Surgical Lights Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 2.62 Billion |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

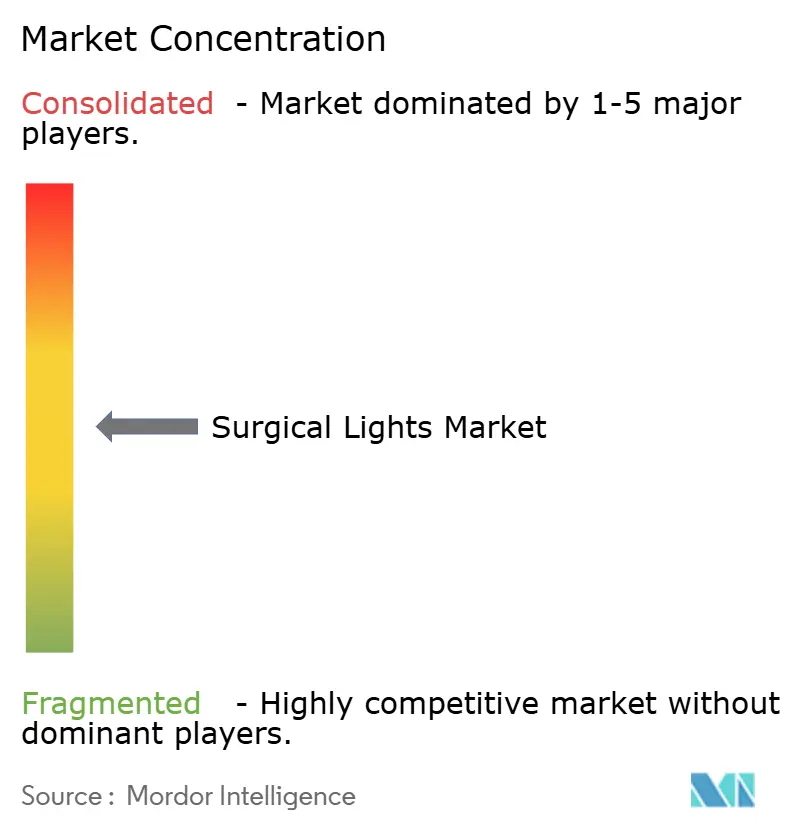

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Lights Market Analysis by Mordor Intelligence

The surgical lights market size was valued at USD 1.91 billion in 2025 and estimated to grow from USD 2.01 billion in 2026 to reach USD 2.62 billion by 2031, at a CAGR of 5.43% during the forecast period (2026-2031). The transition from halogen to high-efficiency LED luminaires sits at the center of this growth because LEDs cut power consumption, reduce heat, last 30,000-50,000 hours, and comply with mercury-phase-out regulations. Greater surgical volumes in hybrid operating rooms, government capital allocations that favor ambulatory surgery center (ASC) builds, and the integration of artificial intelligence (AI) with 4K and augmented-reality imaging further lift demand for precision lighting. Rising healthcare infrastructure projects in India, China, and Southeast Asia create additional momentum, while North America’s reimbursement updates and Europe’s sustainability mandates fuel steady replacement cycles. Although rare-earth element price swings and cybersecurity concerns add friction, manufacturers are offsetting these headwinds through diversified sourcing and FDA-compliant security protocols.

Key Report Takeaways

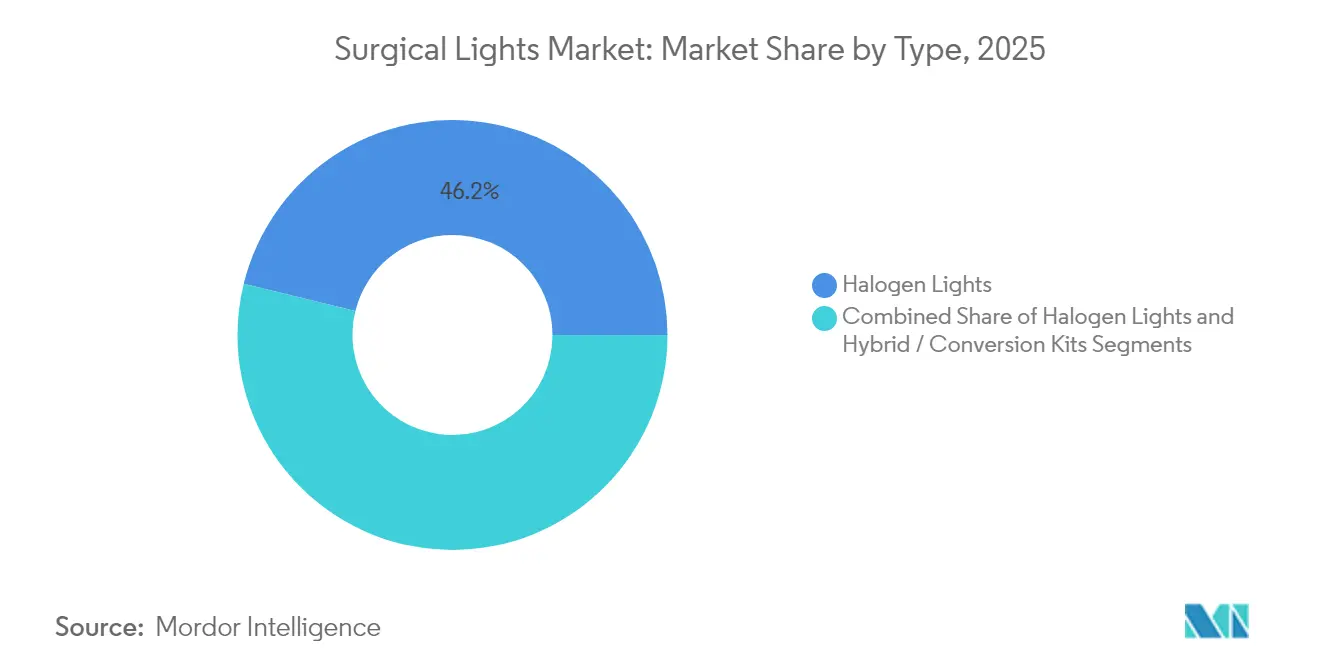

- By type, LED lights led with 53.84% of the surgical lights market share in 2025 and will outpace halogen at a 6.39% CAGR through 2031.

- By mounting configuration, ceiling-mounted systems held a 56.58% revenue share in 2025, whereas surgical headlights advanced fastest at a 6.88% CAGR to 2031.

- By light-intensity range, 100,001–160,000 lux products captured 48.76% share of the surgical lights market size in 2025; >160,000 lux units expand at an 7.82% CAGR to 2031

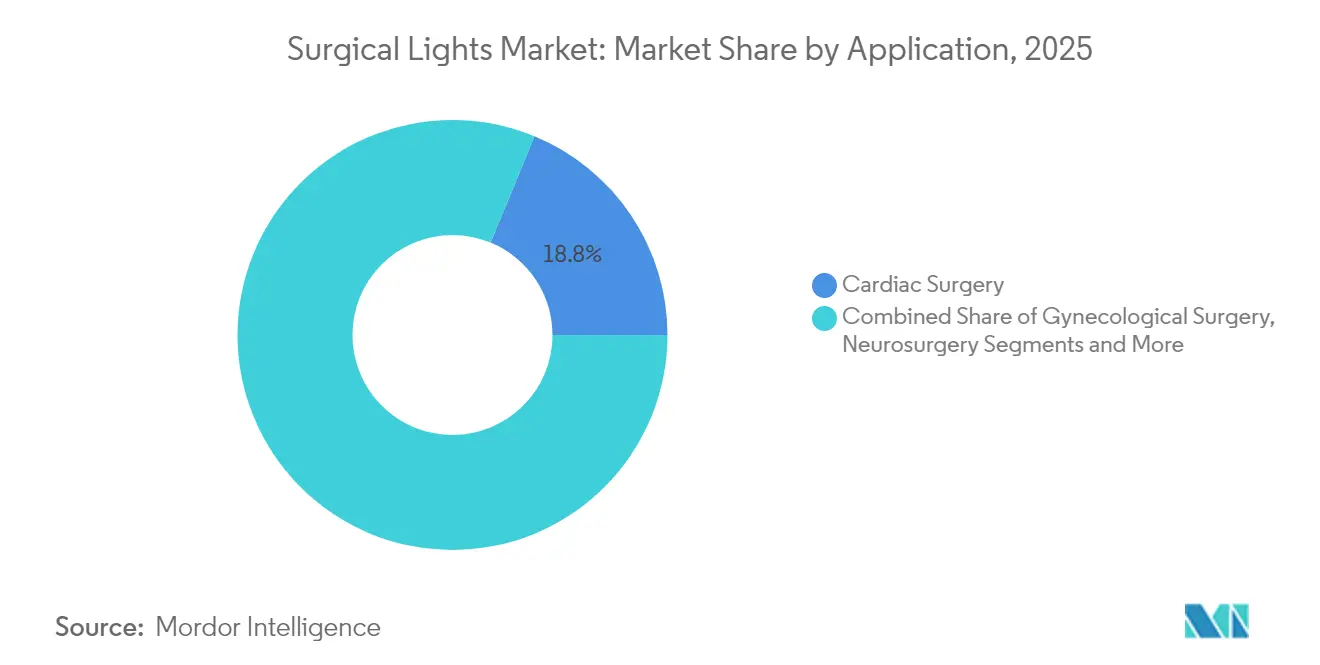

- By application, cardiac surgery led with 18.77% share of the surgical lights market size in 2025, while gynecological surgery posts a 8.63% CAGR to 2031.

- By end user, hospitals controlled 52.61% of the surgical lights market share in 2025; ASCs record the top CAGR at 7.74% through 2031.

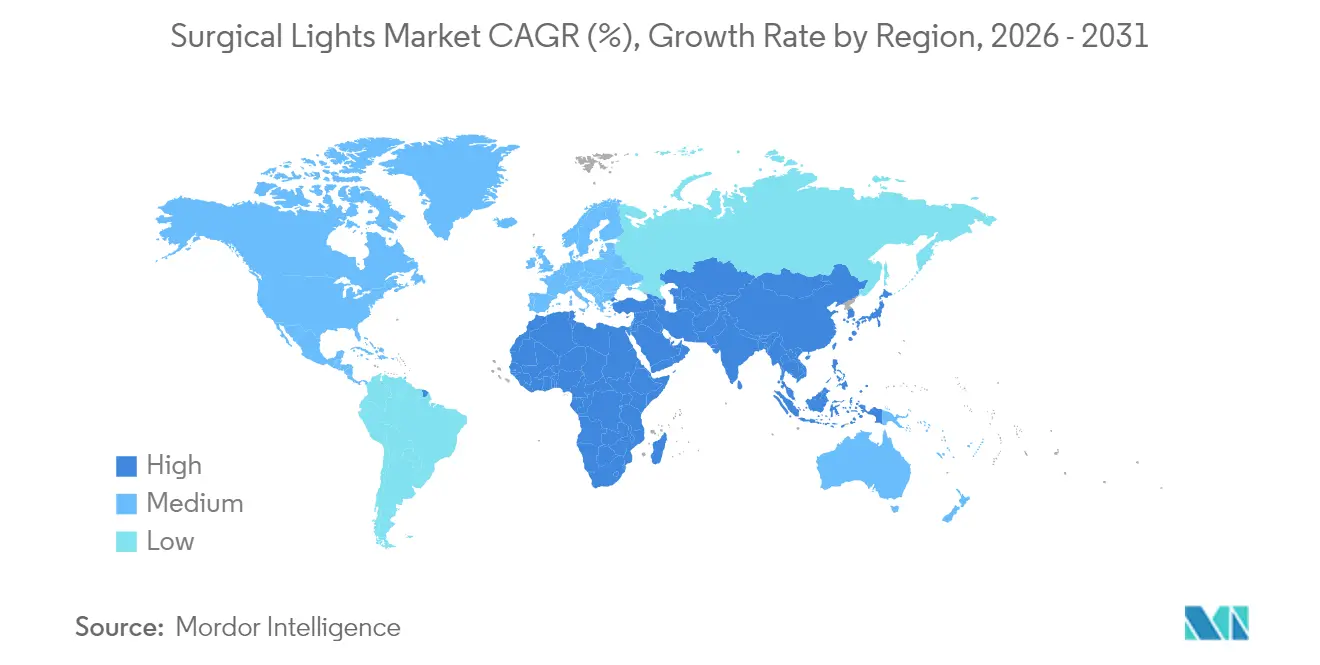

- By geography, North America commanded 32.02% revenue in 2025; Asia-Pacific grows fastest at an 8.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Surgical Lights Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Surgical Volumes In Multi-Disciplinary ORs | +1.2% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Rapid Shift To High-Efficiency LED & Hybrid Luminaires | +1.8% | Global, led by Europe & North America | Short term (≤ 2 years) |

| Government CAPEX Push For Ambulatory Surgery Centers | +0.9% | North America & Europe primary, APAC emerging | Medium term (2-4 years) |

| OR Integration With 4K/AR Imaging Demanding Higher CRI Lights | +0.7% | North America, Europe, developed APAC markets | Long term (≥ 4 years) |

| Sustainability Mandates Phasing-Out Halogen Fixtures | +0.6% | Europe leading, North America following | Short term (≤ 2 years) |

| AI-Driven Adaptive Lighting Improving Workflow & Outcomes | +0.4% | North America, select European markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising global surgical volumes in multi-disciplinary ORs

Hospitals are clustering complex specialties such as cardiovascular, neurosurgical, and orthopedic procedures inside hybrid suites that already handled 2.63 million robotic cases in the United States during 2024.[1]American Hospital Association, “3 Ways Robotic Surgery Is Changing Health Care This Year,” aha.orgSuch variety forces luminaires to supply uniform 360-degree coverage, respond to imaging cues, and maintain sterile touch-free control. Stryker’s Mako SmartRobotics platform, used in 1.5 million procedures across 45 countries, illustrates how imaging-guided robots and lighting now co-evolve. Growth is reinforced as Asian hospitals emulate North American perioperative workflows, escalating unit sales across the surgical lights market.

Rapid shift to high-efficiency LED and hybrid luminaires

The European Union banned most mercury-containing lamps in August 2023 and finishes the exemption period in February 2025, sending a clear market signal that accelerates substitution of halogen bulbs with LEDs. Modern systems such as STERIS HarmonyAIR A-Series reach 160,000 lux yet consume less energy and run 60,000 hours. Getinge’s Maquet Volista adds selectable color temperatures to accommodate tissue types during procedures. Facilities achieve both cost cuts and carbon reductions, which keeps LED adoption on an upward trajectory.

Government CAPEX push for ambulatory surgery centers

United States policy makers raised ASC payment rates 2.9% for 2025, an adjustment worth USD 7.4 billion and permitting 21 new outpatient codes.[2]Ambulatory Surgery Center Association, “CMS Releases 2025 Final Payment Rule,” asassociation.org Illinois approved a USD 13.2 million expansion that adds two ORs at Champaign Surgery Center, demonstrating how incentives turn quickly into brick-and-mortar growth.[3]Illinois Health Facilities and Services Review Board, “24-035 Champaign Surgery Center Expansion,” hfsrb.illinois.govEach new ASC requires compact, easy-to-maintain luminaires, boosting unit demand across the surgical lights market.

OR integration with 4K and AR imaging requiring higher CRI lights

Surgeons increasingly rely on 4K monitors, fluorescence imaging, and augmented-reality overlays that demand color-rendering indices above 95. Leica’s ARveo 8 microscope pairs with GLOW800 fluorescence, and Philips’ LumiGuide fiber-optic navigation calls for uniform spectral output. These specifications anchor premium sales even as price pressure grows elsewhere.

Restraints Impact Analysis of Surgical Lights Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensive Purchase & Maintenance Costs | -0.8% | Global, more pronounced in emerging markets | Medium term (2-4 years) |

| Long Replacement Cycles Hindering Repeat Sales | -0.6% | Global, particularly North America & Europe | Long term (≥ 4 years) |

| Cyber-Security Vulnerabilities In Connected OR Lighting | -0.4% | North America & Europe primarily | Short term (≤ 2 years) |

| Rare-Earth Supply Volatility For High-Power LEDs | -0.7% | Global, supply chain concentrated in China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-intensive purchase and maintenance costs

Premium LED arrays cost more upfront than halogen equivalents, and installation often requires ceiling reinforcements, wireless controls, and sterile-field integration. Facilities juggling competing priorities may postpone replacements, particularly in lower-income economies where foreign-exchange swings inflate import costs. Specialized service teams are also needed for calibration, adding to total cost of ownership.

Rare-earth supply volatility for high-power LEDs

China’s 2024 restrictions on gallium and germanium exports threaten up to USD 3.4 billion in U.S. GDP and have already pushed gallium prices sharply higher. OEMs are exploring recycling streams and alternate mineral sources, but near-term exposures persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Surgical Lights Market Segment Analysis

By Type:

LED units consolidate gains amid halogen legacyLED systems held 53.84% of 2025 revenue and are expanding at a 6.39% CAGR through 2031 as hospitals rush to comply with mercury-phase-out rules and cut operating costs. The long 30,000-50,000-hour lamp life lowers replacement labor, while integrated optics improve color rendering for delicate tissue work. Hybrid conversion kits appeal to budget-sensitive facilities that prefer retrofits over complete ceiling-boom swaps. Halogen’s installed base still accounts for 46.16% of units, mainly in mid-tier hospitals that stagger upgrades to match multi-year capital budgets.

Halogen continues to recede as procurement managers prioritize energy savings, sterilizable handles, and AI-driven beam control available only with LEDs. Stryker’s November 2024 Oculan platform illustrates the shift by offering Fly Eye optics that eliminate hotspots and respond to voice commands. Meanwhile, STERIS markets LED conversion kits that reuse existing ceiling arms, trimming upfront expense for community hospitals. Cumulatively, these trends move the global installed base closer to full LED saturation before 2031.

By Mounting Configuration:

Ceiling booms dominate while headlights surgeCeiling-mounted luminaires delivered 56.58% of 2025 revenue because they minimize shadows and integrate with camera booms and laminar airflow canopies. Their modular design supports hybrid-OR builds that combine open, endovascular, and imaging zones in one suite. Many tertiary centers specify dual-head configurations that reach 160,000 lux and ≥95 CRI for complex cardiac work.

Growth momentum now tilts toward surgeon-worn headlights, which post a 6.88% CAGR through 2031 as minimally invasive techniques spread. Battery-powered models such as MedLED Spectra deliver up to 300,000 lux, allowing uninterrupted focus during laparoscopic or spine cases. Mobile and wall units fill smaller procedure rooms but see slower uptake because ceiling rails are pre-installed in most new theaters. Vendors therefore offer mix-and-match mounting portfolios to suit everything from ambulatory centers to trauma bays.

By Light Intensity Range:

≥160,000-lux category acceleratesThe 100,001–160,000-lux band retained 48.76% share in 2025 thanks to its suitability for general surgery and orthopedics. Facilities value moderate power draw paired with high CRI, and many EMEA tenders still cap brightness in this zone to limit retinal fatigue. Even so, demand is tilting upward as robotics, 4K, and fluorescence imaging push precision limits.

Units exceeding 160,000 lux now clock an 7.82% CAGR because neuro and cardiac teams want brighter, sharper fields that enhance vessel identification. STERIS HarmonyAIR hits the 160,000-lux ceiling with 60,000-hour LEDs, and Stryker’s Chromophare reaches similar output while embedding automatic focus depth. Lower-intensity models below 100,000 lux remain common in exam rooms, yet their share keeps shrinking as outpatient centers standardize on higher-spec lights for broader procedural flexibility.

By Application:

Gynecology outpaces cardiac mainstayCardiac surgery commanded 18.77% of 2025 demand because open-heart and valve repairs need intense, deep-cavity illumination with precise color rendition for microvascular suturing. LED booms that auto-adjust to C-arm positions have become standard in these suites. Neurosurgery and ENT each account for mid-single-digit shares but rely on specialty optics such as narrow-beam spots and IR filters.

Gynecological procedures show the fastest 8.63% CAGR through 2031, propelled by robotic hysterectomies and myomectomies that need shadow-free cones and fluorescence compatibility. Orthopedic and trauma rooms upgrade to LED to reduce heat that can degrade bone cement, while minimally invasive and robotic sub-segments overlap across multiple specialties, amplifying the call for integratable, high-CRI luminaires.

By End User:

ASC build-out reshapes demand mixHospitals still own 52.61% of global revenue because they host highly specialized surgeries and possess the capital for ceiling booms integrated with anesthesia booms and monitor arms. University centers refresh every 7-10 years to keep pace with hybrid-OR standards and infection-control codes. Yet procurement cycles face scrutiny as CFOs weigh lighting against imaging or robotic upgrades.

Ambulatory surgery centers expand at 7.74% CAGR after CMS granted a 2.9% payment bump and added 21 outpatient codes for 2025. Investors favor compact LED rigs with removable sterile handles that suit quick room turnovers. Specialty clinics and dental ORs prioritize budget kits and wall mounts, opting for mid-range brightness that meets procedural needs while keeping acquisition costs below USD 15,000 per room.

Geography Analysis

North America Surgical Lights Market

North America remains the largest regional buyer with a 32.02% share. Strong reimbursement pathways and a mature installed base create a steady replacement rhythm, especially for ceiling LEDs integrated with robotic arms. Stryker’s November 2024 Oculan launch met immediate demand for AI-assisted beam control in U.S. tertiary hospitals.

APAC Surgical Lights Market

Asia-Pacific records an 8.09% CAGR as China, India, and Indonesia expand surgical capacity under public-private healthcare schemes. Stryker opened a Customer Experience Center in Gurgaon to support local clinicians, and Mindray shipped HyLED 9 lights for installations in Turkey and Italy, demonstrating export credibility.

Europe Surgical Lights Market

Europe shows consistent growth aided by the EU mercury ban, which forces halogen retirement and accelerates LED procurement. Philips partners with private radiology provider Evidia to deliver blue-seal MRI suites that also replace older lighting with eco-efficient fixtures.

Competitive Landscape

Global competition inside the surgical lights market remains moderate. Each leader positions lighting as a platform that plugs seamlessly into camera arms, booms, and data networks rather than as a standalone fixture. Product roadmaps now emphasize AI-enabled beam control, ultra-high CRI optics, and software updates that sync with robotic systems, an approach that keeps switching costs high for hospitals. Market dominance is also reinforced through multi-year service contracts that bundle sterilization, bulb warranties, and cybersecurity patches. Regional contenders such as Mindray and Siare grow on price advantage but still face barriers to entry in the premium hospital tier where integration credentials matter most.

Strategic moves underscore a race to widen technology moats. Stryker rolled out the Oculan Lighting Platform in November 2024, adding Fly Eye optics and voice-activated intensity control that tie directly into its Mako robotics suite. KARL STORZ paid USD 28 million for Asensus Surgical in August 2024, pairing LUNA digital laparoscopy with its existing visualization catalog to accelerate cross-selling of advanced lights. Getinge answered with the Maquet Ezea launch in January 2024, a durability-focused line designed for high-turnover rooms. New entrants like Syensqo and MezLight cooperated in January 2025 to debut a PPSU-based headlight that weighs

Surgical Lights Industry Leaders

Getinge AB

STERIS

Stryker Corporation

Koninklijke Philips N.V.

Baxter

- *Disclaimer: Major Players sorted in no particular order

Surgical Lights Market Companies Covered in this Report

- Baxter

- Getinge

- Stryker

- SIMEON Medical

- STERIS

- A-dec

- Integra LifeSciences

- Skytron

- Mediland Enterprise Corporation

- Koninklijke Philips

- KLS Martin Group

- Dr. Mach GmbH

- Herbert Waldmann GmbH

- Merivaara

- Aspen Surgical

- Brandon Medical

- DARAY Medical

- Mindray Bio-Medical

- Eizo Inc.

Recent Industry Developments in Surgical Lights Market

- January 2025: Syensqo and MezLight introduced a surgical lighting system molded in Radel PPSU that lowers weight and improves sterilization cycles.

- January 2024: Activ Surgical completed the first international procedure using ActivSight Intelligent Light at Abdali Hospital in Jordan

- January 2024: Getinge launched Maquet Ezea, a durable light engineered around evolving risk-management standards.

Global Surgical Lights Market Report Scope

Surgical lights, also called surgical lighting or operating lights, are mostly utilized in hospital operating rooms, ambulatory surgery centers, and other locations to provide high-quality lighting for treatments.

The surgical lights market is segmented by type, application, end-user, and geography. Based on type, the market is segmented into halogen lights and LED lights. Based on application, the market is segmented into cardiac surgery, gynecological surgery, neurosurgery, ENT surgery, and other surgeries. Based on end user, the market is segmented into hospitals, ambulatory surgical centers, and other end users. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (USD) for all the above segments.

Segmentation Overview

| LED Lights |

| Halogen Lights |

| Hybrid / Conversion Kits |

| Ceiling-Mounted |

| Mobile / Floor-Standing |

| Wall-Mounted |

| Surgical Headlights |

| ≤100,000 lux |

| 100,001–160,000 lux |

| >160,000 lux |

| Cardiac Surgery |

| Gynecological Surgery |

| Neurosurgery |

| ENT Surgery |

| Orthopedic / Trauma |

| Minimally-Invasive & Robotic |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics & Dental ORs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | LED Lights | |

| Halogen Lights | ||

| Hybrid / Conversion Kits | ||

| By Mounting Configuration | Ceiling-Mounted | |

| Mobile / Floor-Standing | ||

| Wall-Mounted | ||

| Surgical Headlights | ||

| By Light Intensity Range | ≤100,000 lux | |

| 100,001–160,000 lux | ||

| >160,000 lux | ||

| By Application | Cardiac Surgery | |

| Gynecological Surgery | ||

| Neurosurgery | ||

| ENT Surgery | ||

| Orthopedic / Trauma | ||

| Minimally-Invasive & Robotic | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics & Dental ORs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the surgical lights market?

The market stands at USD 2.01 billion in 2026 and is projected to reach USD 2.62 billion by 2031.

Which region holds the largest share in the surgical lights market?

North America leads with 32.02% revenue share in 2025.

Why are LED surgical lights replacing halogen models?

LEDs offer 30,000-50,000 hour lifespans, lower heat, and comply with mercury-phase-out rules, which reduce operating costs.

How fast is the ambulatory surgery center segment growing?

Surgical light purchases by ASCs are increasing at an 7.74% CAGR through 2031.

What intensity range is growing fastest?

Luminaires above 160,000 lux are advancing at an 7.82% CAGR owing to precision requirements in cardiac and neurosurgery.

Page last updated on: