Kyphoplasty Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

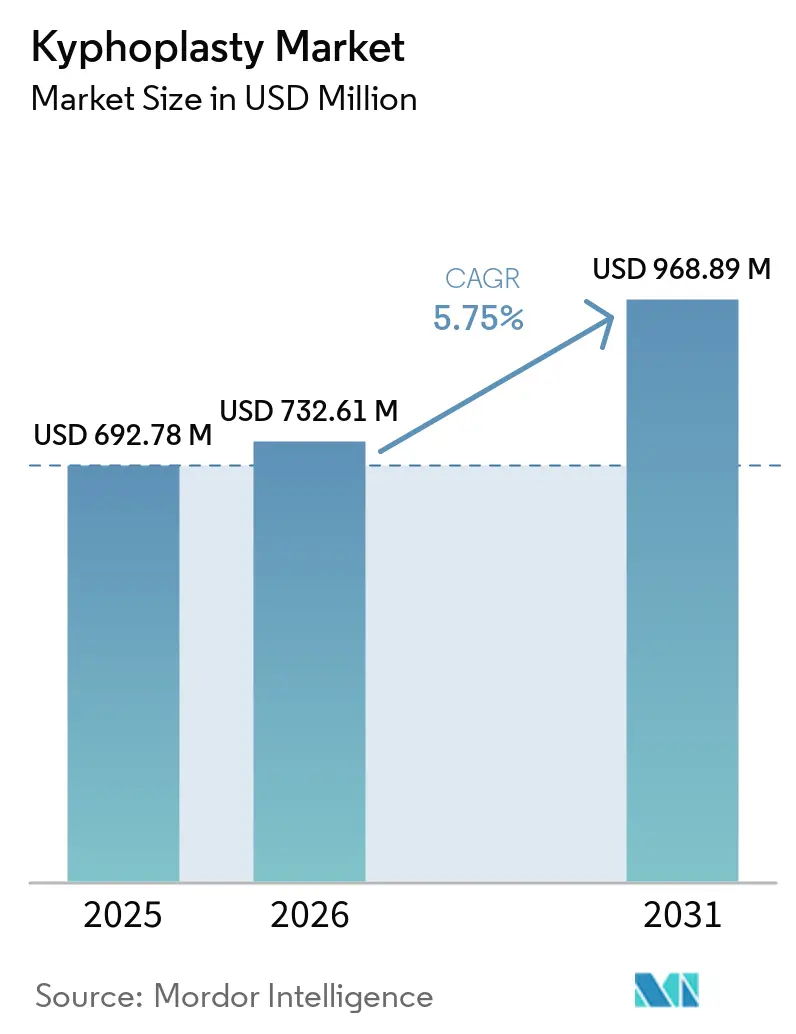

| Market Size (2026) | USD 732.61 Million |

| Market Size (2031) | USD 968.89 Million |

| Growth Rate (2026 - 2031) | 5.75% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kyphoplasty Market Analysis by Mordor Intelligence

The Kyphoplasty Market size was valued at USD 692.78 million in 2025 and is estimated to grow from USD 732.61 million in 2026 to reach USD 968.89 million by 2031, at a CAGR of 5.75% during the forecast period (2026-2031).

The aging global population is driving growth in the kyphoplasty market, with a rising burden of vertebral fractures. This increase is linked to demographic shifts rather than changes in age-standardized rates, ensuring sustained demand. A 2025 study reported 7.5 million vertebral fractures globally in 2024, up from 5.9 million in 1990, highlighting a growing treatable patient base even before improvements in diagnosis and referrals are factored in.[1]Journal of Orthopaedic Surgery and Research, “Global Burden of Vertebral Fractures From 1990 to 2021 and Projections for the Next Three Decades,” Journal of Orthopaedic Surgery and Research, link.springer.com Medtronic maintains a strong position in the moderately competitive market through its Kyphon platform. North America leads in scale, while the Asia-Pacific region is experiencing faster growth. Enhanced reimbursement systems, improved outpatient pathways, and greater clinical adoption of minimally invasive vertebral augmentation are expanding procedural access.

Key Report Takeaways

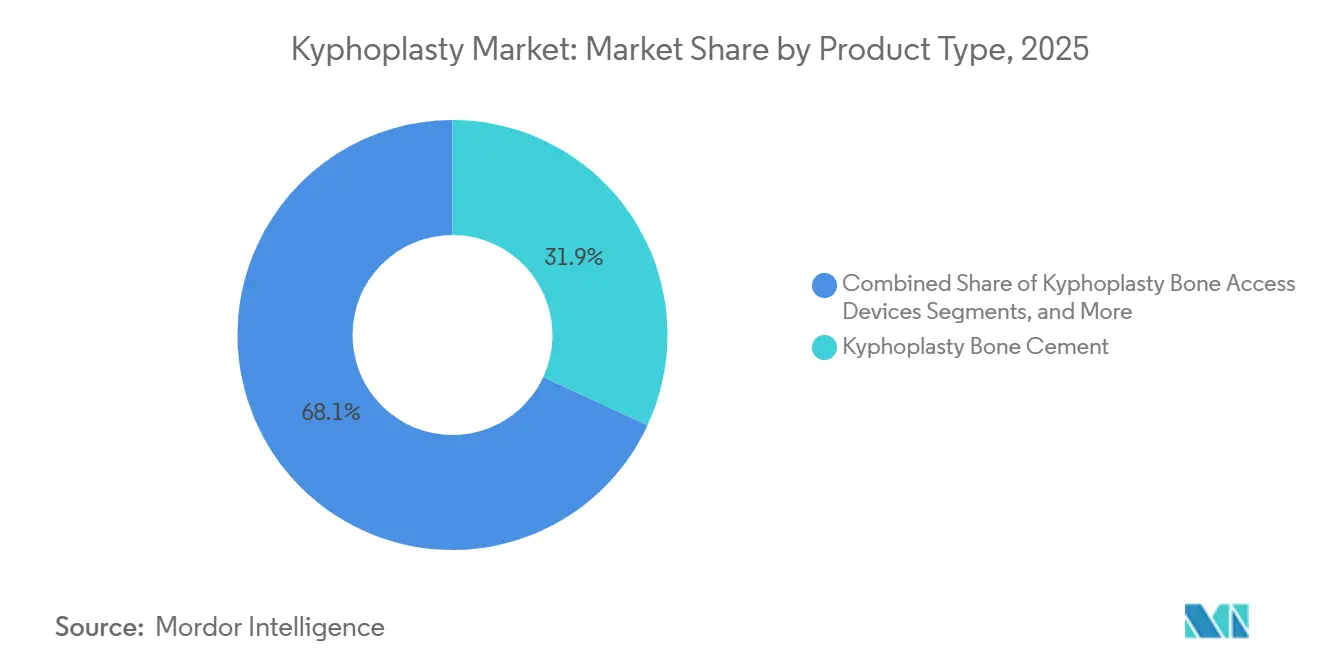

- By product type, kyphoplasty balloon catheters led with 31.89% share in 2025, while kyphoplasty instruments recorded the highest projected CAGR at 6.10% through 2031.

- By indication, osteoporotic vertebral compression fractures accounted for 58.78% share in 2025, while neoplastic vertebral compression fractures are forecast to expand at a 5.95% CAGR through 2031.

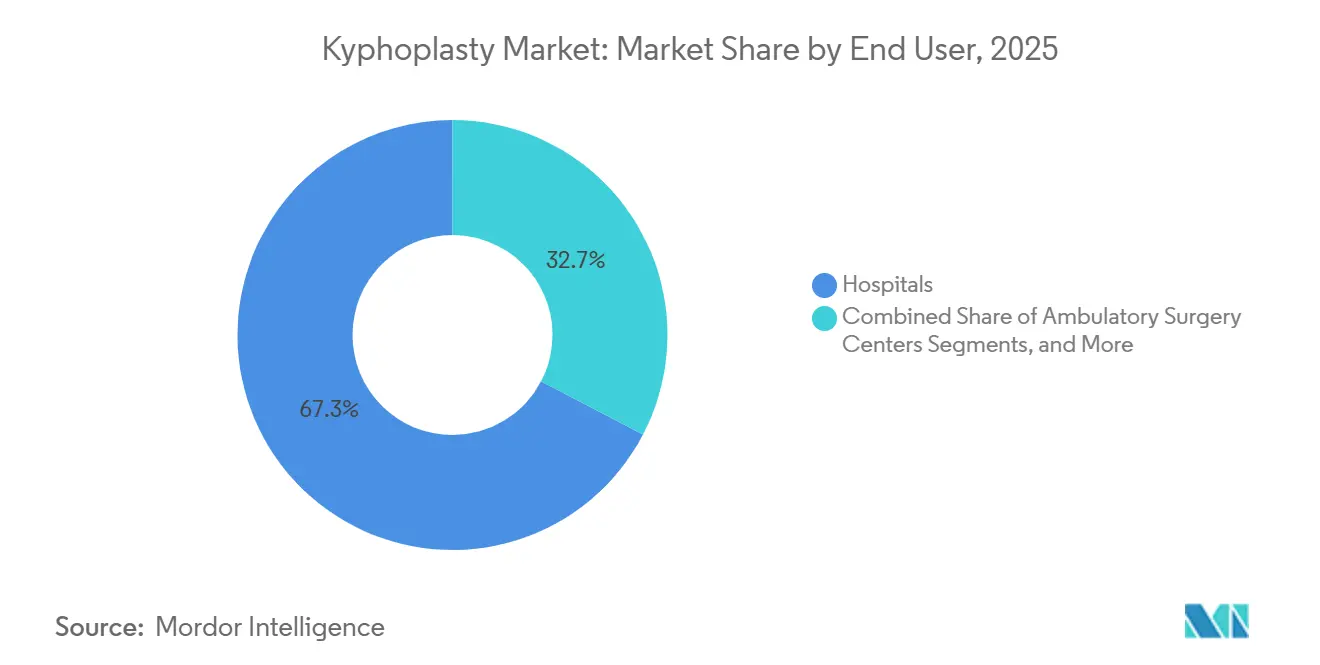

- By end user, hospitals held 67.35% of kyphoplasty market share in 2025, while ambulatory surgery centers are projected to grow at a 6.55% CAGR through 2031.

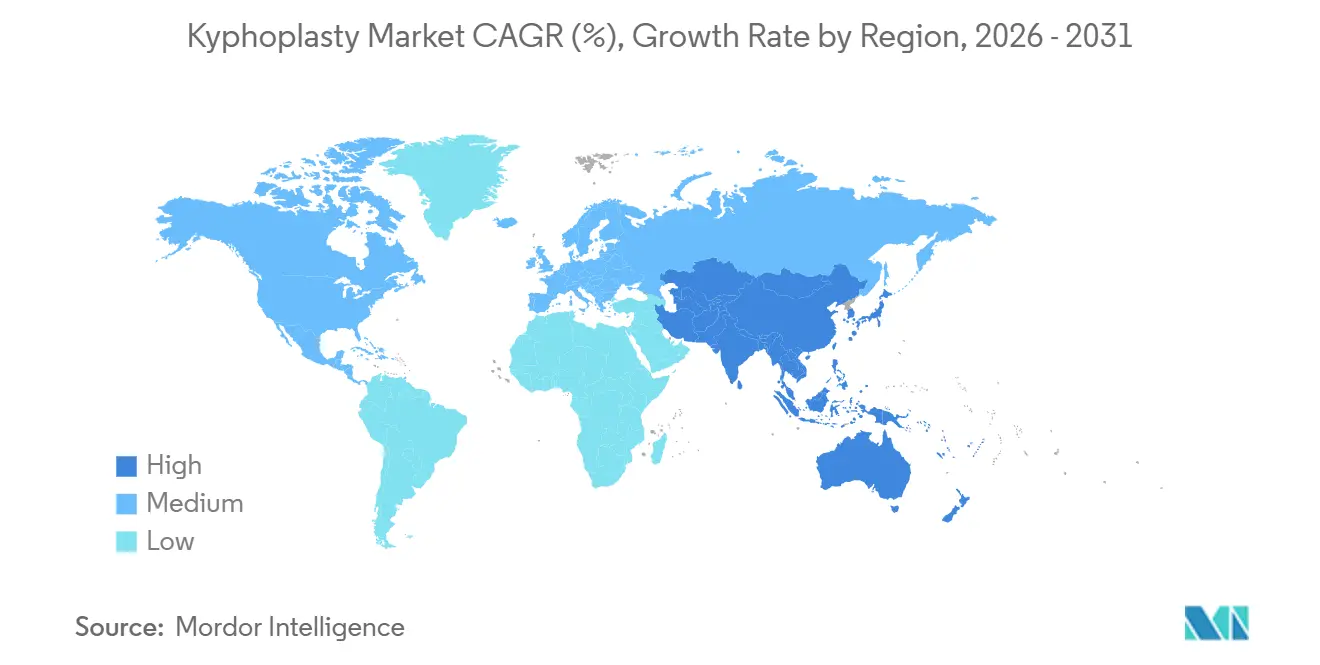

- By geography, North America held 38.95% of the kyphoplasty market size in 2025, while Asia-Pacific is expected to advance at a 7.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Kyphoplasty Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising osteoporotic vertebral compression fracture burden | +1.8% | Global, with strong concentration in North America, Europe, and APAC aging economies including Japan, China, and South Korea | Long term (≥ 4 years) |

| Adoption of minimally invasive spine procedures | +1.2% | Global, with early gains in North America and Europe, followed by spillover into the Middle East and South America | Medium term (2-4 years) |

| Better vertebral height restoration versus vertebroplasty | +0.8% | North America and Europe, where comparative clinical evidence is more closely tied to payer policy | Medium term (2-4 years) |

| Expanded use in malignancy-related vertebral fractures | +0.6% | North America, Western Europe, and Australia, where oncology infrastructure supports multidisciplinary spinal care | Medium term (2-4 years) |

| Growth of ambulatory surgery center-based spine care | +0.5% | North America, especially U.S. Sun Belt states, with early spillover into Europe and APAC private hospital networks | Short term (≤ 2 years) |

| AI-guided navigation and robotic workflow integration | +0.4% | North America, Germany, and Japan, where hospital robotics investments are earlier and deeper | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Osteoporotic Vertebral Compression Fracture Burden

The kyphoplasty market's primary demand is closely tied to the global surge in osteoporotic vertebral compression fractures. A 2025 study forecasted that as the global population ages and preventive measures lag, the prevalence of spinal fractures could jump from 65.2 per 100,000 in 2025 to 128.04 per 100,000 by 2050.[2]Journal of Orthopaedic Surgery and Research, “Global Burden of Vertebral Fractures From 1990 to 2021 and Projections for the Next Three Decades,” Journal of Orthopaedic Surgery and Research, link.springer.com In the U.S., nearly 750,000 new cases of osteoporotic vertebral compression fractures emerge annually.[3]Archives of Medical Science, “Global, Regional, and National Trends in Spinal Fracture Burden From 1990 to 2021 and Projections to 2050,” Archives of Medical Science, archivesofmedicalscience.com The U.K. sees close to 120,000 cases each year, with women aged 85-89 experiencing an incidence rate eight times that of their 60-64 counterparts. Many vertebral fractures initially go unnoticed, limiting conservative care options and increasing the likelihood of surgical intervention after a secondary collapse.[4]Frontiers in Surgery, “Safety and Efficacy of Robot-Assisted Percutaneous Kyphoplasty Under Local Anesthesia in a Day-Surgery Setting for Osteoporotic Vertebral Compression Fractures,” Frontiers in Surgery, frontiersin.org

Adoption of Minimally Invasive Spine Procedures

The kyphoplasty market is benefiting from the shift of spine procedures to minimally invasive and outpatient settings. In 2025, CMS finalized a 2.9% update to the ambulatory surgery center payment rate, leading to total ASC payments nearing USD 7.4 billion.[5]A. Soni, S. Vidyadhara, T. Balamurugan, et al., “Robotic-Assisted Kyphoplasty Demonstrates Superior Efficacy, Safety, and Procedural Efficiency Compared to Fluoroscopy-Guided Techniques, A Retrospective Analysis of 240 Patients,” Journal of Robotic Surgery, link.springer.com This transition supports moving vertebral augmentation from inpatient to outpatient settings. ASC-based procedures favor compact systems, simplified handling, and single-use cement kits, influencing purchasing behaviors in the kyphoplasty market. A 2025 study highlighted that robot-assisted percutaneous kyphoplasty, performed under local anesthesia in a day-surgery setting, resulted in a mean hospital stay of 34 hours, with no 30-day readmissions. Manufacturers offering comprehensive outpatient kits and digital workflow tools are well-positioned as the market increasingly adopts same-day care models.[6]International Osteoporosis Foundation, “Epidemiology of Osteoporosis and Fragility Fractures,” International Osteoporosis Foundation, osteoporosis.foundation

Better Vertebral Height Restoration Versus Vertebroplasty

Clinical differentiation is critical in the kyphoplasty market, particularly in vertebral height restoration compared to vertebroplasty. A 2025 retrospective study revealed that robotic-assisted kyphoplasty achieved a vertebral height restoration rate of 68.00%, surpassing the 64.38% rate of conventional fluoroscopy-guided kyphoplasty. Another 2025 study indicated that kyphoplasty had 58.1% lower odds of cement extravasation compared to vertebroplasty, reducing complications and downstream care costs. The balloon cavity creation in kyphoplasty enables the delivery of higher-viscosity cement at reduced pressure, which needle-only methods struggle to match. Major U.S. payers, including UnitedHealthcare and Premera, now classify kyphoplasty as medically necessary for specific osteoporotic cases post-failed conservative treatment, strengthening its market position over less differentiated alternatives.

Expanded Use in Malignancy-Related Vertebral Fractures

The kyphoplasty market is expanding its clinical reach, particularly in malignancy-related vertebral fractures. Nearly 90% of multiple myeloma patients experience significant osseous involvement, driving demand for vertebral stabilization and pain control. Balloon kyphoplasty is now recognized as a pain relief method for osteolytic spinal lesions in these patients. The North American Spine Society’s 2025 Appropriate Use Criteria for neoplastic compression fractures further emphasize this integration, offering multidisciplinary recommendations across 432 clinical scenarios. Success in this segment depends on disciplined patient selection and outcomes tracking, as failures in treating metastatic vertebral compression fractures often correlate with higher instability markers.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Reimbursement scrutiny and coverage variability | -0.7% | North America, especially CMS WISeR states, and Europe, especially Spain and Italy where reimbursement parity constraints remain | Short term (≤ 2 years) |

| Procedure complexity and learning curve | -0.5% | Global, with stronger effect in the Middle East, South America, and South-East Asia where advanced spine training is still developing | Medium term (2-4 years) |

| Cement leakage and revision risk concerns | -0.4% | Global, with larger impact where post-procedure imaging surveillance is limited | Medium term (2-4 years) |

| Limited adoption in severe collapse and posterior wall fractures | -0.3% | Global, with stronger limits in academic centers that manage more complex fracture patterns | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Scrutiny and Coverage Variability

Reimbursement pressures remain a significant challenge for the kyphoplasty market in North America. The CMS CMMI WISeR Model, effective January 1, 2026, introduced prior authorization and pre-payment medical reviews for kyphoplasty and vertebroplasty in Arizona, New Jersey, Ohio, Oklahoma, Texas, and Washington. These states, with substantial Medicare-age populations, represent a critical portion of the U.S. market. The stricter documentation requirements under this model reduce flexibility for community-based kyphoplasty and may influence payer behavior beyond the pilot states. In Europe, reimbursement parity between kyphoplasty and vertebroplasty in parts of Spain and Italy limits premium pricing, pushing manufacturers to rely more on health economic evidence and real-world data.

Cement Leakage and Revision Risk Concerns

Cement leakage remains a key clinical challenge in the kyphoplasty market, with 2025 meta-analysis data showing leakage rates between 25% and 65%, depending on technique, fracture shape, and imaging protocol. A 2025 study identified hypertension, vertebral collapse degree, cortical continuity, and cement volume as significant predictors, linking the issue to anatomy and procedural control. Additionally, a 2025 meta-analysis of 5,673 patients associated vertebral augmentation with a 2.29 odds ratio for adjacent-level fracture risk, increasing follow-on care costs and complicating borderline case justifications. Robotic workflows have reduced leakage rates, with a 2025 study reporting 5.8% for robot-assisted kyphoplasty compared to 19.2% for fluoroscopy-guided procedures, driving demand for advanced smart injection systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Instrument Precision Is Reshaping The Device Mix

In 2025, Kyphoplasty Balloon Catheters accounted for 31.89% of the kyphoplasty market, maintaining their position as the leading product category. These catheters are essential for cavity creation in every procedure and benefit from single-use economics, ensuring a recurring revenue stream for manufacturers. Bone cement and cement mixing systems, while smaller individually, form a consumable chain that supports kit-level pricing and bundling strategies. Companies like Globus Medical and Medtronic exemplify this approach with integrated procedural systems.

Kyphoplasty Instruments are projected to grow at a 6.10% CAGR from 2026 to 2031, driven by the increasing adoption of navigation and robotic guidance in pedicle access workflows. A 2025 study highlighted that robot-assisted percutaneous kyphoplasty reduced fluoroscopy counts to 6.8 per procedure compared to the conventional average of 39.4. Bone access devices are advancing, particularly for challenging thoracic anatomy, while accessories like biopsy tools are gaining relevance as oncology care integrates ablation and augmentation workflows. This shift favors companies offering integrated procedure kits over standalone components.

By Indication: Oncology Use Is Expanding Faster Than The Core Base

Osteoporotic vertebral compression fractures represented 58.78% of the kyphoplasty market in 2025, driven by a broad, aging patient pool. Early intervention supports procedure volume, with a 2025 study showing better outcomes when kyphoplasty is performed within four weeks of fracture onset. Traumatic vertebral compression fractures, though smaller, benefit from the procedure’s role in restoring structural support for patients unsuitable for open fixation.

Neoplastic vertebral compression fractures are expected to grow at a 5.95% CAGR through 2031, supported by wider use in multiple myeloma and solid tumor populations like breast, lung, and prostate cancers. Kyphoplasty offers significant pain relief for malignancy-related fractures, particularly for frail patients. Companies are integrating ablation systems with cement augmentation, making oncology a key area for future device differentiation through workflow integration.

By End User: Outpatient Migration Is Changing Volume Flow

In 2025, hospitals held 67.35% of the kyphoplasty market share, remaining the dominant end-user due to their management of complex fractures and oncology cases. Regulatory requirements in some European systems and structured oversight in regions like Japan, where an Osaka clinic reported 41 cases in 2024 compared to 26 in 2023, further reinforce hospital adoption. Specialty clinics, while smaller, are gaining relevance in areas with growing private-pay penetration.

Ambulatory surgery centers are projected to grow at a 6.55% CAGR through 2031, supported by a 2.9% CMS payment update for 2025, which increased total ASC payments to nearly USD 7.4 billion. States like Florida, Texas, and Arizona lead ASC adoption due to large Medicare-age populations and favorable outpatient trends. Day-surgery kyphoplasty models with robotic-assisted local anesthesia align with outpatient economics, driving demand for compact, disposable systems tailored for ASC use.

Geography Analysis

In 2025, North America accounted for 38.95% of the kyphoplasty market share, maintaining its position as the largest regional base. The U.S. significantly contributed to this dominance, with nearly 750,000 new osteoporotic vertebral compression fractures annually and consistent procedure volumes supported by Medicare coverage under CPT codes 22513 to 22515. Despite the WISeR model introducing tighter review standards in select states in 2026, the region remains robust. Medtronic leads the market through its Kyphon brand, facing competition from other device manufacturers. Canada is progressing in outpatient migration, while Mexico, though underpenetrated, is gaining relevance as private hospitals invest in minimally invasive spine capabilities.

Europe is the second-largest regional cluster in the kyphoplasty market, with Germany, the U.K., France, Italy, and Spain forming the core procedure base. Germany’s improved reimbursement and coding processes are aiding hospitals in capturing claims more consistently. Clinical evidence highlights the need for timely intervention, as an initial vertebral fracture increases the risk of subsequent fractures within two years. However, reimbursement parity between kyphoplasty and vertebroplasty in parts of Southern Europe limits the premium positioning of balloon-based systems.

Asia-Pacific is the fastest-growing region in the kyphoplasty market, projected to expand at a 7.88% CAGR through 2031. Japan’s 2025 insurance expansion for treating multiple vertebral bodies in one session is expected to improve per-patient economics and reduce repeat admissions. India benefits from the growth of private tertiary care hospitals, while South Korea strengthens its position with established spine surgery training programs. The Middle East, Africa, and South America remain in early stages, with volumes concentrated in GCC hospital systems and Brazil’s private hospitals, where adoption depends on trained surgeons and manufacturer-backed education programs.

Competitive Landscape

Medtronic leads the moderately concentrated kyphoplasty market through its Kyphon franchise and vertebral augmentation portfolio. Its strong position is driven by brand recognition, a broad procedural range, and payer acknowledgment in U.S. medical policies. In FY25, Medtronic's spine segment revenue reached USD 2,424.5 million, reflecting a 4.2% year-over-year growth. The company has strategically linked Kyphon with OsteoCool to strengthen its presence in oncology-related vertebral procedures, enabling it to address cases involving pain relief, ablation, and cement augmentation.

Globus Medical has intensified competition with investments in platforms like KYPHONEX and Apollo balloon offerings, enhancing its position in procedure kits and pressure-control designs. Johnson & Johnson Services, through DePuy Synthes, remains influential in areas where cement formulation and procedural compatibility are key factors. Stryker, in April 2025, divested its U.S. spinal implants business while retaining its Interventional Spine, Neurotechnology, and Enabling Technologies divisions, signaling a strategic focus on vertebral augmentation over implants-only solutions.

Smaller companies are differentiating through niche innovations. Osseon Therapeutics emphasizes steerable balloon access, Teknimed SAS focuses on specialty cement formulations, and Amber Implants promotes a minimally invasive support system for fracture patterns. Amber Implants received FDA 510(k) clearance for its VCFix Spinal System in September 2025 and launched its U.S. pilot in early 2026, marking a significant entry in vertebral fracture stabilization. Smart cement delivery, with real-time pressure monitoring, remains an untapped area that could address leakage issues and expand kyphoplasty adoption. Competition now centers on improving workflow precision, safety, and expanding use cases in the market.

Kyphoplasty Industry Leaders

Medtronic plc

Stryker Corporation

Globus Medical, Inc.

Cook Medical LLC

Merit Medical Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: VB Spine LLC expanded its global manufacturing footprint by acquiring Stryker's spine implant facility in Cestas, France, following its April 2025 formation through the acquisition of Stryker's US spinal implants business.

- September 2025: Amber Implants received FDA 510(k) clearance for its VCFix Spinal System and initiated its US commercial pilot in early 2026 while expanding its pivotal trial in the US.

- April 2025: Stryker Corporation sold its US spinal implants business to Viscogliosi Brothers LLC, forming VB Spine LLC and signaling Stryker's strategic focus on procedural platforms.

Global Kyphoplasty Market Report Scope

As per the scope of the report, kyphoplasty is a minimally invasive procedure used to treat painful vertebral compression fractures, which are often caused by osteoporosis, spinal tumors, or trauma. Its primary goal is to stabilize the collapsed bone, restore lost spinal height, and provide immediate pain relief.

The kyphoplasty market is segmented by product type, indication, end-user, and geography. By product type, the market includes balloon catheters, bone access devices, bone cement, cement mixing systems, instruments, and other products. By indication, the market is categorized into osteoporotic vertebral compression fractures, neoplastic vertebral compression fractures, traumatic vertebral compression fractures, and other vertebral compression fracture indications. By end-user, the market is segmented into hospitals, ambulatory surgery centers, and specialty clinics. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Kyphoplasty Balloon Catheters |

| Kyphoplasty Bone Access Devices |

| Kyphoplasty Bone Cement |

| Kyphoplasty Cement Mixing Systems |

| Kyphoplasty Instruments |

| Others |

| Osteoporotic Vertebral Compression Fractures |

| Neoplastic Vertebral Compression Fractures |

| Traumatic Vertebral Compression Fractures |

| Other Vertebral Compression Fracture Indications |

| Hospitals |

| Ambulatory Surgery Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Kyphoplasty Balloon Catheters | |

| Kyphoplasty Bone Access Devices | ||

| Kyphoplasty Bone Cement | ||

| Kyphoplasty Cement Mixing Systems | ||

| Kyphoplasty Instruments | ||

| Others | ||

| By Indication | Osteoporotic Vertebral Compression Fractures | |

| Neoplastic Vertebral Compression Fractures | ||

| Traumatic Vertebral Compression Fractures | ||

| Other Vertebral Compression Fracture Indications | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the kyphoplasty space in 2026?

The kyphoplasty market size is USD 732.61 million in 2026 and is forecast to reach USD 968.89 million by 2031 at a 5.75% CAGR.

What is driving procedure demand the most?

The strongest support comes from the rising burden of osteoporotic vertebral compression fractures, with 7.5 million incident vertebral fractures reported globally in 2021.

Which product category leads revenue today?

Kyphoplasty Balloon Catheters led product demand with a 31.89% share in 2025 because they remain essential single-use consumables in every procedure.

Which clinical use is growing the fastest?

Neoplastic vertebral compression fractures are the fastest-growing indication, projected to expand at a 5.95% CAGR through 2031 as oncology-linked care pathways widen.

Which end-user setting is expanding most quickly?

Ambulatory surgery centers are growing the fastest, with a 6.55% CAGR through 2031, supported by outpatient reimbursement and workflow gains.

Which region offers the strongest growth outlook?

Asia-Pacific has the strongest growth outlook, with a projected 7.88% CAGR through 2031, supported by reimbursement changes in Japan and fracture burden growth in China.

Page last updated on: