Leukapheresis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

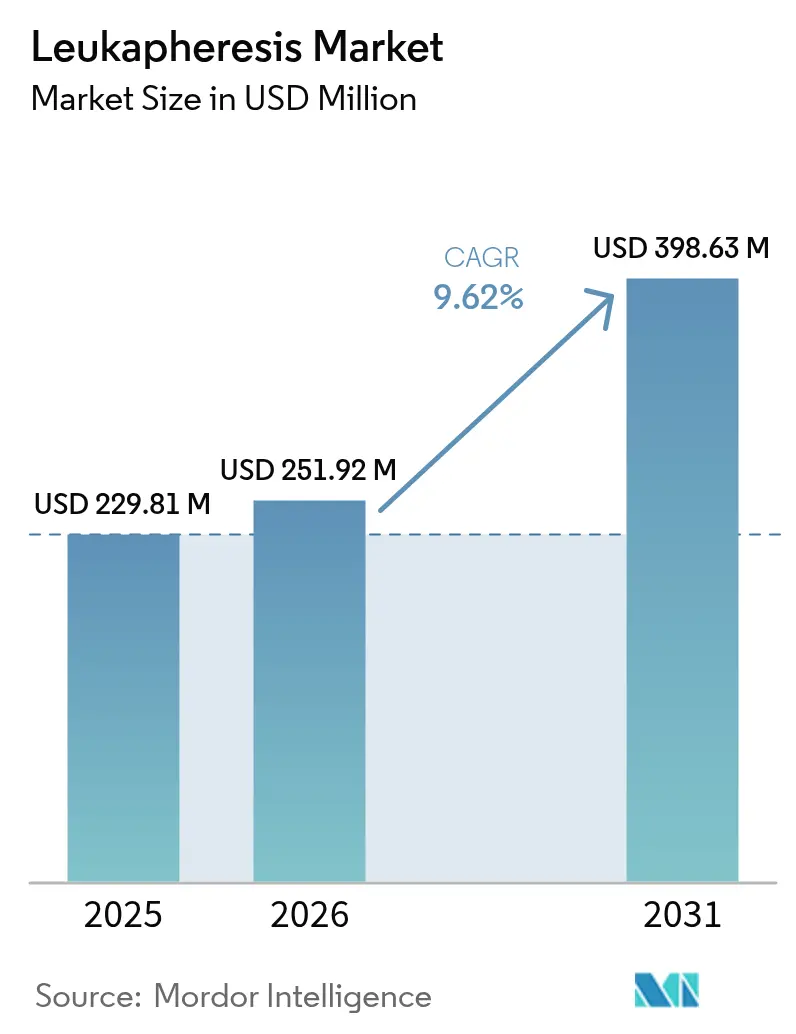

| Market Size (2026) | USD 251.92 Million |

| Market Size (2031) | USD 398.63 Million |

| Growth Rate (2026 - 2031) | 9.62% CAGR |

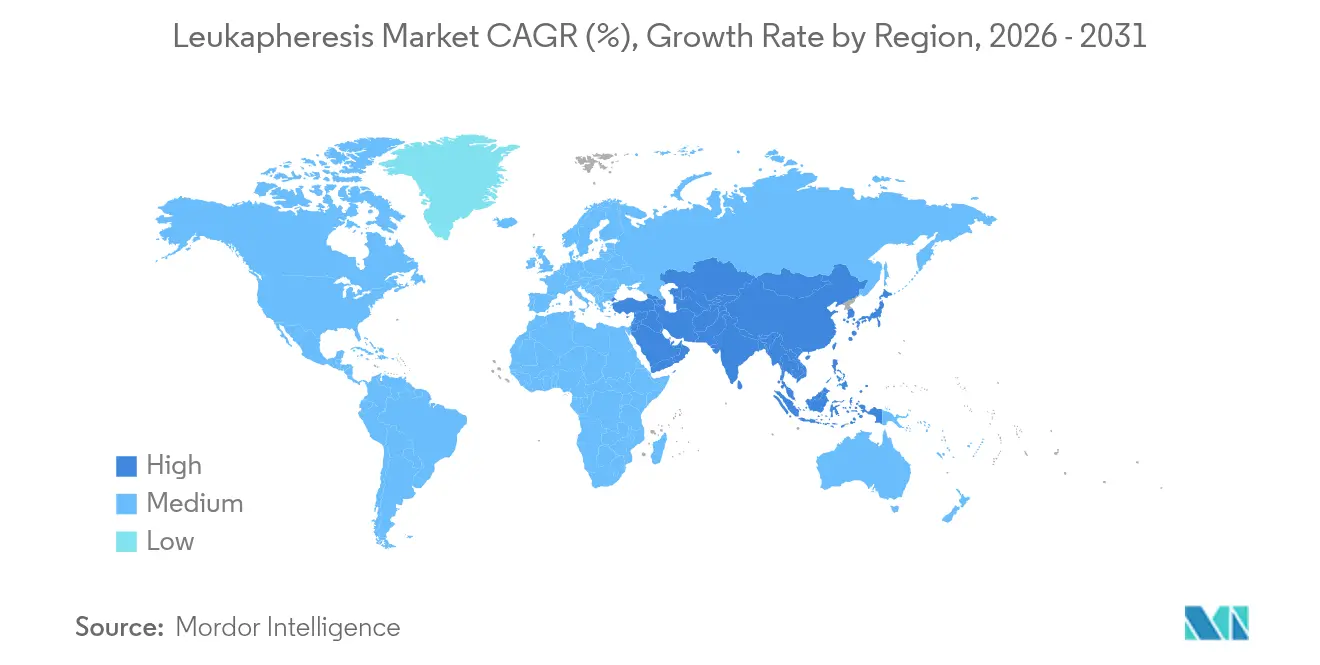

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

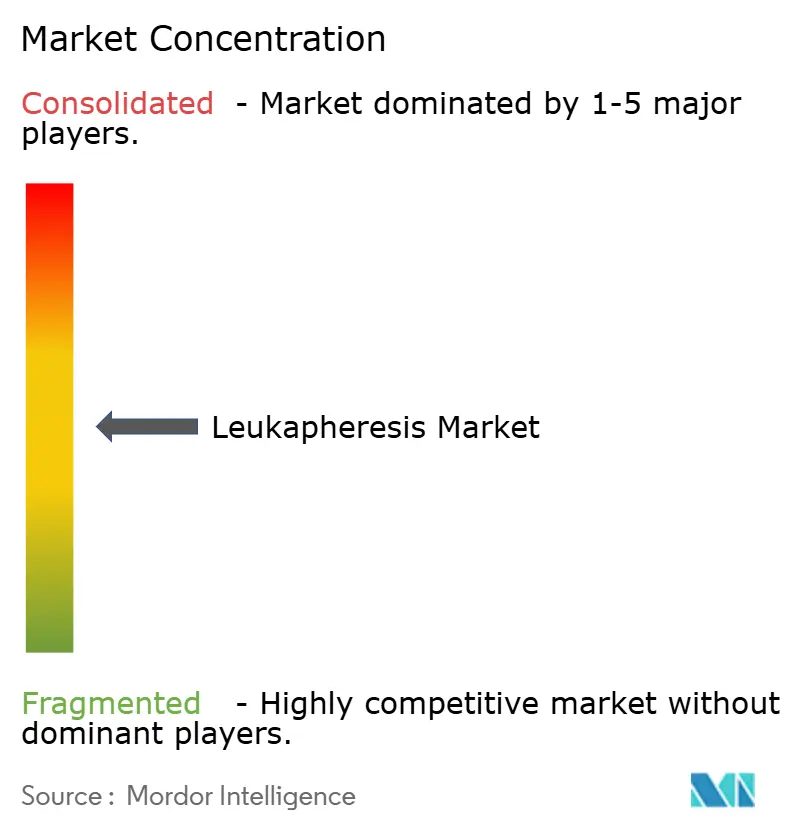

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Leukapheresis Market Analysis by Mordor Intelligence

The Leukapheresis Market size was valued at USD 229.81 million in 2025 and estimated to grow from USD 251.92 million in 2026 to reach USD 398.63 million by 2031, at a CAGR of 9.62% during the forecast period (2026-2031).

Rising leukemia incidence, accelerating CAR-T commercialization, and the shift toward automated continuous-flow apheresis systems anchor this expansion. Hospitals broaden therapeutic use beyond hyperleukocytosis, while cell-therapy manufacturers scale collection capacity to support autologous and emerging allogeneic pipelines. Investment in point-of-care devices and AI-guided donor scheduling improves throughput, easing the pressure created by skilled professional shortages. Cold-chain innovation safeguards cell viability during long-distance transport, lowering manufacturing failure rates and reinforcing demand for premium-quality leukopaks.

Key Report Takeaways

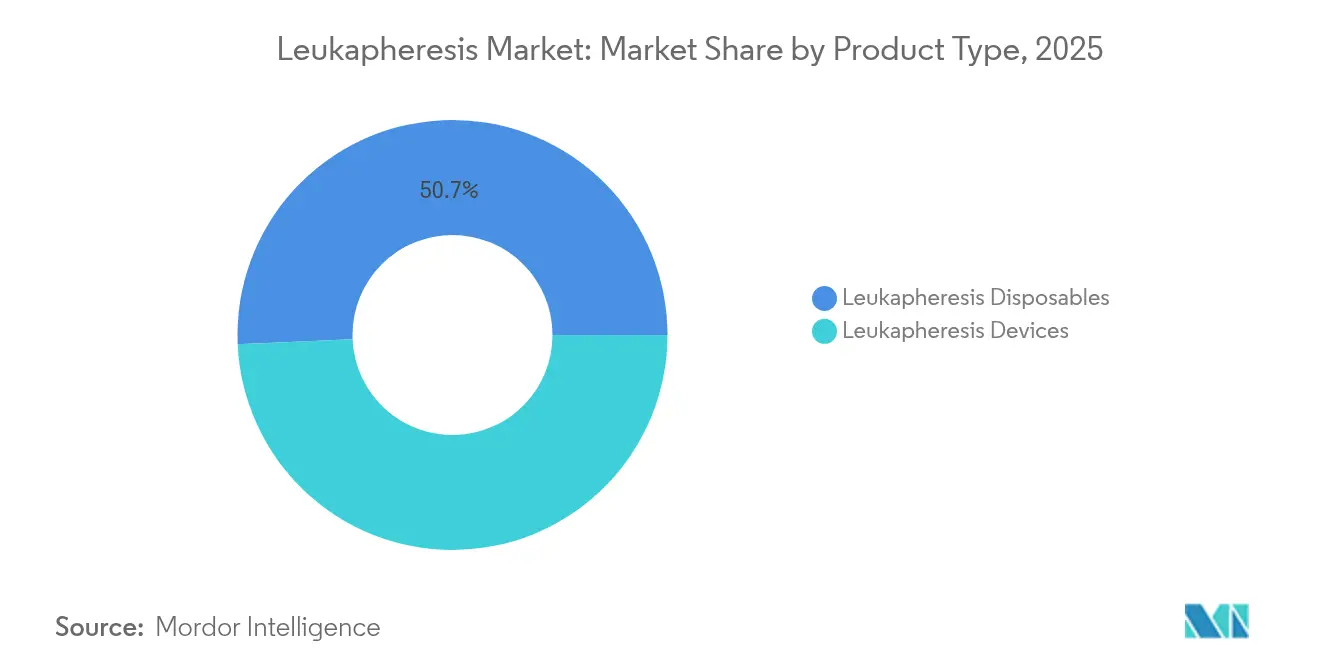

- By product type, leukapheresis disposables held 50.68% of leukapheresis market share in 2025, whereas devices are projected to advance at a 10.37% CAGR through 2031.

- By application, therapeutic procedures accounted for 63.05% of the leukapheresis market size in 2025; research use is forecast to expand at a 11.42% CAGR to 2031.

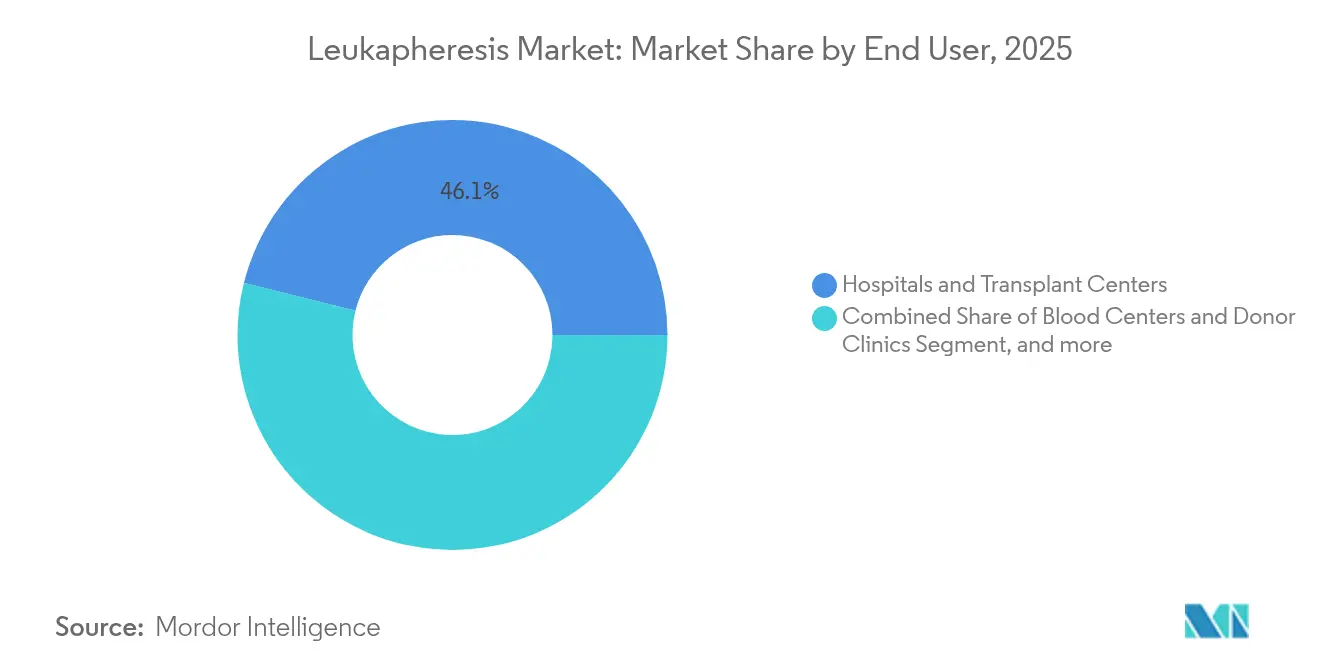

- By end user, hospitals and transplant centers captured 46.10% share of the leukapheresis market size in 2025, while cell- and gene-therapy manufacturers post the highest projected CAGR at 12.01% to 2031.

- By geography, North America led with 45.20% revenue share in 2025; Asia Pacific is on track for an 11.02% CAGR, the fastest regional growth.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Leukapheresis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Leukemia and Associated Hyperleukocytosis | +2.1% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Growing Need for High-Yield, Research-Grade Leukopaks | +1.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Rapid Expansion of CAR-T And Other Cell & Gene Therapy Manufacturing Facilities | +2.3% | Global, led by North America with significant APAC growth | Short term (≤ 2 years) |

| Widespread Uptake of Continuous-Flow Apheresis Systems | +1.5% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Shift Toward Point-of-Care Leukoreduction at the Bedside | +0.9% | North America & EU, pilot programs in APAC | Long term (≥ 4 years) |

| AI-Driven Donor Management and Scheduling Tools | +0.8% | North America & EU, gradual expansion globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Leukemia and Associated Hyperleukocytosis

Incidence curves for acute myeloid leukemia continue to climb, with global cases moving from 79,372 in 1990 to 144,645 in 2021 and trending toward 184,287 by 2040.[1]Peter Lee et al., “Global Burden of Leukemia,” BioMedical Engineering Online, biomedcentral.com Hyperleukocytosis, defined as white-blood-cell counts above 100,000/µl, demands urgent cytoreduction to prevent respiratory distress and neurologic complications.[2]R. H. Liu, “Management of Hyperleukocytosis,” ScienceDirect, sciencedirect.com Leukapheresis has therefore transitioned from elective therapy to standard emergency intervention. Male patients register steeper growth in incidence than females, while adults aged 80-84 exhibit the highest case density. Health-system protocols now automatically route eligible leukemia admissions to apheresis units, ensuring same-day access and cementing procedure volumes across tertiary centers in the leukapheresis market.

Growing Need for High-Yield, Research-Grade Leukopaks

CAR-T and natural-killer-cell manufacturers increasingly specify leukopaks that deliver 10 billion or more mononuclear cells per collection.[3]Biomol GmbH, “Leukopak Product Specification,” biomol.com Manufacturing failure rates correlate directly with starting-material quality; a compromised leukopak can invalidate a USD 300,000 manufacturing run.[4]Lisa Rein, “Cell Therapy Manufacturing Failures,” Cell & Gene, cellandgene.com Over 500 active clinical trials now depend on donor-derived immune cells, and the pivot toward allogeneic “off-the-shelf” therapies elevates recurring demand. Automated continuous-flow centrifugation secures tight leukocyte concentration windows and reduces red-cell contamination, streamlining downstream enrichment. Standardized donor-screening algorithms supported by AI scheduling software raise per-center capacity, enabling suppliers to meet escalating leukopaks requisitions without overtaxing staff.

Rapid Expansion of CAR-T and Other Cell & Gene-Therapy Manufacturing Facilities

Bristol Myers Squibb commissioned a 244,000 sq ft CAR-T plant in Massachusetts in 2025 to lift Breyanzi output. Every production slot begins with leukapheresis; capacity additions therefore deliver a direct linear pull on disposables and device placements. Median vein-to-vein times still span 3-5 weeks, creating a global race to shorten supply chains. Decentralized models, such as Excellos’ partnership with Galapagos, target 7-day cycles by colocating leukapheresis suites with modular vector lines. Equipment vendors now bundle regulatory-grade training and remote-monitoring services to help nascent sites pass validation faster, further broadening the leukapheresis market.

Widespread Uptake of Continuous-Flow Apheresis Systems

Systems like Spectra Optia offer automated interface management that tunes plasma-to-anticoagulant ratios in real time, cutting citrate toxicity events by 40% in published audits. Continuous-flow technology trims processing volumes, lowering procedure time and freeing staff to supervise additional chairs in high-throughput centers. When a large Midwest clinic moved to extended-hour shifts, it reduced peripheral-blood stem-cell collection sessions per patient from 3.2 to 1.7 within six months. Cloud-linked devices feed session data into AI scheduling tools, improving donor return rates and smoothing inventory across centers. The efficiency dividend justifies capital upgrades even for mid-volume sites, stimulating device growth within the leukapheresis market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Costs Associated with Therapeutic Leukapheresis Procedures | -1.4% | Global, most pronounced in emerging markets | Short term (≤ 2 years) |

| Regulatory Complexity in Donor Recruitment and Cross-Border Biologics Movement | -0.8% | Global, with highest impact in multi-national operations | Medium term (2-4 years) |

| Shortage of Skilled Apheresis Professionals | -1.1% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Viability Loss of Harvested Cells During Long-Distance Cold-Chain Transport | -0.6% | Global, particularly affecting remote and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Costs Associated with Therapeutic Leukapheresis Procedures

Patient invoices for single-dose CAR-T therapies routinely exceed USD 500,000 and reach USD 1 million in complex pediatric cases, with leukapheresis comprising a meaningful early share. Stand-alone private collection centers operate 32% cheaper than hospital-based settings, yet most low- and middle-income regions lack such facilities. Equipment depreciation, single-use kits, and mandatory sterility audits inflate baseline costs. Although Medicare’s 2025 rule broadened reimbursement definitions, coverage gaps linger in many public systems aabb.org. Until payors harmonize around bundled-payment models, high procedural outlay will temper demand in price-sensitive geographies.

Shortage of Skilled Apheresis Professionals

The National Marrow Donor Program warns that physician retirements will outpace new hematopoietic-cell-transplant specialists by 2027. Certified apheresis nurses also remain in short supply, and burnout risk rose during pandemic redeployments. While automated devices reduce manual tuning, real-time clinical decisions still require experienced oversight, especially when calcium shifts or hemodynamic instability arise. Certification boards respond by rolling out accelerated fellowships, yet the training pipeline trails the leukapheresis market’s demand curve. Vendors now fund remote-learning modules that cover equipment operation and quality-control protocols, but the talent gap persists as a structural headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Devices Reshape Collection Efficiency

Leukapheresis devices are expanding at a 10.37% CAGR from 2026-2031 as centers upgrade to continuous-flow platforms with optical-detection sensors. The leukapheresis market size for devices equaled USD 113.34 million in 2025 and is positioned to outpace disposables growth through the forecast. Spectra Optia’s algorithmic interface and the FDA-cleared Rika Plasma Donation System V2.1 exemplify device-level innovation. Product pipelines now include portable bedside units that target point-of-care leukoreduction in hematology wards and emergency departments.

Disposables retained 50.68% of leukapheresis market share in 2025 due to their single-use safety profile and recurring-revenue model. Elevated procedure volumes ensure consistent kit sales, reinforcing manufacturer cash flows and incentivizing investment in integrated tubing sets that cut priming times. Leukoreduction filters remain a mature niche, yet demand persists because many blood-bank protocols still enforce universal leukocyte reduction. Columns and cell separators support specialized pathogen-reduction workflows, though their penetration concentrates in academic centers. Overall, packaging disposables with capital-equipment leases locks in account loyalty, anchoring the segment’s leadership within the leukapheresis market.

By Application: Research Use Accelerates Innovation

Therapeutic indications commanded 63.05% of revenue in 2025 aided by guideline status for hyperleukocytosis and stem-cell mobilization. This dominance prevails even as the research segment logs a brisk 11.42% CAGR through 2031. More than 1,100 cell- and gene-therapy developers now require standardized leukopaks for vector optimization, potency assays, and release testing.

Diagnostic leukapheresis further widens the use case by boosting circulating-tumor-cell detection 30-fold over peripheral draws. FDA approvals for novel autologous products, such as afamitresgene autoleucel and obecabtagene autoleucel, validate procedure reliability in advanced oncology protocols. The dual track of established treatments and investigative pipelines keeps utilization high across hospital and industry settings, positioning research as a durable growth pillar for the leukapheresis market.

By End User: Manufacturers Capture Highest Growth

Hospitals and transplant centers accounted for 46.10% of 2025 revenue because they house patient-ready apheresis suites and manage first-line hyperleukocytosis care. Yet cell- and gene-therapy manufacturers show the sharpest trajectory at 12.01% CAGR through 2031. The leukapheresis market share controlled by commercial plants rose from 18% in 2022 to 23% in 2024 as firms internalized collection capacity to de-risk supply.

Blood centers and donor clinics retain a vital role as they recruit healthy donors for allogeneic trials, while academic institutions pilot advanced protocols and validate next-generation columns. Hybrid models now emerge: regional blood centers embed GMP suites to serve biotech clients, blending donor-acquisition strength with manufacturing infrastructure. University Hospitals in the United States processed 4,300 more leukopak samples in 2024 than 2023, signaling converging clinical and manufacturing priorities. This ecosystem evolution enhances overall procedure density and sustains broad-based growth for the leukapheresis market.

Geography Analysis

North America led the leukapheresis market with a 45.20% share in 2025. U.S. leadership stems from FDA regulatory clarity and unmatched CAR-T approval volume, including the 2024 clearances of afamitresgene autoleucel and obecabtagene autoleucel. Medicare’s 2025 reimbursement expansion for therapeutic apheresis further bolsters financial viability. Canada and Mexico contribute through cross-border clinical-trial networks and joint manufacturing initiatives that streamline donor logistics. Concentration of device makers such as Terumo BCT and Haemonetics within the region speeds tech adoption cycles, sustaining North America’s prime position in the leukapheresis market.

Europe remains a mature yet dynamic arena. EMA guidelines deliver consistent evaluation pathways for CAR-T products, fostering steady demand for high-performance leukapheresis systems. The European Blood Alliance campaigns for two million additional voluntary donors, incentivizing centers to adopt continuous-flow platforms that maximize platelet yield and donor comfort. Germany, France, and the United Kingdom invest in integrated apheresis suites tied to national cancer plans, while Italy and Spain expand regional cell-therapy nodes. Supply-chain resilience, particularly in cold-chain trucking, dominates investment agendas and stabilizes procedure throughput.

Asia Pacific posts the fastest growth at an 11.02% CAGR to 2031. Japan’s advanced geriatric care drives premium device uptake, whereas India benefits from government-backed cell-therapy clusters in Hyderabad and Bengaluru. Regulatory authorities in Australia and South Korea introduce accelerated review pathways mirroring FDA’s RMAT designation, catalyzing early commercial rollouts. Overall, infrastructure modernization, coupled with local manufacturing incentives, transitions Asia from technology import destination to fully integrated supply-chain hub in the leukapheresis market.

Competitive Landscape

The leukapheresis market is moderately concentrated. Terumo BCT anchors leadership through iterative device releases and strategic regional manufacturing. In 2024 the company secured FDA clearance for Rika Plasma Donation System V2.1 and consolidated its Global Therapy Innovations unit to merge apheresis and cell-therapy expertise. Fresenius Kabi competes on continuous-flow versatility, integrating software modules that support both plasma exchange and leukocyte collection within a single chassis. Haemonetics sharpened focus by selling its whole-blood assets to GVS for USD 67.1 million in December 2024, redeploying capital toward high-growth automated apheresis platforms.

Barriers to entry remain high due to stringent FDA Class II special controls that demand exhaustive safety validations for automated blood-cell separators. Long-cycle clinical contracting favors incumbents with proven uptime and 24-hour servicing capabilities. Nonetheless, niche entrants target AI-enhanced donor-management and optical-quality-control subsystems, creating collaboration opportunities rather than direct head-on rivalry. Blood-bank software firms integrate apheresis session data with predictive inventory models, reducing wastage and strengthening manufacturer switching costs. Overall, players differentiate on platform reliability and compliance expertise more than on price, reinforcing stable margins across the leukapheresis market.

Leukapheresis Industry Leaders

Asahi Kasei Medical Co. Ltd

Fresenius SE & Co. KGaA

Haemonetics Corporation

Macopharma

Terumo Blood & Cell Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Haemonetics Corporation completed the sale of whole-blood assets to GVS S.p.A. for USD 67.1 million, reallocating resources to automated apheresis solutions.

- November 2024: Terumo Blood and Cell Technologies launched its Global Therapy Innovations business unit to align apheresis and cell-therapy competencies across patient-care pathways.

- November 2024: Autolus Therapeutics gained FDA approval for Aucatzyl (obecabtagene autoleucel) for relapsed/refractory B-cell ALL, expanding CAR-T indications that rely on leukapheresis.

- October 2024: Excellos Inc. became the first decentralized manufacturing node in the Blood Centers of America network to support Galapagos’ CAR-T candidate GLPG5101, targeting a 7-day vein-to-vein interval.

Global Leukapheresis Market Report Scope

Leukapheresis is used to collect blood stem cells or specific immune cells to be used as part of stem cell/bone marrow transplants in treating certain blood cancers.

The leukapheresis market is segmented by type (leukapheresis devices (apheresis devices, leukapheresis columns, cell separators, and leukoreduction filters) and leukapheresis disposables), application (therapeutic applications, research applications), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value in USD for the above segments.

| Leukapheresis Devices | Apheresis Devices |

| Leukapheresis Columns & Cell Separators | |

| Leukoreduction Filters | |

| Leukapheresis Disposables |

| Therapeutic Applications |

| Research Applications |

| Blood Centers & Donor Clinics |

| Hospitals & Transplant Centers |

| Academic & Research Institutes |

| Cell- & Gene-Therapy Manufacturers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Leukapheresis Devices | Apheresis Devices |

| Leukapheresis Columns & Cell Separators | ||

| Leukoreduction Filters | ||

| Leukapheresis Disposables | ||

| By Application | Therapeutic Applications | |

| Research Applications | ||

| By End User | Blood Centers & Donor Clinics | |

| Hospitals & Transplant Centers | ||

| Academic & Research Institutes | ||

| Cell- & Gene-Therapy Manufacturers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected CAGR for the leukapheresis market from 2026 to 2031?

The market is forecast to grow at a 9.62% CAGR, rising from USD 251.92 million in 2026 to USD 398.63 million by 2031.

Which product category currently leads the leukapheresis market?

Leukapheresis disposables lead, holding 50.68% of 2025 revenue due to their single-use safety profile.

Why are cell- and gene-therapy manufacturers the fastest-growing end users?

Commercial CAR-T plants require in-house collection capacity, driving a 12.01% CAGR for this end-user segment.

Which region is expected to expand quickest, and why?

Asia Pacific is set for an 11.02% CAGR owing to infrastructure modernization, regulatory acceleration, and local manufacturing investments.

How do continuous-flow apheresis systems benefit collection centers?

They shorten procedure times, lower anticoagulant exposure, and allow AI-guided monitoring, collectively boosting throughput and donor safety.

Page last updated on: