Forage Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 97.80 Billion |

| Market Size (2031) | USD 128.30 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Forage Feed Market Analysis by Mordor Intelligence

The forage feed market size was valued at USD 93.20 billion in 2025 and estimated to grow from USD 97.80 billion in 2026 to reach USD 128.30 billion by 2031, at a CAGR of 5.60% during the forecast period (2026-2031). Larger dairy herds in China, multi-site beef feedlots in Brazil, and policy-driven methane targets across Canada and the European Union are pushing nutrition managers to secure multi-year offtake contracts that guarantee protein specifications, thereby reducing exposure to spot-market volatility. Export-oriented suppliers in the United States, Australia, and Spain are increasing investments in double-compression and pelletizing lines that raise container density by up to 40%, helping them defend margins against high trans-Pacific freight rates. Carbon-credit upside from nitrogen-fixing legumes, together with feed-grade biochar blends that cut methane by double-digit percentages, is adding new revenue streams for growers while giving processors a pathway to premium-priced, low-carbon meat and dairy products.

Key Report Takeaways

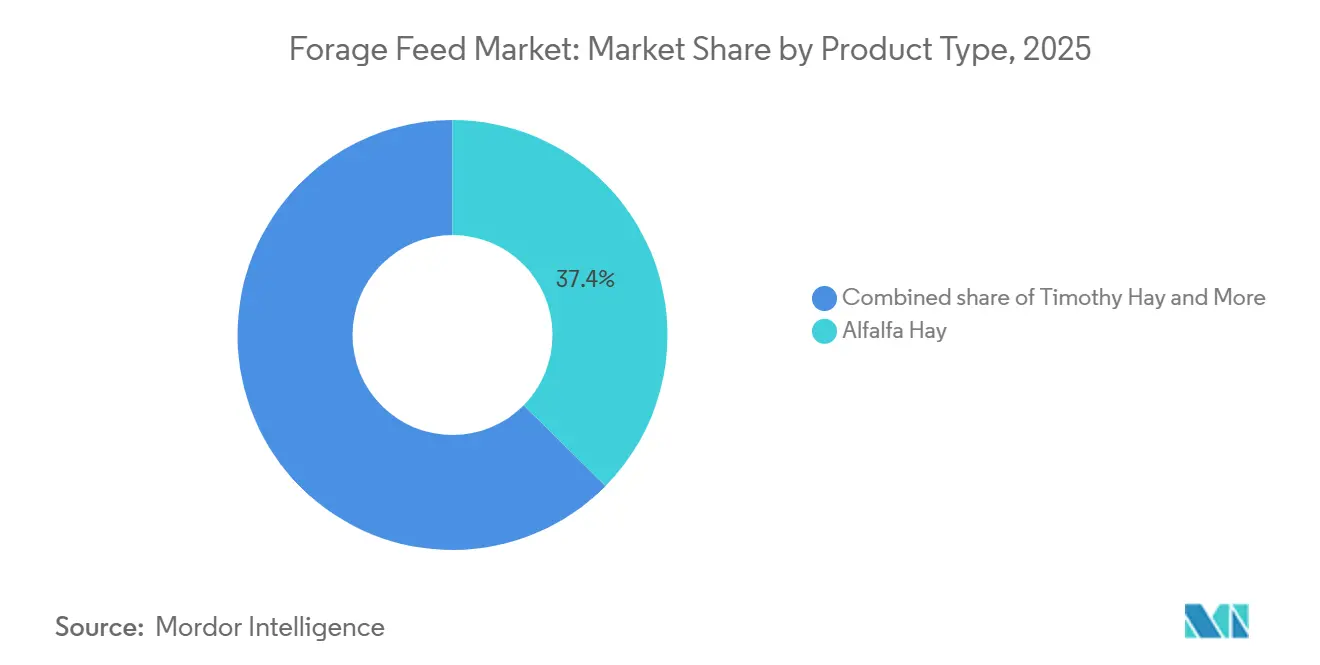

- By product type, alfalfa hay was the largest segment, led with 37.4% of the forage feed market share in 2025, while clover and other legume hay will be the fastest-growing segment and are projected to expand at a 7.8% CAGR through 2031.

- By livestock type, Dairy cattle were the largest segment, accounting for 42.6% of the forage feed market size in 2025, while poultry will be the fastest-growing segment, advancing at a 6.9% CAGR through 2031.

- By form, bales were the largest segment, accounting for 47.0% of the forage feed market share in 2025. Pellets and cubes will be the fastest-growing segment, advancing at an 8.4% CAGR over 2026-2031.

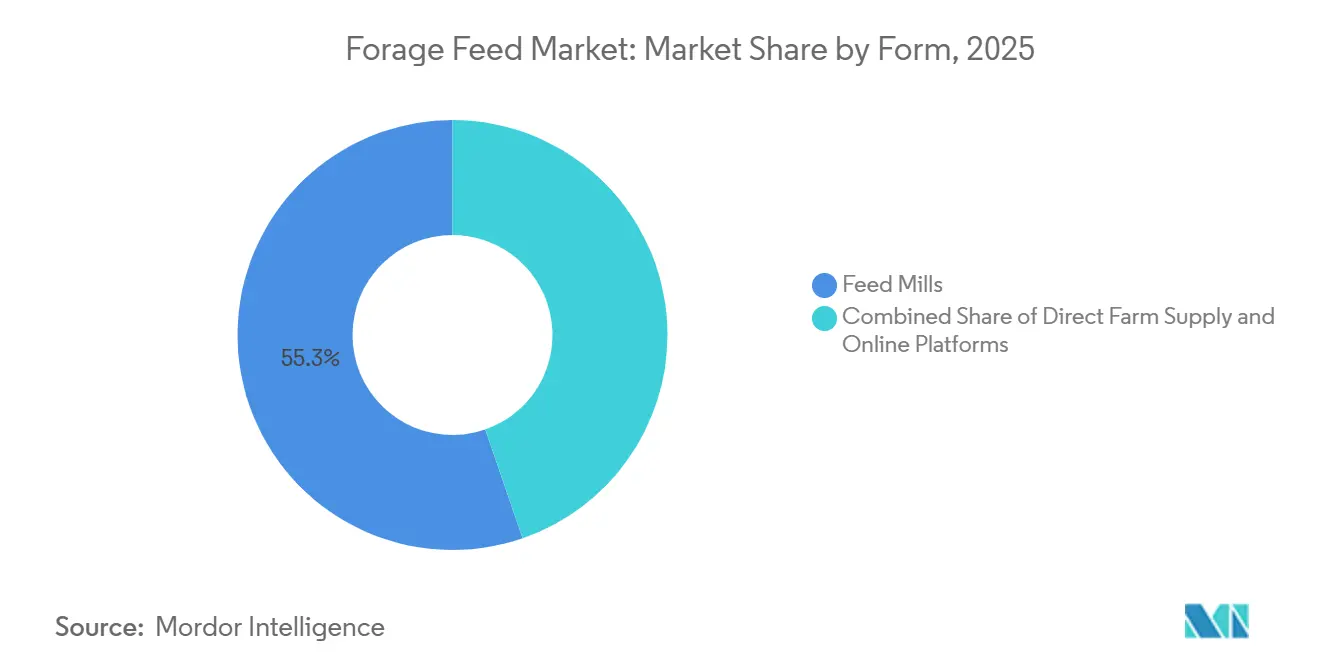

- By distribution channel, Feed mills were the largest segment, feed mills accounted for 55.3% of the forage feed market share in 2025, whereas online platforms are set to grow at a 9.2% CAGR through 2031.

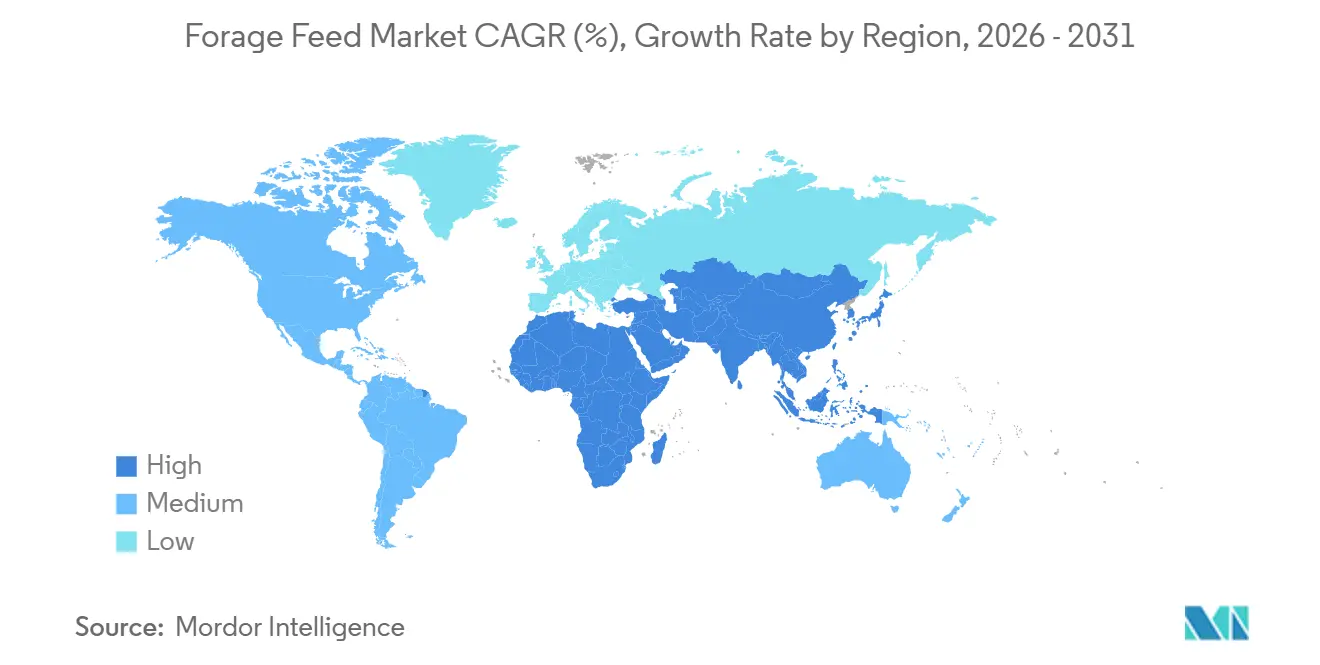

- By geography, North America retained the largest regional position 33.7% of the forage feed market share in 2025, Asia-Pacific is projected to achieve the fastest growth, with a CAGR of 6.3% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Forage Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding large-scale dairy and beef operations | +1.8% | North America, South America, and Asia-Pacific | Long term (≥ 4 years) |

| Rising demand for high-protein meat and dairy | +1.6% | Global, strongest in Asia-Pacific and Africa | Long term (≥ 4 years) |

| Methane mitigation policies favoring high-fiber forage | +0.9% | Europe, Canada, New Zealand, and spillover to North America | Medium term (2-4 years) |

| Carbon-credit upside from nitrogen-fixing forage legumes | +0.6% | North America, Europe, and Australia | Medium term (2-4 years) |

| In-field mobile baler-wrapper robots boosting harvest quality | +0.4% | Australia, Germany, Japan, and early adoption in North America | Long term (≥ 4 years) |

| Feed-grade biochar blends improving forage digestibility | +0.3% | United States, South Korea, and New Zealand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Large-Scale Dairy and Beef Operations

Vertical integration among large-scale dairies and beef feedlots is transforming procurement practices. Operations with more than 5,000 head are increasingly entering into multi-year forage contracts. These agreements ensure consistent volume and protein specifications in exchange for fixed pricing, reducing exposure to spot-market fluctuations. This approach enables nutritionists to formulate rations with consistent dry matter content, improving feed conversion ratios by 8% to 12% in intensive dairy systems [1]Source: U.S. Department of Agriculture Economic Research Service, “Dairy Data,” ers.usda.gov. In these regions, state-backed cooperatives are constructing centralized hay-storage facilities with capacities of up to 50,000 metric tons to mitigate seasonal price volatility. This reflects the perception among Asian dairy processors that North American forage is a premium input, justifying container freight rates exceeding USD 150 per metric tons.

Methane-Mitigation Policies Favoring High-Fiber Forage

Governments in Canada, the European Union, and New Zealand are implementing enteric methane reduction targets that encourage dairy and beef producers to incorporate higher proportions of digestible fiber into livestock rations. This shift promotes the use of legume-based forages over grain-heavy concentrates. This initiative provides a revenue stream that can offset up to 8% of total feed costs for operations that document baseline and post-intervention emissions. Policy incentivizes the adoption of high-fiber forage blends that reduce enteric fermentation and qualify for rebates under the country's Emissions Trading Scheme. Additionally, feed-grade additives such as 3-nitrooxypropanol (3-NOP) and biochar are being tested in combination with legume hay to achieve methane reductions exceeding 20%.

Carbon-Credit Upside from Nitrogen-Fixing Forage Legumes

Legume forages such as alfalfa and clover fix atmospheric nitrogen through symbiotic root nodules, reducing reliance on synthetic fertilizers and promoting soil-carbon sequestration. The European Union's Carbon Border Adjustment Mechanism, set to be phased in starting 2026, will impose tariffs on imported agricultural products based on their embedded emissions. This policy creates an incentive for hay exporters in North and South America to document the carbon-sequestration benefits of legume-based forage systems. By doing so, they can avoid penalty fees, which could reach EUR 50 (USD 54) per metric ton of CO2-equivalent.

Rising Demand for High-Protein Meat and Dairy

The increasing global demand for high-protein foods, including meat and dairy, is a key driver of the forage feed market. Factors such as population growth, rising incomes, and urbanization are driving a shift in consumer preferences toward protein-rich diets featuring beef, poultry, milk, and other animal products. To meet this growing demand, livestock producers need to enhance animal productivity, which depends on a steady supply of high-quality forage feeds like alfalfa, ryegrass, corn silage, and clover. These feeds play a vital role in maintaining animal health, improving growth rates, and increasing milk yields, making them indispensable in modern livestock systems. For instance, in countries such as the United States and China, large-scale dairy and beef industries heavily depend on alfalfa hay and silage to sustain high production levels, driving significant demand for forage crops.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weather volatility and drought risk | -1.8% | National, most acute in Abu Dhabi, and Dubai coastal zones | Short term (≤ 2 years) |

| Competition for arable land with cash crops | -1.4% | National, affecting all species except the oyster | Medium term (2-4 years) |

| Stricter phytosanitary barriers on cross-border hay trade | -1.2% | National, with the highest exposure in the shrimp and salmon segments | Short term (≤ 2 years) |

| Shift toward fermented concentrates over loose forage | -1.0% | National, with only two PCR laboratories serving the entire country | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Weather Volatility and Drought Risk

Consecutive drought years in the United States Great Plains, Australia, and Argentina reduced alfalfa and grass-hay yields by 10% to 15% in 2024 and 2025. This compelled importers in Japan, South Korea, and the United Arab Emirates to diversify their sourcing strategies and accept higher landed costs. In mid-2025, the United States Drought Monitor classified 42% of the alfalfa-producing counties in California, Nevada, and Idaho as experiencing severe to exceptional drought conditions. This resulted in an average 18% reduction in first-cutting yields and drove spot-market prices for premium alfalfa above USD 320 per metric ton, representing a 25% increase from 2024 levels [2]Source: NOAA National Centers for Environmental Information, “U.S. Drought Monitor,” ncei.noaa.gov. Climate models predict that by 2030, extreme-heat days exceeding 35 degrees Celsius will increase by 20% to 30% across major forage-producing regions.

Stricter Phytosanitary Barriers on Cross-Border Hay Trade

China, Japan, Saudi Arabia, and the United Arab Emirates have implemented stricter inspection protocols for imported hay to prevent the spread of invasive pests and plant diseases. In 2024, China's General Administration of Customs introduced revised alfalfa import standards mandating heat treatment at 56 degrees Celsius for 30 minutes or methyl bromide fumigation. This regulation has compelled United States exporters to retrofit compression facilities with thermal chambers, incurring costs exceeding USD 2 million per site. The International Plant Protection Convention is working on harmonized standards for phytosanitary measures in the forage trade. These standards are not projected to be implemented until 2027, leaving exporters to manage a diverse set of country-specific regulations with varying technical requirements and enforcement practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Alfalfa hay was the largest segment, led with 37.4% of the forage feed market share in 2025, underscoring its position as a preferred forage for high-producing dairy cattle. This preference is attributed to its crude protein content exceeding 18% and a relative feed value above 150. Market incentives, including voluntary carbon credit schemes and regulatory emission caps, are encouraging intensive cattle farms to allocate larger budgets to high-fiber, low-protein blends that enhance rumen function. Suppliers are now offering probiotic-infused inoculants and moisture-controlled wrapping, which can extend shelf life by up to eight months.

Clover and other legume hay will be the fastest-growing segment and are projected to expand at a 7.8% CAGR through 2031, marking the fastest growth among all product types. This growth is driven by clover's nitrogen-fixing properties, which enable growers to eliminate the annual synthetic fertilizer costs of USD 80-120 per acre. Additionally, clover supports soil carbon sequestration, qualifying growers for carbon offset payments under protocols administered by Verra and the Climate Action Reserve. The symbiotic root nodules of clover fix atmospheric nitrogen, reducing reliance on synthetic fertilizers and contributing to verified carbon offsets.

By Livestock Type: Poultry Adoption Accelerates on Cage-Free Mandates

Dairy cattle were the largest segment, accounting for 42.6% of the forage feed market share in 2025, driven by intensive operations in North America, Europe, and the Asia-Pacific. These operations formulated total mixed rations with 40% to 55% forage inclusion to support rumen health and maintain milk-fat content above 3.8%. Japan and South Korea collectively imported 450,000 metric tons of timothy and alfalfa hay in 2025. Japanese dairy cooperatives specified protein content above 18% and moisture levels below 12% to optimize milk-fat yields in Holstein herds, which averaged 10,000 kilograms per lactation. The European Union's Farm to Fork strategy aimed to reduce agricultural greenhouse gas emissions by 30% by 2030.

Poultry will be the fastest-growing segment, advancing at a 6.9% CAGR through 2031. Integrators in the United States, Europe, and Southeast Asia are incorporating chopped alfalfa into layer rations to meet cage-free egg standards, which require a minimum fiber intake of 5% to 7% by weight [3]Source: Food and Agriculture Organization, “Livestock Feed and Poultry Production,” fao.org . Population growth and rising per capita incomes in Asia and Africa are driving increased animal protein consumption. Middle-income households in countries such as India, Indonesia, and Nigeria are transitioning from plant-based diets to include poultry at rates that exceed domestic forage production capacity. Chopped and chaffed forage is particularly appealing to poultry integrators blending alfalfa into layer rations. Additionally, dairy operations use fermented haylage and silage additives to maintain nutrient density above 65% total digestible nutrients during extended storage periods.

By Form: Pellets and Cubes Cut Freight and Spoilage

Bales were the largest segment, accounting for 47.0% of the forage feed market share in 2025, highlighting their dominance in domestic markets where producers focus on minimizing processing costs, and buyers tolerate the handling inefficiencies of loose forage. In June 2024, Al Dahra ACX commissioned a new double-compress line in Ellensburg, Washington, adding 180,000 metric tons of annual capacity. This upgrade allows the company to load 26 metric tons of compressed alfalfa per 40-foot container, compared to 18 metric tons for standard bales, resulting in a density improvement that reduces per-ton freight costs by USD 35 to USD 50. Since 2023, Chinese equipment manufacturers, such as Henan RICHI, have significantly reduced pellet mill capital costs, driving broader adoption and reinforcing the forage feed market's shift toward densified formats.

Pellets and cubes will be the fastest-growing segment, advancing at an 8.4% CAGR over 2026-2031, the fastest growth rate among all forms. Export-focused suppliers are increasingly compressing forage to reduce container freight costs by 30% to 40% and to minimize spoilage during transoceanic shipments to markets such as Japan, South Korea, and the Middle East. In 2025, Standlee Premium Products expanded its pelletized forage sales through e-commerce platforms, partnering with Amazon and Chewy to reach small-equine and hobby-farm buyers.

By Distribution Channel: Online Platforms Disrupt Traditional Wholesale

Feed mills were the largest segment, feed mills accounted for 55.3% of the forage feed market share in 2025, benefiting from established relationships with large dairy and beef operations that purchase between 500 and 2,000 metric tons annually under multi-year contracts. Direct farm supply, particularly prominent in regions like Australia and the western United States, attracts large operators by offering customized blends and just-in-time deliveries. Additionally, digital storefronts are gaining traction, especially for niche products such as equine cubes and organic alfalfa flakes, supported by drop-shipment logistics and traceability applications.

Online platforms are set to grow at a 9.2% CAGR through 2031, representing the fastest growth among all channels. This growth is driven by small equine, hobby-farm, and organic-certified buyers increasingly opting for direct-from-producer ordering, which eliminates wholesale markups of 15% to 25% and allows for customization of protein content, cutting length, and packaging size. Early adopters utilizing data analytics to analyze transactional patterns have reported margin improvements, highlighting channel diversification as a key strategic advantage in the forage feed market.

Geography Analysis

North America retained the largest regional position 33.7% of of the forage feed market share in 2025. This growth is supported by industrial-scale dairy complexes, advanced precision agriculture infrastructure, and strong export pipelines. The region faces challenges such as plateauing herd expansions and increased land-use competition. The United States leads production, with California and Arizona exporting dehydrated alfalfa to Asian markets through cost-efficient logistics corridors. Canada benefits from cool-season crop advantages but faces margin pressures due to high freight rates. In Mexico, the forage feed market is gradually expanding as integrated beef processors enhance feeding protocols.

Asia-Pacific will be the fastest-growing forecast to post the quickest 6.3% CAGR through 2031. This growth is driven by population increases, dietary shifts toward Western preferences, and the rapid adoption of vertical livestock integration. China experienced a significant rise in premium compressed alfalfa bale imports during 2024-2025, fueled by intensive dairy operations in Inner Mongolia. In India, the expanding cooperative dairy network, supported by investments in cold-chain infrastructure, is driving demand for fermented haylage and protein-enriched pellets. Australia, a key exporter, faces challenges from recurring droughts and evolving water-allocation policies, which may limit production growth but position water-efficient legumes as strategic crops in the forage feed market.

Europe shows growth potential, driven by sustainability mandates and reforms under the Common Agricultural Policy, which promote nitrogen-fixing legumes and carbon credit initiatives. Germany, France, and the Netherlands maintain strong dairy industries, but phytosanitary restrictions on United States hay imports are encouraging localized sourcing. In Eastern Europe, markets like Hungary are benefiting from new processing investments, such as ADM’s Vitafort joint venture, which supports self-sufficiency goals.

Competitive Landscape

The forage feed market demonstrates moderate concentration, with the top five players, including ADM, Land O'Lakes, Inc., Al Dahra ACX, Inc., Anderson Hay, and Wilbur-Ellis Company LLC, leaving significant opportunities for regionally established firms and emerging technology-driven entrants. Multinational companies such as ADM, Cargill, and Wilbur-Ellis adopt vertical integration strategies that encompass upstream production, midstream processing, and downstream distribution to optimize margins across the value chain.

Regional leaders like Al Dahra ACX and Anderson Hay focus on export logistics, origin certification, and high-compression baling techniques to reduce ocean freight costs. Meanwhile, technology-driven disruptors emphasize innovations such as robotic bale handling, blockchain-based traceability, and carbon-credit aggregation. These advancements enable them to generate additional revenue streams beyond traditional tonnage sales. Sustainability considerations are increasingly shaping procurement decisions, with buyers evaluating factors such as emissions and water-use efficiency. This trend is driving suppliers to invest in solutions like drip irrigation, solar drying, and renewable-energy-powered pellet mills.

Consolidation remains a key trend as mid-tier firms seek to achieve scale efficiencies. For instance, the Andersons' acquisition of a stake in Skyland Grain expanded its storage capacity and enhanced its origination capabilities across the United States Plains. Geographic diversification also serves as a strategic safeguard against climatic and regulatory risks, prompting cross-border collaborations such as ADM's partnership with Vitafort in Hungary. Overall, competitive dynamics in the forage feed market favor companies that combine agronomic expertise with technological innovation, ensuring consistent product quality while minimizing environmental impacts.

Forage Feed Industry Leaders

ADM

Land O'Lakes, Inc.

Al Dahra ACX, Inc.

Anderson Hay

Wilbur-Ellis Company LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Millborn Seeds subsidiary Renovo Seed announced the addition of OptiHarv, a new forage mix, to its portfolio in 2024. The mix combines millets, peas, beans, barley, and brassicas to produce high tonnage for baleage, haylage, or grazing. The blend enables multiple harvests from a single field while yielding high-quality Total Mixed Ration (TMR) throughout the growing season.

- August 2024: Charoen Pokphand Group and COFCO formed a strategic partnership to enhance collaboration in agriculture, food production, and global supply chains. This partnership strengthens CP Group's forage feed operations in China through improved access to raw materials and logistics networks, expanding its presence in the feed market.

- September 2023: MAS Seeds launched a new range of forage mixtures and specialized blends, including MAS4 NUTRI forage, which is rich in legumes and would be used to increase animal diet.

Global Forage Feed Market Report Scope

Forage feed consists of crops that can be fed directly to livestock or slightly processed by partial drying or pre-digestion. The Forage Feed Market Report is Segmented by Product Type (Alfalfa Hay, Timothy Hay, and More), by Livestock Type (Dairy Cattle, Beef Cattle, and More), by Form (Bales, Pellets, and More), by Distribution Channel (Feed Mills, Direct Farm Supply, and More), and by Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Alfalfa Hay |

| Timothy Hay |

| Clover & Other Legume Hay |

| Silage |

| Haylage |

| Other Forage (grass mix, crop residues) |

| Dairy Cattle |

| Beef Cattle |

| Poultry |

| Equine |

| Swine |

| Other Livestock (sheep, goats, camelids) |

| Bales |

| Pellets and Cubes |

| Chopped/Chaffed Forage |

| Fermented Haylage and Silage Additives |

| Feed Mills |

| Direct Farm Supply |

| Online Platforms |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Alfalfa Hay | |

| Timothy Hay | ||

| Clover & Other Legume Hay | ||

| Silage | ||

| Haylage | ||

| Other Forage (grass mix, crop residues) | ||

| By Livestock Type | Dairy Cattle | |

| Beef Cattle | ||

| Poultry | ||

| Equine | ||

| Swine | ||

| Other Livestock (sheep, goats, camelids) | ||

| By Form | Bales | |

| Pellets and Cubes | ||

| Chopped/Chaffed Forage | ||

| Fermented Haylage and Silage Additives | ||

| By Distribution Channel | Feed Mills | |

| Direct Farm Supply | ||

| Online Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the forage feed market?

The forage feed market size was valued at USD 93.20 billion in 2025 and estimated to grow from USD 97.80 billion in 2026 to reach USD 128.30 billion by 2031, at a CAGR of 5.60% during the forecast period (2026-2031).

Which product category dominates sales?

Alfalfa hay held 37.4% of forage feed market share in 2025 due to high crude-protein levels that suit intensive dairy rations.

Which livestock segment is growing the fastest?

Poultry forage use is advancing at a 6.9% CAGR through 2031 as cage-free standards require higher dietary fiber.

Which distribution channel shows the highest growth?

Online platforms are projected to expand at a 9.2% CAGR, driven by small equine and poultry owners ordering directly from producers.

Page last updated on: