Corneal Implants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

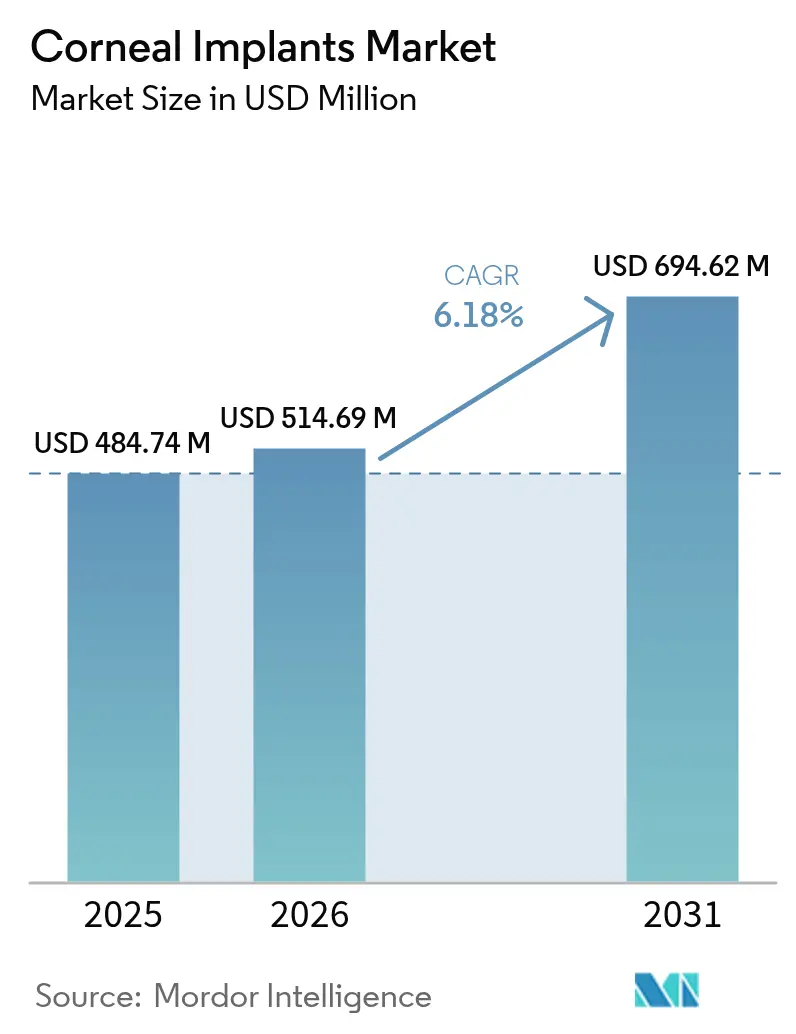

| Market Size (2026) | USD 514.69 Million |

| Market Size (2031) | USD 694.62 Million |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

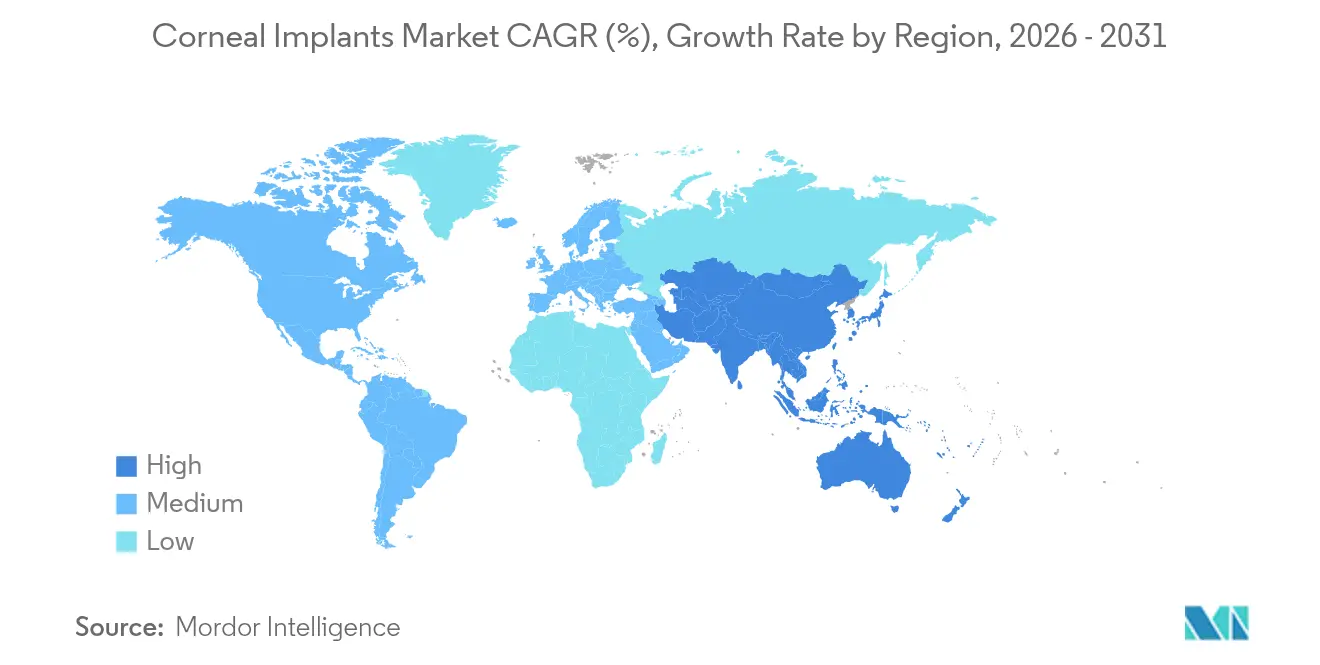

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corneal Implants Market Analysis by Mordor Intelligence

Corneal implants market size in 2026 is estimated at USD 514.69 million, growing from 2025 value of USD 484.74 million with 2031 projections showing USD 694.62 million, growing at 6.18% CAGR over 2026-2031. Growth reflects an industry-wide pivot from reactive corneal care toward proactive intervention, enabled by breakthroughs in artificial biomaterials, femtosecond-laser precision, and 3-D bioprinting. Aging populations enlarge the surgical pipeline while regenerative science expands the candidate pool to cases once deemed inoperable. North America currently dominates revenue because FDA breakthrough designations accelerate device launches, yet Asia-Pacific is the volume engine as rising screen usage drives new pathology. Supply-chain vigilance around medical-grade PMMA and hydrogel inputs remains critical, but the innovation tempo offsets most near-term disruptions.

Key Report Takeaways

- By implant type, human donor tissue led with 69.15% of corneal implants market share in 2025, while artificial implants are advancing at a 7.12% CAGR through 2031.

- By procedure type, penetrating keratoplasty accounted for 45.92% revenue in 2025; endothelial keratoplasty is the fastest-growing segment at 6.9% CAGR to 2031.

- By disease indication, keratoconus held 33.86% share in 2025, whereas Fuchs’ dystrophy solutions will grow 7.22% annually over the same period.

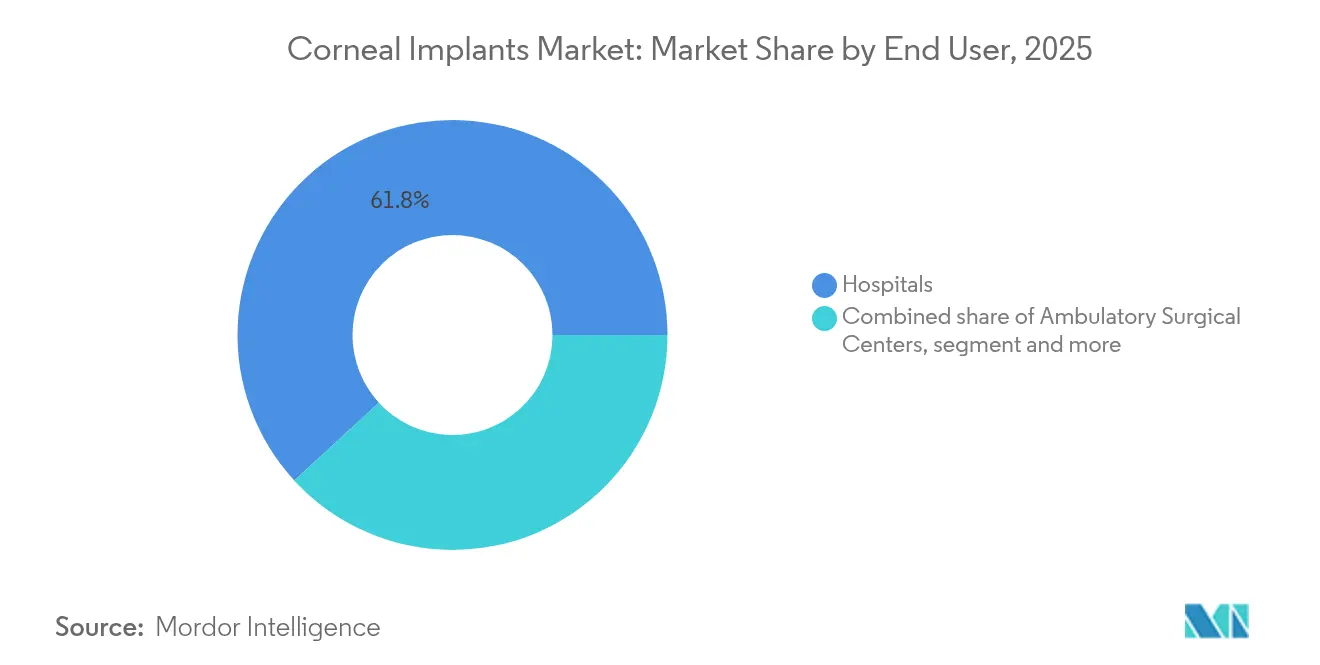

- By end user, hospitals captured 61.83% of the corneal implants market size in 2025; ambulatory surgical centers are projected to expand at 7.35% CAGR.

- By material, PMMA & other polymers led with 43.11% share in 2025; hydrogels are pacing the field with an 7.85% CAGR.

- By geography, North America commanded 50.92% revenue in 2025; Asia-Pacific is expected to post the quickest 7.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Corneal Implants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in corneal implants | +1.8% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Growing incidences of corneal disorders & blindness in elderly | +1.5% | Global, concentrated in aging populations of developed markets | Long term (≥ 4 years) |

| Rising adoption of minimally-invasive lamellar keratoplasty | +1.2% | North America & EU leading, APAC following | Medium term (2-4 years) |

| Advances in bioengineered synthetic endothelial layers | +1.0% | North America & EU core markets | Long term (≥ 4 years) |

| Expansion of eye-bank public-private partnerships in emerging markets | +0.8% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Surge in AI-based pre-operative corneal imaging | +0.7% | Global, with technology hubs leading adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in Corneal Implants

Cross-linked recombinant collagen scaffolds sustained clear corneal regeneration for four years, delivering mean corrected acuity of 20/54 without immunosuppression needs. Patient-specific 3-D-printed lenticules now match individual curvature, solving donor-shortage bottlenecks while lowering rejection risk. Kuragel hydrogel matrices show superior stromal integration versus legacy PMMA designs. Coupling femtosecond lasers with these bio-scaffolds reduces operating time and improves wound integrity. Collectively, these gains broaden the addressable base of the corneal implants market by upgrading clinical outcomes and surgeon confidence.

Growing Incidences of Corneal Disorders & Blindness in Elderly

Fuchs’ endothelial dystrophy affects 4% of U.S. adults over 40, with prevalence climbing steeply after age 60. Medicare data links advanced cases to rising treatment spending, underscoring the economic imperative for definitive surgical cures. Longer life expectancy and heavy digital-device use exacerbate dry-eye and accelerates surface degeneration. Improved safety profiles entice older patients who previously deferred surgery, propelling steady procedure growth.

Rising Adoption of Minimally-Invasive Lamellar Keratoplasty

Ten-year follow-up shows Descemet membrane endothelial keratoplasty (DMEK) with 75% graft survival and only 10% rejection, outclassing full-thickness techniques.[1]F. Scaffidi, “Long-Term Outcomes after DMEK,” Nature, nature.com Shorter healing times and lower astigmatism improve quality-of-life metrics. Uptake of office-based suites grew from 0.5% in 2020 to 2.2% in early 2023, signaling confidence in streamlined settings. Enhanced imaging guides precise tissue dissection, dropping the learning curve and hastening diffusion.

Advances in Bioengineered Synthetic Endothelial Layers

Pandorum Technologies secured USD 11 million in 2024 for Kuragenx exosome-rich hydrogel, slated for first-in-human trials in 2025. Porcine collagen constructs restored vision to 20/36 on average and carry 2-year shelf life. Mass Eye and Ear’s CALEC therapy achieved 93% ocular-surface restoration at 12 months. These shelf-stable, donor-independent options unlock new capacity in regions with limited eye-banking.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of keratoprosthesis & surgery | -1.5% | Global, particularly acute in emerging markets | Medium term (2-4 years) |

| Availability of alternative treatments (CXL, IOLs) | -1.2% | Developed markets with advanced treatment options | Short term (≤ 2 years) |

| Supply-chain bottlenecks for medical-grade PMMA & hydrogels | -0.8% | Global manufacturing hubs, cascading to all markets | Short term (≤ 2 years) |

| Post-keratoplasty microbial keratitis risk | -0.5% | Global, with higher impact in regions with limited post-op care | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Keratoprosthesis & Surgery

A single Boston Keratoprosthesis procedure can exceed USD 30,000 once lifelong follow-up is factored. Reimbursement growth lags inflation, curbing facility investment. Device makers also face 20% of revenue tied to supply-chain expenses, challenging price flexibility. Consequently, cash-strapped health systems delay adoption or choose donor grafts instead.

Availability of Alternative Treatments

Epi-on corneal cross-linking is on track for FDA clearance in 2025, offering non-surgical halting of keratoconus progression. Premium intraocular lenses now deliver high-definition acuity with minimal dysphotopsia, diverting some refractive cases away from transplantation. Twelve-year follow-up finds only 4.3% of CXL patients showing disease progression, rivaling graft durability.[2]R. Koppen, “Twelve-Year Stability after Epi-On Cross-Linking,” Journal of Clinical Medicine, mdpi.com These modalities shrink the pool eligible for implants, at least in early disease stages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Implant Type: Artificial Gains Despite Donor Dominance

Human donor grafts provided 69.15% of corneal implants market revenue in 2025, supported by decades of surgical standardization. Artificial devices, however, are growing 7.12% per year as breakthrough designations speed approvals. EyeYon Medical’s EndoArt membrane cut mean central corneal thickness from 759 µm to 613 µm at 12 months, validating synthetic viability. The Boston Keratoprosthesis tops 20,000 implants worldwide. Newer hydrogel-based optics now promote cellular in-growth, a marked upgrade over inert PMMA. Collectively, these trends reposition the artificial slice of the corneal implants market for sustained share capture through 2031.

Continued donor shortages sustain waitlists, prompting surgeons to trial synthetic options even as they refine tissue matching algorithms in eye banks. Manufacturing scale-up keeps average device costs on a gradual downward path, though specialty follow-up still commands premium fees. Convergence of bioprinting and collagen scaffolds is expected to lift the corneal implants market size for artificial devices at the fastest clip within this decade.

By Procedure Type: Endothelial Techniques Drive Innovation

Penetrating keratoplasty retained 45.92% of global revenue during 2025, yet endothelial keratoplasty is tracking a 6.9% CAGR on superior visual recovery profiles. A 75% 10-year graft survival rate with minimal rejection propels surgeon preference for DMEK. Laser-assisted incisions lower induced astigmatism, which once deterred adoption. Cell-therapy infusions under development promise to merge pharmacologic convenience with surgical durability.

Rising comfort with partial-thickness grafts is redirecting capital budgets toward lamellar instrumentation. The corneal implants market share held by full-thickness techniques will likely shrink as payers reward quicker rehabilitation and fewer complications. Training programs now prioritize lamellar skills, reinforcing momentum.

By Disease Indication: Fuchs’ Dystrophy Emerges as Growth Driver

Keratoconus dominated with 33.86% revenue in 2025, but Fuchs’ dystrophy therapies are on a 7.22% growth trajectory as population aging surges endothelial disease prevalence. Diagnostic AI flags early stromal edema, allowing timely surgical referral and reducing graft failure risk. Medicare’s rising spend on Fuchs’ management underlines the economic stakes.

Cell-based injectable therapies and Descemet stripping only (DSO) procedures widen treatment choice. As these innovations scale, the corneal implants market size for endothelial disorders is set to overtake anterior pathology segments across many advanced economies before 2031.

By End User: ASCs Capitalize on Outpatient Shift

Hospitals held 61.83% revenue in 2025 thanks to complex-case capacity and eye-bank affiliations. Ambulatory surgical centers, expanding 7.35% annually, capture routine grafts by coupling lower facility fees with same-day discharge protocols. Medicare reimburses corneal tissue separately via HCPCS V2785, sustaining ASC margins.

Efficiency-driven private equity investment fuels ASC build-outs, while portable femtosecond lasers cut capital-equipment barriers. The corneal implants market now sees a steady migration of lamellar cases to outpatient venues, freeing hospital theaters for high-acuity revisions.

By Material: Hydrogels Drive Innovation Surge

PMMA and allied polymers contributed 43.11% of 2025 revenue, anchored by the Boston Type I device. Surface nano-hydroxyapatite coatings now elevate biointegration, shrinking sterile melt risk. Hydrogels, meanwhile, register an 7.85% CAGR, buoyed by injectable formats permitting micro-incision delivery and in-situ curing.

Bio-engineered collagen lenticules boosted corneal thickness by up to 285 µm in early trials, restoring functional vision without donor tissue removal. University of Melbourne’s Hygelix scaffold mirrors Descemet’s membrane porosity, fostering nutrient diffusion.These advances should widen the corneal implants market share for hydrogel-based constructs over the medium term.

Geography Analysis

North America controlled 50.92% of global revenue in 2025 owing to FDA breakthrough pathways, eye-bank maturity, and Medicare’s separate tissue reimbursement. Academic hubs such as Mass Eye and Ear partner with device firms to pilot next-gen implants, sustaining a tight innovation loop. Breakthrough designations for products like EndoArt further shorten time-to-clinic. Even so, supply-chain vigilance around PMMA imports remains on strategic watchlists.

Asia-Pacific is the fastest-advancing territory with an 7.7% CAGR through 2031. India alone carries 6.8 million corneal-blind individuals, adding 25,000–30,000 new cases yearly. Eye-bank deficits and surgeon shortages open space for shelf-stable synthetics. Government blindness-eradication drives plus rising middle-class spending underpin procedure volume growth, cementing the region as a critical demand node for the corneal implants market.

Europe shows steady uptake under the Medical Device Regulation introduced in 2022. Recent CE marks for advanced optics illustrate regulators’ receptivity to innovation. Germany’s ophthalmic sector booked EUR 2,066.1 million revenue in fiscal 2024, underscoring industrial depth. First-in-region EndoArt implants in elderly patients underscore readiness to adopt artificial solutions when donor tissue proves infeasible. Cost-effectiveness requirements continue to shape purchase decisions but rarely stifle novel, outcome-improving therapies.

Competitive Landscape

Market structure is moderately fragmented: a handful of long-established device makers such as KERAMED INC. and CorNeat Vision anchor the field, while academic institutes like Mass Eye and Ear supply clinical validation for emerging technologies. This balance keeps average selling prices stable and encourages cross-licensing when smaller firms hold critical patents. Heightened regulatory clarity after multiple FDA breakthrough designations now favors firms with robust quality systems, accelerating time-to-market for well-capitalized entrants.

Strategic collaborations illustrate the sector’s adaptive posture. In March 2025 Pantheon Vision paired with Eyedeal Medical to automate lens-blank production and secure diversified PMMA supply lines. EyeYon Medical’s EndoArt synthetic endothelial layer completed a 24-patient first-in-human series that cut average central corneal thickness by 146 µm at 12 months, positioning the device for wider regulatory filings. Pandorum Technologies raised USD 11 million in June 2024 to advance its Kuragenx “Liquid Cornea” hydrogel toward clinical trials, signaling investor confidence in regenerative approaches. These moves highlight how partnerships, clinical milestones and funding rounds remain primary levers for competitiveness rather than price wars.

Technology convergence is reshaping competitive moats. AI-assisted corneal topography now detects keratoconus with 96.06% accuracy, and vendors integrating such software with implant portfolios enjoy stronger surgeon loyalty. Supply-chain resilience has become a differentiator; firms with dual-region polymer sourcing avoided 2024 raw-material shortages that slowed rivals. Intellectual-property filings around collagen cross-link chemistry and injectable hydrogels climbed 18% year-on-year, suggesting that material science advances will dictate future winners. Overall rivalry stays disciplined as companies prioritize evidence-backed innovation over aggressive discounting, sustaining healthy margins for reinvestment in R&D.

Corneal Implants Industry Leaders

CorneaGen

CorNeat Vision

Aurolab

KERAMED, INC.

LinkoCare LifeSciences AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Pantheon Vision partnered with Eyedeal Medical to expand corneal-implant manufacturing capacity.

- June 2024: EyeYon Medical announced the first UK implantation of the EndoArt synthetic endothelial membrane in a 91-year-old patient.

- June 2024: Pandorum Technologies raised USD 11 million to advance Kuragenx “Liquid Cornea” toward clinical trials.

- April 2024: Pantheon Vision held a pre-market approval meeting with the FDA for its artificial corneal platform.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the corneal implants market as the total annual value of human donor grafts and synthetic keratoprostheses surgically placed to replace opaque or ectatic corneal tissue and restore functional vision. We, therefore, measure revenue generated from finished implant devices supplied to hospitals, ambulatory surgical centers, and ophthalmic clinics worldwide.

Scope Exclusions: Devices used only for corneal diagnostics or measurement (pachymeters, topographers) and post-operative pharmaceuticals are outside the study.

Segmentation Overview

- By Implant Type

- Artificial Corneal Implant

- Human Donor Corneal Implant

- By Procedure Type

- Endothelial Keratoplasty

- Penetrating Keratoplasty

- Anterior Lamellar Keratoplasty

- Intrastromal Corneal Ring Segment Implantation

- By Disease Indication

- Keratoconus

- Fuchs’ Dystrophy

- Infectious Keratitis

- Corneal Ulcers

- Corneal Edema

- Other Indications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Ophthalmic Specialty Clinics

- Others

- By Material

- Collagen-based Biomaterials

- PMMA & Other Polymers

- Hydrogels & Hydrophilic Acrylic

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with corneal surgeons, eye-bank procurement heads, biomaterial scientists, and reimbursement advisers across North America, Europe, Asia-Pacific, and the Gulf help us cross-check annual procedure counts, synthetic graft pricing, donor tissue discard rates, and regulatory lead times. This process fills gaps left by desk research and guides assumption ranges.

Desk Research

Mordor analysts begin with public domain baselines, drawing on tier-one statistics from the Eye Bank Association of America, World Health Organization blindness registries, Eurostat surgical discharge datasets, India's National Program for Control of Blindness, and peer-reviewed journals indexed on PubMed. Company filings and investor decks further clarify pipeline adoption timelines. Subscription resources such as D&B Hoovers for financial splits, Dow Jones Factiva for transaction alerts, and Questel for patent families add depth where public data thin out. The sources listed are illustrative; many additional records support our evidence build-up.

Market-Sizing & Forecasting

A top-down reconstruction starts with country-level keratoplasty volumes and synthetic implant shipments, which are then multiplied by average selling prices adjusted for currency and care-setting mix. Supplier roll-ups and sampled hospital invoices offer selective bottom-up corroboration, enabling calibration. Key model inputs include: 1) keratoplasty incidence trends, 2) synthetic device penetration, 3) donor rejection/discard ratios, 4) average surgery cost inflation, and 5) approval timelines for next-generation polymers. Multivariate regression of these drivers, supplemented by scenario analysis around donor availability shocks, underpins the 2025-2030 outlook.

Data Validation & Update Cycle

Outputs undergo variance checks against independent procedure tallies, exchange-rate audits, and year-on-year growth hygiene tests. A senior analyst reviews anomalies before release. Reports refresh annually, while material device recalls, landmark approvals, or policy shifts trigger interim revisions so clients receive the latest view.

Why Mordor's Corneal Implants Baseline Earns Trust

Published estimates seldom align because firms choose dissimilar scope, equation drivers, and refresh cadence. By centering on implant-only revenue, using verified surgery counts, and revisiting models every twelve months, Mordor Intelligence keeps its baseline tightly anchored to real-world signals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 484.74 Mn (2025) | Mordor Intelligence | |

| USD 525.73 Mn (2025) | Global Consultancy A | Bundles ocular implants broadly and applies uniform global ASP, limiting granular price realism |

| USD 482.60 Mn (2024) | Trade Journal B | Relies on shipment data without regional price dispersion or clinical wastage adjustment |

| USD 446.00 Mn (2023) | Industry Association C | Counts donor grafts only, omitting synthetic keratoprosthesis and emerging-market uptake |

Differences arise mainly from scope breadth and input rigor. By balancing validated procedure data with disciplined price tracking and timely model refreshes, Mordor delivers a transparent, repeatable baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current value of the corneal implants market?

The corneal implants market reached USD 514.69 million in 2026 and is on course to hit USD 694.62 million by 2031.

Which region is growing fastest for corneal implant procedures?

Asia-Pacific is expanding at an 7.7% CAGR thanks to rising healthcare access and a high burden of untreated corneal blindness.

Why are artificial corneas gaining traction?

Synthetic devices bypass donor shortages, offer shelf stability up to two years, and have shown durable clinical outcomes in early trials.

Which surgical technique is seeing the quickest uptake?

Endothelial keratoplasty, especially DMEK, is advancing at 6.9% CAGR due to superior vision recovery and lower rejection risk.

How are ambulatory surgical centers influencing the market?

ASCs provide cost-efficient, same-day corneal procedures and are growing 7.35% annually, shifting volume away from hospitals.

Page last updated on: