Surgical Suction Instruments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

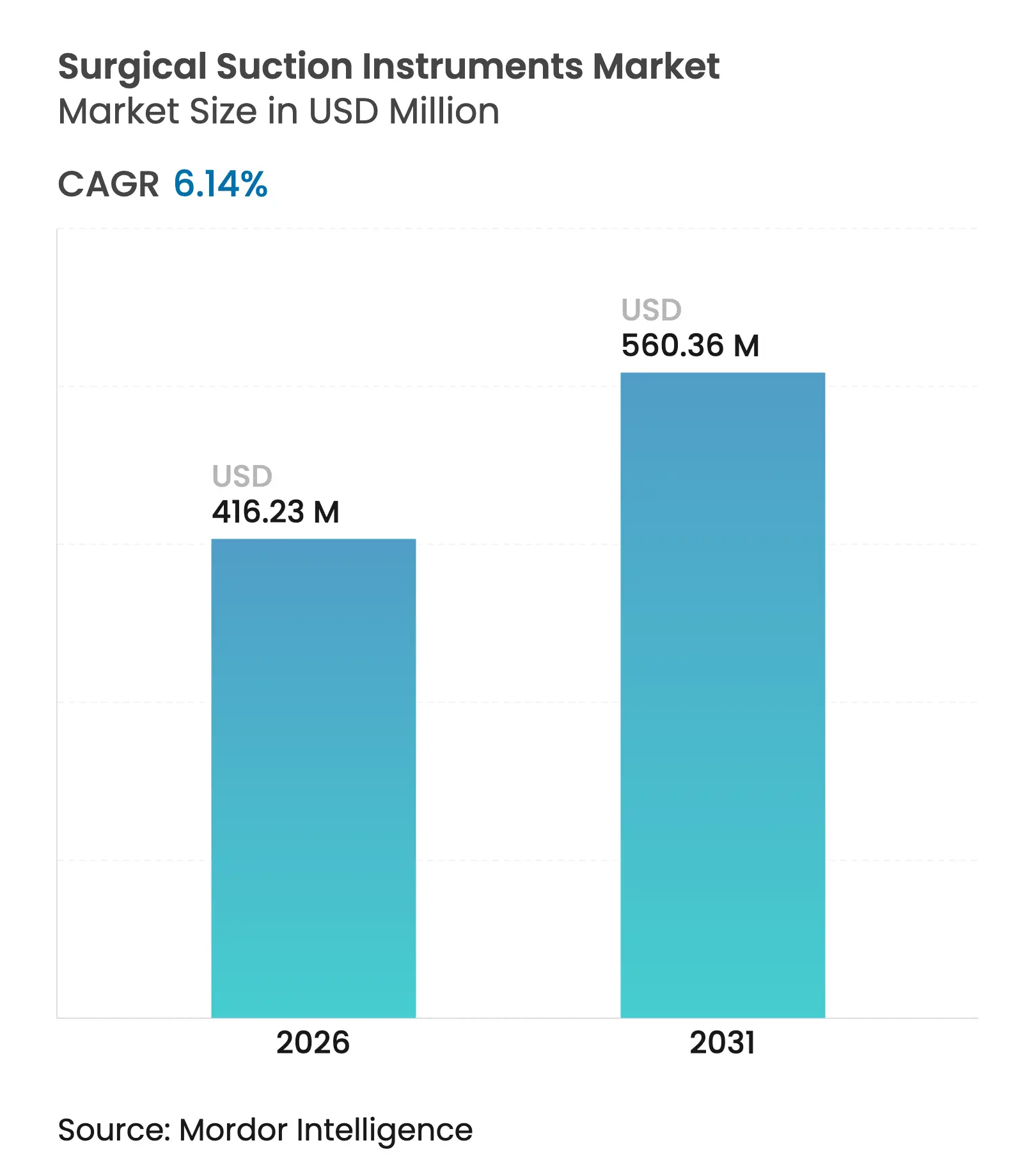

| Market Size (2026) | USD 416.23 Million |

| Market Size (2031) | USD 560.36 Million |

| Growth Rate (2026 - 2031) | 6.14 % CAGR |

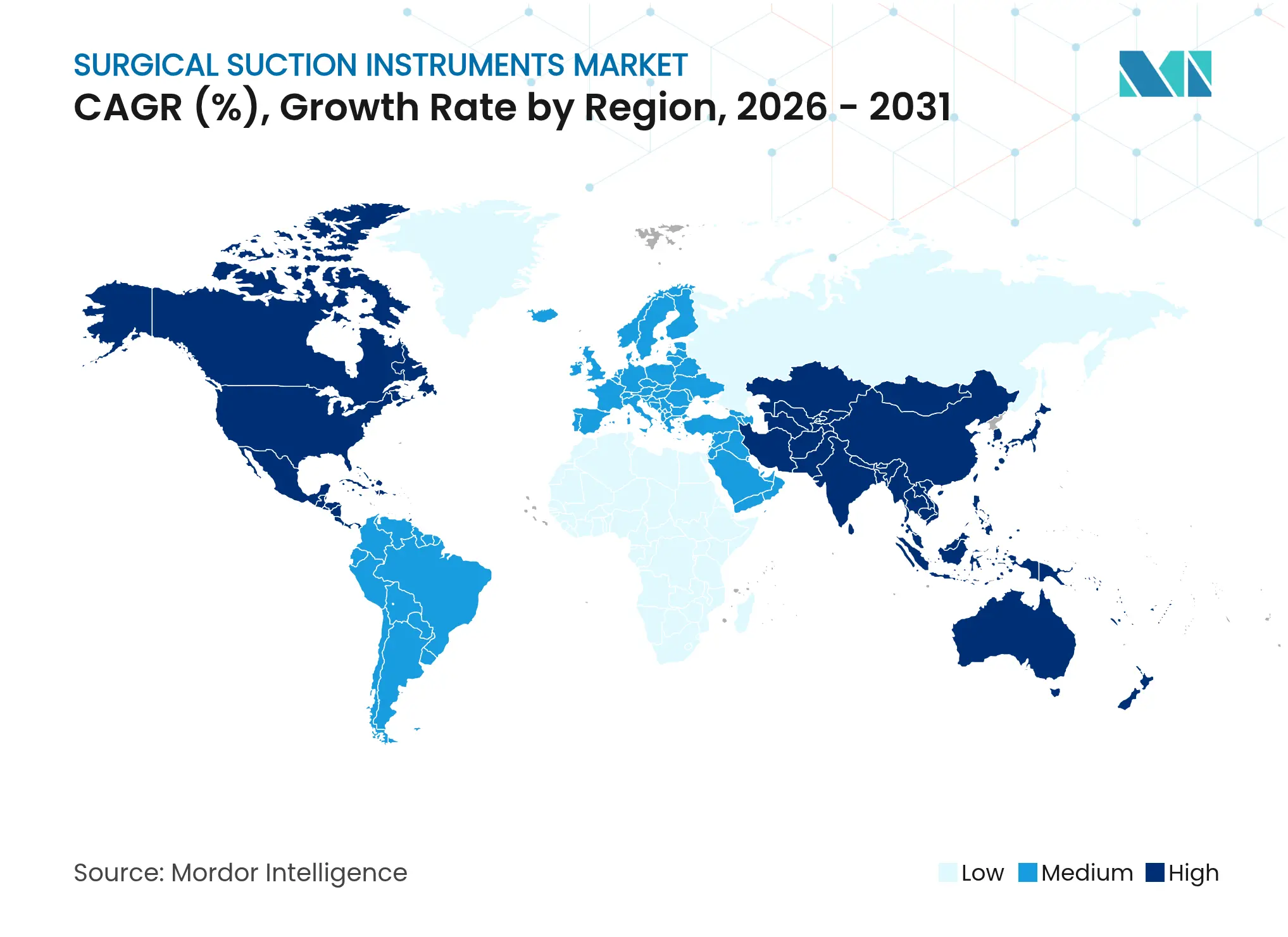

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Surgical Suction Instruments Market Analysis by Mordor Intelligence

The surgical suction instruments market size was valued at USD 392.15 million in 2025 and estimated to grow from USD 416.23 million in 2026 to reach USD 560.36 million by 2031, at a CAGR of 6.14% during the forecast period (2026-2031). Rising surgical volumes, tighter infection-control rules, mandatory smoke-evacuation legislation in 17 U.S. states, and steady gains in outpatient surgery underpin current demand growth [1]Association of periOperative Registered Nurses, “Surgical Smoke Legislation Tracker,” aorn.org . Hospitals seek devices that cut the 7.3% surgical site infection rate that adds USD 15,339 – 17,196 to every affected procedure. Technology upgrades such as Stryker’s Neptune 3, which lowers CO₂ emissions by 98.5%, provide measurable economic and environmental wins. Supply chain diversification, battlefield medicine needs, and the shift from cost to value-based procurement add further momentum across the surgical suction instruments market.

Key Report Takeaways

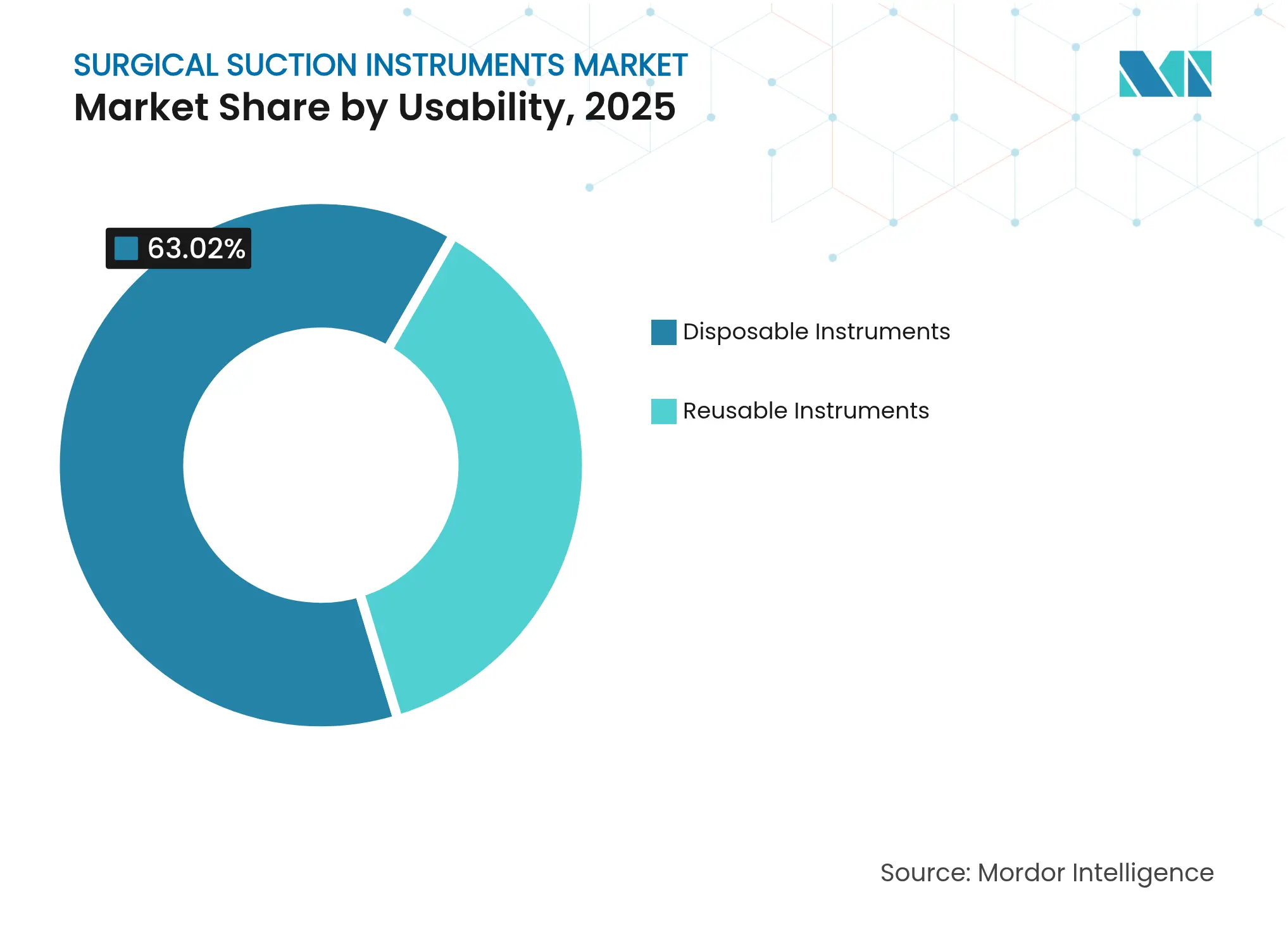

- By usability, disposable instruments held 63.02% of the surgical suction instruments market share in 2025, while reusable instruments are projected to post the fastest 6.78% CAGR through 2031.

- By product type, Yankauer suction tubes led with 41.05% revenue share in 2025; pooled suction tubes are forecast to expand at a 6.9% CAGR to 2031.

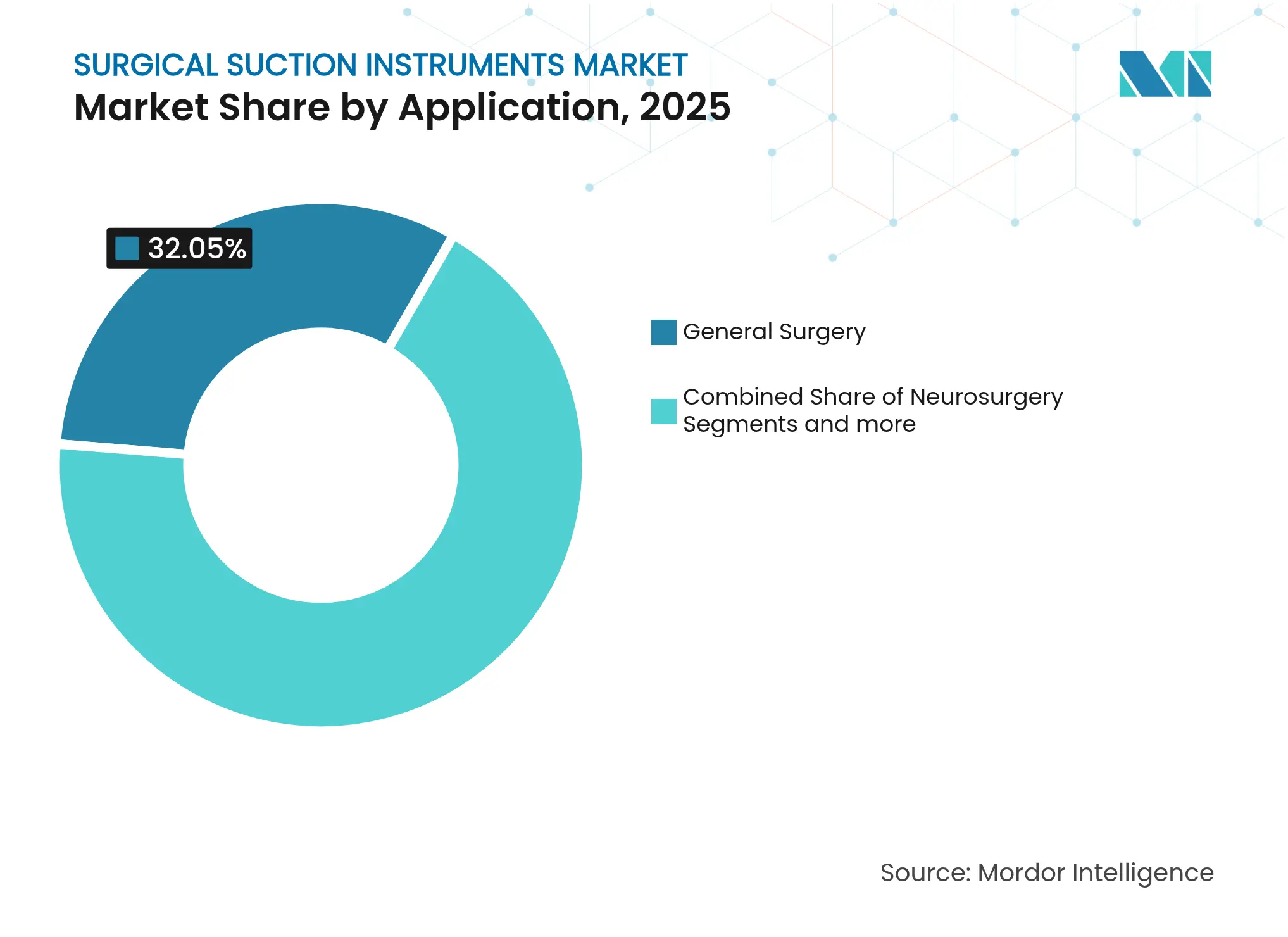

- By application, general surgery accounted for 32.05% of the surgical suction instruments market size in 2025; neurosurgery records the highest 6.89% CAGR through 2031.

- By end user, hospitals and clinics captured 66.35% of 2025 revenue; ambulatory surgical centers grow the fastest at 6.74% CAGR to 2031.

- By geography, North America commanded 42.15% of 2025 revenue; Asia-Pacific is set to grow at a 6.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Suction Instruments Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing number of surgeries and rising healthcare spend

Increasing number of surgeries and rising healthcare spend

| +1.8% | Global with emphasis on North America and Asia-Pacific | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:

Global with emphasis on North America and Asia-Pacific

|

Impact Timeline

:

Medium term (2-4 years)

|

Technological advancements in suction efficiency and

ergonomics

Technological advancements in suction efficiency and

ergonomics

| +1.2% | North America and Europe lead, Asia-Pacific follows | Long term (≥ 4 years) | |||

Adoption in battlefield and emergency field-care medicine

Adoption in battlefield and emergency field-care medicine

| +0.7% | North America and Europe, expanding to conflict regions | Short term (≤ 2 years) | |||

Growing prevalence of chronic and infectious diseases

requiring surgery

Growing prevalence of chronic and infectious diseases

requiring surgery

| +1.1% | Global, pronounced in aging populations | Long term (≥ 4 years) | |||

Integration with smoke evacuation for OR air-quality

compliance

Integration with smoke evacuation for OR air-quality

compliance

| +0.9% | North America leads, Europe follows | Medium term (2-4 years) | |||

Shift toward single-use cannulas for infection control

Shift toward single-use cannulas for infection control

| +0.6% | Global, fastest in mature markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Number of Surgeries and Rising Healthcare Spend

Projected 25% growth in surgical care over the next decade elevates baseline demand, especially for portable systems tailored to outpatient settings. Total joint replacements in ambulatory centers rose 19% year over year, underscoring the push toward efficient, mobile suction platforms. Aging demographics amplify volumes in orthopedics and cardiovascular work that require high-capacity suction. Health systems now rank clinical outcomes above unit price in 32% of procurement decisions, rewarding suppliers that prove measurable value. These converging factors reinforce upward pressure on the surgical suction instruments market.

Technological Advancements in Suction Efficiency and Ergonomics

Rapid smoke clearance within 8 seconds using next-generation nebulization boosts visibility and reduces OR exposure risks. Flexible catheter tips improve reach in confined fields, while articulated handles trim operative time by 40 minutes in complex laparoscopy [2]Xiaosong Lin, "Enhancing laparoscopic visibility: efficient surgical smoke clearance innovatively using nebulization technology," Biomedical Engineering Online, biomedical-engineering-online.biomedcentral.com. Stryker’s Neptune 3 shows sustainability gains by cutting waste weight 98.5% and disposal time nearly eightfold. Such innovations differentiate brands inside the surgical suction instruments market and align with hospital green-procurement goals [3]Vera Kortman, "Advancements in aspiration catheter tip design for thrombectomy: a comprehensive patent review," Frontiers in Medical Technology, frontiersin.org.

Adoption in Battlefield and Emergency Field-Care Medicine

Forward Surgical Teams demand rugged, battery-powered devices that operate inside the critical one-hour window for damage-control surgery. Portable suction integrated into trauma kits supports REBOA and other life-saving interventions that have moved survival from 50.9% mortality toward better outcomes. Product designs now focus on compact form factors, rapid battery swap-outs, and single-use tubing to bypass sterilization hurdles—niches that broaden the surgical suction instruments market footprint.

Growing Prevalence of Chronic and Infectious Diseases Requiring Surgery

Cardiovascular, orthopedic, and oncology caseloads rise with aging societies, lifting demand for reliable fluid management. Surgical site infections at 7.3% incidence add USD 15,339 – 17,196 per case, prompting tighter suction and drainage protocols. Outbreaks linked to inadequately cleaned instruments highlight the role of effective suction in infection prevention. Hospitals favor systems validated for contamination control, bolstering growth for advanced offerings inside the surgical suction instruments market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High device and procedure costs

High device and procedure costs

| –1.4% | Global, pronounced in cost-sensitive markets | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

–1.4%

|

Geographic Relevance

:

Global, pronounced in cost-sensitive markets

|

Impact Timeline

:

Medium term (2-4 years)

|

Lengthy regulatory approval cycles

Lengthy regulatory approval cycles

| –0.8% | North America and Europe, spillover worldwide | Long term (≥ 4 years) | |||

Sustainability pressure versus single-use plastics

Sustainability pressure versus single-use plastics

| –0.6% | Europe leads, North America follows | Medium term (2-4 years) | |||

Component-supply disruptions inflating lead times

Component-supply disruptions inflating lead times

| –0.9% | Global, concentrated in Asia-Pacific manufacturing | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Device and Procedure Costs

Hospitals increasingly favor low-cost alternatives that risk quality trade-offs, compressing supplier margins. Governments aim to slow total device outlays despite forecasts for USD 800 billion global medical device sales by 2030, squeezing budgets for premium suction units. Smaller manufacturers without scale feel pressure, nudging the surgical suction instruments industry toward consolidation.

Lengthy Regulatory Approval Cycles

Average 510(k) reviews for software-enabled devices span 154 – 201 days and extend further with additional queries. ISO 13485 alignment required from February 2026 forces system upgrades, raising compliance burdens. Extended timelines slow market entry for emerging players looking to innovate within the surgical suction instruments market.

Segment Analysis

By Usability: Infection Control Drives Single-Use Adoption

Disposable devices dominate the surgical suction instruments market with 63.02% revenue in 2025. The segment grew as hospitals favored ready-to-use products after inspection failures in 81 of 84 reprocessed LigaSure units. The reusable segment now advances at a 6.78% CAGR on the back of validated vaporized hydrogen peroxide sterilization and hospital sustainability targets. Evidence that multi-use staplers cut waste 50% and resource use over 90% positions reusable systems for value-driven procurement, helping lift the segment’s contribution to the surgical suction instruments market size.

Reusable growth also reflects better cleaning validation. Studies found 94.2% visual failure in metal-lumen suction devices, yet ATP bioluminescence testing improved detection of residual soil. Vendors now bundle scope-channel flushers and audit software to sustain compliance. While infection-control officers still prefer terminally sterilized devices, environmental committees stress waste reduction, sustaining a balanced shift inside the surgical suction instruments market.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Specialized Instruments Gain Market Share

Yankauer tubes remained the workhorse with 41.05% market control in 2025. Their wide use across general, orthopedic, and trauma surgeries secures entrenched demand. However, pooled suction tubes post a 6.9% CAGR because multi-port tips shorten operative time and lower clogging in high-debris fields, especially in bariatric and obstetric surgery.

Innovation spurs growth in niche tools. Frazier tips, designed for neurosurgery, benefit from imaging-guided procedures that need fine 9 Fr lumens. Magnetic clip retrieval systems and thrombectomy catheters appear in the “Others” cluster, pulling incremental revenue toward procedure-specific products. These developments expand the overall surgical suction instruments market size and diversify revenue streams.

By Application: Neurosurgery Drives Fastest Growth

General surgery contributed 32.05% of 2025 revenue, sustained by sheer procedure volumes. Wound debridement, appendectomy, and abdominal trauma rely on high-flow suction to keep views clear and avoid fluid pooling.

Neurosurgery is the fastest riser at 6.89% CAGR. Microscopic brain and spine procedures demand narrow-gauge tips with low-pressure precision to protect neural tissue. Integration with robotic platforms supports steady gains. Cardiothoracic teams adopt pulsatile suction pumps that preserve blood for cell salvage during bypass, while orthopedics leans on evacuation to maintain cement interface clarity in joint replacements. This diverse uptake strengthens long-term prospects for the surgical suction instruments market.

Note: Segment shares of all individual segments available upon report purchase

By End User: ASCs Drive Market Expansion

Hospitals and clinics captured 66.35% of 2025 revenue due to broad service offerings and capital budgets able to absorb premium systems. Infection-control committees in these settings upgrade to integrated smoke evacuation, buoying replacement cycles.

Ambulatory surgical centers grow at 6.74% CAGR as CMS now reimburses shoulder arthroplasty and other complex orthopedic procedures outside hospitals. ASCs favor tabletop or tower systems that roll between suites and operate quietly under local codes. Specialty clinics and mobile field units round out the “Others” category, where battery-driven units open incremental pockets of the surgical suction instruments market.

Geography Analysis

North America retained 42.15% revenue share in 2025. Legislation across 17 states and NFPA 99-2024 reinforce demand for smoke-evacuating suction, prompting fleet-wide replacements. Purchasing teams now rank evidence over cost in 32% of contracts, creating a premium segment for sustainability-tuned systems. Established distributors such as Cardinal Health ensure stock continuity, supporting uptake of advanced options throughout the surgical suction instruments market.

Europe sits second on revenue. The Medical Device Regulation tightens documentation, favoring established suppliers that can handle technical files. Sustainability priorities push multi-use models, with documented 50% waste saves via reusable staplers guiding procurement. Leaders like Germany and France push eco-design labeling, which developers mirror in recyclable packaging and lower-weight tubing.

Asia-Pacific is forecast to expand at a 6.95% CAGR. Governments across China, India, and Indonesia invest in OR modernization as the regional medical device market moves beyond USD 190 billion by 2025. Local manufacturers offer budget systems that shave import duties, but tier-1 hospitals still specify U.S. or European brands for high-risk surgeries. Regional fragmentation and varying tender rules pose entry barriers, yet rising surgical volumes ensure Asia-Pacific produces the largest incremental demand for the surgical suction instruments market.

Competitive Landscape

Market Concentration

Competition is moderate. Cardinal Health, Medline Industries, and Stryker leverage scale, direct sales teams, and service contracts to keep incumbency. Cardinal Health’s medical products unit booked USD 226.8 billion in fiscal 2024, reflecting the cash that underwrites iterative R&D.

Technology leads differentiation. Stryker’s Neptune 3 slashed CO₂ output by 98.5% and sped disposal 7.9-fold, scoring sustainability credits that convert bids. Johnson & Johnson’s Polyphonic AI Fund signals a push for AI-guided suction, positioning it to pair visualization data with fluid extraction.

Midsized firms pursue programmatic M&A. Analysis of 396 device deals shows a string-of-pearls path beats one-off megamergers in shareholder returns. Smaller innovators focus on rugged portable units for military and emergency medicine niches, carving space within the surgical suction instruments market until scale players acquire them.

Surgical Suction Instruments Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Teleflex completed the EUR 760 million (USD 830 million) purchase of BIOTRONIK’s vascular intervention business to broaden its interventional lineup.

- June 2025: Johnson & Johnson launched the Polyphonic AI Fund for Surgery with NVIDIA and Amazon Web Services to seed AI tools in OR workflows.

- June 2025: Stryker agreed to acquire Inari Medical for USD 4.9 billion, gaining high-growth peripheral vascular thrombectomy assets.

- February 2025: Teleflex detailed plans to spin off its vascular access, interventional, and surgical unit into a separate public company by mid-2026.

Table of Contents for Surgical Suction Instruments Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing Number of Surgeries & Rising Healthcare Spend

- 4.2.2Technological Advancements in Suction Efficiency & Ergonomics

- 4.2.3Adoption In Battlefield & Emergency Field?Care Medicine

- 4.2.4Growing Prevalence of Chronic and Infectious Diseases Requiring Surgery

- 4.2.5Integration With Smoke-Evacuation for OR Air-Quality Compliance

- 4.2.6Shift Toward Single-Use Cannulas for Infection Control

- 4.3Market Restraints

- 4.3.1High Device & Procedure Costs

- 4.3.2Lengthy Regulatory Approval Cycles

- 4.3.3Sustainability Pressure Vs Single-Use Plastics

- 4.3.4Component-Supply Disruptions Inflating Lead Times

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porters Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Usability

- 5.1.1Disposable Instruments

- 5.1.2Reusable Instruments

- 5.2By Product Type

- 5.2.1Yankauer Suction Tubes

- 5.2.2Pooled Suction Tubes

- 5.2.3Frazier Suction Tips

- 5.2.4Others

- 5.3By Application

- 5.3.1General Surgery

- 5.3.2Neurosurgery

- 5.3.3ENT and Dental Surgery

- 5.3.4Orthopedic and Spine Surgery

- 5.3.5Cardiothoracic and Vascular Surgery

- 5.3.6Others

- 5.4By End User

- 5.4.1Hospitals and Clinics

- 5.4.2Ambulatory Surgical Centers

- 5.4.3Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1Cardinal Health

- 6.3.2Medline Industries

- 6.3.3CONMED Corporation

- 6.3.4Stryker Corporation

- 6.3.5Teleflex Incorporated

- 6.3.6Allied Healthcare Products

- 6.3.7Wellell Inc

- 6.3.8Applied Medical Resources

- 6.3.9SP Industries (Bel-Art)

- 6.3.10Bionix LLC

- 6.3.11Steris (Cantel Medical)

- 6.3.12Medela AG

- 6.3.13Olympus Corp.

- 6.3.14Laerdal Medical

- 6.3.15Zimmer Biomet

- 6.3.16Hologic (Panther)

- 6.3.17ATMOS MedizinTechnik

- 6.3.18Integra LifeSciences

- 6.3.19New World Medical

- 6.3.20Shanghai Kindly Medical

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Surgical Suction Instruments Market Report Scope

As per the scope of the report, Surgical Suction instruments are appliances that are used to remove substances such as blood, saliva, mucus, and vomit from a person's airway. Suction devices may be mechanical hand pumps or batteries or electrically operated mechanisms. The Surgical Suction Instruments market is segmented by Type (Disposable, Reusable), by End-User (Hospitals and Clinics, Ambulatory Surgical Centers, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.