India GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.93 Billion |

| Market Size (2026) | USD 5.72 Billion |

| Market Size (2031) | USD 13.97 Billion |

| Growth Rate (2026 - 2031) | 19.55% CAGR |

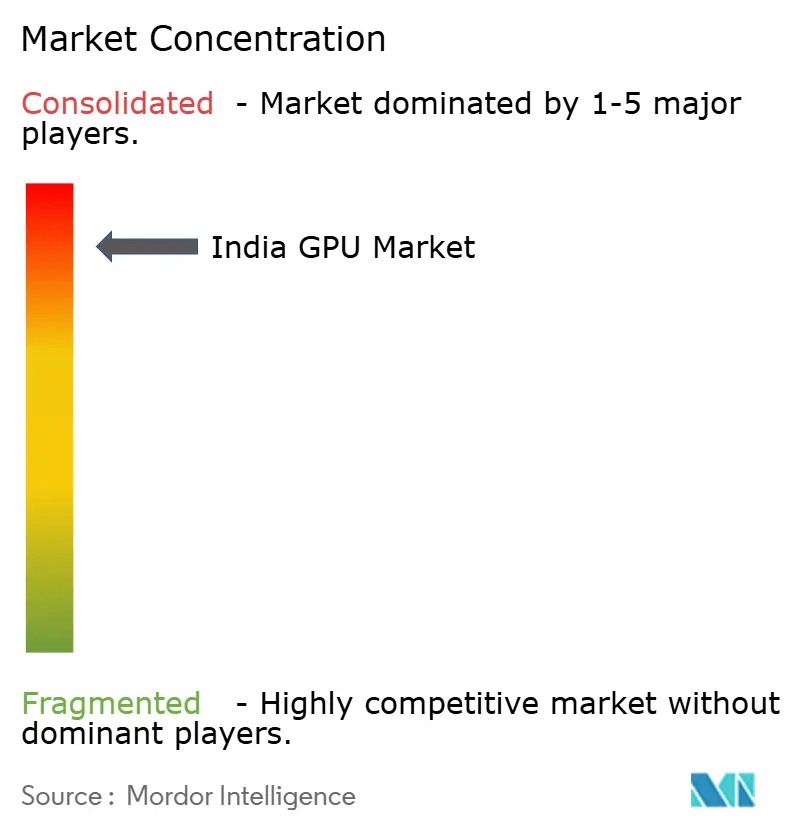

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India GPU Market Analysis by Mordor Intelligence

The India GPU market size is expected to increase from USD 4.93 billion in 2025 to USD 5.72 billion in 2026 and reach USD 13.97 billion by 2031, growing at a CAGR of 19.55% over 2026-2031. Rapid migration of enterprise workloads from CPU-centric servers to GPU-accelerated infrastructure, sizable sovereign AI compute allocations, and hyperscale data center buildouts are redefining demand patterns. Microsoft and Google have earmarked multi-billion-dollar capital outlays for GPU-rich cloud regions, while domestic operators such as Yotta Infrastructure are commissioning superclusters that rival global peers. Gaming hardware refreshes, expanding AI-capable smartphones, and emerging automotive ADAS programs further broaden the consumption base. However, chronic import dependence for sub-7 nm devices, memory supply bottlenecks, and volatility in electricity tariffs continue to temper near-term upside potential.

Key Report Takeaways

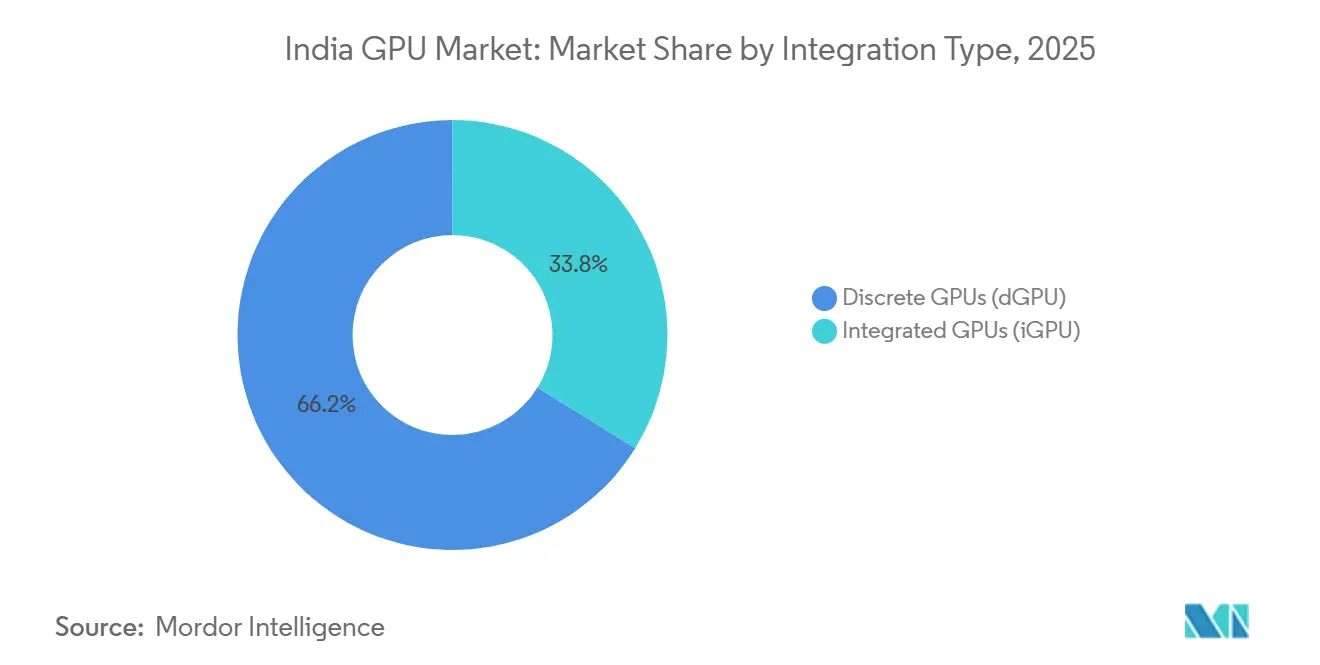

- By integration type, discrete GPUs (dGPU) accounted for 66.18% of the India GPU market size in 2025 and is expected to advance at a 19.94% CAGR through 2031.

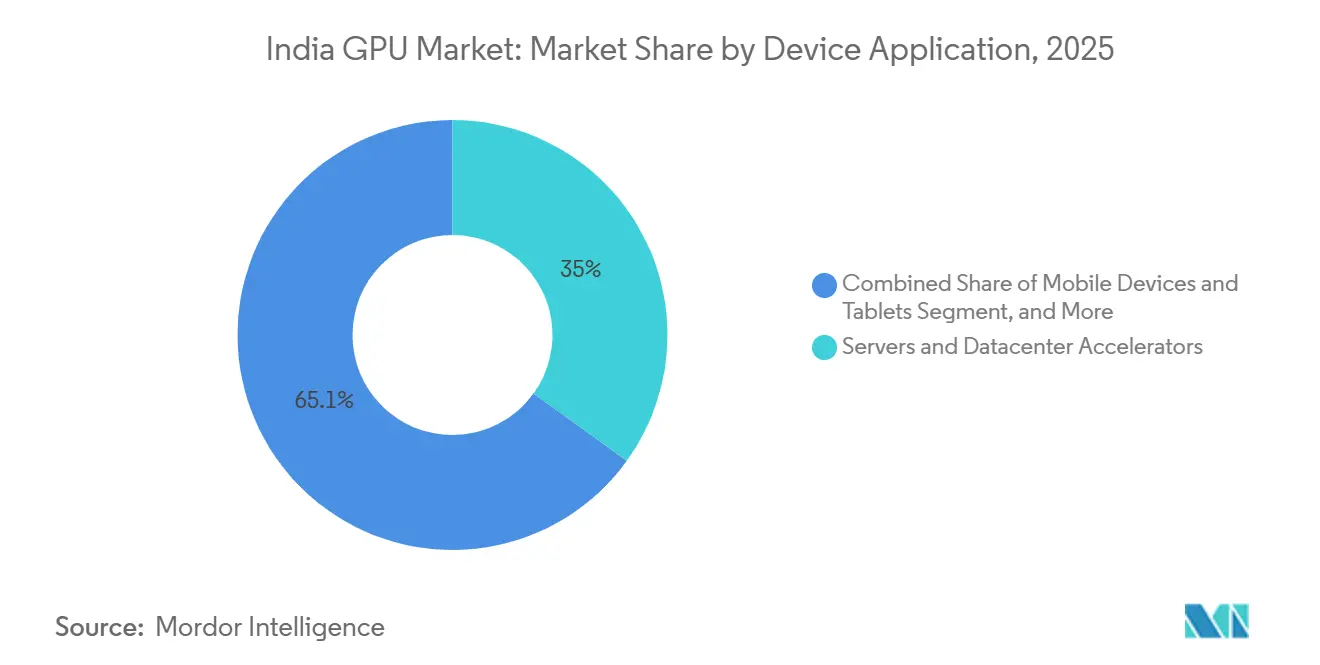

- By device application, the servers and datacenter accelerator segment accounted for 34.95% of the India GPU market size in 2025, and is expected to register a 19.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Cloud Service Provider Investments in Indian Hyperscale DCs | +6.2% | National, concentrated in Mumbai, Hyderabad, Chennai | Medium term (2-4 years) |

| Proliferation of AI Workloads in Edge Devices | +4.8% | National, metros and tier-1 cities | Short term (≤ 2 years) |

| Government PLI Schemes for Semiconductor Manufacturing | +3.5% | National, clusters in Gujarat, Tamil Nadu, Assam | Long term (≥ 4 years) |

| Rapid Expansion of India’s Gaming Ecosystem | +2.7% | National, urban youth demographics | Medium term (2-4 years) |

| Rising Demand for High-Performance Computing in BFSI | +1.9% | Financial hubs | Short term (≤ 2 years) |

| Data-Driven Automotive ADAS Adoption | +0.9% | Premium vehicle segment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Cloud Service Provider Investments in Indian Hyperscale DCs

Hyperscale operators now treat India as a strategic compute region rather than a cost-arbitrage outpost. Microsoft’s multi-region rollout features NVIDIA H100 and forthcoming Blackwell GPUs, while Google is expanding TPU- and GPU-accelerated infrastructure for enterprise AI workloads. Domestic provider Yotta Infrastructure is deploying more than 32,000 H100 units with an upgrade path to Blackwell Ultra, signaling a pivot from general-purpose cloud to inference-optimized clusters.[2]Yotta Infrastructure, “H100 Supercomputing Cluster Fact Sheet,” yottainfra.com The IndiaAI Mission sets aside public funding for 34,000 sovereign GPUs, reducing reliance on foreign clouds.[1]Ministry of Electronics and Information Technology, “IndiaAI Mission: Sovereign AI compute roadmap,” meity.gov.in Collectively, these moves underpin sustained double-digit growth for the India GPU market.

Proliferation of AI Workloads in Edge Devices

Edge inference has graduated from proof-of-concept to volume rollout across retail analytics, industrial vision, and public safety. Qualcomm’s Snapdragon 8 Elite Gen 5 delivers a 23% graphics uplift, enabling on-device generative AI for flagship smartphones, while MediaTek’s Dimensity 9500s brings ray-tracing hardware to mid-premium tiers. Tier-2 smart-city projects leverage edge GPU nodes to meet sub-50 ms latency budgets. The National Payments Corporation of India uses GPU-accelerated models to screen 12 billion monthly payment transactions, demonstrating mission-critical edge inference at a national scale.[3]National Payments Corporation of India, “GPU-Accelerated Fraud Analytics Deployment,” npci.org.in

Government PLI Schemes for Semiconductor Manufacturing

India Semiconductor Mission 2.0 allocates capital subsidies for outsourced assembly, test, and packaging lines, aiming to localize the backend of the value chain. Tata Electronics, in partnership with Powerchip, plans a USD 11 billion 300 mm fab targeting 28 nm nodes, with an aspirational roadmap to 7 nm by 2030. CG Power’s approved OSAT plant will package automotive and industrial GPUs in Sanand. While these moves reduce long-haul logistics and import bills, the absence of domestic sub-10 nm logic capacity leaves the India GPU market reliant on Taiwan and South Korea for advanced dies.

Rapid Expansion of India’s Gaming Ecosystem

India surpassed 520 million gamers in 2025, and Enthusiast PC builders now fuel a discrete GPU upgrade cycle every 24-30 months. NVIDIA’s RTX 5060 Ti and AMD’s Radeon RX 9060 XT target 1080p and 1440p gamers seeking higher frame rates and ray tracing. Handheld consoles such as the ASUS ROG Xbox Ally blend console convenience with PC graphics, expanding addressable demand beyond traditional desktops. Urban e-sports arenas and online retailers offering EMI finance options have widened access for price-sensitive buyers, sustaining unit momentum for the India GPU market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Import Dependence for Advanced Nodes | -3.8% | National, all segments | Long term (≥ 4 years) |

| Global Supply Chain Disruptions Causing Allocation Shortages | -2.9% | Datacenter and enterprise segments | Short term (≤ 2 years) |

| Electricity Cost Volatility Impacting Datacenter TCO | -1.6% | States with higher industrial tariffs | Medium term (2-4 years) |

| Limited Domestic IP for GPU Design Talent Pool | -1.2% | Bengaluru, Hyderabad, Pune | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Import Dependence for Advanced Nodes

India lacks sub-28 nm fabrication, so datacenter GPUs manufactured on 4 nm and below must be imported. GPUs represent roughly 90% of AI server bills of materials, making supply allocation decisions by overseas foundries a critical bottleneck. Long lead times, coupled with limited local high-bandwidth memory packaging, amplify vulnerability to geopolitical shocks.

Global Supply Chain Disruptions Causing Allocation Shortages

HBM scarcity is projected to persist until 2028, inflating component costs and lengthening server deployment cycles. Tier-one U.S. hyperscalers often receive priority, forcing Indian integrators to procure through third-party channels at steep premiums. Alternative accelerators from AMD and Intel offer some relief, yet ecosystem maturity lags NVIDIA’s CUDA, slowing substitution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Integration Type: Discrete GPUs Outpace Integrated Counterparts

Discrete GPUs accounted for 66.18% of the India GPU market share in 2025. Servers, gaming PCs, and professional workstations have gravitated to dedicated silicon that provides higher memory bandwidth and specialized tensor math. Large-scale installations, such as Yotta’s 32,000-plus H100 cluster, illustrate enterprise appetite for top-bin accelerators. Enthusiast gamers are migrating from GTX 1060-class hardware to RTX 50-series cards, aided by board partners that bundle factory overclocks and extended warranties. On the professional side, CAD and media-creation suites exploit driver-certified Quadro and Radeon Pro lines, supporting higher average selling prices.

Integrated GPUs, holding the remaining 33.82%, dominate unit shipments in mainstream laptops and smartphones, where thermals and bill-of-materials ceilings are stringent. Intel Iris Xe and AMD Radeon 700M graphics meet everyday productivity and light creative workloads. In smartphones, Qualcomm Adreno and MediaTek Immortalis cores now handle on-device diffusion models and NPU-assisted photography. The India GPU market size for integrated silicon will continue to climb in absolute terms, although its slice of revenue tilts toward discrete devices because of rising datacenter volumes.

By Device Application: Servers And Datacenters Sustain Leadership

Servers and datacenter accelerators captured 34.95% of the India GPU market size in 2025 and are forecast to post the fastest CAGR through 2031. Public cloud expansions, sovereign AI mandates, and on-premise private-cloud rollouts across BFSI and healthcare are the cornerstones of demand. New service launches, such as Tata Communications’ Vayu AI Cloud, bundle H100 and MI300X instances with managed ML tooling, driving predictable capacity reservations.

Mobile devices and tablets lead in absolute volumes, but value contribution is diluted by low ASPs. AI-capable flagships priced above INR 50,000 integrate advanced GPUs that execute large-language-model inference locally, enhancing privacy and reducing carrier backhaul. PCs and workstations enjoy a cyclical uplift as enterprises standardize on notebooks equipped for AI copilots. Handheld consoles revive portable gaming, and automotive ADAS adoption nudges GPU penetration in premium vehicles. Collectively, these segments ensure the India GPU market maintains a broad, diversified demand base.

Geography Analysis

Metropolitan clusters along India’s western and southern corridors anchor enterprise GPU deployments. Mumbai and Hyderabad host new Azure and AWS availability zones, each requiring tens of thousands of H100-class units. Greater Noida’s proximity to the national capital has attracted Yotta’s supercomputing campus, while Chennai and Pune benefit from Google’s USD-scale expansions. Together, these cities account for roughly 70% of installed datacenter GPU capacity. Bengaluru underpins the software value chain, housing 40% of the nation’s semiconductor design talent and major R&D centers for NVIDIA, AMD, Intel, and Qualcomm. University-industry consortia now run shared GPU clusters that feed AI curriculum and foster toolchain localization. Beyond tier-1 metros, operators such as CtrlS are seeding edge GPU nodes in Ahmedabad, Jaipur, and Lucknow, allowing smart-city applications to execute inference within 50 km of endpoints.

Consumer retail sales mirror the income gradient. Delhi NCR, Mumbai, Bengaluru, Hyderabad, Pune, and Chennai contribute 65% of discrete GPU card shipments, thanks to organized brick-and-mortar chains and e-commerce penetration. Tier-3 towns lean toward laptops with integrated graphics, but EMI-structured online sales are slowly expanding discrete uptake, subtly widening the geographic footprint of the India GPU market.

Competitive Landscape

The market displays moderate concentration. NVIDIA commands about 80% of datacenter accelerators and 70% of discrete gaming GPUs, supported by the CUDA software moat and early access to HBM supply. AMD’s share in gaming cores hovers between 15% and 20%, buoyed by value-for-money offerings that bundle larger VRAM pools. Intel remains a challenger in discrete GPUs, focusing on sub-USD 250 SKUs that appeal to cost-sensitive gamers.

In mobile, Qualcomm and MediaTek collectively power roughly 85% of smartphones above INR 20,000, integrating custom Adreno and Immortalis GPUs. Apple’s M-series chips hold a growing niche in premium laptops, capturing creative professionals who prioritize battery life. Domestic startups such as Saankhya Labs and Steradian Semiconductors pursue domain-specific accelerators for 5G and mmWave radar, signaling early attempts at indigenous IP.

Strategic collaborations are reshaping the supply stack. NVIDIA’s partnership with L&T aims to erect gigawatt-scale AI factories, bundling design, power, and cooling expertise under one roof. Yotta’s USD 2 billion Blackwell deployment showcases vertically integrated infrastructure that secures supply while offering hyperscale economics to domestic enterprises. AMD’s forthcoming RDNA 4 and Intel’s Arc-X refresh promise incremental competition, but software ecosystem depth remains the decisive moat in the India GPU market.

India GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

Qualcomm Technologies Inc.

Samsung Electronics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: NVIDIA expanded its India Deep Tech Alliance to 150 startups, providing H100 and Blackwell access.

- February 2026: L&T and NVIDIA partnered to build gigawatt-scale AI factories, with the first site set for 50,000 GPUs by Q4 2026.

- February 2026: NVIDIA launched AI Grants India, a USD 10 million initiative for 500 startups.

- January 2026: Tata Communications introduced Vayu AI Cloud using H100 and MI300X GPUs.

India GPU Market Report Scope

A GPU is a programmable processor architected for high-throughput, data-parallel computation. It contains hundreds to thousands of smaller, efficient cores optimized for executing the same instruction on multiple data points simultaneously, a model called SIMD (Single Instruction, Multiple Data) or SIMT (Single Instruction, Multiple Threads).

The India GPU Market Report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs) and Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) |

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| By Integration Type | Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) | |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices |

Key Questions Answered in the Report

How large will India’s GPU opportunity become by 2031?

Forecasts point to USD 13.97 billion in revenue by 2031 on a 19.55% CAGR.

Which application is growing fastest?

Servers and datacenter accelerators are expanding at a 19.86% CAGR as enterprises scale AI training and inference.

Who dominates datacenter accelerators?

NVIDIA holds about 80% share, leveraging CUDA software lock-in and early access to HBM supply.

Are domestic fabs reducing import dependence?

Planned 28 nm facilities and OSAT plants help backend localization, but sub-10 nm logic for GPUs remains unavailable until after 2030.

Page last updated on: