Tracheostomy Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

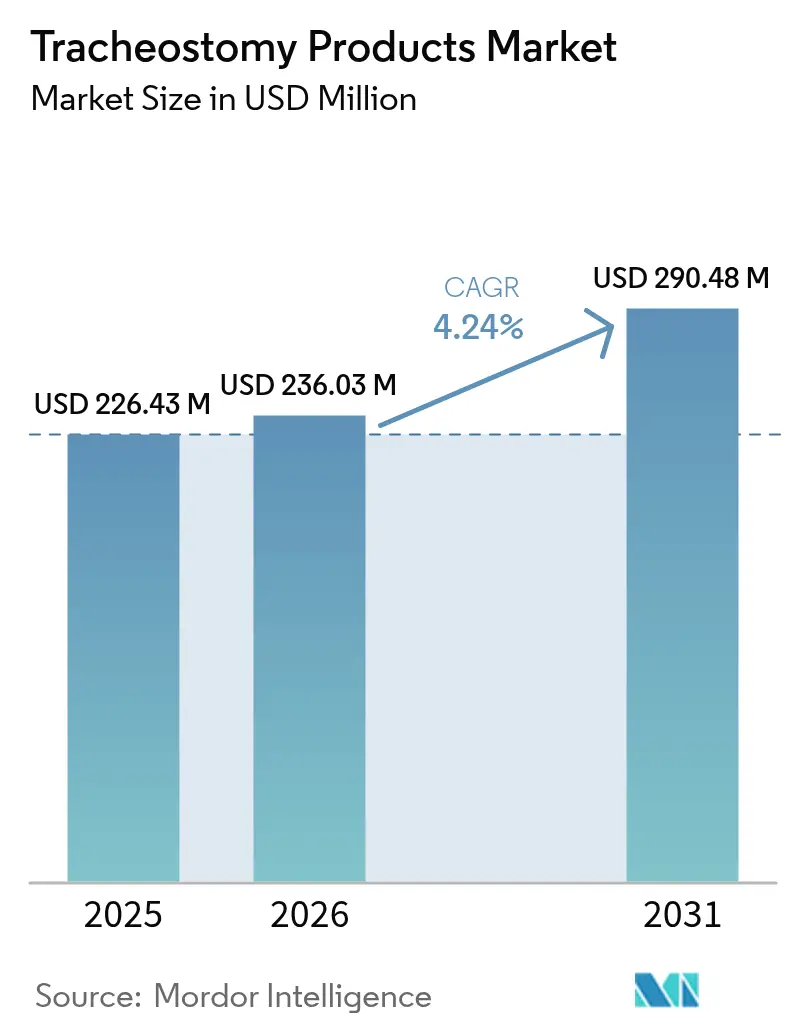

| Market Size (2026) | USD 236.03 Million |

| Market Size (2031) | USD 290.48 Million |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tracheostomy Products Market Analysis by Mordor Intelligence

The tracheostomy products market size was valued at USD 226.43 million in 2025 and estimated to grow from USD 236.03 million in 2026 to reach USD 290.48 million by 2031, at a CAGR of 4.24% during the forecast period (2026-2031). Growth stems from the convergence of minimally invasive percutaneous techniques, material science advances, and an expanding cohort of ventilator-dependent patients seeking safer and more comfortable long-term airway access. Clinical protocols have shifted from emergency surgical openings toward planned procedures, tightening demand for specialized tracheostomy kits that shorten operating time and reduce complications. Hospitals continue to purchase large volumes of conventional tubes, yet home-care programs now influence design priorities by prioritizing intuitive devices, tube exchange simplicity, and integrated remote monitoring. Manufacturers that combine precision-engineered tubes with interoperable IoT sensors gain market visibility, especially in North America where reimbursement favors value-based respiratory care. Supply-chain resilience also shapes investment, as regulators place tracheostomy tubes on critical-device watch lists and urge multisite production to curb shortages.

Key Report Takeaways

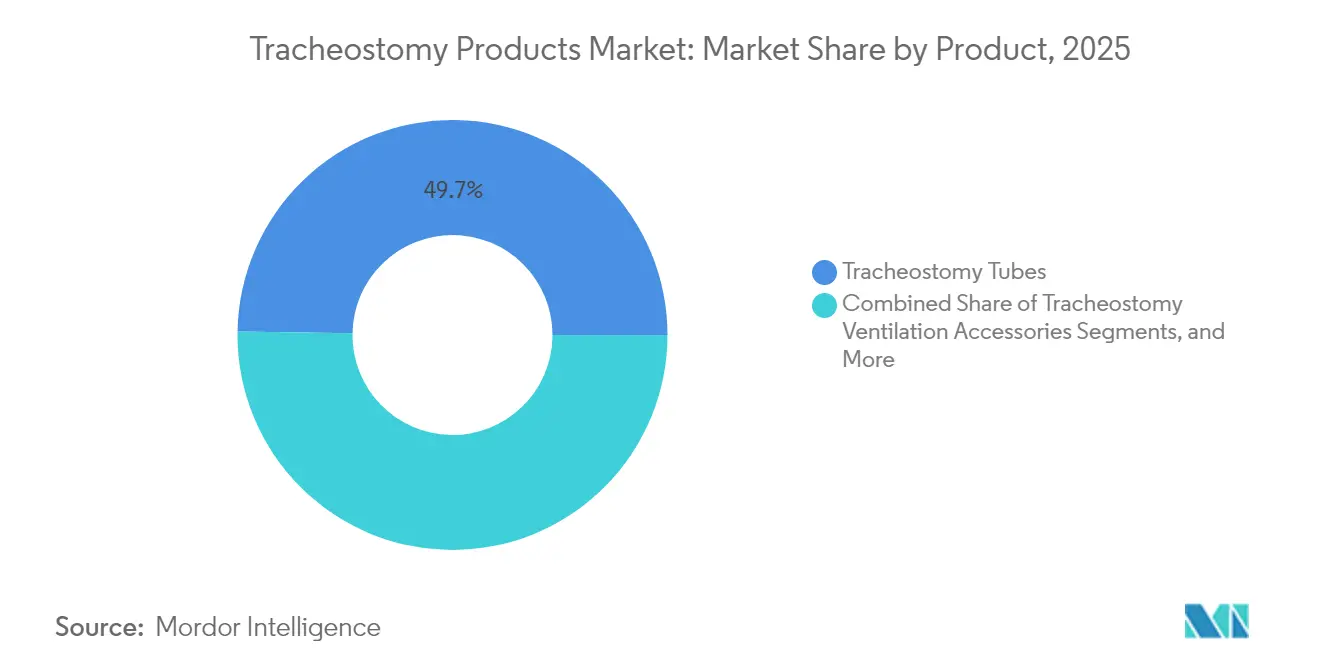

- By product type, tracheostomy tubes led with 49.74% of the tracheostomy products market share in 2025, while ventilation accessories are projected to expand at a 4.74% CAGR through 2031.

- By material, polyvinyl chloride and polyurethane together held 51.88% of the tracheostomy products market size in 2025, but silicone-based devices are advancing at a 4.67% CAGR to 2031.

- By procedure type, percutaneous dilatational tracheostomy captured 53.35% revenue share in 2025; hybrid and endoscopic-assisted methods post the fastest 4.96% CAGR.

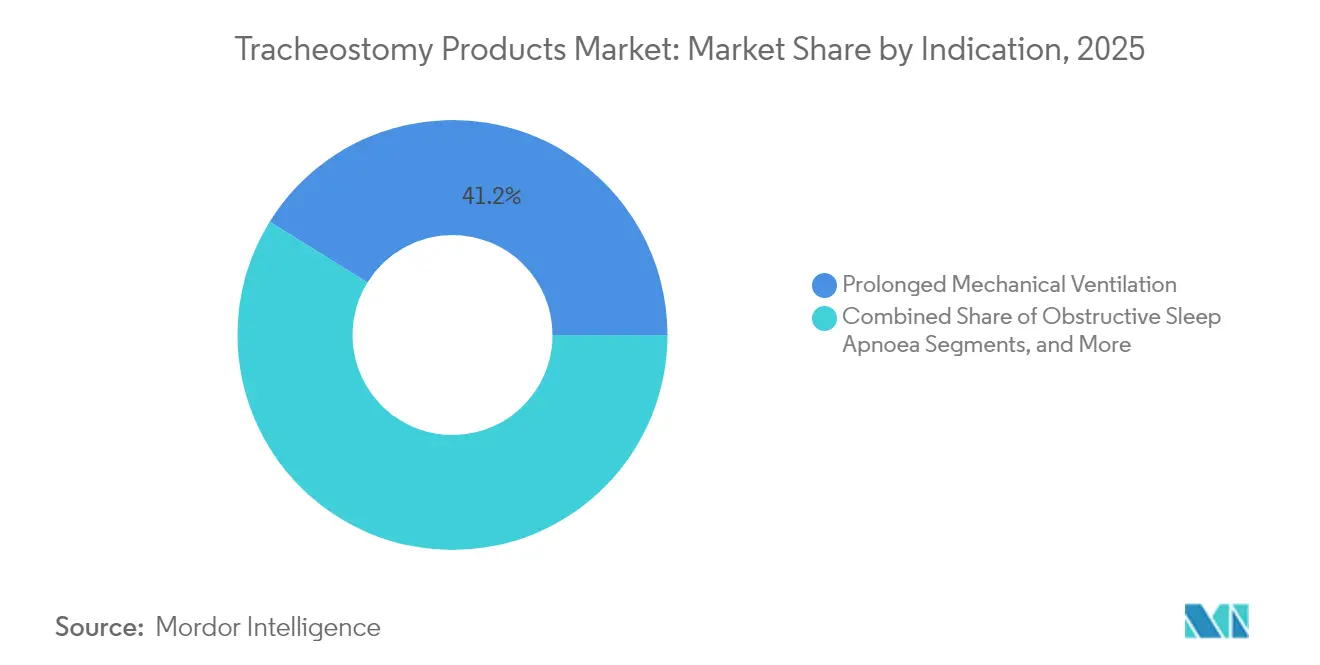

- By indication, prolonged mechanical ventilation accounted for 41.18% of the tracheostomy products market size in 2025, while obstructive sleep apnoea leads future growth at a 5.11% CAGR.

- By end user, hospitals commanded 72.54% of 2025 revenue, whereas home-care settings are enlarging at a 5.06% CAGR on the back of payer-backed weaning programs.

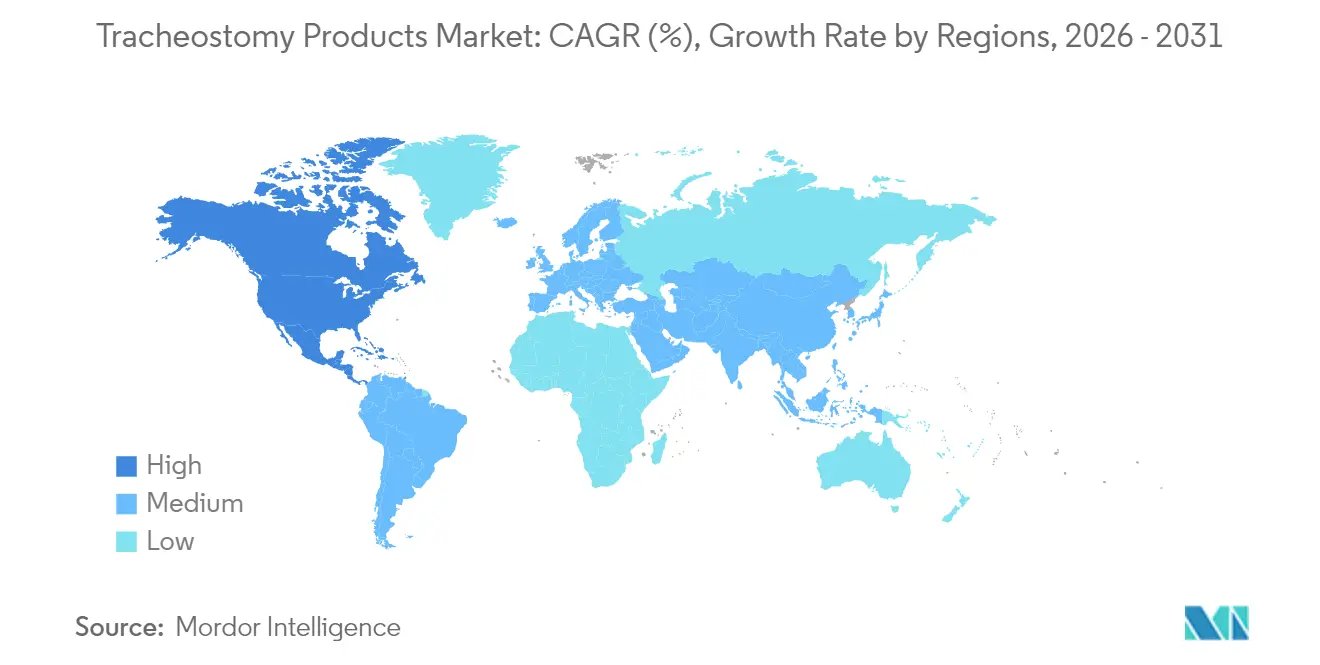

- By geography, North America contributed 42.02% turnover in 2025; Asia-Pacific is set to register a 5.20% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Tracheostomy Products Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic respiratory diseases | +1.2% | Global, with APAC showing highest growth | Long term (≥ 4 years) |

| Aging population & ICU admissions | +0.9% | North America & Europe core, spill-over to APAC | Medium term (2-4 years) |

| Favorable reimbursement in mature markets | +0.7% | North America & EU | Short term (≤ 2 years) |

| Shift toward home-based weaning programmes | +0.8% | Global, with early gains in US, Canada, Germany | Medium term (2-4 years) |

| Wider adoption of minimally-invasive percutaneous techniques | +0.6% | Global | Short term (≤ 2 years) |

| Continuous technological improvements in tubes | +0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Respiratory Diseases

Global chronic respiratory disease cases climbed to 454.56 million in 2024, enlarging the candidate pool for tracheostomy procedures [1]Muhammad Usman, “COVID-19–Associated Tracheal Stenosis: A Systematic Review,” Frontiers in Medicine, frontiersin.org. Post-COVID patients now present longer stenotic segments and cartilage damage, making percutaneous tracheostomy favorable for complex airway rehabilitation. Research on biodegradable stents and drug-eluting tubes broadens treatment choices, encouraging hospitals to invest in higher-priced, complication-mitigating platforms. Device makers that integrate antimicrobial coatings and real-time flow monitoring record stronger adoption because clinicians aim to lower ventilator-associated pneumonia rates while easing prolonged mechanical ventilation transitions. The net effect is a measurable lift in procedural volumes and a preference for advanced kits that optimize decannulation outcomes.

Aging Population and ICU Admissions

Patients aged 50-69 have overtaken older cohorts to form the largest tracheostomy demographic, driven by higher survival in critical-care settings and wider eligibility for elective airway management. Predictive analytics embedded in electronic health records guide clinicians on timing, prompting the purchase of percutaneous systems compatible with bedside ultrasound guidance. With middle-aged survivors returning for repeat evaluations, the tracheostomy products market sees demand for tubes that offer comfort, phonation accessories, and embedded sensors for home monitoring. Vendors that position portfolios around ICU workflow efficiency stand to capture higher replacement sales and service contracts.

Favorable Reimbursement in Mature Markets

Medicare’s 2025 updates grant 4.2% payment increases to skilled nursing facilities and introduce discrete codes for specialized respiratory equipment, directly boosting procurement budgets [2]U.S. Centers for Medicare & Medicaid Services, “CY 2025 Home Health Prospective Payment System Rate Update,” Federal Register, federalregister.gov. Home health rules now reimburse connected tracheostomy devices when they demonstrate reduced readmissions, accelerating payer acceptance of smart tubes. The U.S. and leading EU states further implement social determinants metrics, rewarding suppliers whose products document better quality-of-life outcomes. Firms that present real-world evidence showing fewer tube occlusions or infection events qualify for premium pricing, widening gross margins even as volumes stabilize in hospital settings. The regulatory climate thus channels R&D capital toward sensors, remote dashboards, and disposable tube liners that substantiate measurable value.

Shift Toward Home-Based Weaning Programs

Home decannulation initiatives reveal 31% successful weaning among pediatric cohorts, highlighting cost savings and comfort gains versus prolonged inpatient stays. To support lay caregivers, manufacturers refine tube connectors, suction valves, and audio alarms into integrated platforms that pair with telemedicine portals. Cloud-linked acoustic sensors transmit respiratory sound data to clinicians, enabling proactive intervention and reducing emergency visits. Training videos, color-coded cleaning kits, and single-use consumables form ancillary revenue streams while driving brand loyalty. As reimbursement aligns with at-home ventilator programs, the tracheostomy products market benefits from recurring supply sales and service contracts tied to IoT infrastructure.

Restraints Impact Analysis of Tracheostomy Products Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure & device cost | -0.8% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Device-associated infection risk | -0.6% | Global | Short term (≤ 2 years) |

| Shortage of trained decannulation teams | -0.4% | Global, particularly acute in rural areas | Long term (≥ 4 years) |

| Supply-chain fragility for silicone & silver | -0.5% | Global, with manufacturing concentration in Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure and Device Cost

Tracheostomy kits, postoperative consumables, and specialized staffing together elevate the total cost of ownership, straining budgets in low-resource hospitals. Value-based purchasing now obliges suppliers to furnish pharmacoeconomic models that link premium silicone or silver tubes with shorter ICU stays. Distributors counter price pushback by offering lease-to-own bundles and training packages that spread capital outlays. Emerging-market tenders still favor base-grade PVC tubes, tempering uptake of connected devices despite clinical upside. Cost pressure consequently nudges vendors to streamline component counts, adopt regional manufacturing, and expand portfolio tiers to protect volume share.

Device-Associated Infection Risk

Ventilator-associated pneumonia affects up to 50% of intubated patients, and resistant pathogens complicate therapy, increasing systemic antibiotic use. Hospitals thus hesitate to adopt unproven lumen coatings or porous materials without multi-year outcome data. Regulatory agencies demand rigorous sterility validation, extending approval timelines for nanomaterial or drug-eluting designs. Liability fears push buyers toward incumbent brands with extensive vigilance records, restraining market entry for start-ups despite technical novelties. Suppliers respond by embedding continuous cuff pressure monitors and antimicrobial sleeves into premium SKUs to assure infection-control committees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Tracheostomy Products Market Segment Analysis

By Product Type:

Tubes Sustain Core Revenue while Accessories AccelerateThe tracheostomy products market size attributed to tubes reached USD 112.66 million in 2025, equal to 49.74% of global revenue. Despite ongoing commoditization, tubes retain primacy because every airway procedure needs a well-fitted cannula. Tube makers defend share through incremental gains such as Medtronic’s tapered cuff that cuts leakage by 99% and reduces lateral wall pressure by 18.6%. Ventilation accessories—filters, speaking valves, and humidification chambers—are the fastest climbers at a 4.74% CAGR through 2031 as hospitals seek holistic infection-control bundles. Connected accessories that log airflow metrics integrate seamlessly into electronic records, positioning suppliers for service-based revenue.

Accessory growth also mirrors home-care expansion, where families favor turnkey kits that simplify suction, dressing changes, and emergency management. Smart accessories transmit alerts to telehealth hubs, helping clinicians fine-tune weaning protocols. This evolution from stand-alone cannulas to full airway ecosystems raises switching barriers and promotes multi-product procurement contracts. The tracheostomy products industry thus sees new cross-selling potential, with disposables providing stable recurring income that offsets longer replacement cycles for base tubes.

By Material:

Biocompatible Silicone Advances against Cost-Efficient PVCPVC and polyurethane retained 51.88% market share in 2025 owing to low unit cost and entrenched tooling. Nevertheless, silicone grew at 4.67% CAGR, propelled by reduced hypersensitivity reactions and improved airflow characteristics under high-frequency ventilation modes. The tracheostomy products market benefits when ICUs adopt silicone for complex cases, raising average selling prices and stimulating premium R&D. Hybrid constructions that sandwich silicone liners within PVC shells balance cost with performance and ease regulatory pathways, enabling mid-tier offerings.

Silver and stainless steel tubes continue to serve reconstructive or head-neck oncology needs where durability and antimicrobial traits matter. Emerging biodegradable polymers such as PLGA and PLA attract research funding, offering temporary airway scaffolds that circumvent long-term complications. Nanoparticle-infused coatings disrupt biofilm while preserving lumen patency, yet scale-up challenges linger. Raw material shortages during the pandemic exposed reliance on Asia-centric silicone supply, prompting dual-sourcing and local compounding investments to secure continuity and reassure hospital buyers about delivery timeframes.

By Procedure Type:

Percutaneous Techniques Anchor Modern Airway ManagementPercutaneous dilatational tracheostomy amassed 53.35% of global revenue in 2025, signalling clinician confidence in bedside ultrasound guidance that trims average procedure time to 17 minutes . Its dominance amplifies demand for specialized dilators, curved introducers, and single-use kits offering controlled dilation without bronchoscopic assistance. Hybrid and endoscopic-assisted approaches remain niche but grow fastest at 4.96% CAGR because combined imaging and flexible scopes address anatomical complexities.

Open surgical tracheostomy remains indispensable for trauma and emergent upper-airway obstruction, particularly in lower-resource facilities lacking ultrasound. However, rising practitioner proficiency with percutaneous sets shifts purchasing patterns toward kit-based solutions that bundle introducers, syringe-balloon checkers, and cut-to-fit neck plates. Suppliers that add on-board cuff pressure sensors, disposable drapes, and real-time position indicators convert procedural tools into data sources, reinforcing platform ecosystems and elevating total contract value within the tracheostomy products market.

By Indication:

Ventilator Dependence Prevails yet Sleep Apnoea SurgesProlonged mechanical ventilation comprised 41.18% market share in 2025 and remains the anchor indication as ICUs strive to balance rapid weaning with airway safety. Sophisticated weaning algorithms integrate cough strength, diaphragmatic ultrasound, and endoscopic swallow checks, directing demand toward easily adjustable tubes with subglottic suction ports. Obstructive sleep apnoea shows the swiftest 5.11% CAGR as diagnosis expands beyond morbidly obese adults to encompass craniofacial anomalies and neuromuscular sequelae.

Cancer-related airway obstruction and trauma each call for bespoke tube shapes and extended shafts. Pediatric congenital anomalies drive innovation for smaller diameters, soft flanges, and low-profile connectors tailored to growing necks. Predictive analytics now group indications with ventilation-length forecasts, guiding procurement teams on stocking mix and tube design variations, thereby stabilizing back-orders in the tracheostomy products market.

By End User:

Hospitals Dominate but Home-Care Gains MomentumHospitals delivered 72.54% of tracheostomy revenue in 2025, acting as the central node for initial placement, acute monitoring, and complication management. Budget-prioritized purchasing committees still prefer volume contracts for standard PVC kits, yet specialized ICUs now shift toward smart tubes that integrate with alarm dashboards. In contrast, home-care settings post a 5.06% CAGR as payers finance earlier discharge to curb bed-day costs. Portable suction pumps, reusable cleaning sets, and telemedicine-ready speaking valves populate new consumer-style catalogs.

Ambulatory clinics and day-care centers manage routine tracheostomy changeouts, decannulation assessments, and speech therapy sessions, anchoring recurring accessory orders. Family caregiver training programs drive consumables volume and boost telehealth subscription uptake. Vendors that supply cloud dashboards, replacement reminders, and logistics support improve retention and win multi-year service agreements, strengthening stickiness across the tracheostomy products market.

Geography Analysis

North America Tracheostomy Products Market

North America controlled 42.02% of global revenue in 2025, underpinned by expansive ICU capacity, stringent product-safety oversight, and Medicare payment updates that reward connected respiratory devices. U.S. adoption of percutaneous kits accelerated when professional societies published bedside ultrasound guidelines, and post-acute reimbursement now endorses telemonitored decannulation programs. Canada mirrors this trend through universal coverage, promoting standardized tube bundles that reduce cross-province procurement complexity.

Europe Tracheostomy Products Market

European Union markets collectively provide a robust margin environment thanks to the Medical Device Regulation framework that harmonizes clinical evidence demands and sustains premium pricing for silicone and silver tubes. Germany and France spearhead percutaneous technique uptake due to universal ICU ultrasound access, while Italy and Spain embrace home-based weaning to offset constrained bed capacity. Brexit pushed the United Kingdom to refine its own regulatory files, yet NHS initiatives still favor AI-enabled monitoring tools that document readmission avoidance.

APAC Tracheostomy Products Market

Asia-Pacific registers the fastest 5.20% CAGR as demographic aging, chronic pulmonary disease prevalence, and government healthcare expansion converge. China’s investment in tertiary ICUs and respiratory therapist programs widens the addressable installation base for smart tracheostomy platforms. Japan’s mature health insurance covers high-end silicone tubes, encouraging local production partnerships. India and Southeast Asian nations stimulate price-sensitive segments, prompting hybrid PVC-silicone offerings and incremental adoption of low-cost percutaneous sets. Australia and South Korea, with advanced e-health records, pilot validation studies for IoT-based cuff pressure telemetry, shaping next-generation product specifications across the tracheostomy products market.

Regulatory Landscape

In the United States, tracheostomy tubes and tube cuffs are regulated by the FDA as Class II medical devices under 21 CFR 868.5800. In practice, this typically means 510(k) premarket notification, alongside compliance with Quality System Regulation controls that apply to life-supporting devices. FDA-recognized consensus standards also shape verification and validation packages for market access, with ISO 5366:2016 widely used for design, testing, labeling, and connector requirements across adult and pediatric tracheostomy tubes.

In Europe, tracheostomy tubes fall under the Medical Device Regulation (EU) 2017/745 (MDR). Long-term use tracheostomy tubes are commonly classified as Class IIb under Annex VIII rules, which brings Notified Body involvement and a deeper clinical and post-market evidence burden than lower-risk airway consumables. MDCG guidance on classification under MDR further reinforces the need to separate devices by intended duration of use, and by whether they interface with active devices such as ventilators, shaping conformity assessment pathways (Annex IX/X/XI) and the level of technical documentation required for global portfolio harmonization.

Value Chain Analysis

The value chain begins with raw-material inputs, including medical-grade PVC, polyurethane, and silicone elastomers, plus specialty additives such as antimicrobial coating precursors. Manufacturers then carry out precision extrusion or molding, assemble cuffs and inner cannulas, and package the devices to support sterile presentation. Sterilization (commonly via gamma) is a key midstream step that can constrain throughput if processing capacity tightens. After sterilization, products move through regulatory release, labeling and UDI processes, and then into hospital and home-care channels through direct sales, group purchasing contracts, and medical-device distributors.

Downstream demand is driven by care-setting workflows. Hospitals and ICUs tend to buy tubes and percutaneous dilatational tracheostomy kits in bulk, while home-care programs pull through ventilation accessories, cleaning and care kits, and caregiver-focused consumables on a recurring basis. Portfolio breadth and channel access also matter for maintaining airway coverage, and consolidation is used to expand product lines; for example, Everis Medicals May 2026 acquisition of Hood Laboratories strengthened its surgical and airway management offering, highlighting how M&A can add manufacturing know-how, established customer relationships, and cross-selling leverage across the airway ecosystem.

Competitive Landscape

The tracheostomy products market displays moderate consolidation, with Medtronic, Teleflex, and Smiths Group anchoring global share through broad portfolios, scale production, and regulatory mastery. Medtronic leverages TaperGuard innovations and disposable insertion kits to secure multi-year system agreements with top U.S. IDNs. Teleflex emphasizes percutaneous procedural packs bundled with disinfected bronchoscopes, cutting set-up time for ICU staff and boosting cross-selling. Smiths Group, despite a 2024 Bivona recall related to flange separations, retains hospital loyalty through rapid corrective action and transparent field safety notices.

Digital health entrants pose disruptive potential by embedding low-power sensors and AI flow-pattern analytics into cannula walls. Strategic alliances between traditional device firms and software vendors form to de-risk integration and accelerate FDA clearance. Material-science-focused start-ups pitch biodegradable scaffolds to oncology centers, while contract manufacturers in Malaysia and Mexico add capacity that mitigates silicone supply bottlenecks. Across regions, procurement teams value documented infection-reduction claims and proven supply continuity, steering purchasing toward suppliers that marry innovation with operational reliability. The resulting dynamic sustains moderate pricing power while spurring portfolio diversification across the tracheostomy products market.

Tracheostomy Products Industry Leaders

Medtronic Plc

Smiths Group PLC

Teleflex Incorporated

Boston Medical Products Inc.

TRACOE medical GmbH

- *Disclaimer: Major Players sorted in no particular order

Tracheostomy Products Market Companies Covered in this Report

- Medtronic

- Smiths Group

- Teleflex

- Boston Medical Center

- TRACOE medical

- Cook Group

- Fuji Systems

- Fisher & Paykel Healthcare

- Troge Medical

- Pulmodyne

- Atos Medical AB

- Intersurgical

- Ambu

- Coloplast (Servona)

- Becton Dickinson (CareFusion)

- ICU Medical

- Mercury Medical

- Passy-Muir Inc.

- SunMed LLC

- Boston Scientific

Market Opportunities and Future Outlook

Product differentiation continues to create whitespace beyond commodity PVC tubes, especially where providers target measurable reductions in complications such as biofilm formation, tissue irritation, and infection risk. ISO 5366:2016 serves as a practical anchor for design, testing, labeling, and sterile supply expectations, which supports manufacturers that pair compliant connectors and labeling with advanced materials (silicone and composite constructions). It also helps those that validate performance features such as subglottic suctioning pathways.

Home-care weaning programs and value-based respiratory care expand demand for smart tracheostomy platforms that combine tubes and accessories with monitoring of cuff pressure, airflow, and device integrity, aligning device selection with readmission-avoidance priorities cited in mature reimbursement environments. Recent market activity also points to continued commercial focus on tracheostomy portfolios within broader airway and head-and-neck care: Atos Medicals March 2026 branding rollout across packaging and communications highlights a renewed emphasis on portfolio visibility and standardization at the point of care. In parallel, ongoing research activity, including a March 2026 published feasibility report on an intratracheal sealing disc concept, indicates continued innovation aimed at secure airway management and closure solutions that can flow into next-generation accessory and tube designs.

Recent Industry Developments in Tracheostomy Products Market

- May 2026: Everis Medical announced the acquisition of Hood Laboratories, adding airway management and ENT device capabilities to its portfolio. The deal expands product breadth in surgical airway care and can strengthen distribution leverage for bundled airway solutions across acute and post-acute settings.

- September 2025: Atos Medical updated product documentation for the Tracoe Experc Dilation Set used with the Ciaglia technique for percutaneous dilatational tracheostomy. The update supports procedural standardization and reinforces system-based kit positioning for bedside ICU workflows.

- August 2024: Fisher and Paykel Healthcare introduced the F&P my820 System in the United States, a home respiratory humidifier designed to adjust to ambient conditions and reduce circuit condensation. This launch supports home-care respiratory setups where humidification performance affects secretion management and caregiver burden for tracheostomy patients.

Tracheostomy Products Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers the revenue generated from products used to create and maintain a tracheostomy airway and support ongoing care, from the procedure set through routine replacement and patient comfort items. We treat this as a medical device and consumables market tied directly to tracheostomy care settings.

Scope exclusions: We exclude laryngectomy voice prostheses, general endotracheal intubation supplies, and aftermarket or refurbished items.

Segments Covered in This Report

- By Product Type

- Tracheostomy Tubes

- Tracheostomy Ventilation Accessories

- Tracheostomy Cleaning & Care Kits

- Other Product Types

- By Material

- PVC & Polyurethane

- Silicone

- Metal (Silver / Stainless Steel)

- Biodegradable Polymers & Others

- By Procedure Type

- Surgical / Open Tracheostomy

- Percutaneous Dilatational Tracheostomy (PDT)

- Hybrid / Endoscopic-assisted

- By Indication

- Prolonged Mechanical Ventilation

- Head & Neck Cancer / Tumours

- Obstructive Sleep Apnoea

- Trauma & Emergency Airway

- Neuromuscular & Degenerative Disorders

- Congenital / Other Conditions

- By End User

- Hospitals

- Ambulatory / Day-care Centres

- Home-care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a fact base around tracheostomy procedure volumes and care pathways, then linking those signals to device demand. For this, we refer to non-paywalled sources such as the US Centers for Disease Control and Prevention (CDC), the World Health Organization (WHO), the OECD health statistics, the World Bank, and US FDA database sources for device clearances and safety communications.

To keep assumptions realistic, we also review company annual reports and investor presentations, clinical literature on tracheostomy practice patterns, and hospital and respiratory therapy association websites that describe care protocols. In a few places, we supplement with paid subscriptions for company financials and patent searches, and for shipment level import and export checks where it helps explain regional supply flows. These are illustrative examples, and many other public sources were also used for data collection, validation, and clarifying gaps.

Primary Interviews and Surveys

Primary work is used to pressure test the desk assumptions on unit usage per patient, replacement cycles, and pricing moves across hospitals, ambulatory surgical centers, and home care channels. We speak with a mix of clinical stakeholders and commercial roles, and then reconcile differences by region because procedure practices and reimbursement realities are not the same across geographies.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 48% |

| Mid tier: 42% | Functional/Unit leaders: 31% | EMEA: 31% |

| Smaller Players: 21% | Managers: 56% | Americas: 21% |

Market-Sizing & Forecasting

Market sizing is built using a top-down demand pool, where procedure and prevalence signals are reconstructed into a treated population that uses tracheostomy products, then converted into annual product consumption. When the model is laid out step by step, the main math flows through a small set of practical inputs, and the total is derived at the end.

Key inputs include tracheostomy procedure volumes and ICU utilization indicators, the typical mix of surgical versus percutaneous techniques, the share of cases managed through home care after discharge, and replacement frequency for tubes and related care items. Pricing is handled using average selling price ranges by product group and region, then adjusted for inflation and currency timing for the year being sized. Results are corroborated with selective bottom-up approximations, such as sampled price checks across channels and a limited supplier and distributor revenue roll up to spot over or under counts. Where a country has sparse public procedure data, we use proxy indicators like critical care capacity and respiratory disease burden, then confirm with expert input.

For forecasting, we rely on scenario analysis supported by trend inputs from interviews, since utilization shifts can be driven by guideline adoption, care setting mix changes, and reimbursement signals. Growth rates are applied at the variable level first, then translated into market value, which helps keep the projection anchored to observable drivers.

Data Validation & Update Cycle

Validation is done through multiple checks so totals do not depend on one data point. We compare outputs against independent signals such as procedure trend direction, regional supply patterns, and the implied spend per treated patient, and then we recheck any country that appears out of line.

Before sign-off, assumptions and calculations go through multi step analyst review, and we re-contact select respondents if a key variable shifts or a large variance shows up. Reports are refreshed annually, and interim updates are applied when material events occur, such as major regulatory actions or sudden pricing changes. Right before delivery, a final pass is completed so the numbers reflect the latest available information.

Mordor Intelligence's Tracheostomy Products Market Size Compared Against Other Published Estimates

It is normal to see different market sizes for tracheostomy products because publishers do not always use the same year, the same product list, or the same method for converting procedure demand into device value. Differences also come from pricing assumptions, currency timing, and how frequently estimates are refreshed.

Some published figures lean on a broader device interpretation or a different time base, which can pull in adjacent airway supplies or move the apparent market level when trends are re-anchored to a new starting year. In the Mordor Intelligence view, only devices and consumables tied directly to tracheostomy care are counted, while laryngectomy voice prostheses and general intubation supplies are kept out so the demand pool stays aligned to tracheostomy-specific usage and replacement cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 236.03 M (2026) | |

| Healthcare Publisher A | USD 217.00 M (2024) | Uses an earlier base year and does not clearly state product inclusions and exclusions, so adjacent airway items and different pricing timing can shift the total versus a tracheostomy-only consumption build. |

| Industry Research Group B | USD 230.78 M (2025) | Anchors the series to a different year and can apply different growth pacing across end users, which changes the implied patient volumes and replacement rates used to translate demand into value. |

Taken together, the spread is mainly explained by time base choices and how tightly the product scope is kept to tracheostomy care. By keeping the model tied to procedure linked usage, replacement frequency, and region level pricing logic, we get a market size that can be followed and repeated with clear steps.

Key Questions Answered in the Report

What is the current Tracheostomy Products Market size?

The tracheostomy products market reached USD 236.03 million in 2026 and is projected to grow to USD 290.48 million by 2031 at a 4.24% CAGR.

Who are the key players in Tracheostomy Products Market?

Medtronic Plc, Smiths Group PLC, Teleflex Incorporated, Boston Medical Products Inc. and TRACOE medical GmbH are the major companies operating in the Tracheostomy Products Market.

Which is the fastest growing region in Tracheostomy Products Market?

Asia-Pacific is expanding at a 5.20% CAGR due to rising ICU infrastructure, aging populations, and increasing prevalence of chronic pulmonary diseases.

Why are silicone tracheostomy tubes gaining popularity?

Silicone offers superior biocompatibility and reduced airway irritation, driving a 4.67% CAGR and increasing preference for complex ventilation cases.

Which procedure type holds the largest share?

Percutaneous dilatational tracheostomy leads with 53.35% of global revenue in 2025, reflecting its minimally invasive profile and bedside efficiency.

Page last updated on: