaptogens in animal nutrition?

The biggest drivers are antibiotic growth promoter restrictions, rising demand for natural production systems, heat-stress management, and the growing use of functional additives in aquaculture.

How large is the feed adaptogens space expected to become by 2031?

The Feed Adaptogens Market is projected to reach USD 3.10 billion by 2031, up from USD 1.97 billion in 2026, at a 9.5% CAGR over 2026-2031.

Which source category leads and which one is expanding the fastest?

Herbal adaptogens were the largest source segment with 61.2% share in 2025, while mushroom adaptogens are the fastest-growing source segment with a 9.8% CAGR through 2031.

Why is poultry still the main application area?

Poultry remains the largest livestock segment because of its global scale, short production cycle, and strong exposure to antibiotic restrictions and heat-stress-related performance loss.

Which region offers the strongest current demand base?

Asia-Pacific held the largest regional share at 35.4% in 2025 because of China’s scale, India’s feed expansion, and the region’s leading role in aquaculture output.

What is the main operational risk for suppliers and feed formulators?

Regulatory complexity and raw material quality risks remain the key challenges, especially where botanical approvals are slow and mycotoxin control is inconsistent across supply chains.

Page last updated on: