Ophthalmic Handheld Surgical Instruments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

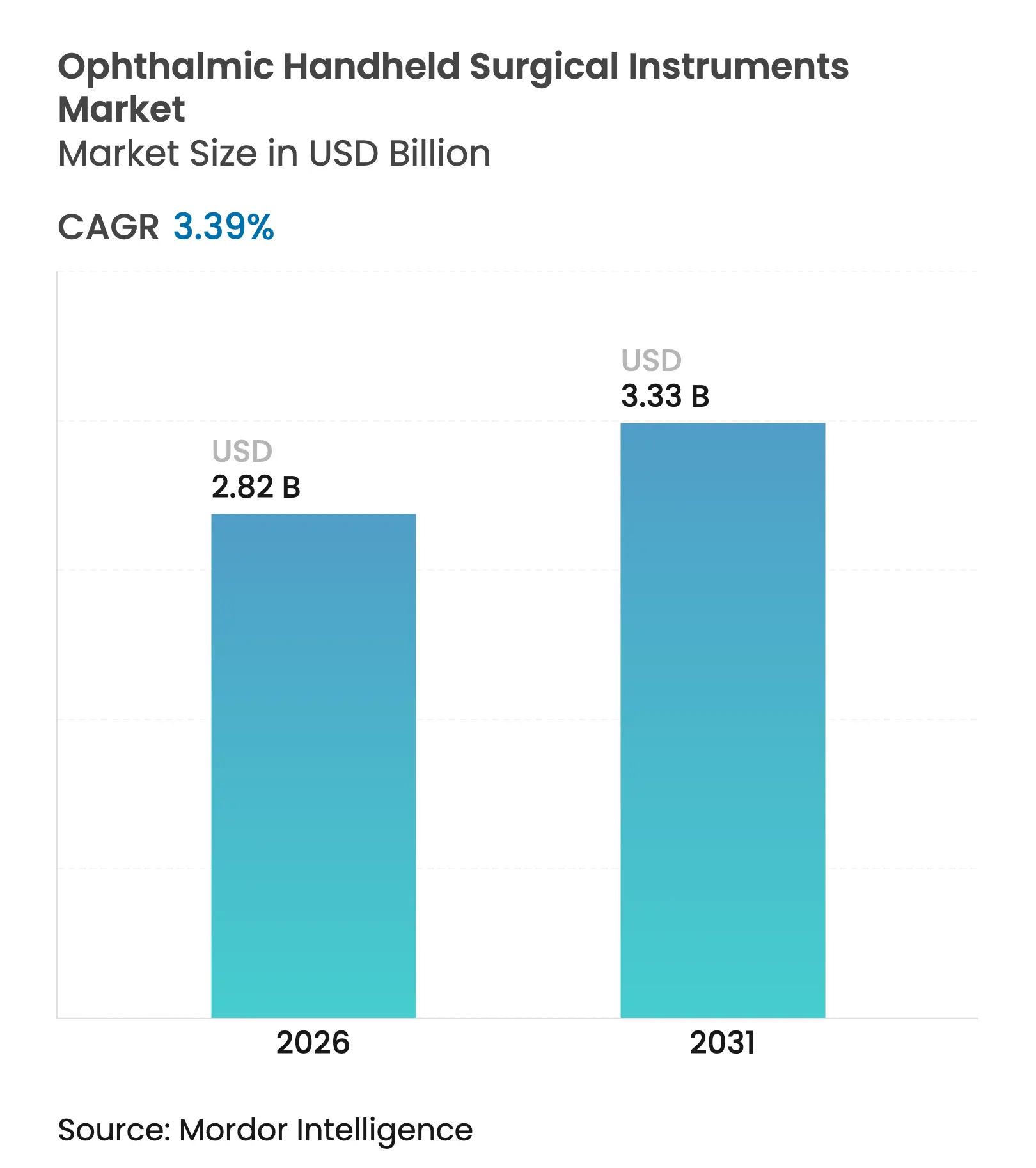

| Market Size (2026) | USD 2.82 Billion |

| Market Size (2031) | USD 3.33 Billion |

| Growth Rate (2026 - 2031) | 3.39 % CAGR |

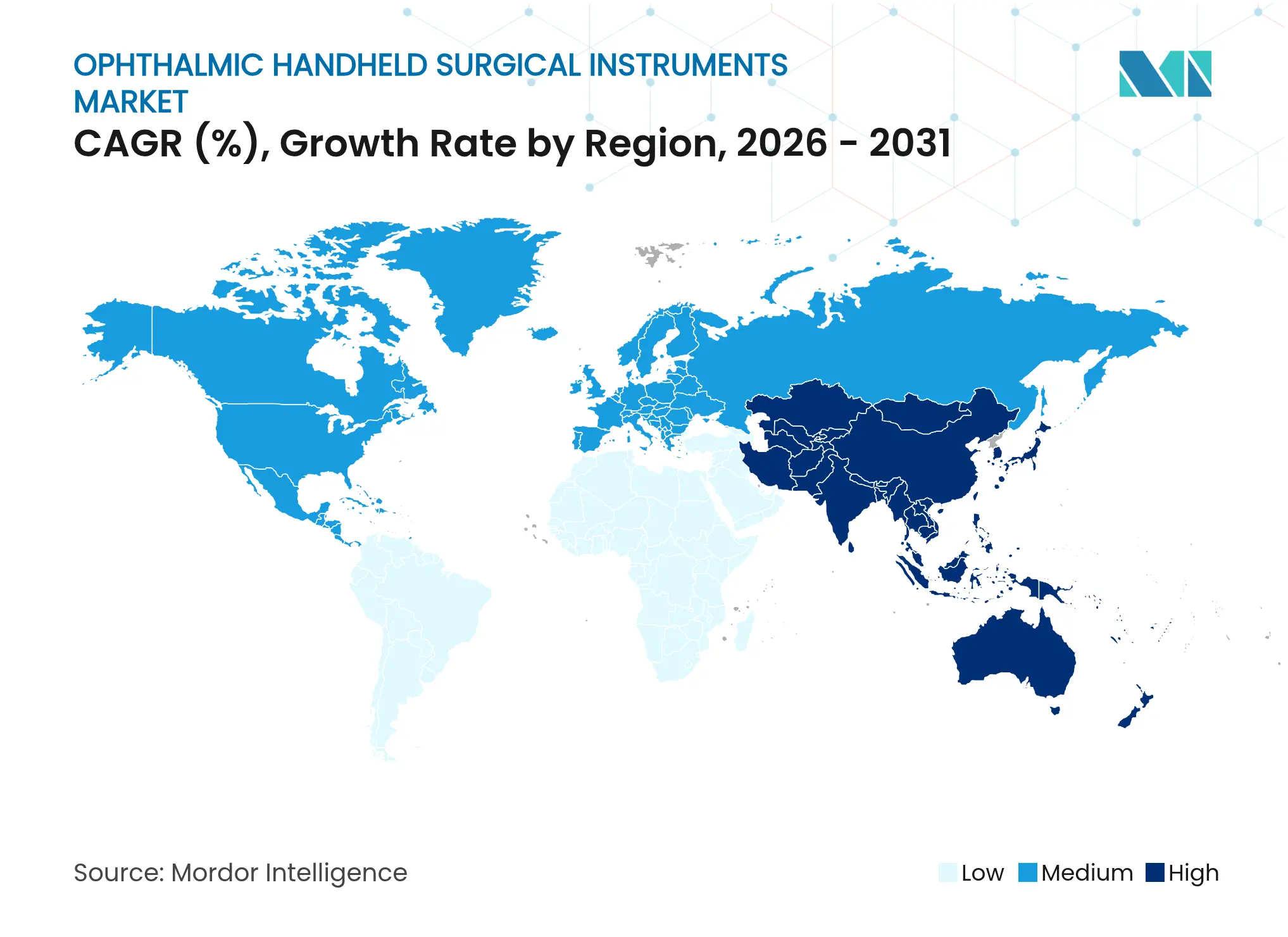

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Ophthalmic Handheld Surgical Instruments Market Analysis by Mordor Intelligence

The ophthalmic handheld surgical instruments market size is expected to grow from USD 2.73 billion in 2025 to USD 2.82 billion in 2026 and is forecast to reach USD 3.33 billion by 2031 at 3.39% CAGR over 2026-2031. Procedure-linked demand tied to cataract and glaucoma surgery, steady reimbursement for minimally invasive techniques, and the worldwide shift toward single-use packs combine to keep growth predictable even as the installed base matures. Facility managers increasingly view handheld instruments as throughput enablers, valuing chairside-ready knife kits that trim turnaround minutes. Manufacturers respond with localized production hubs, hedging currency swings while aligning price-performance mixes to regional budgets. The sales mix continues to tilt toward disposables in high-volume ambulatory surgical centers (ASCs), a setting where sterilization delays erode revenue per operating-room minute. Market leaders now court loyalty by offering modular handle-tip architectures that let surgeons swap ends without re-priming fluidics lines, preserving sterility while protecting productivity.

Key Report Takeaways

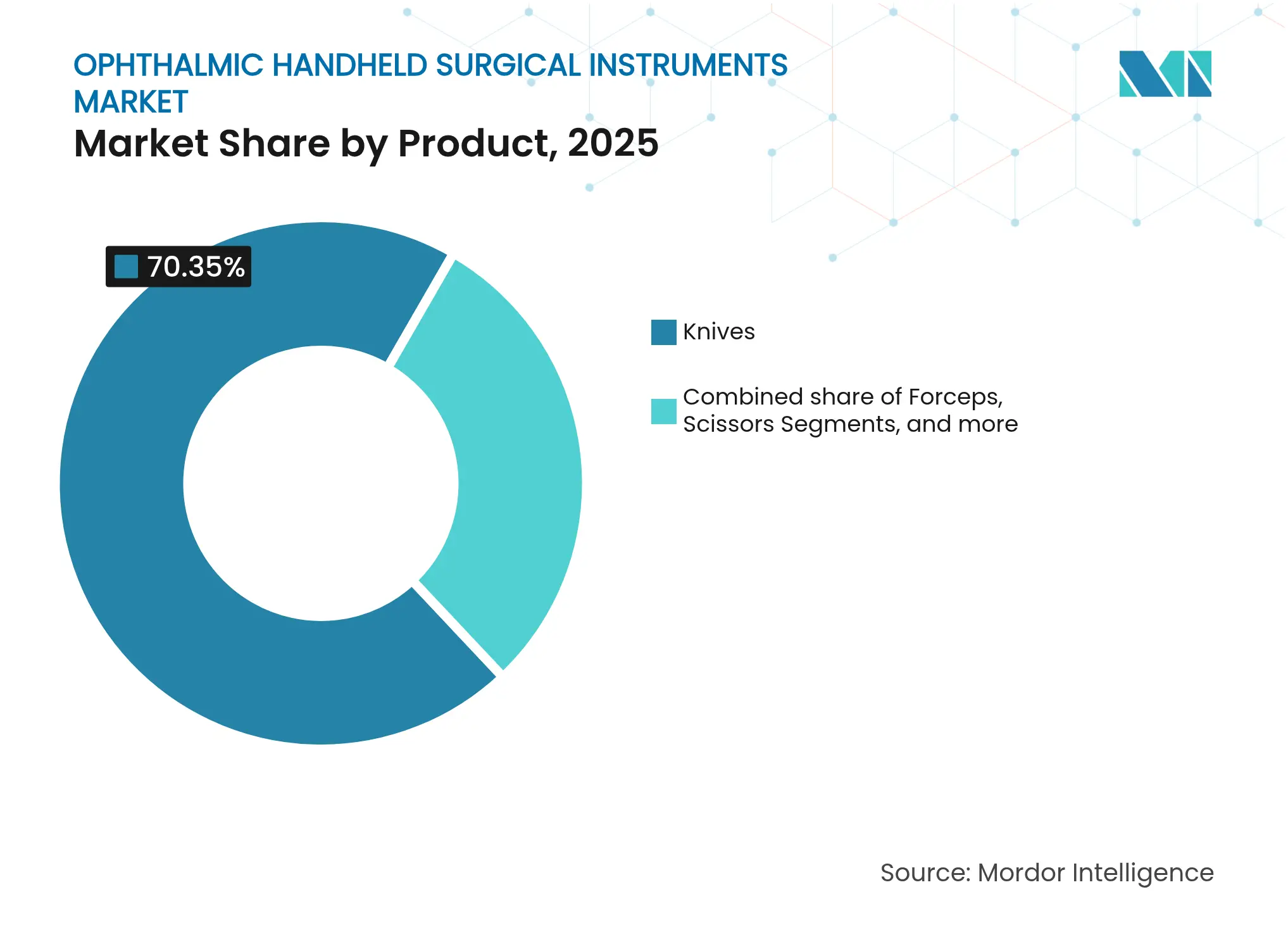

- By product, ophthalmic knives led with 70.35% ophthalmic handheld surgical instruments market share in 2025. Scissors recorded the fastest 3.45% CAGR through 2031.

- By usability, reusable sets accounted for 61.48% of the ophthalmic handheld surgical instruments market size in 2025. Single-use counterparts delivered the highest 5.24% CAGR through 2031.

- By material, stainless-steel captured 54.62% share of the ophthalmic handheld surgical instruments market size in 2025. Titanium is advancing at a 4.88% CAGR between 2026-2031.

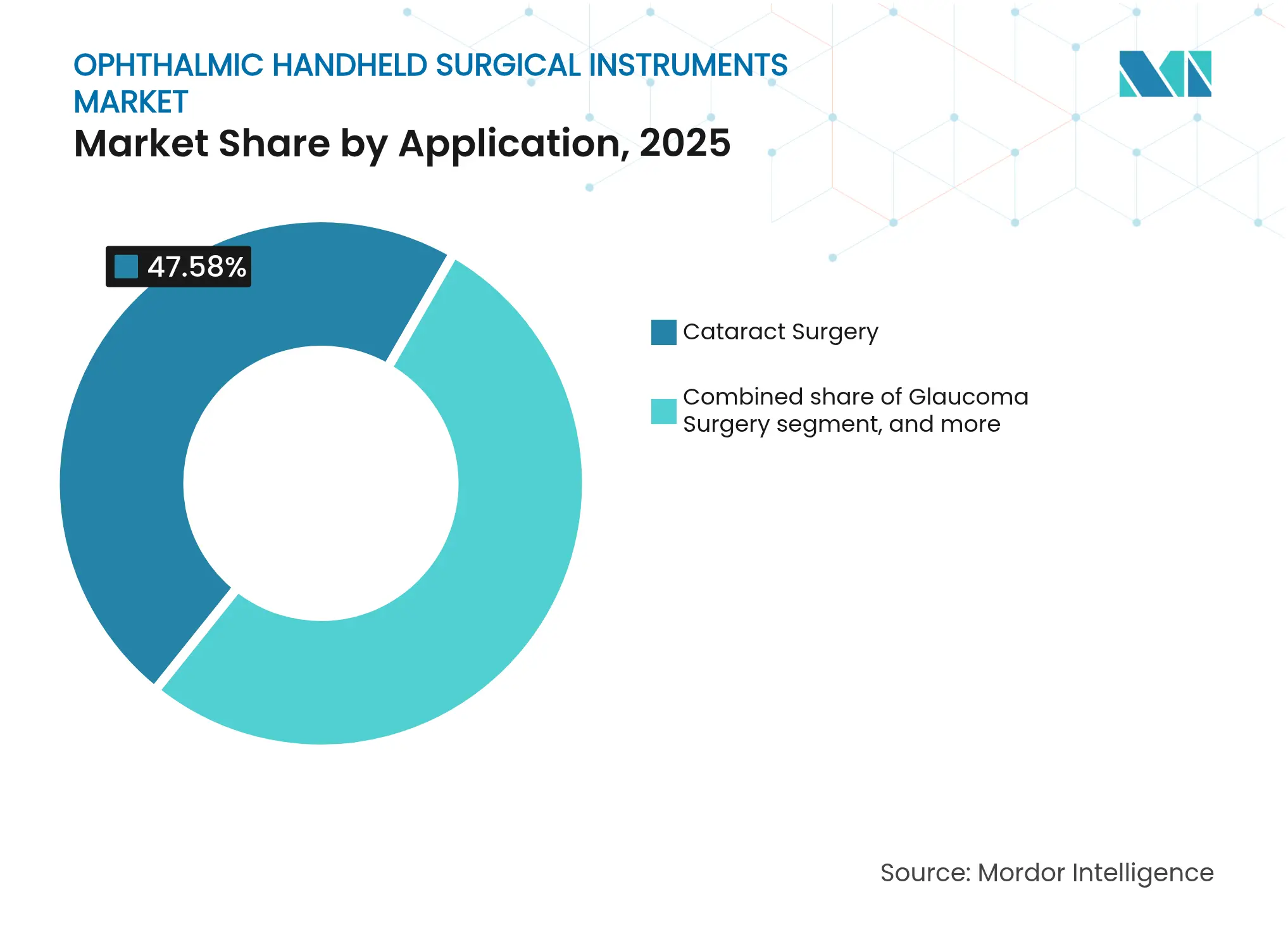

- By application, cataract surgery contributed 47.58% share of the Ophthalmic Handheld Surgical Instruments market size in 2025. Refractive surgery is forecast to expand at a 4.56% CAGR to 2031.

- By end-user, hospitals retained 56.63% Ophthalmic Handheld Surgical Instruments market share in 2025. Ophthalmic specialty clinics posted the quickest 4.62% CAGR through 2031.

- By geography, North America contributed 41.92% share of the ophthalmic handheld surgical instruments market size in 2025. Refractive surgery is forecast to expand at a 4.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ophthalmic Handheld Surgical Instruments Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Global surge in cataract & glaucoma surgical volumes driven by aging demographics Global surge in cataract & glaucoma surgical volumes driven by aging demographics | +0.8% | Global | Long term (≥ 4 years) | % Impact on CAGR Forecast:+0.8% | Geographic Relevance:Global | Impact Timeline:Long term (≥ 4 years) |

Shift toward ambulatory & minimally invasive ophthalmic procedures requiring precision hand tools Shift toward ambulatory & minimally invasive ophthalmic procedures requiring precision hand tools | +0.6% | North America, Europe | Short term (≤ 2 years) | |||

Rising adoption of premium IOLs & refractive corrections fueling demand for micro-incision instruments Rising adoption of premium IOLs & refractive corrections fueling demand for micro-incision instruments | +0.5% | Global | Medium term (2-4 years) | |||

Expansion of vision-health coverage & reimbursement policies supporting instrument upgrades Expansion of vision-health coverage & reimbursement policies supporting instrument upgrades | +0.3% | North America, Asia-Pacific | Medium term (2-4 years) | |||

Growing investments in ophthalmic centers of excellence across emerging markets Growing investments in ophthalmic centers of excellence across emerging markets | +0.4% | Asia-Pacific, Latin America | Long term (≥ 4 years) | |||

Technological innovations in ergonomic & titanium instrument design enhancing surgical efficiency Technological innovations in ergonomic & titanium instrument design enhancing surgical efficiency | +0.5% | Global | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Global Surge in Cataract and Glaucoma Surgical Volumes

Annual cataract procedures are edging toward the mid-thirty-million range worldwide, guaranteeing a stable, procedure-linked revenue foundation for the Ophthalmic Handheld Surgical Instruments market[1]American Academy of Ophthalmology, “Patient-Reported Outcome Measures in Cataract Surgery,” aao.org. Surgeons increasingly combine cataract extraction with glaucoma interventions, boosting demand for multi-purpose knives that support smaller corneal incisions and goniotomy blades that traverse Schlemm’s canal. The United States Food and Drug Administration reclassified ultrasound cyclodestructive devices from Class III to Class II, trimming regulatory friction and spurring next-generation glaucoma-instrument innovation. Regulatory easing effectively behaves like an indirect R&D subsidy for smaller device makers, allowing specialty micro-tools to reach market faster. As procedure complexity grows, facilities emphasize disposable packs to avoid schedule disruptions, reinforcing annuity-style revenues for suppliers positioned at high-volume centers.

Shift toward Ambulatory and Minimally Invasive Procedures

ASCs now conduct nearly 20% of all U.S. outpatient surgeries, with cataract interventions leading the tally. Facility economics reward single-use, ergonomic handpieces that let teams flip rooms quickly without waiting for sterilizers to cool. MIGS volumes keep climbing under expanded Medicare coverage for trabecular stents, driving demand for ultra-narrow-gauge blades able to navigate sub-2 mm entries. Vendors that lock in ASC muscle memory early build durable consumption funnels, because workflow habituation discourages brand switching. Modular handle-tip designs further strengthen loyalty by letting surgeons swap ends intra-case while keeping lines closed. As a result, throughput gains eclipse upfront price when purchasing committees evaluate instrument trays.

Rising Adoption of Premium IOLs and Refractive Corrections

Advanced-technology lenses command higher reimbursements and necessitate blades capable of self-sealing micro-incisions that minimize surgically induced astigmatism. The FDA’s qualification of the Assessment of IntraOcular Lens Implant Symptoms tool (AIOLIS) formalizes patient-reported metrics, tightening feedback loops between lens optics and incision quality[2]Food and Drug Administration, “De Novo Classification of Ultrasound Cyclodestructive Devices,” fda.gov. Refractive lens exchange among middle-aged patients unwilling to wait for cataracts is growing, prompting surgeons to standardize tray contents around small-incision sizes. Entire micro-ecosystems of choppers, phaco tips, and forceps cluster around these incision dimensions, ensuring that a premium IOL decision often cascades into ancillary tool purchases. Instrument suppliers thus benefit from higher average selling prices linked to refractive procedures.

Expansion of Vision Health Coverage and Reimbursement

Broader public and private insurance coverage for MIGS add-on codes and select premium cataract options gives hospitals budget headroom to adopt higher-specification hand instruments. Medicare Local Coverage Determinations now reimburse standalone trabecular stent implantation, legitimizing investment in niche ab-interno blades previously held back by payback uncertainty[3]MedPAC, “Report to the Congress: Medicare Payment Policy,” medpac.gov. Private insurers often split reimbursements, paying fully for the surgical act while leaving lenses partially out-of-pocket, nudging OR managers toward versatile tools able to serve both standard and premium workflows. Reimbursement coding is thus dictating instrument form factors: hospitals increasingly favor devices that streamline billing submissions without forcing tray swaps.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Intensifying price pressure from generic low-cost manufacturers reducing ASPs Intensifying price pressure from generic low-cost manufacturers reducing ASPs | -0.5% | Asia-Pacific, Latin America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.5% | Geographic Relevance:Asia-Pacific, Latin America | Impact Timeline:Medium term (2-4 years) |

Sterilization compliance costs & delays curtailing reusable instrument utilization Sterilization compliance costs & delays curtailing reusable instrument utilization | -0.4% | Global | Short term (≤ 2 years) | |||

Slow regulatory approvals for novel ophthalmic instruments hindering time-to-market Slow regulatory approvals for novel ophthalmic instruments hindering time-to-market | -0.3% | Europe | Medium term (2-4 years) | |||

Supply-chain vulnerabilities in specialty-grade metals affecting production lead times Supply-chain vulnerabilities in specialty-grade metals affecting production lead times | -0.2% | Global | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Intensifying Price Pressure from Low-Cost Entrants

Manufacturers based in India, China, and Pakistan continue to compress average selling prices in stainless-steel commodity lines, eroding margins for incumbents. Larger brands respond by shifting portfolios toward titanium alloys, diamond-like carbon coatings, and subscription-bundled trays that couple hardware with sharpening services. Competitive differentiation is migrating from raw materials to service wraps such as predictive maintenance portals and RFID-enabled inventory tracking, solutions that are harder for low-cost rivals to copy. Western suppliers now emphasize documented edge-retention metrics and lifecycle economics when defending pricing during tenders.

Sterilization Compliance Costs Curtailing Reusable Adoption

Tighter decontamination standards have lengthened sterilization cycles and added documentation burdens, quietly swelling per-procedure overhead for reusable instrument sets. ASCs running 15+ cataract cases per room report that waiting for cooled, re-sterilized choppers costs billable minutes that cannot be recovered. Disposable packs, though higher in direct cost, eliminate those bottlenecks and increasingly include recyclable components to address sustainability objections. Hospitals piloting take-back programs for spent titanium blades find value-analysis committees more willing to approve single-use kits when environmental stewardship boxes are ticked.

Segment Analysis

By Product: Knives Anchor Revenue, Scissors Lead Growth

Ophthalmic knives generated 70.35% Ophthalmic Handheld Surgical Instruments market share in 2025, underscoring their irreplaceable role in reproducible corneal and scleral incisions. Even minute deviations in blade geometry can shift postoperative visual acuity, justifying premium pricing and a high replacement cadence. As facilities push for faster turnover, single-use keratomes with integrated depth guards gain traction, further enlarging the revenue pool tied to knives.

Scissors, although contributing a smaller slice today, are projected to post the highest 3.45% CAGR through 2031. Titanium metallurgy now yields lighter yet sturdier micro-scissors that improve surgeon ergonomics during capsulotomy and epiretinal membrane peeling. Their expanding utility from anterior to posterior segment work signals that blade science rather than pure volume will drive future share gains in this category. The Ophthalmic Handheld Surgical Instruments market therefore rewards continuous metallurgy innovation that translates into tactile advantages at the surgical field.

Forceps maintain a mid-teens share by serving multiple steps such as nucleus manipulation and epiretinal membrane removal. Cannulas capture growth from intravitreal injection volumes that keep climbing with new gene therapies. Speculums, though mature, benefit from nanotechnology coatings that reduce surgical-field fogging and improve patient comfort. As surface-science advances, even legacy products secure upsell opportunities, reinforcing the notion that no segment is fully commoditized.

Note: Segment shares of all individual segments available upon report purchase

By Usability: Reusable Entrenchment Meets Disposable Momentum

Reusable sets captured 61.48% of the Ophthalmic Handheld Surgical Instruments market size in 2025 thanks to existing hospital sterilization infrastructure and amortized capital. However, single-use packs are racing ahead at a 5.24% CAGR as ASCs favor chairside-ready kits that shave several minutes off room turnover. In volume-driven cataract lists, that time saving equates directly to incremental daily cases, a metric executives track closely.

Lifecycle assessments reveal that the energy and water footprint of modern sterilization units can rival the cradle-to-grave impact of recyclable disposables. Manufacturers therefore explore plant-based polymers and titanium take-back schemes to neutralize environmental critiques. The debate is evolving from reusable vs single-use to which format delivers the best blend of sterility assurance, throughput, and sustainability.

By Material: Stainless-Steel Dominance Faces Titanium Up-Swing

Stainless-steel retained 54.62% Ophthalmic Handheld Surgical Instruments market share in 2025 because its balance of hardness, corrosion resistance, and affordable pricing suits high-volume blades. Even so, titanium is expanding at a 4.88% CAGR as surgeons seek reduced hand fatigue and MRI-compatibility in multi-disciplinary theaters. Its biocompatibility profile also attracts premium reimbursement codes in some European tenders, helping offset higher material costs.

Cobalt-chrome alloys are resurging in retinal picks where elastic modulus matters for membrane peeling. Polymer composites occupy a niche for insulated diathermy tips, while breakthroughs in bio-ceramic coatings on titanium foreshadow hybrid tools that combine metal strength with ceramic edge retention. Incremental surface-science wins will likely open mini-premium tiers even within established material lines, suggesting that differentiation remains feasible without wholesale platform shifts.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Application: Cataract Commands Volume, Refractive Sets Pace

Cataract surgery delivered 47.58% of the Ophthalmic Handheld Surgical Instruments market size in 2025, reinforcing its status as the bedrock revenue stream. Procedure counts rise in most economies regardless of macro-cycles, protecting this segment from volatility. Refractive surgery, while smaller in volume, is projected to compound at 4.56% through 2031 and lifts average selling prices because laser-assisted lens exchange needs ultra-thin knives and choppers.

Glaucoma adjunct procedures during cataract extraction spur demand for dual-purpose blades, while retinal surgery, though lower in count, yields the highest revenue per tray due to intricate one-time-use picks and sub-30-gauge micro-scissors. The pipeline of presbyopia-correcting inlays and cell-therapy delivery cannulas ensures that every clinical frontier spawns a new handheld tool, locking in innovation momentum for the long haul.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Hospitals Dominate, Specialty Clinics Accelerate

Hospitals accounted for 56.63% Ophthalmic Handheld Surgical Instruments market share in 2025, aided by their capacity to manage complex cases and absorb sterilization capital. Value-analysis committees increasingly evaluate total-cost-in-use, including sterile processing labor, nudging procurement toward instruments that minimize rework. University-affiliated centers remain early adopters, shaping brand preferences that cascade into community settings.

Ophthalmic specialty clinics logged the fastest 4.62% CAGR by embracing focused care models that rely heavily on turnkey disposable kits, freeing them from central sterile bottlenecks. Office-based intravitreal suites represent a micro-segment whose disposable-heavy cycles may presage office-based anterior procedures once regulators finalize safety frameworks. Ambulatory centers unaffiliated with eye care hold a smaller but reliable slice, absorbing overflow cataract lists from hospital systems under capacity strain.

Geography Analysis

North America retained 41.92% Ophthalmic Handheld Surgical Instruments market share in 2025, underpinned by dense procedure volumes and a reimbursement climate that rewards technology upgrades linked to documented workflow gains. Medicare coverage for combined cataract-MIGS operations accelerates procurement of micro-goniotomy knives, while malpractice-liability sensitivity drives demand for instruments with robust human-factors validation. ASCs capture a growing share of cataract volumes, prompting suppliers to develop ASC-centric packaging that saves set-up time.

Asia Pacific registers the fastest 4.86% CAGR as demographic expansion, urban middle-class growth, and cataract backlog-reduction programs converge. China’s tier-three municipal hospitals and India’s state-sponsored camps absorb cost-optimized stainless-steel sets, whereas premium titanium blades find buyers in urban centers courting medical tourists. Local manufacturers blend low-cost production with incremental R&D, positioning themselves as credible exporters to Southeast Asian markets. Japan’s early adoption of robotic-assisted cataract consoles lifts demand for ultra-short-shaft manual instruments that dovetail with bedside robots.

Europe, governed by the Medical Device Regulation framework, slows time-to-market for incremental modifications but preserves patient safety. Germany, France, and the United Kingdom dominate volume, yet Scandinavian countries lead in procurement policies that reward carbon-footprint reductions. ESCRS-backed sustainability targets compel suppliers to adopt recyclable substrates, giving eco-forward vendors an edge in competitive tenders. Southern European markets, coping with tighter hospital budgets, lean toward refurbished reusable sets, underlining region-specific procurement dynamics.

Competitive Landscape

Market Concentration

The five leading suppliers—Carl Zeiss Meditec, Alcon, BVI Medical, Oertli, and New World Medical—collectively controlled about 45.0% of the Ophthalmic Handheld Surgical Instruments market in 2024, reflecting moderate consolidation. Carl Zeiss Meditec’s EUR 985 million (USD 1.08 billion) purchase of Dutch Ophthalmic Research Center expanded its vitreo-retinal portfolio, illustrating a strategy of marrying visualization platforms with disposable micro-tools to deepen surgeon loyalty. Alcon’s planned USD 356 million acquisition of Lensar extends that template into laser-assisted cataract workflows, bundling femtosecond consoles with proprietary knives and choppers.

Material science remains a differentiation pillar: vacuum-deposited diamond-like carbon coatings that double edge retention help justify premium pricing by cutting sharpening costs in half. Digital integration accelerates: RFID chips embedded in handles feed usage data into hospital ERP dashboards, enabling predictive sharpening schedules and reducing loss. Hospitals may soon evaluate handhelds as data assets rather than mere cutting tools.

Sustainability features grow strategic heft. Oertli’s solar-powered Swiss plant and closed-loop water recycling support European tenders that weight ESG criteria heavily. Emerging-market suppliers scale commodity steel blades and undercut incumbents in price-sensitive regions, forcing midsized Western firms to choose between innovation or cost leadership niches. Market competition thus bifurcates into a premium, innovation-led tier and a high-volume, cost-driven tier.

Ophthalmic Handheld Surgical Instruments Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BVI Medical secured FDA 510(k) clearance for the Leos Laser Endoscopy Ophthalmic System, broadening minimally invasive glaucoma options.

- April 2025: Lohmann & Rauscher Group acquired Unisurge International, adding a UK line of surgical disposables focused on ophthalmic drapes.

- March 2025: Alcon agreed to acquire Lensar, Inc. for USD 356 million, expanding its laser-assisted cataract capabilities.

- March 2025: U.S. and European regulators approved new retina gene therapies, expected to stimulate demand for ultra-fine cannulas suitable for sub-retinal delivery.

- February 2025: New World Medical obtained FDA clearance for the VIA360 Surgical System, adding visco-elastic delivery and trabeculotomy functions.

Table of Contents for Ophthalmic Handheld Surgical Instruments Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Global Surge in Cataract & Glaucoma Surgical Volumes Driven by Aging Demographics

- 4.2.2Shift Toward Ambulatory & Minimally Invasive Ophthalmic Procedures Requiring Precision Hand Tools

- 4.2.3Rising Adoption of Premium IOLs & Refractive Corrections Fueling Demand for Micro-Incision Instruments

- 4.2.4Expansion of Vision Health Coverage & Reimbursement Policies Supporting Instrument Upgrades

- 4.2.5Growing Investments in Ophthalmic Centers of Excellence Across Emerging Markets

- 4.2.6Technological Innovations in Ergonomic & Titanium Instrument Design Enhancing Surgical Efficiency

- 4.3Market Restraints

- 4.3.1Intensifying Price Pressure from Generic Low-Cost Manufacturers Reducing ASPs

- 4.3.2Sterilization Compliance Costs & Delays Curtailing Reusable Instrument Utilization

- 4.3.3Slow Regulatory Approvals for Novel Ophthalmic Instruments Hindering Time-to-Market

- 4.3.4Supply Chain Vulnerabilities in Specialty Grade Metals Affecting Production Lead Times

- 4.4Regulatory Outlook

- 4.5Porter's Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product

- 5.1.1Forceps

- 5.1.2Scissors

- 5.1.3Knives

- 5.1.4Choppers

- 5.1.5Cannula

- 5.1.6Speculum

- 5.1.7Other Products

- 5.2By Usability

- 5.2.1Reusable Instruments

- 5.2.2Single-use / Disposable Instruments

- 5.3By Material

- 5.3.1Stainless-Steel

- 5.3.2Titanium

- 5.3.3Polymer / Composite

- 5.3.4Others

- 5.4By Application

- 5.4.1Cataract Surgery

- 5.4.2Glaucoma Surgery

- 5.4.3Refractive Surgery

- 5.4.4Retinal Surgery

- 5.4.5Other Applications

- 5.5By End-User

- 5.5.1Hospitals

- 5.5.2Ophthalmic Clinics

- 5.5.3Other End-Users

- 5.6Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia Pacific

- 5.6.4Middle East & Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East & Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1BVI

- 6.3.2Geuder AG

- 6.3.3RUMEX International Co.

- 6.3.4Moria SA

- 6.3.5Appasamy Associates Pvt Ltd

- 6.3.6Accutome Inc.

- 6.3.7Duckworth & Kent Ltd.

- 6.3.8Medline Industries LP

- 6.3.9Haag-Streit Group

- 6.3.10Pelion Surgical

- 6.3.11Millennium Surgical

- 6.3.12Surgical Holdings

- 6.3.13Carl Zeiss Meditec AG

- 6.3.14Alcon Inc.

- 6.3.15Bausch + Lomb Corp.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Ophthalmic Handheld Surgical Instruments Market Report Scope

As per the scope of the report, ophthalmic handheld surgical instruments are specialized tools used by ophthalmic surgeons during various surgical procedures related to the eyes. These instruments are designed to be precise, delicate, and versatile to perform intricate procedures with high precision.

The ophthalmic handheld surgical instruments market is segmented by product and end-users. In terms of products, the market is segmented into forceps, scissors, choppers, cannula, speculum, and others. The market is segmented by application as cataract surgery, glaucoma surgery, refractive surgery, and retinal surgery. By end-user, the market is segmented as hospitals, ophthalmic clinics, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.