Laryngoscope Blades and Handles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

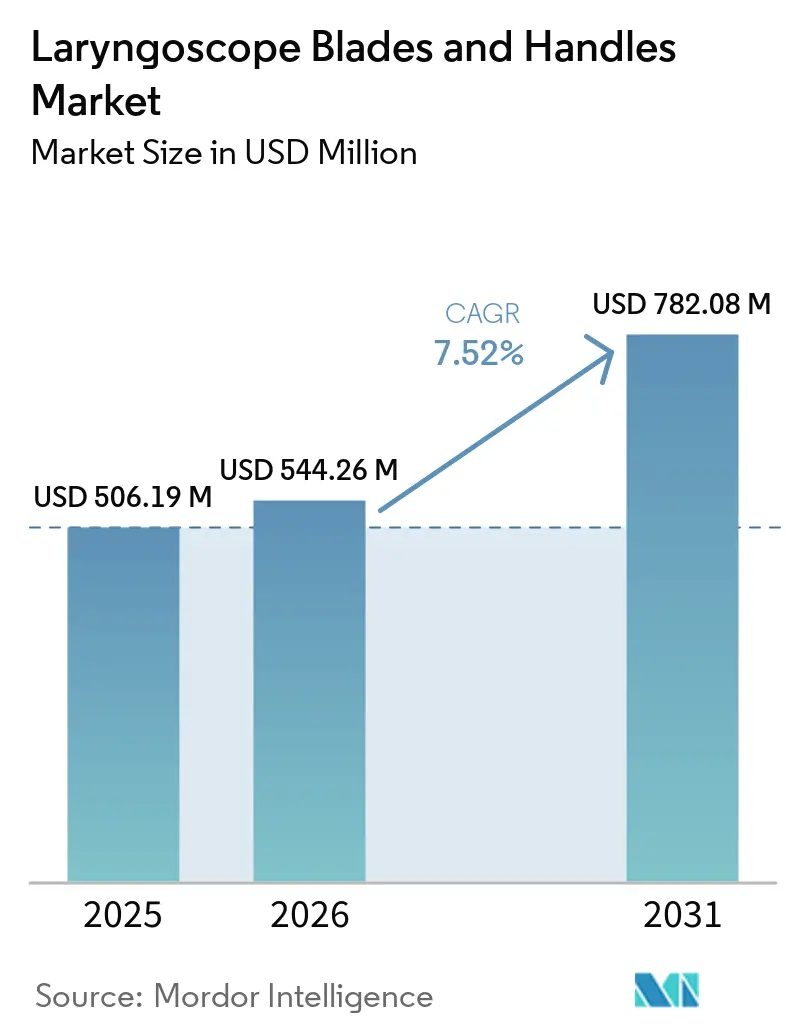

| Market Size (2026) | USD 544.26 Million |

| Market Size (2031) | USD 782.08 Million |

| Growth Rate (2026 - 2031) | 7.52% CAGR |

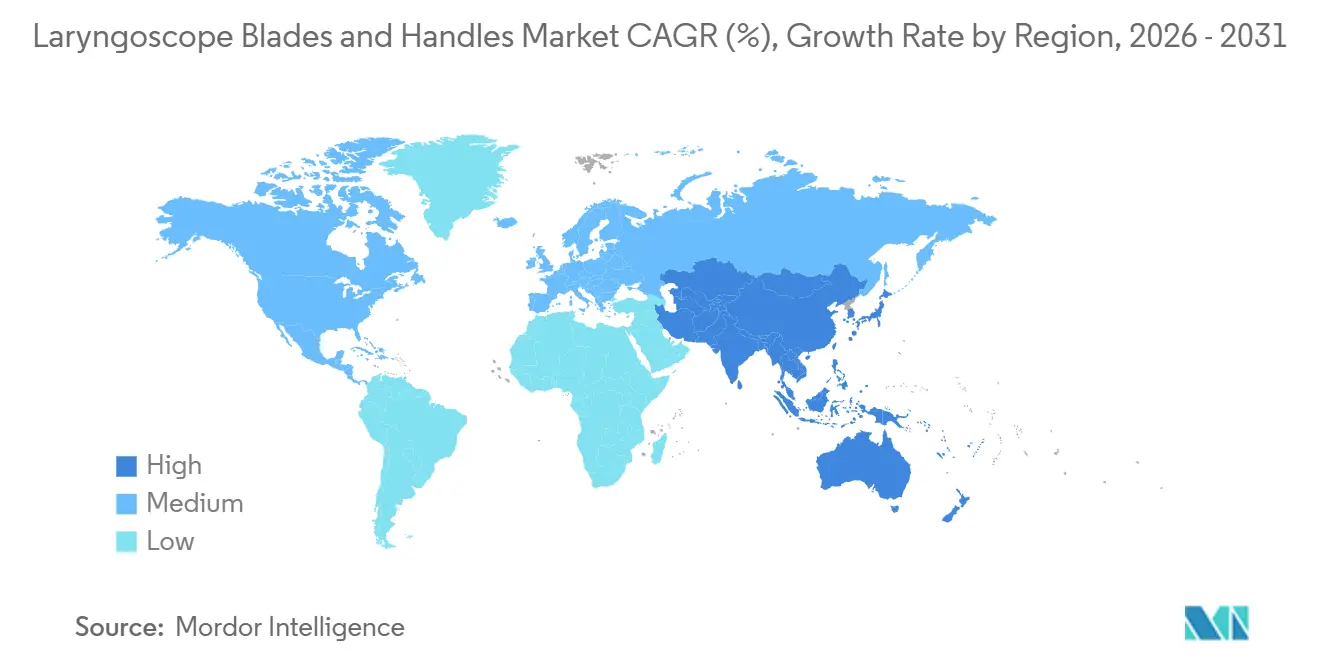

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

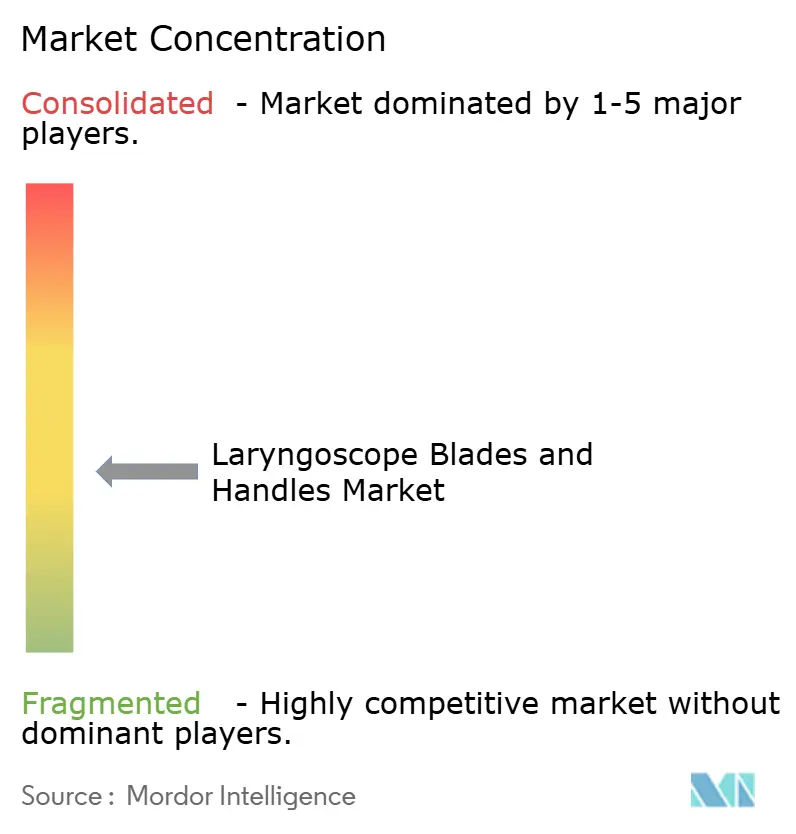

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laryngoscope Blades and Handles Market Analysis by Mordor Intelligence

The Laryngoscope Blades And Handles Market size is expected to increase from USD 506.19 million in 2025 to USD 544.26 million in 2026 and reach USD 782.08 million by 2031, growing at a CAGR of 7.52% over 2026-2031.

The market is being supported by a steady rise in airway intervention demand, as chronic respiratory diseases affected 81.7 million people in the WHO European Region in 2025, while South-East Asia reported that these conditions accounted for nearly 12% of all deaths, which keeps emergency intubation volumes structurally elevated. The laryngoscope blades and handles market is also shifting toward single-use devices because infection control concerns now extend from blades to handles, with reusable handles still showing meaningful contamination risk after routine wipe disinfection in published clinical material. The laryngoscope blades and handles market is moving further toward video-assisted systems as recent clinical evidence in adults and neonates showed better first-attempt success and lower airway trauma, while newer AI-guided systems are lowering operator workload in difficult airway care. The laryngoscope blades and handles market is also benefiting from the expansion of ambulatory and emergency workflows, where compact, integrated, and shelf-stable device formats fit facilities that lack full sterile processing capacity and need predictable per-case device availability. At the same time, environmental scrutiny around disposable plastics, stricter reusable-device reprocessing requirements, and the exit of Baxter from Welch Allyn laryngoscope lines are reshaping competition and product roadmaps across the laryngoscope blades and handles market.

Key Report Takeaways

- By product type, laryngoscope blades held 65.31% of the laryngoscope blades and handles market share in 2025, while laryngoscope handles are projected to record the highest CAGR at 9.38% through 2031.

- By material, stainless steel accounted for 55.24% of demand in 2025, while hybrid and composite material systems are forecast to expand at an 8.52% CAGR through 2031.

- By usage, adult-use configurations led with 62.52% share in 2025, while pediatric use is set to advance at an 8.25% CAGR through 2031.

- By end user, hospitals captured 60.62% of demand in 2025, while ambulatory surgical centers are projected to grow at a 9.25% CAGR through 2031.

- By geography, North America held 39.22% share in 2025, while Asia-Pacific is forecast to register the fastest CAGR at 9.15% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laryngoscope Blades and Handles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Airway Demand From Respiratory Disease Burden | +1.8% | Global, acute in South-East Asia, South America, and Sub-Saharan Africa | Long term (≥ 4 years) |

| Shift Toward Single-Use Blades to Reduce Cross-Contamination Risk | +1.5% | North America and Europe leading, APAC with fast-growing adoption | Medium term (2-4 years) |

| Adoption of Video-Assisted and Fiber-Optic Systems in Difficult Airway Care | +1.4% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Expansion of Emergency, Ambulatory, and Pre-Hospital Airway Workflows | +1.2% | North America, Europe | Short term (≤ 2 years) |

| Preference for Low-Fog, High-Visibility Blade Systems in High-Throughput Settings | +0.8% | North America and Europe high-volume operating rooms | Short term (≤ 2 years) |

| Rising Demand for Ergonomic Handle Architectures That Reduce Clinician Fatigue | +0.7% | North America, Europe, APAC with Japan and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Airway Management Demand From Respiratory Disease Burden

The laryngoscope blades and handles market is seeing durable procedure support from the rising burden of chronic respiratory disease across both developed and emerging care systems. WHO and the European Respiratory Society reported in June 2025 that 81.7 million people in the WHO European Region were living with chronic respiratory diseases, with 6.8 million new diagnoses each year and COPD accounting for 80% of related deaths. The same publication also placed the cost of underdiagnosis above USD 20 billion annually, which points to a large pool of patients who may still present late and require acute airway support rather than early outpatient management. In South-East Asia, the burden is even more important for future volume because WHO reported in 2025 that chronic respiratory diseases were responsible for nearly 12% of all deaths, which keeps emergency and critical care intubation demand structurally elevated in systems that still have uneven ICU access. Much of that installed base still relies on conventional reusable stainless-steel systems, so the first major upgrade path is likely to come from lower-cost video platforms rather than premium monitor-heavy solutions. The projected 23% global rise in COPD between 2020 and 2050 extends this demand base for many years and gives the laryngoscope blades and handles market a rare level of long-range clinical visibility.

Shift Toward Single-Use Blades to Reduce Cross-Contamination Risk

The laryngoscope blades and handles market is moving toward single-use procurement because contamination concerns are no longer limited to the blade surface alone. Flexicare reported clinical data in 2025 showing that 86% of reusable laryngoscope handles remained bacterially positive after standard wipe disinfection, while APSF noted that single-use equipment removes the operational complexity tied to reprocessing steps. This matters because hospital buyers are now treating the handle as a contamination vector with equal importance, which changes a category that was once dominated by reusable hardware. The migration of disposability from blades into handles is changing the revenue mix, since the premium is shifting from a one-time capital item toward recurring procedure-linked consumption. Ambu’s June 2026 expansion of the Recircle program to include bioplastic SureSight blades shows that suppliers are now trying to solve infection control and sustainability together rather than forcing customers to choose one over the other[1]Ambu A/S, “Ambu Recircle Program Expands to Include Bioplastic SureSight Blades,” Press Release, via.ritzau.dk. That combined value proposition is likely to matter more in European public tenders, where environmental scoring is starting to influence award outcomes alongside traditional clinical and cost criteria.

Adoption of Video-Assisted and Fiber-Optic Systems in Difficult Airway Care

The laryngoscope blades and handles market is gaining support from a broader clinical shift toward video-assisted airway management in both routine and difficult cases. A 2025 systematic review and meta-analysis in the Journal of Clinical Medicine found that video laryngoscopy improved first-attempt intubation success and reduced esophageal misplacement in critically ill adults when compared with direct laryngoscopy, especially in difficult airway situations. This evidence moves video systems beyond a rescue role and gives procurement teams stronger justification for standardizing them across operating rooms, ICUs, and emergency care settings. A 2026 study in Frontiers in Medicine then reported a NASA-TLX cognitive workload score of 29.1 ± 6.7 for an AI-guided motorized video laryngoscope, which suggests that guided visualization can reduce operator burden and improve usability among less-experienced clinicians. That trend is important because AI-assisted or camera-optimized systems need blade geometries designed for optics and articulation, and those requirements lift the value of specialized blade SKUs relative to conventional ISO-compatible products. As a result, the laryngoscope blades and handles market is not only shifting toward video, it is also separating into a premium sub-segment where older reusable designs cannot compete on function.

Expansion of Emergency, Ambulatory, and Pre-Hospital Airway Workflows

The laryngoscope blades and handles market is also being shaped by the way airway care is spreading into ambulatory, emergency, and pre-hospital settings. Ambulatory surgical centers often operate without full central sterile processing support, which makes reusable handle systems harder to manage between cases and raises the appeal of integrated single-use formats. That same logic applies in emergency medical services, where equipment must be compact, battery-powered, quick to deploy, and stable in storage. Verathon’s July 2025 launch of GlideScope ClearFit, which pairs one reusable video baton with 6 single-use cover options across Macintosh, Miller, and Hyperangle styles, directly addressed the need for lower-cost flexibility across fast-moving care environments. Teleflex’s U.S. portfolio also reflects this demand pattern by offering single-use and reusable laryngoscope configurations tailored to anesthesia and airway management settings where reliability and readiness matter as much as the device itself. As more cases move outside large inpatient theaters, the laryngoscope blades and handles market is likely to reward suppliers that can support many care settings with a small number of easy-to-stock SKUs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Acquisition Cost of Advanced Video and Fiber-Optic Systems | -1.2% | South America, MEA, Southeast Asia most acute, with secondary drag in Southern and Eastern Europe | Long term (≥ 4 years) |

| Reprocessing Burden and Sterilization Compliance for Reusable Systems | -0.9% | Global, acute in high-volume APAC facilities with constrained autoclave capacity | Medium term (2-4 years) |

| Training Dependency and User Resistance to Advanced Intubation Platforms | -0.6% | APAC, MEA, South America with lower simulation training penetration | Medium term (2-4 years) |

| Environmental Pressure on Disposable Plastic and Mixed-Material Device Waste | -0.5% | European Union leading, North America and Australia with growing institutional pressure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition Cost of Advanced Video and Fiber-Optic Systems

The laryngoscope blades and handles market still faces a clear adoption limit in hospitals that cannot absorb the upfront cost of advanced video and fiber-optic systems. The gap between a basic reusable fiber-optic handle and a proprietary video-enabled setup remains large, and the recurring cost of single-use video blades at USD 15 to USD 80 per procedure adds pressure for facilities that work under strict consumables budgets. This cost barrier matters even when the clinical case for video is strong, because many procurement teams still evaluate airway devices through immediate payback rather than broad care quality metrics. Suppliers are responding with more modular formats that reduce per-case expense and lower entry barriers without removing the benefits of visualization. Verathon’s ClearFit design is one example of that response, because it spreads the video component across multiple single-use cover options and supports a more flexible cost profile for fast-turn care settings. Until similar price-performance models become common, the laryngoscope blades and handles market will continue to see slower conversion in South America, the Middle East and Africa, and non-urban Asia-Pacific accounts.

Reprocessing Burden and Sterilization Compliance for Reusable Systems

The laryngoscope blades and handles market also faces friction from the operational burden tied to reusable-system sterilization and documentation. FDA guidance for devices under product code EQN and 21 CFR 874.4760 requires validated reprocessing instructions that cover cleaning, disinfection, and sterilization, which raises the compliance workload for manufacturers and healthcare facilities alike[2]U.S. Food and Drug Administration, “Devices for Which a 510(k) Should Contain Validation Data,” FDA, fda.gov. APSF also highlighted that published studies found 75% to 86% of reprocessed laryngoscope handles remained positive for bacterial contamination after wipe disinfection, which keeps infection-control questions active even when hospitals follow routine steps. This burden falls hardest on mid-tier hospitals with high procedure volumes and limited autoclave turnaround capacity, because delays in reprocessing can directly affect case flow. The result is a difficult tradeoff where cost-sensitive hospitals still depend on reusable devices, yet those same hospitals face the heaviest process burden in keeping them compliant and readily available. That pressure is likely to keep pulling the laryngoscope blades and handles market toward simpler single-use or hybrid models that reduce audit exposure and workflow interruption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Video-Enabled Laryngoscope Handles Lead Growth in a Blades-Dominant Market

Laryngoscope blades held 65.31% of the laryngoscope blades and handles market share in 2025, which shows that volume is still centered on the consumable side of the category. This position reflects the global installed base of direct laryngoscopy workflows across operating rooms, emergency departments, and intensive care units. Macintosh and Miller designs continue to account for most routine purchasing because they are familiar, broadly compatible, and clinically embedded in everyday intubation practice. Specialized and video-compatible blades are growing faster inside the blades category, but they are still building from a smaller installed base than conventional direct-view products. In practical terms, the laryngoscope blades and handles market still depends on blade turnover for immediate revenue, even as technology upgrades start shifting more value into handles.

Laryngoscope handles are forecast to grow at a 9.38% CAGR through 2031, which makes them the fastest-growing product sub-segment in the laryngoscope blades and handles market. That growth is tied to the move away from passive battery-operated designs and toward active video-enabled configurations that support imaging, connectivity, and broader care-setting use. ISO 7376-2-2025 gave the category a more formal technical framework for video laryngoscopes in September 2025, which helps reduce specification uncertainty during procurement reviews. Ambu’s SureSight Mobile, introduced in December 2025, reflects the standalone path with an integrated screen-and-handle format meant for emergency and unplanned intubation, while SureSight Connect represents a more platform-led approach within the same product family. This points to a split future where monitor-linked systems remain strong in structured operating room environments, while self-contained handles gain share in emergency, transport, and space-constrained settings.

By Material: Stainless Steel Anchors Volume While Composites Reshape the Forward Portfolio

Stainless steel blades and handles commanded 55.24% of demand in 2025, which kept this material base at the center of the laryngoscope blades and handles market. Hospitals continue to rely on steel because it offers high torsional stiffness, dependable dimensional stability, repeated autoclave compatibility, and established fiber-optic coupling performance. Those qualities still matter most in high-throughput operating rooms and reuse-heavy ICU settings, where a stable clinical feel and durable construction remain important to clinicians. Plastic and polymer designs, by contrast, are more closely tied to single-use procurement where lower per-unit cost and easy disposal matter more than long service life. This split means steel remains the default in settings built around reuse, while polymers remain the practical option in facilities that prioritize turnover speed and simpler logistics.

Hybrid and composite material systems are projected to advance at an 8.52% CAGR through 2031, which makes them the fastest-moving material category in the laryngoscope blades and handles market. Their appeal comes from a combination of lower weight, better ergonomic possibilities, and the ability to support single-use formats without fully giving up structural performance. HEINE’s XP disposable blade series shows how suppliers are trying to narrow the performance gap by matching the geometry of reusable stainless-steel products in torsionally stiff polymer composite form. Ambu’s shift into second-generation bioplastic feedstock across SureSight handles and blades adds a separate sustainability angle, which matters as environmental filters gain weight in hospital tenders. China’s T/CITS 370-2025 group standard for video laryngoscopes also helps shape local performance expectations, which is important because material choices will increasingly be judged against both global and domestic compliance benchmarks[3]China National Institute of Standardization, “T/CITS 370-2025, Video Laryngoscopes,” National Digital Standards Library, cnis.ac.cn. Taken together, these changes suggest that composites are not replacing steel across the board, but they are becoming central to the forward product portfolio.

By Usage: Adult Configurations Anchor Volume as Pediatric Demand Scales Up

Adult-use laryngoscope blades and handles accounted for 62.52% of the by-usage market in 2025, which made adult configurations the largest usage segment in the laryngoscope blades and handles market. This result reflects the concentration of intubation volumes in general anesthesia, trauma care, and adult critical care. Standard Macintosh sizes 3 and 4 and Miller sizes 2 and 3 still define much of routine global purchasing, because they cover the broadest procedural need with the least complexity. Neonatal and difficult-airway products remain smaller in volume, but they require much more specialized design, which raises their strategic value for premium suppliers. Pediatric use is forecast to grow at an 8.25% CAGR through 2031, showing that smaller patient categories are becoming a stronger source of incremental demand.

The pediatric growth story is being reinforced by stronger published evidence and more focused product launches across the laryngoscope blades and handles market. A 2025 Frontiers in Pediatrics meta-analysis covering 1,059 neonates across 9 randomized controlled trials found that video laryngoscopy improved first-attempt success with a relative risk of 1.21 and reduced airway trauma with a relative risk of 0.23. That evidence matters because it gives neonatal and pediatric procurement committees a direct clinical basis for moving beyond traditional direct-view blades. Verathon expanded its pediatric care portfolio in February 2025, and Ambu also broadened SureSight Connect with pediatric blade options in 2025, which shows that leading suppliers see this segment as a real innovation priority rather than a niche add-on. As NICUs and pediatric centers look for better first-pass performance and easier training support, pediatric video-enabled blade systems are likely to take a larger role in future product development and hospital replacement planning.

By End User: Hospitals Lead Volume But Ambulatory Surgical Center Growth Reshapes Procurement

Hospitals held 60.62% of demand in 2025, which made them the largest end-user segment in the laryngoscope blades and handles market. That leadership came from ICU, operating room, and emergency department volumes, where blade-handle compatibility, light quality, and sterility carry the highest clinical weight. Hospitals also span the widest technology range, from basic reusable fiber-optic systems in resource-limited sites to fully integrated video laryngoscopy suites in tertiary centers. Emergency medical services form a separate procurement channel inside this broader picture because they require compact, battery-powered, and quickly deployable products rather than central-sterilization-dependent systems. Specialty clinics remain the smallest group, but they are gradually increasing adoption of video-compatible products for ENT and pulmonology airway procedures as per-use economics improve.

Ambulatory surgical centers are forecast to grow at a 9.25% CAGR through 2031, which makes them the fastest-growing end-user group in the laryngoscope blades and handles market. Their procurement logic is different from hospitals because they work with lean inventory, limited sterile processing support, and stronger preference for predictable per-case cost. That operating model naturally supports integrated blade-handle combinations and simpler disposable formats that reduce between-case handling steps. Teleflex’s Rüsch TruLite Secure single-use combination, with pre-fitted batteries, LED illumination, and a 3-year shelf life, is closely aligned with this use pattern. Because ambulatory centers measure efficiency closely and have less legacy dependence on reusable systems, they are likely to become the clearest testing ground for price-performance choices across the category. In that sense, the end-user mix is changing not only where products are sold, but also which product designs gain commercial traction first.

Geography Analysis

North America accounted for 39.22% share of the laryngoscope blades and handles market size in 2025, which kept it as the largest regional contributor. The region benefits from high surgical volumes, mature critical care infrastructure, and consistent replacement demand across hospital and emergency care settings. Baxter’s decision to discontinue all Welch Allyn laryngoscope blade and handle lines, effective March 31, 2026, created a near-term opening in institutional accounts that other suppliers are now contesting. Europe remained the second-largest region, with Germany, France, the UK, and Italy acting as the main volume centers for the laryngoscope blades and handles market. Ambu received CE Mark for its full SureSight portfolio in April 2026, which supports a phased rollout across Europe and increases pressure on legacy reusable-device positions. European public tenders are also giving more weight to environmental compliance, which favors suppliers that can document recyclable materials or take-back pathways. Germany remains especially active in single-use laryngoscope procurement, which reflects the region’s willingness to pair infection control with operational convenience in acute care pathways.

Asia-Pacific is forecast to expand at a 9.15% CAGR through 2031, which makes it the fastest-growing regional block in the laryngoscope blades and handles market. China is pushing growth through hospital modernization, and procurement activity across provincial hospitals shows that compatible single-use blades are increasingly being bought against an existing base of video handles. That pattern matters because it signals a move from initial installation into repeat blade demand, which is more supportive of recurring revenue. India still presents a longer registration path for new entrants in higher-risk devices, but major public hospital networks and medical college systems keep the market commercially attractive because of their procedure volume. Japan adds a different growth profile, since its aging population sustains high per-capita intubation need and supports replacement demand for better-visualization systems rather than only first-time purchases.

The Middle East and Africa and South America together account for the remaining regional demand, but growth varies widely by infrastructure quality and procurement capacity. GCC countries are expanding hospital capacity and continue to favor premium international brands, especially in private care networks where video-assisted systems carry strong clinical and brand value. South Africa’s private hospital groups and Brazil’s tertiary care centers remain the highest-value anchors in their respective sub-regions, while many other accounts still rely on reusable fiber-optic handles paired with disposable or lower-cost blades. EMS expansion across these regions is also supporting demand for rugged, portable, and shelf-stable handle configurations that can be deployed quickly outside a full hospital environment.

Competitive Landscape

The laryngoscope blades and handles market is moderately concentrated in the premium video-integrated segment, where a small group of global suppliers has built recognizable platform ecosystems around screens, handles, and recurring blade sales. Ambu, KARL STORZ, Verathon, Medtronic, and Teleflex are the most visible companies in that higher-value portion of the market, while the conventional blade-and-handle segment remains much more fragmented across interoperable products. European specialists such as HEINE Optotechnik, Rudolf Riester, HENKE-SASS WOLF, Penlon, and Flexicare continue to compete on manufacturing quality, ergonomic design, and specific blade formats. Chinese domestic manufacturers add price pressure in standard configurations, especially where buyers are more focused on affordability than on premium platform features. Baxter’s withdrawal from the category in 2026 removed a known mid-tier competitor and pushed replacement decisions toward suppliers with more active product pipelines and clearer long-term support plans.

Competition in the laryngoscope blades and handles market is increasingly shaped by infection control, sustainability, and platform retention rather than by blade geometry alone. Ambu’s Recircle program now covers 50 hospital sites and more than 140 clinical departments in 4 countries, which gives the company both an environmental credential and a practical way to deepen account ties through its own take-back process. Flexicare and Teleflex remain relevant where hospitals want simpler disposable options without committing fully to a premium video platform, which keeps the middle of the market active even as top-end systems become more specialized. The next area of competition is likely to center on cost-accessible video systems for non-urban Asia-Pacific, South America, and parts of the Middle East and Africa, because those regions need performance gains without large capital commitments. That leaves room for suppliers that can combine acceptable imaging quality, lower recurring blade cost, and easier field deployment in one offering.

Several strategic moves already show how suppliers are positioning for that shift in the laryngoscope blades and handles market. Ambu expanded geographically in April 2026 with CE Mark approval for the full SureSight video laryngoscope portfolio in Europe, which strengthens its regional reach across both planned and unplanned airway care settings. Verathon launched GlideScope ClearFit in July 2025 to offer one reusable video baton with multiple single-use cover options, which directly targets the pressure for lower-cost flexibility in ambulatory and emergency care. Teleflex’s shelf-stable TruLite Secure format and Ambu’s pediatric SureSight expansion show a similar focus on workflow-specific product design, where the winning approach is less about a single flagship device and more about fitting the operational need of each account.

Laryngoscope Blades and Handles Industry Leaders

Teleflex Incorporated

Medtronic plc

Olympus Corporation

Ambu A/S

KARL STORZ SE and Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Ambu received the CE Mark for its SureSight video laryngoscope portfolio in Europe, enabling a phased rollout across EU markets. The portfolio, including SureSight Connect and SureSight Mobile, launched in the US and UK in 2025. This clearance removes a key barrier to scaling Ambu's video laryngoscopy business.

- April 2026: KARL STORZ gained FDA 510(k) clearance (K252624) for its laryngoscope and accessories under 21 CFR 874.4760. This strengthens its US regulatory position for the C-MAC laryngoscope platform and related blade accessories in ENT and anesthesia devices.

Global Laryngoscope Blades and Handles Market Report Scope

As per the scope of the report, laryngoscope blades are instruments inserted into the mouth to lift tissues and visualize the larynx. Handles provide the grip and house the light source for illumination during intubation.

The segmentation of the laryngoscope blades and handles market is categorized by product type, material, usage, end user, and geography. By product type, the market includes blades such as Macintosh blades, Miller blades, straight blades, and specialized and video-compatible blades. It also covers handles, including standard handles, reusable handles, disposable handles, and video-enabled handles. By material, the market is segmented into stainless steel blades and handles, plastic and polymer-based blades and handles, and hybrid and composite material systems. By usage, the market is divided into adult use, pediatric use, and neonatal and difficult airway use. By end user, the market comprises hospitals, ambulatory surgical centers, emergency medical services, and specialty clinics. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Blades | Macintosh Blades |

| Miller Blades | |

| Straight Blades | |

| Specialized and Video-Compatible Blades | |

| Handles | Standard Handles |

| Reusable Handles | |

| Disposable Handles | |

| Video-Enabled Handles |

| Stainless Steel Blades and Handles |

| Plastic and Polymer-Based Blades and Handles |

| Hybrid and Composite Material Systems |

| Adult Use |

| Pediatric Use |

| Neonatal and Difficult Airway Use |

| Hospitals |

| Ambulatory Surgical Centers |

| Emergency Medical Services |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Blades | Macintosh Blades |

| Miller Blades | ||

| Straight Blades | ||

| Specialized and Video-Compatible Blades | ||

| Handles | Standard Handles | |

| Reusable Handles | ||

| Disposable Handles | ||

| Video-Enabled Handles | ||

| By Material | Stainless Steel Blades and Handles | |

| Plastic and Polymer-Based Blades and Handles | ||

| Hybrid and Composite Material Systems | ||

| By Usage | Adult Use | |

| Pediatric Use | ||

| Neonatal and Difficult Airway Use | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Emergency Medical Services | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current outlook for laryngoscope blades and handles market?

The laryngoscope blades and handles market stands at USD 544.26 million in 2026 and is projected to reach USD 782.08 million by 2031 at a 7.52% CAGR.

Why are single-use devices gaining traction in airway management?

Hospitals are responding to contamination concerns around reusable handles and blades, while ambulatory sites also value the simpler workflow and predictable per-case cost.

Which product category leads demand today?

Laryngoscope blades led product demand with a 65.31% share in 2025, reflecting the large installed base of direct laryngoscopy across operating rooms, ICUs, and emergency departments.

Which end-user group is expanding the fastest?

Ambulatory surgical centers are projected to grow at a 9.25% CAGR through 2031 because they favor ready-to-use, inventory-light, and sterilization-light device formats.

Why is Asia-Pacific growing faster than other regions?

Asia-Pacific is forecast to expand at a 9.15% CAGR through 2031, supported by hospital modernization in China, large public hospital demand in India, and replacement demand in Japan.

What is changing competition among leading suppliers?

Competition is shifting toward video platforms, sustainable disposable programs, pediatric expansion, and lower-cost modular designs that fit emergency and ambulatory care use.

Page last updated on: