Laryngeal Airway Mask Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 550.15 Million |

| Market Size (2031) | USD 725.70 Million |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

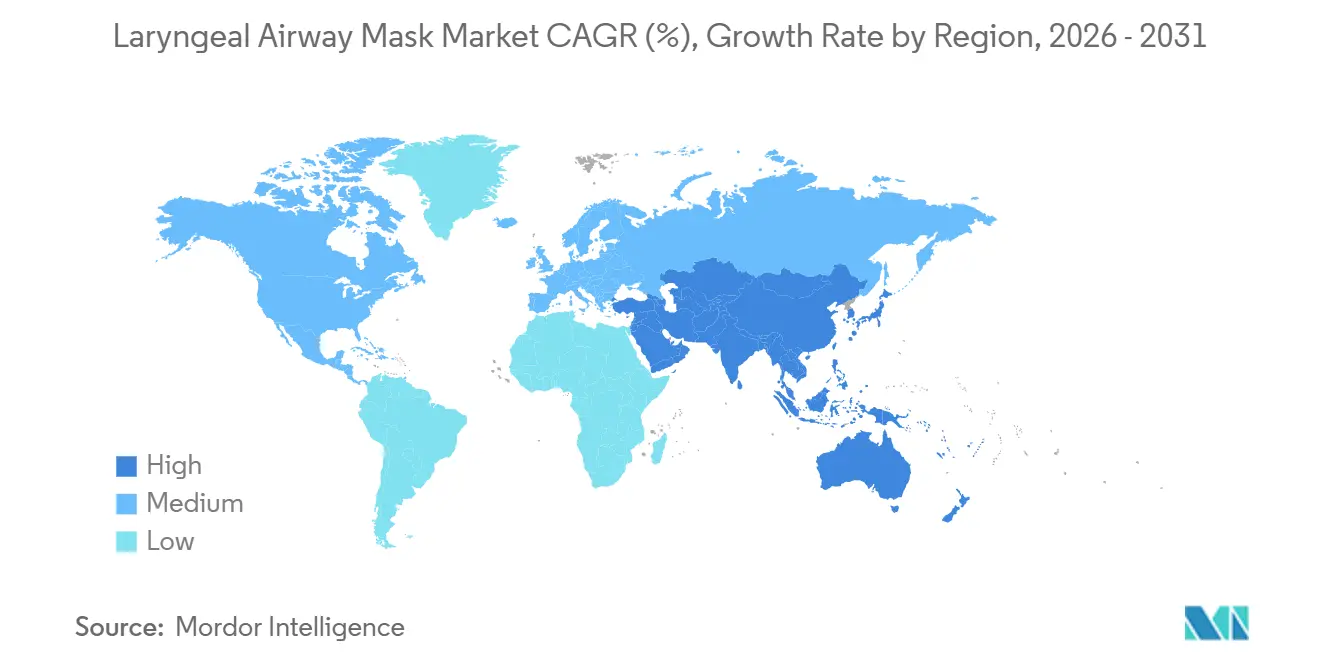

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

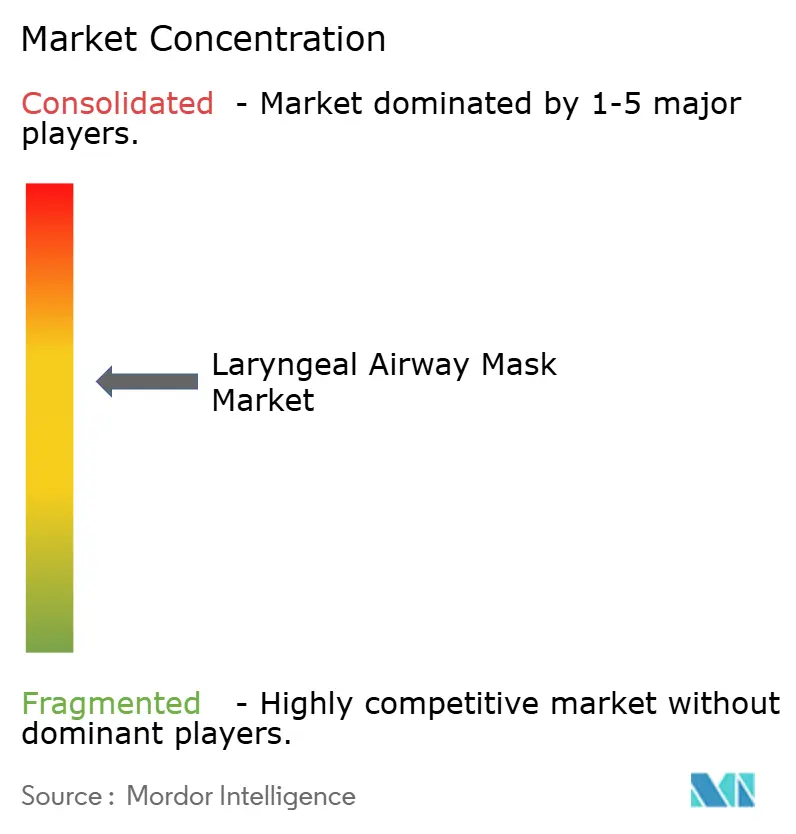

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laryngeal Airway Mask Market Analysis by Mordor Intelligence

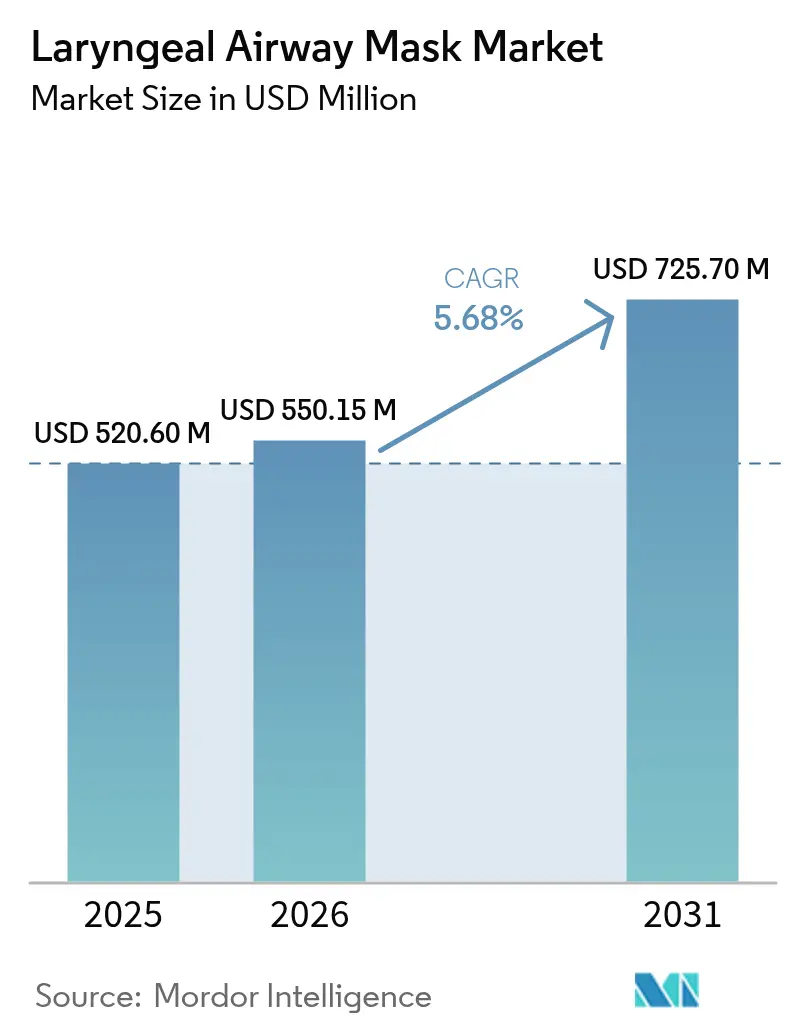

The Laryngeal Airway Mask Market size is projected to be USD 520.60 million in 2025, USD 550.15 million in 2026, and reach USD 725.70 million by 2031, growing at a CAGR of 5.68% from 2026 to 2031.

Demand is expanding beyond operating rooms into military and civilian emergency systems, where supraglottic devices shorten airway-securement time and lower skill thresholds. Disposable masks retain dominance because they remove reprocessing risks, align with hospital infection-control policies, and simplify per-case cost accounting. Specialty second-generation devices are the fastest-growing category, propelled by gastric-drainage channels, video guidance, and pressure-monitoring cuffs that mitigate aspiration and malposition concerns. Parallel momentum comes from pediatric guideline updates, rising ASC procedure volumes, and aging demographics that raise anesthesia caseloads, all of which underpin steady growth in the laryngeal airway mask market.

Key Report Takeaways

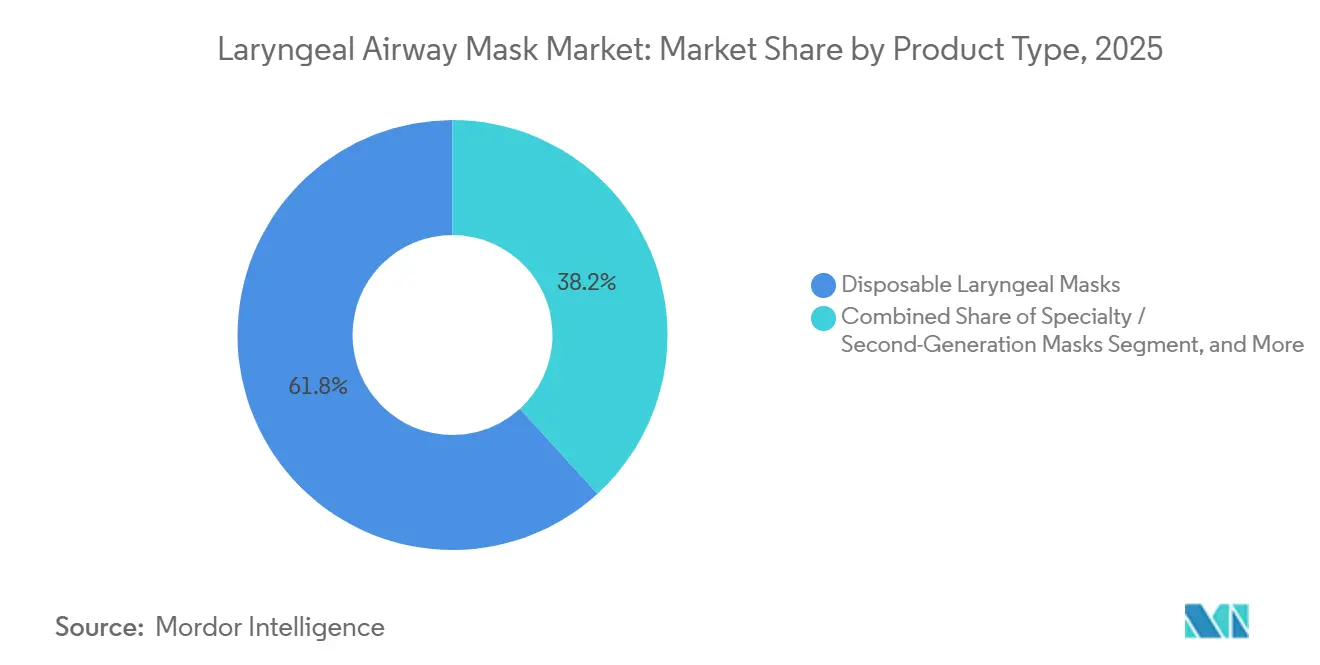

- By product type, disposable devices accounted for 61.78% of the laryngeal airway mask market share in 2025; specialty and second-generation masks are forecast to grow at a 7.78% CAGR through 2031.

- By age group, adult users accounted for 59.85% of demand in 2025, while pediatric and neonatal applications are set to expand at an 8.12% CAGR to 2031.

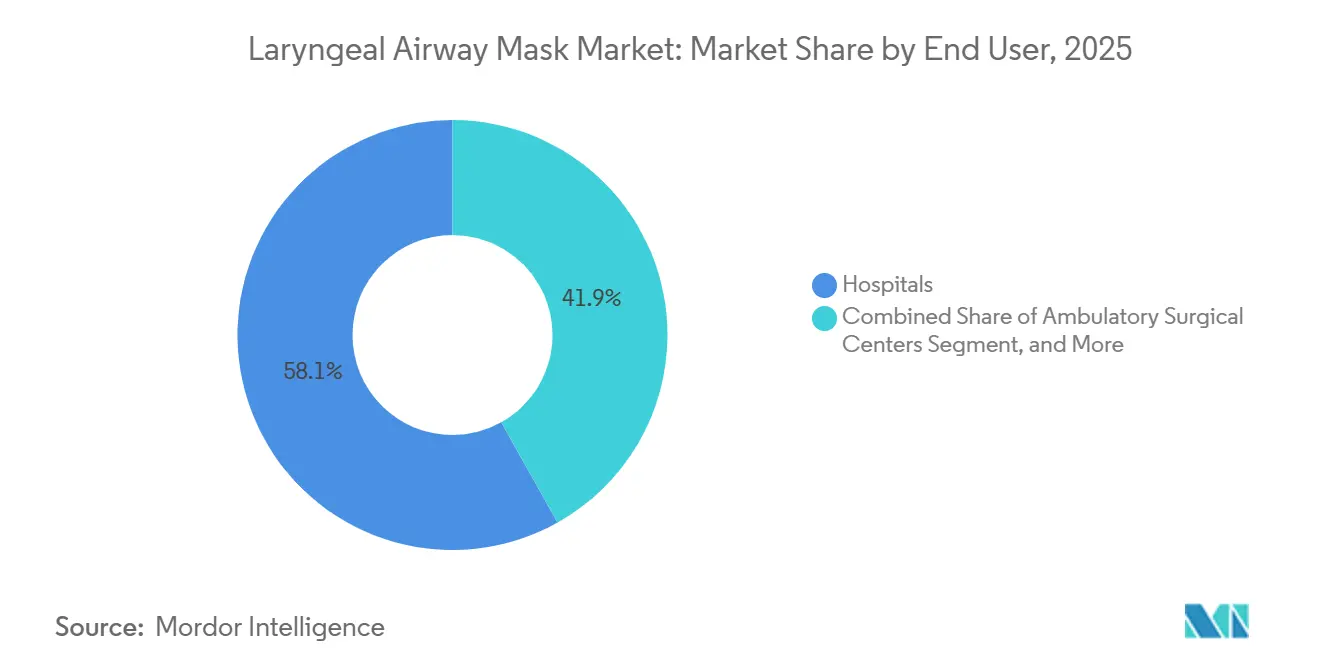

- By end user, hospitals captured 58.12% revenue in 2025; ambulatory surgical centers are projected to grow at an 8.44% CAGR as same-day surgery volumes climb and office-based anesthesia protocols spread.

- By geography, North America led with 36.80% revenue in 2025, yet Asia-Pacific is forecast to grow at an 8.82% CAGR, driven by rising surgical volumes and infrastructure investment.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laryngeal Airway Mask Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising surgical volume linked to chronic diseases | +1.2% | Global with concentration in North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Growing demand for disposable masks in ICUs & ORs | +1.0% | North America, Europe | Short term (≤ 2 years) |

| Ageing population fuelling anesthesia procedures | +0.9% | North America, Europe, Japan, Australia, urban China, India | Long term (≥ 4 years) |

| Rapid design improvements in 2nd-generation devices | +0.8% | Early adoption in North America, Europe; gradual in Asia-Pacific | Medium term (2-4 years) |

| ASC shift to office-based anesthesia | +0.7% | Predominantly North America | Medium term (2-4 years) |

| Military & EMS doctrine favouring supraglottic use | +0.6% | North America, Europe, select Middle East and Asia-Pacific EMS systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Volume Linked to Chronic Diseases

Global surgical need is climbing, yet only 45 nations meet the benchmark of 5,000 procedures per 100,000 population, leaving low-income regions underserved. High-income markets demand advanced masks with integrated monitoring and gastric access, whereas resource-constrained settings focus on cost-effective, durable options suitable for non-physician anesthetists. Australia anticipates a 35.7% rise in anesthesia cases between 2017 and 2032, creating workforce gaps that amplify reliance on efficient supraglottic devices.[1]Australian and New Zealand College of Anaesthetists, “Workforce Projections 2017-2032,” anzca.edu.au The United Kingdom reports a deficit of 1,900 anesthetists, about 15% below requirements, causing elective surgery delays that heighten demand for time-saving airways.[2]Royal College of Anaesthetists, “Workforce Census 2024,” rcoa.ac.uk

Growing Demand for Disposable LMAs in ICUs & ORs

The World Health Organization’s 2024 infection-control guidance endorses single-use devices where sterilization is inconsistent. Disposable laryngeal masks eliminate autoclaving delays, cut cross-contamination risk, and satisfy strict hospital audits, especially in North America and Europe. The U.S. FDA’s 2024 Class II recall of a pediatric supraglottic airway for unapproved indications underscores the regulatory scrutiny surrounding reprocessing claims. Post-market surveillance under ISO 13485 and the EU MDR now underpins supplier qualification.[3]U.S. Food and Drug Administration, “Recall Z-2914-2024: King LTSD Supraglottic Airway,” fda.gov These converging pressures reinforce the centrality of single-use products within the laryngeal airway mask market.

Ageing Population Fuelling Anesthesia Procedures

Japan’s elderly population share reached 29.3% in 2024, while China’s 65-plus cohort surpassed 310 million, driving up surgical demand.[4]Ministry of Health, Labour and Welfare Japan, “Annual Health Statistics 2024,” mhlw.go.jp Older patients are at higher risk of aspiration and have more difficult airways, prompting clinicians to choose second-generation masks equipped with drainage ports and cuff-pressure indicators. Australia’s projected shortfall of anesthesia providers further underscores the need for devices that non-specialists can safely deploy. Simultaneously, United States Medicare ASC payments hit USD 6.8 billion in 2023, reflecting migration of cataract and joint procedures to outpatient settings where fast-turn supraglottic devices excel. These demographics enlarge the laryngeal airway mask market footprint across care venues.

Rapid Design Improvements in 2nd-Generation Devices

Clinical studies show that shifting from first- to second-generation masks cut adverse events by 0.3 percentage points per month in high-volume centers. Emerging third-generation models embed miniature cameras and real-time cuff-pressure sensors, addressing the 5-10% malposition rate that impairs ventilation. Teleflex secured FDA clearance in April 2025 for the LMA Fastrach ETT, which marries supraglottic ventilation with rescue intubation capabilities. Patent filings highlight antimicrobial coatings and wireless pressure alarms that promise fewer mucosal injuries and ICU-stay complications. Such innovations invigorate the laryngeal airway mask market and intensify product-refresh cycles.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent regulatory & quality-system hurdles | -0.8% | Europe, North America | Medium term (2-4 years) |

| Inadequate peri-operative infrastructure in LICs | -0.6% | Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Competition from endotracheal tubes & video laryngoscopes | -0.5% | Developed markets with high specialist density | Short term (≤ 2 years) |

| Sustainability pressure on single-use plastics | -0.4% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory & Quality-System Hurdles

The EU Medical Device Regulation mandates extensive clinical data and periodic recertification, extending device approval timelines by up to two years. Although a 2025 legislative proposal seeks to trim administrative load, manufacturers still face higher compliance costs and deep post-market surveillance obligations. In the United States, heightened FDA scrutiny following multiple airway recalls forces companies to strengthen quality management systems and complaint tracking. Smaller firms struggle to absorb these costs, consolidating the laryngeal airway mask market around well-capitalized incumbents.

Inadequate Peri-Operative Infrastructure in LICs

A Somali facility survey showed only 15% availability of functional anesthesia machines and unreliable oxygen supplies, hampering adoption of advanced airway products. Rwanda reports that just 53.7% of hospitals stock inhalational agents, reflecting broader supply constraints. Physician-anesthetist density averages 0.41 per 100,000 population in sub-Saharan Africa, far below the recommended 10 per 100,000. Limited sterilization resources also push facilities toward single-use masks that they cannot always afford, capping laryngeal airway mask market penetration in low-income territories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposables Dominate, Specialty Devices Accelerate

Disposable masks accounted for 61.78% of the laryngeal mask airways market revenue in 2025. Their infection-control edge convinced infection-prevention committees to adopt “single-use only” policies across many hospitals. Second-generation disposable units featuring gastric drainage and higher seal pressures are advancing at a 7.78% CAGR, raising average selling prices and offsetting commodity-line ASP compression. Reusables linger in resource-constrained health systems but lose ground as sterilization labor and traceability costs approach disposable levels. Specialty masks engineered for bariatric and robotic procedures carve out profitable micro-segments that encourage continuous R&D.

OEMs now optimize sterile-pouch logistics and lean inventory to match just-in-time surgery schedules. Regulatory audits spotlight sterilization process validation, favoring branded vendors with ISO-compliant quality systems. Environmental pushback is real, yet early-stage bioplastic prototypes indicate a feasible middle path between infection control and circular-economy mandates.

By Age Group: Pediatric Surge Driven by Guideline Updates

Adults accounted for 59.85% of the laryngeal mask airways market in 2025, mirroring the broader surgical patient mix. Pediatric and neonatal use, however, posts the fastest 8.12% CAGR through 2031 as randomized trials confirm superior outcomes compared with intubation in airway surgery. The Union of European Neonatal and Perinatal Societies now recommends LMAs in resuscitation when intubation skills are scarce. Device makers roll out micro-cuff models sized for infants weighing under 2 kg.

Asia’s NICU build-outs, notably in regional Chinese trauma centers, boost neonatal demand, while U.S. pediatric dental surgeries add outpatient volume. The demographic mix shift raises design complexity and triggers stricter regulatory scrutiny, forming an IP moat around incumbents.

By End User: ASCs Outpace Hospitals on Efficiency Gains

Hospitals accounted for 58.12% of 2025 revenue, driven by high surgical volumes and early adoption of advanced technologies. Ambulatory surgical centers, however, show the sharpest 8.44% CAGR as payers steer procedures toward same-day discharge. LMAs align with ASC throughput metrics, such as swift insertion, minimal sore throat, and faster recovery, prompting administrators to bundle them into fixed-cost procedure packs. Specialty clinics in ENT and fertility embrace LMAs for hands-free ventilation, while pre-hospital providers extend total addressable demand by standardizing supraglottic airways in advanced life-support kits.

In military medicine, forward surgical teams stock compact LMA kits for prolonged field care, citing ease of use and rapid seal attainment. Collectively, this end-user diversification boosts device volumes beyond traditional OR confines.

Geography Analysis

North America retained 36.80% of 2025 revenue, driven by high procedure density, stringent infection-control policies favoring disposables, and rapid ASC growth. The United States has clinician shortages 15% below anesthetist demand in the United Kingdom, and notable gaps in rural Canada further underscore the need for devices that speed airway establishment. Military and EMS protocols have also widened non-hospital uptake, extending the laryngeal airway mask market beyond conventional theaters.

Europe’s outlook is mixed: MDR compliance costs squeeze margins, yet a 2025 simplification proposal promises partial relief. Germany, France, Italy, Spain, and the U.K. dominate consumption, with centralized procurement exerting downward price pressure. Population aging in Germany and Italy drives procedural growth. At the same time, workforce shortages in Eastern Europe underscore the need for user-friendly supraglottic solutions, supporting the stable expansion of the laryngeal airway mask market.

Asia-Pacific is set to grow at an 8.82% CAGR as surgical infrastructure scales across China, India, Indonesia, and Vietnam. Regulatory harmonization initiatives in ASEAN and India’s production-linked incentive scheme facilitate local manufacturing, trimming import dependency. Japan and Australia, with aging demographics and high surgical intensity, are early adopters of third-generation video masks, enlarging premium-tier demand. Collectively, these factors make Asia-Pacific the most dynamic contributor to the laryngeal airway mask market.

Middle East and Africa remain constrained by infrastructure gaps, yet higher-income GCC states are upgrading peri-operative capabilities and importing advanced second-generation devices through publicly funded expansion programs. In contrast, many sub-Saharan hospitals lack sterilization equipment, restricting uptake despite high unmet need. South America’s core markets, Brazil and Argentina, wrestle with macroeconomic volatility, but gradual hospital modernizations support steady, if modest, growth in the laryngeal airway mask market.

Competitive Landscape

Leading companies such as Ambu, Teleflex, Medtronic, ICU Medical’s Smiths Medical division, and Intersurgical hold significant positions in the laryngeal airway mask market. These players capitalize on extensive product portfolios, ISO 13485 certifications, and strong hospital partnerships to maintain their competitive edge. Teleflex has expanded its airway product range with the introduction of the LMA-Fastrach ETT, strengthening its presence in the difficult-airway segment. Ambu’s single-use AuraGain line remains a preferred choice in infection-sensitive ICUs, supported by clinician-training platforms that enhance customer retention.

Competitors are increasingly focusing on innovation, as evidenced by efforts to incorporate wireless pressure sensors and antimicrobial cuffs into their products, signaling a shift toward enhanced patient safety. Emerging products with video-assisted supraglottic designs, such as SaCoVLM, SafeLM, and Vision Mask, aim to reduce malpositioning and could disrupt mid-tier market segments if pricing aligns with hospital budgets. However, strict regulatory requirements and lengthy procurement cycles continue to slow the pace of market disruption, enabling established leaders to retain their positions.

Opportunities exist in low- and middle-income regions for cost-effective, durable devices designed for use by non-physician personnel. Nevertheless, challenges such as fragmented procurement processes, constrained budgets, and unstable logistics deter many multinational companies. Partnerships with global donors or local manufacturers could provide a viable pathway for market entry, potentially reshaping the competitive dynamics of the laryngeal airway mask market.

Laryngeal Airway Mask Industry Leaders

Teleflex Incorporated

Intersurgical Ltd

Medline Industries, Inc

Asid Bonz GmbH

Ambu A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Smiths Medical, now under ICU Medical, unveiled a silicone cuff redesign for its Portex Bilevel mask to meet upcoming EU microplastics compliance, with market launch slated for Q3 2026.

- July 2025: Teleflex completed the EUR 760 million acquisition of BIOTRONIK’s vascular-intervention unit, broadening its critical-care cross-sell channels.

- April 2025: Teleflex received FDA 510(k) clearance for the LMA Fastrach ETT, enabling endotracheal intubation through a supraglottic conduit in difficult airways.

Global Laryngeal Airway Mask Market Report Scope

As per the scope of the report, a laryngeal mask airway (LMA), also known as the laryngeal mask, is a single-use or reusable supraglottic airway device that may be used as a temporary method to maintain an open airway.

The Laryngeal Airway Mask Market is segmented by product type, end-user, and geography. By product type, the market is segmented into reusable and disposable. By end-user, the market is segmented into hospitals & clinics, ambulatory surgery centers, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Disposable Laryngeal Masks |

| Reusable Laryngeal Masks |

| Specialty / Second-Generation Masks |

| Adult |

| Pediatric & Neonatal |

| Hospitals |

| Ambulatory Surgical Centres |

| Speciality Clinics |

| Pre-hospital Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Disposable Laryngeal Masks | |

| Reusable Laryngeal Masks | ||

| Specialty / Second-Generation Masks | ||

| By Age Group | Adult | |

| Pediatric & Neonatal | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Speciality Clinics | ||

| Pre-hospital Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the laryngeal airway mask market by 2031?

It is expected to reach USD 725.70 million in 2031, reflecting a 5.68% CAGR from 2026.

Which product segment is growing fastest within laryngeal airway masks?

Specialty and second-generation masks, featuring gastric drainage and video guidance, are projected to grow at 7.78% CAGR through 2031.

Why are ambulatory surgical centers important for airway-mask suppliers?

ASC procedure volumes are rising 5.7% annually, and their preference for disposable devices supports an 8.44% CAGR outlook for ASC demand.

How do pediatric guideline changes affect market demand?

The 2025 neonatal resuscitation update endorses laryngeal masks for ?34-week infants, driving an 8.12% CAGR in pediatric and neonatal applications.

What regulatory trend most affects new airway-mask launches in Europe?

EU Medical Device Regulation requirements for clinical evidence and periodic recertification extend approval timelines and increase compliance costs.

Which region is forecast to grow fastest?

Asia-Pacific, at an estimated 8.82% CAGR, propelled by expanding surgical capacity and regulatory harmonization initiatives.

Page last updated on: