South Africa IoT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

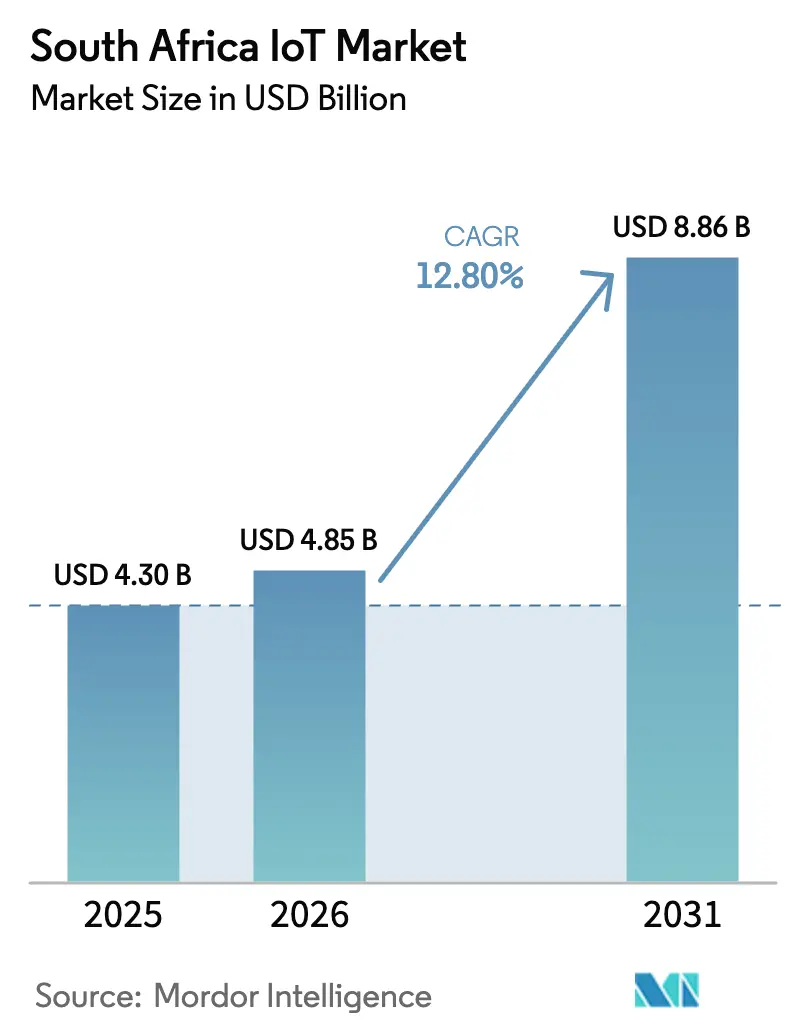

| Base Year Market Size (2025) | USD 4.3 Billion |

| Market Size (2026) | USD 4.85 Billion |

| Market Size (2031) | USD 8.86 Billion |

| Growth Rate (2026 - 2031) | 12.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa IoT Market Analysis by Mordor Intelligence

The South Africa IoT market size is expected to grow from USD 4.3 billion in 2025 to USD 4.85 billion in 2026 and is forecast to reach USD 8.86 billion by 2031 at 12.8% CAGR over 2026-2031. Intensifying cloud adoption, improving spectrum availability, and the commercial launch of nationwide 5G services give enterprises the bandwidth headroom and low-latency environment required for high-value industrial analytics and automation. Hardware demand remains solid; yet rising adoption of managed services shows that local companies now prize real-time insight over device ownership. Satellite–terrestrial hybrids, introduced to mitigate load-shedding outages and rural coverage gaps, expand the addressable base of applications across mining, agriculture, and logistics. Government smart-city financing, paired with falling sensor prices, signals that the South Africa IoT market will keep advancing even as macroeconomic volatility tests private spending.

Key Report Takeaways

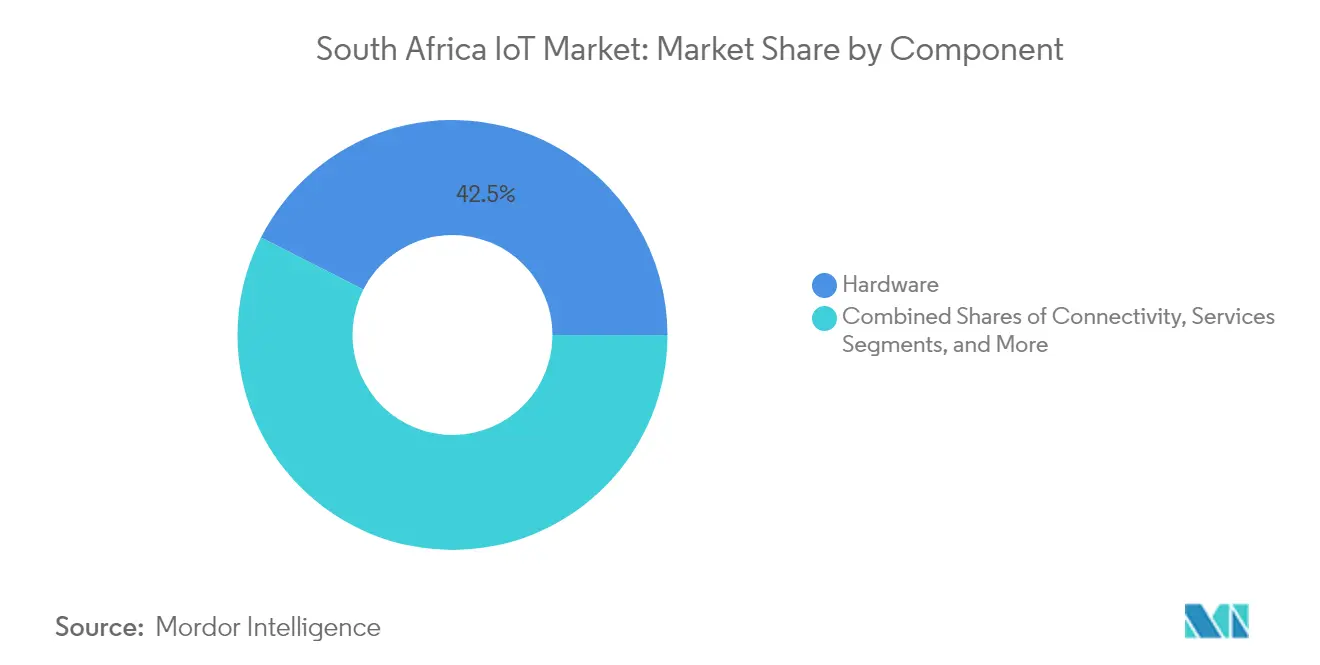

- By component, hardware captured 42.50% revenue share in 2025 in the South Africa IoT market, while services are projected to grow at a 16.78% CAGR through 2031.

- By connectivity technology, 4G/5G cellular IoT led with 45.40% of the South Africa IoT market share in 2025; satellite and hybrid options are forecast to expand at a 20.74% CAGR to 2031.

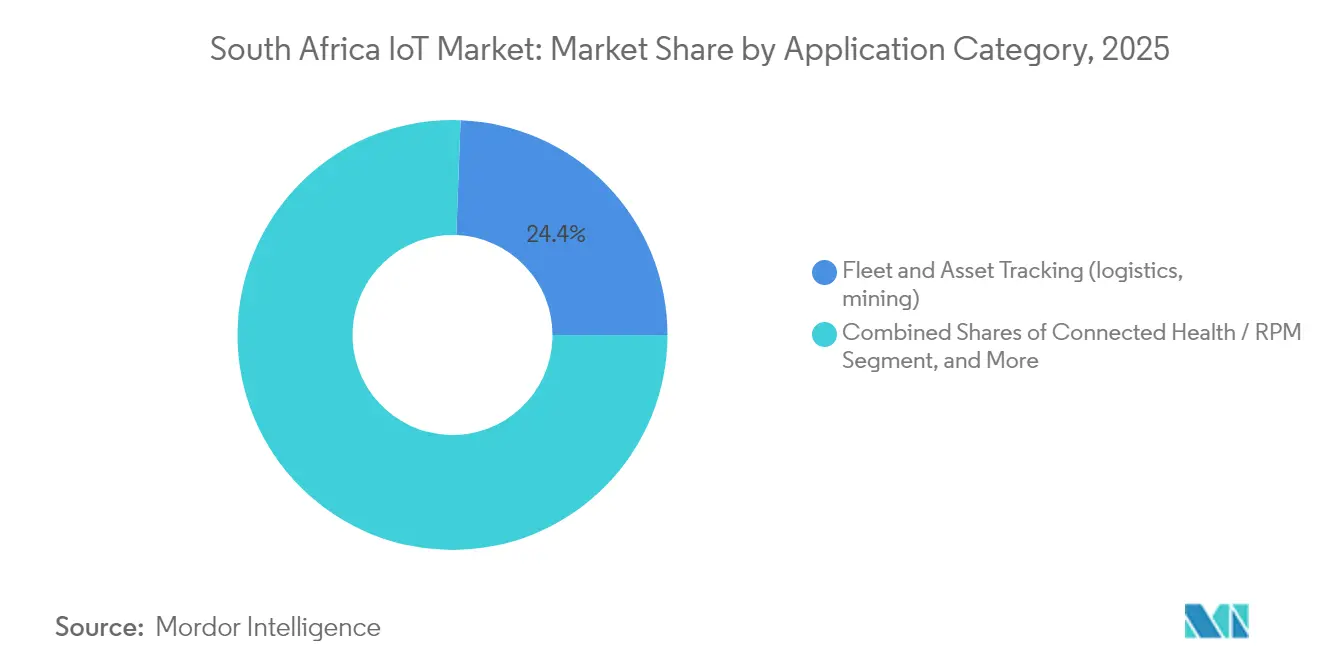

- By application, fleet and asset tracking accounted for 24.40% share of the South Africa IoT market size in 2025; smart agriculture and climate monitoring are on track for a 21.58% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa IoT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile broadband expansion and 5G rollouts | +2.8% | National; early gains in Gauteng, Western Cape, KwaZulu-Natal | Medium term (2–4 years) |

| Government smart-city spending commitments | +2.1% | Cape Town, Johannesburg, eThekwini, Tshwane | Long term (≥ 4 years) |

| Falling module and sensor ASPs | +1.9% | National; local assembly opportunities | Short term (≤ 2 years) |

| Enterprise cloud migration momentum | +1.7% | National; financial and mining sectors | Medium term (2–4 years) |

| NB-IoT / LTE-M spectrum allocation (2024) | +1.4% | National; rural connectivity focus | Medium term (2–4 years) |

| Rapid insurance telematics uptake | +1.2% | Urban centers nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mobile broadband expansion and 5G rollouts

More than half of the population enjoyed 5G coverage by December 2024 as MTN and Vodacom switched on a combined 829 new sites, adding USD 1.5 billion in wireless revenue.[1]Connecting Africa, “South Africa 5G Subscribers Top 10.8 Million,” connectingafrica.comThe throughput uplift lets device makers embed high-definition video and low-latency control loops into surveillance, mining automation, and remote healthcare. New fixed-wireless packages extend enterprise IoT connectivity to SMEs that lack affordable fiber. Ongoing 5.5G and direct-to-device satellite trials point to blended architectures that keep critical sensors online during grid disruptions, removing a long-standing infrastructure bottleneck. With bandwidth constraints easing, device counts climb and average data per node rises, magnifying the addressable analytics opportunity for service providers.

Government smart-city spending commitments

The R940 billion national infrastructure plan earmarks R375 billion for state-owned utilities, many of which tie funding tranches to measurable digital efficiency targets.[2]IOL Business Report, “Infrastructure Drive Earmarks R375 Billion for State-Owned Digital Upgrades,” iol.co.za Municipalities already deploy Sigfox-enabled smart water meters, camera networks, and environmental probes that feed unified control rooms in Cape Town and Johannesburg. Procurement frameworks now bake in interoperability clauses, accelerating vendor accreditation and shrinking sales cycles. Public contracts often include multi-year maintenance clauses, creating predictable demand for managed services. By mandating open standards, local authorities indirectly lower integration hurdles for private-sector adopters, broadening the South Africa IoT market’s appeal to global platform vendors.

Falling module and sensor ASPs

Global chip fab expansion cut cellular module prices 15–20% during 2024, bringing sub-USD 4 LTE Cat-M1 units within reach of mid-tier integrators.[3]African Business, “Africa’s Emerging Semiconductor Chain,” african.business South African firms can now build break-even cases for smart metering or cold-chain tags at scale instead of limiting pilots to high-value assets. Local assembly programs at the Microelectronics and Nanotechnology Centre shorten import lead times and foster specialized designs for harsh mining environments. Because hardware cost is no longer the prime barrier, buyer scrutiny shifts to analytics quality and service uptime, pushing the value pool toward software.

Enterprise cloud migration momentum

Microsoft and AWS launched in-country zones that let regulated industries move petabyte-level telemetry into local data lakes without breaching sovereignty rules. MTN’s USD 690 million first-half 2024 capex strengthened edge nodes that couple private 5G with Azure Stack, giving mines and factories sub-30 millisecond round-trip latency for predictive-maintenance algorithms.[4]MTN Group, “Interim Results 2024,” mtn.com Discovery Health’s new Personal Health Pathways crunches 33 terabytes of patient data daily, proving the economics of cloud-native IoT workflows at national scale. As analytics adoption widens, demand grows for skills in data engineering and ML ops, further propelling the service segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Load-shedding-induced network downtime | -3.2% | National, with severe impact in industrial areas | Short term (≤ 2 years) |

| 2G/3G sunset retrofit costs (SME pain-point) | -2.1% | National, concentrated in rural and township areas | Medium term (2-4 years) |

| Cyber-skills shortage | -1.8% | National, concentrated in urban technology centers | Long term (≥ 4 years) |

| Slow public-sector procurement cycles | -1.4% | National, affecting municipal and government IoT projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Load-shedding-induced network downtime

Eskom generated 25,000 MW against the demand of 31,000 MW in early 2024, forcing rotational cuts that eroded telecom uptime and diverted billions into diesel and lithium battery backups. Even after a temporary reprieve in April 2024, operators kept installing solar plus battery micro-sites to shield IoT gateways. Retailer Shoprite deployed SmartSense to shut down non-critical refrigeration during blackouts, proving that resilient edge architectures can lower energy drag while preserving data. Yet the cost of redundancy still inflates the total cost of ownership and delays ROI for first-time adopters, especially SMEs with thin margins.

Cyber-skills shortage

South Africa ranked third for cybercrime victims in 2024, losing R2.2 billion to attacks that exploited poorly secured endpoints. Only a fraction of network engineers hold modern IoT security credentials, leaving gaps in threat modeling and zero-trust design. Check Point’s July 2024 index pegged national risk at 42%, well above global median levels. Because mining and utilities operate life-critical systems, boards demand proven expertise before green-lighting large telemetry projects. In response, Cisco funded regional academies and vendor-neutral boot camps, yet talent pipelines take years to mature, limiting near-term deployment velocity outside tier-one integrators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Platform Integration

Hardware commanded 42.50% of 2025 revenue, confirming that sensors and gateways remain core to every installation. The South Africa IoT market continues to buy ruggedized units for underground mining and remote agriculture, but growth is tapering as inventories last longer and multi-protocol chips ship ready-certified. Services, by contrast, post a 16.78% CAGR to 2031 because enterprises seek end-to-end governance, root-cause analytics, and lifecycle security patches that in-house teams cannot scale. Multi-tenant device orchestration lowers per-node management cost, while outcome-based contracts shift risk to providers.

Enterprises increasingly bundle software, cloud storage, and 24×7 support into predictable monthly fees, reshaping capital outlays into operating budgets. Trinity’s dual-SIM device-management suite illustrates the pivot: customers pay for guaranteed uptime rather than modems. As vertical templates multiply across healthcare, insurance, and retail, competitive edge moves up the stack toward domain-specific dashboards. This service-centric motion unlocks consistent recurring revenue that smooths the earnings profile of vendors operating in the volatile macro backdrop of the South Africa IoT market.

By Connectivity Technology: Satellite Solutions Address Infrastructure Gaps

4G/5G networks supplied 45.40% of connected nodes in 2025, lifting the South Africa IoT market size for cellular links to roughly USD 1.95 billion. Dense urban grids and mid-band spectrum auctions make mobile broadband the de facto baseline for video, industrial automation, and POS terminals. Nonetheless, satellite-enabled and hybrid links are accelerating at 20.74% CAGR through 2031. This surge follows MTN’s direct-to-device tests with Lynk and the planned launch of Iridium’s 5G-compatible Project Stardust in 2026, projects that promise seamless handover when terrestrial towers go dark.

The reliability of space-based coverage resonates with logistics fleets crossing sparsely populated Karoo or Kalahari routes where cellular fades. Regulatory clearance for non-geostationary constellations pushes device makers to design multi-bearer chipsets, boosting unit volumes. For low-power sensor clusters, LoRa and Sigfox remain viable thanks to 10-year battery life; yet integrators increasingly combine them with satellite backhaul for redundancy. In effect, the connectivity stack is coalescing into a layered model that chooses the lowest-cost bearer per packet while guaranteeing five-nines availability demanded by heavy industry.

By Application Category: Agriculture Innovation Accelerates

Fleet and asset tracking delivered 24.40% of total 2025 sales as mining trucks, port cranes, and cold-chain trailers streamed telematics for compliance and insurance rebates. Voyage visibility platforms track ore from pit to port, while Kumba Iron Ore’s USD 600 million UHDMS plant relies on real-time vibration sensors for predictive shutdowns. The South Africa IoT market size for tracking applications is projected to grow steadily, though its share will dilute as farming and climate systems scale.

Smart agriculture and climate monitoring outpace all other uses at a 21.58% CAGR between 2026-2031. Western Cape vineyards deploy soil probes and aerial drones feeding Vodacom’s MyFarmWeb for moisture-stress alerts, cutting irrigation costs by 20% in pilot fields. Citrus exporters add ethylene-gas meters in reefer containers to protect shelf life on long voyages. Subsidized weather stations in Limpopo supply early-warning indices for insurance parametric payouts that lower smallholder risk. Because agritech touches food security, lenders and development agencies co-finance deployments, accelerating rural sensor density and diversifying revenue streams within the South Africa IoT market.

Geography Analysis

Gauteng anchors enterprise demand with 69% 5G coverage, deep financial services, and head offices for mining majors, making it a natural launchpad for industrial analytics platforms. Western Cape blends a thriving start-up scene with export-oriented horticulture, turning Stellenbosch test beds into commercial smart-farming contracts. KwaZulu-Natal’s port corridors and automotive clusters use IoT to de-risk supply chain bottlenecks; telematics-rich truck fleets now share congestion data with customs brokers to optimize berth allocation.

Rural provinces adopt satellite links and LPWAN to leapfrog tower build-outs, linking weather stations, pump controls, and anti-poaching collars. National Treasury’s funding of 15 million Sigfox water meters pushes device densities beyond urban confines, increasing total addressable nodes even where per-capita income is lower. Municipalities weave connected lighting, CCTV, and parking into integrated command centers, nudging citizens toward app-based service requests that create fresh data pools for predictive planning.

Cross-border trade with Namibia and Botswana prompts logistics players to fit multi-IMSI SIMs, ensuring continuous tracking well into the Trans-Kalahari corridor. Because ICASA enforces technology-neutral spectrum licensing, satellite operators face minimal red tape when onboarding new ground stations, a stance that bolsters regional interoperability. Overall, the South Africa IoT market extends its influence as a continental hub, exporting expertise to neighboring states while attracting multinational platform vendors to set up African headquarters in Johannesburg or Cape Town.

Competitive Landscape

Vodacom, MTN, and Telkom anchor connectivity through nationwide cellular and LPWAN footprints, allowing them to bundle data plans with cloud gateways and managed dashboards. Their combined infrastructure depth yields economies of scale, yet strategic differentiation now resides higher in the stack. MTN channels USD 690 million per year into edge-cloud and AI accelerators, while Vodacom’s alignment with Microsoft and Google enhances its application-layer stickiness. Telkom leverages state-owned backbone routes to underprice backhaul for municipal projects, securing long-term public contracts.

At the application layer, Tracker SA and Cartrack compete for fleet telematics subscriptions, tapping insurance incentives to lift attach rates. Red Ant Agri tailors smart seeding implements and in-field telemetry, reflecting a vertical-focus trend among emergent players. Plentify pursues residential energy management, integrating geyser controls that shave peak demand during power cuts. Global tech giants IBM, Cisco, and Huawei embed middleware and security modules into these local offerings, sharing revenue via joint go-to-market agreements.

Demand for secure, power-resilient solutions sparks opportunities for specialists in battery augmentation, edge compute, and zero-trust orchestration. System integrators that master operational technology protocols alongside IT governance gain an edge in brownfield mines and factories. Because buyers want turnkey outcomes, partnerships that fuse network reach with domain expertise will likely shape future market share gains within the South Africa IoT market.

South Africa IoT Industry Leaders

MTN Group

Microsoft Corporation

IBM Corporation

Huawei Technologies

Vodacom Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: MTN SA and Lynk Global completed Africa’s first satellite-to-smartphone call, enabling direct-to-device IoT connectivity.

- March 2025: Discovery Health rolled out Personal Health Pathways, an AI-powered platform serving 2.1 million members and processing 33 terabytes of data daily.

- March 2025: Gauteng added 193 CCTV cameras in townships and hostel districts to strengthen integrated municipal surveillance.

- February 2025: President Ramaphosa confirmed R940 billion in infrastructure spending over three years, with R375 billion targeted at digitally enabled utilities.

South Africa IoT Market Report Scope

The "Internet of Things" refers to devices connected over the internet using sensors, software, and other technologies incorporated with minimal human intervention. Wearable fitness trackers and autonomous vehicles all function by employing IoT. IoT technology is becoming more accessible to more firms because of inexpensive and trustworthy sensors.

South Africa's IoT market is segmented by component (hardware, software, connectivity, and services) and by end-user industry (manufacturing, transportation, healthcare, retail, energy and utilities, other end-user industries [residential, BFSI, agriculture]). The report offers market forecasts and size in value (USD) for all the above segments.

| Hardware |

| Software and Platforms |

| Connectivity |

| Services |

| 4G / 5G Cellular IoT (incl. NB-IoT, LTE-M) |

| 2G / 3G Legacy Cellular IoT |

| Non-cellular LPWAN (LoRa, Sigfox) |

| Short-Range (Wi-Fi, BLE, Zigbee, RFID) |

| Satellite and Hybrid IoT |

| Fleet and Asset Tracking (logistics, mining) |

| Smart Metering (water, electricity, gas) |

| Industrial Automation / Predictive Maintenance |

| Smart Agriculture and Climate Monitoring |

| Connected Health / RPM |

| Smart Retail and POS |

| Consumer Smart-Home |

| Safety and Security (surveillance, alarms) |

| Micro / Prosumer |

| By Component | Hardware |

| Software and Platforms | |

| Connectivity | |

| Services | |

| By Connectivity Technology | 4G / 5G Cellular IoT (incl. NB-IoT, LTE-M) |

| 2G / 3G Legacy Cellular IoT | |

| Non-cellular LPWAN (LoRa, Sigfox) | |

| Short-Range (Wi-Fi, BLE, Zigbee, RFID) | |

| Satellite and Hybrid IoT | |

| By Application Category | Fleet and Asset Tracking (logistics, mining) |

| Smart Metering (water, electricity, gas) | |

| Industrial Automation / Predictive Maintenance | |

| Smart Agriculture and Climate Monitoring | |

| Connected Health / RPM | |

| Smart Retail and POS | |

| Consumer Smart-Home | |

| Safety and Security (surveillance, alarms) | |

| Micro / Prosumer |

Key Questions Answered in the Report

What is the current size of the South Africa IoT market?

The market is valued at USD 4.85 billion in 2026 and is projected to reach USD 8.86 billion by 2031.

Which component segment is growing fastest?

Services are expanding at a 16.78% CAGR through 2031 as companies seek managed analytics and integration support.

Why are satellite connections gaining traction in South Africa?

Satellite and hybrid links grow at 20.74% CAGR because they bypass load-shedding outages and cover rural areas where cellular coverage is weak.

How large is the fleet and asset tracking opportunity?

Fleet and asset tracking accounts for 24.40% of the South Africa IoT market share in 2025, underscoring steady demand across mining and logistics.

What is the biggest restraint on market growth?

Load-shedding-induced network downtime subtracts 3.2 percentage points from forecast CAGR, making power resilience a prerequisite for new deployments.

Which province leads IoT adoption?

Gauteng holds leadership with 69% 5G coverage and a dense concentration of enterprise headquarters, driving early-stage demand for industrial analytics.

Page last updated on: