Vertebroplasty And Kyphoplasty Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

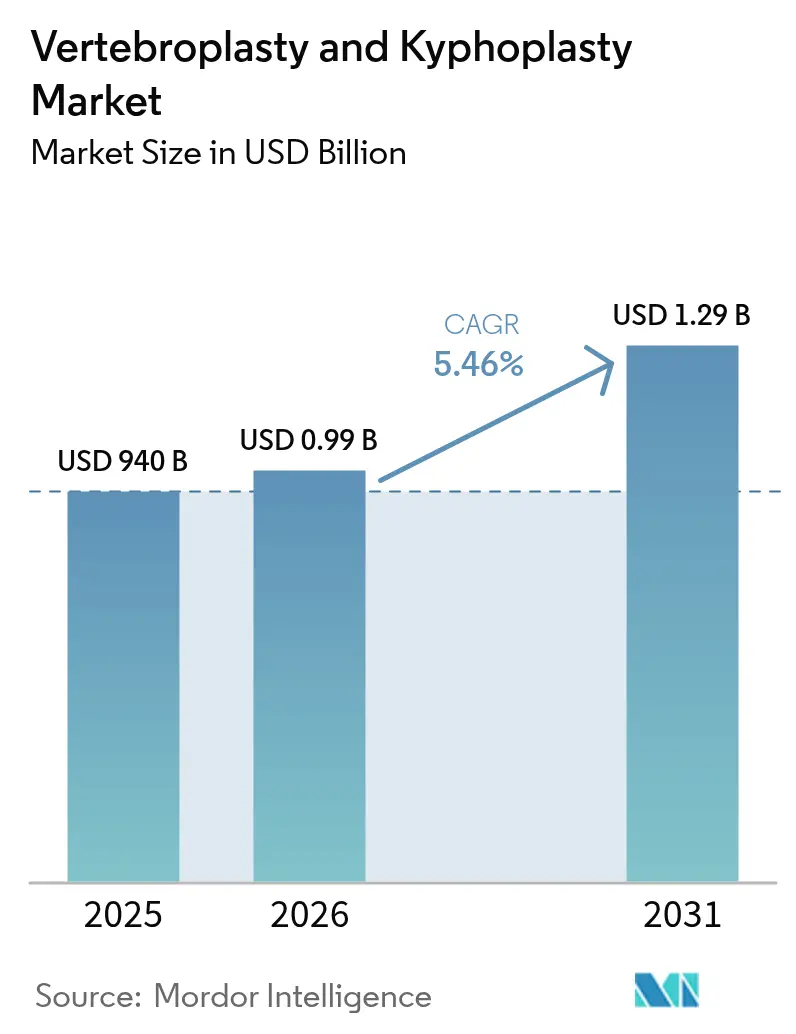

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.29 Billion |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

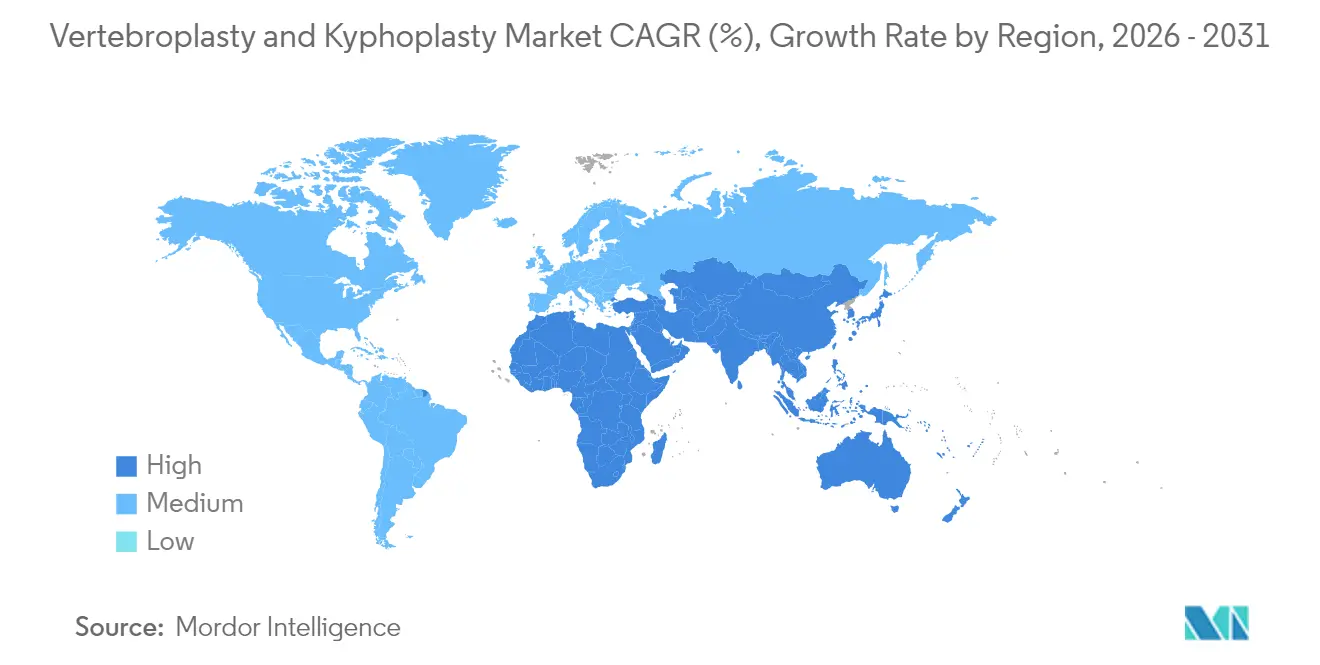

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vertebroplasty And Kyphoplasty Market Analysis by Mordor Intelligence

The vertebroplasty & kyphoplasty market size is expected to grow from USD 940 million in 2025 to USD 991.32 million in 2026 and is forecast to reach USD 1.29 billion by 2031 at 5.46% CAGR over 2026-2031. This expansion is propelled by rising osteoporotic vertebral compression fractures among aging populations, rapid adoption of minimally invasive day-care spine procedures, and steady introduction of AI-driven navigation systems and bioactive bone cements that improve accuracy while lowering complication risk. Asia-Pacific leads growth with a 6.65% CAGR through 2030 on the back of fast-growing elderly cohorts and high osteoporosis prevalence, while ambulatory surgical centers (ASCs) show the strongest end-user momentum at 6.28% CAGR as payers and patients favor cost-effective outpatient care.

Key Report Takeaways

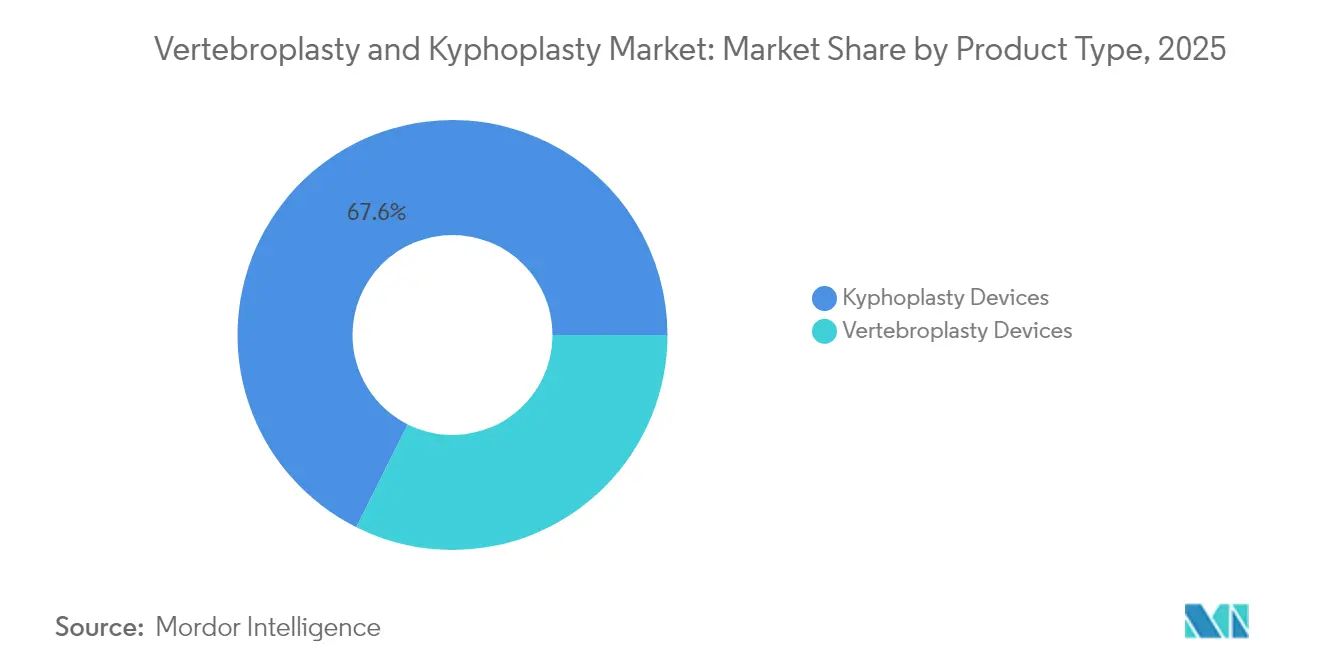

- By product type, kyphoplasty devices commanded 67.62% of the vertebroplasty & kyphoplasty market share in 2025, and the same category is projected to register the fastest 5.57% CAGR through 2031.

- By bone-cement material, polymethylmethacrylate (PMMA) accounted for 71.74% share of the vertebroplasty & kyphoplasty market size in 2025 and is set to grow at a 5.51% CAGR during the forecast window.

- By application, osteoporotic vertebral compression fractures held 58.02% revenue share in 2025, while spinal metastases treatment is forecast to expand at a 5.96% CAGR to 2031.

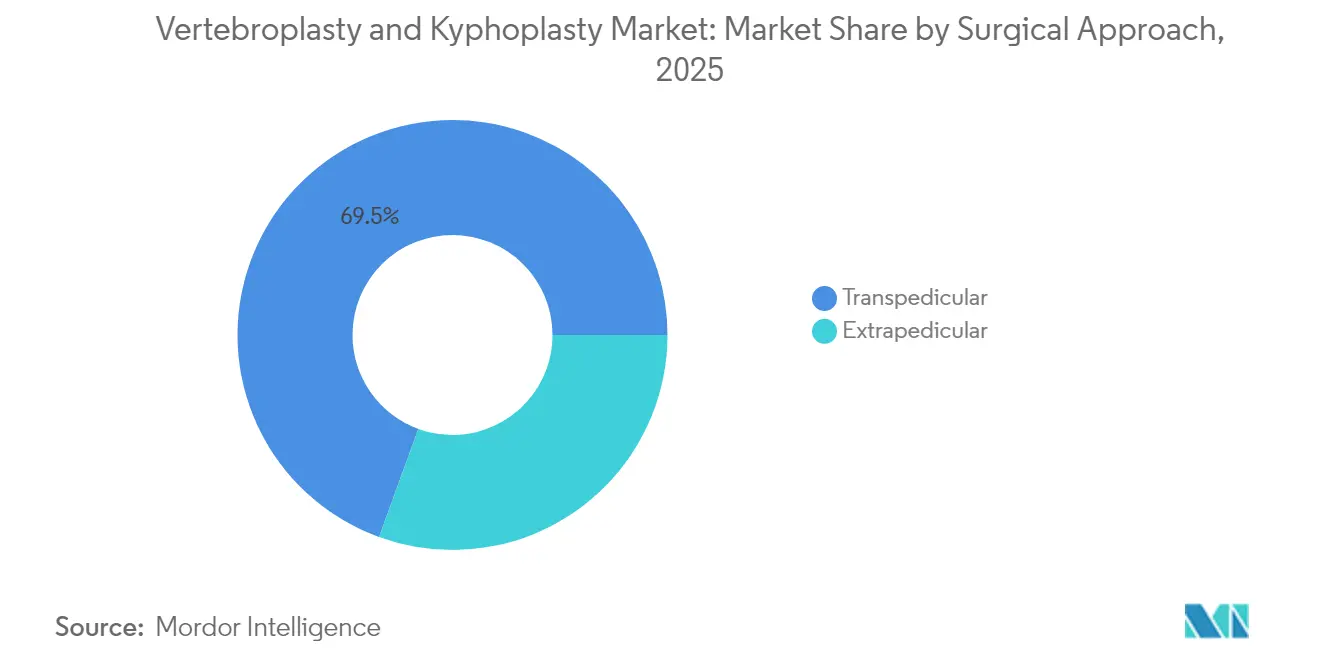

- By surgical approach, the transpedicular technique captured 69.45% of the vertebroplasty and kyphoplasty market share in 2025 and is advancing at a 5.55% CAGR through 2031.

- By end-user, hospitals remained dominant with a 61.32% share in 2025, whereas ASCs are the fastest growing setting, with a 6.12% CAGR over 2026-2031.

- By geography, North America was the largest regional market in 2025; Asia-Pacific is projected to expand at a 6.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vertebroplasty And Kyphoplasty Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing osteoporosis prevalence | +1.2% | Global, with highest impact in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Expanding geriatric demographic | +1.0% | Global, concentrated in developed economies | Long term (≥ 4 years) |

| Preference for minimally-invasive day-care spine surgeries | +0.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Early-intervention clinical guidelines recommending vertebroplasty/kyphoplasty for acute osteoporotic fractures | +0.6% | Global, led by North America and Europe | Short term (≤ 2 years) |

| AI-driven navigation & robotic alignment in vertebral augmentation | +0.5% | North America, Europe, select APAC markets | Medium term (2-4 years) |

| Bioactive, radiopaque & biodegradable bone-cement innovations | +0.4% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Osteoporosis Prevalence

More than 1.4 million vertebral compression fractures occur every year[1]Kathleen H. Miao, “Radiological Diagnosis and Advances in Imaging of Vertebral Compression Fractures,” Journal of Imaging, mdpi.com, and osteoporosis affects 10-30% of women over 40 in Asia-Pacific, driving steady case growth for vertebral augmentation procedures. Nearly 23% of patients with single osteoporotic fractures develop severe sagittal misalignment after conservative treatment, prompting early surgical intervention. The economic drag is evident, as Brazil spent over BRL 288.9 million on osteoporosis care for the elderly during 2008-2010, underscoring cost pressures that favor definitive procedures that restore mobility.

Expanding Geriatric Demographic

One-fifth of people older than 70 experience osteoporotic vertebral compression fractures, with one-third developing chronic pain that often requires augmentation. Japan’s policy focus on healthy life expectancy elevates demand for rapid fracture repair that permits early ambulation and lowers downstream disability costs. Balloon kyphoplasty can enable standing and walking within hours[2]Brannan E. O’Neill, “Utilization of Vertebroplasty/Kyphoplasty in the Management of Compression Fractures: National Trends and Predictors,” Neurospine, e-neurospine.org, helping health systems manage the mobility gap in aging societies.

Preference for Minimally Invasive Day-Care Spine Surgeries

Most vertebroplasty and kyphoplasty procedures last about 30 minutes and deliver pain relief to 90% of patients, ideal characteristics for ASC deployment. Studies report that three-quarters of treated patients resume pre-fracture activity levels, while complication rates stay below 1%. Outpatient care reduces facility costs, and Medicare reimburses CPT 22514 at roughly USD 1,200-1,500, creating a clear economic incentive to shift volume from hospitals to ASCs.

Early-Intervention Guidelines Favoring Vertebral Augmentation

Randomized trials show superior pain and mobility outcomes for vertebroplasty over conservative treatment when performed within six weeks of fracture, prompting societies to recommend early intervention. German data illustrate quality-of-life gains, with balloon kyphoplasty patients reaching EQ-5D scores of 0.44 versus 0.25 for non-surgical management. AI-based imaging now detects fractures earlier, shortening the diagnostic-to-treatment cycle and reinforcing guidelines that advocate prompt vertebral augmentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent FDA & EU-MDR approval timelines | -0.8% | Global, most pronounced in North America and Europe | Medium term (2-4 years) |

| Inconsistent reimbursement for vertebral augmentation | -0.6% | Global, varying by healthcare system structure | Short term (≤ 2 years) |

| Procedure-related adverse events | -0.4% | Global, with regional variation in reporting standards | Long term (≥ 4 years) |

| PMMA monomer supply-chain volatility | -0.3% | Global, concentrated in regions dependent on imports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent FDA & EU-MDR Approval Timelines

Manufacturers now face EU-MDR transition deadlines that extend to 2027-2028 for Class III and certain Class IIb devices, lengthening certification cycles and raising compliance costs. In the US, ongoing post-market surveillance requirements following past cement leakage concerns add data-generation burdens that can slow first-to-market advantage.

Inconsistent Reimbursement for Vertebral Augmentation

Medicare delegates coverage rules to local jurisdictions, creating approval variability for identical clinical scenarios, while private payers often apply narrower indications and deny sacroplasty, complicating provider billing workflows. In China, average hospitalization costs of CNY 35,906 (USD 5,122) for vertebral augmentation can limit access for lower-income patients even as prevalence rises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Kyphoplasty Devices Sustain Leadership

Kyphoplasty devices held 67.62% of the vertebroplasty & kyphoplasty market share in 2025 and are projected to rise at a 5.57% CAGR. The approach restores vertebral height before cement injection, cutting leakage risk and delivering visual-analog-scale pain reductions from 7.7 to 2.2. In comparison, vertebroplasty remains essential for acute stabilization but grows more slowly. The vertebroplasty & kyphoplasty market size for kyphoplasty devices is expected to move from USD 0.64 billion in 2025 to about USD 0.88 billion by 2031 at the stated CAGR, maintaining its dominant contribution to overall revenues. Stryker’s SpineJack, capable of 1,000 N expansion force, and next-gen unipedicular balloons exemplify how engineering upgrades reinforce clinical preference.

The competitive focus now shifts toward hybrid implants that combine the structural benefits of kyphoplasty with vertebroplasty-style cement flows. Early clinical readouts from autonomous puncture systems suggest that procedural speed and accuracy can improve further, supporting sustained demand for premium device platforms. Emerging players demonstrate that well-targeted design tweaks can still carve share despite the presence of large incumbents.

By Bone-Cement Material: PMMA Holds Ground Amid Bioactive Options

PMMA retained 71.74% of the vertebroplasty & kyphoplasty market share in 2025 and is tracking a 5.51% CAGR. The growth of PMMA-based products reflects their broad familiarity and mechanical reliability. Recent formulations fine-tune polymerization temperature and viscosity to reduce extrusion while preserving strength.

At the same time, bioactive cements are carving a noticeable niche. Strontium-substituted hydroxyapatite promotes osseointegration, and PMMA-CPC hybrids blend load-bearing prowess with controlled resorption. Though starting from a small base, the “Other Materials” category is expected to post a higher CAGR than PMMA, aided by surgeon demand for biologically friendly agents that bond with cancellous bone.

By Application: Osteoporotic Fractures Dominate; Oncologic Use Surges

Osteoporotic vertebral compression fractures contributed 58.02% of the vertebroplasty & kyphoplasty market share, mirroring their ubiquity in elderly patients. Despite their maturity, procedure counts continue to scale with demographic aging. The vertebroplasty & kyphoplasty market size linked to this segment will expand steadily owing to guideline-driven early intervention.

Metastatic spine disease, with a 5.96% projected CAGR, is gaining traction as improved cancer survival increases skeletal complications. Augmentation provides palliative stability that supports continued systemic therapy, a value recognized by oncologists who now refer patients earlier. This diversification of indications enhances overall procedural volumes beyond purely osteoporotic contexts.

By Surgical Approach: Transpedicular Route Remains Mainstay

Transpedicular access delivered 69.45% of the vertebroplasty & kyphoplasty market share in 2025, supported by a 97.7% pain-relief success rate. It benefits from favorable anatomy in lumbar and lower thoracic vertebrae and is preferred by many interventionists for predictable needle trajectories. Extrapedicular methods serve niche needs such as mid-thoracic segments where pedicle dimensions restrict instrumentation. AI-assisted navigation and robotics are improving both routes, yet the familiarity of the transpedicular technique underpins its projected 5.55% CAGR.

By End-User: Hospitals Dominate; ASCs Accelerate

Hospitals contributed 61.32% of revenue in 2025, thanks to comprehensive imaging, anesthesia, and perioperative care. Nonetheless, the cost-sensitive environment propels case migration to ASCs, which are forecast to grow at 6.12% CAGR. Strong payer incentives and patient preference for same-day discharge fuel this transition. Hospitals respond by adopting efficiency programs and adding outpatient bays to retain throughput.

Geography Analysis

North America remains the largest territory, supported by Medicare reimbursement that averages USD 1,200-1,500 per case and clinical familiarity built over two decades of data. The region advances at a 4.97% CAGR as demographic aging continues and AI-assisted navigation gains clinical acceptance.

Asia-Pacific, posting the fastest 6.56% CAGR, benefits from high osteoporosis prevalence—52.8% in women and 18.7% in men undergoing spine surgery in China, paired with rising healthcare expenditure. Government campaigns that emphasize active aging and swift fracture repair underpin procedure uptake.

Europe delivers a 5.21% CAGR, buoyed by aging populations and quality-of-life evidence that reinforces adoption, although EU-MDR compliance costs temper rapid product launches. Middle East & Africa and South America trail but still expand above 6% as tertiary centers adopt modern augmentation protocols and local device distributors build channel depth.

Competitive Landscape

The vertebroplasty & kyphoplasty market is moderately fragmented. Medtronic, Johnson & Johnson, and VB Spine (following its 2025 acquisition of Stryker’s spine unit) headline the field, yet smaller innovators such as Amber Implants illustrate ongoing disruption potential.

Strategic priorities center on integrated platforms that marry cement, delivery hardware, and imaging. AI-infused navigation suites that shorten learning curves are differentiators, reinforcing commercial leverage in hospital value analysis committees.

Product roadmaps also emphasize next-generation cements with radiopaque additives and bioactivity. Clinical studies remain pivotal; payers increasingly demand peer-reviewed outcomes before widening coverage. Exhibit positioning now integrates carbon-footprint statements as procurement teams add sustainability to their evaluation matrix.

Vertebroplasty And Kyphoplasty Industry Leaders

Cardinal Health, Inc.

Johnson & Johnson Services, Inc.

Medtronic plc

Merit Medical Systems, Inc.

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amber Implants BV reported no device-related adverse events after one-year follow-up for its Vcfix spinal system, with marked pain reduction, paving the way for broader regulatory submissions.

- May 2025: Stryker received FDA clearance for a minimally invasive back-pain treatment system that complements its vertebral augmentation portfolio after divesting its broader spine division.

- January 2025: Stryker announced the strategic sale of its spinal implants business as part of organizational restructuring under new leadership. The divestiture affects vertebral augmentation product lines and represents a significant shift in the company's strategic focus away from spine technologies.

- June 2024: Medtronic partnered with Merit Medical to commercialize a steerable balloon catheter (Kyphon KyphoFlex) for unipedicular kyphoplasty in the US, with Merit handling manufacturing and Medtronic directing sales and distribution.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the vertebroplasty and kyphoplasty market as total revenue from disposable cement kits, balloons, access needles, inflation pumps, and supporting capital systems used in percutaneous vertebral augmentation procedures that stabilize painful compression fractures of osteoporotic or oncologic origin across hospitals and ambulatory centers.

Scope exclusion: Open spinal fusion implants, biologic grafts, vertebral body stents, and non-surgical pain therapies lie outside this analysis.

Segmentation Overview

- By Product Type

- Vertebroplasty Devices

- Kyphoplasty Devices

- By Bone-Cement Material

- Polymethylmethacrylate (PMMA)

- Calcium Phosphate Cement (CPC)

- Other Materials

- By Application

- Osteoporotic Vertebral Compression Fractures

- Spinal Metastases

- Other Applications

- By Surgical Approach

- Transpedicular

- Extrapedicular

- By End-User

- Hospitals

- Ambulatory Surgical Centres (ASCs)

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed spine surgeons, interventional radiologists, implant distributors, and payer advisors across North America, Europe, and Asia-Pacific to validate incidence-to-treatment rates, ASP corridors, and site-of-care shifts. An online poll of hospital procurement leads cross-checked cement kit consumption per case.

Desk Research

We began with respected public datasets such as the International Osteoporosis Foundation, WHO hospital-discharge files, and CMS Part B claims that pin down fracture incidence and treated volumes. Device pricing and share cues were drawn from SEC filings of listed spine manufacturers, Eurostat procedure registers, and import-export traces on Volza. News feeds compiled through Dow Jones Factiva flagged recalls, launches, and reimbursement shifts that could tilt average selling prices.

A second sweep of tender notices indexed by Tenders Info and peer-reviewed spine journals helped us track kit-use ratios and surgical approach mix before numbers moved into modeling. These references are illustrative only; many additional open and paid resources underpinned the desk review.

These references are illustrative only; many additional open and paid resources underpinned the desk review.

Market-Sizing & Forecasting

We first applied a top-down frame: vertebral-fracture incidence ➔ treated case pool by country ➔ device kit count × verified ASPs. Supplier revenue roll-ups and sampled hospital purchase audits supplied bottom-up guardrails, and any variance was reconciled before totals locked. Core drivers, osteoporosis prevalence, aging population, procedure penetration, kit price trajectories, and reimbursement policy changes feed a multivariate regression with scenario analysis projecting value through 2030.

Data Validation & Update Cycle

Each run passes variance filters, senior peer review, and compliance sign-off. Reports refresh annually, while recalls, guideline shifts, or material price swings trigger interim updates so clients receive the latest view.

Why Mordor's Vertebroplasty & Kyphoplasty Baseline Commands Reliability

Published estimates often diverge because firms track different product bundles, convert currencies on varied dates, or refresh on uneven cadences.

Our disciplined scope selection and yearly refresh anchor the 2025 market at USD 0.94 billion, giving decision-makers an audit-ready figure.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.94 B (2025) | Mordor Intelligence | - |

| USD 0.95 B (2025) | Global Consultancy A | Needle devices only; cements excluded |

| USD 0.79 B (2023) | Regional Consultancy B | Historic ASPs, limited Asia coverage |

Because our model ties treated incidence to transparent price and volume inputs and corroborates them with supplier revenues, it stands as the most dependable starting point for planning.

Key Questions Answered in the Report

What is the primary driver behind hospitals' adoption of AI-guided vertebral augmentation systems?

Hospitals are embracing AI-guided navigation because it shortens puncture time, improves cement placement accuracy, and reduces leakage-related complications, leading to better patient outcomes and fewer revisits.

Why are ambulatory surgical centers gaining vertebroplasty and kyphoplasty volume from hospitals?

ASCs combine shorter procedure times with same-day discharge, giving referring physicians a cost-efficient setting while offering patients quicker recovery in a lower-acuity environment.

How do bioactive bone cements reshape surgeon choices?

New formulations enriched with osteoconductive additives encourage bone bonding and lower post-operative inflammation, prompting many spine specialists to shift away from conventional PMMA in eligible cases.

What impact will the EU Medical Device Regulation have on device launches in this field?

Extended conformity assessments and heightened post-market surveillance under EU-MDR are lengthening approval cycles, pushing manufacturers to front-load clinical evidence and risk-management data before release.

How is the competitive landscape changing after Stryker’s spine divestiture?

The sale created a new mid-tier powerhouse, intensifying rivalry for differentiated implants and accelerating partnerships among imaging, navigation, and cement suppliers seeking bundled offerings.

Which clinical indication is seeing the fastest procedural uptake beyond osteoporosis?

Vertebral stabilization for spinal metastases is rising quickly as oncologists incorporate augmentation to control pain and maintain structural integrity during systemic cancer therapy.

Page last updated on: