IoT Professional Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

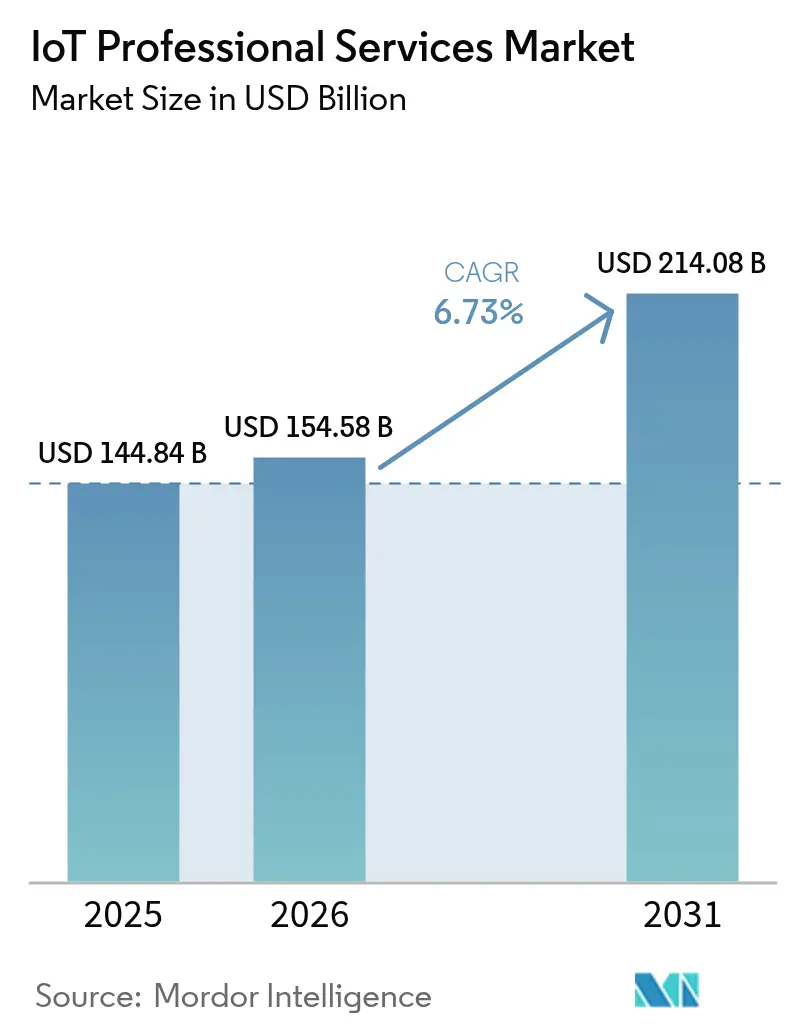

| Market Size (2026) | USD 154.58 Billion |

| Market Size (2031) | USD 214.08 Billion |

| Growth Rate (2026 - 2031) | 6.73% CAGR |

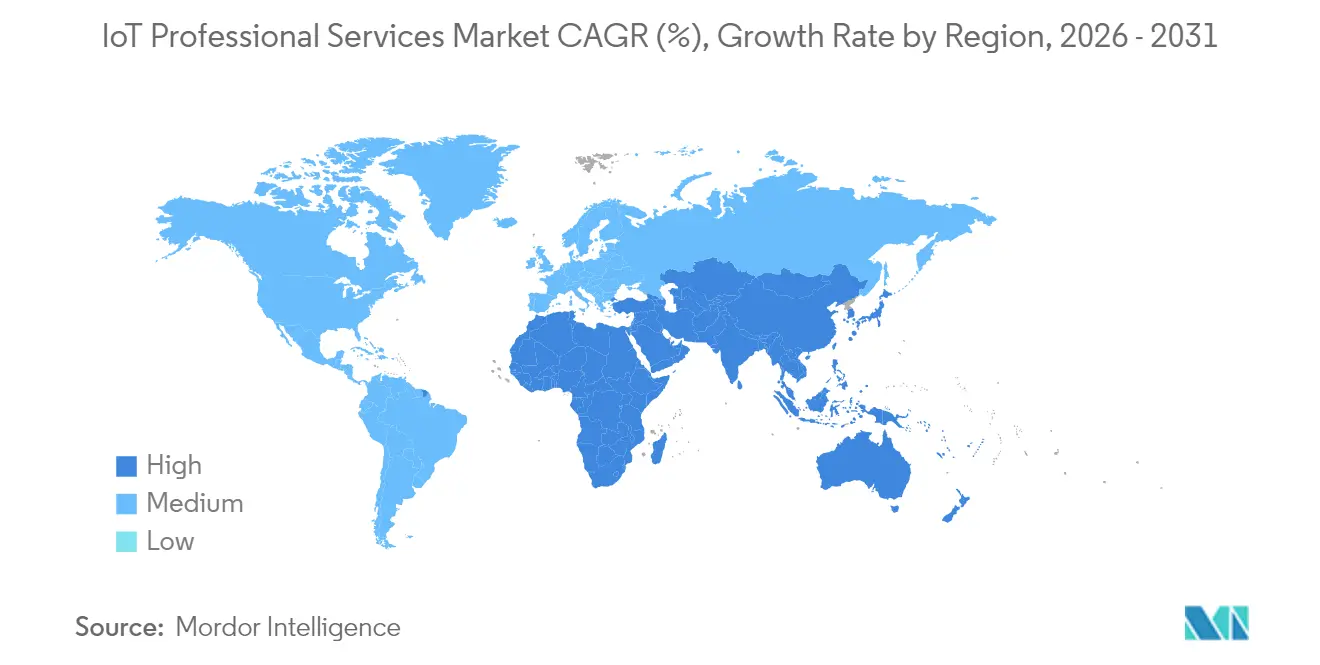

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

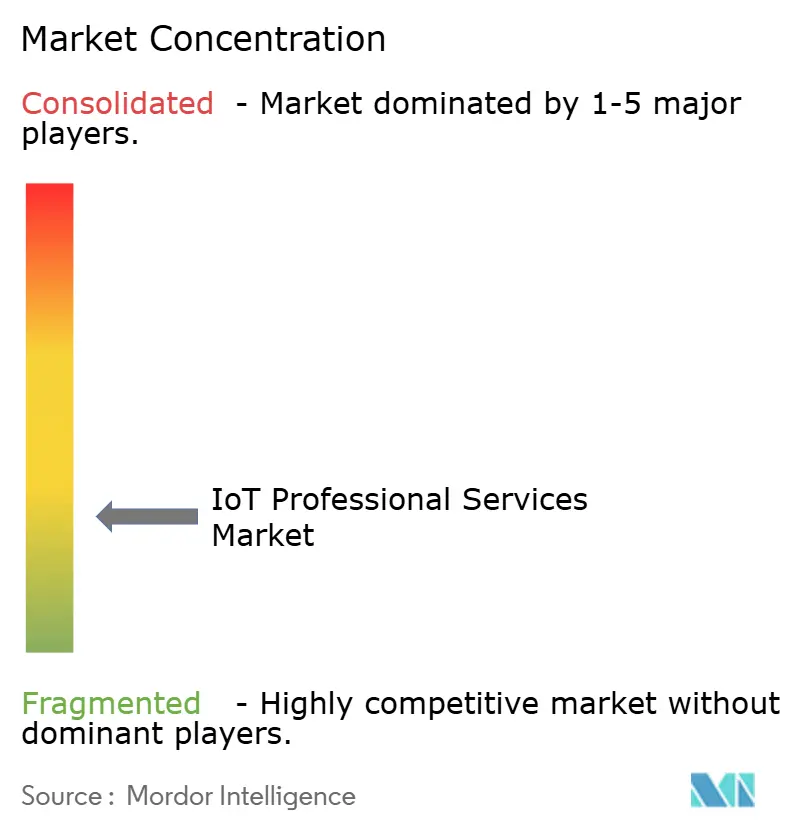

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IoT Professional Services Market Analysis by Mordor Intelligence

The IoT professional services market size was valued at USD 144.84 billion in 2025 and estimated to grow from USD 154.58 billion in 2026 to reach USD 214.08 billion by 2031, at a CAGR of 6.73% during the forecast period (2026-2031). Expanding connected-device ecosystems, 5G rollouts, and edge-computing investments are moving enterprises from experimentation to full-scale deployments that require specialized consulting, system integration, and managed-service expertise. Outcome-based pricing, domain-specific solutions, and regulatory mandates around Industry 4.0 are reshaping how suppliers package and deliver value. Demand is strongest where device volumes and data-driven business models converge, yet rising cyber-risk and talent shortages temper near-term growth expectations. Overall, the IoT professional services market is transitioning from fragmented project work to recurring, platform-enabled engagements that link technology performance to business outcomes.

Key Report Takeaways

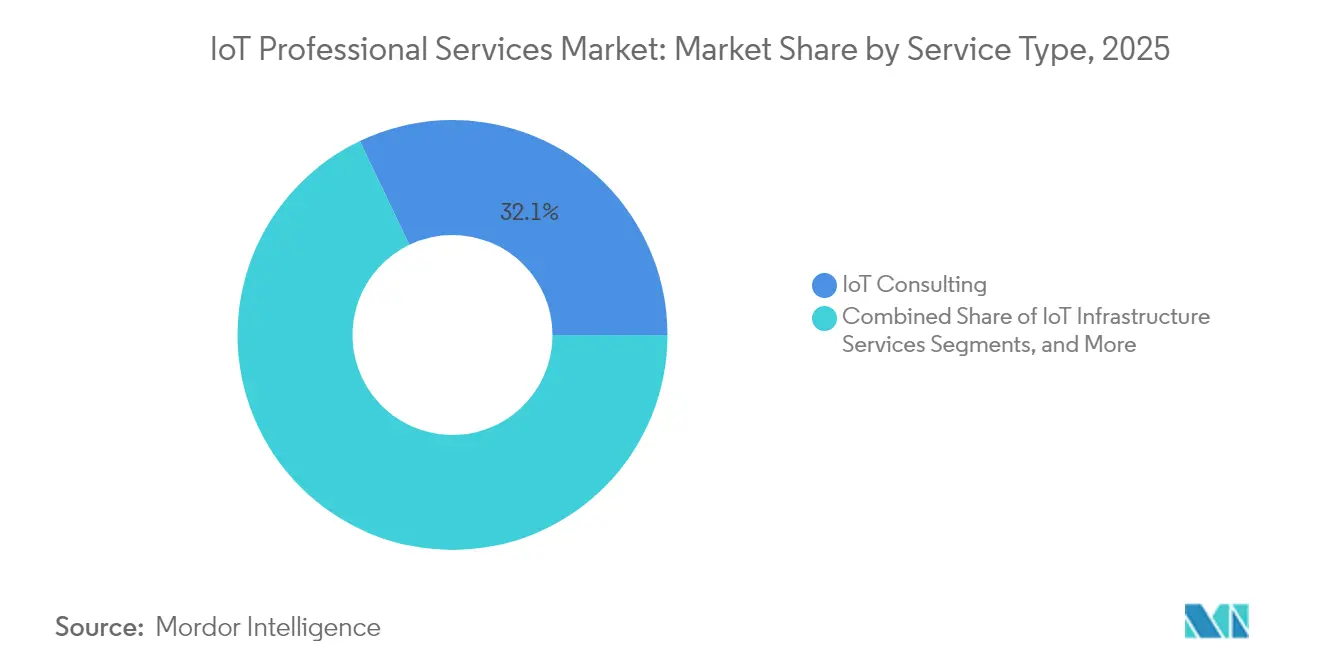

- By service type, IoT consulting led with 32.10% of the IoT professional services market share in 2025, while system design and integration is expanding at a 7.05% CAGR through 2031.

- By organization size, large enterprises accounted for 63.05% of demand in 2025; SMEs record the highest projected CAGR at 7.28% to 2031.

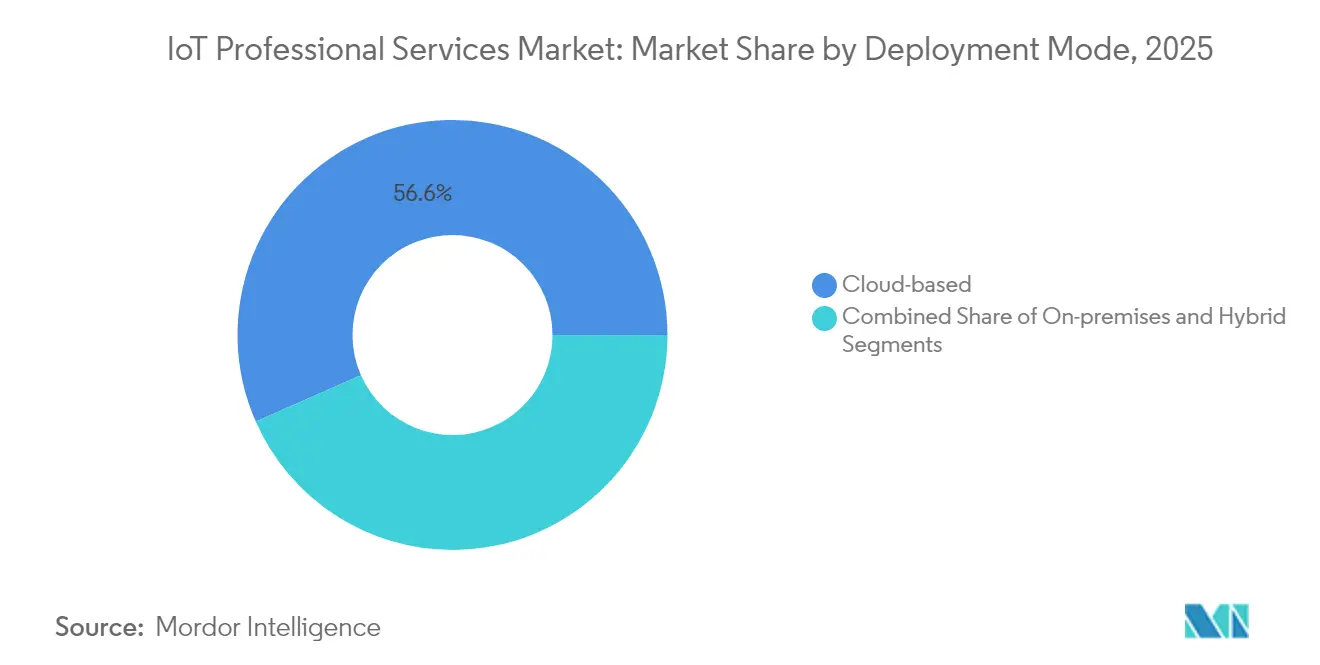

- By deployment mode, cloud-based delivery held 56.60% share of the IoT professional services market size in 2025 and is rising at an 8.08% CAGR.

- By end-user industry, manufacturing captured 25.45% revenue share in 2025, whereas healthcare is set to grow at 7.52% CAGR through 2031.

- By geography, North America retained 36.95% share in 2025, but Asia Pacific is on track for an 7.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IoT Professional Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of connected devices and falling sensor costs | +1.8% | Global, with Asia-Pacific leading adoption | Medium term (2-4 years) |

| Enterprise digital-transformation roadmaps | +1.5% | North America and EU primary, Asia-Pacific emerging | Long term (≥ 4 years) |

| 5G and edge-computing rollout | +1.2% | North America, China, South Korea early deployment | Medium term (2-4 years) |

| Regulatory push for Industry 4.0 and smart infrastructure | +0.9% | EU, Japan, Singapore policy-driven | Long term (≥ 4 years) |

| Outcome-based pricing models for IoT services | +0.6% | Global, with enterprise focus | Short term (≤ 2 years) |

| AI-driven AIOps platforms creating integration demand | +0.8% | North America, China, advanced economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Connected Devices and Falling Sensor Costs

Global connected-device volumes climbed to 18.8 billion units, stretching enterprise capacity to manage diverse hardware, firmware, and communication protocols. Lower sensor prices make large-scale rollouts financially viable, yet device heterogeneity magnifies lifecycle-management complexity. Professional-service partners are therefore asked to design provisioning, configuration, and monitoring frameworks that accommodate multivendor fleets. Lightweight M2M, Zero-Touch onboarding, and secure element authentication are gaining traction as best-practice blueprints. Edge-computing investment, projected to total USD 378 billion by 2028, further amplifies demand for integration services that balance on-premises processing with cloud analytics.

Enterprise Digital-Transformation Roadmaps

Boards increasingly treat IoT data as a strategic asset, folding connected-device projects into broader digital-core programs. IBM reported USD 4.96 billion in consulting revenue tied to digital-transformation engagements, underscoring the shift from isolated pilots to enterprise-wide modernization.[1]International Business Machines Corporation, “2024 Annual Report,” ibm.comService providers are now evaluated on their ability to map operational KPIs to sensor architectures and analytics pipelines that deliver measurable ROI. Outcome-based pricing is gaining favor as buyers demand guarantees on uptime, cost savings, or revenue uplift. As digital cores mature, demand rises for managed-service wraps that continuously optimize device, network, and application performance.

5G and Edge-Computing Rollout

Ultra-reliable low-latency communication enabled by 5G permits time-critical automation that was infeasible on legacy networks. GSMA case studies cite 15–20% productivity gains in smart-factory settings when 5G and edge analytics are combined.[2]GSMA, “Digital Nations Report 2024,” gsma.com To unlock these benefits, enterprises need partners versed in network slicing, private-core deployment, and edge-orchestration tooling. Integrators are packaging reference architectures that blend radio-access, MEC nodes, and IoT platforms into turnkey stacks. The result is a sizable addressable market for planning, spectrum strategy, site engineering, and KPI-driven optimization services.

Regulatory Push for Industry 4.0 and Smart Infrastructure

Policy initiatives such as Malaysia’s Industry4WRD, which targets a 30% productivity uplift in manufacturing, create structured demand for compliance-oriented IoT consulting.[3]Ministry of International Trade and Industry, “Industry4WRD Policy Blueprint,” miti.gov.my In the EU, forthcoming cybersecurity labeling rules oblige manufacturers to embed security-by-design, prompting a surge in certification and audit engagements. Singapore’s multilevel Cybersecurity Labelling Scheme exerts similar pressure in Southeast Asia. Providers able to pair technical depth with regulatory fluency are capturing premium fees for gap assessments, remediation roadmaps, and certification support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cyber-security concerns | -1.4% | Global, with EU GDPR compliance focus | Short term (≤ 2 years) |

| Interoperability and standards fragmentation | -1.1% | Global, particularly affecting SME adoption | Medium term (2-4 years) |

| Shortage of skilled IoT talent | -0.9% | North America, EU, developed markets | Long term (≥ 4 years) |

| Carbon-footprint scrutiny of hyperscale cloud workloads | -0.3% | EU, North America sustainability mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cyber-Security Concerns

Ordr found 82% of healthcare IoT environments host at least one serious vulnerability, fuelling board-level anxiety over ransomware, safety risks, and regulatory fines. Enterprises therefore require layered defenses ranging from secure-boot chips to encrypted data pipelines and micro-segmented networks. The skills needed cut across embedded security, OT protocols, and cloud IAM, yet most IT teams remain understaffed. Service providers investing in SOC-as-a-service, red-team testing, and zero-trust reference architectures are best placed to convert security fears into multi-year retainer contracts.

Interoperability and Standards Fragmentation

Competing protocols such as MQTT, OPC UA, LoRaWAN, and 3GPP LPWA complicate cross-vendor collaboration, especially for SMEs that lack in-house architects. Integration projects often stall while teams reconcile data models, quality-of-service settings, and management APIs. Middleware accelerators, API gateways, and pre-certified device libraries are emerging to bridge gaps, but professional-service expertise remains essential to map disparate systems into coherent digital threads. Fragmentation therefore slows adoption, yet also creates recurring revenue for integrators able to deliver vendor-agnostic blueprints and reference kits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Consulting Leads Integration Growth

IoT consulting retained 32.10% revenue share in 2025, reflecting sustained demand for vendor-neutral strategy, ROI modeling, and business-case validation. System design and integration, however, is expanding at a 7.05% CAGR as enterprises convert roadmaps into production rollouts that involve complex middleware, data lake, and analytics orchestration. Providers differentiate via domain accelerators, reference architectures, and outcome-based contracts that link fees to plant-floor uptime or energy-efficiency gains. The IoT professional services market size for design and integration is projected to widen sharply as 5G and edge projects graduate from pilot to scale.

Momentum is also building in managed-service wraps that combine device monitoring, predictive maintenance, and remote-update orchestration. Suppliers bundle platform subscriptions with SLA-backed operations centers to secure annuity revenue and deepen client lock-in. As integration complexity rises, tooling investments in CI/CD for firmware, digital twin simulation, and AI-driven test automation become table stakes for staying competitive in the IoT professional services market.

By Organization Size: SME Acceleration Drives Market Expansion

Large enterprises generated 63.05% of 2025 spending due to diversified portfolios, global supply chains, and sizeable modernization budgets. Yet SMEs are the fastest-growing buyer group at a 7.28% CAGR, enabled by pay-as-you-go cloud platforms that cut capital outlay and compress deployment timelines. For SMEs, service partners must offer packaged starter kits, modular pricing, and financing bridges that align costs with near-term cash flows. Providers that tailor governance templates, security baselines, and ROI dashboards to resource-constrained teams gain decisive advantage within this swelling sub-segment of the IoT professional services market.

In larger accounts, volume scale yields multi-tower engagements that span advisory, integration, and managed run operations. Projects often feature phased global rollouts coordinated through hybrid delivery centers. In contrast, SME deals emphasize rapid time to value, pre-configured integrations with ERP and CRM, and vertical templates such as cold-chain monitoring or energy sub-metering. This bifurcation forces suppliers to run dual go-to-market motions, preserving depth for Fortune 500 clients while industrializing delivery for high-velocity SME opportunities across the IoT professional services market.

By Deployment Mode: Cloud Dominance Accelerates

Cloud-based delivery captured 56.60% revenue share in 2025 and is expanding at an 8.08% CAGR. Buyers appreciate elastic scaling, built-in AI services, and consumption billing that aligns spend with data volume. Edge-to-cloud reference architectures dominate RFP requirements, with Kubernetes-based orchestration linking on-premises gateways to hyperscale AI engines. The IoT professional services market size for cloud implementations is forecast to outpace on-premises projects by more than 2:1 during the outlook period.

On-premises deployments persist in regulated domains such as defense, utilities, and pharma, where data residency and deterministic latency remain non-negotiable. Hybrid models are therefore gaining ground, blending local processing for critical workloads with cloud analytics for non-sensitive insights. Service partners must master container portability, multi-cloud policy enforcement, and FinOps disciplines to optimize total cost of ownership across mixed environments in the IoT professional services market.

By End-User Industry: Healthcare Disrupts Manufacturing Leadership

Manufacturing commanded 25.45% of 2025 revenue, leveraging IoT for predictive maintenance, quality assurance, and real-time asset tracking. Smart-factory deployments now lean heavily on edge AI for defect detection and energy optimization, fueling continuous demand for plant-floor integration and OT-IT convergence skills. Nevertheless, healthcare is the fastest-growing vertical at a 7.52% CAGR, propelled by remote patient monitoring, smart infusion pumps, and asset-location services. As hospitals modernize legacy infrastructure and pursue value-based care, spending on secure connectivity, data governance, and analytics soars within the IoT professional services market.

Retail, energy, and logistics also present sizable pipelines, each demanding verticalized blueprints that address regulatory nuance, legacy integration, and outcome measurement. For example, utilities prioritize safety-critical SCADA integration, while retailers focus on frictionless checkout and supply-chain cold-chain monitoring. Service providers that offer modular, compliance-ready accelerators can replicate wins across industries and strengthen wallet share in the broader IoT professional services market.

Geography Analysis

North America retained 36.95% of 2025 revenue, supported by advanced 5G coverage, robust venture funding, and federal initiatives such as NIST’s national IoT strategy. Enterprises in the United States prioritize zero-trust security and AI-enabled analytics, driving complex multi-tower engagements that favor providers with end-to-end portfolios. Canada benefits from near-shoring trends and industrial IoT modernization, while Mexico leverages cross-border manufacturing corridors that rely on real-time supply-chain visibility.

Asia-Pacific is the fastest-growing region at an 7.88% CAGR. China allocates sizable smart-city budgets and promotes Industrial Internet platforms to digitize manufacturing. Japan’s Society 5.0 program and Singapore’s Smart Nation initiatives reinforce regional demand for compliance-ready, scalable solutions. India’s semiconductor and AI policies further expand the addressable base. Providers must balance cost-competitive delivery with deep cultural alignment and local-language support to capitalize on this momentum in the IoT professional services market.

Europe maintains steady growth underpinned by GDPR, the EU Cybersecurity Act, and national Industry 4.0 frameworks that create governance-driven demand for consulting and certification support. Germany, France, and the United Kingdom invest heavily in digital-twin programs, while Eastern European economies leverage EU funds to modernize infrastructure. Middle East and Africa remain nascent but show promise as Gulf states accelerate Vision 2030 smart-city portfolios that require turnkey professional-service engagement.

Regulatory Landscape

Cybersecurity and privacy requirements are increasingly driving compliance work for connected products and the services that design, integrate, and operate them. In the United States, the Federal Communications Commission (FCC) finalized a voluntary cybersecurity labeling framework for wireless consumer IoT, the U.S. Cyber Trust Mark, with an effective date in August 2024. The program reflects security-by-design practices and increases demand for professional services that can translate requirements into device onboarding controls, vulnerability management processes, and audit-ready documentation across multi-vendor deployments.

In Europe, the EU Cyber Resilience Act (CRA) sets horizontal cybersecurity obligations for products with digital elements and introduces earlier-stage duties ahead of full application. Member States have a June 2026 milestone to designate notifying authorities, and manufacturer reporting obligations take effect in September 2026, while full CRA application, including conformity assessment and CE marking requirements, follows in December 2027. Alongside these shifts, NIST published NIST IR 8259 Rev. 1 in April 2026, updating foundational cybersecurity activities for IoT product manufacturers and reinforcing a dual-regime environment where providers must support both incentive-driven labeling and mandatory compliance programs across geographies.

Value Chain Analysis

The IoT professional services value chain begins with strategy and solution definition (use-case selection, ROI modeling, and governance), then shifts into architecture and engineering across devices, connectivity, and platforms. Execution typically covers device and gateway selection, network and private-5G/LTE design, edge-to-cloud integration, data engineering, and application enablement (analytics, AIOps, digital twins), followed by testing, security hardening, deployment, and lifecycle operations such as remote monitoring, patching, and managed services. Ecosystem coordination across hyperscalers, industrial software providers, telecom operators, device and embedded partners, and system integrators remains a key focus because interoperability, OT safety constraints, and regulatory requirements often shape the delivery scope.

Recent vendor alliances show where value is concentrating. Multi-year collaborations such as AVEVA with AWS (CONNECT platform expansion and OT system integrator support programs) indicate cloud and industrial software firms pulling through integration and co-delivery services. Collaborations like Kyndryl with Aptiv on edge AI also highlight how advisory and managed services around edge stacks are becoming more central. Partnerships involving connectivity and sensing suppliers, such as Wiliot with AT&T for Physical AI deployments (including systems integration, installation, and maintenance), point to a more bundled model where field services and scalable rollout capabilities help differentiate. Across the chain, shortages of cross-domain talent (OT networking, embedded security, cloud IAM, and data engineering) and the need for repeatable reference architectures remain bottlenecks, pushing providers to industrialize delivery through accelerators, certified device libraries, and platform-centric managed-service wraps.

Competitive Landscape

The IoT professional services market remains moderately fragmented. Accenture generated USD 64.9 billion in FY 2024 revenue and leverages a global network of innovation hubs to capture large transformation deals. IBM combines consulting, Red Hat OpenShift, and Maximo asset-management suites to deliver end-to-end offerings that resonate in industrial sectors. Cognizant’s 2024 acquisitions of Thirdera and Belcan deepen edge-AI and digital-engineering skills that underpin automotive, aerospace, and healthcare wins.

Specialist firms such as Bosch.IO and Virtusa compete through vertical focus and agile delivery, often partnering with hyperscalers to co-sell solution bundles. Platform owners, including Siemens, accelerate service pull-through via acquisitions like Brightly Software, adding CMMS capabilities that complete digital-twin stacks. Telecommunications operators, led by AT&T and Vodafone, leverage private-5G offerings to secure integration and managed-service fees tied to campus-network rollouts.

Emerging trends include AI-driven automation in service delivery, expansion of outcome-based contracts, and investment in training academies to close critical talent gaps. Providers that embed generative AI for code generation, test-case automation, and anomaly prediction shorten deployment cycles and boost margins. Meanwhile, recurring managed services tied to SLAs on uptime, energy reduction, or production throughput secure multi-year revenue streams, prompting incumbents to pivot from time-and-materials toward value-linked engagement models in the IoT professional services market.

IoT Professional Services Industry Leaders

Accenture PLC

IBM Corporation

Tata Consultancy Services

Cognizant

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is in turning security-by-design and product assurance requirements into repeatable delivery and operational playbooks across heterogeneous device fleets. Programs such as the FCC U.S. Cyber Trust Mark (effective August 2024) and the EU Cyber Resilience Act milestones, including September 2026 manufacturer reporting obligations, increase demand for services that combine technical remediation with compliance evidence, such as SBOM and vulnerability disclosure processes, secure update pipelines, and audit-ready controls across edge and cloud environments. This compliance pull extends beyond device makers to enterprises running mixed-vendor estates that need standardized onboarding, continuous monitoring, and coordinated response workflows.

Another opportunity is scaling brownfield industrial and infrastructure deployments where legacy protocols and mixed asset lifecycles make end-to-end integration difficult. The market is moving from basic connectivity toward edge intelligence and OT-IT data convergence, which raises demand for system design and integration work (protocol translation, local anomaly detection, and deterministic operations) as well as ongoing managed services. Evidence of ecosystem investment supports this direction, including AVEVA and AWS expanding industrial intelligence collaboration around the CONNECT platform and system integrator enablement, and Kyndryl and Aptiv announcing collaboration on edge AI solutions integrating Wind River technologies with advisory and managed services. As private cellular, edge stacks, and industrial software platforms mature, service providers with packaged reference architectures, field deployment capability, and lifecycle operations (including FinOps and cyber operations for OT) have clear room to standardize deployments for both large enterprises and resource-constrained SMEs.

Recent Industry Developments

- June 2026: Accenture announced an agreement to acquire Industries eXcellence Group (IndX), a Siemens Digital Industries partner, to strengthen capabilities for industrial software and automation solutions. The deal expands Accenture’s capacity to deliver factory modernization work that blends engineering, OT-IT integration, and industrial platforms. It also deepens access to Siemens-aligned delivery talent and accelerators used in production deployments.

- April 2026: Accenture and Avanade collaborated with Microsoft to co-develop an agentic factory solution aimed at reducing manufacturing downtime. The collaboration links AI-driven orchestration with operational data to support more autonomous plant operations and faster incident resolution. For IoT professional services, it reinforces demand for integration, data engineering, and managed operations that operationalize AI on top of connected factory systems.

- October 2024: Cognizant signed a strategic collaboration agreement with AWS to deliver smart manufacturing and Industry 4.0 solutions, including digital twins and OT security. The collaboration strengthens packaged modernization offerings that combine cloud services with factory connectivity and cybersecurity capabilities. It also supports co-selling and faster deployment paths for enterprises moving from pilots to scaled IoT programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers paid third party services that help an enterprise plan, design, integrate, secure, test, and support Internet of Things solutions across devices, networks, and applications, including related training and ongoing technical support.

Scope exclusions: We exclude managed connectivity bundles and generic cloud hosting fees that are billed mainly as recurring network or hosting subscriptions.

Segmentation Overview

- By Service Type

- IoT Consulting

- IoT Infrastructure Services

- System Design and Integration

- Others

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Deployment Mode

- Cloud-based

- On-premises

- Hybrid

- By End-user Industry

- Manufacturing

- Retail

- Healthcare

- Energy and Utilities

- Transportation and Logistics

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- GCC

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the service scope and demand signals that can be checked publicly. We use sources such as the ITU and OECD for digital connectivity indicators, NIST publications for security and systems guidance signals, the U.S. Census Bureau and Eurostat for enterprise spending and industry output context, and World Bank macro series to normalize comparisons across regions.

On top of that, we review company filings and earnings decks, contract announcements, and association and standards body websites to understand how services are packaged and priced (consulting, system integration, security, support, and training). Where needed, paid database subscriptions are used for company financials and intelligence, news and financials tracking, patent databases, and global contracts and tenders to cross-check supplier activity and demand timing. These desk research inputs are not exhaustive, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focuses on validating what portion of IoT spending turns into professional services revenue, and how it splits between project work and recurring support. We speak with service providers, channel partners, and enterprise buyers across APAC, EMEA, and the Americas, so assumptions on typical engagement size, duration, and security and integration intensity can be checked and then adjusted.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 49% |

| Mid tier: 46% | Functional/Unit leaders: 34% | EMEA: 30% |

| Smaller Players: 15% | Managers: 52% | Americas: 21% |

Market-Sizing & Forecasting

The core model is built using a top-down approach where enterprise IoT adoption indicators and connected-device rollout activity are translated into a services demand pool, followed by service-intensity ratios that vary by industry and region. We then corroborate totals using selective bottom-up approximations, such as sampled project values from public contracts, a limited roll-up of service revenue disclosures where available, and channel checks on typical price ranges, which are then used to tune the final total.

Key inputs include enterprise IoT deployment momentum, the mix of greenfield builds versus upgrades, system integration effort driven by device count and data pipeline complexity, security and compliance workload, and the share of engagements that move into recurring support and maintenance. Because pricing changes over time, average service rates are allowed to move with wage inflation and delivery mix shifts (onsite versus remote, and consulting versus integration heavy work). For forecasting, we use scenario analysis supported by a light multivariate regression, so growth is linked to drivers such as connectivity expansion, cloud and edge adoption, and enterprise capex and opex direction, which were validated in calls.

When bottom-up signals are missing for smaller regions or niche verticals, gaps are handled through proxying based on comparable industry adoption levels, and then rechecked with primary feedback before numbers are finalized.

Data Validation & Update Cycle

Validation is done through a set of cross-checks that compare modeled revenue against independent signals like enterprise digital spending direction, IoT deployment announcements, and the pace of large transformation programs. Outliers are flagged, assumptions are revisited, and follow-up outreach is triggered when a region or vertical moves outside expected bands.

A multi-step analyst review is completed before sign-off so calculation logic, currency handling, and year alignment are consistent throughout. The report is refreshed annually, and interim updates are made when a material event changes service demand or pricing behavior. Before delivery, a final pass is performed so clients receive the most current view available at that time.

Mordor Intelligence's IOT Professional Services Market Size Versus Other Published Estimates

Published values for IoT professional services can look far apart even when they describe similar service activities, because inputs and scope choices are not always aligned. The biggest differences usually come from what is counted as professional services versus adjacent recurring fees, the base year selected, and how service pricing is moved forward year to year.

The main gap comes from including connectivity or hosting-led recurring revenue inside the services pool, where Mordor Intelligence excludes managed connectivity bundles and generic cloud hosting fees, and keeps the estimate tied to consulting, integration, security, support, and training revenue. Differences also show up when one study anchors on an earlier base year, or when aggressive device adoption and faster rate increases are assumed without being checked against contract activity and buyer validation.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 154.58 B (2026) | |

| Industry Publisher A | USD 132.50 B (2024) | Uses an earlier base year, and scope language is broader around deployment enablement, which can shift what gets counted as professional services versus adjacent IoT spend categories. |

| Global Publisher B | USD 102.70 B (2025) | Reports the market in US$ with a different year anchor and a narrower stated segmentation lens, which can undercount broader enterprise integration and support work if it is allocated into other IoT spend buckets. |

Taken together, the spread is mainly explained by year anchoring and what each publisher includes alongside consulting and integration work. Our approach stays traceable to clear service activities and practical demand indicators, which makes the total easier to reproduce and monitor as assumptions change.

Key Questions Answered in the Report

What is the current IoT professional services market size?

The market generated USD 154.58 billion in 2026 and is projected to reach USD 214.08 billion by 2031.

Which service type leads the IoT professional services market?

IoT consulting holds the top position with 32.10% share, though system design & integration is growing fastest at a 7.05% CAGR.

How fast is cloud deployment growing within the IoT professional services market?

Cloud-based delivery is advancing at an 8.08% CAGR, the quickest among deployment modes.

Which region offers the highest growth opportunity?

Asia Pacific shows the strongest upside with an 7.88% CAGR driven by manufacturing modernization and government digital programs.

What is the main restraint facing IoT professional services adoption?

Cyber-security and data-privacy concerns remain the leading barrier, lowering the overall growth trajectory by an estimated 1.4 percentage points.

Page last updated on: