Powered Surgical Instrument Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

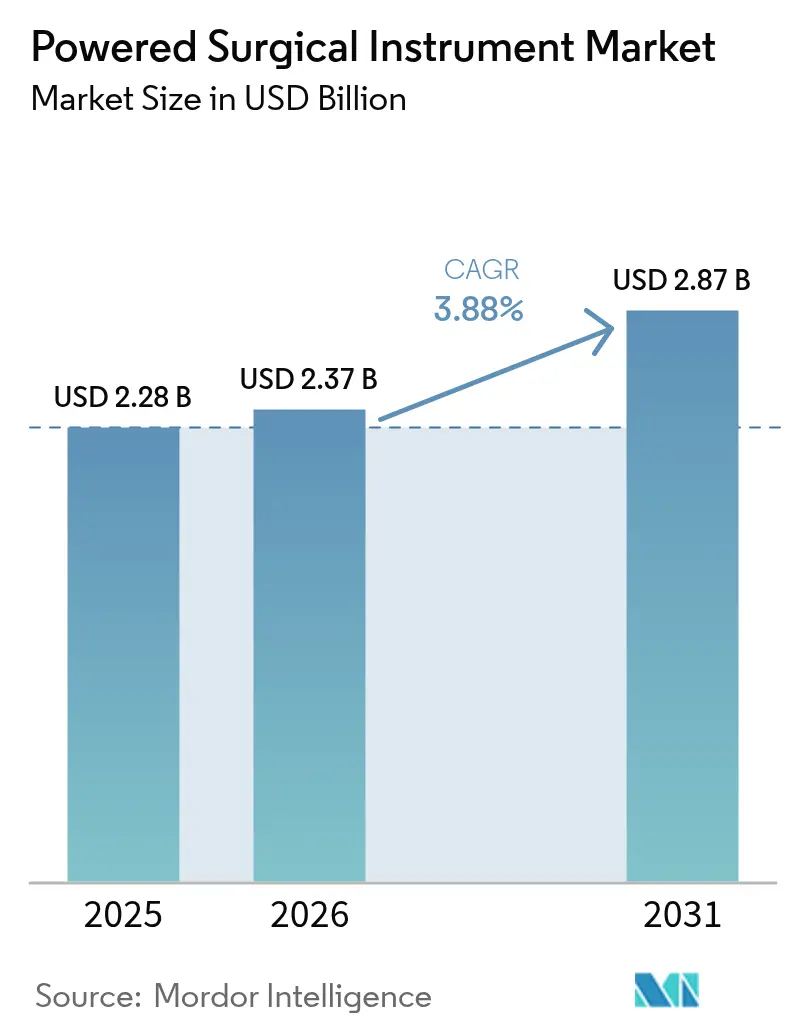

| Market Size (2026) | USD 2.37 Billion |

| Market Size (2031) | USD 2.87 Billion |

| Growth Rate (2026 - 2031) | 3.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Powered Surgical Instrument Market Analysis by Mordor Intelligence

The powered surgical instruments market size is expected to grow from USD 2.28 billion in 2025 to USD 2.37 billion in 2026 and is forecast to reach USD 2.87 billion by 2031 at 3.88% CAGR over 2026-2031. Aging populations, higher surgical volumes, and incremental technological gains sustain growth after the early‐adoption phase. Demand is reinforced by minimally invasive technique preferences, while regulatory moves toward standardized sterilization favor incumbent suppliers. Hospitals also prioritize integrated instrument platforms to satisfy value-based care metrics, supporting premium pricing. Asia-Pacific’s infrastructure build-out and the rise of specialist day-surgery centers underpin a geographic shift that balances North America’s current revenue leadership within the powered surgical instruments market.

Key Report Takeaways

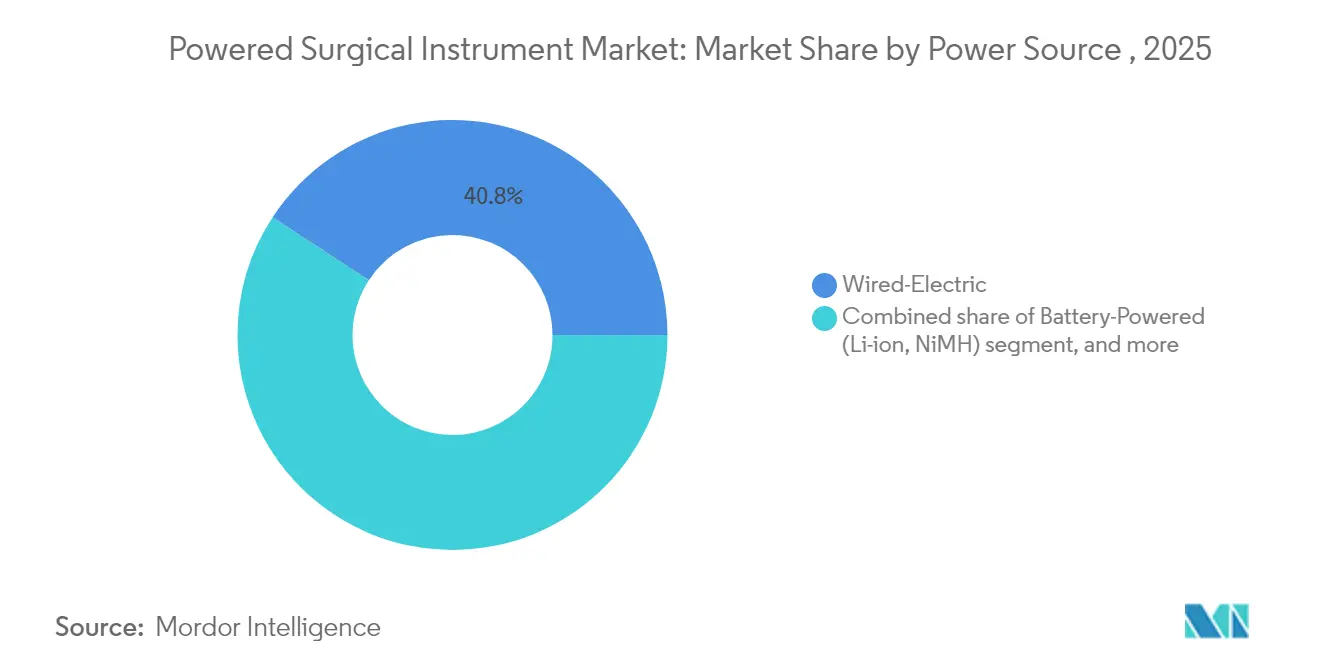

- By power source, wired-electric systems led with 40.78% of powered surgical instruments market share in 2025; battery-powered systems are projected to expand at a 4.72% CAGR through 2031.

- By product type, handpieces accounted for 59.86% share of the powered surgical instruments market size in 2025, while accessories and consumables show the fastest 4.95% CAGR to 2031.

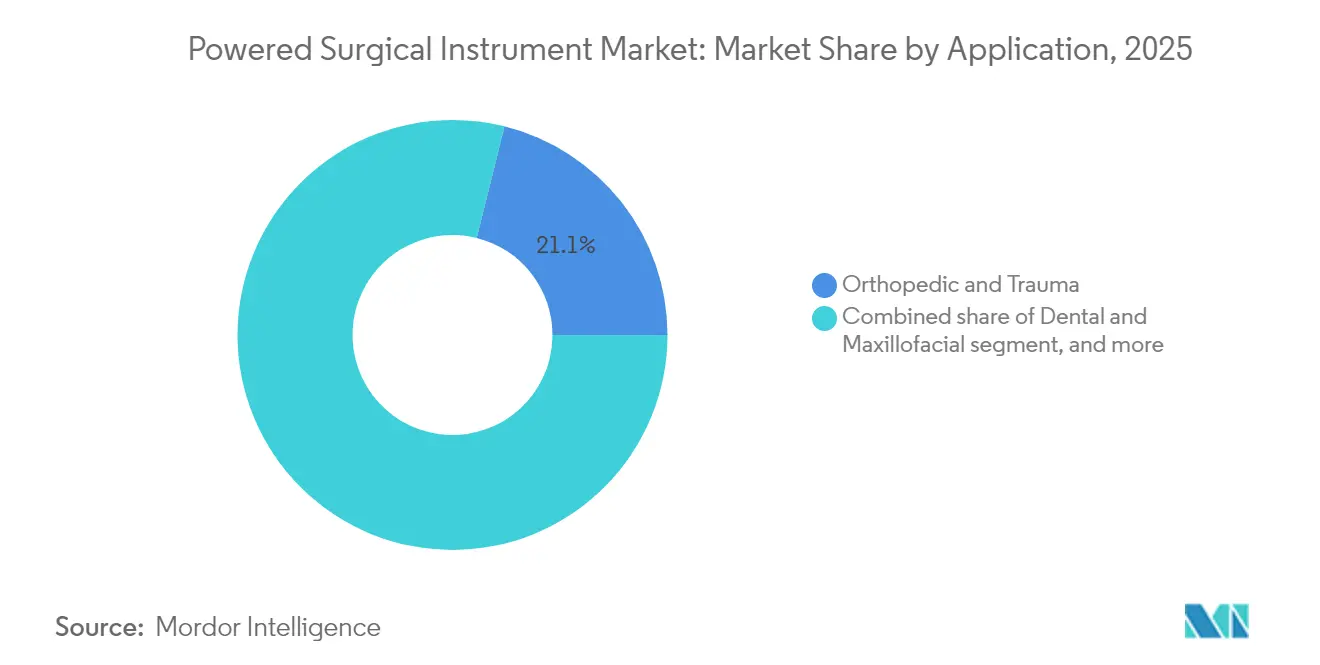

- By application, orthopedic and trauma procedures captured 21.12% share of the powered surgical instruments market size in 2025; plastic and reconstructive surgery is progressing at a 5.96% CAGR.

- By end-user, hospitals held 71.83% of powered surgical instruments market share in 2025, whereas ambulatory surgical centers are set to grow at a 5.63% CAGR.

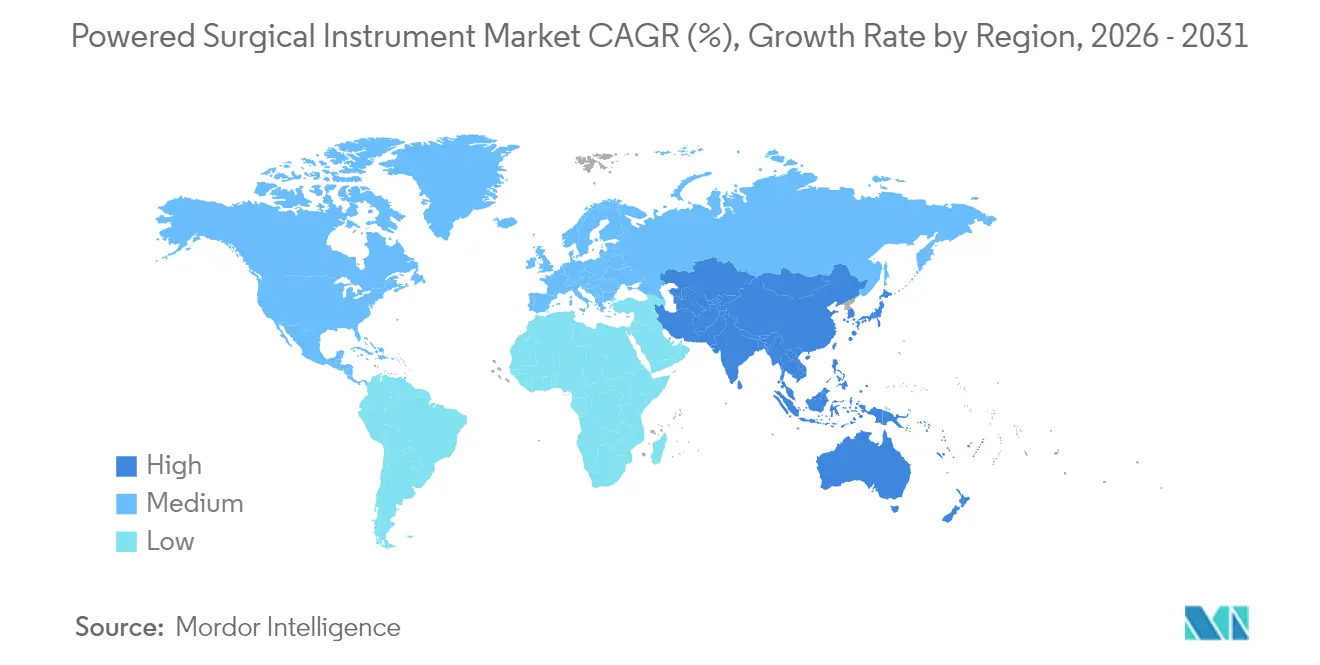

- By geography, North America commanded 35.02% share of the powered surgical instruments market in 2025, yet Asia-Pacific records the fastest 5.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Powered Surgical Instrument Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising volume of surgical procedures and trauma cases | +1.2% | Global, highest in APAC and MEA | Medium term (2-4 years) |

| Growing geriatric population with degenerative disorders | +0.8% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Continuous technological advancements in powered tools | +0.7% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Increasing adoption of minimally invasive and outpatient surgeries | +0.6% | Global, early uptake in developed markets | Medium term (2-4 years) |

| Expansion of specialist day-surgery centers in emerging markets | +0.5% | APAC core, spill-over to MEA & South America | Long term (≥ 4 years) |

| Transition to value-based care driving OR efficiency investments | +0.4% | North America & EU, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Volume of Surgical Procedures and Trauma Cases

Global operating-room activity is rising as insurance coverage broadens in emerging economies and urbanization elevates trauma incidence. Emergency departments rely on power-driven drills and saws to stabilize fractures faster than manual tools, improving outcomes and freeing critical-care beds[1]American College of Surgeons, “Robotic Cholecystectomy Cost Analysis,” facs.org. High-volume centers in Asia-Pacific now integrate hybrid consoles that combine battery and wired modes, shortening turnover time between trauma cases. Traffic accidents and industrial injuries create predictable demand, anchoring the powered surgical instruments market in fast-growing metropolitan regions. Hospitals that treat complex polytrauma increasingly purchase modular handpiece systems to streamline inventory and ensure quick sterilization cycles. Surgeons report shorter operative times, reinforcing administrative support for continued investment in power platforms.

Growing Geriatric Population with Degenerative Disorders

People aged 65 + are the fastest-growing cohort in developed economies, pushing joint-replacement and spinal-fusion volumes upward. These interventions depend on high-torque drills and reamers, securing a long-term revenue base for the powered surgical instruments market. United States reimbursement bundles for hip and knee arthroplasty pressure hospitals to complete procedures efficiently, favoring lightweight battery handpieces that mitigate surgeon fatigue. European day-surgery units now perform same-day hip revisions, leveraging cordless systems to simplify OR setup. Japanese clinics deploy portable consoles to serve rural geriatric patients via mobile surgical teams, widening access. This demographic-linked demand is structural, ensuring a durable sales pipeline for suppliers through 2030 and beyond.

Continuous Technological Advancements in Powered Surgical Tools

Lithium-ion packs now deliver four to six hours of runtime and shed nearly 20% weight versus prior models, improving ergonomics without sacrificing torque. Smart consoles record usage metrics and forecast maintenance needs, enabling predictive service schedules that minimize downtime and extend asset life. Software updates install wirelessly once instruments dock, although hospitals impose cybersecurity protocols to safeguard patient data[2]IEEE, “Future of Surgical Robotics,” ieee.org. Firmware-locked torque settings also aid credentialing by aligning parameters to surgeon preferences. Technology gains allow manufacturers to maintain premium prices, expanding gross margins within the powered surgical instruments market despite procurement scrutiny.

Increasing Adoption of Minimally Invasive and Outpatient Surgeries

Arthroscopic, laparoscopic, and endoscopic approaches shorten recovery and align with payer incentives for shorter stays. Ambulatory surgery centers post mid-single-digit growth as patients choose facilities with shorter check-in to discharge times. Cordless shavers and reciprocating saws designed for 90-minute arthroscopy eliminate tripping hazards in compact ORs. The WALANT technique has popularized office-based hand surgery with power micro-drills that work under local anesthesia, further decentralizing surgical care. Insurers reimburse a growing list of procedures in outpatient settings, feeding demand for portable batteries and sterilizable casings. As a result, suppliers deepen small-footprint console portfolios, reinforcing the powered surgical instruments market in non-hospital environments.

Restraints Impact Analysis of Powered Surgical Instrument Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and maintenance costs of powered instruments | –0.9% | Global, highest in emerging markets | Short term (≤ 2 years) |

| Shortage of skilled surgical workforce in low-income regions | –0.6% | APAC emerging markets, MEA, South America | Long term (≥ 4 years) |

| Stringent regulatory and environmental policies on sterilization and battery disposal | –0.5% | North America & Europe, extending to Japan and Australia | Medium term (2-4 years) |

| Data security concerns with network-connected surgical equipment | –0.3% | Global, with heightened focus in the United States and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs of Powered Instruments

Initial purchase prices range from USD 50,000 to USD 200,000, while annual service contracts typically equal 10-15% of the original spend, challenging budgets of smaller facilities. Studies show robotic cholecystectomy disposables can exceed laparoscopic equivalents without superior outcomes, prompting administrators to question ROI on advanced consoles. Emerging-market clinics often delay upgrades, buying pre-owned wired systems to avoid battery replacement expense. Multiyear leasing models are spreading, yet interest-rate volatility raises financing costs and may temper acquisition plans in the near term. Consequently, capital intensity restrains penetration even as clinical teams voice strong preference for powered solutions.

Shortage of Skilled Surgical Workforce in Low-Income Regions

Many low-income countries operate with surgeon-to-population ratios far below WHO recommendations, limiting procedure volumes irrespective of equipment availability. Training on powered systems demands cadaver labs and virtual simulators that most medical schools lack. Rural hospitals face recruitment struggles as advanced instrumentation remains scarce, perpetuating urban-rural disparities. Where staffing gaps persist, distributors see limited sales potential, slowing powered surgical instruments market expansion. International NGOs provide modular toolkits for mission surgeries, yet these episodic interventions do not create sustained commercial demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Powered Surgical Instrument Market Segment Analysis

By Power Source:

Battery Systems Drive Mobility TrendsLithium-ion battery platforms have propelled the powered surgical instruments market, with battery systems tracking a 4.72% CAGR through 2031. In 2025 wired-electric devices still held 40.78% share, reflecting legacy installations at high-volume centers that value uninterrupted current. Assemblies featuring swappable battery pods cut turnover time in ambulatory suites and gain traction in orthopedic trauma rooms. Hybrid consoles seamlessly transfer from wall power to battery backup during intraoperative repositioning, ensuring sterility of cable-free drapes. Competition now centers on charge-cycle longevity and real-time battery diagnostics that feed into hospital asset software. Over the forecast period, portability advantages keep battery units at the forefront of new installations, especially across Asia-Pacific’s expanding day-surgery grid.

Surgeons cite reduced cord clutter and lighter handpieces as key ergonomic benefits during arthroplasty that may last beyond two hours. Pneumatic platforms retain niche demand in neurosurgery for their ultra-smooth torque delivery, but they lack the connectivity that hospitals expect from digital OR investments. Suppliers therefore integrate Bluetooth firmware updates into battery handles, pairing them with sterilizable charging docks. Price-sensitive hospitals in Latin America still favor wired rigs refurbished through trade-in programs that lower upfront expense. Balanced purchasing across power types keeps the powered surgical instruments market diversified while underscoring battery innovation as an enduring growth lever.

By Product Type:

Consumables Revenue Streams AccelerateHandpieces dominated 59.86% of revenues in 2025, making them the economic cornerstone of the powered surgical instruments market. Saw systems and high-speed drills lead orthopedic demand, while shavers carve share in ENT and sports medicine suites. Meanwhile, accessories and consumables are expanding at a 4.95% CAGR, with single-use burs, blades, and sleeves offering predictable per-case income to manufacturers. Hospitals accept higher variable costs because disposables eliminate re-sterilization labor and align with infection-control audits.

OEMs bundle service contracts with auto‐shipping of blades based on usage data from smart consoles, creating annuity-like revenue. Consumable expansion also smooths earnings against cyclical capital budgets, positioning suppliers to weather macroeconomic swings. Plastic-surgery clinics adopt micro-burring tips for rhinoplasty refinements, illustrating how procedure-specific consumables widen the customer base. Digital ordering portals tied to inventory sensors further lock in clients, reinforcing the powered surgical instruments market through sticky relationships.

By Application:

Plastic Surgery Procedures Accelerate RecoveryOrthopedic and trauma procedures held 21.12% of 2025 revenues, benefiting from rising sports injuries and joint disease in aging societies. Yet plastic and reconstructive surgery is the fastest-moving segment at a 5.96% CAGR as patients resume elective treatments post-pandemic. Power micro-drills and dermal shavers speed cosmetic interventions, supporting outpatient workflows.

Dental and maxillofacial suites leverage slim handpieces to navigate restricted oral fields, while neurosurgery demands torque-controlled micro-saws coupled with navigation sensors. Robotic integrations emerge in cardiothoracic repairs, though uptake is paced by cost. Across all applications the powered surgical instruments market continues to pivot toward cross-specialty platforms that reduce the number of consoles necessary in multi-disciplinary theatres.

By End-User:

Ambulatory Centers Capture Growth PremiumHospitals maintained 71.83% share in 2025, backed by embedded procurement and sterilization capacity. However, ambulatory surgical centers are expanding at 5.63% CAGR thanks to payer incentives and patient convenience. Cordless consoles that fit into compact procedure rooms underpin this shift, while electronic records integration supports rapid scheduling.

Specialty orthopedic clinics deploy high-speed reamers that turn hip revisions into half-day cases, reducing bed needs and readmission risk. Dental surgeries invest in lightweight battery drills to streamline implant workflows. Government trauma units in India pilot battery call-kits that accompany helicopters, illustrating novel field applications. These varied use patterns broaden the powered surgical instruments market across the continuum of care.

Geography Analysis

North America Powered Surgical Instrument Market

North America led with 35.02% revenue share in 2025. Medicare bundles stimulate capital spending on instruments that cut theater time, while United States surgeons adopt smart consoles capable of predictive service diagnostics. Canada’s provincial buying groups favor multi-procedure kits to maximize return under universal budgets, and Mexico’s border hospitals tap the powered surgical instruments market to serve medical tourists.

Europe Powered Surgical Instrument Market

Europe is the second-largest region. Germany, France, and Italy see orthopedic case growth tied to aging citizens, and hospitals adopt value-based contracts that reward shorter length of stay. The United Kingdom aligns purchasing guidelines to NHS cost-per-case thresholds, which puts procurement weight on lifespan analytics from console logs. EU Medical Device Regulation demands robust clinical data that established brands can supply, shielding them against price-led competition while reinforcing patient safety.

APAC Powered Surgical Instrument Market

Asia-Pacific posts the strongest 5.21% CAGR. China’s county hospitals upgrade tool inventories as national insurance expands orthopedic coverage. India’s urban clusters open high-volume day clinics that prefer batterized kits. Japan’s super-aged society sustains steady hip and spine volumes, while South Korea’s cosmetic tourism imports European micro-drills to satisfy foreign patients. ASEAN harmonization has trimmed approval timelines, yet local-content rules spur partnerships between multinationals and regional OEMs. Combined, these dynamics outline a decisive growth vector for the powered surgical instruments market across emerging Asian economies.

Regulatory Landscape

Powered surgical instruments are regulated as medical devices, with market access influenced by quality-system requirements, device classification, and evolving standards for reusable instrumentation and connected equipment. In the United States, FDA oversight covers premarket pathways (including 510(k) for many incremental updates) and manufacturing controls; the FDA Quality Management System Regulation (QMSR) took effect in February 2026, aligning device quality expectations more closely with ISO 13485-style frameworks and increasing compliance focus for global supply chains serving hospitals and ambulatory surgical centers.

In Europe, EU MDR clinical evidence and post-market obligations continue to favor established suppliers with mature technical documentation. In 2026, policy updates introduced tactical pathways for selected device categories, including March 2026, when the European Commission adopted delegated regulations expanding the list of Well-Established Technologies (WET) devices, potentially reducing clinical investigation burdens for eligible technologies. In June 2026, the Commission issued implementing decisions updating harmonised standards under MDR/IVDR, reinforcing the role of conformity to harmonised EN/ISO standards for market access and for reusable instrument verification and testing practices.

Competitive Landscape

Market concentration is moderate, anchored by Stryker, Medtronic, and Johnson & Johnson’s DePuy Synthes, each wielding broad catalogs and dealer networks. These firms compete on battery runtime, ergonomic design, and console analytics. De Soutter Medical and MicroAire pursue niche cranio-maxillofacial segments, capturing clients with tailored service bundles. Asian entrants leverage cost advantage, but stringent sterilization norms temper rapid escalation.

Strategic pivots emphasize platform ecosystems. Johnson & Johnson MedTech collaborates with surgeons worldwide to harmonize outcome classifications, using its Polyphonic digital hub to integrate instrument data and inform performance dashboards. Stryker’s latest console alerts staff when saw blades reach end-of-life cycles, reducing breakage incidents. Partnerships between tool makers and software vendors embed cybersecurity protocols that fulfill hospital IT mandates.

M&A activity continues. Applied Industrial Technologies acquired IRIS Factory Automation in June 2025, adding robotics know-how that can refine assembly of power handpieces. Suppliers also sign manufacturing alliances in India to meet local-content rules, thus expediting tenders. Overall, competitive focus centers on reducing total-procedure cost while bolstering surgeon ergonomics, ensuring the powered surgical instruments market remains technologically vibrant yet commercially disciplined.

Powered Surgical Instrument Industry Leaders

Stryker Corporation

Medtronic plc

Johnson & Johnson (DePuy Synthes)

Zimmer Biomet

B. Braun (Aesculap)

- *Disclaimer: Major Players sorted in no particular order

Powered Surgical Instrument Market Companies Covered in this Report

- Stryker

- Medtronic

- Johnson & Johnson

- Zimmer Biomet

- B. Braun (Aesculap)

- Smiths Group

- Conmed

- De Soutter Medical

- MicroAire

- Adeor Medical

- Panther Healthcare

- Arthrex

- Brasseler USA

- OsteoMed

- MatOrtho

- NSK Nakanishi

- Bien-Air Surgery

- Ruijin Medical

- Arbutus Medical

Market Opportunities and Future Outlook

A whitespace is emerging around platforms that combine traditional powered handpieces with software-defined controls, real-time feedback, and robotic or navigation adjacencies, without requiring facilities to replace existing robotic platforms. In orthopedics, Stryker introduced the Mako Robotic Power System (Mako RPS) as a limited market release in February 2026, framing handheld robotics as a bridge between familiar power-tool workflows and robotic-assisted planning, which aligns with hospital priorities around OR efficiency and standardized execution. In spine and cranial procedures, Medtronic received a CE mark in April 2026 for the Stealth AXiS surgical system integrating planning, navigation, and robotic execution, reinforcing demand for powered tool ecosystems that can connect into broader digital OR infrastructure.

Beyond orthopedic drills and saws, stapling and other energy-adjacent powered systems are broadening the opportunity set, especially where articulation and feedback features address confined anatomies and surgeon preference for actionable intraoperative cues. In April 2026, Johnson and Johnson received CE mark approval for the ETHICON 4000 Surgical Stapler with 3D stapling technology, and Reach Surgical (Genesis MedTech) received CE mark for the iREACH IRIS powered stapler with real-time firing curve feedback and 90-degree articulation. Alongside Olympus receiving FDA 510(k) clearance in April 2026 for the POWERSEAL Open Extended Jaw Sealer/Divider, these launches point to near-term commercialization room for premium disposable interfaces and smart, procedure-specific accessories that complement installed handpiece bases and improve recurring revenue mix.

Recent Industry Developments in Powered Surgical Instrument Market

- April 2026: Olympus received FDA 510(k) clearance for the POWERSEAL Open Extended Jaw Sealer/Divider, enabling integration with powered instrument workflows. The clearance broadens access to energy-assisted sealing across general and specialty surgeries and strengthens Olympus's presence in the instrument ecosystem. This milestone supports a more seamless interface between powered handpieces and procedural software, enhancing intraoperative efficiency.

- June 2025: Johnson and Johnson MedTech launched the KINCISE 2 system, an automated surgical impactor approved for knee and hip revision procedures. By automating impaction steps in high-variability revision cases, the launch supports workflow consistency goals in orthopedic theaters and strengthens ecosystem pull-through for complementary powered tool and implant portfolios.

- August 2024: DePuy Synthes launched the VELYS Active Robotic-Assisted System (VELYS SPINE) for spinal fusion procedures. The platform expands the installed base of navigation and robotics that interfaces with powered instrumentation workflows, accelerating demand for integrated, procedure-ready tool and software combinations in spine surgery.

Powered Surgical Instrument Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the powered surgical instruments market covers revenue from motorized, electrically powered, battery-powered, or pneumatic surgical tools used to cut, drill, ream, staple, shave, or irrigate during procedures, along with the related consoles and consumable attachments that are sold with them.

Scope exclusions: Manual surgical instruments, full robotic surgery platforms, standalone electrosurgical generators, and service or rental revenue are not counted.

Segments Covered in This Report

- By Power Source

- Wired-Electric

- Battery-Powered (Li-ion, NiMH)

- Pneumatic / Nitrogen

- Hybrid Smart Consoles

- By Product Type

- Handpieces

- Drill Systems

- Saw Systems

- Reamer Systems

- Staplers

- Shavers & Debriders

- Other Handpieces

- Power Sources & Controls

- Accessories & Consumables

- Handpieces

- By Application

- Orthopedic & Trauma

- Dental & Maxillofacial

- Neurosurgery & Spine

- Cardiothoracic & Cardiovascular

- Plastic & Reconstructive

- Other Applications

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Orthopedic & Dental Clinics

- Other End-Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the fact base and to make sure our assumptions stay aligned with what is happening in operating rooms and hospital purchasing. We rely on public healthcare statistics and procedure volumes from sources such as the World Health Organization, the US CDC, the OECD, and national health ministries to understand how quickly the surgical pool is changing.

We also use regulatory and product classification references (for example, the US FDA and similar national regulators) to keep product coverage consistent, and we check peer-reviewed clinical literature to understand where powered tools have been adopted in common procedures. Company filings, investor presentations, and credible press releases help us interpret product mix and revenue exposure. Where available, a paid subscription for company financials and patent activity is used selectively for cross-checking. These examples are not exhaustive, and we also referred to other public sources for data collection, validation, and clarification during the research.

Primary Interviews and Surveys

Primary work focuses on validating what is actually purchased and used, then translating that into repeatable market math. We speak with hospital procurement stakeholders, clinicians, sterile processing leaders, and distributors across APAC, EMEA, and the Americas to ground assumptions on replacement cycles, attachment pull-through, and pricing in real buying behavior. When desk inputs conflict, we use follow-up questions to narrow ranges and lock the final model inputs before forecasting.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 16% | APAC: 39% |

| Mid tier: 44% | Functional/Unit leaders: 39% | EMEA: 34% |

| Smaller Players: 20% | Managers: 45% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build using procedure volumes and the share of cases that typically require powered tools, then converts into unit demand by applying tool utilization and replacement patterns. To keep the totals practical, we also run a bottom-up check in parallel. For key tool groups, we multiply sampled average selling prices by estimated unit shipments, then use channel feedback to adjust outliers.

The inputs that drive results most in this market include the mix of orthopedic and trauma procedures, the penetration of powered tools in spine, ENT, and neurosurgery cases, the installed base of consoles and batteries, the average number of attachments used per procedure, and how hospitals manage capital versus disposable budgets. Where country-level procedure volumes are incomplete, we use proxy indicators such as surgery rates per capita and hospital bed capacity, then correct those through interview-led ranges.

For forecasting, we run scenario analysis with a central case supported by expert consensus on procedure growth, elective surgery normalization, and pricing movement for batteries and attachments. Sensitivity checks focus on replacement cycles and attachment pull-through, since small changes in either input can move total market value materially.

Data Validation & Update Cycle

Outputs are checked against independent signals such as procedure trend lines, reported category growth in hospital spending, and observed pricing ranges from buyers and distributors. If a number looks inconsistent, we trace the issue back to a specific input (for example, attachment usage per case), then retest that assumption with targeted callbacks.

Before sign-off, the model and narrative go through multi-step analyst reviews that focus on year-over-year variances, country roll-ups, and currency consistency. The report is refreshed annually, and interim updates are made when there are material events such as regulatory changes, supply disruptions, or major shifts in elective surgery volumes. Right before delivery, we complete a final pass to ensure the dataset reflects the most recent available information.

Mordor Intelligence's Powered Surgical Instruments Market Size Measured Against Other Published Estimates

Published market values for powered surgical instruments can differ even when they appear to cover the same space, mainly because the product basket and the revenue counting point are not consistent across sources. Variations also show up when some estimates lean on older procedure baselines or apply a single global price curve without adjusting for mix.

Standalone electrosurgical generators sit outside Mordor Intelligence's scope, and this one exclusion can reduce totals versus sources that bundle a broader surgical energy spend into the same figure. Additional gaps come from whether accessories and related services are included, whether values are counted at factory-gate or transaction value, and how replacement cycles for consoles, batteries, and attachments are handled across the forecast window.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.37 B (2026) | |

| Global Market Report A | USD 2.36 B (2024) | Uses factory-gate values and states inclusion of related services, which can shift comparability versus transaction-value tool-only models. The year basis is earlier, and accessory and service treatment may not match how consoles, batteries, and attachments are valued in hospital purchasing. |

| Industry Release B | USD 2.60 B (2023) | Often communicated as a high-level press estimate with limited detail on exclusions, and it appears to bundle a wider set of accessories and components. The base year is earlier, and assumptions on procedure growth and pricing are not typically shown for validation. |

Overall, the spread is mainly explained by what is counted as part of the powered tool ecosystem and whether revenues are captured at factory-gate, transaction value, or with services included. By keeping scope items traceable to procedure-linked demand drivers and by checking key inputs with buyers and channel participants, the model stays easier to reproduce and audit from one update cycle to the next.

Key Questions Answered in the Report

What is the current size of the powered surgical instruments market?

The powered surgical instruments market size stands at USD 2.37 billion in 2026 and is projected to reach USD 2.87 billion by 2031.

Which region is growing fastest in the powered surgical instruments market?

Asia-Pacific is expanding at a 5.21% CAGR through 2031, driven by healthcare infrastructure investment and rising day-surgery centers.

Why are battery-powered systems gaining popularity?

Battery platforms offer cord-free mobility, lighter handpieces, and up to six hours of runtime, meeting ergonomic and efficiency goals in ambulatory settings.

Which product category generates the highest recurring revenue?

Accessories and consumables grow fastest at a 4.95% CAGR because single-use blades and burs provide predictable per-procedure income for suppliers.

How do high capital costs affect adoption?

Prices of USD 50,000–200,000 plus annual service contracts deter smaller facilities, especially in emerging markets, slowing market penetration.

What impact will regulatory changes have on new entrants?

Streamlined FDA user-fee negotiations may shorten approval times for incremental updates, yet stringent clinical evidence under EU MDR maintains high entry barriers.

Page last updated on: