Knee Replacement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

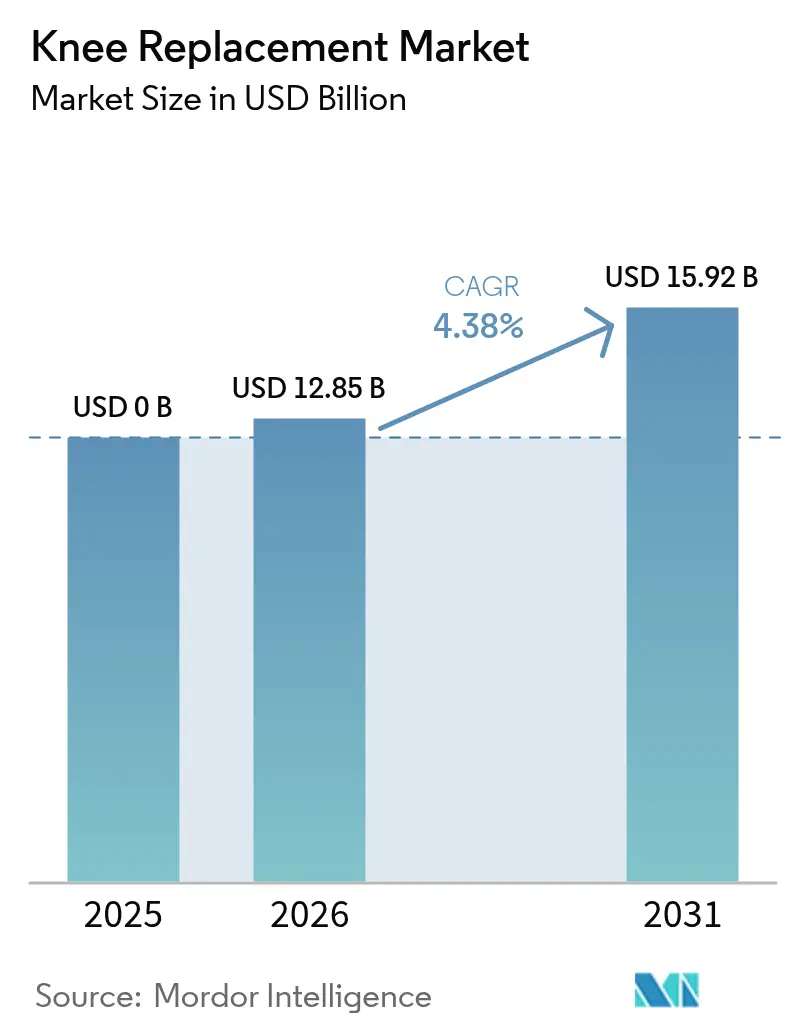

| Market Size (2026) | USD 12.85 Billion |

| Market Size (2031) | USD 15.92 Billion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

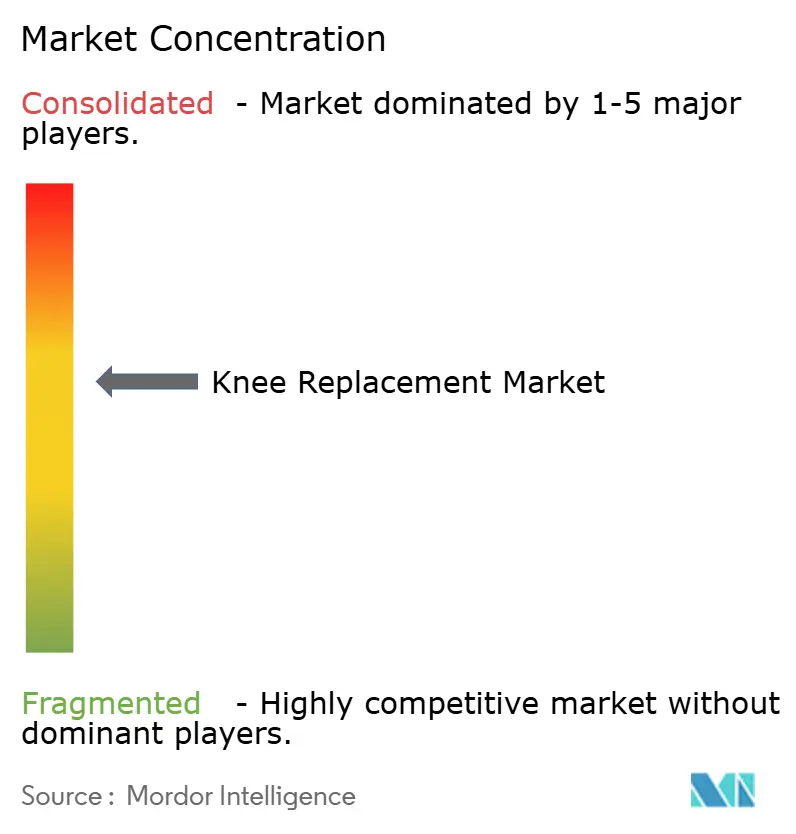

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Knee Replacement Market Analysis by Mordor Intelligence

The Knee Replacement Market size was valued at USD 12.31 billion in 2025 and estimated to grow from USD 12.85 billion in 2026 to reach USD 15.92 billion by 2031, at a CAGR of 4.38% during the forecast period (2026-2031).

Growth rests on a confluence of factors: the rapid expansion of the ≥65-year population, escalating obesity prevalence, and steady improvements in implant design and surgical techniques. Technology adoption is shifting the field toward data-guided precision, with robotic platforms gaining traction among both high-volume hospitals and ambulatory surgical centers. Parallel reimbursement reforms now reward same-day discharge protocols, intensifying competition between inpatient and outpatient settings. Manufacturers are responding through product line extensions, platform acquisitions, and greater focus on sustainability commitments, moves that influence surgeon preferences and purchasing decisions in every major geography.

Key Report Takeaways

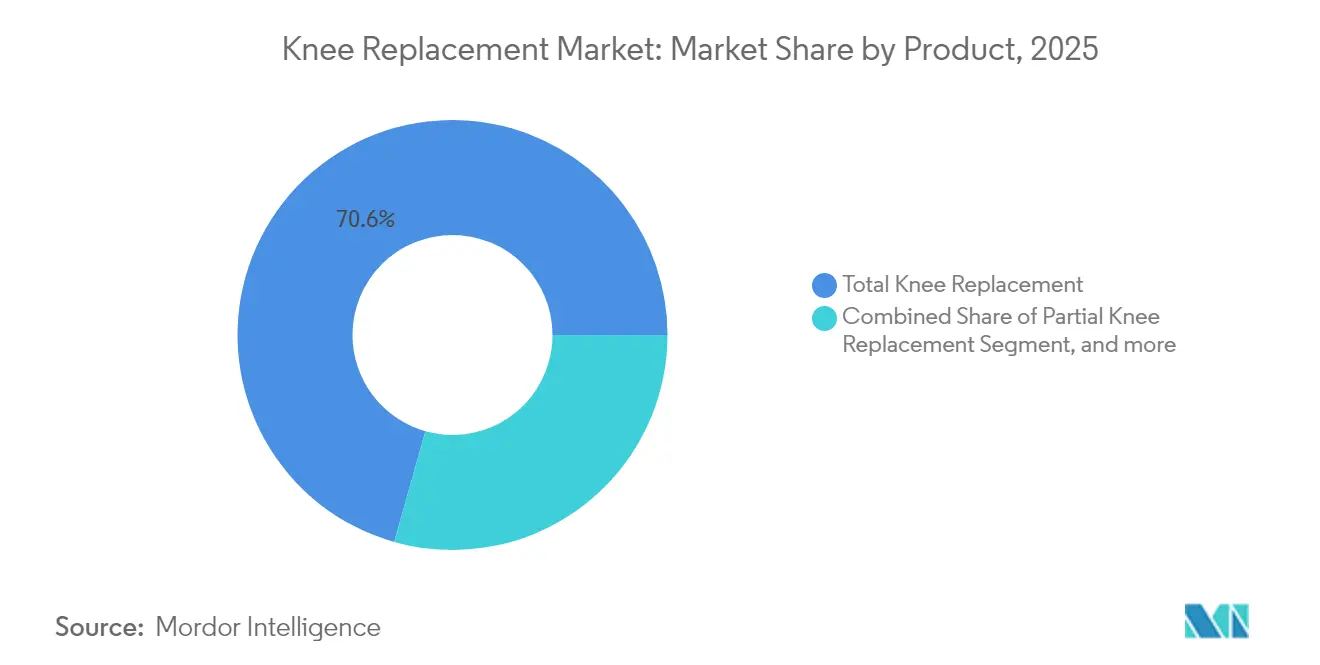

- By product, total knee systems captured 70.63% of knee replacement market share in 2025 and are tracking a 5.54% CAGR to 2031.

- By surgical technology, manual techniques held 52.12% revenue share in 2025, whereas robotic-assisted procedures are expanding at an 11.05% CAGR through 2031.

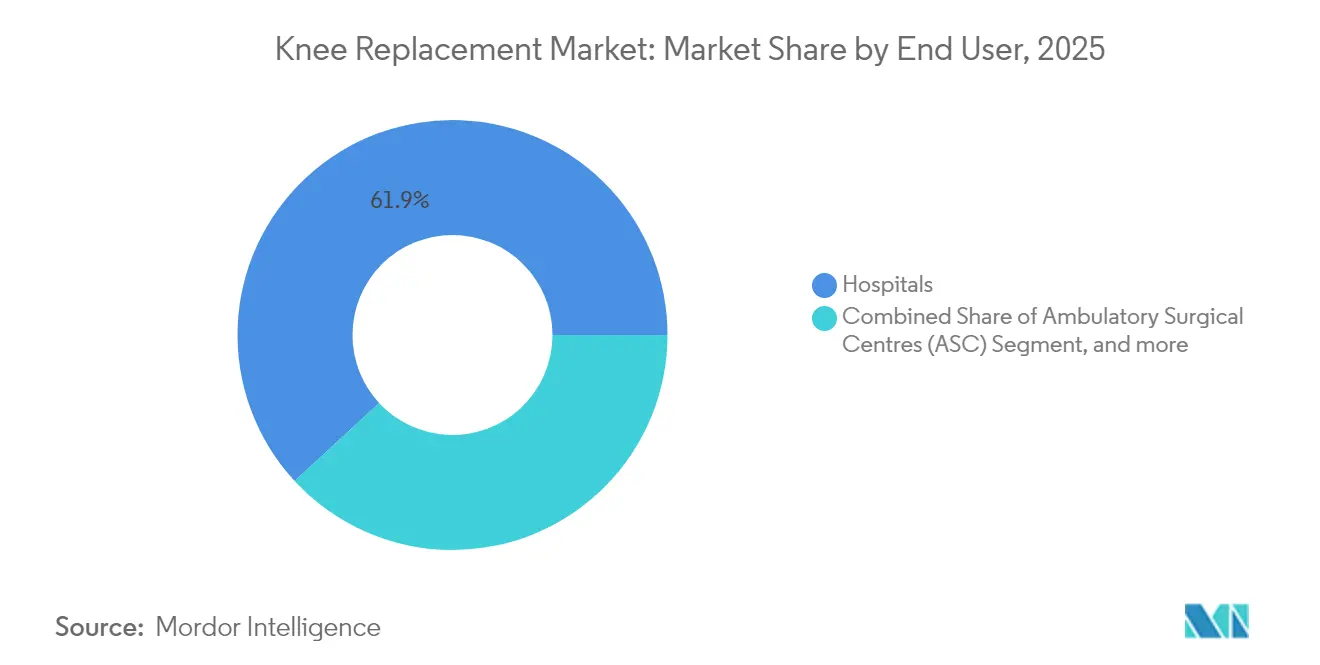

- By end user, hospitals controlled 61.88% of the knee replacement market size in 2025, while ambulatory surgical centers are forecast to grow at 8.73% CAGR to 2031.

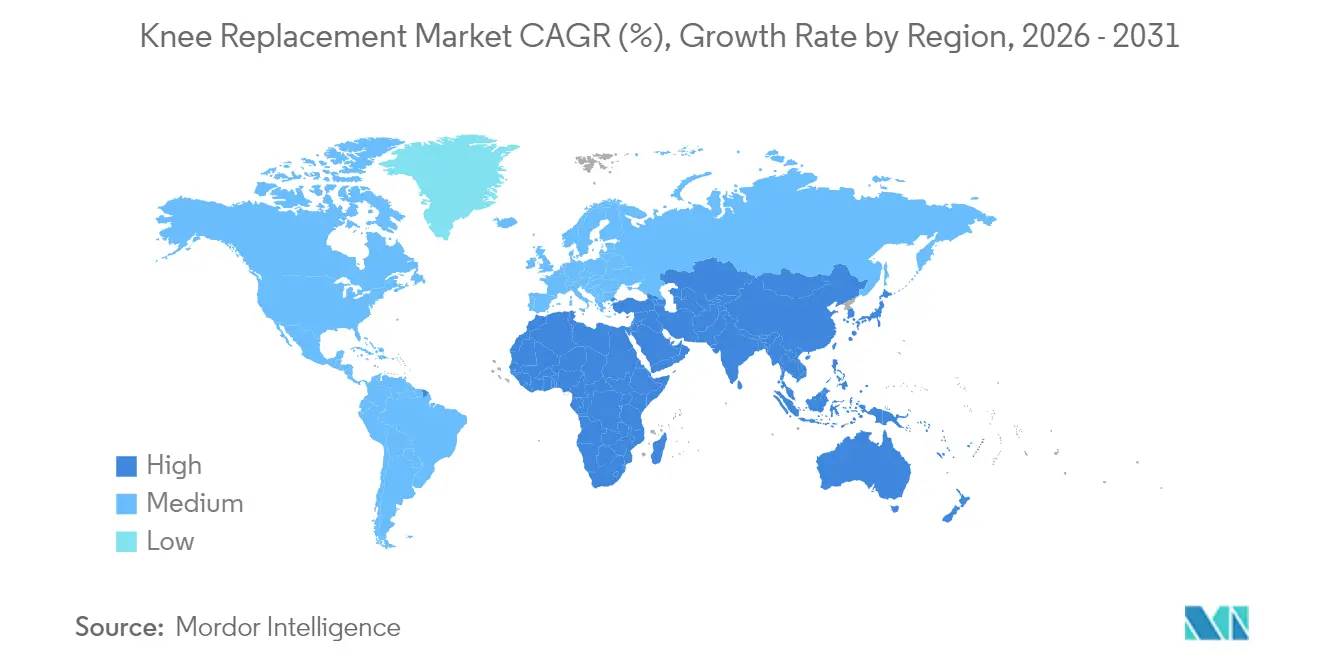

- By geography, North America commanded 40.62% of 2025 revenue, whereas Asia-Pacific is projected to post a 14.62% CAGR during the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Knee Replacement Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing and Obese Population Growth | +1.8% | Global; strongest in North America & Europe | Long term (≥ 4 years) |

| Rapid Adoption of Robotic-Assisted Total Knee Replacement | +1.2% | North America & Europe core; Asia-Pacific emerging | Medium term (2-4 years) |

| Expansion of Outpatient (ASC) Reimbursement Programs | +0.9% | North America dominant; selective European markets | Short term (≤ 2 years) |

| Arthroplasty Capacity Expansion in Emerging Markets | +0.7% | Asia-Pacific core; Latin America spill-over | Long term (≥ 4 years) |

| Customised, 3D-Printed Implant Technologies | +0.4% | Global; early adoption in developed markets | Medium term (2-4 years) |

| Breakthroughs in Military-Grade Polyethylene Longevity | +0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing and Obese Population Growth

Rising life expectancy is intersecting with sedentary lifestyles to boost osteoarthritis incidence and accelerate knee arthroplasty demand, reinforcing long-term expansion in the knee replacement market. Utilization remains highest in the 65-74 cohort, yet the 75-84 group records the fastest growth, while women in high-income markets undergo total knee procedures at rates nine times higher than men.[1]Clinical Orthopaedics Research Group, “Age and Gender Trends in Total Knee Arthroplasty,” pubmed.ncbi.nlm.nih.gov Increasing implant durability now supports interventions in patients in their early 50s, enlarging the addressable pool and shifting revision surgery burdens further into the future.

Rapid Adoption of Robotic-Assisted Total Knee Replacement

Clinical studies now link robotic assistance to tighter ligament balancing, fewer alignment outliers, and higher early-stage patient-reported outcome scores, strengthening the technology’s role within the knee replacement market.. Stryker’s Mako platform has surpassed 1.5 million cumulative procedures, with 95% of surveyed surgeons citing enhanced intra-operative confidence.[2]Stryker Corporation, “Mako SmartRobotics Surgeon Survey Results,” stryker.com Johnson & Johnson’s VELYS system secured FDA clearance in 2024 for unicompartmental knees without CT-based planning, challenging incumbent dominance and spurring a technology race centered on workflow integration and cost-effectiveness.

Expansion of Outpatient (ASC) Reimbursement Programs

The Centers for Medicare & Medicaid Services extended coverage for total knee arthroplasty in ambulatory settings, triggering a surge of ASC investment. Same-day discharge protocols supported by regional anesthesia and multimodal pain regimens deliver infection and readmission rates comparable with inpatient care while improving facility throughput.[3]Smith+Nephew, “ASC Efficiency Data in Robotic Knee Surgery,” smith-nephew.com This trend is particularly pronounced in the United States, where ASC penetration is accelerating, but European markets are beginning to adopt similar models as healthcare systems seek to optimize resource utilization and reduce patient wait times, further reinforcing growth momentum in the knee replacement market.

Arthroplasty Capacity Expansion in Emerging Markets

Urban hospital chains across China, India, Brazil, and Indonesia are scaling joint centers with onsite rehabilitation, tele-monitoring, and bundled payment models, supporting procedural growth in the knee replacement market. Capacity in tier-2 Chinese cities has more than doubled since 2024, although rural penetration still lags markedly, underscoring opportunities for mobile surgical units. However, the expansion is not uniform, with urban centers leading adoption while rural areas lag significantly, creating opportunities for telemedicine and mobile surgical units to bridge access gaps.

Restraints Impact Analysis of Knee Replacement Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-Cap Regulations in China and India | -1.1% | Asia-Pacific; global pricing spill-over | Short term (≤ 2 years) |

| Economic Burden of Revision Surgeries | -0.8% | Global; highest in ageing populations | Medium term (2-4 years) |

| Environmental Scrutiny of Implant Metals' Carbon Footprint | -0.4% | Europe & North America | Medium term (2-4 years) |

| Legal Risks Related to Intellectual Property for Custom Implants | -0.3% | Global; innovation hubs most exposed | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price-Cap Regulations in China and India

China’s volume-based procurement framework cut average knee implant prices by 50%, with devices accounting for 93.21% of total inpatient savings. India’s National Pharmaceutical Pricing Authority imposed caps deemed misaligned with R&D costs, prompting ongoing trade disputes. Manufacturers now segment portfolios into premium and value tiers to shield innovation budgets against mandated markdowns in the global knee replacement market.

Economic Burden of Revision Surgeries

Revision procedures, often 2-3 times costlier than primaries, strain provider margins and public payers, especially as younger, more active recipients raise lifetime revision probability. The mismatch between patient expectation and implant lifespan drives litigation spikes and higher malpractice premiums.This dynamic is particularly problematic as the patient population skews younger due to improved implant longevity expectations, creating a mismatch between patient expectations and clinical reality that manifests in increased litigation risk and insurance costs for healthcare providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Knee Replacement Market Segment Analysis

By Product:

Total Knee Dominance Drives InnovationTotal knee replacement procedures command 70.63% market share in 2025 while simultaneously leading growth at 5.54% CAGR through 2031, creating a rare market dynamic where the dominant segment also drives expansion. This phenomenon reflects the procedure's versatility in addressing various pathologies and the continuous innovation in implant design and surgical techniques. Partial knee replacement procedures are gaining traction as robotic assistance improves precision and outcomes, with Johnson & Johnson's VELYS system receiving FDA clearance for unicompartmental procedures in 2024, addressing the historical underutilization of bone-preserving techniques.

Patellofemoral replacement represents a niche but growing segment within the knee replacement market, particularly for younger patients with isolated anterior knee pain, while revision and complex knee replacement procedures are experiencing increased demand as the installed base of primary implants ages. The revision segment faces unique challenges, including bone loss management and component compatibility issues, driving innovation in modular implant systems and custom 3D-printed solutions. Zimmer Biomet's Oxford Cementless Partial Knee, approved by the FDA in 2024 as the only cementless partial knee implant in the United States, demonstrates 94.1% implant survival at 10 years, significantly exceeding average partial knee performance metrics.

By Surgical Technology:

Robotic Revolution AcceleratesManual surgical techniques maintain 52.12% market dominance in 2025, but robotic-assisted procedures are experiencing explosive growth at 11.05% CAGR, fundamentally reshaping surgical training and patient expectations. Stryker's Mako platform has performed over 1.5 million procedures globally, with the company reporting 8.4% organic growth in U.S. knee procedures driven by robotic adoption. The technology's value proposition extends beyond precision to include real-time soft tissue assessment, improved implant positioning, and reduced revision rates, justifying the significant capital investment required for adoption across the knee replacement market.

Patient-specific instrumentation (PSI) occupies a middle ground between manual and robotic approaches, offering customization benefits without requiring major capital investments, though clinical evidence remains mixed regarding superior outcomes compared to conventional techniques. Computer-navigated surgery represents an earlier generation of precision technology that continues to evolve, particularly in markets where robotic systems are not economically viable. The competitive dynamics are intensifying as Johnson & Johnson's VELYS system challenges Stryker's robotic dominance, while Smith+Nephew's CORI platform focuses on AI-powered planning and visualization capabilities.

By End User:

ASC Growth Challenges Hospital HegemonyHospitals maintain 61.88% market share in 2025, leveraging their comprehensive infrastructure and ability to handle complex cases, but ambulatory surgical centers are expanding rapidly at 8.73% CAGR as reimbursement policies and surgical techniques enable outpatient procedures. The ASC model offers superior efficiency metrics, with reduced overhead costs, specialized workflows, and improved patient satisfaction scores, particularly when combined with robotic assistance that enables same-day discharge protocols. This shift represents a fundamental restructuring of healthcare delivery economics rather than merely a cost-cutting measure.

Orthopedic specialty clinics occupy a growing niche, particularly in markets with fragmented healthcare systems, offering focused expertise and streamlined patient pathways. These facilities often serve as early adopters of new technologies due to their specialized focus and ability to make rapid implementation decisions. The competitive dynamics between end-user segments are driving innovation in patient selection criteria, anesthesia protocols, and post-operative care pathways, with successful ASC models demonstrating that carefully selected patients can achieve equivalent or superior outcomes compared to traditional hospital-based procedures while reducing overall system costs across the knee replacement market.

Geography Analysis

North America Knee Replacement Market

North America led the knee replacement market with 40.62% revenue in 2025, driven by more than 790,000 annual procedures in the United States, strong technology adoption, and robust private-payer coverage. Canada’s publicly funded system introduces wait-time constraints, prompting outbound medical travel to U.S. and Mexican facilities. Mexico capitalizes on that flow, expanding private orthopedic institutes that market US-trained surgeons and bundled robotics packages. Payer pressure to curtail inpatient lengths of stay is sharpening focus on value-based purchasing, while device excise taxes remain under legislative review.

Europe Knee Replacement Market

Europe displays a mature yet heterogeneous profile. Germany retains the highest procedure volume, but reimbursement cuts in France trimmed implant prices by 25%, squeezing provider margins and slowing premium adoption. The United Kingdom’s NHS elective backlog spurs contracting with private hospitals to reach activity targets. Southern European nations, helped by European Investment Bank funding, modernize operating theaters but run lean implant formularies to control costs. Eastern European markets start from lower baselines; EU cohesion funds and skill-transfer partnerships speed orthopedic ward upgrades. Environmental procurement criteria such as carbon-footprint disclosures, pioneered in Scandinavia, are gaining cross-border traction and could reshape vendor qualification standards.

APAC Knee Replacement Market

Asia-Pacific contributes the highest growth at a 14.62% CAGR and is set to transform the global knee replacement market by 2031. China’s volume-based procurement halved device prices yet did not dent procedure uptake; hospitals instead chase throughput to offset lower margins. Japan registers 82,304 annual primary knees, with ceramic-on-ceramic bearings reflecting cultural aversion to metal ions. South Korea’s procedure rate grew 407% over the past decade, supported by national insurance and aggressive marketing of minimally invasive methods. India balances burgeoning demand against price caps, stimulating domestic implant manufacture albeit with constrained innovation budgets. Australia’s injury incidence of 83.9 per 100,000 males illuminates rising sports-related knee trauma, feeding pipeline demand even as government cost-containment tightens.

Regulatory Landscape

Knee implants and associated surgical instrument kits fall under high-scrutiny orthopedic device regimes that shape time-to-market and portfolio strategy. In the United States, the FDA continues to regulate knee joint prosthesis systems under established classification pathways and emphasizes conformity to recognized consensus standards used for performance and safety testing, including ISO 21536 and multiple ASTM methods for knee implant evaluation. These recognized standards and guidance expectations influence how manufacturers plan verification for design changes such as new bearing materials, porous coatings, and cementless fixation variants.

In Europe, EU MDR transition requirements materially affect Class III implantables, including patient-matched and custom-made configurations, with May 26, 2026 as a mandatory certification deadline for Class III custom-made implantable devices. Notified Body review capacity constraints, cited as multi-month review cycles, continue to act as a gating factor for legacy portfolio recertification and new product introductions. In China, the NMPA is tightening and modernizing oversight for high-end medical devices through lifecycle-focused measures, including Announcement No. 63 of 2025, while continuing to approve advanced designs such as knee systems using additive-manufactured porous structures. This reinforces the need for localized compliance, testing, and documentation readiness.

Competitive Landscape

The knee replacement market is moderately concentrated, with Zimmer Biomet, Stryker, and Johnson & Johnson DePuy Synthes occupying the top tier through broad portfolios and entrenched surgeon relationships. Zimmer Biomet recorded USD 3.17 billion in 2024 knee sales and secured FDA clearance for the Oxford Cementless Partial Knee, the only cementless partial implant available in the United States. Stryker, leveraging its Mako platform, reported 8.4% organic growth in U.S. knee procedures as hospitals scaled robotic fleets. Johnson & Johnson counters with its VELYS portfolio and surgeon-centric ecosystem that spans digital planning, implants, and post-operative monitoring.

Strategic transactions shape competitive borders. Zimmer Biomet’s pending acquisition of Paragon 28 adds foot-and-ankle adjacency and diversifies growth, while its collaboration with THINK Surgical bolsters robot portfolio breadth. Smith+Nephew focuses on CORI system enhancements, integrating AI planning and multimodal imaging to differentiate. Tier-two challengers, including Exactech and Medacta, capitalize on niche positioning and surgeon-consultant networks to advance custom implants.

Legal and sustainability vectors increasingly influence rivalry. Patent disputes over patient-specific cutting jigs and robotic kinematic algorithms intensify, with non-practicing entities exploiting intricate orthopedic patent thickets. Concurrently, European tenders mandate lifecycle carbon analyses, pushing vendors to adopt energy-efficient machining and expanded take-back programs for explants. As cost pressures mount, alliances with raw-material suppliers that guarantee low-carbon titanium and cobalt-chrome become competitive differentiators. The combined share of the leading five companies is estimated near 65%, underscoring moderate concentration and leaving space for disruptive entrants focused on niche anatomies or digital-only planning services.

Knee Replacement Industry Leaders

Corin Group

Zimmer Biomet

SurgTech Inc.

Smith & Nephew plc

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Knee Replacement Market Companies Covered in this Report

- Zimmer Biomet

- Stryker

- Johnson & Johnson

- Smiths Group

- B. Braun (Aesculap)

- Exactech

- Medacta Group

- MicroPort Orthopedics

- Medtronic

- Corin Group

- Conformis Inc.

- THINK Surgical

- Waldemar Link GmbH

- DJO Global

- United Orthopedic Corp.

- LimaCorporate

- Amplitude SAS

- Auxein Medical

- Arthrex

- SurgTech

Market Opportunities and Future Outlook

A near-term whitespace sits at the intersection of outpatient migration and simplified instrumentation, where device platforms that reduce tray count, sterilization burden, and operating room turnover can better match ambulatory surgical center workflows. Smith+Nephew pointed to this direction through its March 2026 Landmark Knee System announcement, which focused on tray-efficient designs aligned to ASC throughput needs. FDA activity in February 2026 for the Triathlon Total Knee System (Triathlon X3 medial stabilized tibial bearing insert) under 510(k) clearance also signals ongoing system-level iteration rather than single-component updates. With payer-driven site-of-care shifts already visible in the market, there is room for bundled implant plus enabling-technology offerings that support same-day discharge protocols.

Supply-chain and manufacturing capacity also remains an opportunity area, especially for OEMs and contract manufacturers supporting porous coatings, additive manufacturing, and patient-specific workflows. Autocam Medical broke ground in January 2026 on a USD 70 million, 100,000-square-foot expansion in Indiana to support orthopedic OEM capacity requirements. Croom Medical started construction in February 2026 on its 38,000-square-foot Advanced Centre of Orthopaedic Technologies in Ireland, integrating multi-material additive manufacturing and verticalized production. In June 2026, Croom Medical also brought patient-specific implant manufacturing in-house on ISO 13485:2016-certified lines. On the demand-creation side, Japan provides a proof point for differentiated materials and navigation-enabled workflows, with Advita Ortho reporting first clinical use of a next-generation knee platform in Japan in June 2026 featuring vitamin E-stabilized polyethylene and GPS navigation, supporting ongoing product segmentation around longevity, kinematics, and digital planning integration.

Recent Industry Developments in Knee Replacement Market

- February 2026: The European Union reached a key EU MDR milestone, with May 26, 2026 set as the mandatory certification deadline for Class III custom-made implantable devices, tightening compliance timelines for patient-matched and custom knee implant offerings. The deadline heightened the urgency of Notified Body scheduling and technical documentation readiness, influencing how manufacturers prioritize legacy recertification versus new launches in Europe.

- November 2025: Zimmer Biomet received U.S. FDA 510(k) clearance for ROSA Knee with OptimiZe, an enhanced version of its ROSA Knee System. The clearance strengthens Zimmer Biomet's competitive positioning in robotic-assisted knee replacement by expanding software-enabled capability that ties implants, planning, and intraoperative execution into a single workflow.

- October 2024: Corin Group received U.S. FDA 510(k) clearance for the Unity Knee medial constrained tibial insert, designed to work with the ApolloKnee robotic-assisted surgical platform. This expanded Corin's implant-platform integration options in the United States, supporting a differentiated approach where proprietary robotic applications are paired with compatible implant components to drive adoption.

Knee Replacement Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers the value of knee replacement performed through partial, total, and revision arthroplasty, and it includes the implant system and procedure-related disposable kits that are sold for the surgery.

Scope exclusions: It does not include non-surgical orthobiologic injections, standalone knee braces, or replacement procedures for joints other than the knee.

Segments Covered in This Report

- By Product

- Total Knee Replacement

- Partial Knee Replacement

- Patellofemoral Replacement

- Revision / Complex Knee Replacement

- By Surgical Technology

- Manual

- Robotic-Assisted

- Patient-Specific Instrumentation (PSI)

- Computer-Navigated

- By End User

- Hospitals

- Ambulatory Surgical Centres (ASC)

- Orthopaedic Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean fact base on procedure volumes, patient pools, and reimbursement signals, because these are the anchors that keep the demand model realistic. We relied on non-paywalled sources such as OECD health statistics, the US Centers for Disease Control and Prevention, the World Health Organization health data, and national health ministries and payer schedules where available. For medical device context, sources such as the US FDA device databases and recall notices were reviewed, along with peer-reviewed orthopedic journals that describe utilization and revision patterns.

After that, company filings, investor presentations, and reputable press were used to track product mix changes, pricing direction, and supply conditions for implant materials. We also used paid database subscriptions for company financials and intelligence, and for patent databases to spot technology shifts that can affect adoption over time. The sources mentioned above are illustrative and not exhaustive, and many other public references were also used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on validating model inputs that desk sources do not explain well, such as realistic implant ASP bands, revision share by setting, and how quickly new techniques move into routine practice. We spoke with a mix of implant manufacturers, distributors, orthopedic surgeons, hospital procurement, and ambulatory surgery center administrators across major regions. Follow-up questions were then used to close gaps, reconcile definitions, and confirm assumptions before finalizing the totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 17% | APAC: 39% |

| Mid tier: 52% | Functional/Unit leaders: 29% | EMEA: 36% |

| Smaller Players: 17% | Managers: 54% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where procedure incidence and treated-patient pools are reconstructed from epidemiology, age mix, and healthcare access, and then translated into annual knee replacement volumes by country and care setting. Those volumes are then converted into value using device and kit pricing ranges. The model adjusts for the mix of partial, total, and revision procedures, and for the typical implant component sets used.

To keep the math traceable, the model uses a short list of practical inputs, including osteoarthritis prevalence in older age groups, hospital and ambulatory surgery center share, revision rate trends, average implant system pricing by geography, and the adoption pace of enabling technologies such as robotic assistance, which can change procedure mix. Forecasts are produced using scenario analysis supported by expert views on elective surgery backlogs, payer coverage stability, and expected price movement, and then stress-tested against trend lines from recent historical procedure volumes.

Selective bottom-up checks are used to corroborate the totals, using supplier revenue splits, sampled ASP times volume logic, and distributor channel checks in markets where disclosure is limited. When direct data is missing for smaller countries, we fill gaps using proxy indicators such as orthopedic surgeon density and per-capita procedure rates from comparable health systems, followed by a consistency review at the regional level.

Data Validation & Update Cycle

Validation is done through repeated cross-checks that look for mismatches between procedure volumes, implied pricing, and the resulting market value. Where mismatches show up, they are investigated and corrected before the numbers are signed off. We also compare outputs with independent signals such as implant shipment direction, revision burden commentary in clinical literature, and reported orthopedic revenue trends, which helps flag unusual jumps that do not fit the demand story.

Before publication, the work is reviewed in steps, with assumption logs checked, calculations re-run, and unusual country splits discussed and corrected when needed. Reports are refreshed annually, and interim updates are made when major events materially change procedure volumes, pricing, or reimbursement. Right before delivery, an analyst does a fresh pass on key inputs so clients receive the most current view available.

Mordor Intelligence's Knee Replacement Market Size Compared With Other Published Estimates

Published market sizes for knee replacement often do not match because each publisher draws the market boundary differently and uses its own view on what should be counted as market revenue. Differences also show up when procedure volume sources vary, when pricing is modeled as list price versus realized price, and when the refresh timing captures different elective surgery recovery phases.

Procedure-volume checks from public health statistics and clinical utilization studies, combined with revision-rate signals and realistic implant ASP ranges validated in interviews, are what keep Mordor Intelligence's 2025 estimate tied to arthroplasty implants and disposable kits. This avoids counting surgical technology platforms and broader services that some publishers include.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.31 B (2025) | |

| Industry Publisher A | USD 11.06 B (2025) | This figure appears to apply a narrower revenue capture for the procedure bundle, and it can also reflect more conservative ASP assumptions and a different treatment of revision versus primary mix. |

| Industry Publisher B | USD 13.17 B (2025) | This estimate states a broader scope that can fold in surgical technology platforms and associated services, which expands the revenue pool beyond implants and disposable kits used in the surgery. |

The spread in the table is mainly explained by what gets included around the surgery and how pricing and mix are handled in the math. By keeping the scope tied to arthroplasty implants and procedure-linked kits, and by forcing each region to reconcile to observed procedure activity, the final number stays transparent and repeatable for planning.

Key Questions Answered in the Report

How big is the knee replacement market in 2026?

The knee replacement market size reached USD 12.85 billion in 2026 and is projected to climb to USD 15.92 billion by 2031 at a 4.38% CAGR.

Which product segment leads revenue?

Total knee systems held 70.63% of knee replacement market share in 2025 and remain the primary revenue generator through 2031.

Is robotic surgery overtaking manual knee replacement procedures?

Manual techniques still dominate, yet robotic-assisted cases are expanding at 11.05% CAGR and are on track to match manual volumes in early next decade.

Why are ambulatory surgical centers gaining popularity for knee replacements?

Favorable reimbursement, reduced infection risk, and same-day discharge protocols drive ASC growth, which is expected to outpace hospital settings at 8.73% CAGR.

Which region offers the fastest growth opportunity?

Asia-Pacific leads with a 14.62% CAGR owing to healthcare infrastructure upgrades, rising disposable income, and supportive procurement reforms.

What is the outlook for revision knee surgeries?

Revision volumes will rise as younger patients undergo primaries sooner, but high costs and complex clinical profiles continue to challenge health systems and manufacturers.

Page last updated on: