Video Laryngoscope Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 302.72 Million |

| Market Size (2031) | USD 612.06 Million |

| Growth Rate (2026 - 2031) | 15.12% CAGR |

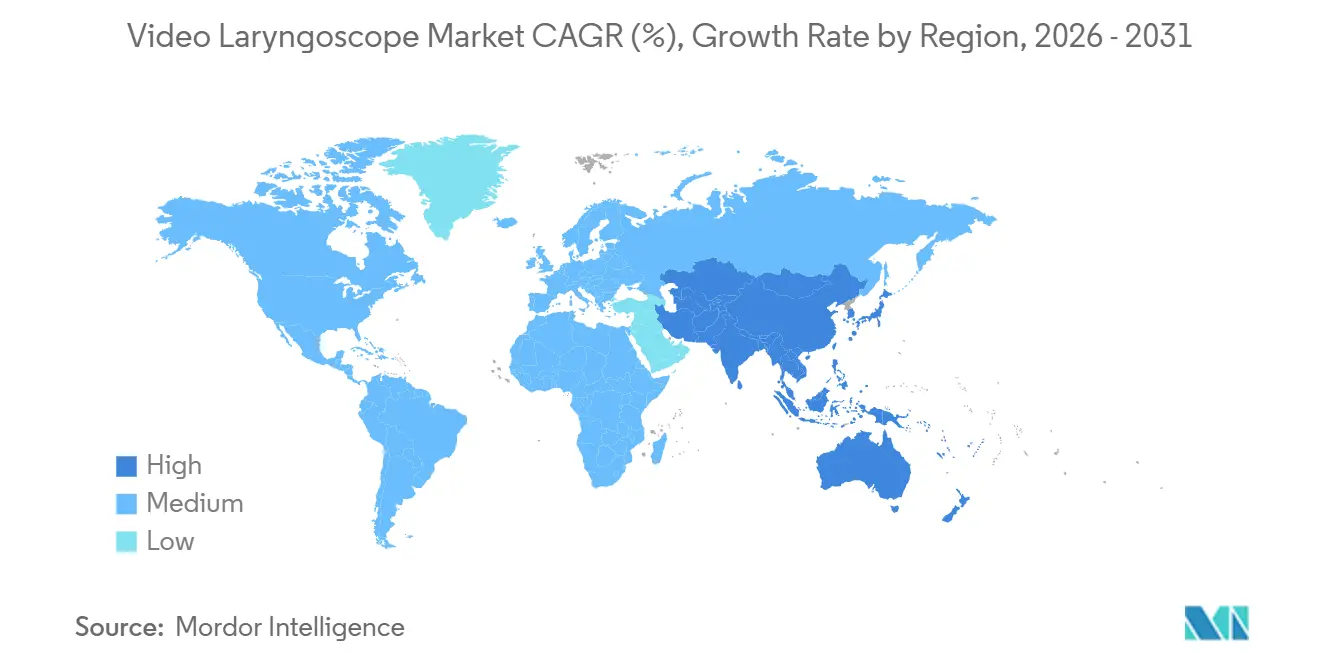

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Laryngoscope Market Analysis by Mordor Intelligence

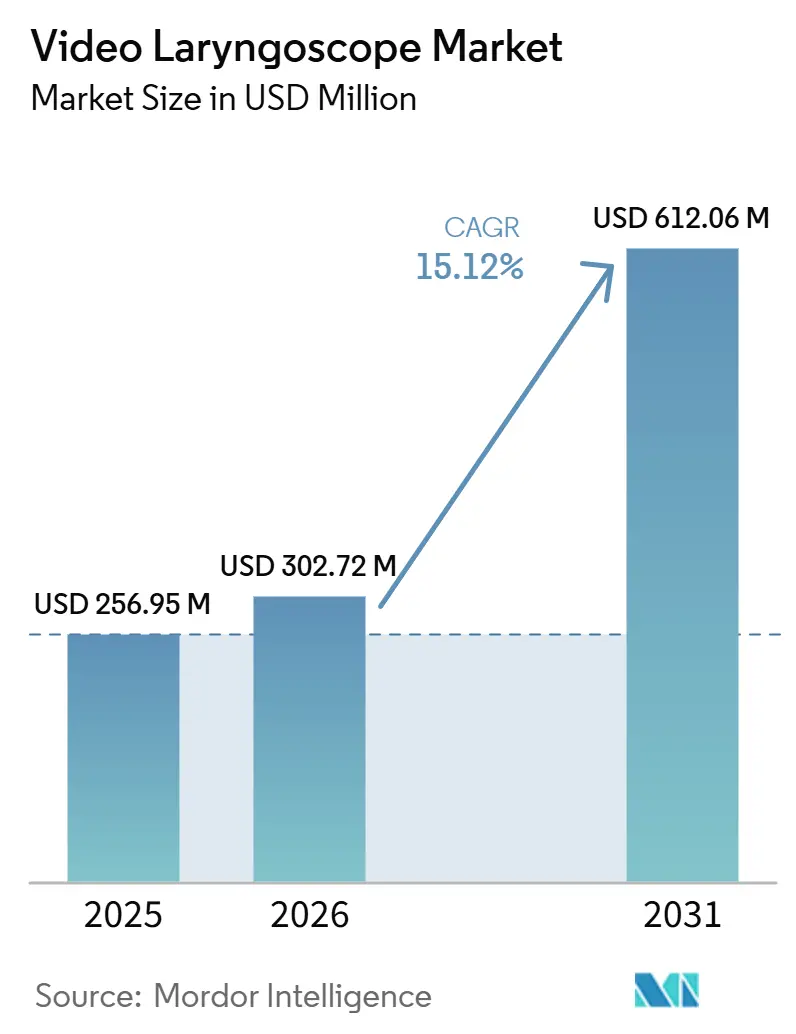

The Video Laryngoscope Market size was valued at USD 256.95 million in 2025 and is estimated to grow from USD 302.72 million in 2026 to reach USD 612.06 million by 2031, at a CAGR of 15.12% during the forecast period (2026-2031).

Clinical demand is expanding across emergency departments, operating rooms, and pre-hospital settings as providers pursue universal video laryngoscopy protocols that improve first-pass success and minimize airway trauma. Rigid platforms still dominate routine intubations, yet flexible, bronchoscope-style systems are winning share in intensive-care and awake fiberoptic procedures because they navigate restricted or tortuous anatomy more easily. Disposable blades are gaining momentum as hospitals weigh infection-prevention savings against the labor and capital costs of reprocessing for high-level disinfection cabinets. Geographic opportunities remain uneven: North America upgrades existing fleets to wireless high-definition models, Asia-Pacific installs first-generation units in thousands of new operating rooms, and Europe prioritizes bio-based disposables that comply with single-use-plastics legislation.

Key Report Takeaways

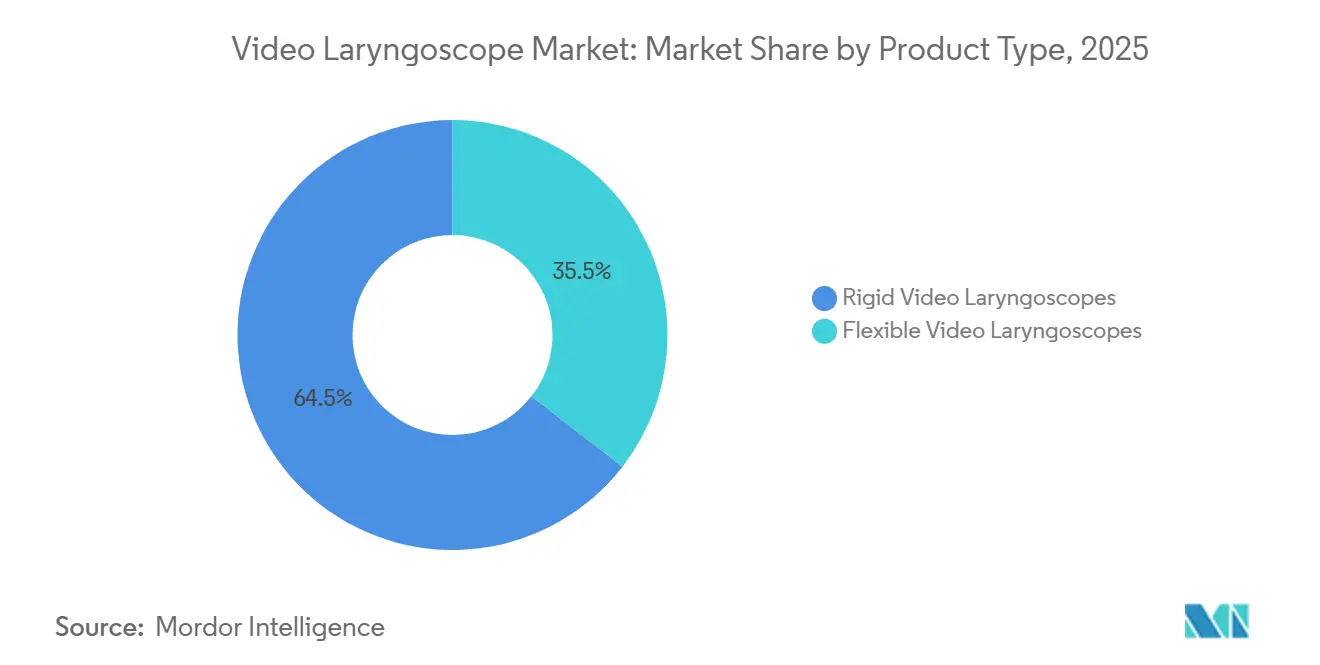

- By product type, rigid video laryngoscopes accounted for 64.55% of revenue in 2025, while flexible devices are on track for a 16.25% CAGR through 2031.

- By usability, reusable platforms accounted for 70.53% of 2025 sales, whereas disposables are advancing at a 16.85% CAGR through the end of the forecast period.

- By blade geometry, standard curved blades held 55.63% of the volume in 2025, and hyper-angulated designs are forecast to grow at a 17.87% CAGR through 2031.

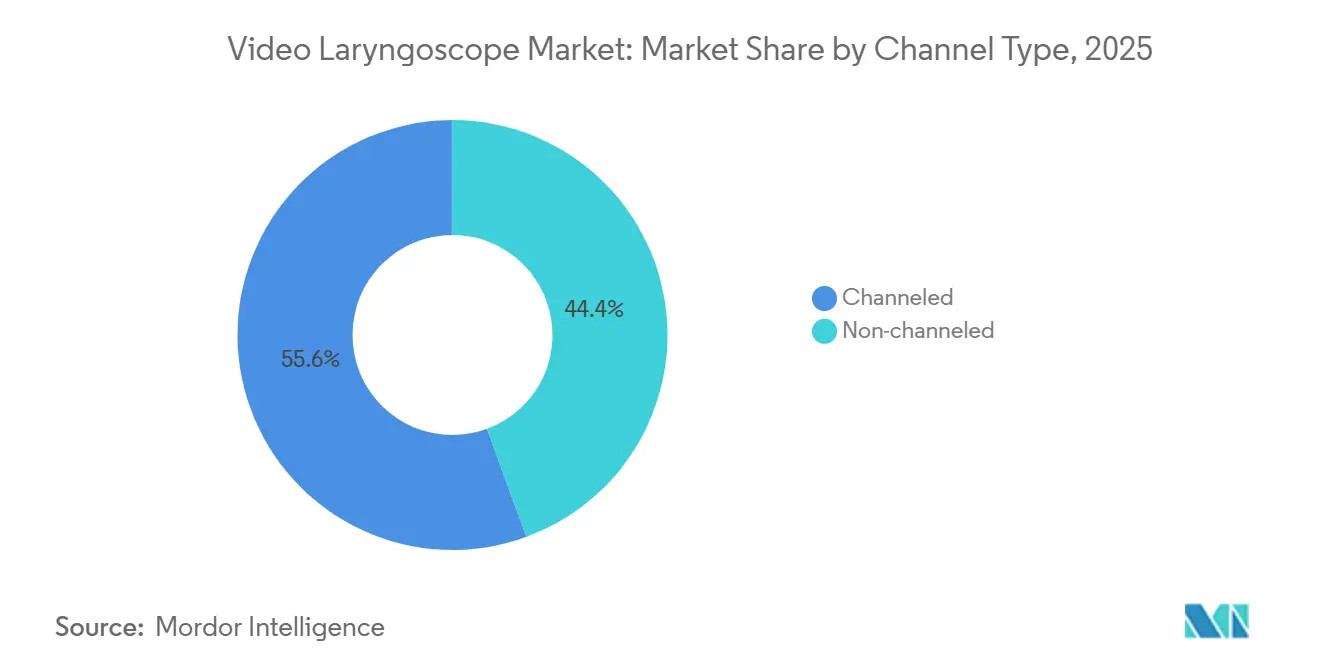

- By channel type, channeled systems captured 55.63% of 2025 demand, yet non-channeled variants are expanding at a 16.27% CAGR through 2031.

- By end user, hospitals retained 66.53% revenue share in 2025, while ambulatory surgical centers are poised for 17.7% CAGR growth to 2031.

- By geography, Asia-Pacific is set to grow at a 16.51% CAGR, outpacing North America’s mature base of 38.13% share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Video Laryngoscope Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Difficult airway prevalence & surgical volume growth | +3.20% | Global, strongest in aging North America & Europe | Medium term (2-4 years) |

| Infection-control push toward disposables | +2.80% | North America & Europe lead, APAC catching up | Short term (≤ 2 years) |

| HD imaging, portability & wireless upgrades | +2.50% | Global, premium uptake in North America, Europe, urban APAC | Medium term (2-4 years) |

| AI-assisted intubation analytics | +1.90% | Early adopters in North America & Europe, pilots in APAC | Long term (≥ 4 years) |

| Tele-intubation for rural EMS | +1.20% | Rural North America, Australia, emerging APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Difficult Airway Cases and Surgical Volumes

Obesity and cervical-spine injury trends are elevating difficult-airway frequency, making indirect visualization indispensable for anesthesia providers. Meta-analyses published in 2024 showed that video laryngoscopes cut failed intubations by 42% compared with direct blades, a margin pivotal for emergency departments seeking to avoid surgical airways[1]Yi-Chen Wang et al., “Video Laryngoscopy Reduces Failed Intubations in Emergency Departments,” PubMed, pubmed.ncbi.nlm.nih.gov. Post-pandemic rebounds in elective surgery have further expanded the candidate pool for video-guided intubation. Institutional adoption of “universal video laryngoscopy” protocols accelerates unit utilization, especially in teaching hospitals where resident training emphasizes first-pass success. ISO 7376-2:2025 now codifies optical baselines, anchoring clinician confidence that any compliant device will perform adequately under difficult-airway conditions[2]International Organization for Standardization, “ISO 7376-2:2025,” iso.org .

Post-COVID Infection-Control Push Toward Disposable Devices

The pandemic spotlighted the hidden costs of reusable blade reprocessing, which can exceed 15 minutes of staff time and consumables per cycle[3]U.S. Food and Drug Administration, “Medical Device Reprocessing Guidance 2024,” fda.gov. Single-use blades eliminate those expenses and remove residual biofilm risk, trading USD 30–50 per procedure for guaranteed sterility. Revised 2024 FDA guidance also tightened reprocessing validation requirements, implicitly discouraging off-label reuse. European hospitals face sustainability mandates, so vendors are fielding bio-based polymers that meet both infection-control and environmental goals[4]European Commission, “Single-Use Plastics Directive Overview,” ec.europa.eu . These converging forces underpin the 16.85% CAGR projected for disposables.

Technological Advances: HD Imaging, Portability, and Wireless Connectivity

ISO-mandated 720p resolution, combined with dynamic light control, delivers crisper glottic views that shorten intubation time, as seen in 2024 clinical trials that demonstrated an 18% speed gain. Battery runtimes now exceed 90 minutes, enabling field and transport applications without auxiliary power. Secure Wi-Fi or Bluetooth links push real-time video into electronic health records, facilitating tele-supervision and closed-loop documentation. Hospitals replace first-generation cabled units with wireless platforms that simplify sterile-field management and enhance workflow flexibility

AI-Assisted Intubation Analytics Boosting First-Pass Success

FDA cleared the first AI software module for video laryngoscopes in 2024, validating real-time anatomical landmark detection under its Software-as-a-Medical-Device pathway. Pilot studies reported 31% fewer esophageal placements among novices using AI prompts, a benefit valued highly in emergency settings. Algorithms also pre-flag airway predictors such as limited mouth opening, guiding clinicians toward alternative strategies before initial blade insertion. A broader rollout depends on cybersecurity safeguards and seamless integration with disparate electronic record systems, challenges most acute in community hospitals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost & Limited Reimbursement | -1.8% | Global, especially APAC & South America | Short term (≤ 2 years) |

| Workforce Shortages in LMICs | -1.5% | Sub-Saharan Africa, South Asia, rural Latin America | Medium term (2-4 years) |

| Environmental Pushback On Single-Use Plastics | -0.9% | Europe leads, North America & APAC building pressure | Medium term (2-4 years) |

| Cybersecurity & Data-Privacy Vulnerabilities | -0.7% | North America & Europe, awareness rising in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Limited Reimbursement Pathways

Hospitals weigh USD 15,000–25,000 outlays for reusable systems against tight operating margins, while CPT code 31500 does not differentiate direct from video intubation, leaving facilities to absorb consumable expenses. Lease programs and value-based contracts tied to complication reduction are emerging but require robust actuarial data seldom available outside academic centers. Cost sensitivity is most acute in Latin America and parts of Asia, where equipment imports face tariffs that inflate list prices.

Shortage of Trained Airway Specialists in LMICs

Sub-Saharan Africa averages only 1 anesthesiologist per 100,000 inhabitants versus 20 in high-income economies, limiting safe device adoption. Video laryngoscopes require hand-eye coordination different from that of direct blades, and simulation labs capable of teaching that nuance are scarce outside capital cities. Regulations often bar nurse anesthetists from advanced airway tasks, further constraining diffusion. Scalable e-learning and task-shifting policies will be required to unlock latent demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flexible Variants Gain Bronchoscopy Crossover

Flexible systems accounted for a modest share of the video laryngoscope market at USD 55 million in 2026, but are forecast to grow at a 16.25% CAGR due to their superior maneuverability in cervical-spine-immobilized or limited-mouth-opening cases. Rigid platforms still held 64.55% 2025 revenue share, favored for routine surgical cases and lower acquisition cost.

Clinical trials in 2025 showed that flexible devices shaved 23 seconds off intubation time in trauma patients, reducing the risk of hypoxemia. Intensive-care units now deploy them for bedside awake intubations, while anesthesiology fellowships incorporate flexible-scope modules into curricula. Higher price tags and maintenance complexity mean rigid models will continue to dominate the video laryngoscope market through the forecast horizon.

By Usability: Disposable Economics Reshape Infection Control

Reusable systems generated 70.53% of 2025 revenue. Yet disposables are set to overtake in specific settings, as total-cost-of-ownership analyses favor single-use blades, particularly when reprocessing labor costs exceed USD 10 per cycle. Hospitals balancing infection-control compliance with sustainability budgets adopt hybrid fleets, using disposables for high-risk infectious cases and reusables elsewhere.

The disposable surge is anchored in ambulatory surgical centers, emergency rooms, and low-resource clinics lacking disinfection infrastructure. If blade prices drop to USD 20, disposables could match reusable per-procedure cost after 50–75 uses, accelerating penetration and lifting the wider video laryngoscope market.

By Blade Geometry: Hyper-Angulated Designs Conquer Anterior Airways

Standard curved blades retained 55.63% 2025 volume, but hyper-angulated devices are outpacing at 17.87% CAGR by solving anterior airway visualization challenges. ISO 7376-2:2025’s curvature nomenclature now lets clinicians compare 60- to 90-degree designs across brands. Pediatric and straight blades serve neonates and patients with narrow interdental gaps, yet represent a small contribution to video laryngoscope market share. Hyper-angulated adoption requires training to avoid levering forces but pays off with better Cormack-Lehane grades and fewer rescue maneuvers, particularly in bariatric populations.

By Channel Type: Non-Channeled Simplicity Wins Cost-Sensitive Markets

Channeled systems held 55.63% 2025 share because integrated suction stabilizes visualization during bloody or vomitus-laden intubations. However, non-channeled designs grow at a 16.27% CAGR, prized for their slimmer profiles and USD 8–12 lower blade costs. Elective surgical suites with fasted patients see negligible benefit from suction channels, fueling non-channeled uptake. Hybrid models that accept clip-on disposable suction modules aim to balance cost and functionality, highlighting how nuanced clinical settings mold the evolution of the video laryngoscope market.

By End User: ASCs Leverage Payment Reforms and Efficiency Mandates

Hospitals accounted for 66.53% of revenue in 2025, but ambulatory surgical centers are the fastest-growing buyers, with a 17.7% CAGR, as CMS adds more procedures to outpatient reimbursement lists. ASCs prize first-pass success because every minute of turnover time erodes slim profit margins.

Portable units certified under IEC 60601-1-12 for pre-hospital ruggedness also attract EMS agencies outfitting advanced life-support ambulances. Training gaps remain; only 38% of United States paramedics reported formal coursework in 2024, limiting field adoption despite favorable device pricing. Nonetheless, the momentum of payment reform keeps this segment pivotal to the future trajectory of the video laryngoscope market.

Geography Analysis

North America generated 38.13% of 2025 revenue, buoyed by FDA 510(k) clearances that compress launch timelines and hospital budgets averaging USD 12–18 million annually for anesthesia technology. U.S. facilities are now replacing first-generation scopes with secure wireless models that integrate seamlessly with electronic records. At the same time, Canada and Mexico face slower uptake due to reimbursement caps and tariffs. Replacement sales constitute 40–50% of 2025–2026 demand, stabilizing the mature regional video laryngoscope market.

Asia-Pacific is forecast to grow at 16.51% CAGR, supported by India’s Ayushman Bharat scheme, which lifted surgical volumes 18% in 2024-2025. China reports 97.18% penetration in tertiary centers yet <30% in county facilities, offering a substantial first-install market. Japan and South Korea are near saturation, focusing on AI-enhanced replacements rather than new installations. Tele-intubation pilots in Australia’s Outback demonstrate how connectivity investments unlock new use cases for the video laryngoscope market.

Europe, the Middle East & Africa, and South America supply the remaining share. The EU’s single-use plastics directive drives bio-based blade launches despite 15–20% higher costs. Gulf states equip new megahospitals with premium systems under Vision 2030 programs, whereas South American public hospitals wrestle with currency volatility and import duties. Regional distribution hubs and vendor financing could help relieve procurement bottlenecks and lift the global video laryngoscope market size further.

Competitive Landscape

Market concentration is moderate, with Medtronic, Karl Storz, and Verathon controlling a sizeable installed base through ISO-compliant optics, broad service networks, and captive consumables. Ambu’s single-use strategy delivered 22% revenue growth in 2025, underscoring rising demand for disposables. Smaller firms exploit price gaps, offering sub-USD 5,000 portable units for rural EMS, though quality perception limits traction in premium segments.

Technological differentiation now pivots on AI analytics, wireless encryption, and dynamic light management rather than core optics. ISO 7376-2:2025 raises entry barriers by specifying illumination uniformity and optical resolution, driving up tooling costs for newcomers. Patent filings in 2024-2025 cluster around hyper-angulated geometries and bio-based polymers, signaling incremental rather than disruptive innovation paths within the video laryngoscope industry.

Chinese entrants such as Tuoren and Hebei Vimed offer 30–40% discounted systems, appealing in cost-sensitive Asia-Pacific and South America but facing regulatory and brand hurdles in North America and Europe. Early-mover advantage will likely accrue to suppliers that integrate AI, cybersecurity, and sustainable materials into unified platforms, defining the next growth wave of the video laryngoscope market.

Video Laryngoscope Industry Leaders

Ambu A/S

Karl Storz SE & Co. KG

Medtronic plc

Olympus Corporation

Verathon Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Ambu A/S unveiled SureSight Mobile, a handheld video laryngoscope with an integrated screen for rapid emergency intubations.

- July 2025: Verathon Inc. launched GlideScope ClearFit, a cover-based device that pairs reusable electronics with low-cost disposable optics to balance cost and sustainability.

Global Video Laryngoscope Market Report Scope

As per the report's scope, a video laryngoscope is a laryngoscopy device equipped with a miniature camera that displays the airway on a screen, allowing clinicians to visualize the glottis without aligning the oral–pharyngeal–laryngeal axes. It improves first‑attempt intubation success, especially in difficult‑airway scenarios, by providing an enhanced, magnified view of the vocal cords. The device typically includes a video blade, light source, and monitor, enabling both real‑time guidance and team visualization. It is now widely used in operating rooms, ICUs, and emergency settings for safer, more controlled airway management.

Video laryngoscope market segmentation includes product type, usability, blade geometry, channel type, end user, and Geography. By product type, the market is segmented into rigid video laryngoscopes and flexible video laryngoscopes. By usability, the market is segmented into reusable devices and disposable devices. By blade geometry, the market is segmented into standard curved, hyper-angulated, and straight/pediatric. By channel type, the market is segmented into channeled and non-channeled. By end user, the market is segmented into hospitals, pre-hospital/EMS, ambulatory surgical centers, and others. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Rigid Video Laryngoscopes |

| Flexible Video Laryngoscopes |

| Reusable Devices |

| Disposable Devices |

| Standard Curved |

| Hyper-angulated |

| Straight / Pediatric |

| Channeled |

| Non-channeled |

| Hospitals |

| Pre-hospital / EMS |

| Ambulatory Surgical Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Rigid Video Laryngoscopes | |

| Flexible Video Laryngoscopes | ||

| By Usability | Reusable Devices | |

| Disposable Devices | ||

| By Blade Geometry | Standard Curved | |

| Hyper-angulated | ||

| Straight / Pediatric | ||

| By Channel Type | Channeled | |

| Non-channeled | ||

| By End User | Hospitals | |

| Pre-hospital / EMS | ||

| Ambulatory Surgical Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the video laryngoscope market in 2026?

The video laryngoscope market size reached USD 302.72 million in 2026 and is projected to double by 2031.

Which segment is expanding the fastest?

Disposable systems are growing at a 16.85% CAGR as hospitals prioritize infection-control efficiency.

Why are hyper-angulated blades gaining popularity?

Their 60–90-degree curvature exposes the glottis in anatomically challenging airways, driving a 17.87% CAGR.

What is the key growth driver in Asia-Pacific?

Large-scale government insurance plans such as India’s Ayushman Bharat are increasing surgical volumes and equipment spending.

Are reimbursement gaps limiting adoption in the United States?

Yes, current CPT codes do not provide separate payment for video laryngoscopy, so hospitals shoulder consumable costs.

How are vendors addressing environmental concerns?

Manufacturers are launching bio-based polymer blades and modular designs that separate reusable electronics from disposable optics to reduce plastic waste.

Page last updated on: