Surgical Blades Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

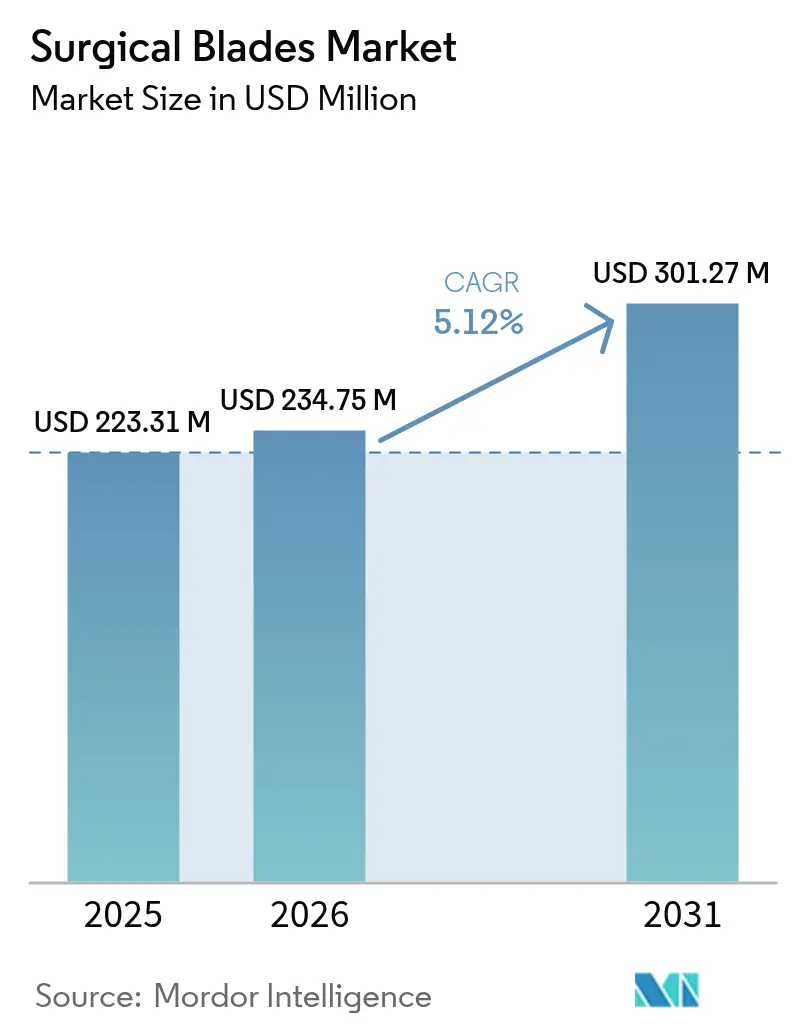

| Market Size (2026) | USD 234.75 Million |

| Market Size (2031) | USD 301.27 Million |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Blades Market Analysis by Mordor Intelligence

The Surgical Blades Market size was valued at USD 223.31 million in 2025 and estimated to grow from USD 234.75 million in 2026 to reach USD 301.27 million by 2031, at a CAGR of 5.12% during the forecast period (2026-2031).

Adoption of minimally invasive procedures, the rising volume of outpatient surgeries, and sustained innovation in blade materials have kept demand steady even as hospitals tighten procurement budgets. Higher-precision cutting requirements in robotic and image-guided surgeries favor premium ceramic and diamond-coated products, while infection-control rules continue to steer clinicians toward sterile, single-use formats. Growth in ambulatory surgery centers is translating into predictable, high-volume contracts for disposable blades, and value-based care models are rewarding suppliers that can prove measurable improvements in outcomes through advanced blade designs.

Key Report Takeaways

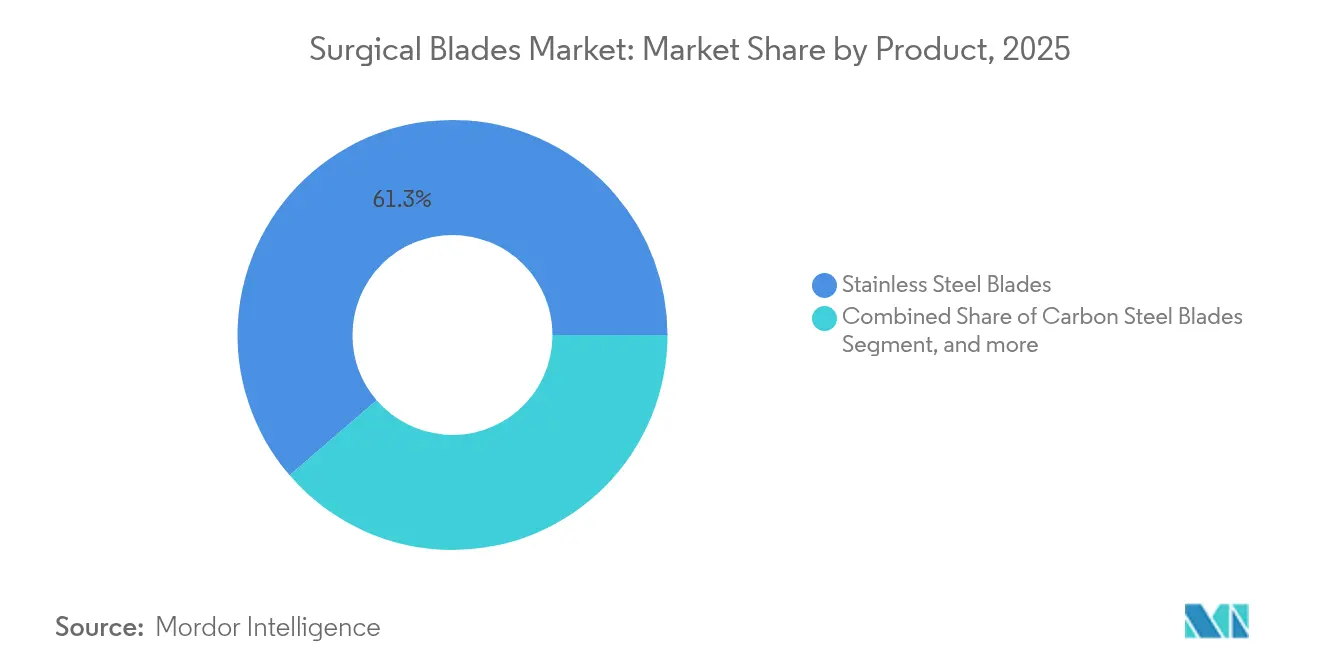

- By product category, stainless steel led with 61.32% revenue share in 2025, while ceramic and diamond-coated blades are projected to register the fastest 5.72% CAGR to 2031.

- By type, sterile blades commanded 71.96% share of the surgical blades market in 2025; non-sterile blades are forecast to expand at a 7.35% CAGR.

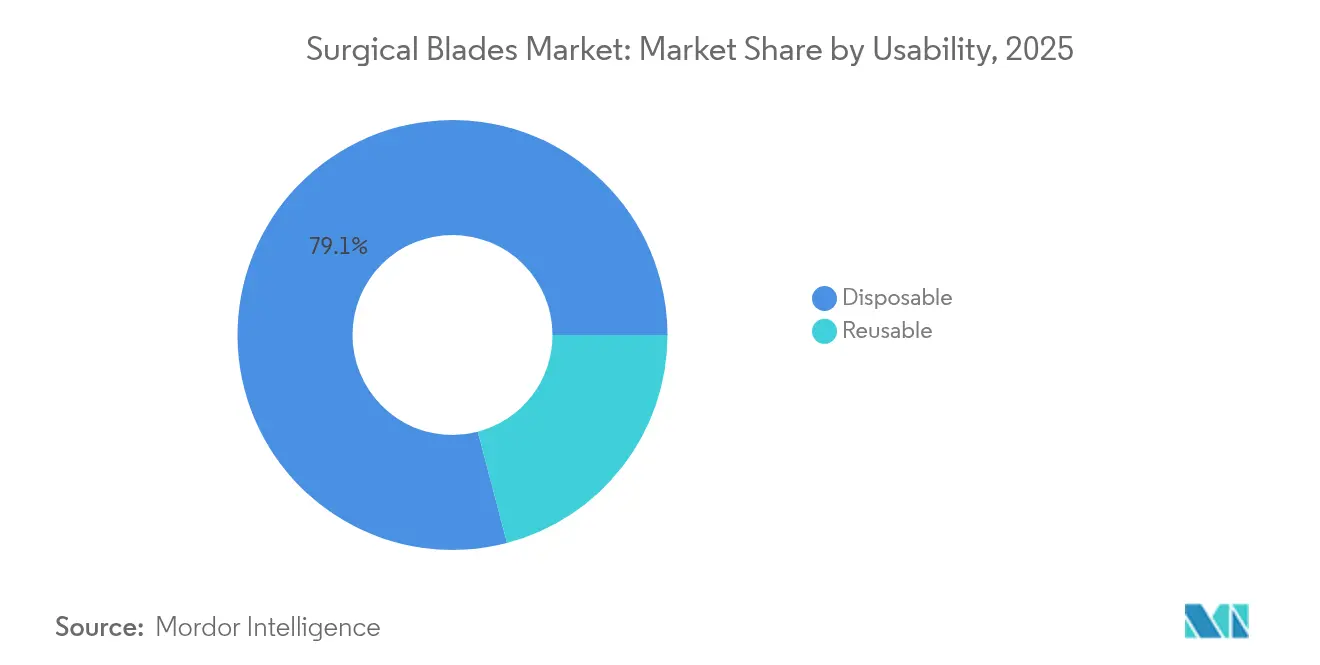

- By usability, disposable formats captured 79.08% of the surgical blades market size in 2025, whereas reusable blades will grow at an 8.18% CAGR through 2031.

- By surgical specialty, orthopedic surgery held 27.55% of surgical blades market share in 2025; cardiovascular surgery is set to rise at a 5.56% CAGR.

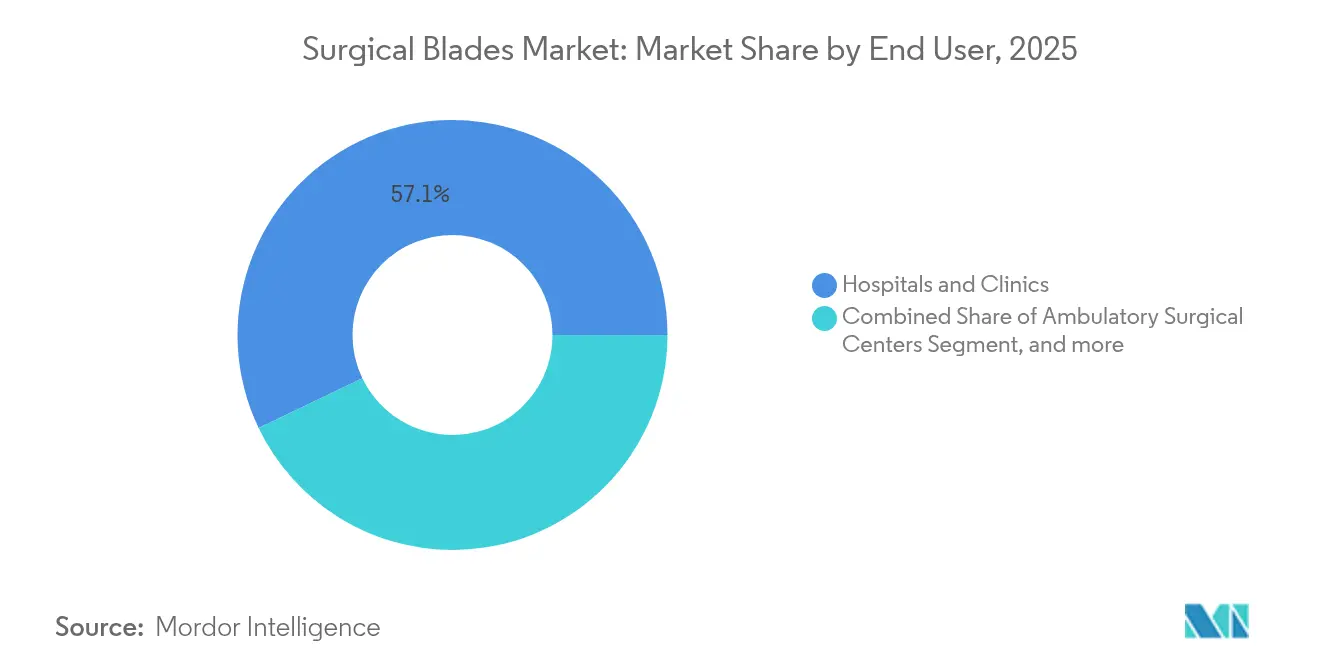

- By end-user, hospitals and clinics accounted for 57.12% share in 2025, yet ambulatory surgery centers show the strongest 6.52% CAGR outlook.

- By geography, North America retained 36.74% regional share in 2025; Asia-Pacific exhibits the highest 7.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Blades Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising number of complex & minimally-invasive surgeries | +1.2% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Rapid expansion of day-care/ambulatory surgery centers | +0.9% | North America & Asia-Pacific core, spill-over to Europe | Short term (≤ 2 years) |

| Heightened infection-control norms favouring single-use blades | +0.8% | Global | Short term (≤ 2 years) |

| Shift to value-based care boosting instrument-tracking adoption | +0.6% | North America & Europe | Medium term (2-4 years) |

| Additive-manufactured (3-D printed) micro-blades for robotic surgery | +0.4% | North America, Europe, Japan | Long term (≥ 4 years) |

| ESG-linked sourcing of “green-steel” blades by hospitals | +0.3% | Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Number of Complex & Minimally Invasive Surgeries

Demand for ultra-sharp, nanometric-polished blades has climbed as surgeons seek to limit thermal injury and reduce postoperative scarring by up to 40% compared with conventional steel instruments.[1]Nan Zhang, “Development of TaMoNbTiZr Alloys for Surgical Applications,” MDPI, mdpi.com Robot-assisted systems now rely on micro-profile blades that can navigate confined anatomical spaces without causing collateral tissue damage. Growth in endoscopic spine, bariatric, and single-port gynecologic procedures has therefore widened the addressable base for premium materials such as ceramic and diamond coatings. Hospitals also favor single-use options for these delicate interventions to guarantee sterility and consistent edge integrity. As imaging platforms improve resolution, the surgical blades market is expected to see continued migration toward smaller, precision-ground geometries that complement minimally invasive workflows.

Rapid Expansion of Day-Care/Ambulatory Surgery Centers

Ambulatory centers prioritize fast turnover, lean staffing, and simplified supply chains. Disposable blade systems align with these goals because they eliminate reprocessing delays and reduce capital spending on sterilization equipment. In the United States and several Asia-Pacific countries, favorable reimbursement schedules and relaxed certificate-of-need rules have accelerated construction of new facilities, each sourcing standard packs of single-use blades for predictable case volumes. Manufacturers benefit from longer-term purchasing agreements that smooth production planning and inventory management. Competitive differentiation now centers on packaging efficiency, sharpness retention until point of use, and integration with digital inventory platforms to monitor open-but-unused stock.

Heightened Infection-Control Norms Favouring Single-Use Blades

Updated guidelines from the Centers for Disease Control and Prevention classify surgical blades as regulated medical waste after a single patient contact.[2]Centers for Disease Control and Prevention, “Guideline for Disinfection and Sterilization in Healthcare Facilities,” CDC, cdc.gov Hospitals have accordingly tightened audit trails and require documented proof of sterility for all cutting instruments. Pre-sterilized blades offer traceable lot numbers and validated shelf lives, easing compliance and lowering the administrative load associated with multi-step reprocessing protocols. The trend has intensified purchasing of individually pouched blades, especially in high-acuity specialties that treat immunocompromised patients. Suppliers that demonstrate robust sterility assurance levels and transparent quality records gain preferred-vendor status in competitive tenders.

Shift to Value-Based Care Boosting Instrument-Tracking Adoption

Outcome-driven reimbursement frameworks reward tools that minimize complications, shorten operating times, and lower readmission rates. Single-use blades embedded with data-matrix identifiers allow automatic linkage of instrument details to electronic health records, supporting post-procedure analytics. Providers are therefore more willing to pay premium prices when clinical evidence shows faster wound healing or reduced transfusion needs. Blade makers able to supply peer-reviewed performance data and compatible tracking software interfaces secure an edge in this evolving purchasing environment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of high-grade specialty steel | -0.7% | Global, particularly Europe & North America | Short term (≤ 2 years) |

| Growing adoption of energy-based cutting devices | -0.9% | North America & Europe | Medium term (2-4 years) |

| Waste-management regulations restricting single-use devices | -0.5% | Europe & select North American jurisdictions | Long term (≥ 4 years) |

| Shortage of sterile-processing technicians in low-income regions | -0.4% | Asia-Pacific emerging markets, MEA, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of High-Grade Specialty Steel

Tariffs and supply disruptions have forced manufacturers to pay wide premiums for European and Japanese alloys that meet medical-grade purity thresholds. Smaller firms without hedging programs face margin compression whenever spot prices spike, occasionally delaying product launches or prompting material substitutions that require fresh validation testing. Quality-driven buyers remain cautious about lower-cost imports that may exhibit variable hardness or trace contaminant levels. Over the next two years, larger suppliers with multi-year contracts or vertically integrated mills are expected to strengthen share by offering stable pricing and uninterrupted supply.

Growing Adoption of Energy-Based Cutting Devices

Electrosurgical, ultrasonic, and laser platforms provide simultaneous cutting and hemostasis, reducing the need for separate scalpels in select laparoscopic and robotic cases. Medtronic’s PlasmaBlade operates at temperatures 64% cooler than standard electrocautery while matching scalpel precision, lowering smoke generation and collateral thermal injury. Comparative trials in BMC Surgery confirmed functional equivalence in 97% of evaluated procedures. Although acquisition costs remain high, hospitals performing large volumes of soft-tissue cases see workflow advantages that justify investment, potentially dampening demand for traditional blades in those departments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Advanced Materials Extend Performance Horizons

Stainless steel retained leadership with 61.32% share in 2025 because its machinability and favorable cost profile suit broad surgical indications. The surgical blades market size for stainless steel products is projected to rise steadily alongside procedure volumes, even as premium materials outpace average growth. Ceramic and diamond-coated variants, expanding at a 5.72% CAGR, address surgeon preference for edges that stay sharper longer and generate less friction. TaMoNbTiZr high-entropy alloys reach hardness values up to 984 HV0.5 after heat treatment, offering potential durability breakthroughs. Titanium alloys such as Ti-33Mo-0.2C form dense titanium-carbide networks that improve corrosion resistance under aggressive cleaning cycles. Surface coating advances, including titanium nitride layers, reduce particulate shedding and virtually eliminate detectable metal ion release, enhancing biocompatibility and extending blade life.

R&D teams increasingly combine additive manufacturing with nano-scale polishing to fabricate micro-profile blades calibrated for robotic wrists. Carbon steel remains a niche option where budget constraints outweigh longevity needs, particularly in emerging markets ordering high volumes of basic disposable scalpels. Yet rapid technology transfer from aerospace metallurgy is accelerating introduction of hybrid composites that align hardness, flexibility, and antimicrobial properties within one substrate. Continued cost reductions should broaden access to these materials, further diversifying the surgical blades market over the forecast window.

By Type: Sterile Packaging Retains the Upper Hand

Sterile blades accounted for 71.96% of revenue in 2025, reflecting hospital mandates for ready-to-use instruments in critical care settings. The FDA updated reprocessing guidance has nonetheless encouraged interest in non-sterile versions where facilities possess validated sterilizers and rigorous documentation workflows.As a result, the non-sterile category will post the fastest 7.35% CAGR. Large integrated delivery networks are aggregating demand to negotiate volume pricing on bulk-packaged, non-sterile blades that they can process centrally, trimming per-case costs. Supply-chain software now flags component expiry in real time, ensuring internal reprocessing cycles do not exceed recommended turnover windows.

Advances in low-temperature hydrogen peroxide plasma units and vaporized peracetic acid systems have raised confidence in in-house sterilization outcomes. Manufacturers selling non-sterile products now supply detailed cycle parameters and material compatibility sheets to support hospital validation. At the same time, emergency departments and small clinics lacking sophisticated reprocessing gear continue to favor single-wrapped sterile blades that arrive ready for immediate use. Competitive positioning therefore hinges on offering flexible packaging configurations, from bulk cartons for sterile processing departments to peel-pouch packs for point-of-care environments.

By Usability: Sustainability Goals Propel Reusable Alternatives

Disposable blades still dominate with 79.08% share in 2025, underpinned by infection-control standards and the operational convenience of single-use kits. Yet reusable blades will experience an 8.18% CAGR as health systems measure waste streams and carbon footprints. The European Union’s circular-economy directives push hospitals to evaluate life-cycle impacts, prompting trials of hardened titanium blades capable of enduring multiple autoclave cycles without edge degradation. The surgical blades market share of reusable products is expected to inch upward as total-cost-of-ownership models reveal breakeven points within 18-24 months for high-utilization theaters.

Emerging surface treatments such as diamond-like-carbon coatings enhance resistance to micro-pitting, allowing dozens of sterilization cycles before resharpening. Centralized sharpening programs, bundled into vendor-managed services, further simplify reuse by guaranteeing edge quality on return. Still, high-throughput ambulatory centers prioritize disposables that avoid reprocessing backlogs and staffing requirements. Suppliers therefore maintain dual portfolios, offering environmentally certified reusable lines alongside low-cost disposables to match diverse institutional priorities.

By Surgical Specialty: Cardiovascular Procedures Accelerate Micro-Blade Demand

Orthopedic surgery consumed 27.55% of blades in 2025, driven by frequent joint replacements and trauma interventions that require robust edges for bone resection. However, cardiovascular procedures will advance fastest at a 5.56% CAGR as minimally invasive valve repairs and coronary artery bypass techniques adopt blades engineered for narrow operative fields. Robotic cardiac platforms integrate wristed instruments holding sub-millimeter blades optimized for root-side bone cutting. General surgery continues to absorb large quantities of standard steel scalpels, yet energy-based alternatives are displacing blades in select hepatobiliary and colorectal cases.

Neurosurgery and ophthalmology maintain stringent requirements for ultra-fine tip geometries to avoid neural or retinal micro-trauma. Plastic and reconstructive surgeons increasingly specify nanometric-polished ceramic blades that leave barely perceptible incision lines, supporting aesthetic outcomes demanded by patients. Collectively, the breadth of specialty needs is widening the surgical blades market, ensuring that material scientists and design engineers target very different performance envelopes within the same overarching product category.

By End-User: Ambulatory Surgery Centers Reshape Procurement Patterns

Hospitals and clinics controlled 57.12% of 2025 volume because they handle complex, multidisciplinary caseloads. Nonetheless, ambulatory centers will outpace all other settings at a 6.52% CAGR as payers incentivize procedures in lower-cost sites. These centers prefer preconfigured blade kits that streamline setup and facilitate rapid room turnover. The surgical blades market size tied to ambulatory facilities is projected to expand significantly in North America and parts of Asia, where liberal licensing rules encourage private investment in stand-alone units.

Academic research institutes influence upstream innovation by partnering with manufacturers on clinical validation studies. Specialty surgical hospitals, such as orthopedic centers of excellence, often standardize on premium blades that maintain sharpness throughout lengthy revision cases, highlighting the continued importance of performance over unit cost in high-acuity environments. Vendors able to dovetail product features with each setting’s workflow stand to secure multi-year, system-wide contracts.

Geography Analysis

North America held 36.74% share in 2025, supported by high procedure volumes, widespread insurance coverage, and early adoption of premium materials. Federal guidance on single-use device reprocessing has provided clear compliance pathways that reassure procurement teams about sterility assurance. Rapid growth in ambulatory centers and continued migration toward value-based payment models sustain demand for single-use, trackable blades. Domestic manufacturers also benefit from logistical proximity, which allows quick replenishment of hospital inventories during peak periods.

Asia-Pacific represents the fastest advancing region at an 7.58% CAGR through 2031. Rising incomes and large-scale investments in surgical infrastructure across China, India, and Southeast Asia are expanding access to elective procedures. Local companies are entering the surgical blades market with competitively priced stainless steel options, while multinational suppliers introduce premium ceramic and titanium lines for tertiary hospitals. Regulatory heterogeneity requires tailored registration strategies, but pipeline reforms in Japan and Australia are shortening time-to-market for innovative devices.

Europe maintains steady growth as sustainability policies influence purchasing. Hospitals weigh lifecycle costs and environmental impacts, leading some to pilot reusable titanium blades despite higher front-end pricing. Germany, France, and the United Kingdom remain major importers of cutting-edge materials, whereas Southern European markets lean toward cost-effective stainless steel disposables. Emerging healthcare systems in the Middle East, Africa, and South America are adding operating rooms and surgeon training programs, but currency volatility and constrained budgets limit uptake of premium blades. Even so, incremental upgrades to infection-control protocols across these regions should gradually lift unit demand.

Competitive Landscape

The surgical blades market features moderate fragmentation, with global brands competing alongside regional specialists. Large players leverage vertically integrated steel processing, automated grinding lines, and advanced coating chambers to sustain scale advantages. Mid-sized manufacturers differentiate through niche geometries or patented surface treatments. Ceramic and diamond-coated innovations have become focal points for premium segment rivalry, as documented hardness and edge-retention metrics provide clear selling points during value-analysis committee reviews.

Competition also revolves around supply-chain reliability. Hospitals impose strict delivery timelines and often dual-source to hedge against shortages of high-grade steel. Companies offering redundant manufacturing footprints and transparent ESG credentials are preferred partners. Marketing narratives increasingly emphasize evidence-based outcomes vendors publish peer-reviewed data linking blade design to reduced incision inflammation, faster closure, or lower suture counts. Firms unable to supply such data risk exclusion from value-based formularies.

Digital enablement is another battleground. Suppliers embed unique device identifiers and radio-frequency tags in packaging, enabling real-time inventory monitoring and automated charge capture. Vendors that integrate dashboards into hospital enterprise resource planning gain stickiness, as switching costs rise once instrument data flows are embedded. Concurrently, private-label brands produced for large distributors compete on price, pressuring margins in the commoditized stainless steel segment. Against this backdrop, strategic acquisitions continue: multinationals absorb material-science start-ups to accelerate pipeline diversification, while regional leaders purchase smaller peers to secure capacity and local regulatory approvals.

Surgical Blades Industry Leaders

Swann-Morton Limited

Aspen Surgical

Hu-Friedy Mfg. Co., LLC

B. Braun SE

KAI Industries Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Intuitive published peer-reviewed data showing that Force Feedback technology in the da Vinci 5 system lowers tissue force by 43%, signalling new specifications for force-sensitive micro-blades.

- May 2025: BD committed USD 2.5 billion to expand U.S. manufacturing over five years, adding capacity for surgical instruments and reinforcing domestic supply chains.

- April 2025: Smith+Nephew reported USD 1,407 million Q1 revenue with 3.2% growth in Orthopaedics, underpinned by new instrument launches that include advanced blade designs.

- March 2025: Apyx Medical announced full-year 2024 results highlighting continued uptake of its energy-based cutting technologies that compete with traditional blades.

Global Surgical Blades Market Report Scope

As per the report's scope, surgical blades, or scalpels, are used for cutting skin and tissue during surgical procedures. Surgical blades vary in size and shape. These are typically made with stainless steel or carbon steel. The surgical blades market is segmented by product (stainless steel blades and high-grade carbon blades), type (sterile and non-sterile), end user (hospitals and clinics, ambulatory surgical centers, and others), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values (in USD million) for the above segments.

| Stainless Steel Blades |

| Carbon Steel Blades |

| Titanium Alloy Blades |

| Ceramic / Diamond-coated Blades |

| Sterile |

| Non-Sterile |

| Disposable |

| Reusable |

| General Surgery |

| Orthopedic Surgery |

| Cardiovascular Surgery |

| Neurosurgery |

| Ophthalmic Surgery |

| Plastic & Reconstructive Surgery |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Specialty Surgical Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Stainless Steel Blades | |

| Carbon Steel Blades | ||

| Titanium Alloy Blades | ||

| Ceramic / Diamond-coated Blades | ||

| By Type | Sterile | |

| Non-Sterile | ||

| By Usability | Disposable | |

| Reusable | ||

| By Surgical Specialty | General Surgery | |

| Orthopedic Surgery | ||

| Cardiovascular Surgery | ||

| Neurosurgery | ||

| Ophthalmic Surgery | ||

| Plastic & Reconstructive Surgery | ||

| By End-User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Specialty Surgical Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the surgical blades market?

The surgical blades market is valued at USD 234.75 million in 2026.

How fast is the surgical blades market expected to grow?

The market is projected to rise at a 5.12% CAGR and reach USD 301.27 million by 2031.

Which product segment holds the largest share?

Stainless steel blades lead with 61.32% revenue share in 2025.

Which geographic region is growing the fastest?

Asia-Pacific is forecast to expand at an 7.58% CAGR through 2031.

Why are disposable blades so widely adopted?

Infection-control guidelines and the operational efficiencies of single-use instruments drive 79.08% market share for disposable blades.

What is the top growth opportunity for manufacturers?

Supplying precision ceramic and diamond-coated blades for minimally invasive and robotic surgeries, the fastest-growing product category at a 5.72% CAGR, offers the strongest upside.

Page last updated on: