Laryngoscope Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

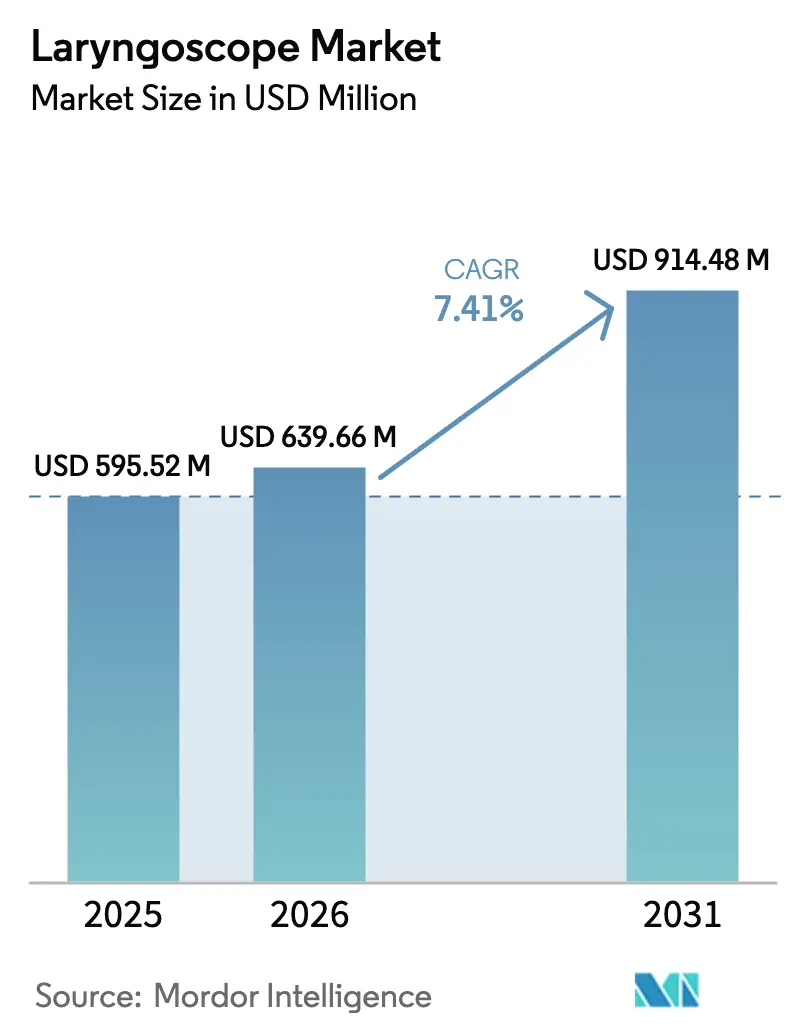

| Market Size (2026) | USD 639.66 Million |

| Market Size (2031) | USD 914.48 Million |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

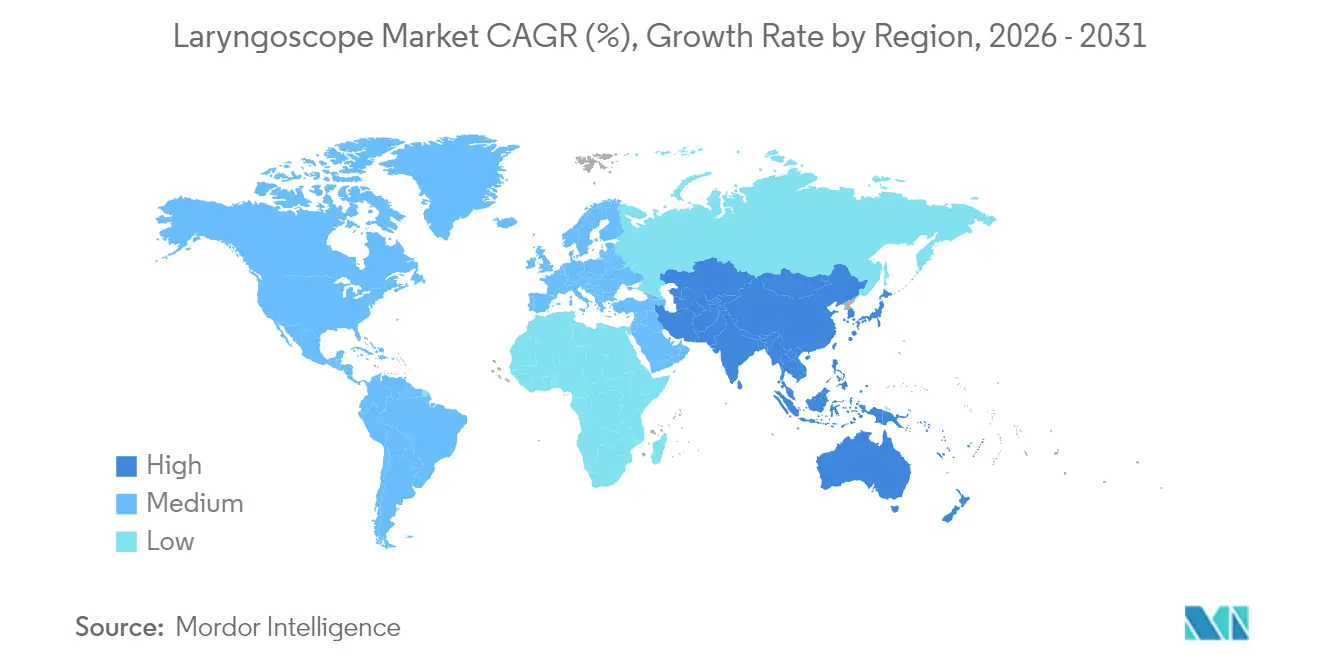

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laryngoscope Market Analysis by Mordor Intelligence

Global laryngoscope market size in 2026 is estimated at USD 639.66 million, growing from 2025 value of USD 595.52 million with 2031 projections showing USD 914.48 million, growing at 7.41% CAGR over 2026-2031. Rising procedure volumes, mandated video-assisted protocols, and AI-enabled guidance systems collectively push demand. Hospitals still dominate purchases, yet ambulatory surgical centers increasingly favor portable single-use units to streamline turnover times. North American clinicians continue to set adoption standards for video-CMOS platforms, but Asia-Pacific health systems now deliver the fastest incremental sales as aging populations swell airway-management caseloads. Supply chain vigilance around CMOS sensors and sterilization capacity remains critical, while environmental scrutiny drives manufacturers toward bio-based disposables and recycling programs.

Key Report Takeaways

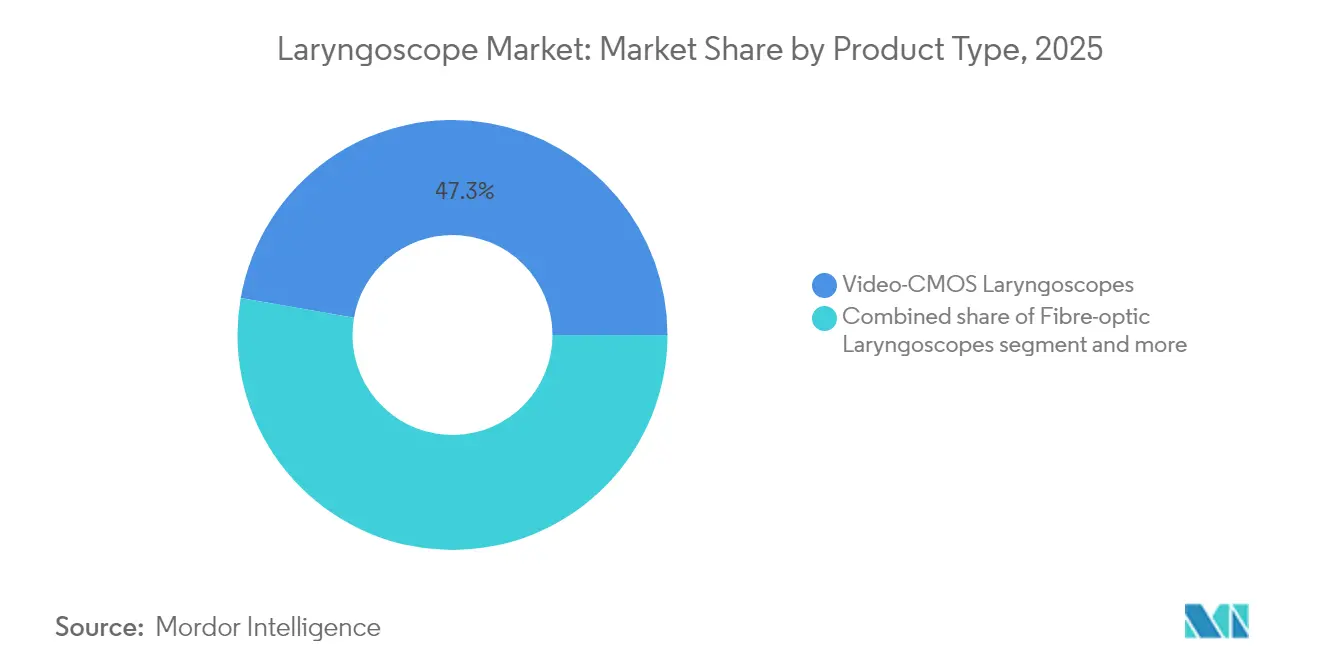

- By product type, video-CMOS laryngoscopes led with 47.25% of laryngoscope market share in 2025 and are forecast to expand at an 8.02% CAGR through 2031.

- By component, blades captured 43.85% share of the laryngoscope market size in 2025, whereas consumables and accessories are advancing at an 8.44% CAGR to 2031.

- By usability, reusable platforms accounted for 59.05% of the laryngoscope market share in 2025; disposable devices are projected to grow at an 8.28% CAGR to 2031.

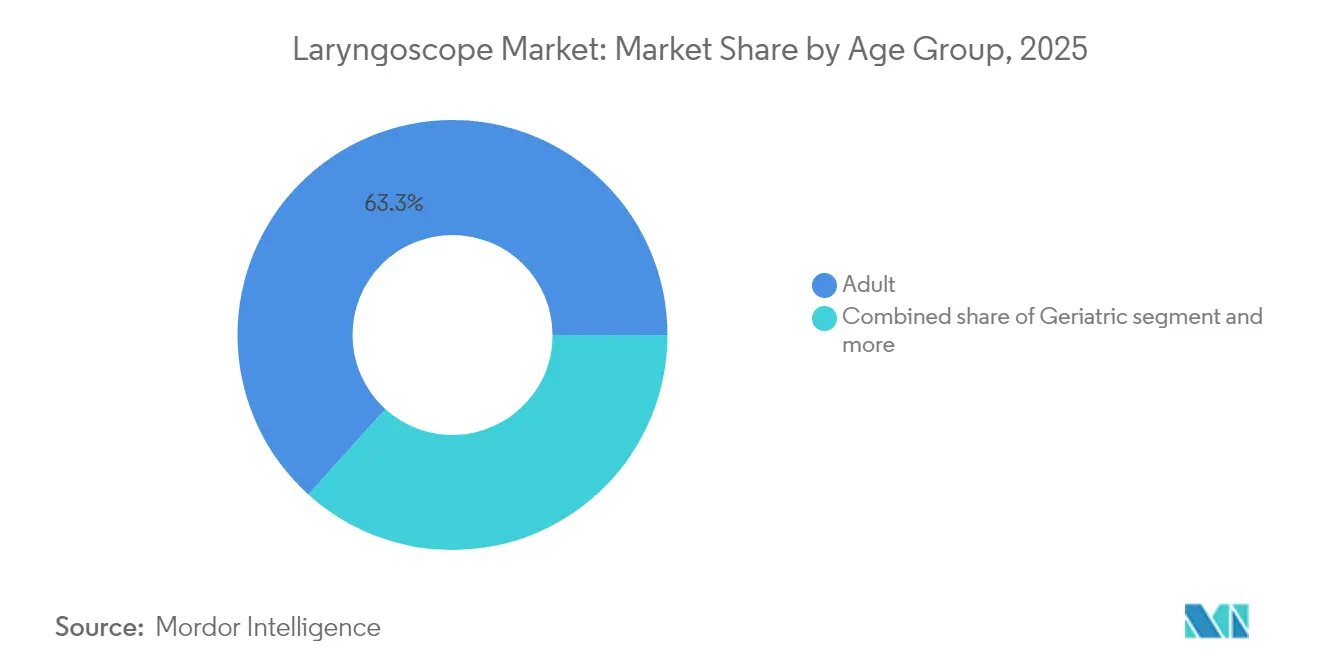

- By age group, adult patients represented 63.30% of laryngoscope market demand in 2025; neonatal and pediatric devices show an 8.20% CAGR through 2031.

- By end user, hospitals held 65.90% of the laryngoscope market size in 2025, whereas ambulatory surgical centers are moving ahead at a 9.07% CAGR to 2031.

- By geography, North America commanded 39.10% of the laryngoscope market size in 2025, whereas Asia-Pacific registers the top regional CAGR of 9.25% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laryngoscope Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of laryngeal disorders & airway-management procedures | +1.8% | Global, amplified in aging societies | Long term (≥ 4 years) |

| Technological advances in video & fiber-optic systems | +2.1% | North America & EU leadership, Asia-Pacific adoption accelerating | Medium term (2-4 years) |

| Shift toward single-use devices for infection control post-COVID-19 | +1.4% | Global, with strict mandates in developed markets | Short term (≤ 2 years) |

| AI-enabled real-time intubation guidance systems | +0.9% | North America & EU early adoption, Asia-Pacific following | Long term (≥ 4 years) |

| Mandatory video protocols in pre-hospital & military care | +0.6% | North America & EU regulatory mandates | Medium term (2-4 years) |

| Expansion of ambulatory surgical centers | +0.7% | North America leading, global diffusion underway | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Laryngeal Disorders & Airway-Management Procedures

Hoarseness after general anesthesia affected 11.77% of 104,720 patients reviewed in 2024, underscoring how common laryngoscopy-based follow-up has become. Direct procedural costs average USD 842 per diagnostic laryngoscopy, and ancillary expenses for consultations and therapy multiply the overall burden. Geriatric populations face higher dysphagia and malignancy risks, pushing clinicians toward early visualization strategies. High-speed videoendoscopy combined with AI now detects organic lesions with 93% accuracy, reshaping diagnostic protocols. These clinical realities sustain long-run demand for both reusable and single-use platforms across inpatient and outpatient settings.

Technological Advances in Video & Fiber-Optic Systems

Video laryngoscopy delivers 74% first-pass success in neonatal cases versus 45% for direct techniques, demonstrating clear performance advantages. Upgraded CMOS sensors bring brighter imaging and lower noise, while quick-connect battery handles cut setup times. Flexible fiber-optic scopes with slim profiles navigate irregular anatomies in ENT and trauma scenarios. Dual-view designs let operators keep traditional sight lines while capturing high-resolution video for documentation and teaching. Real-time AI overlays can mark epiglottis, vocal cords, and tracheal rings, supporting less-experienced practitioners and reducing complications.

Shift Toward Single-Use Devices for Infection Control Post-COVID-19

By 2024, 21.7% of hospitals had switched to disposable blades and 8.7% adopted single-use handles to curb cross-contamination. A life-cycle cost study shows per-use expenses of USD 171.82 for single-use rhinolaryngoscopes compared with USD 238.17 for reusable units when sterilization labor and capital are included. Eliminating reprocessing steps frees staff time and prevents delays in emergency departments and ASCs. Manufacturers now release bio-based plastic laryngoscopes such as Spectrum QC eco, which cuts carbon footprint by 74% while preserving single-use convenience.

AI-Enabled Real-Time Intubation Guidance Systems

Machine-learning models analyze airway images frame by frame, elevating endotracheal tube positioning accuracy from 73.6% to 77.4% and boosting critical misplacement detection to 89.0% . Experimental robotic arms guided by AI navigate through vocal cords autonomously, though mainstream use awaits clearer reimbursement and regulatory pathways. Early adopters report faster decision making in emergency rooms, and teaching hospitals leverage AI overlay recordings for resident education. Combined with high-speed video, stiffness mapping helps differentiate benign from malignant lesions with 83% accuracy, adding oncology value to airway imaging

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device-related airway injuries & postoperative complications | -0.8% | Global, with higher litigation risk in developed markets | Short term (≤ 2 years) |

| High capital & maintenance cost of advanced systems | -1.2% | Emerging markets primarily, cost-sensitive segments | Medium term (2-4 years) |

| Environmental scrutiny on disposable device waste (ESG pressure) | -0.6% | EU & North America regulatory focus | Long term (≥ 4 years) |

| Supply-chain disruptions for CMOS image sensors | -0.9% | Global manufacturing, concentrated in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Device-Related Airway Injuries & Postoperative Complications

Dental trauma, esophageal perforation, and laryngeal swelling continue to generate malpractice exposure. The FDA’s Class I recall of McGrath MAC video laryngoscopes because of battery explosion risk underscores how safety events can disrupt procurement patterns.[1]GlobalData Analysts, “FDA Designates Class I Recall of McGrath Mac Laryngoscopes,” Medical Device Network, medicaldevice-network.com Pediatric intubations carry additional hazards due to narrow airways and limited blade size availability, prompting stricter credentialing and simulation training. Video platforms do mitigate many risks by enhancing glottic visualization, yet equipment failures or misuse still drive litigation and insurance premiums. Hospital risk-management departments therefore weigh safety data heavily when approving capital requests.

High Capital & Maintenance Cost of Advanced Systems

Top-tier video platforms list between USD 15,000 and USD 25,000 while direct laryngoscopes cost USD 200-500. Annual maintenance—sensor calibration, software updates, screen repairs—can add 15% of purchase price. Low-volume rural centers struggle to justify the expense absent targeted funding or lease plans. Utilization-based leasing and pay-per-procedure models have emerged to spread costs, but reimbursement remains static in many markets. The economic calculus often tilts toward single-use blades atop reusable handles as a compromise between safety, affordability, and throughput.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Video-CMOS Dominance Accelerates

Video-CMOS systems held 47.25% of the laryngoscope market share in 2025 thanks to unparalleled visualization and digital integration. First-pass success gains of nearly 30 percentage points over direct techniques win adoption in trauma bays and neonatal ICUs. Direct Macintosh and Miller designs persist in resource-constrained settings for their familiarity and low cost. Fiber-optic scopes address ENT and anticipated difficult airways where flexibility is indispensable.

Video platforms are forecast to grow 8.02% annually to 2031 as health systems codify video intubation into guidelines. As adoption deepens, real-time AI overlays and cloud-based video archiving become standard. Clinicians value the ability to record procedures for quality improvement and medico-legal documentation. Meanwhile, research prototypes that blend rigid optics with embedded augmented-reality cues hint at the next performance leap.

By Component: Blade Innovation Drives Consumables Growth

Blades accounted for 43.85% of the laryngoscope market size in 2025, reflecting their central role and frequent turnover. Metal and polymer edge designs now feature higher-intensity LED lighting and anti-fog coatings. Mac blades dominate adult surgery, while Miller variants are preferred for neonatal airways.

Consumables and accessories show an 8.44% CAGR, propelled by single-use adoption and modular clip-on sensors. Manufacturers pursue recurring revenue through proprietary blade cartridges and disposable light pipes. Hospitals readily approve these expenditures because unit cost is low relative to OR revenue and infection-control benefits are quantifiable.

By Usability: Disposable Momentum Challenges Reusable Economics

Reusable platforms still commanded 59.05% of the laryngoscope market share in 2025 because high-volume centers achieve the lowest cost per use. Stainless steel handles withstand thousands of cycles and interface with a wide blade portfolio.

Disposable models, however, grow at 8.28% annually as COVID-19 shifted infection-risk calculus. Emergency departments appreciate grab-and-go convenience, while ASCs avoid sterilization queues that would slow rapid case turnover. Bio-based plastics and recycling take-back initiatives help reconcile environmental mandates with single-use practicality.

By Age Group: Pediatric Specialization Drives Innovation

Adults generated 63.30% of 2025 revenue, mirroring surgery volumes and emergency callouts. Device selection is broad, from classic Mac blades to dual-view video units.

Neonatal and pediatric segments pace at an 8.20% CAGR because miniaturized optics and gentle curvature blades now achieve 74% first-attempt success versus 45% for direct methods. Color-coded size matrices simplify stocking and reduce errors. Growing recognition of long-term airway trauma in infants encourages early adoption of high-definition video to minimize multiple passes.

By End User: ASC Migration Reshapes Market Dynamics

Hospitals retained 65.90% market control in 2025 through broad procedural scope and capital budgets. Teaching centers standardize on video-CMOS for documentation, resident instruction, and audit trails.

Ambulatory surgical centers expand at 9.07% CAGR, fueled by outpatient procedure migration. Eight of ten U.S. outpatient surgeries now occur in ASCs, and leadership teams prefer compact, portable video units with single-use blades that support fast turnover. Leasing contracts align device costs with fluctuating case volumes.

Geography Analysis

North America held 39.10% of global revenue in 2025. EMS agencies mandate video-laryngoscopy kits on advanced life-support rigs, and hospitals integrate footage into electronic health records. FDA advisories on supply-chain and sterilization resilience shape purchasing decisions.Canada follows similar patterns, while Mexico’s public-hospital modernization drives mid-tier adoption.

Asia-Pacific posts the highest growth at 9.25% CAGR. China funds broad device upgrades, pushing its medical-device market toward USD 210 billion by 2025. Japan’s super-aging society spurs higher per-capita intubation rates. India and Southeast Asia invest in secondary-care networks and medical tourism, prioritizing cost-efficient yet advanced video blades. Reusable-handle plus disposable-blade bundles resonate in these markets.

Europe grows steadily under stringent waste-reduction and infection-prevention directives. Circular-economy regulations accelerate bio-based product rollouts. Germany and France equip ambulance fleets with compact video scopes, while the United Kingdom channels National Health Service funds toward AI-ready platforms. Emerging Central and Eastern European members tap EU cohesion funds to update ENT suites and anesthesia carts.

Competitive Landscape

The laryngoscope market exhibits moderate fragmentation, with leading vendors combining technological edge and strategic acquisitions to fortify positions. Medtronic leverages vertical integration in sensors and batteries to roll out high-lumen video handles that survive autoclave cycles. Ambu, the pioneer in single-use bronchoscopy, extends its model to single-use video laryngoscopes and secures multiyear framework deals with U.S. Veterans Health Administration. KARL STORZ closed its medi-G acquisition in February 2025, bringing precision milling expertise for pediatric blades in-house and widening supply-chain resilience.

Olympus partnered with Proximie in October 2024 to launch a device-agnostic digital-OR platform that streams HD laryngoscope feeds for remote proctoring and AI annotation. Clinicians can overlay guidance cues in real time, shortening learning curves and standardizing technique across multi-site health systems. Safety events intensify rivalry: the FDA’s Class I recall of McGrath MAC in September 2024 for battery explosion risk prompted rapid substitution by competitors touting safer lithium-iron-phosphate chemistries, and several systems won emergency procurement contracts as replacements.

Emerging disruptors attack sustainability and niche clinical gaps. Verathon introduced the Spectrum QC eco made from 80% bio-based plastic, claiming a 74% carbon-footprint cut without compromising rigidity or optical clarity. Start-ups such as Bath-based InovScope prototype 3-D-printed modular blades allowing custom curvature for cranio-facial anomalies, while Seoul’s Airmate integrates AI that predicts tube size based on live vocal-fold measurements. White-space opportunities surface in pediatric and military protocols, where blade miniaturization, ruggedization, and EMI-shielded electronics meet specialized standards. Regulators elevate cybersecurity requirements, compelling vendors to embed encryption chips that guard recorded airway videos. Collectively, these forces ensure that competitive dynamics hinge not only on optical performance but also on life-cycle sustainability, software sophistication, and post-sale training that clinicians now expect from partners in the evolving laryngoscope market.

Laryngoscope Industry Leaders

Medtronic plc

Olympus Corporation

Teleflex Incorporated

Baxter (Hill-Rom Co., Inc.)

Nihon Kohden Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: KARL STORZ completed the acquisition of medi-G to enhance production capabilities in Meßkirch, Germany, strengthening supply chain stability for surgical products including ENT and pediatric laryngoscopes.

- November 2024: Verathon introduced additional sustainable single-use variants that integrate recyclable packaging to address environmental mandates.

- October 2024: Verathon launched Spectrum QC eco, the first single-use video laryngoscope made with 80% bio-based plastics, cutting carbon footprint by 74% while retaining single-use efficiency.

- September 2024: The FDA issued a Class I recall for McGrath MAC laryngoscopes because of potential explosion risks, prompting device replacement programs across U.S. hospitals.

Global Laryngoscope Market Report Scope

Laryngoscopes are endoscopy devices used for visualization of the vocal cords and placement of the endotracheal tube into the trachea. Laryngoscopy is the procedure that healthcare providers use to examine the larynx. Providers may do laryngoscopies in a clinic office or as surgery in an operating room.

The Laryngoscope Market is Segmented by Type (Fiber Optic Laryngoscope, Video Laryngoscope), Component (Laryngoscope Blades, Handles, Consumables and Accessories), Usability (Disposable, Reusable), End-User (Hospital, Clinics, Ambulatory Surgical Centers, Other End-Users), and Geography (North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East and Africa (GCC, South Africa, Rest of Middle East and Africa), and South America (Brazil, Argentina, Rest of South America). The report offers the value (in USD million) for the above segments.

| Direct (Macintosh / Miller) Laryngoscopes |

| Fibre-optic Laryngoscopes |

| Video-CMOS Laryngoscopes |

| Rigid Indirect & Others |

| Blades | Mac Blades |

| Miller Blades | |

| Handles | |

| Consumables & Accessories |

| Disposable |

| Reusable |

| Neonatal & Pediatric |

| Adult |

| Geriatric |

| Hospitals |

| Clinics |

| Ambulatory Surgical Centres (ASCs) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Direct (Macintosh / Miller) Laryngoscopes | |

| Fibre-optic Laryngoscopes | ||

| Video-CMOS Laryngoscopes | ||

| Rigid Indirect & Others | ||

| By Component | Blades | Mac Blades |

| Miller Blades | ||

| Handles | ||

| Consumables & Accessories | ||

| By Usability | Disposable | |

| Reusable | ||

| By Age Group | Neonatal & Pediatric | |

| Adult | ||

| Geriatric | ||

| By End User | Hospitals | |

| Clinics | ||

| Ambulatory Surgical Centres (ASCs) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the laryngoscope market expected to grow between 2026 and 2031?

It is forecast to rise from USD 639.66 million in 2026 to USD 914.48 million in 2031, a 7.41% CAGR.

Which product type holds the largest share today?

Video-CMOS laryngoscopes lead with 47.25% laryngoscope market share in 2025.

Which region is expanding the fastest?

Asia-Pacific records a 9.25% CAGR through 2031 thanks to infrastructure investment and aging demographics.

What is driving adoption in ambulatory surgical centers?

Outpatient procedure migration favors portable single-use video scopes that cut sterilization delays and align with ASC throughput goals.

Page last updated on: