Organic Feed Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

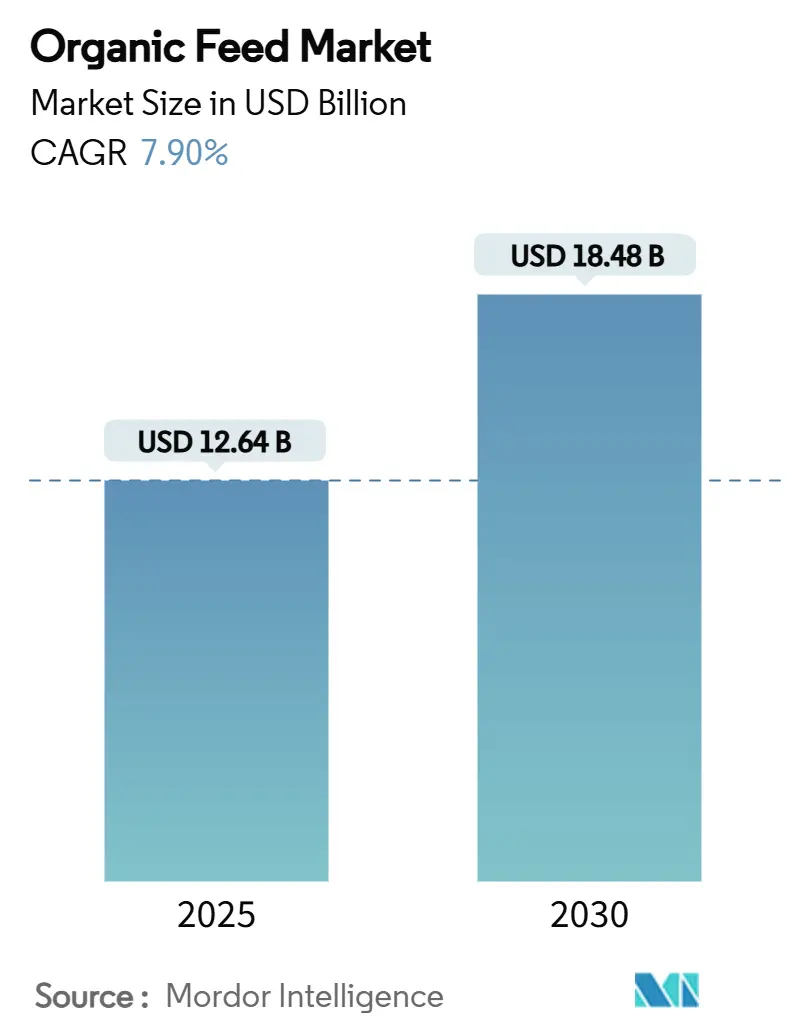

| Market Size (2025) | USD 12.64 Billion |

| Market Size (2030) | USD 18.48 Billion |

| Growth Rate (2025 - 2030) | 7.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Feed Market Analysis by Mordor Intelligence

The organic feed market size stands at USD 12.64 billion in 2025 and is forecast to grow at a 7.9% CAGR, pushing the value to USD 18.48 billion by 2030. Europe leads revenue generation, while Asia-Pacific records the fastest expansion pace. Premium price realization for certified animal protein, expanded alternative-protein approvals, and digital traceability technologies together underpin steady demand growth. Tight global supplies of certified organic crops, rising corporate climate targets, and region-specific feed ingredient policies further shape the competitive landscape. The organic feed market now rewards suppliers able to integrate sustainability metrics, protein diversification, and transparent sourcing into one coherent offer, thereby strengthening customer stickiness and supporting margin defense.

Key Report Takeaways

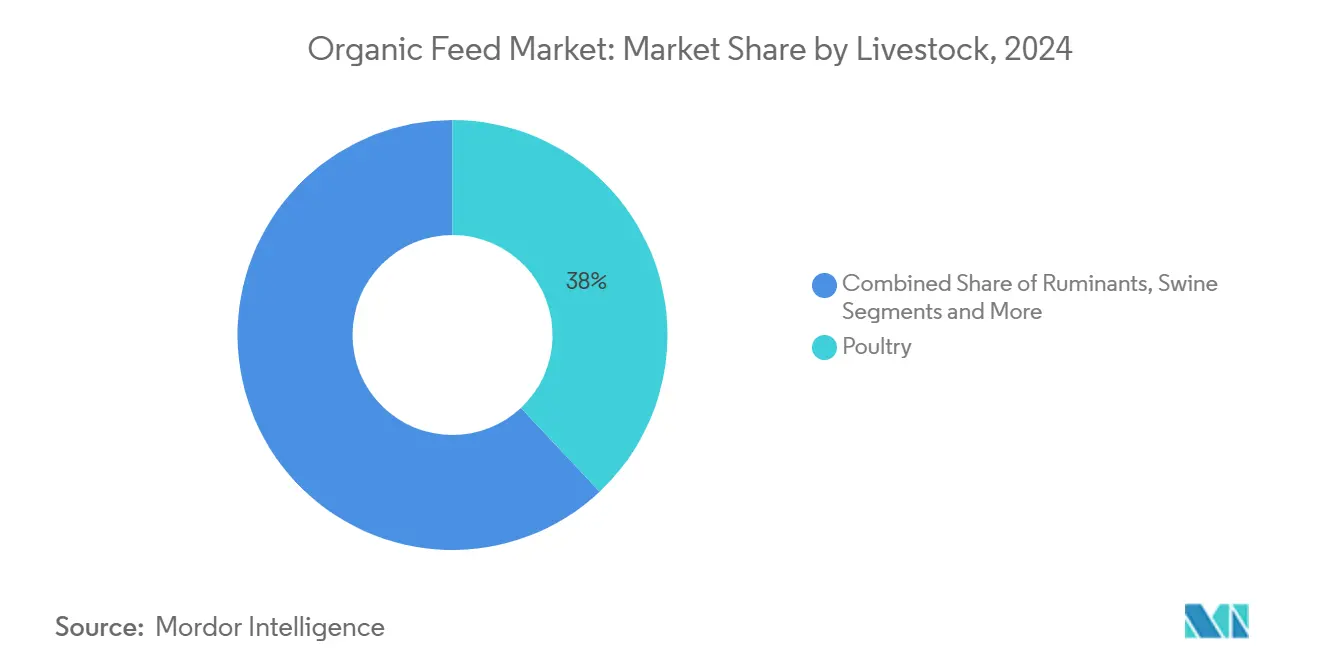

- By livestock, poultry held 38% the global organic feed market share in 2025, and aquaculture is projected to expand at a 10% CAGR to 2030.

- By ingredient type, cereals and grains commanded 46% of the organic feed market size in 2025, while Oilseeds and Meals (insect protein meal) are forecast to rise at a 14% CAGR through 2030.

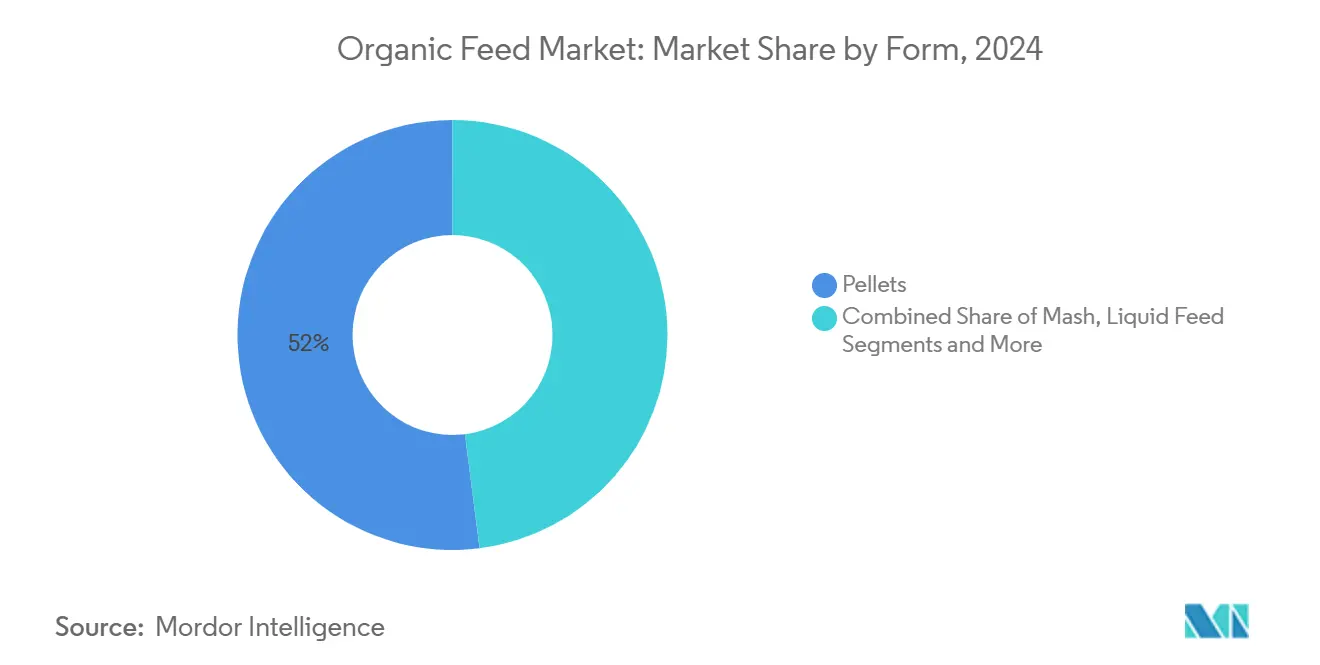

- By form, pellets accounted for 52% of the global organic feed market share in 2025, while liquid feed is projected to lead future growth at a 9.4% CAGR to 2030.

- By distribution channel, the direct-to-farm segment accounted for about 46% of the Global organic feed market size in 2024, and E-Commerce is projected to grow at 11.4% CAGR to 2030.

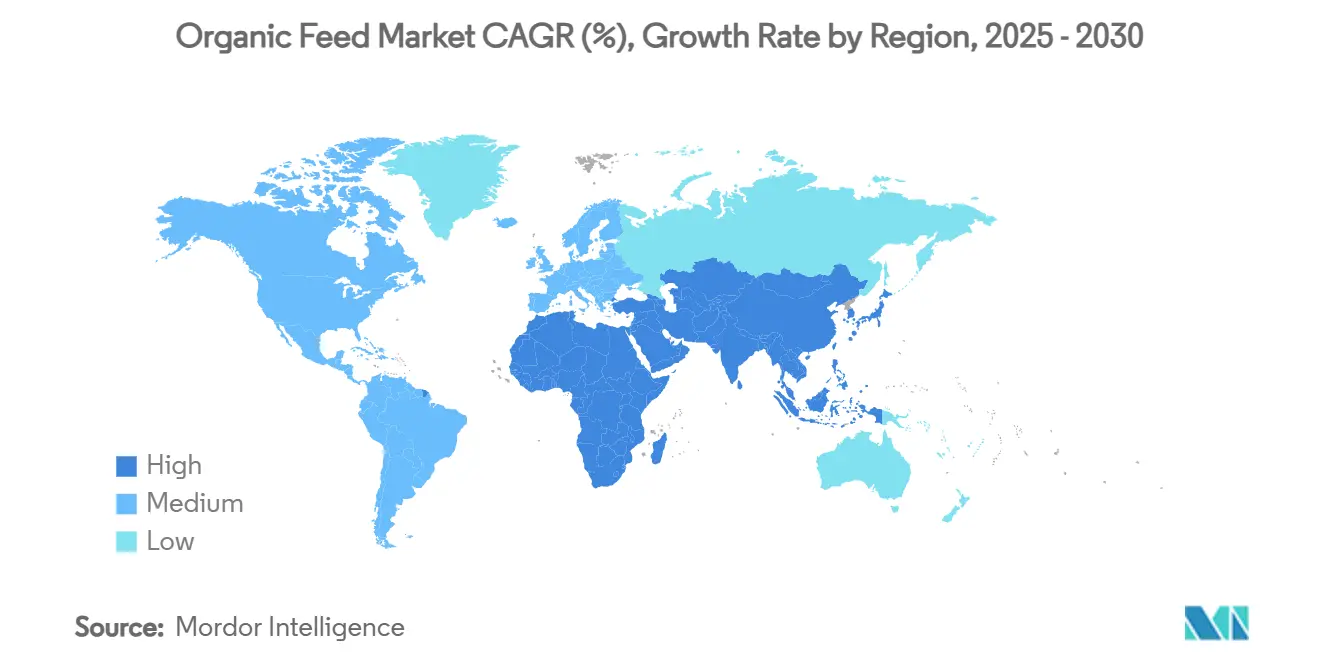

- By region, Europe captured 32% of the organic feed market size in 2025, and Asia-Pacific advances at a 9.9% CAGR to 2030.

Global Organic Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer preference for antibiotic-free protein | +1.8% | North America and Europe dominant, global spillover | Medium term (2-4 years) |

| Regulatory limits on Genetically Modified feed ingredients | +1.5% | Europe core, and Asia-Pacific follow-on | Long term (≥4 years) |

| Premium price realization for organic-certified products | +1.2% | Global developed markets | Short term (≤2 years) |

| Approval of insect protein meal for organic rations | +0.9% | Asia-Pacific leads, Europe, and North America adoption | Long term (≥4 years) |

| Blockchain-based traceability platforms | +0.7% | Europe and North America first movers | Medium term (2-4 years) |

| Corporate net-zero commitments covering feed emissions | +0.6% | Multinational supply chains worldwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Consumer Preference for Antibiotic-Free Protein

Stricter United States Department of Agriculture (USDA) organic livestock rules adopted in January 2025 formalize zero-antibiotic tolerances and have prompted conventional producers to convert to certified formulations that the organic feed market provides [1]Source: United States Department of Agriculture, “Organic Livestock and Poultry Standards,” usda.gov. In Europe, organic milk surpassed EUR 1.32 per liter (USD 1.39 per liter) in 2024, a premium that offsets higher feed costs. Salmon producers in Norway achieved 15 to 20% higher prices after switching to antibiotic-free, organic aquafeed, thereby incentivizing rapid adoption of aquaculture.

Regulatory limits on Genetically Modified feed ingredients

The European Union's continued enforcement of genetically modified feed regulations, coupled with Poland's reaffirmation of its 2030 ban deadline, is prompting feed compounders to invest in segregated grain sourcing and scale up purchases of organic corn and soybeans. This regulatory pressure is reshaping procurement strategies across the region. In parallel, South Korea and Japan are tightening GMO (Genetically Modified Organism) labelling standards, a move that indirectly drives demand for organic feed among export-oriented livestock and poultry producers seeking to meet evolving consumer expectations in high-value markets.

Premium Price Realization for Organic-Certified Products

Average United States retail organic milk exceeded USD 5.00 per half-gallon throughout 2024[2]Source: United States Department of Agriculture," Advertised Prices for Dairy Products at Major Retail Supermarket Outlets ending during the period of 7/11/2025 to 7/17/2025," usda.gov, about 45% higher than conventional milk, enabling producers to absorb elevated feed input costs. This pricing premium supports the viability of organic dairy operations despite higher formulation expenses. In parallel, pet food manufacturers, who often secure two- to threefold markups on their organic product lines, continue sourcing specialty inputs from the organic feed market. Their sustained demand reinforces pricing power for ingredient suppliers, particularly in niche segments such as organic grains, oilseeds, and functional additives.

Approval of Insect Protein Meal for Organic Rations

AAFCO (Association of American Feed Control Officials) cleared mealworm meal for organic pet food in 2024[3]Source: AAFCO (Association of American Feed Control Officials), "Mealworm-based ingredients for dog food now allowed in the U.S," aafco.org, and EFSA (European Food Safety Authority) approved similar use in aquaculture, opening a fast-growing ingredient channel. MYGroup launched its first Black Soldier Fly (BSF) production facility, with additional capacity set to come online in 2025. These developments are projected to ease pressure on traditional organic protein sources while expanding ingredient diversity for formulators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wide price gap with conventional feed | −1.4% | Highest in price-sensitive economies | Short term (≤2 years) |

| Tight supply of certified organic raw materials | −1.1% | Global, Asia-Pacific acute | Medium term (2-4 years) |

| Rise of regenerative but non-certified feed systems | −0.8% | North America and Europe | Long term (≥4 years) |

| Elevated mycotoxin risk due to no chemical preservatives | −0.6% | Humid regions worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Wide Price Gap With Conventional Feed

Organic corn averaged USD 7.20 per bushel versus USD 4.84 for conventional in 2024, highlighting a significant price gap of nearly 49% that sharply inflated formulation costs by around 50%. This disparity not only strained producer margins but also acted as a key deterrent to adoption, especially in markets where end consumers are highly price-sensitive. For instance, in Egypt, this dynamic contributed to a notable spike in red meat prices, as feed inflation cascaded down the value chain and reduced affordability across income groups.

Tight Supply of Certified Organic Raw Materials

Global organic acreage rose only 3.2% in 2024, falling short of rapidly growing demand. The limited expansion, combined with the mandatory three-year transition period for certification, continues to delay supply-side relief. As a result, the organic feed market remains constrained by the tight availability of certified organic raw materials, particularly for key inputs like grains, oilseeds, and plant-based protein meals. This structural imbalance leaves the market highly vulnerable to climatic fluctuations, trade disruptions, and price volatility, challenging feed manufacturers' ability to maintain consistent formulations and supply continuity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Livestock: Poultry Retains Scale, Aquaculture Accelerates

The poultry segment accounted for about 38% of the organic feed market size in 2025, driven by efficient feed-to-meat conversion and stable consumer demand for organic chicken and eggs. Aquaculture, though smaller, posts a 10% CAGR through 2030, reinvigorated by European Food Safety Authority (EFSA) insect protein approval and premium salmon pricing in northern Europe. Ruminants hold second place due to robust dairy premiums, while swine and pet mammals steadily expand, albeit from smaller bases. The organic feed market size for aquaculture is projected to grow during the forecast period, reflecting continuous system upgrades and retailer commitments to sustainable seafood.

Growing Asian seafood consumption, combined with stringent antibiotic rules, positions aquafeed formulators for differentiated offerings. Poultry players adopt multi-grain blends to moderate raw-material volatility, leveraging local cereal cultivation in Europe and North America. Aquaculture innovators dare deploy insect and microbial proteins to reduce reliance on fishmeal, thereby stabilizing llong-termsupply security. Across all animal groups, precision nutrition platforms track feed conversion in real-time, reinforcing data-driven procurement within the organic feed market.

By Ingredient: Cereals Anchor Formulations, Oilseeds and Meals Scales

Cereals and grains accounted for about 46% of the global organic feed market size in 2024, underlining the fundamental energy role of organic corn, wheat, and barley across monogastric diets. The organic feed market size for cereals and grains is set to expand with crop-rotation schemes boosting certified acreage. Insect protein meal, chiefly Black Soldier Fly larvae, is projected to drive the oilseeds and meals segment at a 14% CAGR, offering high digestibility and a circular-economy narrative that resonates with feed buyers.

Oilseed meals remain pivotal for amino-acid balancing, though constrained organic soybean acreage keeps prices elevated. Pulses and legumes gain share as agronomic tools that enhance soil nitrogen, supporting regenerative ambitions. Cakes and by-products, such as soybean meal and cottonseed cake, play a vital role in the organic feed market due to their high protein content and compatibility with organic certification standards. Nutritional supplements, vitamins, probiotics, and minerals command premium margins, differentiating branded products. Feed makers increasingly formulate ingredient matrices that deliver both nutritional value and lower embedded carbon, thereby aligning with corporate climate mandates.

By Form: Pellets Dominate, Liquids Target Precision Feeding

Pellets held 52% of the organic feed market share in 2024, favored for uniform density, lower segregation, and reduced wastage. Automated pellet coolers and die-life enhancements improve plant uptime, limiting cost escalation. Liquid feed, with the fastest growth rate of 9.4% CAGR, underpins micro-batch dosing and individualized nutrient delivery. Improved organic-compliant stabilizers mitigate spoilage risk, helping dairy and swine operations optimize intake.

Crumbles serve starter diets and chick rearing, while mash remains viable where capital for pelleting is scarce. Blocks and cakes retain a niche status among grazing ruminants that require slow-release energy. Precision livestock farming tools integrate viscosity sensors and cloud dashboards, ensuring liquid formulations remain consistent, reinforcing performance claims for the organic feed market.

By Distribution Channel: Digital Platforms Build Momentum

The direct-to-farm segment accounted for about 46% of the Global organic feed market size in 2024. This domination is due to technical service, formulation customization, and credit terms that align most closely with producer preferences. Regional distributors aggregate smaller-lot orders, easing inventory constraints for mid-tier farmers. Cooperatives harness collective bargaining to stabilize cereal supplies and reduce price risk.

E-commerce, now the fastest-growing channel, which is projected to grow at a CAGR of 11.4% during the forecast period, leverages mobile penetration and farm-management apps. Producers in remote Asia-Pacific provinces can now source certified pellets that were previously unavailable locally, expanding the organic feed market footprint overnight

Geography Analysis

Europe contributed 32% of the organic feed market size in 2024 and is projected to grow at a CAGR of 6.5% during the forecast period, driven by stringent Common Agricultural Policy subsidies and consumer willingness to pay sustainability premiums. Germany, France, and the United Kingdom together absorbed well over half the region’s organic feed demand, anchored in dairy and poultry verticals. Regional feed makers integrate blockchain to simplify cross-border certification, enhancing market transparency and trust.

Asia-Pacific, projected to expand at a 9.9% CAGR and hold about 22% global organic feed market share in 2024, benefits from rising disposable income and intensifying aquaculture activity. China and India dominate volume, while Indonesia and Vietnam show the strongest relative expansion. National food-safety reforms accelerate certified feed adoption, and domestic protein suppliers are investing in backward integration. De Heus’s new Indonesian mill exemplifies foreign participation aimed at capturing the organic feed market growth.

North America offers mature but resilient demand backed by stable organic food retail sales. The United States accounts for the majority share, helped by consolidated poultry and dairy sectors that sustain recurring orders. Canada grows through export-oriented beef programs leveraging organic pasture. Supply-side friction remains in consistent organic soybean meal availability, keeping formulation costs at a premium. Imports from South America partially bridge the gap, yet volatility persists during logistic disruptions.

Competitive Landscape

The organic feed market is moderate and is shaped by a core group of industry leaders that bring scale, traceability, and innovation to a space driven by strict certification standards. Cargill, Incorporated and Archer Daniels Midland Company play foundational roles by leveraging vertically integrated supply chains spanning from grain origination to feed milling to ensure ingredient transparency and consistent availability. Both firms are actively piloting blockchain systems aimed at reducing the cost and time associated with regulatory audits, enabling faster batch releases, and reinforcing customer trust in certified organic production.

Purina Animal Nutrition LLC., a division of Land O’Lakes, focuses on specialized livestock and companion animal nutrition, offering feed tailored to organic systems with a strong emphasis on animal health and performance. Their approach supports premium segments within the organic market that demand customized nutrition plans. Nutreco N.V., through its Trouw Nutrition unit, is expanding its organic-compatible offerings by integrating precision nutrition, sustainable sourcing, and alternative protein development, aligning closely with the environmental and traceability demands of organic farming practices.

Alltech complements this ecosystem with its suite of certified organic additives and minerals designed to support gut health and productivity in organic livestock. The company also promotes digital tools to monitor feed systems and enhance sustainability metrics on the farm. Strategic moves across these key players include securing forward contracts for organic raw materials, investing in low-carbon ingredient sourcing, and deploying AI-driven monitoring technologies. As regulatory and consumer pressure for transparency grows, competitive advantage in the organic feed sector hinges on harmonizing cost control with credible, measurable sustainability performance.

Organic Feed Industry Leaders

-

Cargill, Incoporated

-

Nutreco N.V.

-

Archer Daniels Midland Company

-

Alltech Inc

-

Purina Animal Nutrition LLC. (Land O'Lakes, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cargill, Incorporated and Mowi Feed achieved Aquaculture Stewardship Council (ASC Feed Certification), enhancing their ability to supply traceable, organic-compatible aquafeed for premium markets.

- January 2025: MYGroup launched its first Black Soldier Fly farm to expand insect protein production for organic feed applications. This move supports the growing demand for sustainable, organic-approved protein sources in livestock diets, aligning with the market’s shift toward circular and eco-friendly inputs.

- October 2024: Nutreco N.V. renewed its partnership with AgroCares to enhance NutriOpt On-site adviser, a mobile NIR feed-testing tool for real-time analysis of organic ingredients and precision formulation.

- August 2024: Nutreco N.V. opened the “Garden of the Future” in Thurgau, Switzerland, a phytotechnology center for developing plant-derived feed additives (phytocomplexes and bioactives) tailored for organic and sustainable animal feeds.

Global Organic Feed Market Report Scope

| Poultry |

| Ruminants |

| Swine |

| Aquaculture |

| Others |

| Cereals and Grains |

| Oilseeds and Meals |

| Pulses and Legumes |

| Cakes and By-Products |

| Forages |

| Nutritional Supplements |

| Pellets |

| Crumbles |

| Mash |

| Liquid Feed |

| Blocks and Cakes |

| Others |

| Direct to Farms |

| Distributors and Dealers |

| E-commerce |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Livestock | Poultry | |

| Ruminants | ||

| Swine | ||

| Aquaculture | ||

| Others | ||

| By Ingredient | Cereals and Grains | |

| Oilseeds and Meals | ||

| Pulses and Legumes | ||

| Cakes and By-Products | ||

| Forages | ||

| Nutritional Supplements | ||

| By Form | Pellets | |

| Crumbles | ||

| Mash | ||

| Liquid Feed | ||

| Blocks and Cakes | ||

| Others | ||

| By Distribution Channel | Direct to Farms | |

| Distributors and Dealers | ||

| E-commerce | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the organic feed market?

The organic feed market is valued at USD 12.64 billion in 2025.

How fast will the market grow?

It is projected to rise at a 7.9% CAGR, reaching USD 18.48 billion by 2030.

Which region leads revenue?

Europe holds about 32% of total revenue, driven by stringent certification rules and strong consumer demand.

Which animal segment is expanding the fastest?

Aquaculture posts the highest CAGR at 10%, benefiting from premium salmon and shrimp demand.

Page last updated on: