Ophthalmic Eye Dropper Market Size and Share

Market Overview

| Study Period | 2025 - 2030 |

|---|---|

| Market Size (2025) | USD 14.90 Billion |

| Market Size (2030) | USD 20.30 Billion |

| Growth Rate (2025 - 2030) | 6.10% CAGR |

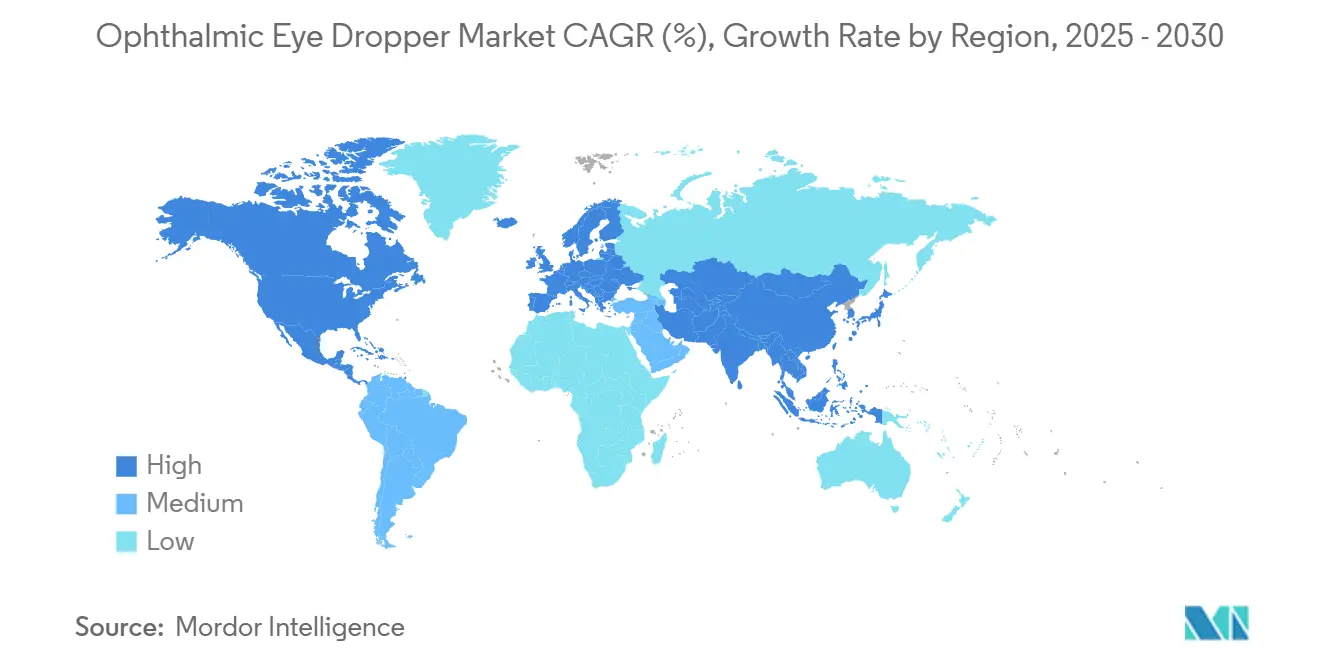

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

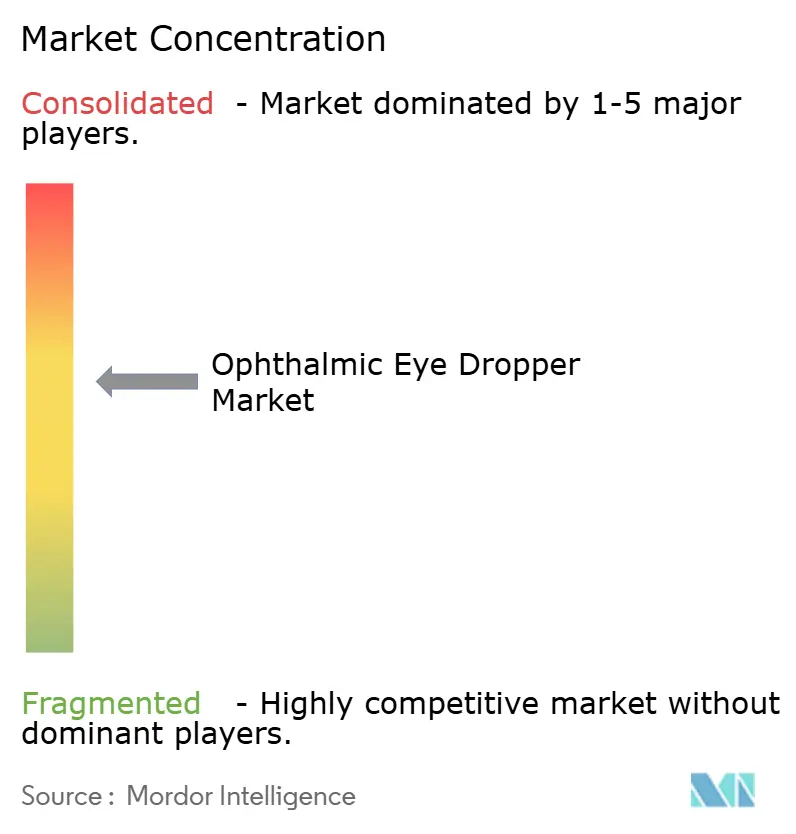

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ophthalmic Eye Dropper Market Analysis by Mordor Intelligence

The global ophthalmic droppers market size stood at USD 14.9 billion in 2025 and is on track to reach USD 20.3 billion by 2030, advancing at a 6.1% CAGR according to Mordor Intelligence. Robust growth reflects an aging population, the climbing prevalence of glaucoma and dry eye syndrome, and the steady rollout of preservative-free, digitally enabled dispensing technologies that foster patient adherence. Regulatory tightening in the United States and Europe is pushing manufacturers toward higher-grade materials and factory automation, giving incumbents with validated lines a competitive edge. Sustainability directives in the European Union and parts of Asia are triggering a visible pivot from conventional LDPE to bio-based resins, and software-enabled smart caps are beginning to transform droppers from passive containers into active monitoring tools. The ophthalmic droppers market continues to lure cross-industry entrants—from electronics and sensors to recycled-polymer specialists—who view ergonomic dispensing and data capture as untapped growth vectors.

Key Report Takeaways

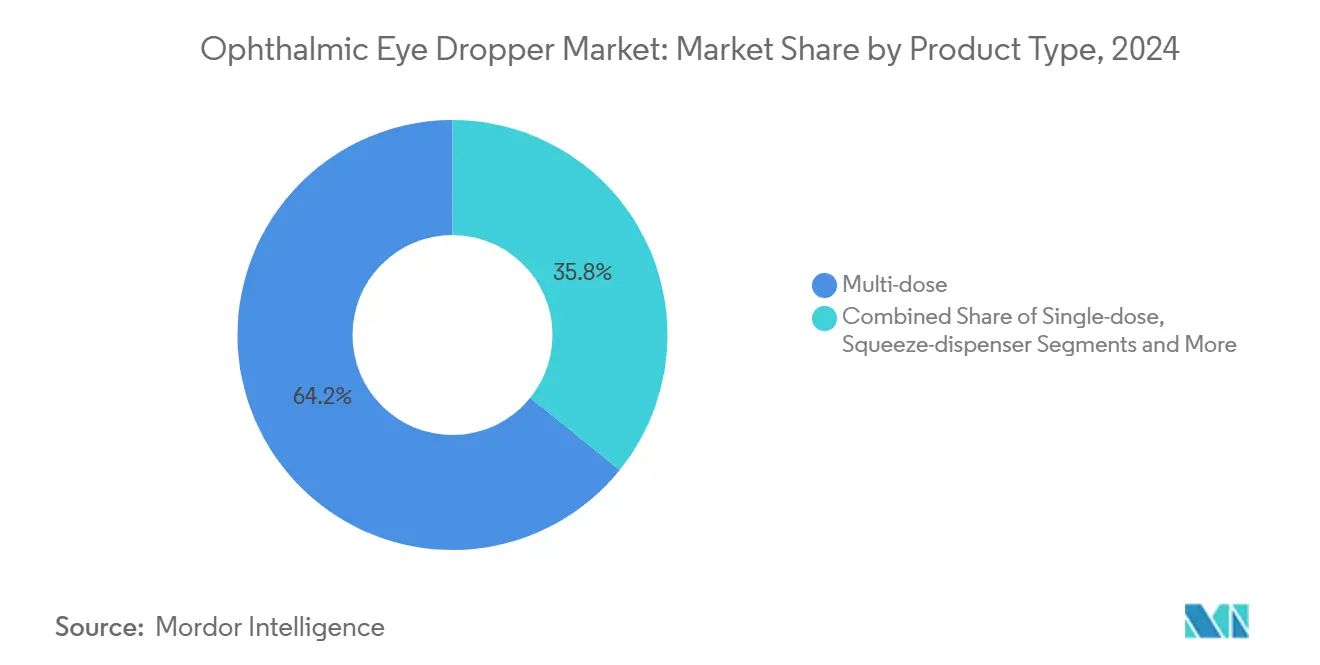

- By product type, multi-dose systems accounted for 64.2% of the ophthalmic droppers market share in 2024 while squeeze-dispenser adaptors are forecast to expand at a 7.8% CAGR through 2030.

- By material, LDPE captured 57.3% share of the ophthalmic droppers market size in 2024 whereas bio-based plastics represent the fastest-rising material segment with a 9.5% CAGR to 2030.

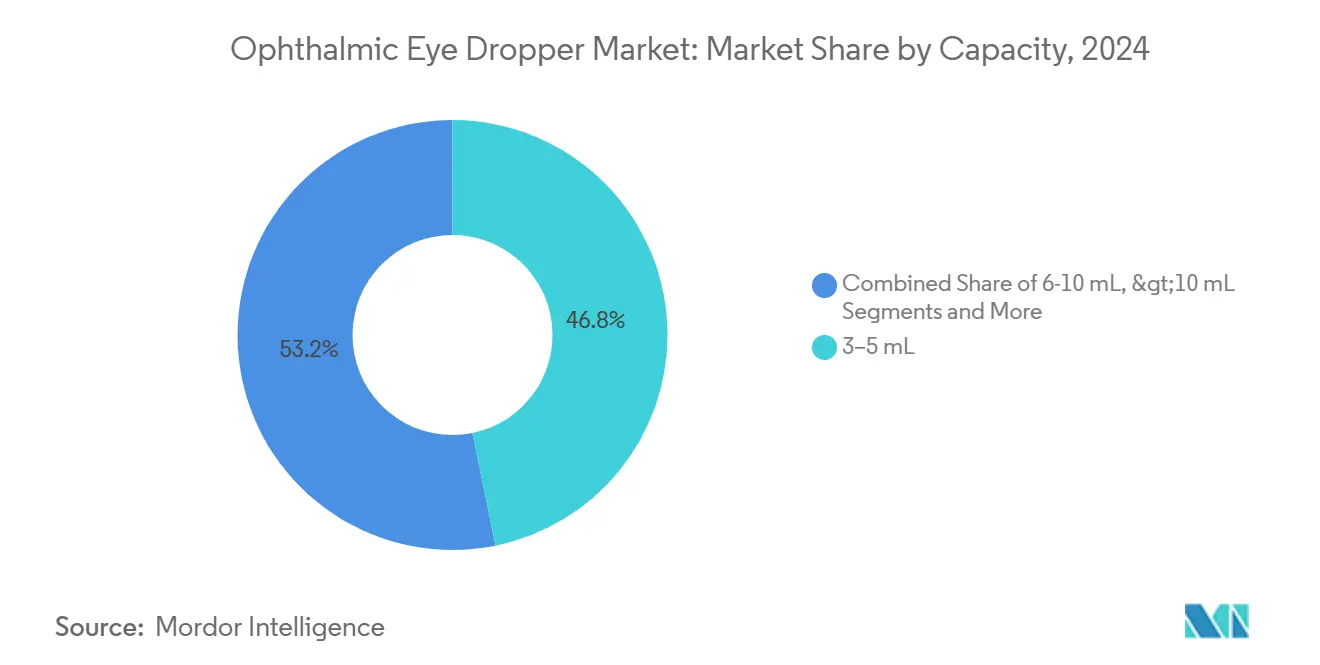

- By capacity, the 3-5 mL range held 46.8% of the ophthalmic droppers market size in 2024, and unit-dose formats below 1 mL are growing at a 6.2% CAGR through 2030.

- By technology, preservative-free sterile-valve droppers led with 52.1% ophthalmic droppers market share in 2024, while connected digital systems are projected to advance at a 7.4% CAGR to 2030.

- By geography, North America commanded 38.4% of the ophthalmic droppers market in 2024; Asia Pacific represents the fastest-growing region with an 8.2% CAGR expected through 2030.

Global Ophthalmic Eye Dropper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Ocular Disorders | +1.80% | Global, with highest impact in Asia Pacific and aging Western populations | Long term (≥ 4 years) |

| Shift Toward Self-Administered Topical Treatments | +1.20% | North America & EU, expanding to APAC urban centers | Medium term (2-4 years) |

| Advances In Formulation And Microdosing Technologies | +1.00% | Global, led by US and European innovation hubs | Medium term (2-4 years) |

| Demand For Adherence-Oriented, Ergonomic Packaging | +0.80% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Growth In Biologics And Preservative-Free Ophthalmics | +0.70% | North America & EU, with spillover to premium APAC markets | Long term (≥ 4 years) |

| Regulatory Focus On Sterility And Dose Accuracy | +0.50% | Global, with strictest enforcement in FDA and EMA jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Ocular Disorders

Rising cases of glaucoma, diabetic retinopathy, and severe dry eye sustain demand for long-term topical therapy, directly boosting the ophthalmic droppers market. U.S. public-health tracking showed 4.22 million diagnosed glaucoma cases by 2022, and 1.5 million patients experienced vision-limiting symptoms that require chronic treatment.[1]Centers for Disease Control and Prevention, "VEHSS Modeled Estimates for Glaucoma," cdc.gov Asia Pacific bears additional pressure as urban diabetes and myopia accelerate faster than specialty-care capacity; thus, easily dispensed drops become frontline therapy because they minimize clinic visits. The economic burden of untreated eye disease compels insurers to reimburse widely available droppers that patients can administer at home. This epidemiological tailwind is set to remain strong for at least the next decade as populations age and screen exposure remains high.

Shift Toward Self-Administered Topical Treatments

Telehealth normalization and hospital cost-containment policies are firmly steering ophthalmology toward home-based care. The U.S. FDA cleared the first Bluetooth-enabled smart bottles that capture timestamped usage data and transmit adherence reports to providers, validating a business model in which packaging doubles as a remote patient-monitoring platform.[2]Husein Husein et al., “Smart Electronic Eyedrop Bottle for Monitoring Glaucoma Medication Adherence,” mdpi.com Device firms are collaborating with pharma houses on tactile collars and pivot-nose tips to help low-vision users orient bottles correctly, an ergonomic tweak that early trials show can raise adherence by up to 30% in seniors. These usability gains can translate into lower downstream surgical costs for health plans, supplying a direct economic incentive to accelerate the distribution of patient-friendly droppers.

Advances in Formulation and Microdosing Technologies

Micro-spray and piezo-print systems can achieve equivalent intraocular pressure reductions using 75% less drug volume than conventional droppers, thereby lowering systemic side effects and stretching pharmacy budgets. The FDA’s 2024 draft guidance requires quantitative validation of delivered-dose accuracy, a rule that inherently favors high-precision dispensers. Nanomicellar drugs exploiting these formats are now reaching late-stage trials for posterior-segment diseases, signaling broad pipeline momentum.

Demand for Adherence-Oriented Ergonomic Packaging

Manufacturers are redesigning bottles to reduce squeeze force by more than half, aiding patients with arthritis. Gerresheimer’s Ophthalmic Plus bottle exemplifies the trend, claiming a 60% lower actuation force than legacy LDPE bottles. Berry Global introduced a flow-controlled tip that delivers uniform drops even if users squeeze erratically, a feature that mitigates waste and ensures therapeutic dosing. Integration of such ergonomic gains with smartphone apps that remind and record dosing promises to convert packaging into a continuous adherence service in the next few years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensive Regulatory Validation Processes | -1.50% | Global, with highest impact in FDA and EMA jurisdictions | Medium term (2-4 years) |

| Drug-Packaging Compatibility And Stability Issues | -0.80% | Global, particularly affecting biologics and preservative-free formulations | Long term (≥ 4 years) |

| Adoption Of Sustained-Release Implants Reducing Drop Use | -0.60% | North America & EU, with early adoption in premium healthcare markets | Long term (≥ 4 years) |

| Rising Sustainability Compliance Costs Impacting Margins | -0.40% | EU leading, expanding to North America and APAC developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Regulatory Validation Processes

Rigorous container-closure integrity testing can push validation expenses past USD 10 million for next-generation droppers, which constrains small entrants. Recent FDA warning letters issued to ophthalmic plants, including Regenerative Processing Plant and Omni Lens, underscore how compliance failures can halt distribution overnight. The European Medicines Agency’s 2024 withdrawal of Durysta shows that even post-approval vigilance remains stringent, increasing sunk-cost risk for implant developers.[3]European Medicines Agency, “Durysta,” ema.europa.eu These financial and regulatory burdens fortify entry barriers and slow category innovation.

Drug-Packaging Compatibility and Stability Issues

Biologics and preservative-free formulas often react with conventional plastics, which can cause potency loss or particulate contamination that triggers recalls. Corning’s Valor Glass and Stevanato’s cross-linked silicone glassware promote safer drug contact but command premium pricing that may deter cost-sensitive buyers. Small pharma firms must therefore budget extra for compatibility testing, prolonging development timelines, and occasionally narrowing viable material options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multi-Dose Dominance Meets Retrofit Innovation

Multi-dose systems generated 64.2% of the ophthalmic droppers market size in 2024, reflecting their entrenched role in chronic glaucoma and dry eye regimens that demand economical multi-week supply. The format’s cost efficiency keeps co-pay levels manageable for payers, while patients favor smaller pharmacy visits. The ophthalmic droppers market anticipates modest pricing pressure in this segment as raw-material costs stabilize and capacity additions in the United States and India reach scale. Squeeze-dispenser adaptors, which clip onto legacy bottles to add unidirectional valves or dose-counting displays, are gaining momentum with a projected 7.8% CAGR through 2030.

Retrofit adaptors satisfy hospitals keen to curb infection risk without overhauling entire supply chains. Meanwhile, single-dose vials persist in cataract surgery packs and emergency departments where sterility is mandatory. Refillable smart droppers integrating NFC chips could emerge as a premium sub-segment, although payers still debate reimbursement levels for hardware-linked analytics. These competitive dynamics show how the ophthalmic droppers market both consolidates around proven formats and experiments with sensorized add-ons that extend product life cycles.

By Material: Sustainability Imperatives Reorder Preferences

LDPE continued to command 57.3% of the ophthalmic droppers market share in 2024 because it balances chemical inertness, flexibility, and low tooling costs. The ophthalmic droppers market nonetheless faces accelerating migration to bio-based resins following the EU Packaging and Packaging Waste Regulation that mandates recyclable or renewable packaging by 2030. Bio-PP and sugarcane LDPE lines are scaling, helped by pharma carbon-footprint pledges. For niche biologics, borosilicate and Valor Glass offer unparalleled barrier properties, albeit at a higher total landed cost. Valor’s ability to minimize delamination has earned early adoption in advanced therapies, adding a high-margin tier within the ophthalmic droppers industry.

This shift strains existing supply chains because recycling streams for medical-grade plastics remain immature in many regions. Suppliers now market closed-loop take-back programs for hospitals, yet logistical economics vary widely. Net impact on the ophthalmic droppers market will be a dual-track landscape: mass-volume LDPE for cost-sensitive therapies and premium glass or bio-plastic for flagship brands seeking carbon-neutral credentials.

By Capacity: Unit-Dose Growth Mirrors Infection-Control Vigilance

The 3-5 mL band represented 46.8% of the ophthalmic droppers market size in 2024, a sweet spot aligning with 30-day prescriptions in glaucoma and allergy therapy. Growth moderates here as formulators test higher-potency micro-dose variants. Sub-1 mL unit-dose formats, however, are climbing 6.2% annually. Hospitals favor them for outpatient cataract and LASIK follow-up, where infection control overrides cost considerations. Regulators also lean toward unit-dose for preservative-free biologics to avoid repeated microbial exposure.

In parallel, larger 6-10 mL bottles hold value in compounded combination drops, particularly for post-surgical steroid-antibiotic blends. Yet as micro-dosing technology advances, even those may downsize to conserve active ingredients, subtly reshaping the capacity mix inside the ophthalmic droppers market.

By Technology: Connected Valves Speed the Digital Turn

Preservative-free sterile-valve systems owned 52.1% share in 2024 thanks to validated barrier membranes that maintain sterility without benzalkonium chloride. The ophthalmic droppers market is now pivoting toward Bluetooth or NFC-equipped variants growing 7.4% a year. Early deployments log 100% dose-event accuracy over a three-week battery cycle, proving technical viability. Antimicrobial tips using silver-ion polymers enter premium tiers, promising multi-week sterility even if users touch the nozzle.

Meanwhile, child-resistant closures integrate spring-loaded collars without raising squeeze force, meeting dual goals of safety and accessibility. Controlled micro-dose motors may ultimately blur lines between droppers and mini-atomizers, introducing new patentable differentiation inside the ophthalmic droppers industry.

Geography Analysis

North America held 38.4% of the ophthalmic droppers market in 2024 due to the highest per-capita healthcare expenditure and a payor environment willing to reimburse premium delivery innovations. Stringent FDA rules boost the credibility of domestic suppliers and encourage capital expansion, as reflected by Gerresheimer’s USD 180 million Georgia plant upgrade that adds 18,000 m² of Class 8 cleanroom space. Consolidation is accelerating, illustrated by McKesson’s USD 850 million purchase of PRISM Vision Holdings, which multiplies distribution channels for new dropper-based therapies. Canada shows similar regulatory rigor, whereas Mexico leverages maquiladora incentives to attract plastic-injection tooling investments.

Asia Pacific is the growth engine with an 8.2% CAGR expected through 2030 on the back of 4.3 billion aging residents, surging myopia prevalence, and an expanding urban middle class. China’s push for local manufacturing parity is prompting global suppliers to co-invest; Berry Global is building a new Bangalore site to shorten lead times and comply with “Made in India” preferences. Japan leans toward high-tech smart droppers that monitor adherence, whereas Southeast Asia values low-cost multi-dose formats but will gradually adopt bio-plastics as regional regulations tighten.

Europe sustains mid-single-digit growth, anchored by harmonized EMA reviews and aggressive sustainability legislation. The EU Packaging and Packaging Waste Regulation presses companies to redesign dropper assemblies for recyclability or compostability by 2030, altering material procurement patterns across Germany, France, and the United Kingdom. FUJIFILM Diosynth’s GBP 100 million microbial facility in Billingham signals that regional biomanufacturing capacity continues to expand, which indirectly elevates demand for compatible high-grade droppers.

Competitive Landscape

Competition is fragmented across three strata: global packaging specialists, pharmaceutical owners of proprietary delivery systems, and technology start-ups embedding sensors. Aptar, Nemera, and Gerresheimer dominate conventional multi-dose bottling through scale economies and a combined global tooling network exceeding 100 injection lines. Their regulatory dossiers often speed time-to-market for client drugs, reinforcing lock-in. Stevanato, Schott Pharma, and Gerresheimer recently formed an alliance to set ready-to-use glass standards, showing how even rivals cooperate when regulatory complexity rises.

Smart-device entrants such as Adherium, Vape-minder, and digital-health spin-offs are chasing data-oriented niches by bundling adherence analytics with subscription platforms for payors. Yet they rely on OEM partnerships for sterile molding know-how, preserving leverage for incumbent plastics firms. Sustainability is another battlefield: Santen rolled out biomass droppers to comply with Japan’s net-zero roadmap, differentiating against generic LDPE formats. Financial disclosure from Aptar shows double-digit revenue growth in proprietary drug delivery systems in Q1 2025, proof that premium, IP-protected droppers gain pricing power despite overall commoditization.

Looking forward, M&A should intensify as suppliers strive for vertical integration, while software-powered adherence ecosystems may redraw value pools away from bottle hardware toward data services. Still, stringent sterility regulations keep the playing field narrower than consumer electronics, capping immediate disruption.

Ophthalmic Eye Dropper Industry Leaders

-

Aptar Pharma

-

Nemera

-

Gerresheimer

-

Berry Global

-

Amcor Healthcare Packaging

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Gerresheimer announced a USD 180 million expansion of its Peachtree City, Georgia, facility, adding 400 new jobs to boost its output of medical systems, including ophthalmic delivery devices.

- March 2025: TekniPlex Healthcare introduced a 10ml squeezable container designed for preservative-free multidose formulations in eye care, manufactured in ISO 8 cleanrooms.

- December 2024: Berry Global showcased its easy-squeeze 10ml ophthalmic bottle at Pharmapack 2025. The bottle is specifically designed for preservative-free prescription and OTC products. It features an ergonomic design for user convenience and optimized flow control for precise drop dispensing.

Global Ophthalmic Eye Dropper Market Report Scope

| Multi-dose Dropper Systems |

| Single-dose Vials/Ampoules |

| Squeeze-dispenser Adaptors |

| Refillable Smart Droppers |

| Custom Compounding Droppers |

| Low-Density PE (LDPE) |

| High-Density PE (HDPE) |

| Polypropylene (PP) |

| Glass (Borosilicate & Others) |

| Bio-based / Compostable Plastics |

| ≤ 2.5 mL |

| 3 - 5 mL |

| 6 -10 mL |

| > 10 mL |

| Unit-Dose (<1 mL) |

| Preservative-free Sterile-Valve Systems |

| Anti-microbial Coated Tips |

| Controlled Micro-Dose (≤ 15 µL) |

| Child-Resistant / Senior-Friendly Designs |

| Connected / Digital-Monitoring Droppers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Multi-dose Dropper Systems | |

| Single-dose Vials/Ampoules | ||

| Squeeze-dispenser Adaptors | ||

| Refillable Smart Droppers | ||

| Custom Compounding Droppers | ||

| By Material | Low-Density PE (LDPE) | |

| High-Density PE (HDPE) | ||

| Polypropylene (PP) | ||

| Glass (Borosilicate & Others) | ||

| Bio-based / Compostable Plastics | ||

| By Capacity | ≤ 2.5 mL | |

| 3 - 5 mL | ||

| 6 -10 mL | ||

| > 10 mL | ||

| Unit-Dose (<1 mL) | ||

| By Technology | Preservative-free Sterile-Valve Systems | |

| Anti-microbial Coated Tips | ||

| Controlled Micro-Dose (≤ 15 µL) | ||

| Child-Resistant / Senior-Friendly Designs | ||

| Connected / Digital-Monitoring Droppers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the global ophthalmic droppers market in 2025?

The ophthalmic droppers market size is USD 14.9 billion in 2025 with a forecast value of USD 20.3 billion by 2030.

Which product type leads sales?

Multi-dose systems hold the top position with 64.2% share of global revenue in 2024.

What is the fastest-growing regional opportunity?

Asia Pacific is projected to grow at an 8.2% CAGR through 2030 due to aging demographics and rapid urbanization.

Why are bio-based plastics gaining traction?

EU sustainability mandates and corporate carbon targets are pushing manufacturers to adopt recyclable or renewable resins.

How are smart droppers changing the category?

Connected droppers track usage in real time, helping physicians monitor adherence and enabling payors to reduce complication costs.

What regulatory hurdle most affects new entrants?

High-cost container-closure validation and leachables testing can exceed USD 10 million, limiting market access for smaller firms.

Page last updated on: